Emerging Markets Monthly Highlights Another Difficult Year Is Ending, Challenges Remain - S&P Global

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Emerging Markets Credit Research

Jose Perez Gorozpe

Economic Research

Tatiana Lysenko

Monthly Highlights Xu Han Elijah Oliveros

Vincent Conti Vishrut Rana

Valerijs Rezvijs

Another Difficult Year Is Ending, Challenges Remain

Dec 16, 2021

Contents

Key Takeaways

Economic And Credit Conditions

Highlights

Macro-Credit Dashboards

GDP Summary

Monetary Policy/FX

Financing Conditions Highlights

Ratings Summary

This report does not constitute a ratings action

2Key Takeaways

We expect the economic recovery among emerging markets (EM) from the pandemic-induced downturn to continue into

Some sectors continue to operate below capacity, which will keep growth above trend

next year. However, in some countries--notably Brazil--growth will be below trend due to idiosyncratic factors.

EM risks are worsening as inflation keeps accelerating in many key countries, adding to existing challenges. Risk of an

extended period of high inflation and lingering high prices has risen for many EMs. Increasing prices could also prompt a

faster-than-expected normalization of U.S. interest rates, possibly leading to tighter financing conditions and market

its key trade

partners in EMs. A resurgence of COVID-19 cases could hit hard, given that vaccination rates remain low in many EMs.

The new Omicron variant is a stark reminder that the pandemic is far from over. Vaccination pace has accelerated in most

key EMs. However, many countries have not yet reached widespread immunity thresholds (70%-80% of population fully

vaccinated), especially in EM Asia and Sub-Saharan Africa. Countries with low vaccination levels remain vulnerable to new

contagion waves and variants. The emergence of the Omicron variant has raised the risk of one-off lockdowns and further

containment measures, which could undermine consumption and investment and extend supply chain disruptions.

Financing conditions have tightened. This is mostly due to rising benchmark yields. Overall, funding costs have risen toward

pre-pandemic levels. In EMEA and Latin America, central banks have been working on rate normalization, pushing up

benchmark yields. Central banks in EM Asia are not yet raising rates and spreads narrowed in November after a few months

of significant widening.

3EM Credit Conditions | Risks Worsen Amid Rising Inflation

Top EM Risks Risk Level Risk Trend

Inflation keeps accelerating in many key

EMs, compounding existing challenges. On

the bright side, higher prices are partly

fueled by the strong economic rebound. The

and vaccinations are progressing, but the

recent emergence of the Omicron variant

threatens the positive momentum. Downside

risks for EMs remain significant.

Improvement in credit conditions across

key EMs could be plateauing over the

coming months, as pre-existing weaknesses

and increasing COVID aftershocks, including

and potential for resurging COVID undermine

economic recovery and business conditions.

Source: Credit Conditions Emerging Markets Q1 2022: Inflation The Unwelcome Guest, Dec. 1, 2021. S&P Global Ratings.

4EM GDP Growth | Recovery Isn't Yet Complete

GDP Growth Forecast For Key Change In Baseline Forecast From We expect the economic recovery among EMs

EMs September 2021 from the pandemic-downturn to continue into

2022. Most economies will continue to normalize

2022F 2023F 2022F 2023F activity towards their pre-pandemic levels, which

will mean GDP growth will be above-trend next

year.

0.0 2.0 4.0 6.0 8.0 10.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 Brazil is a notable exception; growth will be

IND IND below trend in 2022. We see growth of just 0.8%

CHN CHN in 2022, with risks titled to the downside. This is

COL COL due to aggressive monetary policy tightening in

ARG ARG response to a weakening fiscal picture, which has

CHL CHL contributed to above-target inflation

TUR TUR expectations.

PHL PHL

MEX MEX

The scenario for Turkey in 2022 is also highly

BRL BRL

uncertain. Recent aggressive easing of monetary

POL POL policy has fueled inflation expectations and

IDN IDN added significant depreciatory pressure on the

ZAF ZAF lira. This means that the outlook for the economy

MYS MYS in 2022 is also very uncertain. For now, we are

RUS RUS penciling growth to slow to 3.7% in 2022 from

THA THA 9.8% estimated for 2021.

SAU SAU

F--S&P Global Ratings forecast. For India, 2019 = FY 2019 / 20, 2020 = FY 2020 / 21, 2021 = FY 2021 / 22,

2022 = FY 2022 / 23, 2023 = FY 2023 / 24. Source: Oxford Economics.

5EM Vaccination | Omicron Could Undermine Vaccination Progress

Share Of Population Fully Vaccinated And Time To Vaccinate 75% Of Population

Vaccination pace has further accelerated over

the past months in key EMs, but most are

Share of People Fully Vaccinated % Time to cover 75% of the population at current pace (months) months away inoculating 75% of their

populations. Progress has been notable in EM

Asia. On the other hand, there still many EMs,

90%

60

especially in Sub-Saharan Africa, that are far

80% behind and progressing slowly.

70% 50

Booster shots are only on the agenda of few

60%

40 EMs, which could be concerning if the Omicron

50% variant is severe or if current vaccinations are

40% 30 ineffective against this variant.

30% 20 Reaching a 75% of vaccinated population may

20% not slow infections sufficiently, as we have

10

10% seen in many countries that have reached this

0% 0 threshold. However, evidence shows vaccines

prevent severe illness, which is reducing

hospitalizations and deaths, ultimately

supporting the resumption of more service-

related activities, such as tourism.

Note: EM Median is median of EMs in chart. Current pace is based on daily doses as of Dec. 10, 2021. Source: OWID and S&P Global

Ratings.

6COVID-19 Update| Still High Uncertainty Over Omicron

New Daily COVID-19 Cases Per Million Population*

The Omicron variant is a stark reminder that

Chile Poland Russia South Africa Turkey EM Median

the COVID-19 pandemic is far from over.

transmissibility, severity, and the effectiveness of

900 existing vaccines against it. Early evidence

points toward faster transmissibility, which has

800

led many countries to reimpose social-

700 distancing measures and international travel

600 restrictions. Over coming weeks, we expect

500 additional evidence and testing to show the

extent of the danger Omicron poses, in order to

400

enable us to make a more informed assessment

300 of the risks to credit.

200

The emergence of the Omicron variant shows

100 once again that more coordinated and decisive

0

population to prevent the emergence of new,

more dangerous variants.

*Seven-day moving average. Source: OWID.

7EM Credit Spreads| Corporate Spreads Reverse Direction Across Sub-Regions

EM Spreads By Region

− EM offshore risk premia widened

EM Spreads By Region (level, in bps)

overall, but the sub-regional story

Covid-19 Worst Beg. of 2021 12 Month Average Oct. 29, 2021 Recent

1,000 924

flipped from the overarching trends of

previous months. EM Asia saw spreads

800

641 652 narrowed in November after a few

Spreads

600 518

380

months of significant widening. However,

343 329 346 333 333

400 283 282 310 324

261 280 264 235 216 255 the level remains over 40 bps above that

200 at the end of 2020.

0

C EM Corp EM Corp Asia EM Corp LatAm EM Corp EEMEA

− LatAm and EM EMEA reversed a gradual

Note: bps levels. Data as of Nov. 30, 2021. Source: S&P Global Ratings Research, Refinitiv, ICE Data Indices, and Federal Reserve Bank of St. Louis.

trend of spread compression and are

U.S. And EM Spreads

driving up the EM overall credit

spreads in November. This reflects

US and EM Spreads (levels, in bps)

Covid-19 Worst Beg. of 2021 12 Month Average Oct. 29, 2021 Recent monetary normalization and higher

1,500 1308 domestic inflation. Moreover, both

1058

regions have been facing rising risks to

1,000

Spreads

558

679 724 growth, with LatAm also grappling with

520

500 366 430 365 333 371 378 some political uncertainty.

136 122 112 124 162 148 140 151

0

C US IG US HY EM Corp IG EM Corp HY − Both U.S. and EM credit spreads picked

Note: bps levels. Data as of Nov. 30, 2021. HY High Yield; IG Investment Grade. Source: S&P Global Ratings Research, Refinitiv, ICE Data Indices, and up in November, especially for

Federal Reserve Bank of St. Louis.

speculative-grade spreads.

