IF YOU'RE NOT AT - YOU'VE GOT SOME WORK TO DO! YOUR NUMBER'S UP!

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UK

DIGITAL RE VENUE AS A PERCENTAGE OF TOTAL RE VENUE

IF YOU’RE NOT AT

28

YOUR %

NUMBER’S

UP!

YOU’VE GOT SOME

WORK TO DO!

THE RISE OF DIGITAL OVER THE LAST 18 MONTHS HAS BEEN UNDENIABLE.

WE HAVE SEEN THE IMPACT OF DIGITAL ON THOSE BRANDS WHO WERE

READY AND THOSE WHO WERE NOT.

We wanted to understand the state of the nation in the USA and UK and see if digital

consumer behaviour would return to the levels seen prior to the impact of COVID-19.

We have looked at brands who have embraced digital and some of those who have

INTRODUCTION

fallen, and what their share of Digital revenue on total revenue was.

We used a mixture of data from the Office of National Statistics (ONS),

Benedict Evans (the great unbundling), United States Census

Bureau and our own primary research.

YOUR BER’S

We had 124 respondents from our own survey from

Europe and North America. They were primarily in digital or

ecommerce roles or ran agencies who worked in digital. NUM

UP!

nt

reme

d Measu s

n le

ata a merce sa

on D

g a grip our Ecom

in

Gett elerate y Kaushik

c

to ac d by Avinash

wor

Fore

W

SHA

TIM

M AND

BR AHA

ER A

PE T S

L M ON , OPKIN

SA AH

BEN JESSIC

H

WIT

THE FOLLOWING 4 AREAS ARE COVERED IN THIS DOCUMENT TO HELP PROVIDE GUIDANCE

ON WHAT GOOD LOOKS LIKE, WHO IS DOING WELL TODAY AND HOW TO IMPROVE YOUR

DIGITAL MEASUREMENT.

4 1 2 3 4

FOCUS

AREAS

Adoption of Digital How Brands Perform Our Research Measuring Success

How brands are adopting A review of some brands A review of our A guide to the

digital to generate and how they are own research and 4 different levels of

revenue. The impact performing. identification of measurement maturity,

COVID-19 has had on A review of their digital what makes a digitally types of metrics

digital sales in the UK revenue and how they focused vs more and how you can

and USA. compare. traditional business. improve.

1 Adoption of Digital

2 How Brands Perform

We want to see digital revenue as a share of total There have been winners and losers, but most

revenue on every annual report. would agree those who have succeeded were

The share of revenue from digital has grown prepared and embraced digital prior to the last 18

massively in the last 18 months both in the USA and months (outbreak of COVID-19).

UK. The winners have had a larger share of revenue

Understanding your digital revenue contribution coming from digital and in a like for like period have

is critical and it needs to be above the national seen a larger increase in revenue.

average if digital is your brand’s route to growth. The winners are not just purely digital businesses.

The UK average is higher with 2020 averaging 28% There are those who have focused on and

of sales from digital and 32% of from the first half of transitioned to digital, where this source of revenue

EXECUTIVE

2021. now represents the greatest share of sales.

The USA is 14% in 2020 and the first half of 2021.

SUMMARY 3 4

Our Research Measuring Success

The businesses with most of their revenue coming Look at the 4 different levels and see which ones

from digital (more than 75%) were the most best connect with you.

prepared and had least amount of concern about Once you have identified your level of maturity map

staffing and technology. out how you can improve across the different areas

Those organisations with less than 25% of revenue of customer, brand, business and evaluation.

coming from digital, had unrealistic expectations Ensure you have your metrics clearly defined and

coming from digital (as they were the only group start with outcome metrics, not volume based

hoping for more revenue). They additionally were metrics.

most risk adverse of all groups. Want more help and guidance read our book Your

Dashboards and reports were not the centre of Number’s Up! or download one of our micro guides

attention across all businesses with those who are to help you solve you measurement problem.

most digitally focused using data to inform all of wearecrank.com/resources

their decisions.

