Gold Resource Investor, February 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Gold Resource Investor, February 2021

Gold’s Month in Review. Buying Physical Gold. Commodity Comeback. Gold

Technicals. Gold Resource Investor Buys: Altius Minerals, Alamos Gold. Full

Portfolio Table. Portfolio Updates: Sandstorm, Barrick, Kinross, Equinox, Troilus,

Cameco

February 15, 2021

It’s probably fair to say gold’s been widely ignored this past month but, interestingly, gold buying

at bullion dealers has been wild, as more and more general investors are cluing into, and piling

into precious metals as a safe haven. The silver squeeze lit a fire under silver, at least

temporarily, but silver continues strong. In fact, the price of physical metals has detached from

the spot and futures prices.

As a result of this surge in demand, most physical silver products also remain sold out. Trying

to get either metal from a bullion dealer at anything close to normal premiums is impossible right

now. It’s going to be interesting to see how this discrepancy is resolved. I think spot silver

prices will simply rise, premiums will fall, and the price will meet in the middle at much higher

levels than today’s.

This month in Buying Physical Gold I delve into what I think is the best physical gold to buy,

and why. I also list a few bullion dealers I know of. And since premiums are ridiculously high

right now, I suggest a way for you to own gold, at least temporarily, while you wait for premiums

to approach normal once again, giving you a chance to buy then.

While gold has drifted sideways and been ignored by the market (except physical), most

attention has gone to other metals, like silver, and platinum, not to mention base metals like

copper, zinc and nickel. Uranium has been in an odd position. While the metal’s price has

been flat or weak, the shares of producers have been on fire. That’s the market pricing in

renewed strength in longer term uranium pricing, and the anticipation of more to come.

My technical analysis of gold’s action suggests we could be in for a bit more consolidation or

weakness before gold finally renews its uptrend. As a result of ongoing strength in several base

metals, I explain in Commodity Comeback why I think we’re in the early days of a new

commodity supercycle. And I’m adding a new pick this month that will leverage this new secular

bull market, but with low risk and potentially strong upside. It’s a company I’ve followed for

years that has a stellar reputation. And while gold’s not getting the love it deserves, I’ve added

a cheap and superbly run mid-tier gold producer that pays a reasonable dividend.

1

______________________________________

Gold’s Month in Review

While gold is now entering its 7th month of correction/consolidation, consider that it effectively

rose for 8 months in its last rally, from December 2019 to August 2020. This correction may

well last as long. We could be in for a little more sideways action or weakness before the gold

bull market resumes. That’s caused most of the gold holdings in the portfolio to become

oversold and, I believe, attractive to accumulate on days of weakness.

I’m somewhat concerned we could be heading into a period of strength for the USD. While that

in itself isn’t a problem - I don’t expect it to last more than a few months, maybe less - but it

could be a headwind for precious metals and resources, as they are all priced in the USD.

However, demand for these commodities can certainly outstrip the effects of a rising dollar, so

it’s not a certainty that will keep commodities from advancing.

What’s causing this? In a word, yields. U.S. longer term bond yields have been rising, and

that’s attracting capital. Money goes where it’s treated best. So people are plowing their cash

into those bonds as they producer higher yields. But foreigners are noticing too. So they

convert their currencies into US dollars to buy longer term bonds. As a result, that new demand

for the dollar pushes up its value against other major currencies, which weighs, or can weigh, on

gold priced in USD.

Still, gold’s outlook remains solid. None of the fundamental drivers of money printing, massive

stimulus, geopolitical risks, and even a longer term weakening US dollar have changed.

Besides, even in the near term, gold’s seasonal trends show strength in February, potential

weakness in March, followed by renewed strength into summer. We’re in the midst of Chinese

Lunar New Year celebrations, and gold jewelry sales are forecast to surpass last year’s levels.

What’s more, some epidemiologists are warning we could get a huge 3rd wave of Covid-19

cases around April, and that could lead to gold-buying for safe haven protection.

Bitcoin has surged to new all-time highs, near $48,000 USD, with a recent boost from Tesla’s

Elon Musk. Tesla’s latest 10-K filing in the US revealed they bought $1.5 billion worth of bitcoin,

as they’ve adjusted their investment policy:

“In January 2021, we updated our investment policy to provide us with more flexibility to further

diversify and maximize returns on our cash that is not required to maintain adequate operating

liquidity...we may invest a portion of such cash in certain alternative reserve assets

including digital assets, gold bullion, gold exchange-traded funds and other assets as

specified in the future.” (emphasis mine)

As you can see Musk is also allowing for the purchase of gold bullion and gold ETFs to diversify

and maximize returns. With the huge number of people who follow what Musk does, this is big

news. But it’s not just Musk who’s looking for better stores of value for cash. Last Thursday,

the Idaho State House approved a bill, with overwhelming support, that allows the State

Treasurer to preserve state reserve funds from inflation and financial risk by holding physical

gold and silver. Their concern is that reserves are in low-yielding debt like bonds, treasuries

and money market funds, which are at the mercy of inflation risks eroding principal. And in

2

August, the Ohio Police & Fire Pension Fund approved a 5% allocation to gold in order to

diversify and hedge against inflation.

All of this clearly points to generalist investors cluing into the risks of inflation, and the need for

gold for protection. In my view, gold’s just in a period of digesting its strong gains from the first

half of last year. Its future remains bright.

______________________________________

Buying Physical Gold

I’ve been receiving several inquiries lately about what physical gold makes sense to buy. As I

said in the first issue of Gold Resource Investor, bullion-backed ETFs are great, but they’re not

a replacement for physical gold. We have the Sprott Gold ETF (TSX:PHYS: NYSE:PHYS) in

the portfolio, but this is essentially a proxy for gold.