8Regional Economic Highlights

EM ASIA Economics | Current Accounts Show Room For Normalization

Vishrut Rana, Singapore, +65-6216-1008, vishrut.rana@spglobal.com

One feature of the pandemic-driven

Indonesia Malaysia Thailand Philippines downturn in Asia was that current accounts

12% improved sharply. Lockdowns resulted in a

steep drop in domestic demand, but global

10% demand for goods was in better shape,

leading to unusual current account

8%

strengthening.

6%

% of GDP

4% In several economies, current account

balances are still elevated, reflecting that

2%

0% levels.

-2%

Thailand is an exception, where the sudden

-4%

stop in tourism has led to a swift

-6% deterioration in the current account.

Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20 Sep-20 Mar-21 Sep-21

Sources: Office of the National Economic and Social Development Council Thailand, CEIC Data, Bank Indonesia, Department of Statistics

Malaysia, Bangko Sentral ng Pilipinas, Reserve Bank of India, and S&P Global Economics.

10EM EMEA Economics | Inflation Continues To Climb

Tatiana Lysenko, Paris, +33-1-4420-6748, tatiana.lysenko@spglobal.com

Valerijs Rezvijs, London, +44-7929-651386, valerijs.rezvijs@spglobal.com

significant inflationary pressures. The broader impact on the

Inflation Rates In EM EMEA economies economic outlook is highly uncertain and depends on the policy

direction.

South Africa Headline South Africa Core The Turkish lira lost more than 30% of its value against dollar since

Russia Headline Russia Core mid-November following front-loaded loosening of monetary policy

Turkey (right-axis) Headline Turkey (right-axis) Core amid high and rising inflation. Annual inflation in Turkey rose to

16 30

21% in November, with food and energy prices posting the largest

14 increases.

25

12 Other EM EMEA central banks continue tightening. Risk of

20 excessive tightening of monetary stance that we mentioned in our

10

recent EM EMEA Economic Outlook is likely to materialize in

8 15 Russia. Inflation reached new multi-year high of 8.4% year-on-year

6

in November, and price pressures remained broad. Meanwhile,

10

4 central bank signalled that it was ready for another large move in

2

5

mid-December, after raising the key rate 75 bps in October to 7.5%.

The South African Reserve Bank started its hiking cycle in

0 0

November, raising it rate 25 bps to 3.75%.

Dec-19

Mar-20

Jul-20

Dec-20

Mar-21

Jul-21

Nov-19

Oct-20

Nov-20

Oct-21

Nov-21

Jan-20

Apr-20

May-20

Jun-20

Aug-20

Feb-20

Sep-20

Jan-21

Apr-21

May-21

Jun-21

Aug-21

Feb-21

Sep-21 has raised the policy rate by 125 bps in two meetings in November

and December to 1.75%. Uncertainties about the domestic and

global inflation outlook and more hawkish stance of the Fed are

going to keep EM EMEA central banks on a tightening bias.

Note: Core inflation for Turkey does not include price increases for gold. Source: DataStream

and S&P Global.

11LatAm Economics | Monetary Policy Is Restrictive Across The Region

Elijah Oliveros-Rosen, New York, +1-212-438-2228, elijah.oliveros@spglobal.com

Difference Between One-Year Real Ex Ante Interest Rate And Neutral Real Interest Rate Above-target inflation expectations will keep

central banks in a hawkish poise in 2022. We

Brazil Chile Colombia Mexico expect sequential inflation to have peaked by Q4

8 2021, but remain relatively high due to several

factors, including the impact of ongoing supply-

chain disruptions, second round effects of higher

6

Tight monetary energy prices, and the pass-through to import

policy stance costs from weaker exchange rates. We expect

4 central banks in the region to continue to tighten

next year, until inflation expectations become

2

more anchored around their targets.

Brazil stands out as having the most restrictive

0

monetary policy stance in the region, and the

risk of a sharper-than-expected slowdown in

2022 is high. Real rates are currently the highest

-2

Loose monetary

since 2015, during which the economy

policy stance contracted. Unfavorable fiscal dynamics will

-4 keep inflation expectations high throughout

Feb-12

Feb-13

Feb-14

Feb-15

Feb-16

Feb-17

Feb-18

Feb-19

Feb-20

Feb-21

Aug-11

Nov-11

Aug-12

Nov-12

Aug-13

Nov-13

Aug-14

Nov-14

Aug-15

Nov-15

Aug-16

Nov-16

Aug-17

Nov-17

Aug-18

Nov-18

Aug-19

Nov-19

Aug-20

Nov-20

Aug-21

Nov-21

May-12

May-13

May-14

May-15

May-16

May-17

May-18

May-19

May-20

May-21

done with tightening, in our view, following 725

In percentage points. Notes: real ex ante interest rates are based on one-year vanilla interest rate swaps minus one-year ahead inflation bps in hikes this year.

expectations. We assume the following real neutral interest rates: Brazil (3%), Chile (0.5%), Colombia (1.5%), and Mexico (2%) . Source:

Haver Analytics and S&P Global Ratings.

12Macro-Credit Dashboards

GDP Summary | Economic Recovery Continued In Q3 In Most Countries

Latest reading Five-year

Country Period 2019 2020 2021f 2022f 2023f

(y/y) avg

Argentina 17.9 Q2 -0.2 -2.0 -9.9 7.5 2.1 2.1

Brazil 4.0 Q3 -0.5 1.4 -4.4 4.8 0.8 2.0

Chile 17.2 Q3 2.0 0.9 -6.0 11.4 2.0 2.8

Colombia 13.2 Q3 2.4 3.3 -6.8 9.2 3.5 3.0

Mexico 4.5 Q3 2.0 -0.2 -8.5 5.8 2.8 2.3

China 4.9 Q3 6.7 6.0 2.3 8.0 4.9 4.9

India 8.4 Q3 6.9 4.0 -7.3 9.5 7.8 6.0

Indonesia 3.5 Q3 5.0 5.0 -2.1 3.3 5.6 4.8

Malaysia -4.5 Q3 4.9 4.4 -5.6 2.6 6.3 5.2

Philippines 7.1 Q3 6.6 6.1 -9.6 5.0 7.4 7.3

Thailand -0.3 Q3 3.4 2.3 -6.1 1.2 3.6 4.2

Poland 5.5 Q3 4.4 4.7 -2.6 5.2 5.0 3.3

Russia 4.3 Q3 1.0 2.0 -3.0 4.2 2.7 2.0

Saudi Arabia 6.8 Q3 1.6 0.3 -4.1 2.3 3.2 2.5

South Africa 2.9 Q3 1.0 0.1 -6.4 4.9 2.4 1.5

Turkey 7.4 Q3 4.2 0.9 1.8 9.8 3.7 3.1

Note: Red means GDP growth is below five-year average (2015-2019). Blue means the opposite. F Forecast. Source: Haver Analytics and S&P Global Ratings.

14Monetary Policy/FX | More Hikes Last Month

Latest November YTD

Policy Latest rate Next

Country Inflation target inflation exchange exchange

rate decision meeting

reading rate chg. rate chg.

Argentina 38.00% No target 52.1% N/A N/A -1.2% -16.6%

Brazil 9.25% 3.75% +/- 1.5% 10.7% 150 bps hike Feb. 3 0.2% -7.6%

Chile 4.00% 3% +/- 1% 6.7% 125 bps hike N/A -1.8% -14.2%

Colombia 2.50% 3% +/- 1% 5.3% 50 bps hike Dec. 17 -4.9% -13.5%

Mexico 5.00% 3% +/- 1% 7.4% 25 bps hike Dec. 17 -4.1% -7.2%

China 2.20% 3% 2.3% N/A N/A 0.7% 2.6%

India 4.00% 4% +/- 2% 4.9% Hold Feb. 9 -0.4% -2.8%

Indonesia 3.50% 3.5% +/- 1% 1.7% Hold N/A -1.1% -1.9%

Malaysia 1.75% No target 2.9% Hold Jan. 20 -1.5% -4.4%

Philippines 2.00% 3% +/- 1% 4.2% Hold N/A 0.1% -4.7%

Thailand 0.50% 1%-3% 2.7% Hold Dec. 22 -1.5% -11.1%

Poland 1.75% 2.5% +/- 1% 7.0% 50 bps hike Jan. 12 -2.9% -9.1%

Russia 7.50% 4.00% 8.4% 75 bps hike Dec. 17 -4.2% 0.5%

Saudi Arabia 1.00% 3% +/- 1% 0.8% Hold N/A 0.0% 0.0%

South Africa 3.75% 3%-6% 5.5% 25 bps hike Jan. 27 -4.1% -7.5%

Turkey 14.00% 5% +/- 2% 21.3%100 bps cut Jan. 20 -28.7% -44.8%

Note: Red means inflation is above the target range, policy is tightening, and exchange rate is weakening. Blue means the opposite. A positive number for the exchange-rate change means

appreciation. Argentina's central bank no longer targets inflation, nor does it set the policy rate directly (it is set based on monetary aggregates targeting). For China, we use the PBOC's seven-day

reverse repo. Source: Bloomberg, Haver Analytics, and S&P Global Ratings.

