European Equities Opportunities for stock pickers in the age of COVID - June 2020 - MondoAlternative

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investment Week Select Conference

June 2020

European Equities

Opportunities for stock pickers in the age of COVID

Ben Ritchie, Head of European Equities

For Professional Investors Only – Not for public distribution

AS SICAV I - European Equity Fund – portfolio construction group

Clear accountability within a team framework

Sanjeet Mangat Ben Ritchie Jonathan Allison Rosie French

Investment Director Head of European Investment Director ESG Analyst

Equities

• The AS SICAV I - European Equity Fund has been managed by Ben Ritchie, Sanjeet Mangat, and Jonathan Allison since

September 2015

• ESG input to portfolio construction from Rosie French

Source: Aberdeen Standard Investments June 2020

2

AS SICAV I - European Equity Fund

Differentiated investing

• Highly selective strategy focused on the best companies in Europe

Strategy • A true best ideas portfolio aiming to prosper through the cycle

• Bottom-up stock picking with an absolute return mind set

• Idea generation across the market cap spectrum

• Proprietary fundamental research is the cornerstone of the investment process

Execution • High conviction, concentrated portfolio of c.30 stocks

• Implied returns hurdle rate ensures valuation discipline

• Thinking like asset owners with a long-term approach and active engagement

• High active share, high tracking error, and low turnover

Outcome • Attractive upside (110%) and downside capture (70%) drives risk adjusted returns

• Top decile versus peers over 1, 3 and 5 years*

Source: Aberdeen Standard Investments, * Morningstar, Lipper, March 2020. Past performance is not a guide to future results

3AS SICAV I - European Equity Fund – portfolio characteristics

Differentiated Investing

Active 30 83% 5.3%

holdings active share tracking error

Selective 9% 27% 0.8

historic 3yr EPS growth average 5 year ROE debt / equity

vs 6% benchmark vs 19% benchmark vs 1.1 benchmark

Differentiated 110% 70% 38%

upside capture downside capture €3 – 20bn market cap

Source: Aberdeen Standard Investments, Morningstar, 31 March 2020. Past performance is not a guide to future results.

4Aberdeen Standard SICAV I - European Equity Fund performance

Delivering consistently strong performance for clients

YTD 2020 % Q1 2020% 1 Year % 2 Years % p.a. 3 Years % p.a. 4 Years % p.a. 5 Years % p.a. 10 Years %

p.a.

Aberdeen Standard SICAV I

-1.97 -14.09 10.39 8.81 8.33 10.48 4.88 9.55

- European Equity Fund

FTSE World Europe -14.98 -22.71 -3.43 -1.89 -0.74 3.29 0.38 6.77

Arithmetic Relative +13.01 +8.62 +13.81 +10.70 +9.07 +7.19 +4.50 +2.79

Top decile

Percentile Ranking Top decile (4th) Top decile (3rd) Top decile (1st) Top decile (1st) Top decile (1st) Top decile (3rd) Top decile (5th)

(2nd)

2019 % 2018 % 2017 % 2016 %

Aberdeen Standard SICAV I - European Equity Fund 36.77 -6.92 13.61 3.78

FTSE World Europe 26.88 -10.39 11.38 3.15

Arithmetic Relative +9.88 +3.47 +2.22 +0.62

Percentile Ranking Top decile (2nd) Top decile (5th) Top quartile (12th) Second quartile (50th)

Percentile ranking is vs EAA OE Europe Large-Cap Blend Equity

Source: Morningstar Direct, Aberdeen Standard Investments, gross of fees performance in EUR, 31 May 2020. Performance is shown gross of fees and does not reflect investment management fees. Had

such fees been deducted, returns would have been lower. Past performance is not a guide to future results.

5Quality in a long term context – high ROE and low beta

Companies with a low beta and those with higher returns have performed well

High beta names are back to the price levels seen High RoE underperformed between 03 and 07 – this

in the Eurocrisis changed drastically in the GFC

600 1,500 200

1,300

500

175

1,100

400

150

900

300

700

125

200

500

100

100

300

0 100 75

88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Europe High Beta Performance High/Low RoE Performance

Europe Low Beta Performance (rhs)

Source: UBS European Equity Strategy, Thomson Reuters Datastream, FTSE. Source: UBS European Equity Strategy, Thomson Reuters Datastream, FTSE, IBES. For

For illustrative purposes only. Past performance is not a guide to future results. illustrative purposes only. Past performance is not a guide to future results.

6Quality in a long term context – low leverage

Companies with strong balance sheets have also outperformed

Since GFC low leverage has strongly outperformed in Europe

450

400

350

300

250

200

150

100

50

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Low/High Net Debt to Equity Performance

Source: UBS European Equity Strategy, Thomson Reuters Datastream, FTSE, WorldScope. For illustrative purposes only. Past performance is not a guide to future results.

7Sustainable growth is increasingly scarce

Companies with those characteristics deserve a premium

Very few companies have high projected sales growth

STOXX Europe 600 – % companies by sales growth band

60%

50%

40%

30%

20%

10%

0%

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Low growth (8%)

Source: Thomson Reuters Datastream, I/B/E/S, Goldman Sachs Global Investment Research, December 2019. For illustrative purposes only.

