Evolution in the Automotive sector - How does the urge for constant adaptation affect CIE Automotive?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

January 2018

Evolution in the

Automotive

sector

How does the

urge for constant

adaptation affect

CIE Automotive?

1

1. Taking a car to pieces

2. Evolution in the Automotive sector

TABLE OF 3. From ICE to EV

CONTENTS 4. Electrification: Scenarios

5. Uncertainties concerning EVs

6. Other Trends

7. CIE Automotive: constant adaptation

2

1) Taking a car

to pieces

3

ST R U C T U R E & C H A S S I S

S T R U C T U R A L PA R T S , C H A S S I S & S U S P E N S I O N

Source: Honda

Chassis and suspension (rear)

Structural components

Chassis and Source: BMW

suspension (front)

4

INTERIOR & EXTERIOR TRIM

INTERIOR, EXTERIOR TRIM & ROOF SYSTEMS

Interior trim including doors, seat, airbag,

cockpit, sunshade and decorative parts

Exterior trim including logos, emblems,

wheel covers and decorative parts, as

well as roof systems

5

DRIVETRAIN

TRANSMISSION, STEERING,BRAKING SYSTEM

Source: GKN Driveline

Source: Brose

Source: Bosch

Source: GKN Driveline

Driveline plus differential, steering and braking systems

6

P OW E RT R A I N

ENGINE & GEARBOX

Exhaust system

Engine and gearbox, up to

differential

Source: Faurecia

7

2) Evolution

in the

Automotive

sector

8

E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

CASE 1: INJECTION SYSTEM (1/2)

Injector

9

E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

CASE 1: INJECTION SYSTEM (2/2)

Carburettor Obsolete

Distributor Obsolete

Metal Brazing Inox Welded Tube

Forging Inox Seamless Tube

Plastic Rail Metal Inox

Metal Brazing LP

Metal Brazing

water

Machining

2000 bar 2500 bar 3000 bar

Rail1000 bar

10E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

C A S E 2 : A U X I L I A R I E S E L E C T R I F I C AT I O N ( 1 / 2 )

Electric

Steering

Hydraulic

Steering

Source: ZF - TRW

Source: ZF - TRW

Electrification also implies more

number of architectures

11E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

C A S E 2 : A U X I L I A R I E S E L E C T R I F I C AT I O N ( 2 / 2 )

Current booster iBooster

Source: Bosch

Source: Bosch

The amplification in the braking forced changing from

air (vacuum) to electrically driven

12E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

C A S E 3 : M AT E R I A L E V O L U T I O N ( 1 / 2 )

There is a general trend to migrate from casted crankshafts to forged ones,

however, it depends on geographical characteristics (e.g. India) or OEMs

preferences (e.g. Ford). Sector in evolution and diversified.

Source: The University Of Toledo, Ali Fatemi, Jonathan Williams and Farzin

Montazersadgh

Comparison between mechanical properties

of forged and casted crankshafts

13E VO LU T I O N I N T H E AU TO M OT I V E S EC TO R

C A S E 3 : M AT E R I A L E V O L U T I O N ( 2 / 2 )

Source: BMW Group, Dr. Johannes Staeves, GALM, 24.04.20

14E VO LU T I O N I N AU TO M OT I V E S EC TO R

CONCLUSIONS

SECTOR CIE AUTOMOTIVE

It is not the first time the sector evolves. CIE has always been on track.

The rhythm of the evolution depends on CIE is present in all main

the market and segments. geographical markets and several

segments.

Evolution breaks the maturity cycle of For CIE, it means higher profitability

the components. as it moves away from commodities.

153) From ICE

to EV

VW Golf (ICE)

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017)

General Motors Chevrolet Bolt (EV)

16

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017)I N T E R N A L CO M B U ST I O N E N G I N E ( I C E ) * V E H I C L E

POWERTRAIN

Source: U.S.