ADOPTION OF DIGITAL

TO SEE DIGITAL REVENUE

OUR AS A PERCENTAGE OF

AMBITION TOTAL REVENUE ON EVERY

ANNUAL REPORT

SLOW

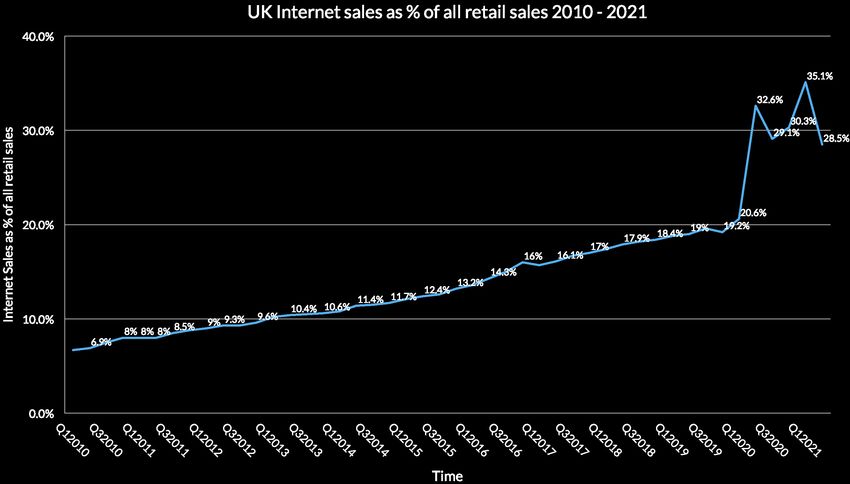

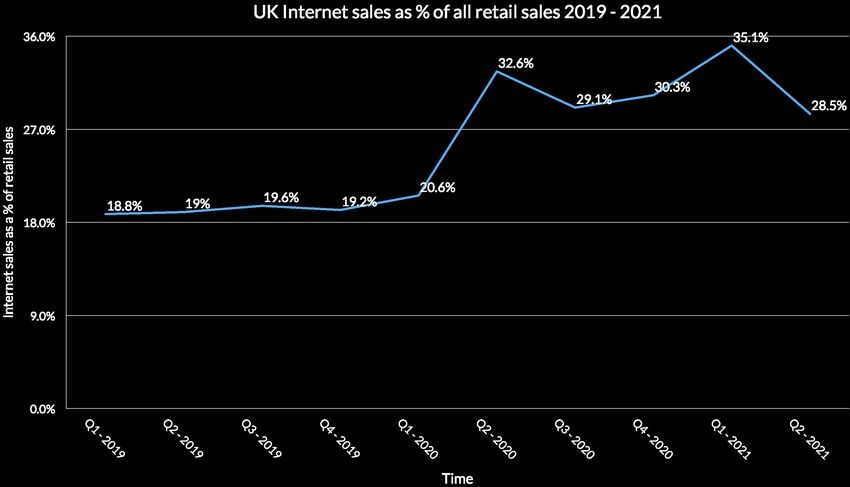

UK DIGITAL REVENUE AS A PERCENTAGE OF TOTAL REVENUE

AND STEADY

GROWTH

From 2010 to to 2019 there was a steady

increase of digital sales.

Digital revenue share only grew from 16% to

19% from 2017 to 2019.

It wasn’t until Quarter 2 2020 that the

adoption of digital really spiked due to the

lockdown in the UK and closure of stores.

SOURCE: ONS https://www.ons.gov.uk/businessindustryandtrade/retailindustry/datasets/retailsalesindexinternetsales

Quarter 1 (Jan - Mar) 2010 until Quarter 2 (Apr - Jun) 2021 - Seasonally adjusted internet sales as a percentage of total retail sales.

NO

UK DIGITAL REVENUE AS A PERCENTAGE OF TOTAL REVENUE - PRE AND POST COVID 19

RETURN

TO

NORMAL

There was a 72% year on year increase Q2 2019 to

Q2 2020.

As lockdowns have been eased in the UK there has

been a slight decline in online sales as expected with

stores opening back up.

However this hasn’t been a big a drop as expected

with digital sales contribution dropping to 28.5% in

Q2 2021 far from the previous 19% from Q2 2019.

Digital is here to stay and the focus on digital is

more important than ever.

SOURCE: ONS https://www.ons.gov.uk/businessindustryandtrade/retailindustry/datasets/retailsalesindexinternetsales

Quarter 1 (Jan - Mar) 2019 until Quarter 2 (Apr - Jun) 2021 - Seasonally adjusted internet sales as a percentage of total retail sales.