8Outlook much more compelling than European GDP

Portfolio growth underpinned by powerful structural drivers

Digitisation of Industry Changing Demographics Consumer Trends

Source: © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate the investment management style described herein and

not as an investment recommendation or indication of future performance

9Our portfolio companies have better growth potential

Higher, more predictable growth supports higher multiples

• European nominal GDP growth rates of c. 3.2% p.a. compared to portfolio FCF growth of 8.4% p.a. and net income growth 10% p.a. over the

period from 2002

• Since 2010 European equities have grown earnings at less than 2% per annum

• Expect earnings growth around 10ppts better than the market in 2020

European GDP (EUR m) FCF (EUR m) - ex financials Net Income (EUR m)

500

450

400

350

300

250

200

150

100

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: Aberdeen Standard Investments, BAML, Bloomberg, January 2020. Past performance is not a guide to future results

10Europe is a leader in ESG

ESG integrated strategies have outperformed and we are well positioned

European companies have persistently higher ESG scores Performance of ESG Integration Strategies across regions

7.0

140

Average of the MSCI Overall ESG score

6.5

6.0 130

Index of excess returns

5.5 120

5.0

110

4.5

100

4.0

90

3.5

3.0 80

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2014

2015

2016

2017

2018

2019

2020

Europe USA EM Europe USA Asia Ex Japan

Japan GEM

Source: MSCI ESG Research LLC, BofA Merrill Lynch European Equity Quant Strategy; Source: J.P. Morgan QDS, MSCI ESG Research LLC, Arabesque, RepRisk, November 2019.

November 2019. For illustrative purposes only. For illustrative purposes only.

11Equities remain compelling value relative to bonds

Yield spread at historic levels

Equities have a substantial yield ‘cushion’ Equity valuations remain at a 100y low versus bonds

German 10y treasury yield and cash yield (dividend yield and

buyback yield)

10 600

MSCI Europe - Dividend Yield - Bond Yield

400

8

200

6

0

4 -200

-400

2

-600

0

-800

-2 -1,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 1923 1933 1943 1953 1963 1973 1983 1993 2003 2013

Europe cash yield Germany 10y bond yield DY - BY Median

Source: MSCI, Global Financial Data, Thomson Reuters Datastream, Morgan Stanley

Source: Bloomberg, Thomson Reuters Datastream, Worldscope, Goldman Sachs Global Research.Note: Government bond yield uses market cap weighted average of European

Investment Research December 2019. For illustrative purposes only. country 10y bond yields. January 2020. For illustrative purposes only.

12If low growth, low inflation and low interest rates persist?

Quality outperformance may be secular rather than cyclical

‘Growth defensives’ outperform in Europe and Japan

Time 0 = 4Q 1990 Japan, 3Q 2008 Europe

25

0 Consumer Staples +

Healthcare relative

20 performance

0

15

0

10

0

50

0

-3 0 3 6 9 12 15 18 21 24 27

Years from first negative in earnings growth

Europe (‘08) Japan (‘90)

Source: Thomson Reuters Datastream, Worldscope, Goldman Sachs Global Investment Research, 30 September 2019. For illustrative purposes only Past performance is not a guide to future

results..

13Outlook • Coronavirus will have a significant impact on the global economy and corporate earnings will take a major hit in 2020 • Our emphasis is on making sure our companies can trade through this period with as little equity dilution and franchise damage as possible • We have taken advantage of selective opportunities to invest capital at attractive potential returns • Portfolios have performed well during this period in both falling and rising markets • In the short term the most distressed companies will likely lead any rally • But over the medium to long term we believe such an environment favours a focus on quality companies which can offer both resilience to volatility and participate in the available growth opportunities • The powerful structural growth drivers which underpin the portfolio are only likely to accelerate as a result of this event • In particular the Social and Environmental focus of ESG is also likely to intensify and we are well positioned to manage associated risks and take advantage of opportunities that arise Source: Aberdeen Standard Investments, June 2020 14

Appendices

Equities: What makes us different

Collaborative culture strengthens our investment decision making

• Global research platform delivers actionable investment c.150 investment professionals 4,000 monitored stocks

insights through rigorous fundamental research 11 countries, 14 offices >6,000 company engagements

• Embedded ESG analysis and active stewardship enhances

risk-adjusted returns

• Collaboration and team debate strengthens stock insights,

builds conviction and enhances portfolio construction

23%

17%

• Truly active equity investing targets strong returns across a

broad range of client outcomes

Equity AuM 10%

€140.8 billion

25% 9%

6%

4% 6%

High Active Income

Responsible Investing Small Cap

An exchange rate of £1:€1.18018 has been used

Please note that Small Cap is Focus on Change and Long Term Quality (LTQ) is managed within the regional teams. Source: Aberdeen Standard Investments, 31 December 2019

16ASI active equity team

Local insights, global perspectives

Devan Kaloo

Global Head of Equities

Boo Siew Yan Stuart Ives

Mark Vincent

Global Head of Business Global Head of Business

Global Head of Research

Operations Strategic Development

Ralph Bassett Andrew Paisley

Dominic Byrne Flavia Cheong Devan Kaloo Andrew Millington Ben Ritchie

Head of North Head of Smaller

Head of Global Head of Asia Head of GEM Head of UK Head of Europe

America Companies

Kwok Chern-Yeh Joanne Irvine Brian Fox Lesley Duncan Will James Abby Glennie

Deputy Head Deputy Head Deputy Head Deputy Head Deputy Head Deputy Head

Edinburgh

12 investors

Tokyo London Boston Edinburgh

London Edinburgh Edinburgh 8 investors

1 Investor 6 investors 15 investors 7 investors 10 investors 7 investors

Boston Singapore São Paulo Philadelphia

15 investors London London

2 investors 5 investors 10 investors 5 investors 8 investors

New York Sydney

1 investor 8 investors

Singapore Bangkok

1 Investor 3 investors

Kuala Lumpur ESG Cross-Asset Class Team

6 investors Equity Dealing (24) Equity Investment specialists (11)

