Differences of Opinion and the Cross Section of Stock Returns

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE JOURNAL OF FINANCE • VOL. LVII, NO. 5 • OCTOBER 2002

Differences of Opinion and the Cross Section

of Stock Returns

KARL B. DIETHER, CHRISTOPHER J. MALLOY,

and ANNA SCHERBINA*

ABSTRACT

We provide evidence that stocks with higher dispersion in analysts’ earnings fore-

casts earn lower future returns than otherwise similar stocks. This effect is most

pronounced in small stocks and stocks that have performed poorly over the past

year. Interpreting dispersion in analysts’ forecasts as a proxy for differences in

opinion about a stock, we show that this evidence is consistent with the hypothesis

that prices will ref lect the optimistic view whenever investors with the lowest

valuations do not trade. By contrast, our evidence is inconsistent with a view that

dispersion in analysts’ forecasts proxies for risk.

IN THIS PAPER WE ANALYZE THE ROLE of dispersion in analysts’ earnings forecasts

in predicting the cross section of future stock returns. We find that stocks

with higher dispersion in analysts’ earnings forecasts earn significantly lower

future returns than otherwise similar stocks. In particular, a portfolio of

stocks in the highest quintile of dispersion underperforms a portfolio of stocks

in the lowest quintile of dispersion by 9.48 percent per year. This effect is

strongest in small stocks, and stocks that have performed poorly over the

past year. Our results are robust to various risk-adjustment techniques, and

are inconsistent with an interpretation of dispersion in analysts’ forecasts as

a proxy for risk.

We postulate that dispersion in analysts’ earnings forecasts can be viewed

as a proxy for differences of opinion among investors. Differences of opin-

ion are typically modeled via dogmatic beliefs or asymmetric information

sets, and have been included in numerous models that relax the standard

* Diether and Malloy are at the Graduate School of Business, University of Chicago; Scherbina

is at Harvard Business School. This paper combines results from two earlier papers: “Analyst

Disagreement and the Cross Section of Stock Returns” by Karl B. Diether and Christopher J.

Malloy and “Stock Prices and Differences of Opinion: Empirical Evidence that Prices Ref lect

Optimism” by Anna Scherbina. The authors thank Nick Barberis, Kent Daniel, Doug Diamond,

Eugene Fama, Rick Green ~the editor!, Kathleen Hagerty, Gilles Hilary, Ravi Jagannathan,

Robert Korajczyk, Owen Lamont, Joel Lander, Robert MacDonald, Cade Massey, Lior Menzly,

Toby Moskowitz, Jeremy Nalewaik, Lubos Pastor, Chris Polk, Todd Pulvino, David Robinson,

Richard Thaler, Beverly Walther, Volker Wieland, Andy Wong, and an anonymous referee. Data

on analysts’ forecasts was provided by I0B0E0S Inc. under a program to encourage academic

research. All remaining errors are our own.

21132114 The Journal of Finance

assumption of homogeneous expectations.1 When included in models in place

of the standard assumption of homogeneous expectations, heterogeneous

beliefs can change the stock market equilibria. For example, Williams ~1977!

and Goetzmann and Massa ~2001! show that heterogeneous beliefs can

affect aggregate market returns, while Miller ~1977!, Jarrow ~1980!, May-

shar ~1982!, Diamond and Verrecchia ~1987!, Morris ~1996!, Viswanathan

~2000!, and Chen, Hong, and Stein ~2001! produce cross-sectional asset

pricing predictions. And yet, to date there has been little empirical re-

search to investigate how differences of opinion affect asset prices. Since

many of the theoretical papers that incorporate differences of opinion pro-

duce conf licting cross-sectional implications, the debate can only be re-

solved with a careful empirical investigation. Our paper takes a step in

this direction.