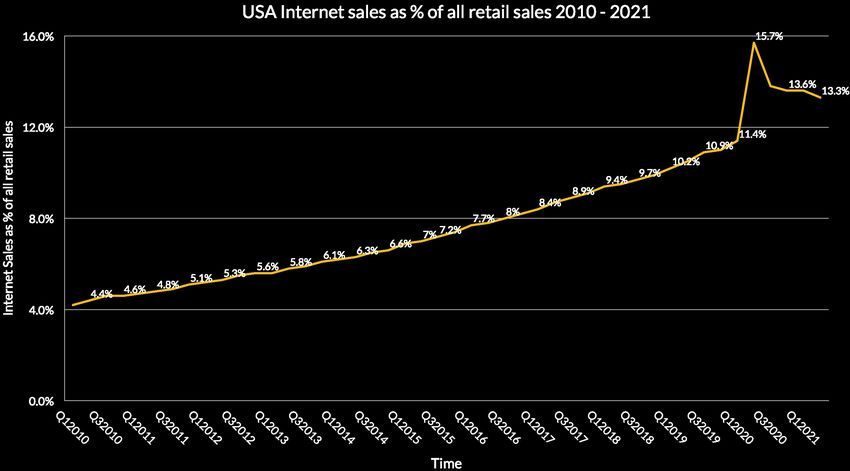

A LOWER

USA DIGITAL REVENUE AS A PERCENTAGE OF TOTAL REVENUE

STARTING

POINT

From 2010 to to 2019 digital sales share grew but at

a slower rate in the USA compared to the UK. Digital

revenue share only grew from 8% to 10% from 2017

to 2019. It wasn’t until Quarter 1 2020 that there

was a big increase in sales from digital with the

outbreak of COVID-19.

The adoption of digital is lower in the USA but this is

not a surprise given the size of the country and the

historically slower delivery times 2-3 days compared

to the UK average of 1.7 days down from 2.1 days.

The rise of services like Instacart, Deliveroo and

Uber Eats, will make a difference but same/next day

delivery for niche brands might take longer.

SOURCE: United States Census Bureau https://www.census.gov/retail/mrts/www/data/excel/tsadjustedsales.xls

Quarter 1 (Jan - Mar) 2010 until Quarter 2 (Apr - Jun) 2021 - Seasonally adjusted internet sales as a percentage of total retail sales.USA DIGITAL REVENUE AS A PERCENTAGE OF TOTAL REVENUE - PRE AND POST COVID 19

BIG GAINS

BUT

NOT HUGE

There was a 50% year on year increase Q2 2019 to

Q2 2020. One reason for the smaller increase might

be due to the limited number of lockdowns in the

USA forcing consumers to purchase online.

There has been a drop in digital revenue share,

however this has not returned to the levels prior

to the COVID-19 outbreak. At 13% it is still above

the 10%-11% average from 2019. Digital is still an

important channel in the USA but less of a critical

factor compared to the UK.

SOURCE: United States Census Bureau https://www.census.gov/retail/mrts/www/data/excel/tsadjustedsales.xls

Quarter 1 (Jan - Mar) 2019 until Quarter 2 (Apr - Jun) 2021 - Seasonally adjusted internet sales as a percentage of total retail sales.WHAT DOES A BUSINESS THAT FOCUSES ON DIGITAL LOOK LIKE?

WHAT DOES Internet sales as % of all retail sales 2020 - and H1 2021 for USA and UK

GOOD

LOOK LIKE?

Internet Sales as % of all retail salesUK

For those organisations who are focused on growing

their digital offering, the baseline in the USA is 14%

and the UK is 32%.

This means if your share of digital revenue is less

than either of these numbers, you must focus on

growing your digital revenue. Increase the role of

digital, budget and digital savvy team members onto

your board of directors.

SOURCE: Based on data from United States Census Bureau https://www.census.gov/retail/mrts/www/data/excel/tsadjustedsales.xls and

ONS (UK) https://www.ons.gov.uk/businessindustryandtrade/retailindustry/datasets/retailsalesindexinternetsales Seasonally adjusted internet sales as a percentage of total retail sales.GLOBAL AVERAGES HIDE THE TRUTH

WHAT WORKS

FOR YOU

AND YOUR

MARKET?

Do not set a target globally for digital revenue share,

as you’ll need a different approach in each market.

Each country has its own level of maturity and

therefore the required investment digital represents.

For example the approach you take in South Korea vs

Spain, where more investment is required in digital in

South Korea given the higher rate of digital adoption

in that market.

SOURCE: eMarketer 2020 - https://www.emarketer.com/chart/244425/top-10-countries-ranked-by-retail-ecommerce- sales-share-2021-2022-of-total-retail-sales

Note: Estimates are based on the analysis of data from other research firms and government agencies, historical trends, reported and estimated revenues from major online retailers,

consumer online buying trends, and macro-level economic conditions.HOW BRANDS PERFORM

DIRECT TO CONSUMER IS GROWING

OBSERVATIONS

Not all brands can become digital first brands. Price

point and margin are critical factors for making that

decision.

It is easier for L’Oreal to become a digitally focused

business when their average order value is likely to

be £50 ($68). Versus Hershey who might struggle

to sell chocolate if the cost of delivery is similar to

the cost of the products.

Creating a sense of urgency for Dettol (Reckitt) and

Dove (Unilever) might be harder. However changing

the offering to your cleaning subscription of body

care subscription across a variety of brands might

work.

Offering products direct to consumer has to be

more than putting products on a website if the

price point or sense of urgency is not there. Maybe

Hershey could create a subscription service offering

customised confectionary for their customers, or to

send as gifts throughout the year.