Sidenote: If you really want to buy physical gold, but it’s either not in stock or the

premiums are too high (like right now), then here’s a technique you can use. Decide on

the amount you are prepared to allocate to gold bullion, and buy that amount of a

physically backed gold ETF, like PHYS, then wait. When the items you want are back in

stock and the premiums have returned to normal, then you can sell your ETF holdings,

and use that cash to purchase physical bullion instead.

What’s more, PHYS sometimes trades above its net asset value (NAV), and sometimes below.

It’s like you’re buying gold either at a premium or a discount to its current price. You can track

the current premium or discount here: https://www.sprott.com/investment-strategies/physical-

bullion-trusts/gold-and-silver/net-asset-value-premium-discount/#. Obviously, the ideal is to buy

at a discount which, as I write, is about -4%, and to sell at a premium.

There’s a long list of reasons physical gold beats out other investments, and even other forms of

gold ownership.

Here are just a few…

1. Gold is indestructible. It won’t rust, corrode or decompose. Gold jewelry and coins

made thousands of years ago are found regularly by archaeologists and treasure

hunters. Some is even found by accident, like when farmers turn over their land. In

short, unless you lose or sell it, your gold is not going anywhere.

2. Gold has no counterparty risk. Unlike a bond, stock, or even cash, you don’t depend on

someone else to honor it. There’s no chance of a default.

3. Gold is a store of value. That’s because it has intrinsic worth. And since there’s plenty

of work required to find and extract gold from the earth, it will always have value.

4. Gold is privacy. A few ounces stored safely gives you direct control over a valuable

asset.

5. Gold is liquid. You can sell your gold almost anywhere, anytime. It has, countless

times, been a life saver for displaced people.

6. Gold can’t be hacked. It’s not just digits in a database somewhere for you to depend on.

3

7. Gold retains its value. Of course over time that will fluctuate. But over years and

decades, and especially compared to fiat money, gold always wins out.

First a word on bullion versus collectible coins (numismatics). Collectibles are almost another

world onto itself. They are a whole other market often with sizeable premiums to the gold

content because of rarity/collectability. So buyers pay a lot more money beyond the value of the

gold. That’s not to say it isn’t worthwhile, only that it takes a lot of knowledge and experience to

do right. Investors need to be extremely well-versed in this market, and need to be wary of

collectible sellers. They may try to “push” a collectible coin over a bullion coin because it’s good

for them. Buyer beware. Just make sure you know exactly how much gold is in the coin you’re

buying, and compare that to the spot price of gold, to ensure you’re getting as much gold as you

can for the amount you’re spending.

What to Buy

Gold bars or wafers (smaller, thin bars) are great to get the closest value to the gold content

without overpaying. But there are two main disadvantages versus coins. Bars from some

refiners are very simple, and so may be easier targets for counterfeiting. Bars produced by

government mints are more difficult to counterfeit, but they are not as well recognized as

government mint coins. Either way, if you do buy bars, I suggest they be from the most

recognized gold refiners. A quick internet search will find those for you.

Therefore, hands down, you’ll want government-mint produced bullion coins as a first

choice.

That’s because they’re instantly recognizable, often almost anywhere in the world. They’re also

standard in size and gold purity. And in many cases, essentially the same coin has been

produced for decades on end.

Here are my three favorite gold coins.

1. The one-ounce Canadian Maple Leaf coin. In 1982, the Royal Canadian Mint was the

first refinery to produce 9999 fine gold bullion coins. That means they are 99.99% pure

gold with a maple leaf on one side and Queen Elizabeth II on the reverse. Over 25

million of these coins have been sold since 1979, making the Canadian Maple Leaf one-

ounce gold coin one of the most popular, especially in North America. (In 1999, for the

25th anniversary of the Gold Maple Leaf, the mint went a huge step further, producing

99999 fine gold bullion coins which are 99.999% pure gold).

42. The American Eagle one-ounce gold coin. It’s produced by the U.S. Mint and issued

in limited quantities every year. It has Lady Liberty on one side and bald eagles on the

obverse. Between 1986 and 1991 it had roman numerals, then in 1992 the Mint began

using Arabic numerals. It contains one troy ounce of pure gold, but is 22 karat, since it

also contains 3% silver and 5.33% copper for durability. Right now, premiums are about

8-14%, which is double to triple the normal level. One-ounce Gold Eagles are a favorite

of U.S. investors. That makes for a large market which offers great liquidity.

3. The South African Krugerrand one-ounce gold coin. Rounding out my top three is

the Krugerrand. Like the American Eagle, the Krugerrand is also 22 karat, alloyed with

8.33% copper for durability, giving the coin a rose-tinted hue. Available since 1967, the

Krugerrand is the oldest circulating bullion coin in modern history. At one time, it was

the only bullion coin available in the market. Produced by the South African Mint, one

side displays a springbok antelope, and the obverse has an image of Paul Kruger, the

President of the historical South African Republic.

There you have them, three of the most popular gold coins available today.

Depending on where you live, you may have a predisposition towards a particular one of these

coins and that’s just fine, because they’re all great. They each enjoy wide circulation and global

recognition.

5Where to buy

There are several well-known precious metals dealers in Canada and the U.S. Note: the

following names are not recommendations or endorsements. They are simply bullion

dealers I know have been around for a long time, and about whom I’ve typically heard

positive comments. I strongly suggest doing your own due diligence to get feedback on

customer satisfaction, reliability, etc. Also, be sure to compare prices! Premiums often vary

considerably from dealer to dealer.

