GUIDE - V12 Retail Finance

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

R E TA I L E R

GUIDE

CONTENTS

1. Introduction 3 7. Instore signature 14

2. Retailer obligations 8. Web applications 16

2.1 Advertising and Compliance 3 9. Releasing the goods to the customer 16

2.2 Change of trading entity, names and 3 10. V12 Self Service Portal 17

business ownership 3 11. Discussing a credit decision 17

2.3 Validation Checks 4 12. How to search for an existing application 18

2.4 Preventing Fraud 4 13. How to re-send a copy of an 19

agreement to the customer

2.5 Delivery of Goods 5

14. When to request payment 20

2.6 Proof of delivery requirements 5

15. How to request a payment 20

2.7 Extended warranty/ 5

16. Application status 21

service plan products

17. How to cancel an application 22

2.8 Merchandise complaints 6

18. Reports 22

2.9 Security 6

19. Payments 22

2.10 Anti-money laundering requirements 7

20. Written credit quotations 23

3. Customer eligibility 7

21. Vulnerable customers 23

4. How to login to the V12 system 8

22. Contact us 24

5. Administration within the V12 portal 9

6. Processing an application 10

6.1 Data protection 13

RETAILER GUIDE 2

VERSION 5

1. INTRODUCTION

At V12 Retail Finance we know that our market leading software needs to be as accessible and user friendly as possible.

That’s why the V12 Retail Finance system has been developed over the past 10 years in close collaboration with our retail

partners. It offers easier application processing and faster credit decisions across all channels – whether in-store, mail order

or online – helping you increase sales and profitability. This guide should give you everything you need to know about the

system, but if you still have questions please call our Sales Support Team on 02920 468918.

V12 Retail Finance Limited are owned by Secure Trust Bank PLC. V12 Retail Finance Limited. Registered in England and Wales

4585692.Authorised and regulated by the Financial Conduct Authority. Registration number: 679653. Registered office: One

Arleston Way, Solihull, B90 4LH. Correspondence address: 20 Neptune Court, Vanguard Way, Cardiff, CF24 5PJ.

V12 Retail Finance Limited act as a credit broker and introduces to one or more lenders, for which they will receive a commission.

Secure Trust Bank PLC. Registered in England and Wales 541132. Authorised by the Prudential Regulation Authority and

regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registration number: 204550.

Registered Office for both: One Arleston Way, Solihull, B90 4LH.

V12 Retail Finance (V12) is a trading name of Secure Trust Bank PLC.

2. RETAILER OBLIGATIONS

2.1 ADVERTISING AND COMPLIANCE

As the retailer, you are responsible for the way you advertise and promote the use of finance to the customer. You can only

promote the use of finance, as defined by the Financial Conduct Authority (FCA) Consumer Credit Sourcebook, if you are

authorised by the FCA and it is your responsibility to ensure all financial promotions are compliant with the regulations.

You can refer to V12’s Credit Advertising Guidelines which can be found on the V12 portal next to the Retailer Guide.

2.2 CHANGE OF TRADING ENTITY, NAMES AND BUSINESS OWNERSHIP

You are also required to update us of any changes that could affect your contractual obligations with us, our customers or, if

you are a regulated business, any Financial Conduct Authority permissions you hold.

As soon as you become aware of any future or existing changes to your company, including areas such as changes to the

contracting entity, structure and trading styles it is your responsibility to contact us immediately so we can agree the best

course of any action. Failure to do so may result in restrictions to your account whilst a resolution is agreed

RETAILER GUIDE 3

VERSION 5

2.3 VALIDATION CHECKS 2.4 FRAUD PREVENTION

For the in-store application, web and mail order application At V12 Retail Finance, we take our responsibility and

journey we validate customer information with the cutting commitment to the identification and mitigation of fraud

edge fraud validation tools. This process runs in the very seriously. We would like to remind you of your own

background and you won’t be required to ask the customer responsibilities to co-operate in fraud investigation and

for any additional verification checks. defences, ensuring timely disclosure of all evidence held by

you relating to V12 fraud investigations.

If the customer is making a web or mail order purchase

then the goods must be delivered inside the verified V12 may introduce further checks or rules in the credit

address on the customer’s credit agreement or an address decision process to mitigate against potential fraud losses,

approved by V12 Retail Finance. We do not permit the to keep V12, our retailers and our customers safe.

collection of goods from any other location that is not

V12 Retail Finance and our retailers should never profit

approved by V12 Retail Finance, including but not limited

from fraudulent activity. Any fraud cases identified where

to, a store, and delivery depot or drop point.