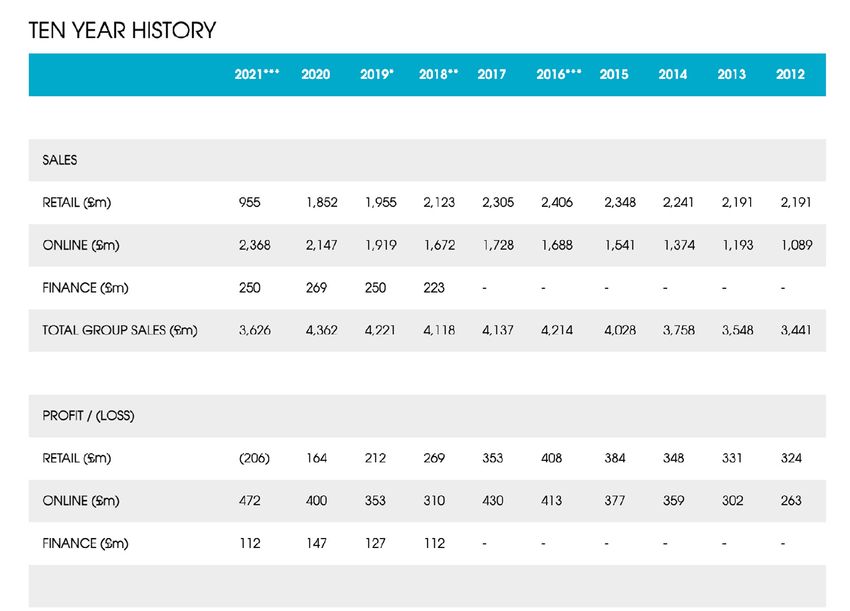

SOURCE: Benedict Evans (the great unbundling January 2020 - https://www.ben-evans.com/presentations)LAURA ASHLEY VS NEXT PLC

COMPARING

TRADITIONAL

Digital revenue Digital revenue

as a share of as a share of

total revenue total revenue

Revenue in millions

was 25% was 23%

RETAILERS Laura Ashley annual sales

Laura Ashley had seen a decline in sales overall and

a decline in digital sales. Their digital revenue share

also decreased. When COVID-19 hit it forced their

Digital revenue Digital revenue

closure as a share of as a share of

total revenue total revenue

Revenue in millions

was 41% was 45%

Next plc had grown their digital offering and were

ready for COVID-19. They still turned a profit even

with a £206m loss from retail stores in 2021.

Next annual sales

SOURCE: Companies house Laura Ashley Annual report 2019 and https://www.nextplc.co.uk/investors/ten-year-historyASSOCIATED BRITISH FOODS VS ASOS

COMPARING

OFFLINE AND

£ in millions

ONLINE Associated British Foods (Primark) annual sales and net income

Associated British Foods (ABF) net income

declined 48%. Currently it does not offer any online

purchasing options for Primark. This might be due

to low margins on product, but click and collect isn’t

even offered.

£ in millions

ASOS net income grew 361% year on year with.

Currently ASOS operates direct to consumer and

generates 3rd party income from its websites.

ASOS annual sales and net income

SOURCE: ABF (Primark) 2020 annual report and ASOS 2020 annual reportSTRUGGLING GET IN TOUCH OR LEARN

WITH HOW TO IMPROVE YOUR

YOUR

MEASUREMENT? DIGITAL MEASURMENT

IN OUR BOOK

O UR

Y BER’S

10% off NUM

UP!

nt

reme

d Measu s

n le

ata a merce sa

use Research UK as coupon code ing a

on D

grip our Ecom

y

Gett elerate Kaushik

c

to ac y Avin

b

ash

word

Fore

W

SHA

TIM

AND

AM

R AH

R AB

E TE

N , P PKINS

A L MO H O

S A

BEN JESSIC

H

WITOUR RESEARCH

WHAT DOES WHAT THE

GOOD LEADERS IN DIGITAL

LOOK LIKE?