The theoretical debate centers on the intuitively appealing idea ~set forth

by Miller ~1977!! that prices will ref lect a more optimistic valuation if pes-

simistic investors are kept out of the market by high short-sale costs. In

Miller ’s model ~as in other price-optimism models such as Morris ~1996!,

Chen et al. ~2001!, and Viswanathan ~2000!!, optimists hold the stock be-

cause they have the highest valuations. They suffer losses in expectation

since the best estimate of the stock value is the average opinion. These price-

optimism models suggest that the bigger the disagreement about a stock’s

value, the higher the market price relative to the true value of the stock, and

the lower its future returns. By contrast, this predicted upward bias in prices

disappears in models such as Diamond and Verrecchia ~1987! and Hong and

Stein ~2000! that introduce inf luential rational agents. The Diamond and

Verrecchia model depends on the existence of a perfectly rational market

maker with unlimited computational abilities who can instantaneously es-

timate the unbiased stock value, conditional on all publicly available infor-

mation. On the other hand, the Hong and Stein result relies on perfectly

rational arbitrageurs that can eliminate mispricing, perhaps a questionable

assumption in light of the burgeoning literature on the limits to arbitrage.

For example, Shleifer and Vishny ~1997!, Gromb and Vayanos ~2001!, and

Chen et al. provide compelling theoretical explanations why arbitrageurs

may fail to close the arbitrage opportunity.

In light of the strong assumptions behind the models that predict unbi-

ased prices when opinions diverge, perhaps it is not surprising that our

results strongly support the basic Miller ~1977! prediction. While we use

dispersion in analysts’ earnings per share forecasts as a proxy for differ-

ences of opinion, Chen et al. ~2001! use breadth of mutual fund ownership as

a measure of the magnitude of disagreement among investors and come to

the same conclusion. The authors find that reductions ~increases! in breadth

of ownership lead to lower ~higher! future returns, as Miller would predict.

1

Harris and Raviv ~1993! were the first to explicitly model investors who were dogmatic

about their beliefs. However, their model attempts to explain trading volume rather than stock

prices.Differences of Opinion 2115

In addition, Lee and Swaminathan’s ~2000! finding that higher trading vol-

ume, another possible proxy for differences of opinion, predicts lower future

returns is consistent with the Miller story as well.

On a more general level, given boundedly rational agents and limited ar-

bitrage, any friction that prevents the revelation of negative opinions will

produce the upward bias in prices that we find in the data. For example, we

provide evidence that the incentive structure of analysts ~which discourages

analysts with poor outlooks from voicing their opinions! can be viewed as an

alternative mechanism to the short-sale constraints emphasized in the Miller

~1977! model.

Finally, our results strongly reject the interpretation of dispersion in an-

alysts’ forecasts as a measure of risk. While we show that dispersion is pos-

itively related to earnings variability, standard deviation in returns, and

market b, the strong negative relation between dispersion and future re-

turns is hard to reconcile within a risk-based framework. In fact, Gebhardt,

Lee, and Swaminathan ~2001! include dispersion in analysts’ forecasts as

one of their proxies for risk in their attempts to explain implied cost of

capital estimates, and are surprised to find the same negative relation that

we document here. However, they do not examine the source and robustness

of this result in any depth. Other prior evidence of a dispersion effect is

mixed. Cragg and Malkiel ~1982! report a positive relation between disper-

sion in forecasts and future returns, but they do so using an extremely lim-

ited sample ~including only 175 companies, with yearly forecasts from 1961

to 1969!. By contrast, Ackert and Athanassakos ~1997! provide evidence that

standard deviation in analysts’ forecasts is negatively related to future re-

turns, but do so using a sample of only 167 firms.

The layout of the paper is as follows. In the next section, we discuss three

competing hypotheses, the data, and our sample characteristics. Section II

describes our procedure of forming portfolios on the basis of dispersion in

analysts’ forecasts and presents our initial results. Section III explores a

risk-based explanation for our findings, while Section IV presents various

robustness checks. Finally, Section V evaluates potential explanations for

our results, and Section VI provides a summary and concludes.

I. Methodology

A. Competing Hypotheses

Our main objective in this paper is to analyze the role of dispersion in

analysts’ earnings forecasts in predicting the cross section of future stock

returns. In particular, we test three competing hypotheses about the rela-

tion between dispersion in forecasts and future returns.