(c.20)

China/Hong Kong

8 investors

Jakarta ESG on-desk analysts (8) Equity quants (11) Investment support (35)

4 investors

* Regional numbers include head of desk, deputy head, fund managers and embedded ESG personnel

Includes affiliated persons operating under inter-company agreement. Source: Aberdeen Standard Investments, 31 March 2020

17European Equities at ASI

Research-driven, high conviction active investing in Europe

Why ASI for European Equities European Equities Franchise Why European Equities

• Well-resourced, experienced, • High Active • Europe is an attractive market for

dynamic team active stock pickers

• Long Term Quality

• World class proprietary research • Complex and misunderstood

platform • Focus on Change

• Environmental, Social, and

• ESG at the heart of our investment • Income Governance (ESG) leadership

process

• Income • International expertise

• Supporting a comprehensive suite

of highly active products • Defensive Income • Idiosyncratic, Income and Quality

opportunities

• Responsible Investing

• Ethical

A team with best in class Delivering differentiated Compelling investment

capabilities outcomes opportunities

18European Equities team

Well-resourced, experienced and dynamic team

Ben Ritchie Will James Kay Eyre Jonathan Fearon Jonathan Allison Tom Dorner Sanjeet Mangat Ian Hewett

Head of European Deputy Head of Senior Investment Investment Director Investment Director Investment Director Investment Director Investment Director

Equities European Equities Director (19/14) (17/15) (14/5) (13/13) (13/13)

(18/18) (18/13) (35/24) Banks, Diversified Media, Travel, Insurance Real Estate Luxury Goods,

Autos Chemicals Construction Finanials Ingredients Telecoms

Kurt Cruickshank Sarah Norris Stuart Brown Roseanna Ivory Jamie Mills O’Brien Sasha Kachanova Rosie French

Investment Director Investment Director Investment Director Investment Manager Investment Manager Investment Analyst ESG Analyst

(12/12) (9/9) (7/7) (5/5) (5/5) (4/4) (4/4)

Aerospace, Industrials, Healthcare, Pharma, Industrials, Utilities Consumer Staples, Tech Hardware, Household Goods, Pulp & Paper

Support Services Payments Transport, Metals Internet, Energy, Retail, Infrastructure

Software

Equity Dealing (24) Global ESG (20) Investment Support (36) Research Quant (11) Equity Investment specialists (11)

Years of experience (Industry / ASI)

Source: Aberdeen Standard Investments, 31 March 2020

19Equity research underpins our strategy

Fundamental, focused and insightful

Stock Research Note

Foundations

• Business fundamentals

Broad universe and proactive Deep company level analysis Conviction developed through • Evaluation of ESG risks and

opportunities

engagement delivers investment insights rigorous team debate

Dynamics

• Proprietary research platform • Globally consistent approach • Informed peer review of

providing deep company level and common language delivers research builds conviction • Key drivers of business change

insights actionable insights that influence corporate value

• Broad team company knowledge

• Broad and dynamic opportunity • ESG analysis fully embedded in strengthened through effective

set; quant tools support and all our company assessments team discussion Financials and valuation

refine coverage • Financial analysis and

• Sector analysis provides deeper • Clear team and individual

• Outstanding corporate access understanding of companies responsibilities ensure assessment of market

and engagement collaboration and accountability expectations

Investment Insight

• Investment thesis and non-

consensus insight; risk factors &

downside scenarios

Source: Aberdeen Standard Investments, 31 March 2020

20European Equities investment process

Accountability and performance evaluated at each stage of the process

Idea generation Research Peer review Portfolio construction

Europe inc UK universe >800 stocks c.700 stocks with full coverage inc UK Inc UK c.200 buy rated stocks

Europe ex UK universe > 500 stocks c.300 stocks with full coverage ex UK Ex UK c.100 buy rated stocks

Broad Universe Deep Analysis Rigorous Team Debate Focused on Client Outcomes

• Wide & dynamic opportunity set • Common investment language • Informed peer review of insights • Pods drive clear accountability

• Quant tools refine coverage • Fully embedded ESG • Collaboration on sectors & themes • Bottom up, best ideas led

• Outstanding corporate access • Clear non-consensus insights • Cross asset class insights • Quant and risk analytics

• Deep sector expertise • Continuous review of outputs • Winners list ranks ideas • Effective diversification

ESG considerations embedded throughout the process

Comprehensive independent oversight of investment process and client mandate parameters

21We focus on the best businesses in Europe

A highly selective approach

Why does Quality Investing Work?

