Global Capital Markets Outlook - Finding Sea Legs in the Storm - AllianceBernstein

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Capital

Markets Outlook

Finding Sea Legs in the

Storm

Second Quarter 2022

The information herein reflects prevailing market conditions and our judgments, which are subject to change, as of the date of this document. In preparing this document, we have relied upon and

assumed, without independent verification, the accuracy and completeness of all information available from public sources. Opinions and estimates may be changed without notice and involve a number

of assumptions that may not prove valid. There is no guarantee that any forecasts or opinions in this material will be realized. Information should not be construed as investment advice.1Q 2022 Returns Recap

Returns in US Dollars

1Q:2022 One-Year 24 Mar 2020–31 Mar 2022

Returns (Percent) Returns (Percent) Returns (Percent)

World –5.2 10.1 96.4

US –4.6 15.7 109.0

Equities Europe –7.4 3.5 74.8

Japan –6.6 –6.5 48.3

Emerging-Market –7.0 –11.4 57.3

Global High-Yield –5.7 –3.8 29.3

Credit Emerging-Market Debt –10.0 –7.4 14.6

Global Corporate –6.8 –4.4 8.7

Government US –5.6 –3.7 –7.6

Bonds

Japan –7.0 –10.5 –10.6

Euro-Area –5.0 –5.6 –2.4

Alternatives Commodities 25.6 49.3 101.1

Assets Global REITs* –3.6 20.0 100.2

Long/Short Equity –2.8 4.2 42.7

Alternative Relative Value 0.5 4.3 24.7

Strategies† Event-Driven –1.2 3.3 42.6

Macro 7.7 24.3

11.4

Past performance does not guarantee future results.

Global high yield, global corporates, and Japan and euro-area government bonds in hedged USD terms. All other non-US returns in unhedged USD terms. Emerging-market debt

returns are for dollar-denominated bonds as represented by the J.P. Morgan Emerging Markets Bond Index Global Diversified. An investor cannot invest directly in an index, and its

performance does not reflect the performance of any AllianceBernstein (AB) portfolio. The unmanaged index does not reflect the fees and expenses associated with the active

management of a portfolio.

*Real estate investment trusts. †Returns reflect HFRI index returns (see Index Definitions in the Appendix).

As of 31 March 2022; Relative Value, Event-Driven, and Macro returns for the third column are from 1 April 2020 to 31 March 2022

Source: Bloomberg Barclays, Hedge Fund Research, J.P. Morgan, Morningstar, MSCI, Standard & Poor’s (S&P) Dow Jones and AB

Global Capital Markets Outlook 2A Tale of Two Halves: S&P Prices First Reflected Aggressive Central Banks

and Then Added Global Conflict

Repricing meets geopolitical conflict and the impact of accelerating sanctions

Repricing: Inflation, the Fed and Rates Russian Invasion Economic Sanctions Ramp Up

4,900

All-Time High

4,800

Dec FOMC Meeting Minutes

Istanbul Peace Talks Fail

4,700

Meta 4Q Jan CPI

Dec Earnings Report Start of Istanbul

4,600 Payrolls Peace Talks

“Imminent Russian

Dec CPI Threat” Significant Ruble

Report Jan FOMC 2/10

4,500 Depreciation

Meeting Increased Inverts

Fighting by

4,400 Separatists WTI Oil

Breaks $100/bbl Russia Says It Will

Reduce Operations

4,300 Near Kiev

First Economic Fed Raises Rates 25 b.p.

4,200 Sanctions Issued US Oil

Embargo

Russia Invades Ukraine Rumored Feb CPI Report

4,100

1/3 1/7 1/11 1/15 1/19 1/23 1/27 1/31 2/4 2/8 2/12 2/16 2/20 2/24 2/28 3/4 3/8 3/12 3/16 3/20 3/24 3/28

Historical analysis and current forecasts do not guarantee future results.

b.p.; basis points; FOMC: Federal Open Market Committee

Through 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 3Inflationary Pressures Piling On

Pandemic Reopening Drivers Geopolitical Drivers

• Strong labor market boosting household income • Rising commodity prices due to the invasion of Ukraine

• Accumulated savings from past fiscal support • Potential supply shortages for commodities in Europe

• Robust demand for goods associated with lifestyle transitions • China’s zero-COVID policy and renewed lockdowns

• Supply-chain disruptions globally • Politicians facing pressure to ease the stress on households

• Transportation bottlenecks domestically

• Rising wages for service industries

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 4Geopolitics Push Inflation Risks to the Upside…

Balance of Risks Pushing Out the Inflation Normalization Timeline

Inflation AB global inflation forecasts (percent)

5.5

The upside risk has become the base case for inflation:

persistent inflation raises elevated risks that expectations 5.0

drift, and rising commodity prices hit consumers directly 4.5

and immediately 2022

4.0

50% 50% 3.5

45%

40% 3.0

2021 2023

2.5

2.0

10% Fed’s Target Inflation Rate

5% 1.5

1.0

Downside Central Upside Apr Aug Dec Apr Aug Dec Apr

20 20 20 21 21 21 22

Mar Apr

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 5…Driving More Aggressive Rate Expectations

Upper Bounds of Federal Funds Rate (FFR) Through Time Fed and Market Expectations (Percent)

Percent

2021 2022 2023 2024 Longer Run 7

3.75 — — ●● ●● — Expected Expected

FFR (Market) FFR (Fed)

3.50 — — ● ●● — 6

YE 22 2.5% 1.9%

3.25 — ● ●● ● — YE 23 3.2% 2.8%

YE 24 N/A 2.8%

3.00 — — ●●● ●●● ●● 5

LR N/A 2.4%

2.75 — ● ●●● ●● —

2.50 — ●●● ●●●● ●●● ●●●●●● 4

2.25 — ●● ● ●●● ●●●●●●

Market Implied FFR

2.00 — ●●●●● — — ● 3

1.75 — ●●● — — — YE YE

1.50 — ● — — — 2 23 24 LR

1.25 — — — — — YE

22

1.00 — — — — — 1

0.75 — — — — — Median Fed

Dot Plot

●●●●●●●●●●● 0

0.00 — — — —

●●●●●●● 06 08 10 12 14 16 18 20 22 24 LR

Historical analysis and current forecasts do not guarantee future results.

YE: year-end; LR: longer run

As of 11 April 2022

Source: Bloomberg, US Federal Reserve and AB

Global Capital Markets Outlook 6The Market Started “Tightening” Months Ago

Two-Year Treasury (Percent) Goldman Sachs Financial Conditions Index

2.5 102

Two-Year

Treasury Yield 101

2.0

30 Sep 2021 0.27%

31 Dec 2021 0.73% 100

1.5 28 Feb 2022 1.43%

31 Mar 2022 2.33% 99

1.0

98

0.5

97

0.0 96

Oct Dec Feb Apr Jun Aug Oct Dec Feb Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr

20 20 21 21 21 21 21 21 22 20 20 20 20 21 21 21 21 22 22

Historical analysis and current forecasts do not guarantee future results.

