Europe's answer to the US tech giants? Find it in your favourite bag! - July 2021 - SW ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

July 2021

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Europe’s answer to the US tech giants?

Find it in your favourite bag!

It is hard to imagine a traditional European industry matching the fabulous performance

Piers Nestler of the US tech giants. Welcome to personal luxury goods stocks, some of which have been

Investment Analyst the most brilliant stars in the investment universe. This has been especially true of the three

French heavyweights, Hermès, Kering (which we have held for the past five years) and LVMH.

These now account for over a quarter of the global personal luxury goods market, with the early

Covid‑induced fall of 20% in demand for luxury goods no more than a blip in the relentless

uptrend of their share prices as the leading brands managed to gain further market share.

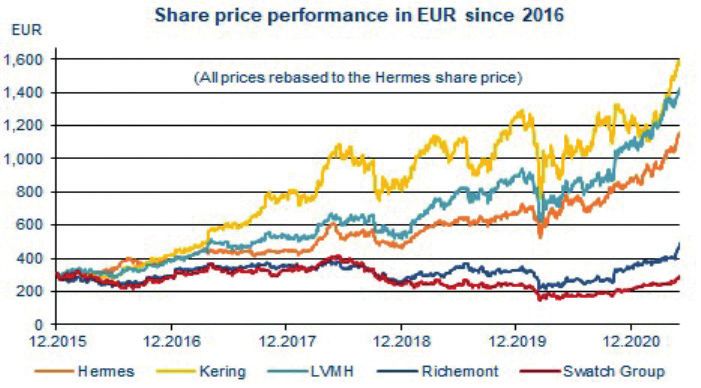

In the space of just five years, the share prices of the three French luxury players have tripled or

quadrupled. This is not far short of FAANG-style performance.

This came against a background of outstanding operating results. Growth has been spurred by

the irrepressible spending power of Chinese shoppers, by new categories – such as high-end

sneakers and casualwear – and by lower opening price points for luxury goods. Even more

impressive, perhaps, has been the expansion of the valuation multiples of these soft-luxury

producers, with investors rewarding growth stocks with hefty premiums, seemingly appreciating

their shares just as much as the products they sell. This contrasts with the hard-luxury segment

represented by the watch and jewellery groups Richemont and Swatch (the latter a position

Piers is an Investment Analyst at recently added to our portfolios), which has been trailing in every respect, especially since the

S. W. Mitchell Capital, with a particular dramatic change in their fortunes following the anti-corruption measures in China in the first

focus on Continental Europe, especially half of the last decade.

the German-speaking countries.

Piers joined SWMC in September,

2020 after 20 years as an independent

equity analyst. Prior to that he was

an analyst at various German banks,

including B. Metzler and Landesbank

Rheinland-Pfalz, where he was head of

research. He has worked closely with

the SWMC team since the 1990s.

Piers was born in Germany and educated

at University College London, where he

read Economics. Piers speaks German

and English.

In this report, we show that the valuations of the two watch and jewellery makers are most likely

to offer some room for upside surprise. By contrast, the shares of the three soft luxury goods

producers seem already priced to perfection.

Short-term momentum in the luxury goods sector has been characterised, as just noted, by a

swift recovery in demand. Such a result was not obvious as Covid-19 began to take a grip: before

the epidemic, about two-thirds of sales of luxury goods in Europe were driven by tourists, mainly

from China and the US, and tourism-related sales accounted for about 30% globally. Tourism, of

course, collapsed, but with little opportunity to spend money on experiences such as travel and

entertainment, those purchases were largely – and quickly – repatriated. It appears that luxury

goods have undiminished appeal.

The quick revival in demand is perhaps unsurprising given that, in spite of the pandemic, global

financial wealth reached new highs in 2020. According to a report by Boston Consulting Group

(BCG), it rose 8.3% as strong stock markets and a spike in savings fuelled a wealth boom.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 2

Europe’s answer to the US tech giants?