Department of Energy

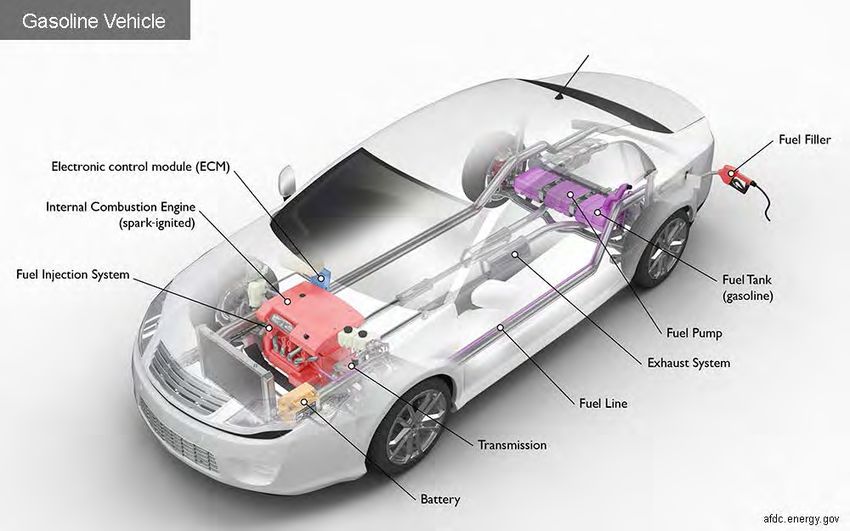

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

FCEV: Fuel Cell Electric Vehicle (operates on electricity produced using a fuel cell powered by hydrogen, rather than drawing electricity from a battery).

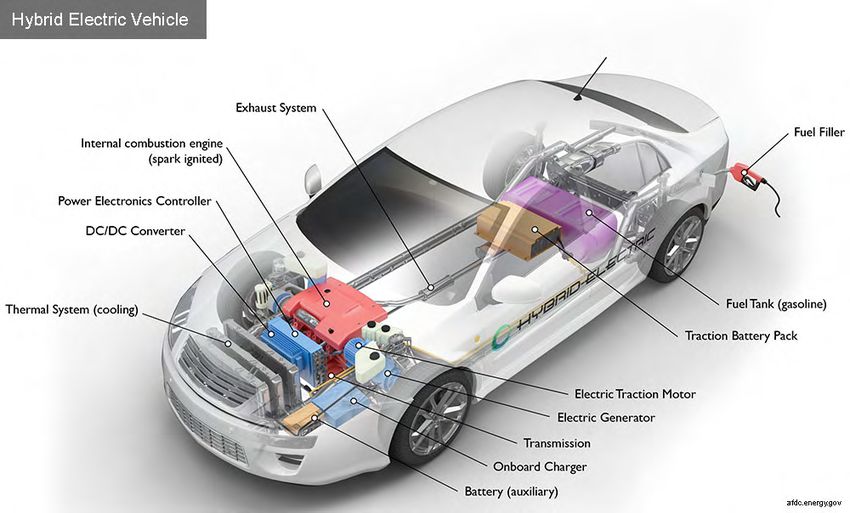

BEV: Battery Electric Vehicle (fully operates on battery electric power). 17H Y B R I D E L EC T R I C V E H I C L E ( H E V ) *

POWERTRAIN

Source: U.S.

Department of Energy

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

FCEV: Fuel Cell Electric Vehicle (operates on electricity produced using a fuel cell powered by hydrogen, rather than drawing electricity from a battery).

BEV: Battery Electric Vehicle (fully operates on battery electric power). 18E L EC T R I C V E H I C L E ( E V ) *