The market consistently underestimates the sustainability of returns from high quality companies:

• Quality companies have fewer tail risks and a greater margin of safety

• Quality companies produce less volatile earnings streams – earnings are more resilient and predictable

• Quality companies can better navigate an uncertain future and capitalise on opportunities to create value

What do we mean by Quality? Every company graded on 5 factors:

Sustainable

1. Durability of the business model and moat ESG competitive

advantage

2. Attractiveness of the industry

3. Strength of financials Management

Predictable

execution and

4. Capability of management growth

track record

5. Assessment of ESG risks

Quality

Balance Attractive

Approximately 15% of the European market enters our universe sheet industry

strength characteristics

Returns hurdle rate ensures valuation discipline

Good returns Earnings

on capital resilience

Source: Aberdeen Standard Investments

22Aberdeen Standard SICAV I - European Equity Fund – top 10 holdings Emphasis on market leading franchises Company name Portfolio % Country Sector Market Leader ASML 5.1 Netherlands Technology Hardware and Equipment Semiconductor Manufacturing Novo-Nordisk 5.1 Denmark Health Care Diabetes Treatment Prosus 4.5 Netherlands Software and Computer Services Consumer Internet London Stock Exchange 4.4 UK Financial Services Institutional Financial Services Wolters Kluwer 4.3 Netherlands Media Information Analytics Deutsche Boerse 4.2 Germany Financial Services Financial Exchanges Nestlé 4.1 Switzerland Food Producers Food and Beverages Kerry Group 4.1 Ireland Food Producers Taste & Nutrition Ubisoft Entertainment 3.8 France Communication Services Video Games RELX 3.8 UK Media Information Analytics Companies selected for illustrative purposes only to demonstrate Aberdeen Standard Investment’s investment management style and not as an investment recommendation or indication of future performance. Source: Aberdeen Standard Investments, 31 May 2020 23

Aberdeen Standard SICAV I - European Equity Fund – sector / country allocation

A balanced proposition

Sector – Absolute Weights Sector – Relative Weights

Technology

Consumer Goods 23.2

Consumer Goods

Technology 22.4 Health Care

Consumer Services

Health Care 19.7

Basic Materials

Financials 11.9 Telecommunications

Industrials 10.7 Industrials

Utilities

Consumer Services 8.3

Financials

Basic Materials 3.7 Oil & Gas

0.0 5.0 10.0 15.0 20.0 25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0 15.0 20.0

Source: Aberdeen Standard Investments, excluding cash, 31 May 2020 Source: Aberdeen Standard Investments, excluding cash, 31 May 2020

Benchmark: FTSE World - Europe

Country – Absolute Weights Country – Relative Weights

Netherlands

UK 20.4 Ireland

Germany

Netherlands Denmark

18.8 Italy

Germany 17.7 Czech Republic

Greece

France 14.1 Hungary

Spain

Switzerland 9.7 Austria

Portugal

Denmark 5.2 Turkey

Poland

Ireland 4.2 Norway

3.8 Belgium

Italy France

Finland

Spain 3.7 Sweden

Sweden 2.4 Switzerland UK

0.0 5.0 10.0 15.0 20.0 25.0 -12.0 -7.0 -2.0 3.0 8.0 13.0 18.0

Source: Aberdeen Standard Investments, excluding cash, 31 May 2020

Source: Aberdeen Standard Investments, excluding cash, 31 May 2020 Benchmark: FTSE World - Europe

24AS SICAV I - European Equity Fund – portfolio activity Disciplined execution YTD to end May Additions Reductions Introductions Exits Source: Aberdeen Standard Investments. June 2020. © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or indication of future performance 25

Heineken

Global number one in premium beer

Foundations

• Highly consolidated industry at global and regional level

• Strong positions in markets where structures allow higher margins

• Competitive and reinvestment moats given scale and geography

Dynamics

• Premiumisation in evidence across almost every market

• Brand Heineken is growing at 2x rest of portfolio

• Low and no alcoholic trends driving higher margin Heineken 0.0

Financials & Valuation

• Consistent returns, always in excess of WACC

• Good cash generation through time given fairly low capital needs

• Valuation implies limited operating leverage and fading returns

Investment Insight

5% 40% 60% • Volume drivers and attractive premium mix underpin MSD growth

• Sustainability of revenue growth is underappreciated by the market

Heineken brand CAGR Profit from Premium Profit from Developing

over 15 years Brands Markets • Operating leverage to be supported by favourable geographic mix

Source: Heineken. Company selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or indication of future

performance. January 2020

26ASML

Market leading semiconductor equipment supplier

Foundations

• Cyclical industry but with attractive long-term structural growth

• Dominant share in lithography stage of semiconductor chip production

• R&D leadership confers pricing power and impressive earnings visibility

Dynamics

• Semiconductor cycle is recovering

• Lithography market entering EUV era where ASML is a monopolist

• Customers already committing to next generation technology

Financials & Valuation

• Net cash balance sheet reflects management conservatism

• Cash conversion is strong, due to asset-light model, and improving

• Valuation implies a conservative interpretation of 2025 guidance

Investment Insight

4.6% 8% 100% • Margins to exceed expectations through EUV ramp up and services mix

• Shareholder returns can accelerate supported by cash inflection

Lithography expenditure ASML revenue growth ASML EUV

CAGR 2018-2023 CAGR 2018-2023 market share • Earnings visibility is underappreciated in valuation

Source: ASML, SocGen. Forecasts are not guaranteed and actual events or results may differ materially

© ASML. Company selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or indication of future performance.