Find it in your favourite bag!

The recovery in luxury spending is driven to a large extent by China. This is a reminder that the

rise of the Chinese consumer has been a truly transformative event for the global luxury goods

industry. Chinese consumers are now said to account for around 70% of the growth in demand

for luxury goods. What is more, China presents an opportunity rather than a threat to the luxury

goods sector (unlike the situation in many other industries). This is because up to now a brand’s

image in the luxury market has in large part been built on heritage, and heritage cannot be

replicated overnight.

That said, younger consumers are as interested in aspiration as in heritage. This is seen as

one explanation for the huge success of Gucci’s strategic change of course in 2015 when a new

creative director presented a collection which marked a radical break with the company’s past –

almost overnight the brand became associated with sustainability and inclusiveness, resembling

a creative cultural club rather than a traditional fashion group. Luxury is not a static concept.

Growth

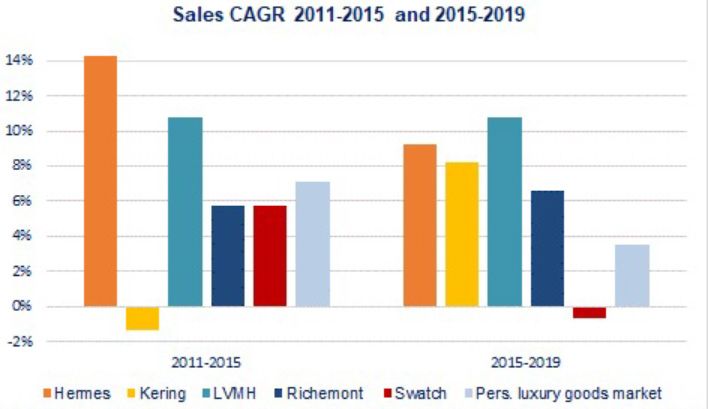

Prior to the pandemic, both Hermès and LVMH enjoyed outstanding double-digit compound

annual growth rates (CAGR). These were twice the pace of the overall growth in the market for

personal luxury goods which, according to the management consultancy firm Bain & Company,

rose at a CAGR of 5.3% between 2011 and 2019. The winning formula of Hermès and LVMH has

been diversification and product proliferation, while maintaining authenticity and exclusivity.

Hermès has managed to diversify its traditional leather business into new ‘métiers’. The recent

launch of the Beauty line brings its number of product categories to 16. At the same time, the

group continues to expand existing product lines by widening its ranges while preserving

their individual character. Bags, for instance, are available in an ever-increasing number of

combinations of size, colour and types of leather.

LVMH, the world’s largest luxury goods company by revenues, is seven times the size of Hermès

and more than three times larger than Kering. It has followed a similar strategy, and has been

equally successful in driving its fashion and leather goods business to ever new heights under its

Louis Vuitton label.

While Kering’s sales declined between 2011 and 2015, this was entirely due to the deconsolidation

of Redcats and Fnac, which had combined sales of around EUR 7.0bn. As a result, overall sales

grew only moderately over the decade to 2019, with a CAGR of 3.3%, the lowest in the sample

here under review except for Swatch Group. But revenues began to reaccelerate in the middle of

the past decade with the spectacular reinvigoration of Gucci referred to above. This translated

into a huge commercial success, with sales of the group’s flagship brand rising at a CAGR of

about 25% between 2015 and 2019, lifting Kering’s average annual growth rate during that

period to 8.2%. By 2019, Gucci accounted for more than 60% of the group’s total sales.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 3

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Growth continued

While the top-performing French groups have gained substantial market share, the fortunes

of the Swiss watchmakers Richemont and Swatch Group have not been as straightforward.

In the early part of the last decade, they benefitted enormously from a Chinese-induced boom,

especially for premium and ultra-luxury watches, a boom to a significant extent based on gifting.

This improved their product mix and paved the way for successive price increases. At one point

gifting was estimated to account for one-third of the watch market in mainland China.