DOTHE

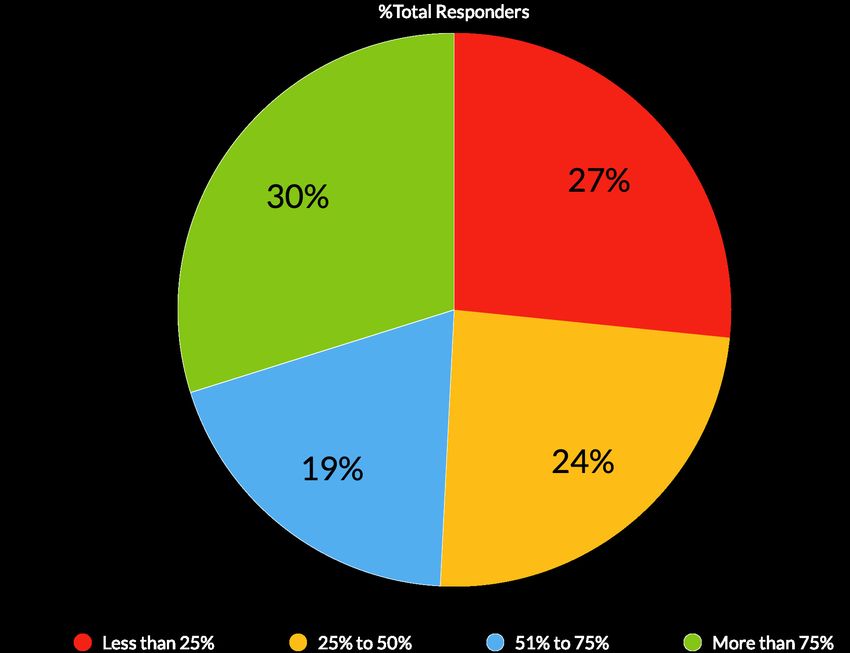

Overall 41% of

QUESTION: HAS DIGITAL GENERATED THE REVENUE RETURNS YOU EXPECT respondents

found they had

GIVEN THE MARKET CHANGES WE’VE SEEN RECENTLY? more revenue

than they

EXPECTATIONS

expected.

Question: Digital as % of Revenue

OF DIGITAL

Has digital generated the revenue returns Less than 25%

25% to 50%

you expect given the market changes we’ve 51% to 75%

seen recently? More than 75%

Everyone

About what No I was hoping No change Yes more than

I expected for more I expected

Overall most saw more revenue than they expected, 50%

showing huge and unexpected growth in the last

41%

18 months.

38%

Those with more than 25% digital revenue were 32%

most surprised, with more than 41% in all audience

groups saying, “Yes - more than I expected”. 25%

18%

Those with less than 25% digital revenue were

the audience who were hoping for more or saw no 13% 9%

change in digital revenue.

0%

SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsMost list these

THE

top 3 metrics:

Conversion rate

QUESTION: CHOOSE THE TOP 3 METRICS YOUR ORGANISATION IS FOCUSED ON (61%), Revenue

(40%) and Cost

per acquisition

TOP 3

(35%)

Question: Choose the top three metrics your organisation is focused on

METRICS

Overall conversion rate and revenue were the

Digital as % of Revenue

Metric

Less than 25%

Share of

responses

Metric

25% to 50%

Share of

responses

Metric

51% to 75%

Share of

responses

Metric

Over 75%

Share of

responses

Metric

Everyone

Share of

responses

Conversion rate 61% Conversion rate 79% Conversion rate 58% Revenue 55% Conversion rate 61%

top metrics showing a good level of measurement

Cost per acquisition 35% Cost per acquisition 38% Average order value 37% Conversion rate 48% Revenue 40%

maturity.

Revenue 32% Revenue 38% Cost per acquisition 32% Cost per acquisition 45% Cost per acquisition 35%

The group with 75% or more digital revenue were Revenue on advertising 42% Revenue on advertising 33%

Average order value 29% Average order value 25% Revenue 32%

the only group who focused on outcomes, with 55% spend spend

Return on Return on

listing revenue as their top metric. Advertising spend

26%

Advertising spend

25% Visitors 32% Visitors 23% Visitors 27%

Visitors 26% Visitors 25% Return on 26% 19% 26%

Average order value Average order value

Cost per acquisition was the lowest for those who Advertising spend

Add to cart and

had 25% digital revenue or less with only 35% Click-through rate 19% Click-through rate 17%

completion rate

21% Click-through rate 13% Click-through rate 15%

choosing this metric. Add to cart and

13%

Add to cart and

13%

Revenue per user or

16% Cost per click 13%

Revenue per user or

11%

completion rate completion rate Engagements per lead Engagements per lead

Conversion rate was the most popular metrics Cost per click 10% Cost per click 13% Sessions 16% Dwell time/time on site 10% Add to cart and

completion rate

10%

overall with 61% of respondents choosing this Sessions 6% Sessions 13% Click-through rate 11% Revenue per user or 10% Sessions 10%

Engagements per lead

performance metric.

SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsMost

BARRIERS

respondents

QUESTION: WHAT ARE YOUR BIGGEST BARRIERS TO GROWING DIGITAL (56%) said

REVENUE FURTHER? they needed

more budget

towards digital.

TO GROWING Question:

What are your biggest barriers

Digital as % of Revenue

Less than 25%

DIGITAL

25% to 50%

to growing digital revenue further? 51% to 75%

More than 75%

Everyone

More budget Measuring our We do not have Risk to moving Technology is out Our agencies

Most audiences wanted more budget towards towards digital digital activity and the right skills from what of date don't get it

connecting it today we know

digital or had issues with connecting revenue to to revenue

digital activity. It was good to see agencies were not

60% 57%

seen as a hindrance with very few stating this was 56%

51%

an issue. 49%

45%

The 75% or more group were those who were most 35%

likely to have the right technology or team in place. 30%

30%

Only 16% state technology or 5% skills as barriers.