Through 7 April 2022

Source: Bloomberg, Goldman Sachs and AB

Global Capital Markets Outlook 7Compounded Inflationary Pressures Reduce Growth Expectations

Balance of Risks: Growth Growth Impact from Rising Rates Growth Impact from Russia

• Increased incentive to save • Higher commodity prices reduce

55%55% demand more broadly

• Higher discount rate for business

investment • Geopolitics can hurt consumer

confidence

40% 40%

• Cost of capital rising

• Friction between economies with

• Financial market stress reducing wealth different vulnerabilities

• Fears of recession can become self- • Business investment in Europe

fulfilling

• Long-term energy investment

uncertainty

5% 5%

Downside Central Upside

Mar Apr

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 8Rising Energy Prices Disproportionately Hitting Europe

Monthly Average (1 January 2019 = 100)

700

European Natural Gas

600

500

400

300

Crude Oil

200

Retail Gasoline (US)

100

US Natural Gas

0

Jan 19 May 19 Sep 19 Jan 20 May 20 Sep 20 Jan 21 May 21 Sep 21 Jan 22

Historical analysis and current forecasts do not guarantee future results.

Through 31 March 2022

Source: Refinitiv and AB

Global Capital Markets Outlook 9Yield Curve as a Forecast: A Brief History

The Yield Curve Has Flattened Precipitously Timing Matters Too

Indexed to peak in yields

120 350

Recession US Treasury 10-

Year–Two-Year

300

100 Spread

250

80

200

Basis Points

60 150

2014–2019

40 100

1992–1998 50

20

0

0

2003–2006 –50

2021–Present

–20 –100

13

25

37

49

61

73

85

97

1

109

121

133

145

157

169

181

193

205

217

229

241

253

265

277

289

301

313

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Weeks into Cycle

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 10Yield Curve as a Forecast: Here’s Three More Ways to Look at It

Near-Term Forward Spread and Real Yields (Percent) ISM Manufacturing and Recessions

Recessions (Percent)

3.0 4 70

2.5 3 65

2007

2.0 2

60

1.5 1

2019 55

1.0 0

50

0.5 –1

45

0.0 –2

40

–0.5 –3

Current

–1.0 –4 35

–1.5 –5 30

97 99 01 03 05 07 09 11 13 15 17 19 21 1 2 3 4 5 6 7 8 9 10 85 88 91 94 97 00 03 06 09 12 15 18 21

Maturity

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 11Strong Consumer Supports Economic Backdrop

Real Wages Total Liquid Assets and the Long-Term Trend (USD Trillions)

Income outpacing inflation

16 16,000

Nominal Paycheck

14

14,000

12

Actual

10

12,000

Year over Year (Percent)

8

6 10,000

4

Trend

2 8,000

0

6,000

–2

–4

Real Paycheck 4,000

–6

–8 2,000

12 13 14 15 16 17 18 19 20 21 22 99 01 03 05 07 09 11 13 15 17 19 21

Historical analysis and current forecasts do not guarantee future results.

Through 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 12Macro Summary

Global growth to see meaningful slowdown in 2022

AB Global Economic Forecast: April 2022

Real Growth (Percent) Inflation (Percent) Official Rates (Percent) Long Rates (Percent)

22F 23F 22F 23F 22F 23F 22F 23F

Global 2.8 2.8 5.2 3.1 2.67 2.77 2.86 3.04

Industrial Countries 2.2 1.7 4.9 2.3 0.93 1.38 1.60 1.93

Emerging Countries 3.8 4.5 5.7 4.3 5.25 4.82 4.76 4.70

US 2.8 1.9 4.5 2.5 1.88 2.75 2.75 3.25

Euro Area 0.5 1.0 6.5 2.0 –0.50 –0.25 –0.10 0.00

UK 3.0 1.5 7.5 3.5 2.00 2.00 2.00 2.25

Japan 2.5 2.0 1.5 1.5 –0.10 0.25 0.25 0.50

China 5.3 5.4 1.9 2.3 2.00 2.00 3.00 3.10

Past performance and current analysis do not guarantee future results.

Growth and inflation forecasts are calendar-year averages. Interest rates are year-end forecasts. Real growth aggregates represent 48 country forecasts, not all of which are

shown. Long rates are 10-year yields.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 132022 Earnings Growth Expected to Moderate as Policy Supports Weaken

and Consumers Return to Pre-Pandemic Spending Habits

S&P 500’s Expected Bottom-Up Negative Guidance Rising Positive Guidance Falling

Earnings Set to Fall Before Slow

Growth

70 100 70

90

60 60

80

50 70 50

60

40 40

50

30 30

40

20 30 20

20

10 10

10

0 0 0

2Q: 3Q: 4Q: 1Q: 2Q: 3Q: 4Q: 1Q: 2Q: 3Q: 4Q: 4Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q: 3Q: 1Q:

20 20 20 21 21 21 21 22* 22* 22* 22* 23* 18 19 19 20 20 21 21 22 18 19 19 20 20 21 21 22

Historical analysis and current forecasts do not guarantee future results.

*FactSet estimate

As of 31 March 2022

Source: FactSet and AB

Global Capital Markets Outlook 14Valuations: Finding a “Fair Value” in a Tightening and More Uncertain

Market

S&P 500 Trailing and Forward P/Es

33

Time Period P/E P/FE1 P/FE2 P/FE3

31 March 2022 23.4 20.1 18.3 16.2

28

Five-Year Average 22.6 19.9 17.5 15.8

Pre-Pandemic* 21.9 19.3 17.3 15.5

23

10-Year Average 20.1 18.0 16.0 14.3

Average Since 2000 19.6 17.3 15.2 13.8

18

Pre-Pandemic Five-Year Average 19.5 17.6 15.8 14.2

Average P/E When FFR Is 0% 19.2 17.0 15.0 13.4

13

Average P/E When Rates Increasing† 19.2 17.1 15.4 14.2

January 2014–November 2016 18.5 17.0 15.3 13.6

8

10 11 12 13 14 15 16 17 18 19 20 21 22

Trailing 12 Months P/E CY 2022 P/E

CY 2023 P/E CY 2024 P/E

Historical analysis and current forecasts do not guarantee future results.

Price/earnings (P/E) is for the trailing 12 month; price/forward earnings (P/FE)1 is for the calendar year 2022; P/FE2 is for the calendar year 2023; P/FE3 is for the calendar year

2024.