January 2020

27Hannover Re

Reinsurer with a significant cost advantage

Foundations

• Attractive industry in which share is moving to the market leaders

• Efficient allocation of resources provides a significant cost advantage

• Counter-cyclical use of reserve buffer provides more stable earnings

Dynamics

• Positive pricing momentum in the industry

• Turnaround of the Life business is on track

• P&C continues to deliver superior returns versus peers

Financials & Valuation

• Robust balance sheet and strongest reserve buffer in the peer group

• Solid actuarial control has led to lower exposure to large loss events

• Valuation implies returns remain strong, which is reasonable

Investment Insight

10% >8% 3% • Resolution to Life profitability offers upside to earnings estimates

• Positive price momentum and share gains drive attractive growth

Reserve buffer relative to Premium growth CAGR Higher ROE

market cap since 1995 than peers • Sustainability of that growth is underappreciated in the valuation

Source: Hannover Re, Kepler Chevreux. Company selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or

indication of future performance. January 2020

28AAlong

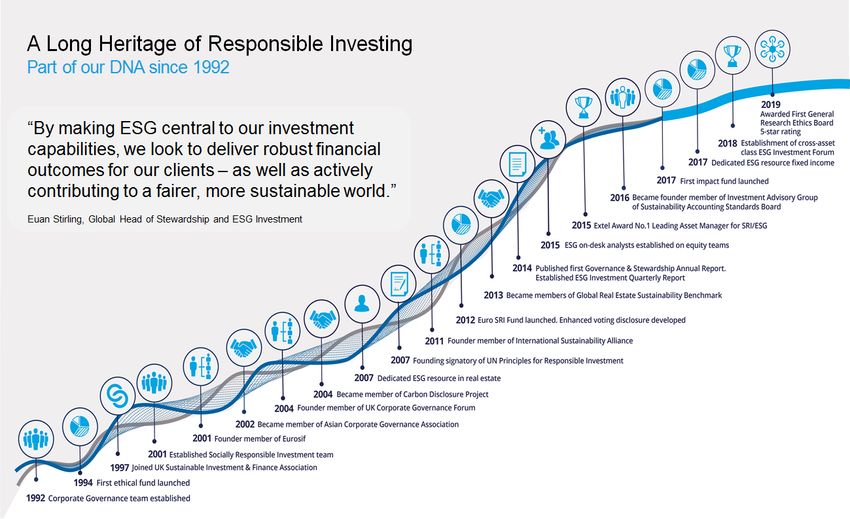

Longheritage

Heritageof of

responsible

Responsible

investing

Investing

Part

Part of

of ASI’s DNA

our DNA since

since 19921992

Source: Aberdeen Standard Investments, January 2020

29ESG investment purpose and philosophy

Our primary goal is to generate better long term outcomes for our clients

Equity Analysts On-desk ESG Specialists

ESG factors are financially material, and • ESG risk and opportunities • Regional ESG expertise on

defined in every stock note themes & sectors

impact corporate performance

• Company engagement • ESG focussed engagement

Understanding ESG risks and opportunities

alongside other financial metrics allows us

to make better investment decisions

Informed and constructive engagement

Central ESG capability

helps foster better companies, enhancing

the value of our clients’ investment • Research on ESG themes, event-driven

issues and global sectors

• Active stewardship on behalf of

shareholders by voting and engaging to

influence change

Source: Aberdeen Standard Investments, 31 March 2020

30ESG at the heart of our investment process

Fundamental ESG analysis drives engagement, voting and investment decision making

Proprietary ESG Ratings Full Integration

100% of companies under We have 20 years+ experience of

coverage are rated by our analysts integrating ESG factors into our

using internal ASI Equities ESG equity investment process. ESG is

ratings with lowest scoring now a core part of every company

companies excluded research note and sector review

Engaged Owners Active Voters

235 engagements on ESG topics in 884 European meetings voted in

2019, representing 33% of all 2019- 10% of votes were against

European company meetings. 56 management and 5% of votes

meetings were dedicated solely to differed from ISS Policy

ESG

Source: Aberdeen Standard Investment, May 20

31External fund ratings indicate greater exposure to ESG leaders than peers

Aberdeen Standard SICAV I - European Equity Fund

MSCI ESG Rating Distribution

MSCI ESG 35% 32%

Rating 29%

30%

26%

25%

AA 20%

15%

10%

9%

4%

5%

0% 0% 0%

0%

CCC B BB BBB A AA AAA Not

Rated

Quality Peer ESG

Score Percentile Leaders

7.8 46th 61%

Source: MSCI ESG Manager (April 2020 data)

32Fund carbon footprint

An alternative lens contributing to portfolio construction

Carbon intensity roughly half that of the benchmark Fund “owned“ emissions less than 15% of the benchmark

Aberdeen Standard SICAV I - European Equity Fund Aberdeen Standard SICAV I - European Equity Fund

FTSE World Europe Index FTSE World Europe Index

Scope 1 Scope 1

Portfolio Scope 2 Portfolio Scope 2

Scope 3 Scope 3

Benchmark Benchmark

0 100 200 300 0 25000 50000 75000 100000

tCO2e/$m revenue tCO2e

51.5% 11.6% 18,357

Carbon Footprint Relative Carbon Relative Apportioned Equivalent Cars Taken

Intensity Fund Emissions Off The Road

Source: Trucost, 2018; ASI-fund data as of 1st June 2020. Relative Carbon Intensity, Apportioned Total Emissions and Avoided Emissions metrics refer to scope 1, 2 & 3 emissions data. Cars taken off the

road are calculated as avoided emissions (84,446tCO2e) divided by 4.6t which is the annual CO2 emitted by an average passenger car doing 11,500m (EPA)

33How big is the coronavirus hit to Europe?