19% 19%

They were also the least risk averse. 16%

15%

Only those who had 25% or less were most 5% 4%

0%

concerned about moving from what they know 0%

(45%). Technology and skills was the biggest barrier

for the between 25% and 50%. SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsENSURE

Most respondents

QUESTION: HOW PREPARED IS YOUR ORGANISATION FOR THE (54%) said they had

a plan and changes

CHANGES AHEAD? were being applied

now

PLANNING Question:

How prepared is your organisation

Digital as % of Revenue

Less than 25%

IS IN PLACE

25% to 50%

for the changes ahead? 51% to 75%

More than 75%

Everyone

USING DATA

We are fully We do not have We have a plan We have a plan

prepared and a plan . . . help! and changes are but have not

have already made being applied now yet started

the necessary changes making changes

70%

Most audiences had a plan in place and were at

varying degrees of that plan being implemented. 54%

52%

53%

The 75% or more group were those who were most

39%

likely to have already implemented a plan with 52%

35%

saying their plan was already in place, compared to 29%

all respondents at 29%.

18% 15%

Only those who were 50% or less had no plan at all, 10%

and they also tended to also have a plan which had 0%

2%

0%

not started implementation.

SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsOverall 53%

DATA

said they used

QUESTION: HOW DO YOU MEASURE SUCCESS AND HOW MUCH IS data to measure

marketing

DATA AND ANALYSIS A FACTOR? effectiveness,

with some use of

NOT

analysis

Question: Digital as % of Revenue

DASHBOARDS

How do you measure sucess and Less than 25%

25% to 50%

how much is data and analysis a factor?

51% to 75%

More than 75%

Everyone

Data and analysis Data is not used Data is used to measure We have dashboards

is at the centre of to make decisions marketing effectiveness and reports to measure

Very few of the audience used dashboards and all decision making in digital and we use some analysis campaign performance,

for decisions but do not use analysis

reports to measure campaigns. Most used data to

70%

measure campaign effectiveness.

51% 53%

Those in the 75% or more group were the most data 53%

43%

focused, with 51% saying they use data and analysis

35% 35%

for all decision making, compared to all respondents

at 35%.

18%

Those in the 25% or less group were the only 4% 5%

8%

audience to not use data at all to make decisions in 0% 0%

digital. SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsMEASURING SUCCESS

THE ENGAGEMENT VISIBILITY

Recording of non-transactional

user behaviour

4 SHOPPING VISIBILITY

Using Google Analytics Enhanced

Ecommerce to understand

L E V E L O F M AT U R I T Y

Not all brands can become digital first brands. Price shopping behaviour

LEVELS

point and margin are critical factors for making that

decision.

It is easier for L’Oreal to become a digitally focused

OF

business when their average order value is likely to Using Google Analytics Ecommerce

be £50 ($68). Versus Hershey who might struggle TRANSACTION VISIBILITY to measure revenue and sales

to sell chocolate if the cost of deliver is similar to the

cost of the products.

MATURITY

Creating a sense of urgency for Domestos (Reckitt)

and Dove (Unilever) might be harder.

Offering products direct to consumer has to more TRAFFIC VISIBILITY

Tracking visitor volume and pages viewed

on the website (Google Analytics)

than putting products on a website if the price point

or sense of urgency is not there.

S TA R T H ER ETRAFFIC ENGAGEMENT VISIBILITY

Recording of non-transactional

user behaviour

VISIBILITY Using Google Analytics Enhanced

Ecommerce to understand

SHOPPING VISIBILITY

L E V E L O F M AT U R I T Y

shopping behaviour

KEY CHALLENGES:

• Which traffic is engaging the most?

• Can you connect the impact of the website to

Using Google Analytics Ecommerce

sales? TRANSACTION VISIBILITY to measure revenue and sales

• What content or products are most popular (i.e.

most viewed)?

Tracking visitor volume and pages viewed

TRAFFIC VISIBILITY on the website (Google Analytics)

S TA R T H ER ETRANSACTION ENGAGEMENT VISIBILITY

Recording of non-transactional

user behaviour

VISIBILITY Using Google Analytics Enhanced

Ecommerce to understand

SHOPPING VISIBILITY

L E V E L O F M AT U R I T Y

shopping behaviour

KEY CHALLENGES:

• Which products are performing the best?

• Which campaigns are the most profitable vs Using Google Analytics Ecommerce

those costing money? TRANSACTION VISIBILITY to measure revenue and sales

• Where have customers fallen out of the purchase

journey?