15Real Effective Exchange Rates | Most Currencies Weakened Last Month

Broad Real Effective Exchange Rates

10.0

Stronger

5.0

0.0

-5.0

-10.0

-15.0

-20.0

-25.0

Weaker

-30.0

MXN

MYR

COP

PLN

BRL

CLP

TRY

SAR

PHP

THB

INR

ZAR

ARS

IDR

RUB

CNY

Percent change from 10-year average. Note: Data is computed on 10 years of the monthly average data of the J.P. Morgan Real Broad Effective Exchange Rate Index (PPI-deflated). Data as of Nov. 30,

2021. Source: S&P Global Ratings, Haver Analytics, and J.P. Morgan.

16Real Interest Rates | Monetary Policy Normalization Still Have Ways To Go

Deviation In Current Real Benchmark Interest Rates From 10-Year Average

IDR

Tighter

SAR

CNY

INR

ZAR

MYR

RUB

PHP

THB

Looser

MXN

COP

CLP

TRY

BRL

PLN

-600 -500 -400 -300 -200 -100 0 100

available data to calculate the average. We exclude Argentina. For China, we

use the seven-day reverse repo rate. Data as of November 30. Source: Haver Analytics and S&P Global Ratings.

17EM Heat Map

Color Coding

Sovereign-- h

Financial Institutions BICRA--The overall assessment of economic risk and industry risk, which ultimately leads to the classification of banking systems int -grade scale. The points range fro

ry 011.

Nonfinancial Corporates-- p °We assess return on capital by using

the median of our rated corporates in their respective countries, then we adjust for inflation, we then rank it based on our bal debt monitor with data as of March 2020.

Source: *-IIF 1Q 2020. t - Source: Bangko Sental NG Pilipinas; Corporate Variables Capital IQ 1Q 2020. S&P Global Ratings. 19Financing Conditions Highlights

Financing Conditions | EM (ex. Greater China) Corporate Debt Growth Remains Steady

Emerging Markets (ex. China) Greater China

50%

45% 44% − EM (excluding Greater China)

debt growth is still on track

40% with the growth rate of

34% outstanding bond debt of the

35%

past few years.

31% 30%

30% 28%

27%

−

25%

increased in 2020 marginally

20% over the 2019 pace. The 2021

16% 16% 15%

YTD growth rate is on course to

15%

15% 13% 13% dip back to pre-COVID pace.

10%

5%

0%

2016 2017 2018 2019 2020 2021YTD

Corporate debt growth computed as total cumulative corporate (financial and non-financial bond issuance divided by bond debt outstanding from beginning

of the year). Data as of Nov. 30, 2021. Source: Refinitiv and S&P Global Ratings.

21EM Yields | Most Benchmark Yields Stable, But With Key Exceptions

Change In Local Currency 10-Year Bond Yields Since The End Of 2020

− As of the end of November, most

1,000

Nov Oct EM benchmark yields relatively

776

800 693 stabilized, with some key

600 541 exceptions. Of note, Brazil and Chile

437

saw yields drop over the month, as

(bps)

361

400 322

253 230 264 233

193 197 205 markets reassessed rate hike

142 144 159

200

59 66 37 17

87 95 50 52 expectations amid slower growth.

0

-24 -17

(200)

− Turkey saw a further sharp rise in

Turkeyat theBrazil

Note: Data pulled end of Nov.Russia Colombia

2021. Chile data is as Mexico ChileSource:

of Nov. 30, 2021. Thailand Indonesia

S&P Global South and

Ratings Research Malaysia Poland

Bloomberg. India China

C Africa yields amid worse inflation

expectations, as authorities

Change In Dollar-Denominated 10-Year Bond Yields Since The End Of 2020 continue to prefer easing rates.

Russia, Poland, and Colombia saw

250

205 Nov Oct 20-50 bps increases in yields.

200 169

145 143

150

(bps)

100 63

− Where available, 10-year yields for

51

50 34 44

28 37 dollar-denominated bonds were

0 lower than last month, except for

Turkey Brazil Philippines Mexico Indonesia Turkey.

C

Note: Data pulled at the end of November 2021. The selection of country/economy is subject to data availability. Source: S&P Global Ratings Research and Bloomberg.

22EM Corporate Issuance | By Market

2016 2017 2018 2019 2020 2021 YTD − EM (excluding Greater China) issuance is

still on pace to match the one in 2020, it

but has decelerated.

140

124 123

118 118 120 − EM Asian issuances remained strong and

120 115

112 have surpassed the 2020 levels. But

(US$ Bil.)

106

99 101 activity has been largely limited to

100 investment-grade or state-owned

companies after spreads began rising in

80 September. LatAm and EMEA had lower

70 71

issuances than last year.

60

− EMs have continued to generally take

40 recent global monetary policy

developments in stride. Nonetheless, we

20 continue to watch the potential impacts

of the upcoming normalization of global

rates on both domestic and external

C 0

Domestic Foreign financing costs.

Excluding Greater China. Data as of Nov. 30, 2021, and full year data for 2016-2020. Source: S&P Global Ratings Research and Refinitiv.

23EM | Financial And Non-Financial Corporate Issuance

EM Cumulative Corporate Bond Issuances EM Regional Bond Issuances

EMEA (LHS) Emerging Asia (ex. GC) (LHS) Latin America (LHS) Greater China (RHS)

2016 2017 2018 2019 2020 2021 YTD

300

120 1800

250 1600

100

1400

(US$ Bil.)

200

(US$ Bil.)

(US$ Bil.)

80 1200

150 1000

60

800

100

40 600

50 400

20

200

0

0 0

C C 2016 2017 2018 2019 2020 2021 YTD

Excluding Greater China. Data as of Nov. 30, 2021. Data includes not rated and both financial and non- Data as of Nov. 30, 2021, and full year data for 2006-2020, for both financial and non-financial entities.

financial entities. Source: S&P Global Ratings Research and Refinitiv. Left Hand Side (LHS), Right Hand Side (RHS). Source: S&P Global Ratings Research and Refinitiv.

24Issuance | Sovereign Top Deals By Debt Amount In The Past 90 Days

S&P

S&P issue sovereign

Issue date Issuer Economy Market place rating rating Security description Currency Issuance ($ mil.)

13-Sep-21 Turkey Turkey U.S. public BB B+ 6.500% global notes due '33 USD 1,500

14-Sep-21 Chile Chile U.S. public A A 0.555% global notes due '29 EUR 1,083

14-Sep-21 Chile Chile U.S. public A A 3.250% global notes due '71 USD 959

13-Sep-21 Indonesia Indonesia U.S. public BBB BBB 3.200% global notes due '61 USD 639

13-Sep-21 Indonesia Indonesia U.S. public BBB BBB 1.300% global notes due '34 EUR 587

3.200% sr med term nts due

13-Oct-21 Poland Poland Foreign public A- A- '24 CNY 467

Data as of Nov. 30, 2021 (last 90 days); includes local/foreign currencies; EM excludes China. Red means speculative-grade rating , blue means investment-grade rating, and grey means not rated. Source: S&P Global Ratings

Research.

25Issuance | EM Sovereign Debt

2018 2019 2020 2021 YTD (US$ Bil.)

250

20

18

200

16

14

(US$ Bil.)

150

12

10

100

8

6

4 50

2

0 0

C

C

Data as of Nov. 30, 2021; includes local/foreign currencies. China includes mainland China and Hong Kong. Source: Refinitiv and Dealogic.