In Canada

Kitco: https://www.kitco.com/

Sprott Money: https://www.sprottmoney.com/

Border Gold: https://www.bordergold.com/

SilverGold Bull: https://silvergoldbull.ca/

In the United States

Kitco: https://www.kitco.com/

GoldSilver.com: https://goldsilver.com/

Investment Rarities: https://www.investmentrarities.com/

Apmex: https://www.apmex.com/

Miles Franklin: https://www.milesfranklin.com/

I know many of you are located in Europe or beyond. While I’m not familiar with bullion dealers

elsewhere, you should have no difficulty finding reputable ones closer to where you live. Keep

in mind that most will ship your gold, with insurance protection, over long distances. As always,

do your own detailed research before buying.

______________________________________

Commodity Comeback

Odds are very good that we are at the dawn of a new commodities supercycle. As you know,

commodities are the raw “stuff” we use to make things. That includes everything from precious

like gold and silver, to base metals like copper, nickel, zinc and lead. It also includes energy

staples, like oil, gas and uranium. And beyond that, “soft commodities” are things like corn,

wheat, coffee and soya, to name just a few.

One of the best ways to know where a sector stands in the bigger picture is to compare it to

other assets. And looking back over longer periods of time often provides great perspective.

That’s why I absolutely love this chart.

6It’s the ratio between the Goldman Sachs Commodity Index and the S&P 500. Looking back all

the way to 1972, commodities have never been cheaper relative to the broad stock market.

Never. The average of this ratio is 3.9 over 50 years. Today, it sits near 0.5.

So for commodities just to make it back to their average levels versus stocks, they will need to

rise almost 700%. And remember, that’s the overall index, and it’s the underlying commodities.

Needless to say, some commodities will outperform others. But the companies involved in

producing those commodities will do even better as their profits leverage rising revenues

against relatively stable costs.

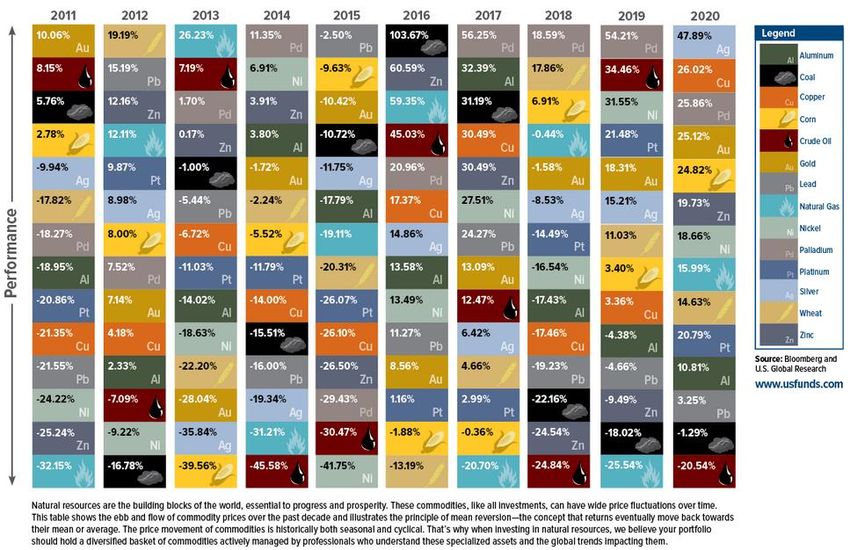

The following table lays out the annual performances of a number of commodities.

7As you can see, in 2020 nickel was up 19%, corn gained 25%, while palladium and copper both

gained 26%. In a recent 2021 Commodities Outlook: REVing up a structural bull market (Nov.

18, 2020), Goldman Sachs said, “Looking at the 2020s, we believe that similar structural forces

to those which drove commodities in the 2000s could be at play.”

A commodities supercycle is considered to be a multi-decade trend, where a wide range of

basic resources enjoy rising prices thanks to a structural shift in in demand versus supply.

Typically, what happens, is that supply stagnates or drops for several years as economic

demand is itself weak or constant. However, at one point a new business cycle starts, and

demand picks up, while supply is unable to immediately react. Producing most commodities is

a highly capital intensive endeavour. That means a lot of money to build and ramp up

production, not to mention the delays in finding, permitting, and building any new projects.

Typical delays can be in order of 10 years or more.

With supply unable to meet growing demand, prices rise. It’s Economics 101. So producers of

those commodities enjoy higher revenues, and higher profits as their costs remain fixed or rise

more slowly than the underlying commodity. And as profits expand, so do their share prices.

You have a solid trend for years or decades as supply struggles to catch up to demand. It’s a

secular bull market.

What’s sowing the seeds for a new commodities supercycle? The drivers are numerous, which

reinforces the probabilities. First we have a shift. In the above table, 12 of the 14 commodities

ranked showed gains last year. In 2019, it was just 9. In 2018, just the top 3 commodities eked

out a gain. Then we have all the usual suspects you’ve heard about: near zero interest rates

and bond-buying from central banks, massive government spending and deficits, ongoing

8printing to increase the money supply exponentially, stimulus cheques being given to the

majority of the population, huge infrastructure, green energy, and Covid-19 fighting and relief

spending. Oh, and possibly a new long term bear market in the U.S. dollar, in which

commodities are priced. Plus all the pent up demand from people unable to go out and spend

due to pandemic restrictions. I believe the large gains in base metals and energy over the past

year are the markets sensing that a flood of consumption is coming our way.