The bonanza ended with China’s clampdown on corruption. This also had a profound impact on

Hong Kong, which used to attract large numbers of Chinese shoppers looking for lower prices.

Hong Kong was by far the biggest market for Swiss watch exports at that time, more than twice

the size of China. More recently, the political turmoil in the former British colony has aggravated

the woes of the Swiss watch industry in Hong Kong. To avoid damage to brand reputations

resulting from retailers discounting unsold inventory, Richemont and Swatch Group had to

clear the supply overhang through buybacks from and lower sell-ins to wholesale partners.

Swatch Group has also reduced the number of its own stores (from 92 to 38 in 2020). Richemont

is expected to follow suit.

At the same time, the growing popularity of smartwatches has dampened demand for Swiss

watches, especially at the lower end of the market. This was an additional burden for Swatch

Group, with its basic range segment (Swatch, Tissot) contributing to poor sales performance in

the second half of the last decade. Swiss statistics show that exports of watches costing less than

CHF 500, which represented around 13% of total export value in 2015, declined by around 23%

over the following years, even as total watch exports rose by 1.3%.

Capital efficiency

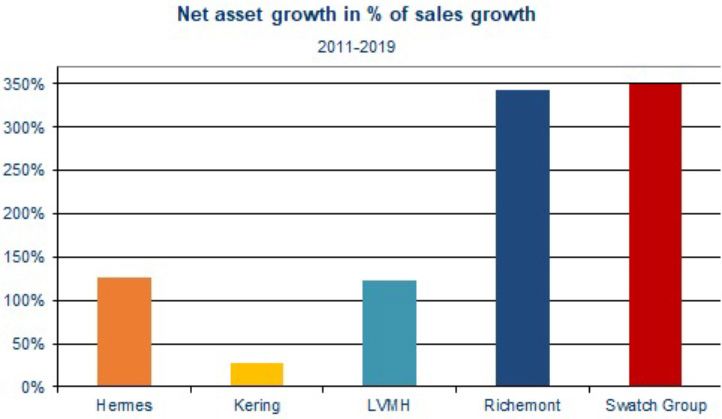

Sluggish sales growth was not the only problem faced by the Swiss watch and jewellery makers.

While Richemont’s sales actually grew from EUR 8.9bn in FY 2011 to EUR 14.2bn in FY 2020

(31 March), the increase in net assets far outpaced sales, rising more than threefold from

EUR 8.6bn to EUR 27.0bn. There were several reasons for this: A disproportionally high increase

in working capital, accounting gains, goodwill and intangibles arising from the acquisition of

the multibrand e-tailer platform YNAP, an increase in liquid funds of around EUR 5.0bn and a

fairly strong rise in lease liabilities from less than EUR 1.0bn to EUR 3.2bn.

Swatch Group’s asset base rose by a good 50% between 2011 and 2019, which was actually the

lowest increase in the sample except for Kering. Its asset turn nevertheless declined significantly

because of Swatch’s muted sales growth (CAGR of just 2.5%). The balance sheet expansion was

mainly caused by its Harry Winston jewellery brand acquisition, which, among other things,

boosted working capital due to the high value of gemstone inventory.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 4

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Capital efficiency continued

At Hermès, capital intensity went up somewhat, mainly as a result of a mounting cash balance,

which accounted for nearly two thirds of the rise in net assets. LVMH’s net assets to sales

ratio also increased but would have been more or less stable without changes in the scope of

consolidation, notably the acquisition of Christian Dior Couture in 2017. Kering’s very low asset

growth was due to several divestments (Fnac, its stake in Puma, Redcats).

Profitability

The outstanding position of Hermès in terms of growth and capital discipline extends to its

margin profile, which is characterised by an EBIT margin consistently above 30%. At that level

Hermès plays in its own league. LVMH’s margin has been equally stable, hovering around the

20% mark. In the fashion and leather goods business, LVMH’s profitability nearly matches that

of Hermès. However, its margin is mainly diluted by its retailing division (DFS, Sephora), and

by its perfumes and cosmetics, and its watches and jewellery businesses. Kering has seen a

strong margin recovery on the back of the Gucci revival, getting almost to the 30% mark before

Covid-19 brought a setback.