Widespread recessions amid an unprecedented decline in activity

Eurozone PMIs have fallen sharply… ...and we expect a deep contraction in Eurozone GDP

105

GDP q/q (LHS) Composite PMI (RHS)

2% 100

60

95

0%

50

90

-2% 40 85

30 80

-4%

20 75

Q1 2019

Q1 2020

Q1 2021

Q1 2022

-6%

10

Official baseline Pre-crisis trend

-8% 0 Deep reverse J V-shaped recovery

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

W-shaped recovery

Source: Haver, Aberdeen Standard Investments, April 2020 Source: Aberdeen Standard Investments, April 2020

34Impact on companies

Cyclical sectors most negatively affected

EPS of ‘Cyclical-Value’ companies have been The shift in earnings estimates is skewed towards

revised down Cyclical-Value sectors

Smart EPS revision STOXX Europe 600

0% EPS revisions in Q1-2020 (%)

0%

-10% -10%

-20%

-20%

-30%

-30% -40%

-50%

-40%

-60%

-70%

-50%

Technology

Retail

Industrial G&S

Health Care

Insurance

Real Estate

Food & Beverage

Media

STOXX Europe 600

Travel & Leisure

Construction & Mat

Auto & Parts

Oil & Gas

Telecoms

Utilities

Personal & HHG

Chemicals

Financial Services

Basic Resources

Banks

-60%

Cyclical

Defensive

Growth

Europe

Value

Commodities

Source: FactSet, MSCI, Goldman Sachs Global Investment Research Source: FactSet, Goldman Sachs Global Investment Research

35Aberdeen Standard SICAV I - European Equity Fund

Performance: 31 May 2020

Fund return % Reference index return % Difference %

Current month 6.10 3.31 +2.79

Last three months 3.50 -5.94 +9.45

Year to date -1.97 -14.98 +13.01

Annualised periods

1 year 10.39 -3.43 +13.81

3 years 8.33 -0.74 +9.07

5 years 4.88 0.38 +4.50

Since inception 9.05 7.73 +1.32

Cumulative periods

1 year 10.39 -3.43 +13.81

3 years 27.13 -2.21 +29.34

5 years 26.90 1.89 +25.01

Since inception 967.92 665.62 +302.30

Calendar years

2019 36.77 26.88 +9.88

2018 -6.92 -10.39 +3.47

2017 13.61 11.38 +2.22

2016 3.78 3.15 +0.62

2015 3.80 8.84 -5.04

Inception: 29 January 1993. Reference index: FTSE World Europe. Source: Aberdeen Standard Investments, Performance is shown gross of fees and does not reflect investment management fees. Had

such fees been deducted, returns would have been lower. Past performance is not a guide to future results

36Aberdeen Standard SICAV I - European Equity Fund

Country attribution: Twelve months to 31 May 2020

Portfolio Benchmark Currency Net management effects

Weight (%) Return (%) Weight (%) Return (%) Return (%) Currency Allocation Selection Total

Total 100.0 10.39 100.0 -3.43 0.18 0.04 1.93 11.83 13.81

Equities 97.6 10.70 100.0 -3.43 0.18 0.01 1.80 11.83 13.63

Austria -- -- 0.3 -23.94 0.00 0.01 0.07 -0.06 0.01

Belgium -- -- 1.4 -16.98 0.00 0.00 0.23 0.00 0.24

Czech Republic -- -- 0.1 -24.60 -4.04 0.00 0.02 0.00 0.02

Denmark 5.1 32.45 3.6 27.03 0.19 -0.02 0.54 0.25 0.76

Finland -- -- 2.1 3.85 0.00 0.01 -0.20 0.07 -0.12

France 13.8 -0.06 16.1 -7.10 0.00 0.00 0.09 1.11 1.20

Germany 17.3 24.50 14.4 -0.43 0.00 0.02 0.14 3.07 3.23

Greece -- -- 0.1 -25.68 0.00 0.00 0.04 0.00 0.04

Hungary -- -- 0.2 -18.98 -6.19 0.02 0.02 0.00 0.03

Ireland 4.1 7.56 0.4 -10.40 0.00 -0.00 -0.26 0.77 0.51

Italy 3.7 4.52 3.7 -7.73 0.00 0.00 0.08 0.42 0.50

Netherlands 18.3 12.07 6.6 7.86 0.00 0.01 1.20 0.97 2.18

Norway -- -- 1.0 -17.26 -9.78 0.13 0.04 0.00 0.17

Poland -- -- 0.5 -22.96 -3.89 0.02 0.09 0.00 0.12

Portugal -- -- 0.3 14.04 0.00 -0.00 -0.05 0.00 -0.05

Spain 3.6 -24.95 3.9 -19.63 0.00 0.00 0.17 -0.21 -0.04

Sweden 2.4 49.42 4.8 11.47 1.23 -0.03 -0.31 0.65 0.32

Switzerland 9.5 13.72 16.1 11.69 4.89 -0.22 -0.43 0.22 -0.44

Turkey -- -- 0.3 -5.37 -14.30 0.06 -0.06 0.00 0.00

UK 19.9 7.22 24.2 -13.20 -1.73 -0.01 0.38 4.56 4.93

Cash 2.4 -0.64 -- -- 0.00 0.04 0.14 0.00 0.18

Source: Aberdeen Standard Investments, BPSS, Thomson Reuters Datastream, EUR. Benchmark: FTSE World Europe. Performance is shown gross of fees and does not reflect investment management

fees. Had such fees been deducted, returns would have been lower. Past performance is not a guide to future results.