And Goldman Sachs is not alone. Bank of America has also forecast a surge in commodity

prices as a result of post-pandemic global economic recovery. JPMorgan said in a recent note

that metal, energy and agricultural prices are reaching multi-year highs, signaling a commodity

supercycle that may last for several years. I agree. That’s why we have two uranium plays in

the portfolio, as well as Sandstorm which has royalties on base metals uranium, nickel and

copper. And it’ why one of my new picks this month has exposure to base metals and energy.

______________________________________

Gold Technicals

In my mid-month update, I explained that gold has been consolidating ever since it peaked at an

all-time high in August.

9The chart above appears to be forming a descending triangle pattern. These are considered

bearish, meaning one would expect gold to possibly break below support around $1,800.

What’s more, gold is trading below its 50-day and 200-day moving averages, which is also

bearish. However, the action which started the triangle back in August was a bullish trend.

Also, the RSI and MACD momentum indicators are both showing positive divergence, meaning

they are in a bullish (upward) trend, while gold has trended downwards. And so I’m waiting to

see, and hopeful that gold will hold more or less near $1,800. That price will be crucial to watch

for new action. It may even test $1,750 to wash out the weak holders before resuming a

renewed trend higher.

Meanwhile, the main headwind appears to be the US dollar.

In fact, I said this in the mid-month update, and I think it can still be a near-term threat. It’s been

rising since the start of 2021, both the RSI and MACD momentum indicators are confirming this

trend, and it’s certainly not overbought. So it could have legs for awhile still. But keep in mind

that gold can, and has in the past, done well even with the dollar rising. It’s just more difficult.

Gold stocks have behaved in a similar way.

10GDX (a large gold miner ETF) is below its 50-day and 200-day moving average, while the

momentum indicators are both showing positive divergence. GDX has strong support near $34,

but could drop to $30 before resuming a new uptrend.

______________________________________

Gold Resource Investor Buys

Altius Minerals Corp.

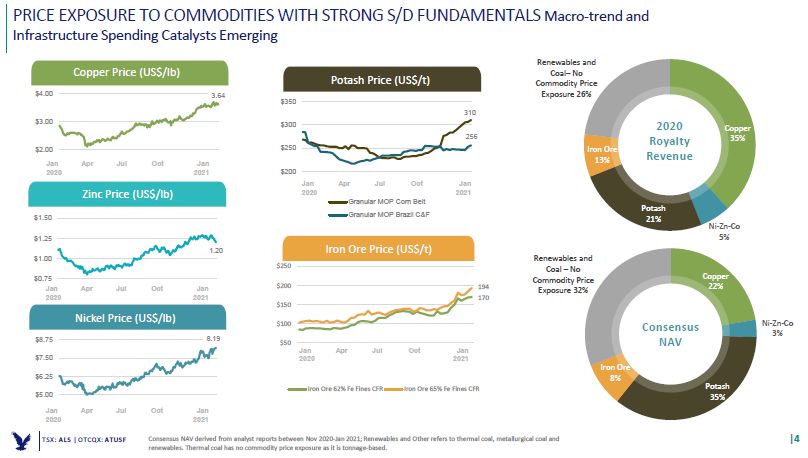

Altius Minerals Corp. (TSX:ALS; OTC:ATUSF) is a $650M market cap company that has

essentially two lines of business: generating and acquiring royalties on long life projects. In fact,

they typically focus on base metals, energy and potash, all of which I expect will do particularly

well over the next several years as I explained above in Commodity Comeback.

Here’s a little background on how Altius, which has been around for nearly 25 years, came into

existence. Company co-founder Brian Dalton, President and CEO, was a geology university

student when the Voisey’s Bay nickel deposit was discovered. It turned out o be one of the

most substantial mineral discoveries in Canada in the last 4 decades. And that struck a chord

with Dalton and his classmates, who realized the potential of value creation from prospecting

11and exploration. Eventually Altius was formed, and Dalton helped grow the company to an

asset base in excess of $500 million. He’s been diligently executing the company’s business

model of generating prospective projects and joint venturing them to others while retaining

royalties, as well as acquiring accretive royalties.

I spoke to Chad Wells, who’s part of the company’s executive team since 2001, and he

described the company’s roots to me. As he explained, Dalton wanted to create a company that

would be self-funded, rather that continuously go back to the market to sell shares and raise

money. And so Altius bought a portion of the Voisey’s Bay royalty for $10 million, which paid $1

million annually. That allowed them to operate and generate prospects they could joint venture

out. One of their earliest was a large uranium project which eventually became a massive $200

million windfall for Altius.

So in 2010-2011, they set out to build a list of their 20 favorite royalties globally, with a

preference for non-gold royalties as that space was already well-served. But that was the peak

of the last commodities cycle, and everything was pricey. So they were patient. It didn’t take

too long, because by 2013 the sector had sold off considerably. They called Sherritt

International, which owned their 3rd most desirable royalty. It was for sale, and they inked a deal

for 6 potash and 5 coal royalties which they split with Liberty Mutual of Boston. Eventually,

Liberty sold their half to Altius.

Then in 2015 they acquired a royalty on the polymetallic (copper, zinc, gold-silver) 777deposit in

Manitoba, operated by Hudbay Minerals. In 2016 they acquired a royalty on Lundin Mining’s

Chapada copper deposit in Brazil, which could become one of the most profitable copper mines

on the planet.

Today, Altius’s goal is to create growth through its diversified portfolio of royalties on projects

that are long life, high margin operations. They are also focused on sustainability-related

growth, by emphasizing renewable electricity generation, transportation electrification, reduced

emissions from steelmaking and increasing agricultural yield requirements. As a result, that’s

highly likely to bode well for shareholders, as Altius’s commodity exposures include copper,

renewable based electricity, several key battery metals (lithium, nickel and cobalt), clean iron

ore, and potash.