26Issuance | EM Financial And Non-Financial Top 20 Deals For The

Past 90 Days

Maturity Market S&P issue

Issue date Issuer Economy Sector Security description Currency Issuance ($ Mil.)

date place rating

3.404% gtd mdm-trm nts

22-Apr-21 28-Apr-61 Petronas Capital Ltd. Malaysia Financial institution U.S. private A- due '61 US 1,750

27-Oct-21 2-Nov-31 Ecopetrol S.A. Colombia Integrated oil and gas U.S. public BB+ 4.625% global nts due '31 US 1,250

2.480% gtd mdm-trm nts

22-Apr-21 28-Jan-32 Petronas Capital Ltd. Malaysia Financial institution U.S. private A- due '32 US 1,250

PT Indofood CBP Sukses 3.398% sr unsec nts due

2-Jun-21 9-Jun-31 Makmur Indonesia Consumer products Euro public NR '31 US 1,150

7.970% fxd/straight bd due

5-May-21 29-Apr-26 Vnesheconombank Russia Banks Euro private NR '26 RR 1,071

3.882% gtd sr unsec nt due

12-Apr-21 19-Apr-31 GENM Capital Labuan Ltd. Malaysia Insurance U.S. private BBB '31 US 1,000

15-Sep-21 23-Sep-36 Bangkok Bank PCL Thailand Banks U.S. private NR Mdm-trm sub nts due '36 US 1,000

1.400% mdm-trm nts due

3-Feb-21 9-Feb-26 PT Pertamina (Persero) Indonesia Integrated oil and gas U.S. private NR '26 US 1,000

4.125% gtd global nts due

26-Apr-21 3-May-28 Natura Cosmeticos S.A. Brazil Consumer products U.S. private BB '28 US 1,000

2.250% mdm-trm nts due

4-Jan-21 13-Jan-31 Export-Import Bank of India India Banks U.S. private BBB- '31 US 990

Data as of Nov. 30, 2021 (last 90 days); excludes sovereign issuances and China. Red means speculative-grade rating , blue means investment-grade rating, and grey means NR (not rated). Table is for foreign currency only

without perpetual. Source: S&P Global Ratings Research.

27Issuance | EM Financial And Non-Financial Top 20 Deals For The

Maturity S&P issue Issuance ($

Issue date date Issuer Economy Sector Market place rating Security description Currency Mil.)

3-Feb-21 9-Feb-31 PT Pertamina (Persero) Indonesia Integrated oil and gas U.S. private NR 2.300% mdm-trm nts due '31 US 900

27-Jul-21 30-Jul-26 Oi Movel S.A. - In Judicial Brazil Telecommunications Euro public B 8.750% gtd sec nts due '26 US 880

18-Mar-21 9-Mar-28 Veresaeva 6 Llc Russia Finance company Euro private NR Float rate nts due '28 RR 877

3-Feb-21 26-Jan-28 Veresaeva 6 Llc Russia Finance company Euro private NR Float rate nts due '28 RR 857

22-Apr-21 28-May-28 Fomento Econo Mexicano Mexico Consumer products U.S. public A- Global bonds due '28 EUR 838

Malaysia Wakala Sukuk 2.070% Islamic finance due

21-Apr-21 28-Apr-31 Bhd Malaysia Finance company U.S. private A- '31 US 800

1-Sep-21 8-Sep-24 Adani Green Energy Ltd. India Utility U.S. private NR 4.375% sr sec nts due '24 US 750

3-Feb-21 10-Feb-31 Indian Railway Fin Corp Ltd. India Broker U.S. private BBB- 2.800% mdm-trm nts due '31 US 750

17-Feb-21 24-Feb-26 Ozon Holdings PLC Russia Retail/restaurants Euro public NR 1.875% conv. bds due '26 US 750

27-Oct-21 2-Nov-51 Ecopetrol S.A. Colombia Integrated oil and gas U.S. public BB+ 5.875% global nts due '51 US 750

Data as of Nov. 30, 2021 (last 90 days); excludes sovereign issuances and China. Red means speculative-grade rating , blue means investment-grade rating, and grey means not rated. Table is for foreign currency only

without perpetual. Source: S&P Global Ratings Research.

28Maturing Debt | EM Financial And Non-Financial

Deals Coming Due In December 2021 And January 2022

Issue Maturity Market S&P issue

date date Issuer Economy Sector place rating Security description Currency Issuance ($ Mil.)

Tanner Servicios Foreign

5-Mar-19 3-Dec-21 Financieros Chile Broker public BBB- 1.000% sen nts due '21 SFR 125

4.750% sr unsec nts due

1-Dec-11 6-Dec-21 ENAP Chile Integrated oil and gas EURO/144A BBB- '21 US 492

Pacific Rubiales Energy 7.250% sr ensec nts due

5-Dec-11 12-Dec-21 Corp. Colombia Integrated oil and gas EURO/144A BB '21 US 300

9-Dec-14 12-Dec-21 Liberty Group Ltd. South Africa Broker Euro public NR Mdm-trm sub nts due '21 SAR 44

Foreign 2.375% gtd mdm-trm nts

18-May-16 14-Dec-21 Petroleos Mexicanos Mexico Integrated oil and gas public BBB+ due '21 SFR 153

11.500% sen amort nt due

9-Jun-16 14-Dec-21 Edesa S.A. Argentina Utility Euro public NR '21 US 64

Foreign 0.678% fxd/straight bd due

13-Dec-16 16-Dec-21 ICICI Bank Ltd. India Banks private BBB- '21 Y 87

Itau Unibanco Holding 6.200% mdm-trm sub nts

14-Jun-11 21-Dec-21 S.A. Brazil Banks EURO/144A NR due '21 US 249

Itau Unibanco Holding 6.200% mdm-trm sub nts

14-Jun-11 21-Dec-21 S.A. Brazil Banks EURO/144A NR due '21 US 249

Itau Unibanco Holding 6.200% sub global nt due

17-Jan-12 21-Dec-21 S.A. Brazil Banks U.S. private NR '21 US 558

Data as of Nov. 30, 2021; excludes sovereign issuances. Red means speculative-grade rating , blue means investment-grade rating, and grey means not rated. Table does not include China deals and for foreign currency only

without perpetuals. Source: S&P Global Ratings Research.

29Maturing Debt | EM Financial And Non-Financial

S&P issue Security

Issue date Maturity date Issuer Economy Sector Market place rating description Currency Issuance ($ Mil.)

Float rate nts due

28-Dec-16 28-Dec-21 Ghelamco Invest Poland Broker Euro public NR '21 PZ 27

Forest products

and building 4.750% sr unsec

4-Jan-12 11-Jan-22 Arauco Chile materials EURO/144A BBB nts due '22 US 493

Forest products

Cemex S.A.B. de and building 4.750% gtd bds

5-Sep-14 11-Jan-22 C.V. Mexico materials EURO/144A B due '22 EUR 518

Adani Ports & SE 3.950% sr unsec

11-Jan-17 19-Jan-22 Zone Ltd. India Transportation EURO/144A BBB- nts due '22 US 499

8.750% sen nts

12-Jan-17 20-Jan-22 Genneia S.A. Argentina Utility EURO/144A B+ due '22 US 350

8.750% sen nts

23-Jan-18 20-Jan-22 Genneia S.A. Argentina Utility EURO/144A B+ due '22 US 164

Santander

Consumer Bank 0.875% mdm-trm

10-Jan-19 21-Jan-22 SA.. Poland Banks Euro public NR nts due '22 EUR 574

Petroleos Integrated oil and 4.875% gtd mdm-

17-Jan-12 24-Jan-22 Mexicanos Mexico gas EURO/144A BBB trm nts due '22 US 2,083

Bharat Petroleum Integrated oil and 4.375% mdm-trm

17-Jan-19 24-Jan-22 Corp. Ltd. India gas Euro public NR nts due '22 US 499

Grupo Bimbo Consumer 4.500% gtd bds

18-Jan-12 25-Jan-22 S.A.B. de C.V. Mexico products EURO/144A NR due '22 US 794

Data as of Nov. 30, 2021; excludes sovereign. Red means speculative-grade rating , blue means investment-grade rating, and grey means not rated. Table does not include China deals and

for foreign currency only without perpetuals. Source: S&P Global Ratings Research.

30Maturing Debt | EM Financial And Non-Financial

S&P issue Security

Issue date Maturity date Issuer Economy Sector Market place rating description Currency Issuance ($ Mil.)