The first hypothesis views dispersion in forecasts as a proxy for differ-

ences of opinion among investors. This hypothesis centers on Miller’s ~1977!

conjecture that whenever stock valuations differ, equity prices tend to re-

f lect the view of the more optimistic investors, leading to low future returns.2116 The Journal of Finance

Miller argues that when opinions diverge and short-sale constraints bind,

investors with pessimistic valuations do not sell the stock, and optimistic

demand pushes stock prices up. Miller’s verbal model assumes that inves-

tors are boundedly rational in the sense that they are overconfident about

their own valuations.2 However, his argument can be easily modified to ac-

commodate investors who are not overconfident, but rather make inaccurate

inferences about others’ signals. For example, if the short-sale constraint

binds, an informed investor with a low valuation will not sell the stock.

However, an informed investor may also stay out of the market if she agrees

with the market price. Boundedly rational market participants may errone-

ously assume that the informed investor did not trade simply because her

valuation equaled the market price. If so, boundedly rational traders will

not revise their valuations downward after observing that the informed in-

vestor did not trade, and the stock price will remain unchanged. In this

scenario, negative information will not be appropriately incorporated, and

the market price will be upwardly biased.

The first hypothesis suggests that the larger the disagreement about a

stock’s value ~either caused by overconfidence or by inaccurate inferences

about others’ signals!, the higher the market price relative to the true value

of the stock, and the lower its future returns. And although Miller’s ~1977!

model focuses on short-sale constraints, any friction that prevents the rev-

elation of negative opinions will produce this negative relation between dis-

persion in forecasts and future returns.

The second hypothesis also views dispersion in forecasts as a proxy for

differences of opinion, but states that market prices will be unbiased when

opinions about the correct valuation diverge, and so future returns will be

independent of the current level of disagreement about the stock value. This

prediction is stated in Diamond and Verrecchia ~1987!. As a price-setting

mechanism, the authors model a rational market-maker who correctly sets

bid and ask prices, conditioned on the possibility that some informed inves-

tors with low valuations are constrained from selling stock. The outcome is

that stock prices are unbiased: No trading profits can be made based on the

publicly available information. The key assumption of the model is that the

market-maker has perfect knowledge of his economic environment and can

perform Bayesian updating in the short time between two consecutive trades.

Similarly, Hong and Stein ~2000! achieve unbiased prices by introducing

competitive, risk-neutral, and perfectly rational arbitrageurs who do not face

short-sale constraints. The arbitrageurs correctly infer the expected stock

value from the actions of informed overconfident short-sale-constrained in-

vestors in a price auction. The market clears at the price that is equal to

expected stock value. Thus, both of these models predict no relation between

observed dispersion in analysts’ forecasts and future returns.

2

See Gervais, Heaton, and Odean ~2000! and Daniel, Hirshleifer, and Subrahmanyam ~2001!

for models that explicitly model overconfidence; in these models, investors are overconfident in

the sense that they overestimate the precision of their private signals.Differences of Opinion 2117

The final hypothesis views dispersion in analysts’ earnings forecasts as a

proxy for risk. Investors who are not well diversified will demand to be

compensated for the idiosyncratic risk of the securities they hold ~see, e.g.,

Merton ~1987!!. Since dispersion in analysts’ forecasts likely indicates a more

volatile, less predictable earnings stream, stocks with higher dispersion in

analysts’ forecasts should earn higher future returns, and dispersion in an-

alysts’ forecasts will hold explanatory power beyond the standard risk factors.

In summary, the first hypothesis predicts a negative relation between dis-

persion and future returns. The second hypothesis predicts no relation. And

the third hypothesis predicts a positive relation.

B. Data and Sample Characteristics

Returns are drawn from the Center for Research in Securities Prices ~CRSP!

Monthly Stocks Combined File, which includes NYSE, AMEX, and Nasdaq

stocks. For many of the tests in the paper, firms must also have data in

COMPUSTAT on book equity for the fiscal year ending in calendar year

t 2 1.3 The data on analysts’ earnings estimates are taken from the Insti-

tutional Brokers Estimate System ~I0B0E0S!.

The nature of our inquiry makes the standard-issue I0B0E0S data set un-

suitable for our purposes because of the following reporting inaccuracy.