In fact, here’s a list of the company’s 14 royalties on producing assets throughout the Americas.

12Canadian royalties include a 4% NSR royalty on Hudbay's 777 copper-zinc mine in Manitoba, 6

potash mines and 5 coal mines located in western Canada, and a royalty on the Voisey's Bay

nickel-copper-cobalt mine in Labrador. In Brazil, they hold a 3.7% "stream" interest on Lundin

Mining's Chapada Mine. There is also a royalty on the Gunnison copper ISL mine in the USA.

The Company also receives regular dividend income from is equity ownership in Labrador Iron

Ore Royalty Company, which is treated as iron ore royalty revenue, being a pass-through

vehicle.

13Source: company presentation

In addition to this, over the years the company has built a sizeable portfolio interest in junior

resource companies, by receiving (in part) share payments for earn-ins on joint ventured

projects, as well as investing in top tier juniors. The benefit of this model has meant exposure to

several opportunities, while requiring little spending and generating new royalties at zero or

even negative costs. This year alone, Altius is exposed to the potential upside from an amazing

+178,000 meters of drilling, all done and funded by partners’ $150 million of capital raised.

The company aims to move away from coal, as legislation is increasingly forcing utilities to

generate power from cleaner sources. In fact, Altius is suing the provincial government of

Alberta, and the federal government, for a 2015 mandated coal fired shutdown by 2030. Their

argument is the government action is tantamount to expropriation, and cannot be done without

proper and fair compensation, as power generation and revenues to Altius were to extend all

the way to 2055.

It’s reinvesting the income from those projects into the renewable energy sector through a new

vehicle call Altius Renewable Royalties. This has allowed management to quickly scale its

investments. Today Altius has royalty interests in the project portfolios of two leading U.S. wind

and solar development companies, Tri Global Energy and APEX Clean Energy. The Tri Global

deal has seen Altius invest $55M, so that when Tri Global sells a project, Altius get a 3% gross-

revenue royalty on wind and 1.5% on solar. With APEX, Altius has a similar investment but for

$35M.

The company has decided that it can get the market to recognize the true value of its

renewables portfolio. Therefore, it recently announced it would “spin out” its Altius Renewable

Royalties Corp. (ARR) in an IPO. Management estimates the value of this business is about

$300M, whereas the market is only giving it about $80-$100M inside of Altius. Once spun out,

Altius will retain 2/3 of the new business, and expects it will have a market value of about

14$300M. I believe this could be a great catalyst for the share price, which could readily gain $2-

$3 once completed. The company has strong cash flow, which should be about $67.5M for

2020, which means the company is only being valued at 10x cash flow. They plan to pay down

a portion of debt, which is currently $141 million, while cash and public equity holdings are

valued at $136 million. Last year they bought back $6m in shares, and paid out $8M in

dividends, which produces a respectable dividend yield around 1.2% at the current price. This

is a compelling investment on several fronts. Altius is an exceedingly well-managed,

conservative company with considerable upside potential. Amazingly, the company has only 16

employees, 41.5 million shares outstanding, and boasts a market cap of $650M. I think Altius

could well generate a 40%-50% return over the next year as commodity prices rise, projects

continue to grow cash flows, and its portfolio of junior shares gains market value.

Strengths

• Highly experienced team with long track record of value creation

• Low risk royalty model with exposure to base metals, agriculture, renewable energy

• Pays growing dividend currently at 1.2%

• Big potential upside with junior shares portfolio through joint ventures, royalties

• Catalysts: Altius Renewable Royalties spin out, commodity price increases

Weaknesses

• Potential loss of income from early end to coal royalties

• Risk of US dollar strength could stall commodity prices near term

• Low daily trading volume

Alamos Gold Inc.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) is a $4 billion, mid-tier gold producer. Its production is

low cost, and likely to grow substantially over the next few years. The company should produce

about 500,000 ounces this year from two mines in Canada and one in Mexico. I like both

management and the company’s growth profile. Alamos has a significant portfolio of

development projects in Canada, Turkey, Mexico, and the U.S.

Alamos is aptly led by its President and CEO, John McCluskey. He co-founded Alamos back in

2003, built a successful gold miner, and is also a Director of the World Gold Council. Back in

2015, Alamos combined with AuRico Gold in what was a $1.5B deal, and that launched the

basis for the company we have today. In 2017 Alamos acquired Richmont Mines, which owned

the Island Gold Mine. That was a savvy move, as Island has turned to be a serious profit

machine. About 70% of production is Canadian and 30% Mexican. 2020 estimated output is

405,000-435,000 ounces at an all-in sustaining cost (AISC) of about $1,050. This year’s

production is forecast to grow by 17% to 470,000-510,000 ounces, while AISC is expected to

remain stable. The company will spend about $218M on high-return internal growth projects.

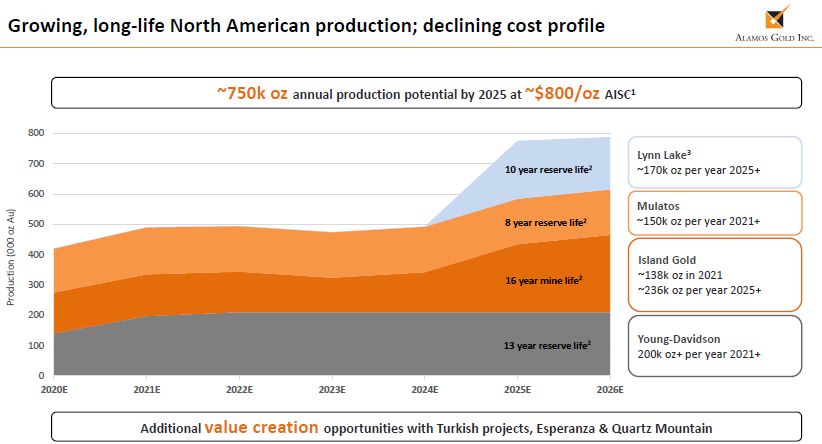

Let’s look at the producing mines.