Tracking visitor volume and pages viewed

TRAFFIC VISIBILITY on the website (Google Analytics)

S TA R T H ER ESHOPPING ENGAGEMENT VISIBILITY

Recording of non-transactional

user behaviour

VISIBILITY Using Google Analytics Enhanced

Ecommerce to understand

SHOPPING VISIBILITY

L E V E L O F M AT U R I T Y

shopping behaviour

KEY CHALLENGES:

• Where are customers struggling to find the right

product?

Using Google Analytics Ecommerce

• Which SKUs (colour and sizes) are selling well in TRANSACTION VISIBILITY to measure revenue and sales

what channel?

• What products and price points should I offer to

my mobile vs desktop audiences?

Tracking visitor volume and pages viewed

TRAFFIC VISIBILITY on the website (Google Analytics)

S TA R T H ER EENGAGEMENT ENGAGEMENT VISIBILITY

Recording of non-transactional

user behaviour

VISIBILITY Using Google Analytics Enhanced

Ecommerce to understand

SHOPPING VISIBILITY

L E V E L O F M AT U R I T Y

shopping behaviour

KEY CHALLENGES:

• What content (including videos) is my audience

engaging with for research vs purchase?

Using Google Analytics Ecommerce

• What impact are wishlists and account creation TRANSACTION VISIBILITY to measure revenue and sales

having on repeat sales?

• What products should I bundle for each of my

channels?

Tracking visitor volume and pages viewed

TRAFFIC VISIBILITY on the website (Google Analytics)

S TA R T H ER EWHERE TO FOCUS TO IMPROVE MATURITY

CUSTOMER BRAND BUSINESS EVALUATION

TESTING AND TRAFFIC

CONTENT MEDIA MERCHANDISING OFFERS IMPACT AWARENESS GOALS SKILLS DATA USED METRICS

EXPERIMENTATION CLASSIFICATION

Show product Incentivise offers to Monitor website visitors Use paid search, Track non-

Measure the cost of Value of purchasers

Categorise content into: recommendations or certain actions (writing a from non-prompted shopping, display, transactional actions

ENGAGEMENT

visitors who engage Understand user Trading, Test different who engaged with

VISIBILITY

- Used for awareness content based on wishlist review, sharing content, channels (direct, referral affiliates/online partners Paid and organic social such as wishlist, social

on your website and behaviour to drive merchandising, media elements on a given content, reviews,

- Used for research/intent or other non transactional creating a wishlist), e.g. and organic search), and paid social to drive is correctly classified sharing and viewing of

then purchase on a repeat purchase and content teams page or signed up to a

- Used for purchase engagement (“Things you get free delivery for during brand campaigns brand awareness videos, and categorise

returning visit newsletter

might like”) creating an account to understand impact and sales your content pages

Validate brand building Capture product detail

Show products which Use retargeting Lifetime customer

by comparing the page views, add to

Categorise content have been most viewed (visitors who have visited Recover lost Trading, Test different product profit, average order

VISIBILITY

SHOPPING

Measure the cost of Make overall site wide click-through rate, bounce Email is correctly cart, checkout journey,

and link to revenue or popular purchases on and shown intent) to customers/non- merchandising and list page formats/ profit, cart completion

discount/offers offers, e.g. 20% off rate, conversion rate and classified and group products

generation homepage and on product create brand affinity purchasers media teams layouts rate, product detail

cost per acquisition as into category and sub-

list/category pages and sales page view rate

visitors know your brand categories

Track share of page 1 Capture visitors who

Digitial revenue as a

Show popular products from organic search. Use some digital media Google media is make transactions

TRANSACTION

Create content based on Measure cost per % of total revenue,

VISIBILITY

and highest revenue Monitor brand terms for brand building and Drive sales and Trading and media A/B testing on correctly classified on your website,

what products generate acquisition of purchasing No offers available revenue, conversion

products first on and if your share of page offer-led messaging transactions teams landing pages and referrals only from ensuring you record

the most revenue visitors rate, average order

homepage 1 increased from brand genuine sources the number and value

profit, items per basket

building of transactions

Measure impressions Benchmark your overall

Visitors and sessions,

and click-through rate, share of organic search Limited measurement, Record website

VISIBILITY

TRAFFIC

Prioritise content based All media and brand Traffic is not page impressions,

engaged visitors those Show popular pages first N/A and uncover the brand Drive repeat visitors someone who can use None visitors who browse

on most viewed building is offline categorised bounce rate, session

who do not bounce to and category terms you Google Analytics your web pages

duration

calculate cost per visitor are leading1 2

OUTCOME PERFORMANCE

METRICS METRICS

NOT ALL

Actions relating directly Sales related behaviour that

to revenue to understand gives an understanding into

trading. marketing effectiveness.

