First World Hybrid Real Estate Plc - 18th February 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

First World Hybrid Real Estate Plc

18th February 2021

First World Hybrid Real Estate CONTENTS • (1) REVIEW OF THE UK MARKET - DRIVERS, INFLUENCES, RISKS, THREATS o Brexit and importance of ‘no deal Brexit’ off the table o UK government financial support and the impact of the vaccine on the UK economy o UK property market and sector trends – Work from home (WFH) and online shopping • (2) FWHRE UPDATE o Impact of COVID 19 on FWHRE portfolio o Review of FWHRE key performance areas – collections, valuations, investment returns (1, 3, 5 years) o 21st portfolio acquisition, DHL Doncaster o Flows, redemptions, liquidity and debt rates o Comparison with inflation linked bond o Outlook

First World Hybrid Real Estate Fund

• Major themes and trends impacting on UK property

• Brexit

• COVID pandemic – lock downs and vaccine rollout

• Govt financial support – the longer-term implications

• WFH – a new normal?

• Online shopping – from convenience to necessity

• Hybrid Real Estate

Quality

Defensive

Dividends

UK Property Market- Major themes and trends

• Brexit

• UK voted to leave the EU in 2016 referendum – more than 4 ½ years ago!

• Withdrawal Agreement signed in 2017 and negotiations commenced ….

• Somewhat as expected, trade deal signed late December 2020

• Frictionless trade with EU, zero tariffs or quotas on UK goods, no hard border in Ireland - significant risk to

UK economy avoided

Positive impact on distribution type property with greater emphasis on supply chains

GBP firmed from a low of 1.14 to USD to 1.39 and 1.07 to Euro to 1.15.

58% of 2020 property investment transactions funded by foreign investors (Source: Carter Jonas Estate

Agents UK)

UK remains a well regulated, transparent 1st world economy with entrenched property rights and a

desirable place to store wealth

UK Property Market - Major themes and trends

• Covid-19 pandemic

• WHO declared a pandemic in Feb 2020. UK enters first hard lockdown in March 2020.

• Significant business interruption – esp. retail, hospitality and tourism, resulting in financial hardship &

Company Voluntary Arrangements (CVA’s)

• Valuers adopt Material Uncertainty Clause in valuations necessitating suspension of property funds

• Massive govt intervention - business aid packages £66 bn, Furlough £73 bn, Bond purchases £875 bn,

being much greater and more rapid than the GFC support

• Impressive vaccine rollout – up to 3m jabs a week, circa 15m in total (gov.uk) (as at current date)

GDP contracted sharply but strong rebound expected

Interest rates now 0.1% and expected to remain low – good for prop financing / prop yields attractive

Inflation low and expected to remain < 2% due to debt burden and unemployment

WFH – a more flexible approach, but an unlikely new normal?

Online shopping – convenience to necessity, where to now?

WFH – a new normal? • WFH was / remains a given • Government lock down requirement • Business risk • Question is – what is the long-term impact? • 12 months is a long time – changes become habits • Business - cost saving opportunities but surely people interaction remains important? • Employees – morale, learning, social interaction • Practical experience Short term demand of office space uncertain Longer term – need for offices not going away

Online – a new normal?

Online trends

• Convenience to necessity - where to from here?

• Now around 1/3rd of retail

• 1st time online shoppers in 2020 confirming that they

will continue to shop online

Retailers continue to fail (Debenhams & Arcadia

being the latest), resulting in increased vacancies

and falling rentals - bad for retail shopping centres

and high street

Online operators thrive – increasing demand for

logistics and distribution warehousing

UK Property Market

Winners/Losers

Winners

• Logistics property – record take-up in 2020 of 50.1m sqft

(source Savills), underpinning rental growth

• Rental collections for DW focused funds remained very

much intact

• Strong investment demand - yield compression for well

let, long income assets

• All industrial property – 8.7% total return (TR) for 2020*

Losers

• Shopping centres and high street retail – TR for shopping

centres a dismal negative 20%*

• Retail warehouses – TR of negative 8%*, but with positive

contribution in Q4, showing resilience

• Offices – more flexible approach to work unclear but

likely to normalise over time – TR a negative 1%*

* MSCI/ IPD returns

First World Hybrid Real Estate

Covid19 Trading update & 2020 highlights

• The Fund has, and continues to be, well placed given

o the type of properties it owns (mainly distribution warehousing and with no investment in high street

retail or shopping centres)

o the nature and length of the leases

o the financial strength of the tenants

• 2020 (Jan 2021) highlights

o 100% of rental collected

o both direct property portfolio and REIT portfolio increased in value

o quarterly dividends continued (Q3 and Q4 2020 at increased level)

o Fund price appreciated

o Exchanged contracts to acquire a high-quality DHL warehouse for £22.65m (subject to vendor

conditionality)