V12 Retail Finance suffers a financial loss, due to the action

Please refer to section 2.5 for information around or inaction of a retailer, the retailer will incur a charge back

obligation of delivery of goods. of 10% of the loan amount. This represents the level of

profit made by the retailer from the fraudulent transaction,

and ensures neither V12 nor our partners ever profit from

the proceeds of fraud.

RETAILER GUIDE 4

VERSION 5

2.5 DELIVERY OF GOODS

oods must be delivered to the address on the customer’s

G You should only deliver goods to the person named

credit agreement or an address verified by V12. on the credit agreement or a family member of that

person, as disputes can still arise even though goods are

nder no circumstances should goods be left outside of

U

delivered to the address on the agreement.

the address or in communal areas.

You must not release goods to third parties apparently

here delivery of goods has been unsuccessful, goods

W

employed by the customer (e.g. taxi drivers,

must always be returned to the depot and delivery

messengers, couriers etc).

re-arranged to the approved address. Under no

circumstances should the collection of goods be made ou should take reasonable precautions to ensure you

Y

from any other location that is not approved by V12 are delivering to the right person, and retain delivery

Retail Finance, including but not limited to, a store, notes for a minimum period of 24 months.

delivery depot or drop point.

Delivery notes should be available to present on

ou should instruct your carrier not to deliver goods if

Y demand to V12 Retail Finance. Failure to present within

the address appears to be uninhabited. 14 days of the request could result in claw back of the

loan amount paid to you.

2.6

PROOF OF DELIVERY REQUIREMENTS

All proofs of delivery must include the following information:

Name of delivery company Date and time of delivery

The delivery tracking number Delivery GPS tracking

The name and address goods were Delivery route

delivered to

The delivery driver’s name

The name of the recipient of the goods

and their signature

2.7 EXTENDED WARRANTY/SERVICE PLAN PRODUCTS

V12 Retail Finance do not allow finance to be used for payment of any extended warranty or insurance products without

our prior approval.

RETAILER GUIDE 5

VERSION 5

2.8 MERCHANDISE COMPLAINTS

If a customer claims the product is defective please make the customer aware that they are required to maintain their

payments until the complaint is resolved. There is no legal obligation to waive the terms of the agreement whilst a complaint

is being investigated. If a merchandise complaint is made against you, V12 requires you to act in line with its complaints

policy which complies with Applicable Laws as part of the agreement between the retailer, V12 and the customer, to

promptly assist in the resolution of the issue.

Although the customer may not have a justified complaint, under the finance agreement all parties mentioned above, share

the responsibility to achieve consensus and ensure the customer is treated fairly throughout the complaint process. We take

this responsibility seriously and respectfully insist our retail partners do the same.

In the event of non-cooperation, or failure to reach an agreement on a resolution, we may be required to claw back the

original amount paid to you. Where the retailer’s actions cause V12 to incur a cost as a result of a complaint against the

retailer, V12 is entitled to recover amounts paid due to but not limited to:

Distress & inconvenience paid to the customer

Statutory interest payments

Costs for independent reports

Any payments required to put the customer back in their original position

Financial Ombudsman Service (FOS) Fees

Financial Ombudsman Service awards

Any associated legal costs

If the customer is unsatisfied with the resolution and the complaint is linked to a regulated agreement, they will be eligible

to take their complaint to the FOS.

If the agreement is non-regulated, although the customer is not eligible to contact the FOS, we would expect all parties to work

together to ensure that the customers’ consumer rights are respected as there are other options open to the customer should

they decide to escalate their concerns

2.9 SECURITY

Security is an important concern for both the customer and the retailer during any online transaction. The V12 Retail Finance

gateway encrypts information submitted and uses proven techniques to ensure the security and integrity of sensitive data.

The public web servers used by V12 are certified by a leading certificate authority, ensuring that nobody can impersonate

V12 Retail Finance to obtain confidential information. Data storage on the systems and the communication between servers

is regularly audited to the highest standards to ensure a secure transaction environment. This includes regular third party

testing for vulnerabilities and reviews of application security and access control procedures.