METRICS

(Revenue, repeat (Conversion rate or

purchase rate or lifetime average order value)

customer profit)

ARE

CREATED

3 4

BEHAVIOUR VOLUME

METRICS METRICS

EQUAL Actions relating to visitors:

what they are doing and

engaging with.

(Add to cart or basket

An overall view of how

visitors are engaging

with your brand.

(Number of visitors to

abandonment rate) the website)TO

METRICS

ALIGNING

MATURITY

METRICS TYPE

VOLUME

OUTCOME

BEHAVIOUR

PERFORMANCE

TRAFFIC

VISIBILITY

TRANSACTION

VISIBILITY

SHOPPING

VISIBILITY

ECOMMERCE MATURITY LEVEL

ENGAGEMENT

VISIBILITYWANT TO GET IN TOUCH OR LEARN

CREATE HOW TO MAP OUT YOUR

YOUR

MEASUREMENT DIGITAL MEASUREMENT

ROADMAP? NEXT STEPS IN OUR BOOK

YOUR BER’S

NUM 10% off

UP!

t

men

ata and

ce

sure

Mea ales

s

use Research UK as coupon code

on D commer

grip E

etting a ate your ik

G

celer Kaus

h

to ac d by Avinash

wor

Fore

W

SHA

TIM

AND

RA HAM

R AB

E TE

O N , P PKINS

M

SAL SICA HO

B EN ESAPPENDIX LXX LXXI

QUESTION: HOW MUCH REVENUE DOES DIGITAL GENERATE AS A PERCENTAGE OF YOUR

RESEARCH ORGANISATIONS TOTAL REVENUE?

PARTICIPANTS

A survey was deployed from January to March

2021. We collected 124 respondents, who were

from UK, USA, Europe and Australia.

The survey was deployed to those who worked in

digital with a mixture of brands and agencies and

software providers.

SOURCE: Primary research from wearecrank from 25th January to 1st April 2021: 124 respondentsCOMPARING

WINNERS AND

LOSERS

SOURCE: Companies house Laura Ashley Annual report 2019 and https://www.nextplc.co.uk/investors/ten-year-historyPURELY OFFLINE

VS

PURELY ONLINE

SOURCE: Associated British Foods Plc and ASOS plc1 2

FREE STUFF. OVERWHELMED?

About Crank. Go to: I am baffled and want to know what this

wearecrank.com/resources digital thing is all about?

to get your hands on some goodies. This We offer senior and team coaching based

Def 1. verb: Turn a handle in order to start an engine. will continually be updated with new on our method in this book. To this end

content to help people master their we often get asked to either speak at

culture of measurement journey.

Def 2. noun: A person who is obsessed by a particular subject. events or work with teams to help them

We know there is a lot in the book and we understand how they can create their own

We’re a delightful mashup of the two. are here to help. Hopefully you can tell we culture .of digital measurement. This can be

love digital measurement and some of our

educational or more prescriptive by taking

enthusiasm has rubbed off.

We’re unashamed digital marketing and ecommerce nuts who crank new life, new value and new growth your data and auditing how you measure

into digital businesses just like yours. We have been working with digital data

today.

for over 20 years but have really focused

on Google Analytics and built our own book@wearecrank.com

analysis tools in the last 5 years.

WE’RE SHARP YET BLUNT

3 4

For over 5 years Crank has been working with ecommerce businesses, advising them on how they create

growth through better measurement and use of data. We have worked with a variety of businesses from

beauty, technology, software, higher education, charities and fashion.

A MEASUREMENT I NEED A

We are Sharply focused on highlighting the actions that enable you to grow your business.

ROADMAP. UNICORN.

How good is good and where do I need Interpretation, where can I find one of those

Blunt about showing you the evidence that points to engagement and growth. to start? unicorns?

We can help create your measurement Fortunately this is exactly what we have

No more 100-page presentations or meaningless charts. Just clear marketing actions in a language you roadmap. We will use our methodology been doing using data directly from Google

understand. to benchmark you business and help you analytics. Our software extracts the data and

understand what you need to put in place our team then performs the magic. Actually

Giving you the focus you need to execute the most important actions while maximising limited time, budget first to ensure you have solidified your what we do is interpret and translate our

and resource. metric maturity. We will then work with findings into a set of actions your team can

you to create a prioritised roadmap to get on with. These are data driven and are

Our goal is to get digital revenue as a percentage of total revenue on every annual report. We want help you work out your immediate next impartial. We just want to help you deliver

transparency, with a common set of critical digital metrics, so shareholders and leaders of businesses can steps. growth.

clearly show much they are investing in digital and how much it is contributing to their business.

Digital isn’t going anywhere, and the quicker you embrace it, the better off you’ll be. We are here to help

you understand how to measure your business and what you need to do to make the most of it.

weareCrank.com +(44) 20 3302 0807 book@wearecrank.com

LXXIXYou can also read