*21 February 2020. †Last two Fed cycle hikes

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 15Scenario Chart: Choose Your Own Adventure

S&P 500 Return Scenario Chart

2022

15 16 17 18 19 20 21 22 23 S&P Price Level 2022 Price Return*

205 3,075 3,280 3,485 3,690 3,895 4,100 4,305 4,510 4,715 3,655 –19.3%

210 3,150 3,360 3,570 3,780 3,990 4,200 4,410 4,620 4,830 3,960 –12.6%

215 3,225 3,440 3,655 3,870 4,085 4,300 4,515 4,730 4,945 4,180 –7.7%

220 3,300 3,520 3,740 3,960 4,180 4,400 4,620 4,840 5,060 4,275 –5.6%

225 3,375 3,600 3,825 4,050 4,275 4,530 4,725 4,950 5,175 4,530 0.0%

230 3,450 3,680 3,910 4,140 4,370 4,600 4,830 5,060 5,290 4,620 2.0%

235 3,525 3,760 3,995 4,230 4,465 4,700 4,935 5,170 5,405 4,725 4.3%

240 3,600 3,840 4,080 4,320 4,560 4,800 5,040 5,280 5,520 4,830 6.6%

245 3,675 3,920 4,165 4,410 4,655 4,900 5,145 5,390 5,635 4,935 8.9%

2023

15 16 17 18 19 20 21 22 23 S&P Price Level 2023 Price Return†

230 3,450 3,680 3,910 4,140 4,370 4,600 4,830 5,060 5,290 3,840 –7.9%

235 3,525 3,760 3,995 4,230 4,465 4,700 4,935 5,170 5,405 4,000 –6.0%

240 3,600 3,840 4,080 4,320 4,560 4,800 5,040 5,280 5,520 4,250 –3.1%

245 3,675 3,920 4,165 4,410 4,655 4,900 5,145 5,390 5,635 4,335 –2.2%

250 3,750 4,000 4,250 4,530 4,750 5,000 5,250 5,500 5,750 4,530 0.0%

255 3,825 4,080 4,335 4,590 4,845 5,100 5,355 5,610 5,865 4,655 1.4%

260 3,900 4,160 4,420 4,680 4,940 5,200 5,460 5,720 5,980 4,845 3.4%

270 4,050 4,320 4,590 4,860 5,130 5,400 5,670 5,940 6,210 5,000 5.1%

275 4,125 4,400 4,675 4,950 5,225 5,500 5,775 6,050 6,325 5,200 7.1%

Historical analysis and current forecasts do not guarantee future results.

*Based on S&P 500’s closing price of 4,530. †Annualized return based on same closing price

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 16Equity

Global Capital Markets Outlook 17Systematic Repricing, but Opportunities Remain

Value and energy dominate; growth and quality underperform

1Q Returns Historical 4Q:21 1Q:22

(Percent) P/FE P/FE P/FE

Russell 1000 Value –0.7 14 17 16

S&P 500 –4.6 15 21 19

Index MSCI EAFE –5.8 13 15 14

Russell 2000 –7.5 21 25 22

Russell 1000 Growth –9.0 17 30 26

Value –1.5 13 16 15

Small Cap –5.9 20 20 18

Factor* Momentum –7.4 20 24 20

Quality –8.8 17 25 22

Growth –9.0 18 34 30

Energy 39.0 16 11 11

Utilities 4.8 15 21 21

Consumer Staples –1.0 17 22 21

Financials –1.5 13 15 14

Materials –2.4 15 17 16

Sector Industrials –2.4 15 21 20

Healthcare –2.6 15 18 17

Real Estate –6.3 39 51 45

Technology –8.4 16 28 24

Consumer Discretionary –9.0 17 30 26

Communication Services –11.9 14 20 17

Current analysis does not guarantee future results.

Historical P/FE is the average from 7 January 2005 to 21 February 2020

P/FE is the blended forward 12-months price/earnings ratio calculated by dividing the price of the security by Bloomberg Estimates (BEst) EPS

*MSCI USA Factor indices; 1Q returns are total return

As of 31 March 2022. Source: Bloomberg, FTSE Russell, MSCI and S&P

Global Capital Markets Outlook 18P/E Multiple Upside Remains Limited, and Look Beyond Mega-Caps

A case for being active

Tighter Financial Conditions Constrain P/Es Valuation Premium of 10 Largest Stocks by Market Cap

vs. Rest of S&P 500

23 95 Easing 70 80

S&P 500 P/E (Left Scale)

96

21 70

60

97

19 Premium (Right Scale)

60

98 50

P/E Ratio (×)

17

99 50

Index Level

P/E Ratio

Percent

40

15 100 10 Largest P/FE

40

101 30

13

30

102

11 Goldman Sachs 20

Financial 103 20

Conditions Index

9 10

104 10

The Rest P/FE Whole Index P/FE

7 105 Tightening

06 08 10 12 14 16 18 20 22 0 0

18 19 20 21 22

Historical analysis and current forecasts do not guarantee future results.

All data are for S&P 500

Left display through 31 March 2022; right display through 1 March 2022

Source: Bloomberg, Goldman Sachs, S&P and AB

Global Capital Markets Outlook 19Anatomy of an Inflation vs. an Economic Growth Scare

Radically different factor performance over distinct sell-offs

Lower Quality and Value Higher Quality and Growth

20

High–Low Quintile Performance

15

10

5

(Percent)

0

–5

–10

–15

–20

Low Price to Low P/E High Div High FCF High ROA High ROE Stable Sales Stable

Book Yield Yield Growth Earnings

Growth

Feb/Mar 2020 1Q 2022

Past performance does not guarantee future results.

Factor performance difference between highest ranked and lowest ranked quintiles. Low Price to Book Value, Low Price to Earnings, High Dividend Yield, High Free-Cash-Flow

Yield, High Return on Assets, High Return on Equity, Stable Sales Growth and Stable Earnings Growth

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 20Slower Economic and Earnings Growth Calls for a Quality Bias

Declines in New Orders Tend to Dampen Positive Earnings A Quality Checklist for the Current Environment

Revisions: This Has Been Taking Hold

90 75 Attributes Quality Value Profitable Growth

S&P 500 Company Positive

80 EPS Revisions—Up/Total, High/Stable Profits

70

IBES (Left Scale)

Strong Free Cash Flow

70

65

Positive Earnings Revisions

60

60

Percent

Pricing Power

50

55 Profitable Reinvestment

40

Innovation/Unique

50

30 Sustainable Themes

45

20 High-Valuation Growth

ISM New Orders

Mfg. Index 40 Higher-Cost Operators

10

High Levels of Debt

0 35

00 02 04 06 08 10 12 14 16 18 20 22

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: Bloomberg, Institutional Brokers’ Estimate System (IBES), Institute for Supply Management (ISM), Piper Sandler and AB

Global Capital Markets Outlook 21An Improved Entry Point for Growth Stocks

Focus on profitability and positive earnings revisions

Growth’s COVID-19 P/E Premium vs. Value Meaningfully High Return on Assets Stocks Are More Attractively Priced

Lower, and May Rise Further from Recent Lows and Those Having Positive EPS Revisions Remain Cheap

13

S&P 500 Growth Index P/E – S&P Expensive 80

500 Value Index P/E

12

11

10

Long-Term

Average = 8.6x

9 40

8

7 Growth Valuations Relative to

Value Reached 2019 Levels

6

5 0 1

Cheap

Sep 19

Sep 20

Sep 21

Jan 19

May 19

Jan 20

May 20

Jan 21

May 21

Jan 22

High ROA Positive EPS Revisons

4Q:21 1Q:22

Historical analysis and current forecasts do not guarantee future results.