Young-Davidson (Ontario) is one of Canada’s largest underground mines. It’s also the

company’s flagship. The mine transitioned to new larger infrastructure as it moves toward a

lower mine expansion, which is driving healthy free cash flow. Production should be up about

15200,000 ozs. this year at much lower costs. The mine has 11,000 acres of contiguous leases

and claims in Northern Ontario. It has a 13 year mine life based on 2019 reserves of 3.15M

ozs. There’s another 1.3M ozs. in resources, plus great exploration potential to extend the mine

life.

Island Gold (Ontario) is an underground gold-silver mine, which is the world’s sixth highest

grade gold mine, with reserves averaging 10.4 g/t gold. It should produce 130,000-145,000

ounces at an AISC of just $750-800/oz. A Phase III shaft expansion to 2000 tonnes per day

should be completed in 2025. Reserves are 1.2M ozs., and resources are another almost 2.5M

ozs. Alamos completed its acquisition of Trillium Mining in December for $25M, bringing a large

land package of 5,418 hectares adjacent to the Island Gold deposit. This means a 57%

increased land package with great exploration potential. Recent drilling demonstrated a high

probability the structure hosting the Island Gold Deposit extends onto the Trillium mineral

tenure.

Mulatos (Mexico) is located in the state of Sonora, and is an open-pit mine which started

producing back in 2005 and was the company’s founding operation. Despite producing well

over 2M ozs. since then, the mine still boasts reserves of 1.56M ozs., supplemented by another

2.9M ozs. in resources. Initial production at La Yaqui Grande project should start in Q3 2022,

and higher grades should help drive Mulatos costs significantly lower. Mulatos still boasts a

large underexplored land package comprised of 28,773 hectares of mineral concessions with

significant exploration potential. The operation has an eight year mine life based on current

Mineral Reserves, similar to the start of production in 2005, demonstrating a strong track record

of exploration success.

Source: company presentation

Beyond these three producing mines, all of which have good upside along with healthy mine

lives, Alamos has been pushing the boundaries with several other attractive development

16options. There are three in Turkey, Lynn Lake in Manitoba (Canada), Esperanza in Mexico, and

Quartz Mountain in the U.S.

Kirazli (Turkey) is one of the lowest cost undeveloped gold projects in the world. It’s projected

to produce 104K ozs. annually at an AISC of just $373, leaving huge margin for profit. Fully

permitted, Alamos began construction in 2019, but stopped activities pending renewal of mining

concessions which expired in October 2019. Concerns over the project’s risks to the

environment circulated on social media at the time, but the company has demonstrated its

environmental stewardship and operation within permit allowances. While all conditions have

been met for renewal of the concessions, the federal government and local communities remain

supportive. Agi-Dagi and Camyurt (Turkey) should both be profitable operations, but will only

be funded once Kirazli starts up and flows cash.

Lynn Lake is one of the highest-grade open-pit deposits in Canada. With great infrastructure

already in place, and permitting being advanced, a construction decision is expected in 2022.

Once built it will produce 170K ozs. annually at $745 AISC. Esperanza is undergoing

permitting, and with good infrastructure and low technical risk, it should produce over 100K ozs.

per year at low cost. Quartz Mountain was bought for $3.5M, and is at the advanced

exploration stage.

Alamos is a great addition to the portfolio, with low cost, safe production at low overall AISC of

about $1,050/oz. Management is conservative and disciplined, having resisted buying

overpriced projects at the peak of the last market cycle. As a result, they now enjoy being debt-

free, cash rich, and fully funded for organic growth. The company boasts a 300% increase in its

dividend since 2018. Its capital structure is healthy with 400m shares outstanding. While the

current P/E is high at 39.8, its forward P/E is just 15.94, and it’s undervalued relative to its

peers. I think Alamos could well deliver a double in its share price in the next year, especially if

gold makes a run for $2,300 in 2021 as I expect.

Strengths

• Catalysts are growth on the horizon at all 3 producing mines

• Big potential upside 50% growth by 2025 from existing & near-term producing projects

• Operations in safe jurisdictions

• Debt free & $174M cash

• Pays dividend

Weaknesses

• Turkey could offer geopolitical risk, bringing higher uncertainty to Kirazli, Agi-Dagi and

Camyurt projects, though mostly priced in already

• Almost exclusively gold production; no significant revenues from other metals

______________________________________

Gold Resource Portfolio

17• Most gold holdings are looking oversold right now, which makes them attractive to

accumulate on weak days.

• Silver holdings look more fully valued, but also attractive to accumulate on weak days

• Uranium holdings may be overbought in the near term

Company Stock Symbol Bought Price Current Change

Managed Investments ETFs holding gold miners, provides instant diversification

TSX:PHYS

NYSE:PHYS 11-Jan-21 $18.57 $18.35 -1%

Sprott Gold ETF

Simple way to gain exposure to gold prices, but not a replacement for owning

physical gold.