Forest products

Green River and building Zero cpn cvt zero

19-Jan-17 25-Jan-22 Holding Co Ltd. Thailand materials Euro public NR bonds due '22 US 43

2.750%

Firstrand Bank fxd/straight bd

5-Nov-14 31-Jan-22 Ltd. South Africa Banks Euro public NR due '22 SAR 9

6.750%

Metals, mining fxd/straight bd

9-Jun-16 31-Jan-22 EVRAZ GROUP Russia and steel Euro public B+ due '22 US 500

Forest products

and building 8.20% gtd bds

23-Jan-17 31-Jan-22 Tecnoglass Inc. Colombia materials EURO/144A BB- due '22 US 207

Data as of Nov. 30, 2021; excludes sovereign. Red means speculative-grade rating , blue means investment-grade rating, and grey means not rated. Table does not include China deals and

for foreign currency only without perpetuals. Source: S&P Global Ratings Research.

31Ratings Summary

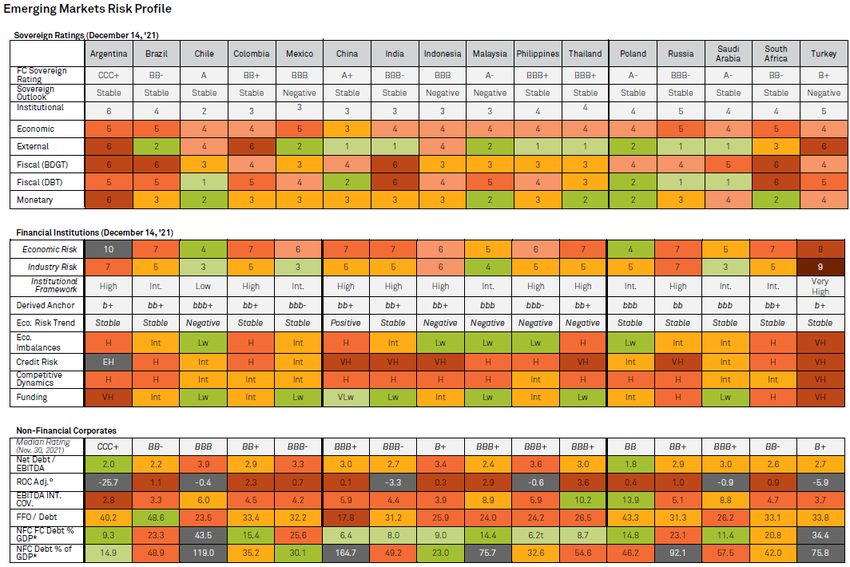

Ratings Summary | Sovereigns

Economy Rating Outlook 5 Year CDS Spread Median Rating Financials Median Rating Non - Financials

Argentina CCC+ Stable 2367 CCC+

Brazil BB- Stable 221 BB-

Chile A Stable 86 BBB

China A+ Stable 45 A BBB+

Colombia BB+ Stable 207 BB+

India BBB- Stable 93 BBB-

Indonesia BBB Negative 78 B+

Malaysia A- Negative 50 BBB+

Mexico BBB Negative 101 BB+ BBB-

Philippines BBB+ Stable 60 BBB+

Poland A- Stable 51 A- BB

Russia BBB- Stable 108 BB BB+

Saudi Arabia A- Stable 53 BBB BBB+

South Africa BB- Stable 215 BB-

Thailand BBB+ Stable 29 A- BBB+

Turkey B+ Negative 520 B+

Note: Foreign currency ratings. Red means speculative-grade rating, and blue means investment-grade rating. Data and CDS spread are as of Dec. 14, 2021. China median rating includes China, Hong Kong, Macau,

Taiwan, and Red Chip companies. Source: S&P Global Ratings Research and S&P Capital IQ.

33Rating Actions | Top 15 By Debt Amount In The Past 90 Days

Debt amount

Rating date Issuer Economy Sector To From Action type ($ Mil.)

20-Oct-21 Tata Motors Ltd. (Tata Sons Pte. Ltd.) India Automotive BB- B Upgrade 7,647

13-Oct-21 Concern Rossium LLC Russia Bank B+ B Upgrade 4,873

Chemicals, packaging and

2-Sep-21 Braskem S.A. (Odebrecht S.A.) Brazil environmental services BBB- BB+ Upgrade 3,250

20-Oct-21 Tata Steel Ltd. (Tata Sons Pte. Ltd.) India Metals, mining and steel BBB- BB Upgrade 2,300

Chemicals, packaging and

30-Sep-21 Braskem Idesa, S.A.P.I. and subsidiary Mexico environmental services B+ B Upgrade 900

21-Sep-21 Holding Co. Metalloinvest JSC Russia Metals, mining and steel BBB- BB+ Upgrade 800

Oil and gas exploration and

7-Oct-21 Compania General de Combustibles S.A. Argentina production CCC+ CCC Upgrade 585

Oil and gas exploration and

12-Nov-21 Serba Dinamik Holdings Berhad Malaysia production CC CCC Downgrade 500

10-Nov-21 Guacolda Energia S.A. Chile Utility B B+ Downgrade 500

23-Sep-21 Ratch Group Public Co. Ltd. Thailand Utility BBB BBB+ Downgrade 437

29-Oct-21 Controladora Mabe, S.A. de C.V. Mexico Consumer products BBB BBB- Upgrade 370

25-Oct-21 Manappuram Finance Ltd. India Finance company BB- B+ Upgrade 300

13-Oct-21 Gazprombank JSC Russia Bank BBB- BB+ Upgrade 139

28-Sep-21 PT Profesional Telekomunikasi Indonesia Indonesia Telecommunications BBB- BBB Downgrade 133

Data as of Nov. 30, 2021, excludes sovereigns, Greater China and the Red Chip companies and includes only latest rating changes. Source: S&P Global Ratings Research.

34EM | Total Rating Actions

By Economy

Positive Outlook/CreditWatch Revisions Upgrade Downgrade Negative Outlook/CreditWatch Revisions

60

40

Number Of Issuers

20

0

(20)

(40)

(60)

C

Note: Data includes sovereigns. Data from Feb. 3, 2020, to Nov. 19, 2021. Greater China includes mainland China, Taiwan, Macao and Hong Kong. Source: S&P Global Ratings.

35EM | Rating Actions

By Economy

CreditWatch Negative Downgrade Negative Outlook Change

0 10 20 30 40 50 60 70 80 90

Argentina

Brazil

Chile

Colombia

Greater China

India

Indonesia

Malaysia

Mexico

Philippines

Poland

Russia

Saudi Arabia

South Africa

Thailand

Turkey

C

Number Of Issuers

Note: Data includes sovereigns. Data from Feb. 3, 2020, to Nov. 19, 2021. Greater China includes mainland China, Taiwan, Macao and Hong Kong. Source: S&P Global Ratings.

36EM | Total Rating Actions

By Sector

40 Positive Outlook/CreditWatch Revisions Upgrade Downgrade Negative Outlook/CreditWatch Revisions

30

20

10

Number Of Issuers

0

(10)

(20)

(30)

(40)

(50)

Aerospace and Banks Business and Chemicals Energy Homebuilders Insurance Metals and Real Estate Sovereign Telecom Transportation

C defense consumer and Mining infra

services developers

Note: Data includes sovereigns. Data from Feb. 3, 2020, to Nov. 19, 2021. Greater China includes mainland China, Taiwan, Macao and Hong Kong. Source: S&P Global Ratings.

37EM | Total Rating Actions

By Sector

Investment Grade Speculative Grade

0 20 40 60 80 100 120

Aerospace and defense

Automotive

Banks

Building materials

Business and consumer services

Capital Goods

Chemicals

Consumer products

Energy

Health care

Homebuilders and developers

Hotels and gaming

Insurance

Media and Entertainment

Metals and Mining

NBFI

Real Estate

Retailing

Sovereign

Technology

Telecom

Transportation

Transportation infra

Utilities

C

Number Of Issuers

Note: Data includes sovereigns. Data from Feb. 3, 2020, to Nov. 19, 2021. Greater China includes mainland China, Taiwan, Macao and Hong Kong. Source: S&P Global Ratings.