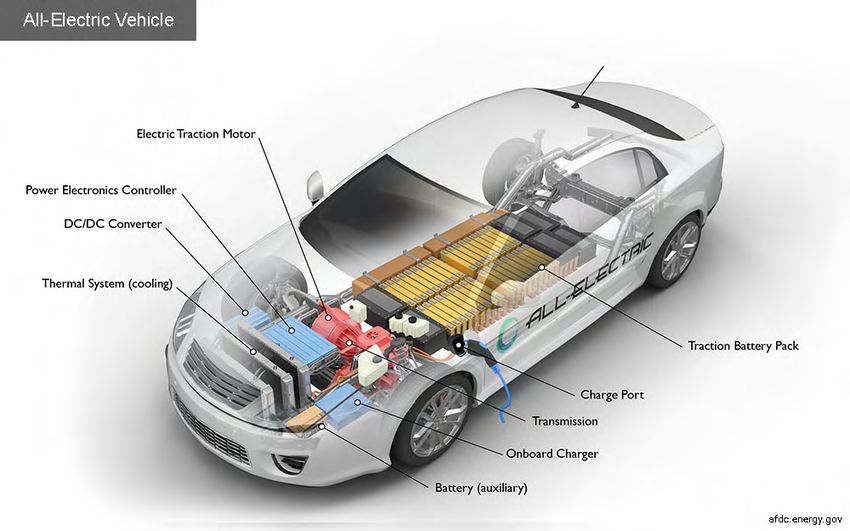

POWERTRAIN

Source: U.S.

Department of Energy

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

FCEV: Fuel Cell Electric Vehicle (operates on electricity produced using a fuel cell powered by hydrogen, rather than drawing electricity from a battery).

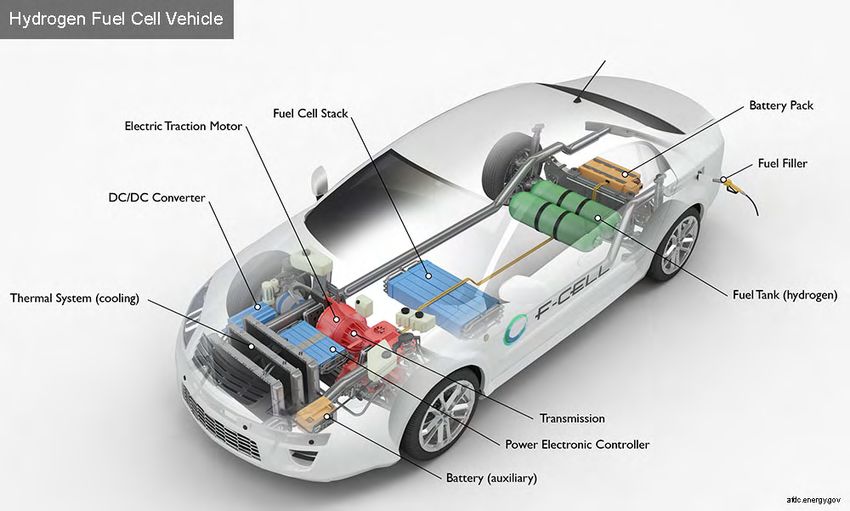

BEV: Battery Electric Vehicle (fully operates on battery electric power). 19F U E L C E L L E L EC T R I C V E H I C L E ( FC E V ) * ( H Y D RO G E N )

POWERTRAIN

Source: U.S.

Department of Energy

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

FCEV: Fuel Cell Electric Vehicle (operates on electricity produced using a fuel cell powered by hydrogen, rather than drawing electricity from a battery).

BEV: Battery Electric Vehicle (fully operates on battery electric power). 204) Electrification:

Scenarios

21E L EC T R I C V E H I C L E P E N E T R AT I O N

FORECASTS 2025

UBS IHS Bosch Schaeffler (Accelerated Scenario)

BEV BEV BEV BEV

9% 4%

(P)HEV 7% (P)HEV 15%

(P)HEV

11% 11%

23%

ICE

80%* ICE

50%

(P)HEV

ICE

ICE 35%

73%*

82%

*Includes Mild Hybrid *Expects 58% of ICE to be

gasoline and 15% to be Diesel.

Source: Schaeffler 2017 Global Auto

Source: UBS Q-Series Report; May 2017. Source: IHS 2017. Source: Bosch Innovation Day 2017.

Industry Conference.

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

BEV: Battery Electric Vehicle (fully operates on battery electric power).

22E L EC T R I C V E H I C L E P E N E T R AT I O N

FORECASTS 2025

Faurecia Continental Roland Berger MCPI Energies

BEV BEV BEV BEV

7% 8% 7% 5% HEV

9%

(P)HEV

(P)HEV HEV

18%

24% 25%

ICE ICE

69%* ICE 68%*

74% ICE

86%

*Expects 57% of ICE to be *Expects 56% of ICE to be

gasoline and 12% to be Diesel. gasoline and 12% to be Diesel.