Please remember to:

- always ensure that your password is kept secure

- frequently change your password

- ensure that you’re using equipment that’s up to date

- report any breach in your system to us as soon as possible

RETAILER GUIDE 6

VERSION 5

2.10 ANTI-MONEY LAUNDERING REQUIREMENTS

V12 Retail Finance, as a FCA authorised and regulated company, complies with the Money Laundering, Terrorist Financing

and Transfer of Funds (Information on the Payer) Regulations 2017. One focus of these regulation is to deter, prevent and

detect money laundering.

V12 Retail Finance have a number of controls in place to meet these regulatory requirements along with those placed upon

us by other relevant legislation and industry guidance.

One key requirement is to identify and verify an applicant prior to entering into a business relationship. Where possible,

these checks are undertaken electronically. However where this is not an option, the applicant will be required to provide

relevant documentation for review. If this is the case, once the application has received a positive credit decision, an email

will be sent direct to the customer setting out the requirement and detailing what documentation is acceptable.

3. CUSTOMER ELIGIBILITY

Before completing a credit application you should establish We don’t permit Owners, Directors, Partners, Sole Traders

that the customer qualifies for finance and can satisfy all to obtain finance to purchase goods from their business.

the following pre-check criteria.

If an employee is applying for finance to purchase

Please make sure that the customer: goods through their employer, they must seek

permission from their line manager who

is 18 or older

must then process the application.

Is, or their partner is, in permanent paid employment,

self-employed, retired and receiving a pension, working

student in part time work or in receipt of a disability benefit

has been a resident in the UK for at least 3 years

has a debit or credit card in their name, which is

registered to their address, in order to pay for the deposit

(if applicable)

has a Bank or Building Society current account available

(you’ll need this to complete the direct debit instruction)

Note: finance is not available for unemployed individuals.

Applications that have previously been rejected should

not be re-proposed within a 3-month period.

RETAILER GUIDE 7

VERSION 5

4

HOW TO LOG IN TO THE V12 SYSTEM

1. Go to www.v12retailfinance.com. Please save this link to your favourites or to your desktop.

2. Click on ‘Retailer log in’ at the top right hand side

3. Log in using the details given to you by your V12 account manager. Please note that your password is case

sensitive and has to be typed rather than copy & pasted. If you can’t remember your password then you can click

on the forgotten password link to retrieve it. If you can’t recall your username then you will need to contact us.

The best way to do this is to send an email to SalesSupport@v12finance.com from your business email address,

alternatively you can call our Sales Support Team on 02920 468918.

4. Please note that access to the V12 system is restricted to approved users only.

An approved user is someone who:

• is an employee of the Retailer; and

• has either (a) been approved for access to the V12 system by V12 Retail Finance directly, or (b) has been

approved for access to the V12 System by an employee of the Retailer who has been granted V12 system

administration rights by V12 Retail Finance

If you require access to the V12 System for individuals other than a direct employee of your business, such

as a third party or web developer, you will need to contact V12 Retail Finance Sales Support Team to discuss

your access requirements in order to approve your request and provide system access. It is your responsibility

to ensure you exercise the appropriate level of governance over your employees and agents. The Financial

Conduct Authority (FCA) has set out its expectations of regulated firms in the Consumer Credit Sourcebook

Chapter 14. For more information about the responsibilities of credit brokers, please refer to the FCA’s website.

RETAILER GUIDE 8

VERSION 5

5. ADMINISTRATION WITHIN THE V12 PORTAL

ADMINISTRATION

Each retailer will have their own V12 system administrator

which we have agreed with you. The administration functions

are only available to users as specified by you and can have

access to more functionality of the V12 system.

If you wish to add or amend users who have these functions,

please contact V12 Sales Support.

USERS

To make changes to existing users select ‘user’ and select

the username you want to update. Once you have made the

appropriate changes select ‘apply’.

To add new users select ‘user’ then ‘add new’. Enter the user

information, select the required access levels and branches

required. Select “Apply’, this will create the user and

generate an email to them to create their password. For more

information about adding users please refer to section 4 “How

to log in to the V12 System”.

PRODUCTS

You can view all of the available products that are set up on

your system. If you wish to offer a product that is not currently

live on your account please contact our V12 Sales Support

Team or your account manager.

SUMMARY

This will show your V12 Account Manager’s contact

details in case you need to speak directly with them.

It will also display the sales channels that you use and

the bank account details we hold for you. If these need

to be changed, please contact your account manager

or V12 Sales Support.