The Swiss watchmakers’ peak operating margins of around 25% in the first part of the last

decade were due to the special situation in China. They were not sustainable. Swatch Group

faced additional margin pressure from sales erosion in its basic range (Swatch used to be a

CHF 1.0bn brand but has declined to around CHF 300m), while in recent years Richemont’s

margins were burdened by the acquisitions of online distributors YNAP and Watchfinder.

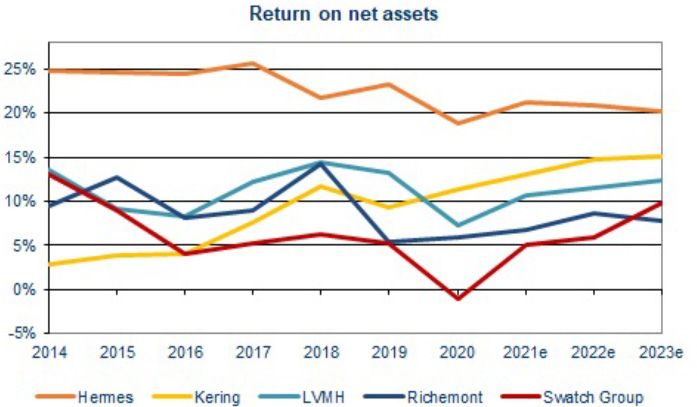

Going forward, consensus estimates suggest that the strongest margin improvement up to 2023

will be at Richemont and Swatch Group, followed by LVMH. Hermès and Kering, which already

boast industry-leading margins, are expected to recover to pre-pandemic levels.

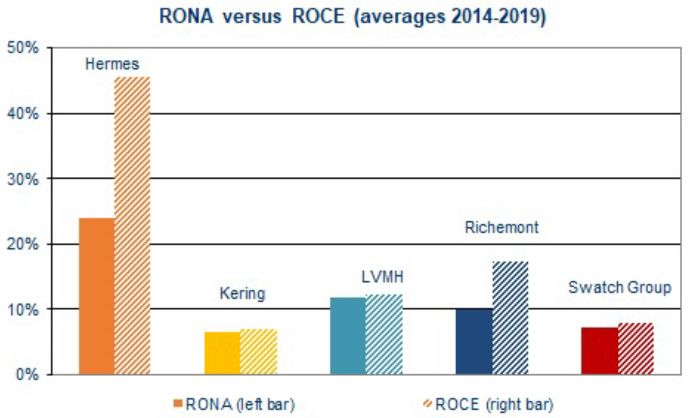

Return on capital

Superior margins, combined with strong sales growth and only a modest increase in

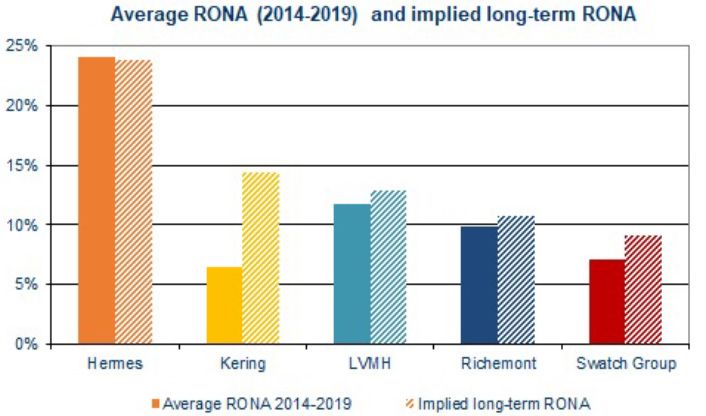

capital intensity, mean that Hermès is also the gold standard in terms of return on capital.