First World Hybrid Real Estate

Performance – Return Composition (GBP) at 31 January 2021

Annualised returns – period ending 31

1 Year 3 Years 5 Years

January 2021

Total Return 8.2% 7.4% 7.4%

Income 4.8% 4.9% 5.1%

Capital growth 3.3% 2.4% 2.3%

Income return as expected – predictable at target 4.50%

Price return – based on property valuations and REIT prices

Source Bloomberg and MarriottFirst World Hybrid Real Estate

Performance – Comparative returns (GBP) at 31 January 2021

Annualised returns – period ending 31

1 Year 3 Years 5 Years

January 2021

FWHRE 8.2% 7.4% 7.4%

UK REITs -15.1% -0.9% 0.9%

SA Listed property (GBP) -37.2% -24.0% -6.7%

SA Listed property (ZAR) -33.9% -18.4% -8.2%

Listed and publicly traded REITs have been exceptionally volatile and returns

have been significantly impacted by COVID-19 market uncertainty.First World Hybrid Real Estate

Performance - without the volatility at 31 January 2021

£1,800,000 First World Hybrid Real Estate(FWHRE) vs. Listed UK REITs £1,793,206

£1,700,000

Independently appraised

£1,600,000

Distribution warehousing emphasis

£1,500,000

£1,400,000

£1,300,000 £1,307,111

£1,200,000

£1,100,000

Listed volatility

£1,000,000

Retail prime office emphasis

£900,000

£800,000

Jan 14

Oct 14

Jan 15

Oct 15

Jan 16

Oct 16

Jan 17

Oct 17

Jan 18

Oct 18

Jan 19

Oct 19

Jan 20

Oct 20

Jan 21

Apr 14

Jul 14

Jul 18

Jul 19

Jul 20

Apr 15

Jul 15

Apr 16

Jul 16

Apr 17

Jul 17

Apr 18

Apr 19

Apr 20

Source: Bloomberg and Marriott First World Hybrid Real Estate NAREIT Index (UK)

Pricing of FWHRE was temporarily placed on hold between 19 March 2020 and 21 August 2020 due to uncertainty around direct real estate valuations in the UK and material

uncertainty conditionality adopted by valuers. As a result, the returns for this period utilise indicative pricing for FWHRE. The Fund reopened for trade on 24 August 2020.First World Hybrid Real Estate

Defensive – large warehousing dominant REITs at January 2021

£1,200,000 First World Hybrid Real Estate(FWHRE) selected REITS vs. Listed UK • REITS are a fundamental part

Property

£1,100,000

of structure and held to

£1,086,315

provide liquidity

£1,000,000

• By design the Fund REITS are

warehousing dominant, no

£900,000

exposure to traditional retail

£823,679

£800,000

• See strong relative out-

performance by REITs held by

£700,000

Fund – confirmation of property

type selection.

£600,000

£500,000

30 Nov 20

30 Apr 20

31 May 20

31 Jul 20

31 Oct 20

31 Dec 19

31 Aug 20

31 Jan 20

29 Feb 20

31 Mar 20

30 Jun 20

30 Sep 20

31 Dec 20

FWHRE selected REIT's UK Reit Index

Source: BloombergFirst World Hybrid Real Estate Quality – large, liquid, warehouse dominant REITs

First World Hybrid Real Estate

Quality – property type?

Covid 19 Structural shifts are likely to favour the First World portfolio

• DRIVERS OF DISTRIBUTION WAREHOUSE OUTPERFORMANCE

o Big increase in online shopping with new entrants looking for warehouse space

o Resulting in very robust performance for 69% of the portfolio

• DRIVERS OF REGIONAL OFFICE RESILIENCE

o With the mitigating factors mentioned in the preamble we don’t think WFH is a a permanent solution

o We believe the regional office portfolio (20% exposure) will be stable going forward

• YES CONTAGION IN THE RETAIL WAREHOUSE SECTOR WITH VALUATION LOSSES

o With food-stores, retail warehouse has been the best performing retail sub-sector

o Small exposure to this sector at 11% and we expect stable pricing and possibly firming this year

The property portfolio is well positioned for the futureFirst World Hybrid Real Estate Quality - 20 institutional grade modern properties