RETAILER GUIDE 9

VERSION 5

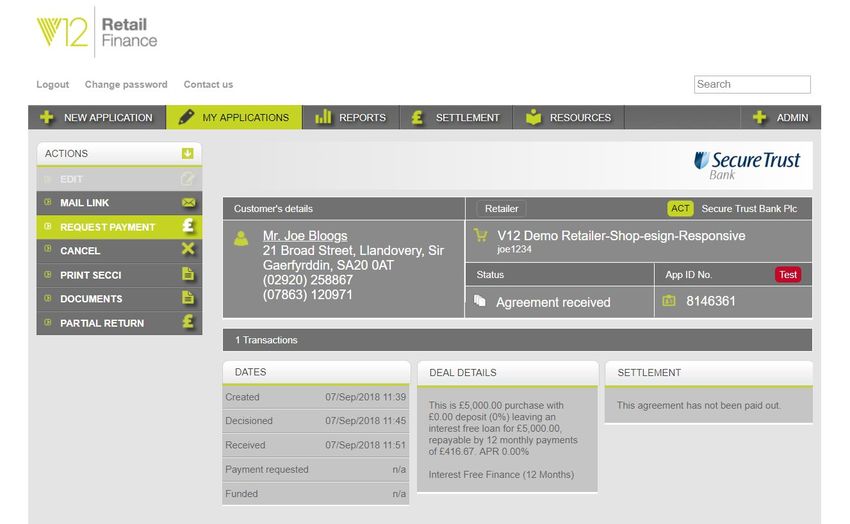

6. PROCESSING AN APPLICATION:

1 To access the V12 portal, log in using the details 2 Alternatively if you have requested a finance

given to you by your V12 account manager. Please calculator from us, you can use the calculator to

note that your password is case sensitive and has to discuss finance options with your customer. Once

be typed rather than copy and pasted. the customer has chosen their finance option select

‘Apply’ and continue with the application as below.

3 Once you are logged into the portal you will see 4 If the customer is in-store with you, please select the

the V12 dashboard which gives you access to all of ‘Shop’ option. If you would like to send an email to the

the functionality you require. In order to start a new customer and allow them to complete the application

finance application for your customer, click on the at home please select the ‘Mail Order’ option.

‘New Application’ icon.

5 You will then be asked to enter a cash price for the

total cost of the goods that are being financed and a

deposit amount if applicable (If a deposit is required

this must be taken using a chip and pin enabled card

in the name of the applicant. The minimum deposit

amount will be detailed on your client agreement

business schedule and the maximum deposit is

50% of the cost of the goods). You can also add

a reference number for your own use, such as the

customer invoice number, surname or sales person.

For mail order applications you will be required to

complete the customer’s first name and surname

along with an email address for us to send the

application form to.

RETAILER GUIDE 10

VERSION 5

6 The finance options you have available to offer will

be displayed. Choose the required option and select

‘Create Application’.

7 You are now free to proceed through the application

screen, entering the required information.

Dependent on your in-store set up you may wish to

allow the customer to fill these details in themselves.

To ensure customers are informed on how their

personal details are collected during the credit

application and will be used by V12 Retail Finance

Limited and Secure Trust Bank PLC, customers should

take time to read the information displayed on this

page thoroughly. The customer will be asked to

confirm if they are happy for us to share their details

8 We will ask for the customer’s personal details such with the retailer they are purchasing goods from,

as title, name and last name. All fields are mandatory before proceeding to fill in their details.

other than those marked as optional.

9 You will now be required to enter the customer’s

details such as: nationality, DOB, home address and

time at the address, we will also require 3 years’ of

UK address history.

Please remember that customer email address

10 Please select the customer’s employment information. cannot be the same as the user email address.

RETAILER GUIDE 11

VERSION 511 Once complete, select ‘Next’ and enter the 12 When you select ‘Next’ the customer will be

customer’s sort code and account number for the reminded of the credit search process and that a

account they want their monthly direct debits to log of the search will be left on their credit file. The

come from if the application is successful. customer will then need to select their marketing

preferences. We will never sell or pass on the

customer’s details for marketing purposes, however

we would like to make them aware of our products

and services or those from carefully selected third

parties such as lenders and brokers which we think

13 Once you have entered the details, please click they may be interested in. Finally the customer will

‘Next’. It usually takes under 20 seconds for a need to choose if they would like their statements

credit decision. to be sent to them electronically rather than by post,

If we are able to provide finance for the customer we which can be done by selecting that they wish to go

will show that the application has been ‘Approved’. paperless.