Its pre‑pandemic return on net assets (RONA) of around 23% was about ten percentage points

ahead of its nearest rivals. Swatch Group has the weakest return profile with an average return

of around 5% in the years prior to the pandemic.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 5

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Return on capital continued

Kering’s strong improvement in its return on capital resulted from the near tripling of its

operating margin, coupled with very modest capital requirements. By contrast, the two Swiss

groups did not only experience the lowest sales growth, they also had to invest more than two

euros (or Swiss francs) for every euro (or franc) of additional sales. Incidentally, the recognition

of off-balance-sheet leases as a right-of-use asset has had no impact on returns, as we always

treated operating leases as if they were capitalised.

Hermès’ outstanding position within the luxury goods sector becomes even more apparent if

one looks at the return on capital employed (ROCE), i.e. the return on its net operating assets

excluding cash balances and other financial assets. Over the period 2014 to 2019, its ROCE

was on average more than 20 percentage points higher than its RONA, widening the gap to its

peers even further. The big discrepancy is explained by its huge cash position, which basically

generates no return, but accounted for almost two-thirds of net assets in 2019. The other group

with a significant difference between RONA and ROCE is Richemont, where cash and bond

investments make up around 35% of net assets.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 6

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Implied return expectations

The analysis so far gives some credence to the share price performances of the five stocks under

review, at least in relative terms. The next part looks at the extent to which past performance

and track records are guiding investors’ expectations and how credible they are. To do this,

we compare past returns and growth rates, the two key valuation parameters, with the implied

long-term assumptions in current market capitalisations. This is based on a uniform cost of

capital of 7.5%.

Over the next five years, BCG expects financial wealth to grow on average by about 5% p.a.

Wealthy Chinese consumers look set to continue to drive worldwide growth in luxury spending.

Market researchers expect China’s luxury spending to double by 2025 as there will be a surge in

upper middle-class households.

While this bodes well for the luxury goods producers, there are also trends that require them to

constantly review their business models. One of the biggest challenges for these companies is the

generational shift in luxury goods spending towards the millennials, i.e. the demographic cohorts

born between 1980 and 2010. They are expected to increase their share of global personal luxury

goods purchases from around 44% of the total market in 2019 to about two-thirds by 2025.

With a greater desire for more responsible consumption, their purchasing decisions are likely to

be influenced to a far greater extent by sustainability and environmental considerations than,

for instance, those of the baby boomer generation.

This in turn could further stimulate the second-hand luxury market as it supports the circular

economy. According to Verified Market Research, the global luxury resale market is projected

to increase from USD 16.2bn in 2018 to USD 68.5bn by 2026, which implies a CAGR of 15.5%.

Online distribution is seen as a contributing factor to this trend. Online sales are expected to

account for up to 30% of the luxury market by 2025, which should give it sufficient scale to be

margin enhancing.

Making credible forecasts about the future returns of these companies for more than a few years

is virtually impossible. In the absence of any forces or trends that could fundamentally disrupt

this market, investors’ best guess would therefore be to take the track record and the outlook for

these companies over the next couple of years as a guide to their longer-term prospects.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 7

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Implied return expectations continued

For Hermès, consensus forecasts up to 2023 imply returns somewhat below its 2014 to 2019

average return, while longer-term market expectations reflect returns on a par with the recent

average. For LVMH analysts’ estimates suggest returns slightly above recent levels. Expectations

for Kering deviate the most from its recent track record because of the ongoing momentum at Gucci.

According to consensus figures, the two watch and jewellery makers, Richemont and Swatch

Group, will recoup some but not all of the margin/return erosion they suffered over the last few

years. This is in line with statements by the companies that in their watch business an operating

margin of around 20% should be well within reach. This compares to 12.8% at Richemont

(FY ending 31 March 2019) and 14.4% at Swatch Group (2019, watches and jewellery).