I0B0E0S analysts’ forecasts are adjusted historically for stock splits in order

to produce a smooth time series of earnings per share estimates. For exam-

ple, analysts’ earnings per share estimates for December 1976 are reported

on the basis of the number of shares outstanding as of today, rather than the

number of shares outstanding as of December 1976. However, after dividing

historical analysts’ forecasts by a split adjustment factor, I0B0E0S rounds

the estimate to the nearest cent. For example, for a stock that has split

10-fold, actual earnings per share estimates of 10 cents and 14 cents would

be reported as 1 cent per share each. I0B0E0S would then include an adjust-

ment factor of 10 in the Adjustment File, so that the “unadjusted” earnings

per share estimates would be 10 cents each, rather than the correct values

of 10 cents and 14 cents, respectively. The observed variance of analysts’

forecasts would then be zero, when in fact it is positive. Observations with

no dispersion in analysts’ forecasts would thus contain ex-post information

about the future success of the firm, embedded in the number of stock splits.

We conducted our analysis on the raw forecast data, unadjusted for stock

splits ~provided by I0B0E0S on request!. Had we utilized the commonly used

I0B0E0S files, we would have found that as a group, stocks with the lowest

levels of dispersion earned high abnormal returns, simply because we would

have been picking up observations of firms that did well in the future.4

3

Limiting the sample for all tests to include only those firms that have data in COM-

PUSTAT on book equity does not significantly alter any of our results.

4

We believe we are the first to document this error. This finding has important implications

for prior and subsequent empirical research that uses I0B0E0S data to investigate issues re-

lated to dispersion ~e.g., herding among security analysts!.2118 The Journal of Finance

I0B0E0S data includes U.S. Detail History and Summary History data sets.

The Summary History data set contains the summary statistics on analyst

forecasts, such as mean and standard deviation values. These variables are

calculated on the basis of all outstanding forecasts as of ~ordinarily! the

third Thursday of each month. The Detail History file contains individual

analysts’ forecasts organized by the date on which the forecast was issued.

Each record also contains a revision date, that is, the date on which the

forecast was last confirmed as accurate.

To address concerns that the U.S. Summary History file makes use of

analysts’ forecasts that are no longer current, we calculate forecast statistics

from the Detail History file and match them to the numbers in the Sum-

mary History file. We compute month-end averages and standard deviations

from the individual estimates in the Detail History file by extending each

forecast until its revision date. For example, if the forecast was made in May

and was last confirmed as accurate in July, it will be used in our computa-

tion of averages and standard deviations for May, June, and July. If an an-

alyst makes more than one forecast in a given month, only the last forecast

is used in our calculations.

In some records, a revision date precedes the actual forecast date, which

constitutes an error on the part of I0B0E0S. In this case, the forecast will be

assumed valid only for the month in which it was made. In addition, occa-

sional aberrant observations in the Detail History file are not picked up by

the Summary History file. Even given these inconsistencies, the mean and

standard deviation values calculated from the Detail History file data closely

track the values in the Summary History file. Generally, when compiling

statistics from the Detail History file, we obtain fewer monthly forecasts

than reported in the Summary History file because we assume that fore-

casts are no longer valid past the revision date, which is not the case for the

Summary History file conventions. We compute our portfolio results in Sec-

tion II using data in both the Summary History and Detail History files.

Since the results are very similar, we report only the results obtained using

the Summary History file throughout the paper.

For each stock in CRSP, we set the coverage in any given month equal to

the number of I0B0E0S analysts who provide fiscal year one earnings esti-

mates that month.5 Obviously each stock must be covered by two or more

analysts during that month, since we define dispersion as the standard de-

viation of earnings forecasts scaled by the absolute value of the mean earn-

ings forecast.

There is an unavoidable issue of data deletion when using the I0B0E0S

database, since many firms listed on CRSP are not covered by I0B0E0S.

However, LaPorta ~1996! presents evidence showing that the performance of

stocks in the I0B0E0S sample is almost identical to those in CRSP. The most

salient feature of the sample of stocks in the intersection of CRSP, COM-

5

All of the tests in this paper were replicated for different fiscal periods ~e.g., two years!.