This will then lead onto the next page with the Please refer to section 6.1 on page 13 for further

important pre-contract credit information. information relating to credit searches, marketing

preferences and how personal data will be used

14 For retailers with in-store eSign move onto to

REFERRED

section 7 “in-store signature”.

If the application is more complex, we may

need to refer the decision. We appreciate

the customer is in-store waiting, so shop

applications are always prioritised and we

should provide a decision within 10 minutes. If

we require further information we will contact

the shop and ask to speak with the customer.

As soon as we have reached a decision we will

amend the status of the account online. We

therefore request that you regularly check the

status on the V12 system.

DECLINED

The declined decision will show on your screen.

You must print off the decision straight away so

that it can be passed to the customer.

RETAILER GUIDE 12

VERSION 56.1 DATA PROTECTION

Before continuing to the next stage of the application journey, you need to provide customers’ with the data protection

statement shown on the application screen which explains to the customer how their personal information will be used. The

process differs slightly depending on how the customer is applying for finance:

WEB

A link explaining to the customer “how your personal

information will be used” is within the Privacy Statement,

before the customer clicks the “process my application”

button after entering their application details. They are able to

print a copy off via their browser if they wish.

IN-STORE

This same links exists. You need to bring the customer’s

attention to this information, especially the “marketing

preference” boxes as you cannot proceed with the application

until the boxes have been ticked. You must then tick the

labelled box to tell us that you have shown the customer this

information page. You can print a copy off for the customer

if they wish.

MAIL ORDER

Again, you must bring the customer’s attention to this

information, especially the marketing preference boxes.

You must then tick the labelled box to tell us that you have

drawn the customer’s attention to this information page.

If the customer is completing this process at home then they

will tick to confirm they have read and understood how we

will use their personal information.

It is your responsibility to comply with the General Data Protection Regulations.

RETAILER GUIDE 13

VERSION 57. INSTORE SIGNATURE

1 Once we have successfully approved the customer 2 You will also be asked to read the important

you will need to read out the displayed important information statement out to the customer before you

information to the customer regarding pre-contract continue. This section includes important information

credit information and allow them to read the regarding the finance and it’s important that the

pre-contract credit information stored on the blue customer is happy with this before you proceed.

hyperlink below.

3 You are now required to read the important 4 You will now see a warning to remind you that all

information regarding the electronic signature of the following sections of the application must

process. be completed solely by the customer. For mail order

applications this message will not be displayed.

5 The customer will be asked to provide the answers to 6 This will lead into the pre-contract credit information

some security questions which should remain private, which the customer will read and select next when

only one question and answer is required. This will be they are happy to proceed.

used for data protection purposes when the customer

contacts us. For mail order applications this will not

be displayed.

RETAILER GUIDE 14

VERSION 57 The customer will now see the credit agreement, 8 A pop up box will appear asking the customer to

which covers all of the terms of their agreement confirm they wish to complete the application.

with V12 Retail Finance. The named customer on

the credit agreement is required to sign using our

eSign facility if they would like to continue. To sign

the agreement the named customer on the credit

agreement is required to click in the green box on the

bottom right of the application. The named customer

on the credit agreement will complete the same eSign

process if the application is online or via mail order. If

you use our in-store wet sign process, please print the

document to allow the customer to sign.*

If you have any issues during this process, you can contact

us on 02920 468900.

9 And that’s it! The page will automatically refresh to

display a message advising that the loan agreement

is signed and complete. We will automatically send

the customer the agreement to their email address,

however if they would like a copy to take away with

them you can click the hyperlink and print the signed

version for them.

*Please send all signed credit agreements to:

Customer Services, V12 Retail Finance, 20 Neptune Court,

Vanguard Way, Cardiff CF24 5PJ.

The application decision is valid for 90 days

from approval. Applications older than 90 days and not

received by V12 must be re-approved.

RETAILER GUIDE 15

VERSION 58. WEB APPLICATIONS

The V12 system is designed to be easily integrated into Declined

your web store. We have developed plugins for popular

The customer will be given an option to print off our

web stores as well as a range of tools to allow easy

information page about declined applications.

integration into any system or site. For more information

on how to integrate the V12 system into your web store, Referred

please contact your Account Manager or V12 Sales If the application is more complex, we may need to refer

Support Team. the decision. We should provide a decision within 2 hours.

In a small number of cases, it may take longer to carry out

Web applications decisions

additional checks. If we require further information we will

Approved contact the customer directly. As soon as we have reached

a decision we will amend the status of the account in the

The decision will show on the customer’s screen, along with

V12 system and advise you via email.

the next steps the customer will need to take, for example

pay a deposit if required, carry out the identity verification and

eSign the credit agreement. We will inform you of our decision

directly by email and also by updating the V12 system status.