NYSE:SGDM 8-Sep-18 $15.23 $28.76 89%

Sprott Gold Miners ETF

Great option for investors seeking exposure to large gold miners without having

to select stocks

NYSE:SGDJ 8-Sep-18 $23.53 $46.50 98%

Sprott Jr. Gold Miners ETF

Great option for investors seeking exposure to mid-tier silver miners without

having to select stocks

Royalty & Streaming Lower risk: finance projects and collect royalties/streams

TSX:SSL

22-Jan-19 $6.04 $8.27 37%

NYSE:SAND

Sandstorm Gold

Focus on near-term production means portfolio is ramping up significantly over

next few years. Great leverage to gold

TSX:MMX

31-Dec-19 $6.61 $6.72 2%

NYSE: MMX

Maverix Metals Premier emerging gold royalty company, with small dividend. Aggressive

growth

focus gives potential for scale-related re-rating during this bull market.

TSX:ALS

12-Feb-21 $15.79 $15.79 0%

OTC:ATUSF

Altius Minerals

Exposure to several non-gold commodities. Well-managed, shareholder-

friendly, attractive yield, low-risk royalties, expanding into renewable energy

Low risk: Multiple producing projects across several

Large Leverage Producers

jurisdictions

TSX:ABX

1-Jun-20 $33.11 $28.12 -15%

NYSE:GOLD

Barrick Gold

Largest gold miner in the world --> go-to Buy for generalist dollars wanting

gold exposure. Will perform thru gold market. Dividend.

TSX:K

14-Jul-18 $4.94 $9.35 89%

NYSE:KGC

Kinross Gold

Strong balance sheet, controlled costs, respected name that will attract

generalist investors. And undervalued!!

Growing Producers Medium risk: Producing or Near-Production assets

18TSX:EQX

13-Oct-18 $5.00 $12.23 145%

NYSE:EQX

Equinox Gold

One of the strongest growth profiles in the gold sector. Likely to keep dealing

for additional assets.

TSX:SSRM

18-Nov-18 $14.72 $21.00 43%

Nasdaq:SSRM

SSR Mining

Reliable producer: lots of cash, options for organic growth, controlled costs,

and good dividend.

TSX:CXB

3-Nov-20 $2.10 $1.81 -14%

OTCQX:CXBMF

Calibre Mining Still-new producer with top tier management giving new life to mines & projects

in Nicaragua. Major geologic potential, production ramping up by 50% in 2021,

company still undervalued on most metrics

TSX:KNT

3-Nov-20 $7.25 $7.46 3%

OTCQX:KNTNF

K92 Mining Production ramping up with Stage 2 expansion complete at uber high grade

mine. Drills turning on multiple targets, from high-grade veins beside the mine

to strong porphyry targets.

TSX:AGI

12-Feb-21 $10.36 $10.36 0%

NYSE:AGI

Alamos Gold

Strong growth profile in the gold sector. Controlled costs and healthy balance

sheet.

Developers Advancing project(s) towards production

TSX:TLG

13-Jan-21 $1.18 $1.07 -9%

OTC:CHXMF

Troilus Gold

Medium to higher risk. Experienced team advancing large, quality project

towards production

Optionality Plays Medium to high risk: Advancing & de-risking projects for sale or JV

TSX:SEA

13-Jan-21 $25.84 $23.54 -9%

NYSE:SA

Seabridge Gold

Medium to higher risk. Experienced team de-risking multiple very large, trophy

projects towards joint venture or sale

Low risk: Multiple producing projects across several

Silver

jurisdictions

TSX:PAAS

30-Sep-19 $20.75 $33.33 61%

NYSE:PAAS

Pan American Silver

Largest public silver miner, with largest silver reserves globally. Low cost

producer, with significant silver revenues

TSX:MAG

21-Jun-17 $16.83 $24.26 44%

NYSE:MAG

MAG Silver

Owns 44% of large high-grade silver deposit. Transitioning to producer, very

robust, long-life project with big upside potential to expand resource

Base Metals

19TSX:CCO

NYSE:CCJ 26-Mar-19 $15.97 $20.02 25%

Cameco

Cameco is largest public uranium company. Ideal stock to own for U exposure

TSX:NXE

NYSE:NXE 2-Dec-15 $0.64 $5.07 692%

NexGen Energy

Pushing the best uranium discovery in decades towards production just as the

Uranium bull market gets started.

• Note: I’m a long-term shareholder in Alamos Gold.

• The price for Seabridge Gold was inadvertently indicated in US dollars in the January

Issue. It will be shown in Canadian dollars going forward

______________________________________

Gold Resource Updates

Sandstorm Gold (TSX:SSL; NYSE:SAND)

Sandstorm just announced Q4 and full year results. Q4 brought record cash flows of $22.5M

and net income at $10.5M. For the full year 2020, it had another record year of revenues and

cash flow, and this despite Covid-19 shutdowns. Attributable gold equivalent ounces sold were

52,176, record revenues at $93M (vs. $89.4M in 2019), record operating margins of $1,514/oz.

(vs. $1,115/oz. in 2019), record cash flows of $68.3M (vs. $60.7M in 2019), and net income of

$13.8M (vs. $16.4M in 2019). Management is forecasting between 52,000 and 62,000 gold

ounces this year, and 125,000 gold equivalent production by 2024. Solid results for a company,

still not being valued by the market. Sandstorm looks cheap.

Barrick Gold (TSX:ABX; NYSE:GOLD)

Barrick’s Tongon gold mine in Cote d’Ivoire produced 284,863 ounces of gold in 2020, at the top

end of its guidance for the year. Strong throughput with cost-reduction initiatives should mean

lower costs than in 2019. The Loulo-Gounkoto mine complex produced an impressive 680,215

ounces of gold in 2020, exceeding its full year guidance despite Covid-19 and other challenges,

all while improving its safety performance. Barrick is well off its 2020 highs, and with a P/E of

just 16.5 is looking oversold.