38EM | Total Rating Actions

− The rating actions slightly

Negative Outlook/CreditWatch Revisions Downgrade Upgrade Positive Outlook/CreditWatch Revisions

decreased compared with the

40 previous month. For November

2021, we saw four downgrades,

20 four CreditWatch listings/outlook

revisions to negative, four

0

upgrades, and two CreditWatch

listings/outlook revisions to

Number Of Issuers

-20

positive in EMs.

-40

-60 − The largest number of

downgrades were in May 2020

-80 (34).

-100

− The most CreditWatch

-120 listings/outlook revisions to

Oct

Oct

March

April

March

July

April

July

Nov

Jan

Nov

May

May

June

June

Aug

Sept

Feb

Dec

Aug

Sept

Feb negative occurred in April 2020

(94).

2020 2021

Data includes sovereigns. Data from Feb. 3, 2020, to Nov. 19, 2021. EMs consist of Argentina, Brazil, Chile, China, Colombia, Mexico, India, Indonesia, Malaysia,

Thailand, the Philippines, Poland, Russia, Saudi Arabia, South Africa, and Turkey. Source: S&P Global Ratings.

39EM Downgrade Potential | By Bias

The Number Of Sectors With Above-Average Downgrade Potential Remained Steady In November

Count of EM 16 Corporate Sectors With Above-Average Downgrade Potential (RHS)

EM 16 Corporate Negative Bias (LHS)

12-month trailing average EM 16 Corporate Negative Bias (LHS) (count)

(%)

0.6 18

16

0.5

14

0.4 12

10

0.3

8

0.2 6

4

0.1

2

0 0

Data as of Nov. 30, 2021. Negative bias is the percentage of ratings with negative outlooks or that are on CreditWatch with negative implications. Count of Corporate Sectors With Above-Average Downgrade Potential shows

the number of sectors with a negative bias that is above the long-term negative bias for that sector. Source: S&P Global Ratings Research.

40Downgrade Potential | Regional Negative Bias

− EM Asia (excluding China). The November

EM Downgrade Potential Differentiated Across Region 2021 downgrade potential was 29%, up

10-Year Average 5-Year Average 11/30/2021

from October 2021 (27%), and much higher

than both five- and 10-year historical

averages.

35%

30%

29% − EEMEA. The November downgrade

potential (6%) increased from 5% in

25%

24% October but remains the lowest among

20% other EM regions.

19%

18%

16% 16%

14%

− LatAm. The November downgrade

potential (25%) was below its five-year

6% average (35%) and its 10-year average

(30%).

C

EM Asia (ex. China) EEMEA Latin America Greater China − Greater China. The November downgrade

potential (14%) increased when compared

with last month (10%) but remains below

both of its historical averages.

ata as of Nov. 30, 2021, and excludes sovereigns. Latin America: Argentina, Brazil, Chile, Colombia, and Mexico. EM Asia: India, Indonesia, Malaysia,

Thailand, and the Philippines. EEMEA: Poland, Russia, Saudi Arabia, South Africa, and Turkey. Greater China: China, Hong Kong, Macau, Taiwan, and Red

Chip companies. Source: S&P Global Ratings Research.

41EM Downgrade Potential | By Sector

The Homebuilders/Real Estate Companies, Retail And Restaurants Lead The November Downgrade Potential

Current Negative Bias (Nov. 30, 2021) 5-Year Averages

Automotive (10)

CP&ES (15)

Capital goods (13)

Sector (Number of Issuers)

Consumer products (33)

Financial institutions (146)

Forest (9)

Health care (5)

High technology (13)

Home/RE (54)

Insurance (21)

Media/entert (5)

Metals/mining/steel (33)

Oil & Gas (22)

Retail (11)

Telecommunications (23)

Transportation (14)

Utilities (67)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Negative Bias

ata as of Nov. 30, 2021, and includes sectors with more than five issuers only; excludes sovereigns. EMs consist of Argentina, Brazil, Chile, China, Colombia, Mexico, India, Indonesia, Malaysia, Thailand, the Philippines,

Poland, Russia, Saudi Arabia, South Africa, and Turkey. Greater China--China, Hong Kong, Macau, Taiwan, and Red Chip companies. Media/entert--Media and entertainment, Retail--Retail/restaurants, CP&ES--Chemicals,

packaging, and environmental services, Home/RE--Homebuilders/real estate companies, Forest--Forest products and building materials. Source: S&P Global Ratings Research.

42By Sector

Neg/Negative Stable Pos/Positive

16000

14000

12000

Debt (US$Mn)

10000

8000

6000

4000

2000

0

Utilities Oil and gas Telecommunications Capital goods Home/RE Consumer products CP&ES Financial institutions Media/entert Automotive

Based on local currency ratings. CP&ES--Chemicals, packaging, and environmental services, Metals/mining/steel--Metals, mining and steel, Retail--Retail/restaurants, Media/entert--Media and entertainment, Home/RE--Homebuilders/real

estate co., and Forest--Forest products and building materials. Data as of Nov. 30, 2021. Source: S&P Global Ratings Research.

43Rating Actions | -

Debt amount

Rating date Issuer Economy Sector To From (mil.)

Oil and gas exploration and

8-May-20 YPF S.A Argentina production CCC+ B- 1,969

18-Jun-20 Oi S.A. Brazil Telecommunications CC B- 1,654

8-May-20 Pampa Energia S.A. Argentina Utilities CCC+ B- 1,550

27-Apr-20 CAR Inc. Cayman Islands Transportation CCC B- 557

30-Apr-20 PT Alam Sutera Realty Tbk. Indonesia Homebuilders/real estate CCC+ B- 545

8-May-20 Transportadora de Gas del Sur S.A. (TGS) (Compania De Inversiones de Energia S.A.) Argentina Utilities CCC+ B- 500

8-Apr-20 GCL New Energy Holdings Ltd. (GCL-Poly Energy Holdings Ltd.) Bermuda Utilities CCC B- 500

17-Mar-20 IRSA Inversiones y Representaciones S.A. (Cresud S.A.C.I.F. y A.) Argentina Homebuilders/real estate CCC+ B- 431

8-May-20 Telecom Argentina S.A. Argentina Telecommunications CCC+ B- 400

29-Apr-20 Aeropuertos Argentina 2000 S.A. Argentina Utilities CC B- 400

19-Jun-20 PT Modernland Realty Tbk. Indonesia Homebuilders/real estate CCC B- 390

16-Mar-20 Banco Hipotecario S.A. Argentina Bank CCC B- 350

6-Apr-20 Grupo Kaltex, S.A. de C.V. Mexico Consumer products CCC B- 320

13-Jan-20 Empresa Distribuidora Y Comercializadora Norte S.A. Argentina Utilities CCC+ B- 300

Oil and gas exploration and

8-May-20 Compania General de Combustibles S.A. Argentina production CCC+ B- 300

8-May-20 CAPEX S.A. Argentina Utilities CCC+ B- 300

8-May-20 AES Argentina Generacion S.A (AES Corp. (The)) Argentina Utilities CCC+ B- 300

9-Apr-20 PT Gajah Tunggal Tbk. Indonesia Automotive CCC+ B- 250

8-May-20 Banco De Galicia Y Buenos Aires S.A.U. Argentina Bank CCC+ B- 250

19-Mar-20 PT MNC Investama Tbk. Indonesia Media and entertainment CCC B- 231

8-Apr-20 Pearl Holding III Ltd. China Automotive CCC+ B- 175

13-Apr-20 Compania de Transporte de Energia Electrica en Alta Tension TRANSENER S.A. Argentina Utilities CCC+ B- 99

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Dec. 31, 2020; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global Ratings Research.

44Rating Actions | -

-

Debt

amount ($

Rating Date Issuer Economy Sector To From Mil.)

22-Apr-21 Alpha Holding S.A. de C.V. Mexico Financial institutions CCC B- 300

Homebuilders/real estate

18-Jun-21 Sichuan Languang Development Co., Ltd. China company CCC- B- 750

Homebuilders/real estate

5-Aug-21 China Evergrande Group Cayman Islands company CCC B- 16,260

Oil and gas exploration and

18-Aug-21 Serba Dinamik Holdings Berhad Malaysia production CCC B- 500

Homebuilders/real estate

22-Sep-21 Xinyuan Real Estate Co. Ltd. Cayman Islands company CCC B- 300

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Nov. 30, 2021; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global Ratings Research.