For more information refer to section 6 “Processing an

application”, point 5 of the journey.

9

RELEASING THE GOODS TO THE CUSTOMER

In-store/shop applications Once we have received your document we will update

the status of the application to ‘Agreement Received’.

If the customer has used the eSign facility and signed

the document electronically in-store, this will update You can send the goods to the customer’s address on

the application to ‘Agreement Received’ status on your the application form once we have updated the status

account. Once the agreement shows this status you can of the agreement to ‘Agreement Received’. You can

release the goods to the customer. search for all applications at this status by selecting ‘My

applications’ and then clicking ‘Awaiting fulfilment’ in

For wet signature agreements that have not been

the quick searches on the left of the screen.

signed using eSign, please post the ‘V12 Copy’ to

V12 Retail Finance, 20 Neptune Court, Vanguard Way, For more information refer to section 2 “Retailer

Cardiff, CF24 5PJ. Obligations” points 2.3 (“Validation Checks”), 2.4

(“Fraud Prevention”) and section 19 “Payments”.

RETAILER GUIDE 16

VERSION 510. V12 SELF-SERVICE PORTAL

As soon as the customer’s credit agreement is live, they will be able to access the V12 Self-Service Portal. The V12

Self-Service Portal has been developed with functionality that allows customers to self-serve their V12 account on any

device, at any time of the day. The customer can change their bank details or payment date, update their personal details,

and send our Customer Service Team a secure message, all 24 hours a day.

The customer will receive a link to log into the Portal in their welcome letter or email, the process to register is quick and

simple and the customer can begin managing their account straight away.

If you would like to know more about the V12 Self-Service Portal, please contact your Account Manager.

11. DISCUSSING A CREDIT DECISION

In-store/shop application

We acknowledge mistakes can happen when inputting an application (such as spelling errors or

incorrect house numbers) and this can lead to a declined decision. In the rare instance that this

might have happened, please contact the underwriting team on 02920 468916.

Mail order and web applications

In the event that a customer wishes to speak to us about our decision, we advise

all customers to obtain an up-to-date copy of their credit report (through

TransUnion, Equifax or Experian) before contacting us.

Customers can contact us by phone on 02920 468916 or by

email to underwriting@v12finance.com where we will aim to

respond within 24 hours.

RETAILER GUIDE 17

VERSION 512. HOW TO SEARCH FOR AN EXISTING APPLICATION

1 If you know the application number or your order 2 Alternatively select ‘My Applications’ to search using

reference use the search box on the top right hand other criteria, for example via ‘Date’ or ‘Store’.

side ‘Search’ and enter the details.

3 If you know the customer’s details select ‘Locate 4 This will then give you the option to enter the

customer’ at the bottom of the list. customer’s personal information.

5 Click on the App ID number to bring up the

customer’s details.