As of 31 March 2022

Source: Bloomberg, Piper Sandler and AB

Global Capital Markets Outlook 22Opportunities Emerge in Quality Growth

Identifying disconnects between price and fundamentals

Healthcare Sector: Wide Industry …Select Industries Now Offer Attractive Global Robotic Surgical Procedures

Return Dispersion, but… Risk/Reward Are Growing

25 1,600

16.7

20 1,400

15 8.8

7.7

1,200

10

YTD Total Return

1,000

Thousands

05

00 800

–05 –6.0 600

–10 Healthcare

Sector Index –13.1 400

–15

200

–20

–21.8

–25 Healthcare Life Sciences Healthcare 0

–25 –05 15 Equipment Tools and Supplies 14 15 16 17 18 19 20 21

Services

2014–2021 Procedure Growth: 16%

EPS Growth YTD Total Return 2023 Earnings Growth

Past performance does not guarantee future results.

Based on consensus estimates.

Left and middle displays as of 31 March 2022; right display through 31 December 2021

Source: Bloomberg, S&P, Strategas Research Partners, company reports and AB

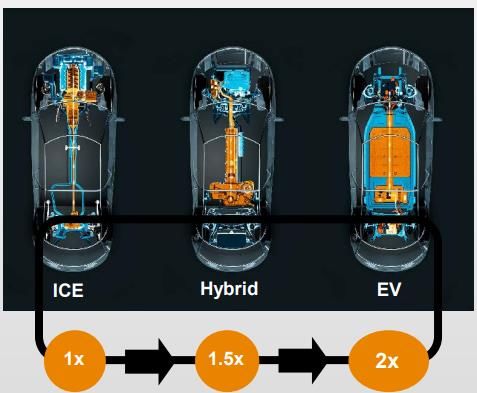

Global Capital Markets Outlook 23Continue to Emphasize Enduring Themes: A Focus on Electric Vehicles

Seek companies that provide the enabling technology or service (e.g., semiconductors)

Robust Production Rates for Electric Announced Battery-Electric Vehicles Semiconductor Content Increases ~2x

Vehicles (EV) (BEV) Sales Mix by Brand with a Full EV versus an ICE Vehicle

36 Manufacturer Target Date BEV Target

PHEV and EV Audi 2040 90%

Production 30

Expected to BMW 2030 50%

Grow at a 25%

Ford Europe 2030 100%

CAGR 22

General Motors 2035 100%

15 Hyundai Motor 2040 78%

Mercedes-Benz 2039 100%

9

Porsche 2030 80%

4

Volvo 2030 100%

VW Group

2030 50%

2020 2022E 2024E 2026E 2028E 2030E Worldwide

Historical analysis and current forecasts do not guarantee future results.

CAGR: compound annual growth rate; PHEV: plug-in hybrid vehicle; ICE: internal combustion engine

Left display as of 31 August 2021; middle display as of 22 April 2021; right display as of 31 December 2021

Source: IHS Markit, Infineon Technologies, TE Connectivity and AB

Global Capital Markets Outlook 24Value Stocks Can Continue to Advance, but Be Selective

High free-cash-flow stocks lagged; however, they remain inexpensive

Higher Yields: A Tailwind for Lower- High Free-Cash-Flow Yield Stocks Lost Deep Value Does Not Always Equal

Duration Value Stocks Ground to Lower-Quality Counterparts Good Value; Favor High Free Cash

Flow

6 1.0

16.0% Expensive

S&P 500 Pure Value/

S&P 500 Pure Growth

5 0.9

0.8

4

0.7

8.4%

Ratio

Yield

3

0.6

2 5.1%

0.5

16 14

1 10-Year Treasury 0.4 1.3% 8

(Left Scale) 5

0 0.3 Cheap

02 05 08 11 14 17 20 4Q:21 1Q:22 High Free- High Book

Cash-Flow Yield Value/Price

High FCF Yield High BV/Price 4Q:21 1Q:22

Past performance and historical analysis do not guarantee future results.

High free-cash-flow (FCF) yield: last 12 months cash flow from operations less than three-year average CAPEX to market cap; high book value/price: stockholder's equity minus

preferred stock divided by market cap

Left display through 31 March 2022; middle display as of 31 March 2022; right display as of 1 March 2022

Source: Bloomberg, FactSet, FTSE Russell, MSCI, S&P and AB

Global Capital Markets Outlook 25Areas of Focus for Value Equities

Consumer Discretionary Stocks Were The Breadth of the Sector Allows for Total Liquid Assets vs. Trend: A

Out of Favor Vast Stock Selection Opportunities Favorable Backdrop for Consumers

16

50 35.9

40

14

30 Actual

Consumer

12

YTD Total Return

20 Discretionary 12.1

10.4

Sector Index

10

10

Thousands

0

8

–10

–7.8

–20

6

–17.3

–30

–24.7 4

–40

Automotive Apparel, Auto Parts &

Retail Accessories & Equipment Trend

–50

Luxury Goods 2

–50 –25 0 25 50

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

EPS Growth YTD Total Return 2023 EPS Growth

Based on consensus estimates. Left display not shown are casinos and gaming, and hotels, resorts and cruise lines.

As of 31 March 2022

Source: Bloomberg, Refinitiv, S&P, Strategas Research Partners and AB

Global Capital Markets Outlook 26Timing the Market Means Getting Out and Getting Back In

Timing the market vs. time in the market

S&P 500 Rolling Three-Year Returns The Cost of Missing Out

Annualized (1988–2021) S&P 500 return in 2022 (percent)

11.0% 7.0

–4.6

4.0% 4.1%

–15.0

Average Miss Best Bonds* Jan–Mar 2022 Miss Best Miss Worst

Three-Year Return Five Days Return Five Days Five Days

Past performance is not necessarily indicative of future results. There is no guarantee that any estimates or forecasts will be realized.

*Bonds represented by annualized return of the Lipper Short/Intermediate Municipal Bond Fund Average from January 1988 through December 2021

Left display as of 31 December 2021; right display as of 31 March 2022

Source: Bloomberg, Lipper, S&P and AB

Global Capital Markets Outlook 27Fixed Income

Global Capital Markets Outlook 28Pace of Rising Yields Accelerated in March as Geopolitical Concerns Grew

Belly of the Curve Saw the Greatest Rise High-Yield YTW Surges on Back of Rising Rates and

Widening Spreads

3.5 700

Market Implied 2023 FFR

3.0 Fed and AB 2023 FFR Est. 600

31 Mar 2022

2.5 Market Implied 2022 FFR 500

325

Fed and AB

2.0 28 Feb 2022 400

Percent

2022 FFR Est.

1.5 300

283

31 Dec 289

2021

1.0 200

30 Sep 2021 276

0.5 100

115 138

0.0 0

1 2 3 6 1 2 3 5 7 10 20 30 30 Sep 2021 31 Dec 2021 31 Mar 2022

Mo. Mo. Mo. Mo. Yr. Yr. Yr. Yr. Yr. Yr. Yr. Yr.