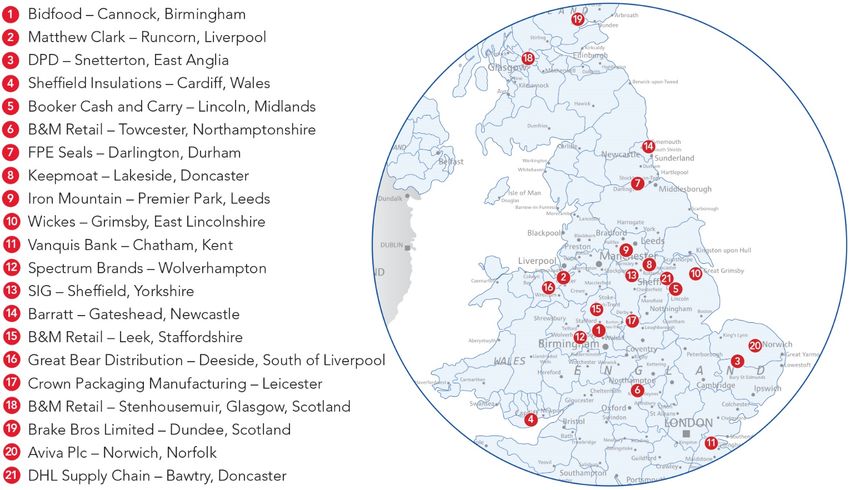

First World Hybrid Real Estate Quality - 21st portfolio acquisition - DHL Doncaster • A strategic distribution location in Doncaster, on the A1 north/south arterial providing DHL with excellent links to key distribution routes • Let to DHL Supply Chain Ltd for further 10 years, expiring December 2030, part of the worlds leading postal and logistics company, Deutsche Post DHL with 470 000 employers in 220 countries with Group revenue of €63.3bn. • Single storey, modern 272, 399 sqft distribution warehouse with offices • Fully repairing and insuring lease (ie tenant responsible for all operating costs) with 5 yearly 2.0% per annum compound fixed uplifts • Purchase price £22.65m at a 5.00% net initial yield • Transaction Completion subject to vendor conditionality

First World Hybrid Real Estate Quality – 21st portfolio acquisition - DHL Doncaster

First World Hybrid Real Estate

Quality – property type (post DHL deal)

• Emphasizes distribution warehouse &

logistics focussed fund

• Complimented with limited retail

warehousing and regional offices

• The portfolio has a very favourable

WAULT to expiry of 9.4 years with 100%

occupancy/zero vacancies

No high street retail /shopping centres, leisure or student accomFirst World Hybrid Real Estate Defensive – geographical spread

First World Hybrid Real Estate

Defensive – tenants

• Diversified tenant base, substantial tenants

o DHL 13% - Worlds leading postal & logistics company, ptp £135m, net worth £398m

o Crown 11% - UK leading can manufacturer, £850m tangible net assets.

o B&M 11% (3 properties) – UK leading variety goods value retailer. FTSE 100 company with £750m tangible net

assets. Traded throughout lockdown with significant increase in sales (Q4 2020 LFL sales up 21%).

• Mainly UK consumer facing businesses

o No London or international head offices

o No export focussed

o No automotive

Tenant selection and financial standing underpins income certaintyFirst World Hybrid Real Estate

Defensive - valuation policy

• Due to Material Uncertainty the Fund moved to obtaining quarterly valuation updates on a

temporary basis from 1st Aug to 31st Dec 2020.

• From 1st Jan 2021 back to six monthly intervals.

• During 2020, 66 valuation updates were received, resulting in £2.5m net increase in portfolio

value

o 18 were up, unsurprisingly mainly the distribution warehousing properties

o 14 were down, including all the retail warehousing properties

o 34 were retained at previous levels

• In 2021 6 valuation updates received resulting in a £20 000 net increase in portfolio value.

Rolling valuation of portfolio, by design, to reduce volatilityFirst World Hybrid Real Estate

Property portfolio debt - well placed, defensive

• Loan to value (LTV) – pre-DHL

o Max 50% LTV on property acquisition price

o Actual LTV is 44% on property portfolio value andFirst World Hybrid Real Estate

Liquidity & Redemptions – defensive approach

• Liquidity target levels

o 25% Target Liquidity Level (of NAV), with 20% Minimum Liquidity Level

o Held primarily in REIT portfolio

o Yield dilutive but permanent feature of Fund to meet reasonable redemptions

• Actual liquidity

o The current liquidity level is 37% but will revert to target levels when the DHL deal is concluded

• Redemptions

o 2020 : 4% of NAV (2019 : 7%)

o Redemptions have been well below historic trendsFirst World Hybrid Real Estate

Dividends – predictable, reliable income yield

LONGER TERM RETURN EXPECTATIONS 4.5% to

6.5% pa (Sterling)