RETAILER GUIDE 18

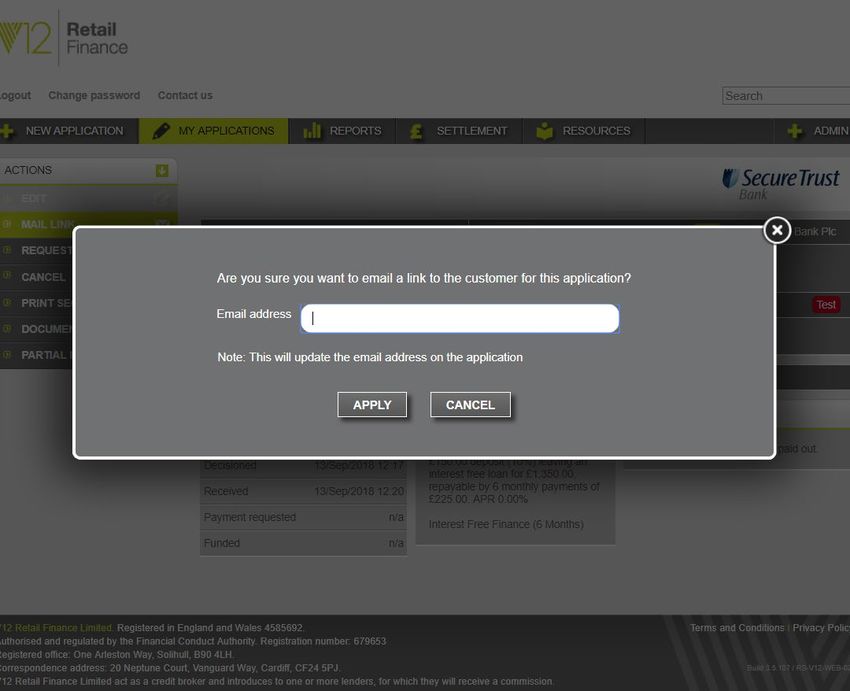

VERSION 513. HOW TO RE-SEND A COPY OF AN AGREEMENT TO THE CUSTOMER

1 Search for the customer’s account (by using the 2 When the customer’s account has loaded you will see

Search box in the top right hand corner). the action menu on the left hand side.

3 Choose option ‘Mail Link’. 4 This will offer a pop up for you to type the customer’s

email address and click ‘Apply’.

RETAILER GUIDE 19

VERSION 514

WHEN TO REQUEST PAYMENT

Requesting payment differs depending on which Shop (wet sign) – payment is automatically requested

channel the application has come from. You can request on receipt of the signed credit agreement, unless you

payment: have made alternative arrangements where you request

manual payments.

Online eSign – when the customer has signed the

documents and had the goods delivered to their home Mail Order – when the customer has signed the

address on the credit agreement or an alternative V12 documents and had the goods delivered to their home

approved delivery address or had the service provided. address on the application form or had the service

provided.

Shop eSign – when the customer has signed the

documents and taken the goods from the shop or For more information refer to section 2 “Retailer

taken delivery or had the service provided. Obligations” points 2.3 (“Validation Checks”) and 2.4

(“Fraud Prevention”).

15. HOW TO REQUEST A PAYMENT

1 Search for the customer’s application (please see 2 You can access all agreements at this stage by

‘How to search for an existing application’). selecting ‘Awaiting fulfilment’ within the quick

searches section of the ‘My Applications’ page.

3 Select the application you would like to request 4 From the ‘Actions’ menu located on the left hand

payment for by clicking on the application number. side, select the option ‘Request Payment’.

RETAILER GUIDE 20

VERSION 516. APPLICATION STATUS

ew – a new application that has not yet been submitted for credit checking as the details are not

N

fully completed. Any applications not submitted for decision within 7 days of being created will be

automatically cancelled.

Referred – an application that requires further review by V12.

Information Required – an application that has been reviewed by V12 and is awaiting further information

from the customer.

Declined – an application that has not met our minimum criteria.

Approved – an application that has been approved but has not yet been signed by the customer.

greement Received – an application that has been approved, passed our identity verification

A

and V12 are in receipt of a signed credit agreement. At this stage the goods can be provided

to the customer or dispatched.

Cancelled – an application that has been cancelled before we have made payment

to you.

ayment Requested – an application that you have requested to be paid

P

for that will shortly be processed, following the goods being provided to

the customer or dispatched.

ayment Processed – an application that has been paid out to

P

you in full.

law Back Requested – an application that has been

C

paid out and then cancelled (claw back is the

terminology we use when claiming funds back

from our retailers). Once the money has been

returned to V12, the application status will

show as Cancelled.

RETAILER GUIDE 21

VERSION 517

HOW TO CANCEL CANCELLATIONS

AN APPLICATION

A cancellation may occur for various reasons. Rest

assured, we will only cancel an authorised or funded

1. S

earch for the customer’s account (please see

sale upon your request.

‘How to search for an existing application’).

Before we have settled your payment: Letting us

2. S

elect the application you would like to cancel

know at this stage will ensure that we cannot process

by clicking on the application number

the application further and process your payment

3. O

nce the customer account has loaded, you will unintentionally.

see an ‘Action’ menu on the left hand side.

After we have settled your payment: We will cancel

5. If you want to add notes, for example a reason for the customer’s active finance agreement. You will need

cancellation, you can do so via the pop up box. to refund any deposit paid by the customer if taken

Once you’ve finished, confirm you want to cancel by you. We will claw back the amounts previously

by clicking ‘Yes’. settled to you under this transaction, and refund the

4. Choose the option ‘Cancel’. customer with any instalments made under the finance

agreement along with their deposit if taken by us.

Any commissions paid to you in association with a

If the application is cancelled then any deposit cancelled agreement will be clawed back accordingly

we have taken from the customer on your behalf and may be subject to an administration fee.

will also be refunded to the customer.