Treasury Yield OAS

Historical analysis does not guarantee future results.

YTW: yield to worst

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 29Elevated Yields Suggest Attractive Forward Five-Year Returns…

Starting YTW vs. Forward Five-Year If You Invested During the…

Annualized Returns (Percent)

All-Time

0.25

YTW Wides

for HY

Spreads

0.20

22.0

21.2

Telecom

0.15 Bubble

Missed the

14.3 All-Time Post-GFC

Before

13.2 Tights for Rally

2008 Before the

HY

0.10 Sell-Off Taper

Spreads

9.3 9.3 Tantrum

6.7 6.8 7.3 7.7

6.1 6.1 6.5

0.05

Five-Year Forward Returns

0.00

06 08 10 12 14 16 18 20 22 Oct 02 Dec 04 May 07 Nov 08 Dec 09 Dec 12 Mar 22

YTW Five-Year Forward Returns

Past performance and historical analysis do not guarantee future results.

HY: high-yield; GFC: global financial crisis

Left display YTW and returns represent Bloomberg US Corporate High Yield; right display YTW and returns represent Bloomberg Global Corporate High Yield (USD Hedged).

As of 31 March 2022

Source: Bloomberg and AB

Global Capital Markets Outlook 30…and Offer an Opportunity to De-Risk Equities

Over time, high-yield bonds could generate equity-like returns with half the risk

Historical Returns and Volatility When HY Draws Down ~5%, Equities Draw Down More

July 1983–March 2022 (percent) Calendar year max. drawdown (percent)

0

14.9

–10

11.6

8.5 –20

8.3

–30

–40

–50

Annualized Return Annualized Volatility 1998 2000 2001 2002 2008 2011 2015 2018 2020 2022

US High Yield S&P 500 US High Yield S&P 500

Past performance and historical analysis do not guarantee future results. Individuals cannot invest directly in an index.

US high yield is represented by Bloomberg US Corporate High Yield.

As of 31 March 2022

Source: Bloomberg, S&P and AB

Global Capital Markets Outlook 31US High Yield Fundamentals Are Expected to Remain Robust

Net Leverage (Debt/EBITDA) Interest Coverage (EBITDA/Interest)

5.2 6.0

5.5

4.7 5.0

4.5

4.2

4.0

3.7 3.5

3.0

3.2 2.5

1Q:06 1Q:11 1Q:16 1Q:21 1Q:06 1Q:11 1Q:16 1Q:21

Net Income Margin (Percent) Default Rates (Percent)

8 12

6 9

4

6

2

0 3

–2 0

1Q:06 1Q:11 1Q:16 1Q:21 06 08 10 12 14 16 18 20 22

Historical and current analyses do not guarantee future results.

Ex financials. Data represent ~70% of ex financials US High Yield in market value. Metrics data are calculated using median.

As of 31 March 2022

Source: Morgan Stanley, S&P Compustat and AB

Global Capital Markets Outlook 32Taxable Overview: Relative Opportunities Exist

High Yield Investment Grade Securitized

Overview Overview CRTs (Credit Risk–Transfer Securities)

• High Yield can serve as a surrogate to • Uncertain macro backdrop gives cause for • Floating-rate securities should benefit from

equities concern, though strong corporate higher coupons as the Fed hikes

• Current yields are largely compensating fundamentals should assuage worries • Exposure to the strong housing market,

you for volatility rather than default risk. • Balanced technical backdrop and which benefits from strong technicals and

When volatility declines, the market will valuations limit spread compression fundamentals

rally • Recent macro volatility may impact

• HY does well in general when rates move corporate funding ambitions and reinforce Commercial Mortgage-Backed

higher, but there are often pockets of the balance sheet policy discipline, providing a Securities (CMBX.6)

market that perform very poorly in this near-term tailwind • Loss-adjusted yields point to expected

environment returns in mid-single digits to mid-teens

Positioning • CMBX.6 has been benefiting from the

• reopening of the US economy, which is

Positioning Favor the belly of the curve in the US

supportive of sectors like retail and lodging.

• Reducing more cyclical credits and adding positioning for carry-over compression; flat

Strong recent performance

more defensive credits credit curves in Europe warrant short

• Adding BBs in the new issue market, exposure

Collateralized Loan Obligations (CLOs)

reducing CCC exposure • Maintain risk in lower-quality credit;

• Having reduced energy exposure as • Very attractive spread pick up over similarly

selectivity is key amid expected dispersion

valuations are less compelling rated corporates

in outcomes • Strong fundamentals of the underlying

• BBB spreads offer further room for loans and strong structure

compression

Current analysis does not guarantee future results.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 33Yields Globally Have Risen Off Lows as Volatility Has Increased

10-Year Yield-to-Worst Range

October 2011–March 2022

13.89

11.86

11.50 11.36 11.46

9.72 10.21 10.98

9.44 9.13

8.73

6.81 7.24 6.90 6.68

6.01 6.28

5.37 5.78

5.59 5.29

4.04 4.21 4.51 4.45 4.11

3.88 3.68

3.75 2.70 3.07 2.66 2.35

2.19 2.44

US High Yield Pan-Euro Pan European EM USD EM LC EM USD Corp. + BBB IG

High Yield EMG HY High Yield Gov't HY Quasi-Sov CMBS

Max Min 30 September 2021 31 December 2021 31 March 2022

Past performance does not guarantee future results.

EMG: emerging; EM: emerging markets; USD: US dollar; LC: local currency; IG: investment-grade; CMBS: commercial mortgage-backed securities

Historical information provided for illustrative purposes only. US High Yield is represented by Bloomberg US High Yield Corporate Index; Pan-Euro High Yield by Bloomberg Pan-

European High Yield; Pan-European EMG HY by Bloomberg Pan European EMG High Yield; EM LC Gov’t HY by Bloomberg EM Local Currency Government High Yield; EM USD

Corp + Quasi-Sov by Bloomberg EM USD Corp + Quasi Sovereign High Yield; EM USD High Yield by Bloomberg EM USD Sovereign High Yield; BBB IG CMBS by Bloomberg

CMBS IG BBB Index.