45Rating Actions | EM Fallen Angels In 2020 And 2021 YTD

Debt

amount

Rating date Issuer Economy Sector To From ($ Mil.)

15-Jun-20 Embraer S.A. Brazil Aerospace and defense BB+ BBB- 500

26-Jun-20 Axis Bank Ltd. India Bank BB+ BBB- 1,095

8-Jul-20 Braskem S.A. (Odebrecht S.A.) Brazil Chemicals, packaging and environmental services BB+ BBB- 4,150

14-Jul-20 Zijin Mining Group Co. Ltd. China Metals, mining and steel BB+ BBB- 350

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Dec. 31, 2020; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global

Ratings Research.

Six EM fallen angels so far in 2021 including one sovereign.

Debt

amount

Rating date Issuer Economy Sector To From (Mil.)

25-Mar-21 Empresa Nacional del Petroleo Chile Utilities BB+ BBB- 2,480

19-May-21 Republic of Colombia Colombia Sovereign BB+ BBB- 30,184

20-May-21 Grupo de Inversiones Suramericana S.A. Colombia Diversified BB+ BBB- 550

20-May-21 Financiera de Desarrollo Territorial S.A. FINDETER Colombia Bank BB+ BBB- 500

20-May-21 Ecopetrol S.A. Colombia Integrated Oil & Gas BB+ BBB- 9,850

Cayman

09-Nov-21 Shimao Group Holdings Ltd. Islands Homebuilders/Real Estate Co. BB+ BBB- 1,000

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Nov. 30, 2021; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global

Ratings Research.

46Rating Actions | EM Rising Stars In 2020 And 2021 YTD

Rating date Issuer Economy Sector To From Debt amount ($ Mil.)

Mobile TeleSystems PJSC (Sistema

17-Sep-20 (PJSFC)) Russia Telecommunications BBB- BB+ 1,000

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Dec. 31, 2020; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global

Ratings Research.

Seven EM rising stars so far in 2021.

Debt

amount

Rating date Issuer Economy Sector To From ($ Mil.)

12-Apr-21 Sovcomflot PAO Russia Transportation BBB- BB+ 750

8-Apr-21 Shimao Group Holdings Ltd. Cayman Islands Homebuilders/real estate company BBB- BB+ 2,100

18-Mar-21 Grupo Cementos de Chihuahua S.A.B. de C.V. Mexico Forest products and building materials BBB- BB+ 260

Chemicals, packaging and environmental

2-Sep-21 Braskem S.A. (Odebrecht S.A.) Brazil services BBB- BB+ 3,250

21-Sep-21 Holding Co. Metalloinvest JSC Russia Metals, mining and steel BBB- BB+ 800

13-Oct-21 Gazprombank JSC Russia Banks BBB- BB+ 139

20-Oct-21 Tata Steel Ltd. (Tata Sons Pte. Ltd.) India Metals, mining and steel BBB- BB 2,300

Debt volume includes subsidiaries and excludes zero debt. Note: Red means speculative-grade rating. Data as of Nov 30, 2021; includes sovereigns and Greater China and Red Chips companies. Source: S&P Global

Ratings Research.

47Rating Actions | List Of Defaulters In 2020 And 2021 YTD

Debt amount

Rating date Issuer Economy Sector To From Action type ($ Mil.)

14-Jan-20 Qinghai Provincial Investment Group Co. Ltd. China Metals, mining and steel D CCC- Downgrade 850

21-Jan-20 Panda Green Energy Group Ltd. Bermuda Utilities SD CC Downgrade 350

21-Jan-20 Republic of Argentina Argentina Sovereign SD CCC- Downgrade 137,602

21-Feb-20 Tunghsu Group Co. Ltd. China High technology SD CCC- Downgrade 390

Cayman Homebuilders/real

27-Mar-20 Yida China Holdings Ltd. Islands estate SD CC Downgrade 300

7-Apr-20 Republic of Argentina Argentina Sovereign SD CCC- Downgrade 139,092

10-Apr-20 Vestel Elektronik Sanayi Ve Ticaret A.S. Turkey High technology SD CCC+ Downgrade -

Media and

24-Apr-20 Enjoy S.A. Chile entertainment D B- Downgrade 300

11-May-20 Yihua Enterprise (Group) Co. Ltd. China Consumer products SD CCC Downgrade -

19-May-20 Aeropuertos Argentina 2000 S.A. Argentina Utilities SD CC Downgrade 750

27-May-20 Latam Airlines Group S.A. Chile Transportation D CCC- Downgrade 1,800

2-Jun-20 Grupo Famsa, S.A.B. de C.V. Mexico Retail/restaurants SD CCC- Downgrade 81

1-Jul-20 Grupo Aeromexico, S.A.B. de C.V. Mexico Transportation D B- Downgrade 400

Media and

1-Jul-20 Grupo Posadas, S. A. B. de C. V. Mexico entertainment D CC Downgrade 400

Homebuilders/real

8-Jul-20 PT Modernland Realty Tbk. Indonesia estate SD CCC- Downgrade 390

9-Oct-20 Oi S.A. Brazil Telecommunications SD CC Downgrade 1,654

Data is by end of year for 2020, and as of Nov. 30 for 2021. Includes both rated and zero debt defaults. Includes sovereigns, Greater China, and Red Chip companies. Excludes five confidential issuers in 2020 and six in

2021 YTD. D Default; SD Selective Default. Source: S&P Global Ratings Research and S&P Global Market Intelligence's CreditPro®.

48Rating Actions |

Debt amount ($

Rating date Issuer Economy Sector To From Action type Mil.)

14-Oct-20 Banco Hipotecario S.A. Argentina Bank SD CC Downgrade 350

Corp Group Banking S.A. (Inversiones CorpGroup

16-Oct-20 Interhold, Ltda.) Chile Financial institutions D CC Downgrade 500

Homebuilders/real estate

28-Oct-20 PT Alam Sutera Realty Tbk. Indonesia company D CC Downgrade 545

IRSA Inversiones y Representaciones S.A. (Cresud Homebuilders/real estate

12-Nov-20 S.A.C.I.F. y A.) Argentina company SD CC Downgrade 360

Oil and gas exploration and

26-Feb-21 YPF S.A. Argentina production SD CC Downgrade 2,900

Cayman Homebuilders/real estate

2-Mar-21 Sunshine 100 China Holdings Ltd.(A) Islands companies SD CCC- Downgrade -

13-Apr-21 YPF Energia Electrica S.A. (YPF S.A.) Argentina Utilities SD CCC- Downgrade 400

27-Apr-21 Maxcom Telecomunicaciones, S.A.B. de C.V. Mexico Telecommunications D CCC- Downgrade 57

28-Apr-21 Future Retail Ltd. India Retail/restaurants SD CCC- Downgrade 500

Homebuilders/real estate

13-Jul-21 Sichuan Languang Development Co. Ltd. China companies D CCC- Downgrade -

20-Jul-21 Alpha Holding S.A. de C.V. Mexico Financial institutions D CC Downgrade 300

Data is by end of year for 2020, and as of Nov. 30 for 2021. Includes both rated and zero debt defaults. Includes sovereigns, Greater China, and Red Chip companies. Excludes five confidential issuers in 2020 and six in

2021 YTD. D Default; SD Selective Default. Source: S&P Global Ratings Research and S&P Global Market Intelligence's CreditPro®.

49Rating Actions |

Debt amount ($

Rating date Issuer Economy Sector To From Action type Mil.)

Cayman Homebuilders/real estate

11-Aug-21 Sunshine 100 China Holdings Ltd. (B) Islands companies SD CCC- Downgrade -

CLISA-Compania Latinoamericana de Infraestructura &

13-Aug-21 Servicios S.A. Argentina Capital goods SD CC Downgrade 905

Cayman Homebuilders/real estate

5-Oct-21 Fantasia Holdings Group Co. Ltd. Islands company SD CCC Downgrade 1,950

Cayman Homebuilders/real estate

19-Oct-21 Sinic Holdings (Group) Co. Ltd. Islands company SD CC Downgrade -

Investimentos e Participacoes em Infraestrutura S.A. -

11-Nov-21 Invepar Brazil Utilities D CC Downgrade -

Data is by end of year for 2020, and as of Nov. 30 for 2021. Includes both rated and zero debt defaults. Includes sovereigns, Greater China, and Red Chip companies. Excludes five confidential issuers in 2020 and six in

2021 YTD. D Default; SD Selective Default. Source: S&P Global Ratings Research and S&P Global Market Intelligence's CreditPro®.