Kinross Gold (TSX:K; NYSE:KGC)

Kinross reported a reserves increase of 5.7M ozs, up 23% over 2019 to 30M ozs. This helped

the Kupol and Paracatu mines extend their mine lives by 1 year and the Chirano by 3 years. In

2021, Kinross expects to ramp up its global exploration program with a focus in Russia and

Chirano, and will continue to prioritize opportunities within the footprint of existing mines in its

global portfolio for mineral resource and reserve additions. The company met guidance for a

ninth year in a row and delivered record free cash flow of more than $1 billion. Its production is

expected to grow by 20% in 2023. Production for 2020 was 2,366,648M ozs, at an all-in

20sustaining cost of just $1,013. Cash position is $1.2B. It’s exceedingly cheap right now,

offering a dividend of 1.63% and a P/E of just 8.82.

Equinox Gold (TSX:EQX; NYSE:EQX)

Equinox provided guidance that it would produce 600,000 – 665,000 gold ounces, up 33% over

2020’s output of 477,200 ounces. All-in sustaining costs should be $1,190 - $1,275. The

company will prioritize investments this year that should help establish lower-cost production,

longer min-life mines and strong near-term production growth to about 900,000 and significantly

lower costs in 2022 and about 1M ozs. of gold in 2023. They aim to complete the acquisition of

Premier Gold Mines in Q1, and integrate the producing Mercedes Mine and and construction-

ready, multi-million-ounce Hardrock project into their portfolio and plans. EQX’s share of

production from Hardrock would further reduce costs per ounce produced and boost production

by more than 200,000 ounces annually starting in 2024. Equinox is pricier than some peers on

a price/production ounce basis, but the market is looking forward at its superb growth profile.

EQX has become oversold as gold’s sold off.

Troilus Gold (TSX:TLG; OTC:CHXMF)

Troilus recently reported new drilling assay from its Troilus Gold Project (Quebec,Canada).

Highlights include new higher grade zones that extend know mineralization at least 100m below

the PEA (Preliminary Economic Assessment) pit with 1.2g/t gold equivalent over 16m, 6.66 g/t

gold eq. over 3m. And a new high-grade zone outlined within 50 metres of surface within the

PEA pit in a step-out hole intersected 1.44 g/t gold eq. over 6 m, and several high-grade

intersections within broader intervals, located over 100 metres below the pit wall proposed in the

PEA, with a hole intersecting 20.42 g/t gold eq. over 1m. These are all in the Southwest Zone,

located 2.5 km from the main mineral resource, which already has a resource of about 580,000

ozs. gold eq. Troilus has sold off with the sector and is also looking oversold.

Cameco Corp. (CCO:EQX; NYSE:CCJ)

Cameco reported its Q4 and full year 2020 results. Q4 net earnings were $80M, and they had

an annual net loss of $53M. Covid limited production to 5M lbs. uranium, so they purchased

11.5M lbs. more than forecast at an average $40.41/lb. to manage risk, and incurred $55M

more in care and maintenance costs than planned. Cigar Lake production remains suspended,

while restart remains dependent on the ability to maintain safe operations, so 2021 production is

uncertain. $8M to $10M monthly care and maintenance will be ongoing at Cigar Lake. Long

term contract portfolio continued to grow, as more utilities migrate to that end. $400M of 3.75%

debt due in 2022 was replace with 2.95% debt due in 2027. At year end the company had

$943M in cash and short term investments, and $1B in long term debt, and $1B in undrawn

credit facility. CCO shares have recently broken out to 2-year highs as the market absorbs the

reality of uranium being part of a greener future. I think it’s still relatively cheap at current levels.

______________________________________

EDITORIAL POLICY AND COPYRIGHT: Companies are selected based solely on merit; fees are not

paid. This document is protected by copyright laws and may not be reproduced in any form for other than

personal use without prior written consent from the publisher.

21DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell

or solicit any offer to buy any security. The information presented on this website is subject to change

without notice, and neither Resource Maven (Maven) nor its affiliates assume any responsibility to update

this information. Maven is not registered as a securities broker-dealer or an investment adviser in any

jurisdiction. Additionally, it is not intended to be a complete description of the securities, markets, or

developments referred to in the material. Maven cannot and does not assess, verify or guarantee the

adequacy, accuracy or completeness of any information, the suitability or profitability of any particular

investment, or the potential value of any investment or informational source. Additionally, Maven in no

way warrants the solvency, financial condition, or investment advisability of any of the securities

mentioned. Furthermore, Maven accepts no liability whatsoever for any direct or consequential loss

arising from any use of our product, website, or other content.

The reader bears responsibility for his/her own investment research and decisions and should seek the

advice of a qualified investment advisor and investigate and fully understand any and all risks before

investing. Information and statistical data contained in this website were obtained or derived from sources

believed to be reliable. However, Maven does not represent that any such information, opinion or

statistical data is accurate or complete and should not be relied upon as such. This publication may

provide addresses of, or contain hyperlinks to, Internet websites. Maven has not reviewed the Internet

website of any third party and takes no responsibility for the contents thereof. Each such address or

hyperlink is provided solely for the convenience and information of this website's users, and the content of

linked third-party websites is not in any way incorporated into this website. Those who choose to access

such third-party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or

their affiliates may own securities of or may have participated in the financings of some or all of the

companies mentioned in this publication.

22You can also read