As of 31 March 2022

Source: Bloomberg, Morningstar and AB

Global Capital Markets Outlook 34By the Numbers

A blended credit portfolio offers a better income-to-risk profile today

Hypothetical Portfolio Characteristics

Starting 1-Year 5-Year

Corporate Emerging Securitized Hypothetical US High YTW Forward Forward

Credit Markets Credit Portfolio Yield Index Date US HY Returns Returns

Global IG EM EM EM IG

31 Mar 30 Sep 31 Mar 30 Sep 31/5/06 8.3% 13.2% 10.4%

High BBB HC HC LC CRTs BBB

2022 2021 2022 2021

Yield Corp Sov Corp Gov’t CMBS

31/7/07 9.1% 0.0% 11.7%

Percent

Market 50.0% 5.0% 15.0% 10.0% 7.5% 5.0% 7.5% 100% 100% 100% 100% 29/1/10 9.0% 16.1% 8.4%

Weight

30/6/11 7.3% 7.3% 8.2%

YTW

6.5 3.9 8.7 8.3 11.4 6.3 5.8 7.2 5.5 6.0 4.0

(Percent) 31/5/12 7.9% 14.4% 7.7%

OAS (b.p.) 428 142 632 586 121 606 329 439 402 325 289 30/11/15 8.0% 12.1% 9.0%

Credit 31/10/18 6.9% 8.5% —

B+ BBB B BB/B B B- BBB Ba/B Ba/B Ba/B Ba/B

Quality

31/3/20 9.4% 23.9% —

Duration

4.3 8.6 5.6 4.6 4.3 0.2 4.5 4.6 4.6 3.9 4.0

(Years) 31/3/22 6.0% — —

Past performance does not guarantee future results.

EM: emerging markets; HC: hard currency; LC: local currency; CRTs: credit-risk transfers; CMBS: commercial mortgage-backed loans. Simulated or hypothetical performance

results have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Results include estimates of trading

costs and market impact; however, because these trades have not actually been executed, results may have under- or overcompensated for these costs. Simulated or hypothetical

trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to

achieve returns or a volatility profile similar to those being shown. IG BBB Corp: Bloomberg BBB Investment-Grade Corporates; EM HC Sov: EM USD Aggregate (rated high yield);

EM HC Corp: EM USD Corp + Quasi-Sov (rated high yield); EM LC Gov’t: EM Local Currency Government (rated high yield). Securitized includes Agency CRTs; IG BBB CMBS:

CMBS IG BBB Index. Bloomberg indices were used for the hypothetical portfolio characteristics.

As of 31 March 2022. Source: Bloomberg and AB

Global Capital Markets Outlook 35Appendix

Global Capital Markets Outlook 36Global Forecast Overview

Key Assumptions Central Narrative Key Risks

• Geopolitical: The war in Ukraine is • Global growth: Challenged consumers Key Upside Risks

likely to keep commodity prices will have to allocate more money to

• A timely resolution to the Ukraine war

elevated for some time to come commodity-based essential goods and

could provide relief through lower

reduce discretionary spending

• COVID-19: Caseloads may wax and commodity prices

wane, but we do not expect widespread • Inflation: Rising commodity prices will

• Fiscal authorities could provide

economic disruption push inflation higher and keep it there

significant relief to consumers struggling

for longer

• Fiscal policy: European fiscal policy with higher energy prices

may mitigate some downside risk from • Yields: Tighter monetary policy will

Key Downside Risks

the war push yields up and flatten yield curves

• A protracted military conflict could

• Monetary policy: Rates will move • USD: Stronger for now, as the Fed pulls dampen sentiment throughout Europe

higher and faster than previously ahead of other central banks in policy and beyond

anticipated tightening

• Inflation expectations could de-anchor,

forcing very aggressive monetary-policy

tightening

Past performance and current analysis do not guarantee future results.

As of 31 March 2022

Source: AB

Global Capital Markets Outlook 37Growth Stocks Experienced Extreme and Unusual Underperformance

December 2021–February 2022 was the worst three-month period of growth underperformance in more than 30

years: –14.3%

EAFE Growth vs. Value Indices: Three-Month Rolling Companies Persisting with ≥ 10% YoY Earnings Growth

Performance Differential (Since 1990) Top 1,000 global companies (1989–2021)

131 4.0 378 400

128

3.5%

3.5 350

3.0 300

Number of Companies

Excess (Percent)

2.5 250

2.3%

Annualized Excess

2.0 Returns vs. MSCI World 200

Jan–Mar 22: –12.3%

(Left Scale)

Dec 21–Feb 22: –14.3% 48

Mar–May 00: –14.0% 43 1.5 150

Feb–Apr 99: –13.7%

1.0 100

62 Number of

14 Companies

0.5 0.8% 50

8

4 4 3 4 12

0.0 0Further Small-Cap Upside Expected, but Be Discerningly Active

Currently favoring more economically sensitive versus defensive sectors

Historically, Small-Caps Have …and Remain Attractive Relative to Maintain an Even Measure Between

Generated Positive Returns in Rising Large-Cap Stocks Small/SMID Value and Growth Styles

Rate Environments… Russell 2000 vs. Russell 1000

Change in

1.50

US Treasury Yields Russell 2000 Return

(Percentage Points)* Large-

Caps Favored Value Sectors: Favored Growth Sectors:

Oct 82–Jun 84 3.1

Are Cheap Consumer Discretionary, Financials, Technology,

Aug 86–Sep 87 2.7 Industrials, Technology Industrials

Feb 88–Feb 89 1.1

1.25

Jul 89–Apr 90 1.2

Sep 93–Nov 94 2.5

Dec 95–Aug 96 1.4 Average

Ratio (×)

4Q

Nov 96–Mar 97 0.9 2021

Sep 98–Jan 00 2.2 1.00

Oct 01–Mar 02 1.2

Sep 02–Jun 06 1.5

Dec 08–Dec 09 1.6

Aug 10–Mar 11 1.0

Jul 12–Dec 13 1.6 0.75 Focus on:

Feb 15–Jun 15 0.9 Small- Value with a Catalyst (V)

Jul 16–Mar 17 1.0 Caps Strong Free Cash Flow (V)

Are Cheap

Sep 17–Feb 18 0.9

Unrecognized Growth Potential (G)

Mar 20–Mar 21 1.2 Positive Earnings Revisions (G)

Aug 21–? 1.1 0.50

79 84 89 94 99 04 09 14 19

–10 0 10 20 30 40 50

Historical analysis and current forecasts do not guarantee future results.