Source: Faurecia Investor’s Day, June 2017. Source: UBS Q-Series Report; May 2017. Source: Faurecia Investor’s Day, June 2017. Source: MDPI Energies Journal 2017.

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

BEV: Battery Electric Vehicle (fully operates on battery electric power).

23The diversity of forecasts for short

and medium term reflects how

sensible the EV growth is to a large

number of uncertainties.

245) Uncertainties

concerning EVs

25ELECTRIFICATION

IS A REALITY.

BUT THERE IS A WIDE RANGE OF

UNCERTAINTIES THAT CAN

ACCELERATE MORE OR LESS THE

DEVELOPMENT AND

COMPETITIVENESS OF THE EV.

26U N C E RTA I N T I E S

CONSUMER CONCERNS

Source: Breakthrough of electric vehicle threatens European car industry by ING Economics Department, July 2017

“The car industry is at a turning point. Battery electric

vehicles (BEV) are becoming increasingly competitive.

The major barriers to demand – charging infrastructure,

range and pricing - are about to be broken”:

“Charging infrastructure: ultra fast charging of batteries will enable a

300km charge in 20 minutes. This will further improve over time.”

“Range anxiety: New battery technology should improve range to increasingly

meet consumer expectations from 2020 onwards.”

“Pricing and total cost of ownership: Battery costs continue to decline.

Although purchase prices will remain relatively high for quite some time,

electric vehicles have low costs of operation. This should enable a high

range battery electric vehicle to become cost competitive (on total cost of

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017) ownership) with a comparable petrol car in 2024.”

Price, range anxiety and charging time are key consumer concerns

27U N C E RTA I N T I E S

R AW M AT E R I A L AVA I L A B I L I T Y

Source: El País (November 2017)

Is Lithium supply as easy to ramp up as it

is abundant?

Lithium is relatively abundant. Yet

successfully designing, building,

commissioning and maintaining output from

brine and hard-rock deposits is more

technically challenging than many other

mineral commodities. A shortage of

experienced knowhow, lengthy development

timelines, process plant issues and quality

differentials present

challenges likely to result in more gradual

supply growth than developers may wish for. Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017)

As demand these materials grows, their availability is questioned

28U N C E RTA I N T I E S

R AW M AT E R I A L C O S T S

Source: Reuters (August 2017)

Lithium Price Evolution

Source: LME (Nov 2017)

Source: Bloomberg/CRU Group (August

Source: MDPI Energies Journal 2017 2017)

As demand these materials grows, their price increases significantly

29U N C E RTA I N T I E S

B AT T E R Y C O S T S

Source: MDPI Energies Journal 2017

“While policy and consumer behaviour are difficult to predict,

battery costs are coming down fast. We're already ahead of lithium-

ion battery costs projected for 2030. And with 10 battery

gigafactories under development around the world, battery costs

and prices are expected to further outpace projections.”

Source: Wood Mackenzie, July 17

https://www.greentechmedia.com/articles/read/everyone-is-revising-electric-vehicle-forecasts-upward#gs.Sy=GPno

Battery costs are expected to be reduced

Source: Elektrel quoting McKinsey 30U N C E RTA I N T I E S

F U E L B A N I N C I T I E S : S T R O N G E R F U E L C O N S U M P T I O N A N D Z E R O E M I S S I O N M A N D AT E S

Average emissions of the EU fleet

of new cars in 2030 will have to be

30% lower than in 2021. For the

EU fleet of new vans in 2030, the

reduction also amounts to 30%.