Both groups claim to have become less dependent on volume. This should reduce the danger of

oversupplying the market, which is seen as a key prerequisite for higher margins. The backbone

of the expected margin improvements is vigorous cost cutting during the pandemic. Swatch

Group, for instance, reduced personnel expenses by nearly a quarter and other operating

expenses by around 30%, which amounted to total savings of about CHF 1.4bn. Richemont

managed to improve its operating margin by almost 60 basis points in FY 2021 (31 March),

even though sales declined by 7.7%.

Distribution is another source of higher profitability. In the past, the watchmakers tried

to supply the wholesale channels with as many timepieces as possible. This contributed to a

boom-and-bust cycle as independent multi-brand retailers tend to de-stock in a downturn and

restock faster when demand improves. The watchmakers have therefore started to focus on

fewer but stronger third-party multi-brand distributors, which are estimated to account for as

much as 70% of total sales at Swatch Group. At the same time, efforts are underway to enhance

higher‑margin direct‑to-consumer channels, including online sales, as they provide more

control over inventories, allow better pricing and help to gain market share.

In contrast to the watch business, Richemont’s Jewellery Maisons (Cartier and Van

Cleef & Arpels) generate operating margins north of 30%. These assets account for around 50%

of sales but generate basically all the group profit. This points to the potential for Swatch Group

and its admittedly much smaller Harry Winston jewellery business, which it acquired in 2013.

Harry Winston accounts for about 10% of total sales, but its profitability is a long way short of

30%. It is said that it put too much emphasis on high-end jewellery while lacking geographical

diversification, as the main focus has been on Japan and the US. At Richemont, the equivalent

to Swatch Group’s upside in the jewellery business is the potential generated by scaling-up its

online business and improving its loss-making fashion and accessories businesses.

While it remains to be seen how much of the savings the groups can hold on to, there now seem

plenty of reasons why the two watchmakers should at least narrow the profitability gap to the

soft luxury segment. This is why the returns of Richemont and Swatch Group could be expected

to exceed their average returns during the period 2014 to 2019. For structural reasons, Swatch

Group might be perceived to have a slightly lower return potential than Richemont, given its

smaller jewellery business and its greater exposure to the lower end of the watch market.

Implied growth expectations

Taking the markets’ likely return assumptions as given, what are the growth rates implied by

current market capitalisations? This of course depends on how far out the period of superior

growth will extend before each company’s growth rate subsides to the same perpetual growth

rate of 3.5%. The shorter the period of extraordinary growth, the higher the implied growth

rate. It appears that a period of 25 years of turbo-charged growth would be required to arrive at

half-way plausible growth rates.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 8

Europe’s answer to the US tech giants?

Find it in your favourite bag!

Implied growth expectations continued

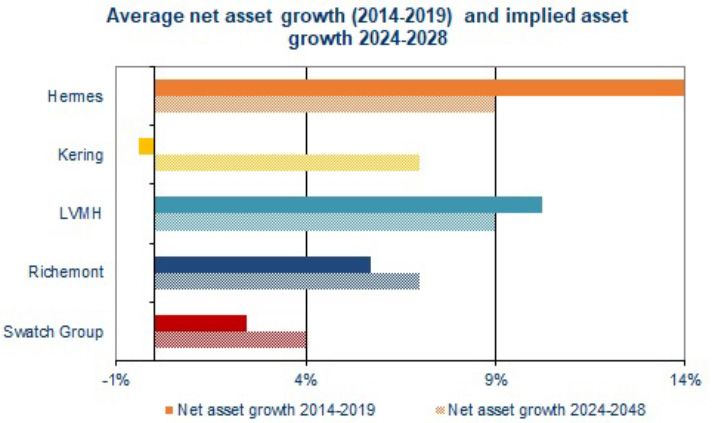

Growth expectations are highest – perhaps unsurprisingly – for the growth champions of the past

five years, with implied annual growth for Hermès and LVMH amounting to 9.0% p.a. This is

quite formidable for any established company and especially for LVMH, which is already larger

than the rest of the sample combined. If growth materialised on that scale, LVMH’s net assets

would increase by a factor of 10 from just under EUR 84bn in 2020 to around EUR 840bn by

2048. This optimism probably reflects investors’ confidence that LVMH will be able to develop

Dior into the next mega-brand, while the acquisition of Tiffany should make an important

contribution to LVMH’s position in the highly attractive branded jewellery segment.