Underpinned by

• Reliable income

• Expected rental growth

The differential between property and bond yields is significant. Should the low

interest rate environment continue (as seems likely) there is an argument for

property yield compression to continue with consequent value growth.First World Hybrid Real Estate

Dividends – Reliable income & rental growth

DHL Doncaster

Yield 5.0%

Income Growth 2.0% pa

Term 10 years

WAULTComparing FWHRE to 10 year UK Government Bonds

10 year expected outcome for a £100 000 investment

UK Government Bonds (10yr) First World Hybrid

Real Estate

Fixed Inflation Linked

Yield +0.5% -2.8% ±4.5%

UK Inflation

Income Growth 0% 0%-2%

(assuming 2.0%)

Term 10 years 10 Years ±10 years

WAULT

Expected Return

+0.5% -0.8% 4.5%-6.5%

(p.a.)Comparing FWHRE to 10-year UK Government Bonds

(fixed and inflation linked)

UK Government Bonds (10yr) First World Hybrid

Real Estate

Fixed Inflation Linked

£155 000

£100 000

£105 000 £92 000 to

Investment

£187 000

Source: Bloomberg & Marriott, For inflation linked bond returns are assuming UK Inflation average 2% on averageFirst World Hybrid Real Estate Quality, Defensive, Dividends • The Fund is structured to offer better liquidity and pricing certainty than typical direct property investments but with less volatility than publicly quoted and traded property, this with the comfort of a Regulated Fund. • Due to the type of property it owns and the length of leases and its tenants The Fund has performed well and remains well placed for a post C19 environment. • The Fund’s leases and tenant strength can be expected to underpin a robust and attractive dividend yield in Sterling. • The occupational market applicable to the Fund’s properties is supportive of modest capital growth over time.

Collective investment schemes are generally for the medium to long-term. The value of participatory interests or the investment may go down as well as up. Past performance is not necessarily a guide to future performance. Collective investment schemes are traded at ruling prices and the First World Hybrid Real Estate Fund (FWHREF) can engage in borrowing. If required, FWHRE may borrow up to 50% of the net asset value of the Fund for the purpose of achieving its investment objectives. Forward pricing is used. The Net Asset Value (NAV) is calculated in line with the Offering Document . Purchase requests must be received by the manager (FIM Capital) by 17h00 Isle of Man time on a valuation day. Repurchase requests must be received by the manager prior to 5.00 p.m. five clear Business Days before a Redemption Day as per the Offering Document. FWHRE provides a reasonable but not absolute level of liquidity due to the inclusion of cash and listed REITS in addition to the direct real estate portfolio. Large redemption requests may therefore be delayed. Prices are published on a weekly basis on the Marriott website, www.Marriott.co.za and on TISE. Unit trusts are calculated on a net asset value basis. Net asset value is the value of all assets in the portfolio including any income accrual and less any permissible deductions from the portfolio. FWHRE does not provide any guarantees with respect to the capital or the return of the portfolio. A schedule of fees and charges and maximum commissions is available on request from Marriott. Where initial fees are applicable, these fees are deducted from the investment consideration and the balance invested in units at the net asset value. Commissions and incentives may be paid and if so, would be included in the overall costs. Different classes of shares may apply to the fund and will be subject to different fees and charges. The inclusion of foreign securities in a portfolio are subject to risks including but not limited to potential constraints on liquidity and the repatriation of funds, macroeconomic risks, political risks, foreign exchange risks, tax risks, settlement risks and the potential limitations on the availability of market information. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. In addition, investments in regulated funds may involve special risks that could lead to a loss of all or a substantial portion of the investment. Declaration of distribution for Class A, where relevant, is quarterly. Performance figures are based on lump sum investment. Individual investor performance may differ as a result of initial fees, the actual investment date, the date of reinvestment and dividend withholding tax. This Fund may be closed to new investors in order to manage it more efficiently in accordance with its mandate. The TER shows the percentage of the average Net Asset Value of the portfolio that was incurred as charges, levies and fees relating to the management of the portfolio. A higher TER ratio does not necessarily imply poor return, nor does a low TER imply a good return. The current TER cannot be regarded as an indication of future TERs. Marriott Asset Management (Pty) Ltd is the intermediary services provider for the Fund. FIM Capital Ltd have been appointed as Manager of the Fund, and are regulated by the Isle of Man Financial Services Authority. Copies of the offering document, financial statements and constitutional documentation for the Fund can be obtained from their address, 55 Athol Street, Douglas, Isle of Man IM1 1LA Licensed Financial Services Provider

You can also read