Legislation evolution can affect the penetration of EVs

31U N C E RTA I N T I E S

GRANTS ON HEV & EV

Evolution of BEV Sales in Denmark:

Source: Bloomberg Markets, June 2017

Grants evolution can change the buyer decisions. (Anticipation, postponing, cancelling…)

32U N C E RTA I N T I E S

HUGE INVESTMENT IN CHARGING INFRASTRUCTURES

Source: Cinco Días https://cincodias.elpais.com/cincodias/2017/04/21/companias/1492777826_740308.html (April 2017)

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017)

Infrastructure requirements are huge and their returns uncertain

33U N C E RTA I N T I E S

H U G E I N V E S T M E N T I N B AT T E R Y FA C T O R I E S

Battery factories investment

requirements are huge

Tesla in 2013 said…:

Source: Wood Mackenzie, June 17

https://www.greentechmedia.com/articles/read/10-battery-gigafactories-are-now-in-progress-

and-musk-may-add-4-more#gs.em7MLmw

34U N C E RTA I N T I E S

REAL EMISSIONS

Source: Motor.es, July 2017.

Source: Expansión, 11/11/2017. Source: Union of Concerned Scientists.

EV do produce pollution but studies show that they do far less

than equivalent ICE vehicles

35U N C E RTA I N T I E S

P R O F I TA B I L I T Y I N R I S K

Source: Automotive News

Source: El Mundo

EV needs volume to be

profitable

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown – Disruption Ahead? (May 2017)

36U N C E RTA I N T I E S

D I V E R S I F I E D W O R L D : E V S A L E S D ATA I N 2 0 1 6

Source: Movilidad Eléctrica; datos de ventas de vehículos eléctricos e híbridos

The majority of worldwide sales of EV are concentrated in China and Europe,

followed by the US

37U N C E RTA I N T I E S

DIVERSIFIED WORLD

Electrification is expected to occur

in the first place in China and

Europe – as well as US if Trump is

successor is “greener”. The rest of

the world will probably take longer

due to the fact that they have less

US buyers were expected to

incentives (governmental switch to smaller cars but

legislation, subsidies, etc.). low fuel prices have stopped

the trend:

38

Source: UBS Report - Q-Series UBS Evidence Lab Electric Car Teardown –

Disruption Ahead? (May 2017)6) Other Trends

Diesel &

Autonomous Car

39D I E S E L V E H I C L ES

C O M M U N I C AT I N G V E S S E L S

There is a clear trend to decrease Diesel engine,

demand is falling. So far, Diesel and Gasoline

volumes are communicating vessels

Headline of the news Body of the news

40D I E S E L V E H I C L ES

FORECASTS 2025

Faurecia IHS Roland Berger

ICE BEV ICE BEV

BEV ICE Diesel

Diesel 4% Diesel 7%

7% 15%

12% (P)HEV 12%

(P)HEV 23% HEV

24% 25%

ICE ICE

ICE

Gasoline Gasoline

Gasoline

57% 56%

58%

Source: Faurecia Investor’s Day, June 2017. Source: IHS 2017. Source: Faurecia Investor’s Day, June 2017.

*Abbreviations:

ICE: Internal Combustion Engine (operates on fuel).

HEV: Hybrid Electric Vehicle (operates on ICE plus an assisting battery charged by braking energy for short distances).

PHEV: Plug-in Hybrid Electric Vehicle (same as HEV but battery can be charged by plugging).

BEV: Battery Electric Vehicle (fully operates on battery electric power).

41D I E S E L V E H I C L ES

ICE IS ALSO MOVING

Source: Automotive Engineering, October 2017.

The perfect mix between the advantages of the

diesel and gasoline engines

42AU TO N O M O U S V E H I C L E

Source: ACEA (European Automobile Manufacturers Association).

Autonomous vehicle could even become a more

effective way of emission reduction than EV

43AU TO N O M O U S V E H I C L E

Source: Bosch Innovation Day 2017

First step in the autonomous road map implies a drastic emissions reduction,

without added cost.

44AU TO N O M O U S V E H I C L E

Source: Prime Research, “Smart Efficiency and Digital Intelligence”.

Entry of new players coming from software sector is not so clear as some sources

expects. Automotive sector has already a high content of software developments

457) CIE Automotive:

constant adaptation

46C I E SA L E S P I E BY V E H I C L E A R EA C I E G RO U P

Structural Parts,

Chassis &

Drivetrain Suspension

25% 28%

Interior &

Engine & Exterior Trim

Gearbox 22%

25%

Includes MHCV, Two-wheeler and

Tractors.

Different pace in different geographies.