37Aberdeen Standard SICAV I - European Equity Fund

Sector attribution: Twelve months to 31 May 2020

Portfolio Benchmark Net management effects

Weight (%) Return (%) Weight (%) Return (%) Allocation Selection Total

Total 100.0 10.39 100.0 -3.43 7.71 6.11 13.82

Equities 97.6 10.70 100.0 -3.43 7.53 6.11 13.64

Oil & Gas 0.0 -- 5.3 -34.50 2.75 -0.18 2.57

Basic Materials 3.6 1.49 6.2 -0.88 0.15 -0.14 0.01

Industrials 10.5 17.50 14.5 -0.55 0.72 1.12 1.84

Consumer Goods 22.6 -2.71 19.0 -2.28 -0.08 0.05 -0.03

Health Care 19.2 22.93 17.3 25.06 -0.03 0.29 0.26

Consumer Services 8.1 5.22 6.1 -6.19 -0.73 1.57 0.84

Telecommunications 0.0 -- 3.1 -7.18 0.13 0.00 0.13

Utilities 0.0 -- 4.8 11.89 -0.68 0.00 -0.68

Financials 11.6 13.94 17.0 -20.29 4.09 1.99 6.09

Technology 21.9 14.66 6.7 15.67 1.19 1.42 2.61

Cash 2.4 -0.64 -- -- 0.18 0.00 0.18

Source: Aberdeen Standard Investments, Benchmark: FTSE World Europe. Performance is shown gross of fees and does not reflect investment management fees. Had such fees been deducted, returns

would have been lower. Past performance is not a guide to future results.

38Discrete performance 1 Year to 31 May (net of fees) Aberdeen Standard SICAV I - European Equity Fund Year ended 31 May (%) 2020 2019 2018 2017 2016 Fund 10.01 4.40 5.30 14.90 -16.57 Benchmark -3.43 -0.33 1.60 16.41 -10.49 Source: Lipper. Basis: Share Class A Acc Total Return, NAV to NAV, net of annual charges, gross Income reinvested, (EUR). Benchmark FTSE World Europe The comparator shown may be used for risk monitoring and portfolio construction purposes, as well as to provide a performance comparator; it is not an integral part of the Objective and Investment Policy for the fund and should not be considered as such. All return data includes investment management fees, performance fees, and operational charges and expenses, and assumes the reinvestment of all distributions. The returns provided do not reflect the initial sales charge and, if included, the performance shown would be lower. Source: Aberdeen Standard Investments, 31 May 2020. Past performance is not a guide to future results 39

Aberdeen Standard SICAV I - European Equity Fund The following risk factors should be considered prior to making an investment decision Investment Objective The Fund aims to achieve a combination of growth and income by investing in companies listed on stock markets across Europe. The Fund aims to outperform the FTSE World Europe Index (EUR) benchmark before charges. Investment Policy Portfolio Securities The Fund invests mostly in equities and equity related securities of companies based, or carrying out much of their business in Europe. Management Process The Fund is actively managed. The benchmark is used as a reference point for portfolio construction and as a basis for setting risk constraints. In order to achieve its objective, the Fund will take positions whose weightings diverge from the benchmark and may invest in securities which are not included in the benchmark. The investments of the Fund may deviate significantly from the components and their weightings in the benchmark. Due to the active nature of the management process, the Fund's performance profile may deviate significantly from that of the benchmark over the longer term. Derivatives and Techniques Derivatives will only be used for hedging or to provide exposures that could be achieved through investment in the assets in which the Fund is primarily invested. Usage of derivatives is monitored to ensure that the Fund is not exposed to excessive or unintended risks. Investors in the fund may buy and sell shares on any dealing day (as defined in the Prospectus). If you invest in income shares, income from investments in the fund will be paid out to you. If you invest in accumulation shares, income will be added to the value of your shares. Recommendation: the fund may not be appropriate for investors who plan to withdraw their money within five years. Investors should satisfy themselves that their attitude to risk aligns with the risk profile of this fund before investing. 40

Aberdeen Standard SICAV I - European Equity Fund The following risk factors should be considered prior to making an investment decision Risk and reward profile This indicator reflects the volatility of the fund's share price over the last five years which in turn reflects the volatility of the underlying assets in which the fund invests. Historical data may not be a reliable indication for the future. The current rating is not guaranteed and may change if the volatility of the assets in which the fund invests changes. The lowest rating does not mean risk free. The fund is rated as 5 because of the extent to which the following risk factors apply: • The use of derivatives carries the risk of reduced liquidity, substantial loss and increased volatility in adverse market conditions, such as a failure amongst market participants. The use of derivatives may result in the fund being leveraged (where market exposure and thus the potential for loss by the fund exceeds the amount it has invested) and in these market conditions the effect of leverage will be to magnify losses. • The fund invests in equity and equity related securities. These are sensitive to variations in the stock markets which can be volatile and change substantially in short periods of time. All investment involves risk. This fund offers no guarantee against loss or that the fund's objective will be attained. The price of assets and the income from them may go down as well as up and cannot be guaranteed; an investor may receive back less than their original investment. Inflation reduces the buying power of your investment and income. The value of assets held in the fund may rise and fall as a result of exchange rate fluctuations. The fund could lose money if an entity (counterparty) with which it does business becomes unwilling or unable to honour its obligations to the fund. In extreme market conditions some securities may become hard to value or sell at a desired price. This could affect the fund's ability to meet redemptions in a timely manner. The fund could lose money as the result of a failure or delay in operational processes and systems including but not limited to third party providers failing or going into administration. Where the share class is described as "hedged", currency hedging techniques are used to provide you with a return that is close to the performance of the Fund in its base currency. Hedging will reduce, but not eliminate, the effect of exchange rate movements between the base currency of the Fund and the currency of the share class. The currency exposure being hedged is not necessarily related to the currency positions within the Fund's investment portfolio. Hedging will give rise to additional risks and costs. 41