*Total percentage-point change in nominal 10-year US Treasury bond yield

Left and right displays as of 31 March 2022; middle display through 28 February 2022

Source: FactSet, FTSE Russell and AB

Global Capital Markets Outlook 39Geopolitical Events Only Rarely Have a Lasting Market Impact

Select geopolitical events since 1970 and S&P 500 returns (percent)

First First

Event Trading Day 1 Week 1 Month 1 Quarter 1 Year Event Trading Day 1 Week 1 Month 1 Quarter 1 Year

Watergate 19/6/1972 –0.1 –1.4 0.4 –3.0 Madrid Train Bombings 11/3/2004 0.0 1.5 1.5 9.5

Yom Kippur War* 8/10/1973 1.4 –3.9 –10.0 –43.2 Orange Revolution–Ukraine 22/11/2004 1.1 2.2 3.1 8.6

Three Mile Island Accident 28/3/1979 –0.1 –0.7 –0.2 –4.2 Asian Tsunami 27/12/2004 0.3 –3.4 –2.7 6.8

Iran Hostage Crisis* 5/11/1979 –1.0 3.6 12.3 24.3 London Bombings 7/7/2005 2.4 2.7 0.2 8.6

Reagan Assassination Attempt* 30/3/1981 0.6 0.6 –1.6 –16.9 Hurricane Katrina 29/8/2005 1.1 1.0 5.7 9.5

Challenger Space Shuttle 28/1/1986 3.2 9.3 16.8 32.0 Arab Spring 17/12/2010 1.2 4.2 1.6 0.2

Iran-Contra Affair 3/11/1986 0.7 2.1 12.3 3.2 Hurricane Sandy 29/10/2012 1.1 –0.0 7.0 27.3

Iraq Invades Kuwait* 2/8/1990 –4.7 –8.9 –12.8 12.8 Boston Marathon Bombing 15/4/2013 –2.1 3.0 6.3 16.7

Desert Storm/First Gulf War* 17/1/1991 4.5 17.2 23.6 36.6 Russia/Ukraine/Crimea 27/2/2014 1.6 0.5 3.5 16.8

LA Riots 29/4/1992 2.0 2.3 2.8 10.2 Greek Referendum 5/11/2015 –1.2 –0.3 –8.4 1.4

WTC Bombing (1993) 26/2/1993 1.2 2.1 2.2 8.3 Brexit 24/6/2016 –0.7 3.1 3.0 17.8

Oklahoma City Bombing 19/4/1995 1.4 3.1 11.3 30.5 Trump Surprise Election Win 8/11/2016 1.6 5.4 8.1 24.0

Centennial Olympic Park Bombing 29/7/1996 4.3 4.6 10.8 50.6 Hurricane Harvey/Irma/Maria 25/8/2017 1.4 2.8 7.2 20.2

Kenya/Tanzania Embassy Bombings 7/8/1998 –1.3 –0.5 5.1 21.0 US-China Trade War‡ 22/1/2018 2.2 –2.6 –3.7 –3.1

USS Cole Bombing* 12/10/2000 –1.6 0.2 –2.5 –18.5 Coronavirus Outbreak 19/2/2020 –7.1 –28.7 –13.3 15.9

Bush-Gore Hanging Chad* 7/11/2000 –5.6 –5.5 –5.3 –20.9

9/11* 17/9/2001 –4.9 –0.9 4.7 –15.5 Summary 1 Week 1 Month 1 Quarter 1 Year

War in Afghanistan* 8/10/2001 1.9 3.0 9.8 –24.2 Average 0.1 0.2 4.1 9.3

SARS† 11/2/2003 –0.1 –3.2 12.2 39.5 % of Events Negative 40 37 29 29

Second Gulf War 20/3/2003 –0.5 2.4 14.3 29.2 Conflict/War Avg. 0.7 1.7 4.7 4.7

Terrorism Avg. –0.1 0.7 4.4 12.4

Political Avg. –0.2 1.1 2.4 5.3

Key Takeaway: Stocks have generally shrugged off geopolitical events,

Environmental Avg. 0.8 –0.1 3.4 11.9

as they rarely have a lasting impact on the business cycle.

Social Avg. –0.5 –3.9 7.6 16.2

Historical analysis does not guarantee future results. There is no guarantee that any estimates or forecasts will be realized.

*Denotes the geopolitical event occurred during a recession or six months prior to the start of a recession. †Date that China officially notified the WHO of the outbreak. ‡Tariffs on

imports of solar panels and washing machines imposed

As of 30 September 2021. Source: FactSet, National Bureau of Economic Research, S&P, World Heath Organization and AB

Global Capital Markets Outlook 40As Expansion Leads to Moderation, Seek Profitable Growth and Quality

Recovery Expansion Moderation Contraction

Cyclical Value Growth Growth Low Volatility

Positive

Small-Cap Quality Dividend Yield

Dividend Yield

Quality Small-Cap Cyclical Value Small-Cap

Neutral

Quality Low Volatility Quality

Dividend Yield

Low Volatility Cyclical Value Small-Cap Cyclical Value

Negative

Growth Low Volatility Growth

Dividend Yield

For illustrative purposes only. Past performance does not guarantee future results.

Small-cap: market capitalization; cyclical value: book to price, forward earnings to price; quality: return on equity; growth/momentum: 12-month price momentum, year-over-year

earnings growth; low volatility: low historical beta; defensive value: earnings to price, dividend yield. Cycles based on PMI. From 1 January 1991 through 31 May 2021

As of 31 December 2021

Source: Bloomberg, Center for Research in Security Prices (CRSP), Cornerstone Data, IHS Markit, Morningstar, MSCI, S&P Compustat, Thomson Reuters I/B/E/S and AB

Global Capital Markets Outlook 41A Word About Risk

Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date

of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection,

forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after

the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide

tax, legal or accounting advice. It does not take an investor's personal investment objectives or financial situation into account; investors should discuss their

individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or

an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This

publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as

advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB

L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company

registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA -

Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a

registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers

Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The

product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been

issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as

"wholesale clients," as defined in the Corporations Act 2001 (Cth of Australia), and should not be construed as advice. Note to Singapore Readers: This

document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the

management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein

(Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to

Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the

Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers

in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of

institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives,

financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional

distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in

Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-

management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services

in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act

2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or

provide financial-planning services in Malaysia. Important Note For UK and EU Readers: For Professional Client or Investment Professional use only. Not for

inspection by distribution or quotation to, the general public.

Global Capital Markets Outlook 42A Word About Risk

The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication.

AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion

in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this

publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or

accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual

circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or

solicitation for the purchase or sale of any financial instrument, product or service sponsored by AllianceBernstein L.P. or its affiliates.

Important Risk Information Related to Investing in Equity and Short Strategies

All investments involve risk. Equity securities may rise and decline in value due to both real and perceived market and economic factors as well as general

industry conditions.

A short strategy may not always be able to close out a short position on favorable terms. Short sales involve the risk of loss by subsequently buying a security at a

higher price than the price at which it sold the security short. The amount of such loss is theoretically unlimited (since it is limited only by the increase in value of

the security sold short). In contrast, the risk of loss from a long position is limited to the investment in the long position, since its value cannot fall below zero. Short

selling is a form of leverage. To mitigate leverage risk, a strategy will always hold liquid assets (including its long positions) at least equal to its short position

exposure, marked to market daily.