Small yearly commercial effort (2%).

47C I E SA L E S P I E BY V E H I C L E A R EA M A H I N D R A C I E

Powertrain

24% Includes Two-wheelers.

Comm Vehicles & Different pace in

different geographies.

Tractors

52%

Interior & Drivetrain

Exterior Trim 17%

1%

Structure &

Chassis

6%

48P OT E N T I A L E L EC T R I F I C AT I O N E F F EC T S O N C I E

Powertrain

Components Additional

Outsourcing

Gearbox

New components for new

Components

ICE engine generations

New components for new

ICE gearbox generations

New components

for (P)HEV

New components

for BEV

Market

49O P P O RT U N I T I E S

ADDITIONAL OUTSOURCING

Source: Breakthrough of electric vehicle threatens European car industry by ING Economics Department, July 2017

New developments and technologies (EV, batteries, connectivity, autonomous,…)

will need an enormous effort from OEM and main Tier1 (resources and Capex).

Traditional technologies could be outsource to reduce efforts

50A L R EA DY T H E R E

ALREADY IN SERIAL PRODUCTION

OEMs and Tier1 Technologies

Renault Stamping

Nissan Plastic

Tesla Aluminium & Machining

M&M Reva Forging

Borg Warner

CIE Automotive is already working with

the key players

51A L R EA DY T H E R E

R E N A U LT

Platine assembles

Aluminium

Battery support

Aluminium

End plate

Aluminium

52A L R EA DY T H E R E

R E N A U LT

Battery structure

Metal stamping Winding hub

Metal stamping

Carter battery charger cover

Metal stamping

Lower carter battery cover

Metal stamping

Upper carter battery cover

Metal stamping

53A L R EA DY T H E R E

NISSAN

e-Reducer Housing Clutch

Aluminium

e-Reducer Housing Trans Case

Aluminium

54A L R EA DY T H E R E

TESLA

Aluminium battery cover

Stamping & welding

Corners (BIW) Skid plate (BIW)

Stamping & welding Stamping & ecoat (painting)

Floor (battery parts)

Stamping, riveting, welding & painting

Wall (battery parts) Cross member (battery parts)

Stamping & riveting Stamping & welding

55A L R EA DY T H E R E

M &M R E VA

Rear spindle

Forging

Battery pack

Composites

56A L R EA DY T H E R E

BORG WARNER

Source: Autogreen Magazine

Rotor components

Forging and machining

57A L R EA DY T H E R E

I N T E G R AT E D F R O M V E R Y E A R LY S TA G E S

Diversity of partners & new players

Working with OEMs, Tier 1 in electric motors, electronics, Technological Centres,

and Universities in R&D projects.

58A L R EA DY T H E R E

I N T E G R AT E D F R O M V E R Y E A R LY S TA G E S

Analysing different type of architectures

Multi-technological environment

59A L R EA DY T H E R E

REAL EXAMPLES

Demonstration in real car

R&D projects involving customers.

Integrated in a ZOE vehicle.

Tested in Renault test circuit at

Paris.

Exceeding the requirements.

60O P P O RT U N I T I E S

N AT U R A L E V O L U T I O N

Some components could have direct substitute in the new powertrains

ICE component EV component

61O P P O RT U N I T I E S

N E W PA R T S

Inverter (DC/AC) Motor controller

Source: Renault

Source: Toyota (Prius 3rd Gen) Source: Delphi

Converter (DC/AC) Charger

Source: EV-Guide (Delphi 2,2 kW) Source: Delphi

62O P P O RT U N I T I E S

N E W PA R T S

Battery module

Source: Green Car Congress 2017. Audi A3

63O P P O RT U N I T I E S

N E W PA R T S

Battery cells stacking Battery module. Metal

Source: Automotive Energy Supplier Corporation

Source: Toyota

Battery module. Plastic

Running project at CIE

Examples

Source: KIA

64O P P O RT U N I T I E S

N E W PA R T S

Battery cooling

Charging port

Source: EV-Guide

Charging port

Source: Green Car Congress 2017. Audi A3

Source: Delphi

65Managing high

value added

processes

66You can also read