For professional clients only Not for public distribution Past performance is not a guide to future results. The value of investments, and the income from them, can go down as well as up and clients may get back less than the amount invested. The views expressed in this presentation should not be construed as advice or an investment recommendation on how to construct a portfolio or whether to buy, retain or sell a particular investment. The information contained in the presentation is for exclusive use by professional customers/eligible counterparties (ECPs) and not the general public. The information is being given only to those persons who have received this document directly from Aberdeen Asset Managers Limited or Standard Life Investments Limited (together “Aberdeen Standard Investments”) and must not be acted or relied upon by persons receiving a copy of this document other than directly from Aberdeen Standard Investments. No part of this document may be copied or duplicated in any form or by any means or redistributed without the written consent of Aberdeen Standard Investments. The information contained herein including any expressions of opinion or forecast have been obtained from or is based upon sources believed by us to be reliable but is not guaranteed as to the accuracy or completeness. No information, opinions or data in this document constitute investment, legal, tax or other advice and are not to be relied upon in making an investment or other decision. Subscriptions for shares in the Fund may only be made on the basis of the latest prospectus, relevant Key Investor Information Document (KIID). These can be obtained free of charge from Aberdeen Standard Investments, 1 George Street, Edinburgh, EH2 2LL, Scotland and are also available on www.aberdeenstandard.com FTSE International Limited (‘FTSE’) © FTSE 2020. ‘FTSE®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under licence. RAFI® is a registered trademark of Research Affiliates, LLC. All rights in the FTSE indices and / or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. 42

For professional clients only Not for public distribution The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from marketing) any kind of investment decision and may not be relied on as such. Historical data and analysis, should not be taken as an indication or guarantee of any future performance analysis forecast or prediction. The MSCI information is provided on an ‘as is’ basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the ‘MSCI’ Parties) expressly disclaims all warranties (including without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages (www.msci.com). © 2020 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. For more detailed information about Morningstar's Analyst Rating, including its methodology, please go to: http://corporate.morningstar.com/us/documents/MethodologyDocuments/AnalystRatingforFundsMethodology.pdf The Morningstar Analyst Rating for Funds is a forward-looking analysis of a fund. Morningstar has identified five key areas crucial to predicting the future success of a fund: People, Parent, Process, Performance, and Price. The pillars are used in determining the Morningstar Analyst Rating for a fund. Morningstar Analyst Ratings are assigned on a five-tier scale running from Gold to Negative. The top three ratings, Gold, Silver, and Bronze, all indicate that our analysts think highly of a fund; the difference between them corresponds to differences in the level of analyst conviction in a fund’s ability to outperform its benchmark and peers through time, within the context of the level of risk taken over the long term. Neutral represents funds in which our analysts don’t have a strong positive or negative conviction over the long term and Negative represents funds that possess at least one flaw that our analysts believe is likely to significantly hamper future performance over the long term. Long term is defined as a full market cycle or at least five years. Past performance of a security may or may not be sustained in future and is no indication of future performance. For detailed information about the Morningstar Analyst Rating for Funds, please visit http://global.morningstar.com/managerdisclosures 43

For professional clients only

Not for public distribution

Aberdeen Standard SICAV I is a Luxembourg-domiciled UCITS fund, incorporated as a Société Anonyme and organized as a Société d’Invetissement á

Capital Variable (a “SICAV”). The information contained in this marketing document is intended to be of general interest only and should not be considered

as an offer, or solicitation, to deal in the shares of any securities or financial instruments. Aberdeen Standard SICAV I has been authorized for public sale in

certain jurisdictions and private placement exemptions may be available in others. It is not intended for distribution or use by any person or entity that is a

citizen or resident of or located in any jurisdiction where such distribution, publication or use would be prohibited. Before investing, investors should consider

carefully the investment objective, risks, charges, and expenses of a fund. This and other important information is contained in the prospectus, which can be

obtained from a financial advisor and are also available on www.aberdeenstandard.com. Prospective investors should read the prospectus carefully before

investing. Subscriptions for shares in the Fund may only be made on the basis of the latest prospectus and relevant Key Investor Information Document

(KIID) which provides additional information as well as the risks of investing and may be obtained free of charge from Aberdeen Asset Managers Limited, 10

Queens Terrace, Aberdeen, AB10 1XL, Scotland and are also available on www.aberdeenstandard.com.

Any data contained herein which is attributed to a third party ("Third Party Data") is the property of (a) third party supplier(s) (the “Owner”) and is licensed for

use by Standard Life Aberdeen*. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate,

complete or timely. To the extent permitted by applicable law, none of the Owner, Standard Life Aberdeen* or any other third party (including any third party

involved in providing and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Neither the

Owner nor any other third party sponsors, endorses or promotes the fund or product to which Third Party Data relates.

Standard Life Aberdeen means the relevant member of Standard Life Aberdeen group, being Standard Life Aberdeen plc together with its subsidiaries,

subsidiary undertakings and associated companies (whether direct or indirect) from time to time.

Issued by Aberdeen Standard Investments Luxembourg S.A.

” Aberdeen Standard Investments Luxembourg S.A. 35a Avenue J.F. Kennedy, L-1855 Luxembourg. No. S00000822. Authorised in Luxembourg and

regulated by CSSF.

GB-120620-119233-2

44You can also read