Kering’s net assets actually shrank between 2014 and 2019 due to the deconsolidation of Puma,

which might weigh on growth expectations, which are somewhat lower than those for Hermès

and LVMH. Implied growth rates for Richemont and Swatch Group are likely to reflect investors’

concerns about the outlook for watches.

Consultancy firm McKinsey expects a growth rate of just 1% to 3% for luxury watches between

2019 and 2025. This is likely to be driven by timepieces with a retail value of more than

EUR 3,000, while mid-market brands are forecast to stagnate or even decline. As mentioned, the

entry-level segment has been challenged for some time by the strong growth of smartwatches.

Since 2016, the volume of connected watches rose more than threefold to about 75 million units

in 2020. During that period, the volume of total Swiss watch exports declined from just over

25 million units to less than 14 million units.

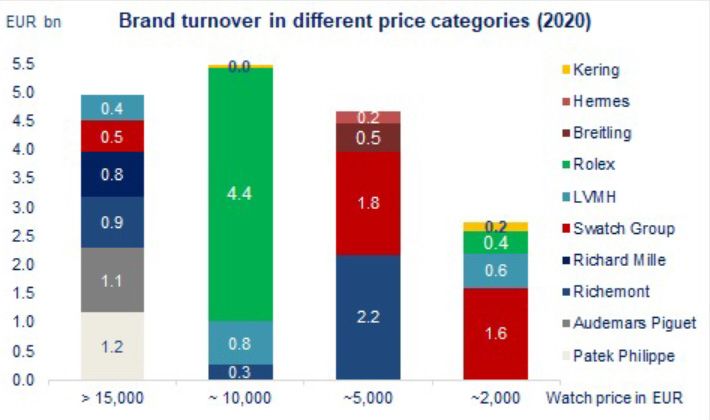

Richemont and Swatch Group are both strongest at the lower end of the premium segment, i.e.

in the price categories around EUR 2,000 (mainly Swatch Group) and EUR 5,000. The higher

price points around EUR 10,000 and above are dominated by non-listed companies, especially

Rolex, but also Patek Philippe and Audemars Piguet.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 9Europe’s answer to the US tech giants?

Find it in your favourite bag!

Implied growth expectations continued

All the same, there are some new growth opportunities for the watchmakers. These include the

increasingly important second-hand market. This market is expected to expand by as much as

8% to 10% p.a., reaching a volume of around USD 29bn to USD 32bn by 2025, which by then

would amount to more than 50% of the first-hand market.

What is more, hard luxury includes one of the fastest growing categories of the personal luxury

goods sector: branded jewellery. Consultancy group McKinsey forecasts a CAGR of 8% to 12%

for this segment from 2019 to 2025. It is estimated that branded jewellery accounts for just a fifth

of the fine jewellery market, whereas in luxury watches brand penetration is as high as 90%. At

Richemont, the jewellery segment contributes just over half of total sales, compared to around

10% at Swatch Group. It is therefore understandable that investors discount lower growth rates

for Swatch Group compared to Richemont. Besides the jewellery business, Richemont’s growth

should be further underpinned by its pre-owned watch business and its online activities which

have been strengthened through a global e-commerce partnership (New Luxury Retail) with

Farfetch and Alibaba. Richemont’s growth potential relative to the soft luxury goods producers

might therefore be a bit underappreciated.