Important Risk Information Related to Investing in Emerging Markets and Foreign Currencies

Investing in emerging-market debt poses risks, including those generally associated with fixed-income investments. Fixed-income securities may lose value due to

market fluctuations or changes in interest rates. Longer-maturity bonds are more vulnerable to rising interest rates. A bond issuer’s credit rating may be lowered

due to deteriorating financial condition; this may result in losses and potentially default, or failure to meet payment obligations. The default probability is higher in

bonds with lower, noninvestment-grade ratings (commonly known as “junk bonds”).

There are other potential risks when investing in emerging-market debt. Non-US securities may be more volatile because of the associated political, regulatory,

market and economic uncertainties; these risks can be magnified in emerging-market securities. Emerging-market bonds may also be exposed to fluctuating

currency values. If a bond’s currency weakens against the US dollar, this can negatively affect its value when translated back into US-dollar terms.

Bond Ratings Definition

A measure of the quality and safety of a bond or portfolio, based on the issuer’s financial condition, and not based on the financial condition of the fund itself. AAA

is highest (best) and D is lowest (worst). Ratings are subject to change. Investment-grade securities are those rated BBB and above. If applicable, the Pre-

Refunded category includes bonds which are secured by US government securities and therefore are deemed high-quality investment grade by the advisor.

Global Capital Markets Outlook 43Index Definitions

Following are definitions of the indices referred to in this presentation. It is important to recognize

that all indices are unmanaged and do not reflect fees and expenses associated with the active

management of a mutual fund portfolio. Investors cannot invest directly in an index, and its

performance does not reflect the performance of any AB mutual fund.

• Bloomberg Emerging Markets Hard Currency (USD) Aggregate Index: A hard currency emerging markets debt benchmark that includes USD-denominated debt from

sovereign, quasi-sovereign, and corporate EM issuers.

• Bloomberg Emerging Markets Local Currency Government Index: Tracks the fixed-rate local currency sovereign debt of emerging market countries.

• Bloomberg Global Aggregate Corporate Bond Index: Tracks the performance of investment-grade corporate bonds publicly issued in the global market and found in the Global

Aggregate. (Represents global corporate on slide 2.)

• Bloomberg Global High-Yield Bond Index: Provides a broad-based measure of the global high-yield fixed-income markets. It represents the union of the US High-Yield, Pan-

European High Yield, US Emerging Markets High-Yield, CMBS High Yield and Pan-European Emerging Markets High-Yield indices. (Represents high yield on slide 2.)

• Bloomberg Global Treasury Index: Tracks fixed-rate local currency government debt of investment-grade countries. The index represents the Treasury sector of the Global

Aggregate Bond Index.

• Bloomberg Global Treasury: Euro Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Euro Area Treasury sector of the Global Aggregate Bond

Index. (Represents euro-area government bonds on slide 2.)

• Bloomberg Global Treasury: Japan Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Japanese Treasury sector of the Global Aggregate Bond

Index. (Represents Japan government bonds on slide 2.)

• Bloomberg Pan-European High Yield Index: Measures the market of non-investment grade, fixed-rate corporate bonds denominated in the following currencies: euro, pounds

sterling, Danish krone, Norwegian krone, Swedish krona, and Swiss franc.

• Bloomberg US Aggregate Bond Index: A broad-based benchmark that measures the investment-grade, US dollar–denominated, fixed-rate, taxable bond market, including

US Treasuries, government-related and corporate securities, mortgage-backed securities (MBS [agency fixed-rate and hybrid ARM pass-throughs]), asset-backed securities

(ABS), and commercial mortgage-backed securities (CMBS).

• Bloomberg US Corporate High-Yield Bond Index: Represents the corporate component of the Bloomberg US High-Yield Index.

• Bloomberg US Treasury Index: Includes fixed-rate, local-currency sovereign debt that makes up the US Treasury sector of the Global Aggregate Index. (Represents US

government bonds on slide 2.)

Global Capital Markets Outlook 44Index Definitions (cont.)

• Goldman Sachs Financial Conditions Index: The index is defined as a weighted average of riskless interest rates, the exchange rate, equity valuations, and credit spreads,

with weights that correspond to the direct impact of each variable on GDP.

• Goldman Sachs Non-Profitable Technology Index: The index consists of non-profitable US listed companies in innovative industries. Tech is defined quite broadly to

include new economy companies across GICS industry groupings. The basket is optimized for liquidity with no name initially weighted greater than 4.65%.

• HFRI Equity Hedge Index: Investment managers who maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment

processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly

focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation

ranges of typical portfolios. EH managers would typically maintain at least 50% exposure to, and may in some cases be entirely invested in, equities, both long and short.

• HFRI Event Driven Index: Investment managers who maintain positions in companies currently or prospectively involved in corporate transactions of a wide variety including

but not limited to mergers, restructurings, financial distress, tender offers, shareholder buybacks, debt exchanges, security issuance or other capital structure adjustments.

Security types can range from most senior in the capital structure to most junior or subordinated, and frequently involve additional derivative securities. Event Driven exposure

includes a combination of sensitivities to equity markets, credit markets and idiosyncratic, company-specific developments. Investment theses are typically predicated on

fundamental characteristics (as opposed to quantitative), with the realization of the thesis predicated on a specific development exogenous to the existing capital structure.

• HFRI Fund Weighted Composite Index: A global, equal-weighted index of more than 2,000 single-manager funds that report to HFR Database. Constituent funds report

monthly performance net of all fees in US dollars and have a minimum of $50 million under management or 12-month track record of active performance.

• HFRI Macro: Investment Managers which trade a broad range of strategies in which the investment process is predicated on movements in underlying economic variables and

the impact these have on equity, fixed income, hard currency and commodity markets. Managers employ a variety of techniques, both discretionary and systematic analysis,

combinations of top down and bottom up theses, quantitative and fundamental approaches and long and short term holding periods. Although some strategies employ RV

techniques, Macro strategies are distinct from RV strategies in that the primary investment thesis is predicated on predicted or future movements in the underlying instruments,

rather than realization of a valuation discrepancy between securities. In a similar way, while both Macro and equity hedge managers may hold equity securities, the overriding

investment thesis is predicated on the impact movements in underlying macroeconomic variables may have on security prices, as opposes to EH, in which the fundamental

characteristics on the company are the most significant are integral to investment thesis.

• HFRI Relative Value: Investment Managers who maintain positions in which the investment thesis is predicated on realization of a valuation discrepancy in the relationship

between multiple securities. Managers employ a variety of fundamental and quantitative techniques to establish investment theses, and security types range broadly across

equity, fixed income, derivative or other security types. Fixed income strategies are typically quantitatively driven to measure the existing relationship between instruments and,

in some cases, identify attractive positions in which the risk adjusted spread between these instruments represents an attractive opportunity for the investment manager. RV

position may be involved in corporate transactions also, but as opposed to ED exposures, the investment thesis is predicated on realization of a pricing discrepancy between

related securities, as opposed to the outcome of the corporate transaction.

Global Capital Markets Outlook 45You can also read