50Rating Actions | Fallen Angels And Potential Fallen Angels

Six EM Fallen Angels In 2021 YTD − Six EM fallen angels. Through November

Fallen Angels Average Potential Fallen Angels 2021, one Cayman Islands-based Shimao

35 Group Holdings Ltd, one Chile based

30 Empresa Nacional del Petroleo, and four

25

Colombia-based entities, including the

Issuers

20

15

sovereign, were the fallen angels in EMs.

10

5

0 − Among the current EM potential fallen

C 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 angels (PFAs), there were none on

Data as of Nov. 30, 2021. Parent only. Include Red Chip companies. Source: S&P Global Ratings Research.

CreditWatch, indicating lower immediate

downgrade risk, as PFAs with negative

outlooks typically have a one-in-three

EM PFAs By Economy chance of a downgrade within two years

Nov. 30, 2021 PFAs Nov. 30, 2020 PFAs

of receiving the negative outlook.

8

PFA Count of Issuers

6 − The count of global PFAs is stable. Media

4

and entertainment, and financial

institutions continued to lead the count of

2 potential fallen angels. For more

'BBB' Pulse: The Future

0

C Brazil Chile Greater China Colombia India Indonesia Looks Bright As Potential Rising Stars

Data as of Nov. 30, 2021. Include Red Chip companies. Source: S&P Global Ratings Research.

Shoot Up

51Rating Actions | Rising Stars And Potential Rising Stars

Seven EM Rising Stars So Far In 2021

Rising Stars Average Potential Rising Stars − Seven EM rising stars. Through

16

November 2021, there were three from

14

12 Russia, and one each rising star from

Issuers

10 Brazil, the Cayman Islands, Mexico,

8

6

and India.

4

2

0 − Among the current EM potential rising

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

C starts (PRS), there were none on

Data as of Nov. 30, 2021. Parent only. Include Red Chip companies. Source: S&P Global Ratings Research. CreditWatch positive.

EM PRS By Economy − The number of global PRS increased.

Nov. 30, 2021 PRSs Nov. 30, 2020 PRSs Of the PRS (issuers rated 'BB+' with

4 positive outlooks or ratings on

PRS Count of Issuers

3

CreditWatch with positive

implications), American utilities lead

2

among the sectors. For more

1 'BBB' Pulse: The

0 Future Looks Bright As Potential Rising

Brazil Mexico South Africa Russia Greater China

C Stars Shoot Up

Data as of Nov. 30, 2021. Include Red Chip companies. Source: S&P Global Ratings Research. 2021.

52Rating Actions | Weakest Links And Defaults

EM Weakest Links Reached Record Highs In 2020

Weakest Links Count (left scale) Weakest Link Share of Speculative-Grade Population (%) (right scale)

35 18% − Weakest links. EMs saw 10

30 16% issuers on the weakest links list

14%

Number of Issuers

25

12% (5% of total speculative-grade

20 10% issuers), reflecting default

15 8%

10

6% prospects for the weakest issuers.

4%

5 2%

0 0% − Default rates. The 12 month-

Oct-18 Apr-19 Oct-19 Apr-20 Oct-20 Apr-21 Oct-21

trailing speculative-grade default

Data as of Nov. 30, 2021 (OLCW). Parent only. Source: S&P Global Ratings Research .

rates decreased in October across

EM (see chart). EEMEA default

12 Month-Trailing Speculative-Grade Default Rates Fell Across The Region rate remained at 0%.

8

EM Asia (ex. China) EEMEA Latin America Emerging Markets (ex. China) − For more information, see

7 Weakest Links Have Fallen Over

6 Latin America, 3.25%

50% To Date In 2021

5

Emerging Markets (ex. China), Dec. 14, 2021.

Default Rate (%)

4

2.38%

3

EM Asia (ex. China), 2.17%

2

1 EEMEA, 0.00%

0

C Aug-18 Aug-19 Aug-20 Aug-21

CreditPro data as of Oct. 31, 2021. Default rates are trailing 12-month speculative-grade default rates. Source: S&P Global Ratings Research and S&P Global Market

Intelligence's CreditPro®.

53Rating Actions | Defaults

Year-End Global Corporate Defaults By Reason

Bankruptcy-Related

Distressed Exchanges / Out-Of-Court Restructuring

300 Missed principal/interest payments and default on financial obligations

Regulatory Intervention

Number Of Defaults

250

Confidential

200

150

100

50

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

*Data as of Nov. 30, 2021. Data has been updated to reflect confidential issuers. Excludes sovereigns, includes Greater China, and Red Chip companies. Source: S&P Global Ratings Research and S&P Global

Year-End EM 16 Corporate Defaults By Reason

Bankruptcy-Related Distressed Exchanges / Out-Of-Court Restructuring Missed principal/interest payments and default on financial obligations Regulatory Intervention Confidential

30

25

20

Number Of Defaults

15

10

5

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

Year

*Data as of Nov. 30, 2021. Data has been updated to reflect confidential issuers. Excludes sovereigns, includes Greater China, and Red Chip companies. Source: S&P Global Ratings Research and S&P Global Market

54Related Research

EMs | Related Research

Weakest Links Have Fallen Over 50% To Date In 2021, Dec. 14, 2021

Research Update:Turkey Outlook Revised To Negative On Uncertain Policy Direction Amid Rising External Risks; Ratings Affirmed, Dec. 10, 2021

Default, Transition, and Recovery: 2020 Annual Emerging And Frontier Markets Corporate Default And Rating Transition Study, Dec. 9, 2021

COVID-19 Impact: Key Takeaways From Our Articles, Dec. 8, 2021

Global Actions On Corporations, Sovereigns, International Public Finance, And Project Finance To Date In 2021, Dec. 7, 2021

Global Corporate Default Tally Remains At 67 As Defaults Continue To Slow, Dec. 2, 2021

Global Credit Outlook 2022: Aftershocks, Future Shocks, And Transitions, Dec. 1, 2021

Credit Conditions: Emerging Markets: Inflation, The Unwelcome Guest, Dec. 1, 2021

Emerging Markets Will Inflation Be The Next Pandemic?, Dec. 1, 2021

Economic Outlook Emerging Markets Q1 2022: Recovery Isn't Yet Complete While COVID-19 And Inflation Risks Remain Front And Center, Nov. 30,

2021

Economic Outlook EMEA Emerging Markets Q1 2022: High Inflation And COVID-19 Threaten To Slow Recovery, Nov. 30, 2021

Economic Outlook Latin America Q1 2022: High Inflation And Labor Market Weakness Will Keep Risks Elevated In 2022, Nov. 30, 2021

'BBB' Pulse: The Future Looks Bright As Potential Rising Stars Shoot Up, Nov. 24, 2021

Caucasus And Central Asian Economies Look To Commodities And Domestic Demand To Emerge From The Pandemic, Nov. 11, 2021

56EMs | Contacts

Economics Global Paul F Gruenwald, New York, +1-212-438-1710, paul.gruenwald@spglobal.com

Emerging Markets Satyam Panday, New York, +1-212-438-6009, Satyam.panday@spglobal.com

EM Asia Vishrut Rana, Singapore, +65-6216-1008, vishrut.rana@spglobal.com

EM Europe, Middle-East & Africa Tatiana Lysenko, Paris, +33-14-420-6748, tatiana.lysenko@spglobal.com

Latin America Elijah Oliveros-Rosen, New York, +1-212-438-2228, elijah.oliveros@spglobal.com

Research Global Alexandra Dimitrijevic, London, +44-20-7176-3128, alexandra.dimitrijevic@spglobal.com

Emerging Markets Jose Perez-Gorozpe, Mexico City, +52-55-5081-4442, jose.perez-gorozpe@spglobal.com

Credit Market Research Patrick Drury Byrne, Dublin, +353-1- 568-0605, Patrick.drurybyrne@spglobal.com

Ratings Performance Analytics Nick Kraemer, New York, +1-212-438-1698, nick.kraemer@spglobal.com

Lyndon Fernandes, lyndon.fernandes@spglobal.com

Research Support

Nivritti Mishra, nivritti.mishra@spglobal.com

57You can also read