Except for Swatch Group, the implied growth rates for the companies under review are well

above industry forecasts. Market researchers predict a compound annual growth rate for the

personal luxury goods sector of up to 5% over the next years. This compares with a projection

by Credit Suisse of average annual growth in global wealth of nearly 7% until 2025. However,

growth rates among luxury brands have been so widely spread that sector averages are not very

meaningful. This is because the larger luxury groups have been grabbing a bigger slice of the pie

at the expense of many smaller players. The top ten luxury groups already account for more than

half of total luxury goods sales, a trend that looks set to continue as several independent luxury

goods producers in Europe and some large US luxury department stores were already struggling

even before the pandemic set in.

Conclusions

Luxury has its price, which is also reflected in the quoted companies in this space, some of

which are trading at eyewatering levels, having themselves almost mutated into luxury items.

This is especially true for the French players and LVMH in particular, which is already the most

valuable quoted company in Europe.

There are plenty of good reasons for their high valuation: the great track record of soft luxury

goods producers, healthy market fundamentals, low interest rates, democratisation of luxury

goods through lower opening price points, the scarcity value of some products for which there

are waiting lists of a year or longer. This is to name just a few. There is nothing to suggest that

the fortunes of these luxury goods brands are likely to change any time soon. But given the

scale of the growth, and the return expectations already discounted, which basically imply

stellar performances over the remaining lifetime of many seasoned investors, one wonders if

these stocks are beginning to have a scarcity value themselves. This is particularly true for the

three mega-brands Gucci (Kering), Hermès and Louis Vuitton (LVMH). If there is some value for

money left, it is most likely to be found in the watches and jewellery segment, which has at least

the potential to surprise on the upside.

Piers Nestler

July 2021

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021

Please see full disclaimer on page 11 10Europe’s answer to the US tech giants?

Find it in your favourite bag!

CONTACT US

ENQUIRIES

Nadia Manzoor

S. W. Mitchell Capital LLP S. W. Mitchell Capital LLP

Princes House, 38 Jermyn Street E. nadia@swmitchellcapital.com Princes House, 38 Jermyn Street

London SW1Y 6DN T. +44 (0)20 7290 4517 London SW1Y 6DN

S. W. MITCHELL CAPITAL

Visit our website Follow us on twitter

swmitchellcapital.com @SWMCapital

DISCLAIMER

This thought piece is a confidential communication issued by S. W. Mitchell Capital LLP and is for information only. It was prepared by S. W. Mitchell Capital LLP only for, and is directed only at persons

that qualify as Professional Clients or Eligible Counterparties under the FCA rules, including appropriate institutional investors and intermediaries. It is not intended for the use of and should not be relied

on by any person who would qualify as a Retail Client. No person receiving a copy of this newsletter may copy it for transmission to another person. This document has been prepared from sources which

are believed to be accurate, however in producing it S. W. Mitchell Capital LLP may have relied on information obtained from third parties and accepts no liability for the accuracy or completeness of such

information. It is the responsibility of every person reading this document to satisfy himself as to the full observance of the laws of any relevant country, including obtaining any government or other

consent which may be required or observing any other formality which needs to be observed in that country.

Past performance should not be seen as an indication of future performance and will not necessarily be repeated. The value of investments and the income from them may fall as well as rise and is not

Designed and produced by lyonsbennett.com

guaranteed. The investor may not get back the original amount invested. Changes in rates or exchange may cause the value of investments to fluctuate.

S. W. Mitchell Capital LLP is a Limited Liability Partnership registered in England No. OC312953. Registered address 38 Jermyn Street, London SW1Y 6DN. Regulated and authorised in the UK by the

Financial Conduct Authority.

The material provided herein has been provided by S. W. Mitchell Capital LLP and is for informational purposes only. S.W. Mitchell Capital LLP serves as investment sub-adviser to one or more mutual

funds distributed through Northern Lights Distributors, LLC member FINRA/SIPC. Northern Lights Distributors, LLC and S.W. Mitchell Capital LLP are not affiliated entities.

Europe’s answer to the US tech giants? Find it in your favourite bag! | July 2021 11You can also read