18. REPORTS

Reporting functions are controlled by access level. If the reports tab does not show on your configuration, please speak

to one of the admin users for your business.

In the V12 system, you will see a panel called ‘Reports’. Clicking on this will display a host of useful information that can

be customised using the options on the left to change the details and dates of the report.

Reporting can be completed at both an individual branch level and at a central, company wide level.

All reports are generated in real time and can be downloaded where you see the ‘Export to CSV’ button.

19. PAYMENTS

We provide a comprehensive fulfilment service and will release your payment once you have confirmed that the goods

have been delivered. The V12 Retail Finance payment system is fully automated to achieve the fastest possible turnaround.

The V12 Retail Finance portal provides all the settlement data you require electronically, so we will not send any paper

remittance out to you. Payments are made through the Bankers Automated Clearing System (BACS) ensuring prompt,

efficient settlement.

RETAILER GUIDE 22

VERSION 520. WRITTEN CREDIT QUOTATIONS

If the customer requests a written credit quotation, please ask them to send their request to V12 Retail Finance,

20 Neptune Court, Vanguard Way, Cardiff, CF24 5PJ. We will then send a written credit quotation directly to the customer.

21. VULNERABLE CUSTOMERS

A vulnerable customer is someone who, due to their personal circumstances, is especially susceptible to detriment,

particularly when a firm is not acting with appropriate levels of care. Although the decision to lend rests with V12 as the

finance provider, the retailer is the person who may have direct contact with the customer and so may be in a good position

to recognise the signs of vulnerability.

How to identify a vulnerable customer Things to think about

Vulnerability can take many different forms and is not eing able to identify possible vulnerability, as part

B

always obvious. Some customers will tell you if they have of the credit application process and taking time to

a problem, but others may be more reluctant to do so, consider it for every application.

because they fear that if they admit to a problem, this may

Implementing training procedures on vulnerability or

affect their chances of obtaining finance. If you believe that

sourcing training requirements.

a customer might be vulnerable, is being pressured, or that

something is not quite right, then ask them more questions Become familiar with your firm’s vulnerability policy.

and alert us if you’re concerned.

Types of vulnerability You will need to alert us if you think a customer may have,

There are many different types of vulnerability – some or is experiencing, a particular vulnerability which may

examples are given below (please be aware that this is not affect their ability to enter into a credit agreement. We

a definitive list) have dedicated staff who can help in these situations. If

you identify an issue, you can discuss with the customer

Customer has difficulty in understanding basic numeracy

how best to meet their needs. It may be that before being

Customer is unable to read, or if English is not their first referred to the lender or entering into a credit agreement,

language the customer would benefit from taking more time to

consider whether they are able to fully understand the

Customer has a mental health issue

commitment. Remember to ask the customer for explicit

ustomer mentions having been diagnosed with a

C consent when informing us about an identified vulnerability.

serious illness

Where you feel it’s appropriate to discuss a customer’s

Customer repeatedly asks the same questions despite circumstances with us, V12 have a dedicated Specialist

adequate explanations having been provided to them Support Team that can help. You can contact them on 0333

122 1112 or by email at sst@v12finance.com.

We strongly suggest you refer to FCA Occasional Paper No. Specialist Support Team opening hours are: Monday to

8: Consumer Vulnerability for more details of identifying and Friday 8am to 6pm. Those hours exclude weekends and

managing vulnerable customers. bank holidays, if you would like to contact the team on

these days please send an email to: sst@v12finance.com

and they will respond within 2 working days of the business

opening hours detailed above.

RETAILER GUIDE 23

VERSION 522

CONTACT US

Please send all credit agreements and Customer services

correspondence to this address: Telephone: 02920 468900

V12 Retail Finance Limited Email: customerservices@v12finance.com

20 Neptune Court

Vanguard Way Sales Support

Cardiff Telephone: 02920 468918

CF24 5PJ Email: SalesSupport@v12finance.com

Specialist Support Team

Registered Office: Please do not send credit

Telephone: 0333 122 1112

agreements to this address:

Email: sst@v12finance.com

One Arleston Way

Underwriting department

Solihull

Telephone: 02920 468916

West Midlands

Email: underwriting@v12finance.com

B90 4LH

Validation Team

Telephone: 02920 466325

Email: validation@v12finance.com

You can also find your account manager’s contact details

under the Admin > Contacts area of our system.

RETAILER GUIDE 24

VERSION 5You can also read