Discussion of these and other robustness checks is presented in Section IV.Differences of Opinion 2119

Table I

Summary Statistics on Analyst Coverage:

January 1976 to December 2000

Descriptive statistics for NYSE, AMEX, and Nasdaq stocks during the period from January

1976 to December 2000. Panel A reports statistics for all stocks, while Panel B limits the sam-

ple to only eligible stocks. A stock is “eligible” to be included in our analysis if it has a one

~fiscal! year I0B0E0S earnings estimate, is covered by two or more analysts, and has a price

greater than five dollars. Panels C and D report the same statistics as in Panels A and B for

January 1983, and breaks the sample down by size decile ~formed using NYSE-based market

capitalization deciles!.

Summary Statistics for 1976–2000

Panel A: All CRSP Stocks Panel B: Eligible Stocks

Number Mean Percentage Number Mean Mean

of Size of Firms of Size No. of

Date Firms ~Millions! Eligible Firms ~Millions! Estimates

0101976 5,065 184.6 12.8 650 910.2 6.47

1201979 4,781 267.5 29.2 1,395 621.5 7.47

1201982 5,438 305.6 31.9 1,735 766.0 8.78

1201985 6,227 362.4 35.4 2,203 938.5 9.95

1201988 6,798 408.6 34.0 2,309 1,094.1 9.82

1201991 6,643 610.1 35.5 2,361 1,590.1 9.23

1201994 8,029 633.8 40.7 3,269 1,423.9 8.26

1201997 8,839 1,241.2 46.8 4,140 2,473.1 7.19

1202000 7,823 2,032.9 40.5 3,166 4,740.6 7.79

Summary Statistics by Size for 0101983

Panel C: All CRSP Stocks Panel D: Eligible Stocks

Number Mean Percentage Number Mean Mean

NYSE of Size of Firms of Size No. of

Breakpoints Firms ~Millions! Eligible Firms ~Millions! Estimates

Decile 1 2,969 15.2 4.1 123 34.1 2.76

Decile 2 517 61.2 31.9 165 62.7 3.39

Decile 3 406 96.9 50.5 205 97.8 3.81

Decile 4 323 151.5 69.3 224 151.0 4.90

Decile 5 258 229.4 79.1 204 229.2 6.79

Decile 6 231 343.3 84.0 194 343.9 8.26

Decile 7 191 528.5 89.0 170 526.8 11.22

Decile 8 173 809.1 89.0 154 809.9 13.60

Decile 9 160 1,381.2 92.5 148 1,366.2 16.91

Decile 10 165 5,709.0 92.1 152 5,079.4 19.59

PUSTAT, and I0B0E0S is that it is heavily tilted towards big stocks. As Hong,

Lim, and Stein ~2000! note, the smallest firms are simply not covered. Table I

provides an overview of the extent of analyst coverage for NYSE, AMEX, and

Nasdaq stocks. As shown in Panel A, in January of 1976, only 12.8 percent

of stocks are even eligible to be included in our sample. There is a marked2120 The Journal of Finance

deepening of coverage by the end of 1979, with the fraction of eligible firms

increasing to 29.2 percent. But Panel C shows that even by January of 1983

~the beginning point of our chosen data sample!, only 4.1 percent of firms in

the first decile are eligible for our sample. Additionally, fewer firms in our

sample are delisted for cause relative to the entire CRSP universe.6 This

suggests that financially distressed firms may be underrepresented in our

sample.

We choose the time period of January 1983 through November 2000 for

our portfolio tests in Section II for two reasons. First, by January of 1983,

the cross section of stocks has substantial variation in size and book-to-

market ratio. Second, the data in the Detail History file are not available

prior to 1983. Since we replicate portfolio results from Section II with the

Detail History file data, we need to use post-1982 data. Using the entire

sample makes our results slightly stronger.

II. Portfolio Strategies

In this section, we assign stocks to portfolios based on certain character-

istics, such as dispersion in analyst forecasts, in order to draw conclusions

about average returns for these classes of stocks. This is a standard ap-

proach in asset pricing, which reduces the variability in returns. The meth-

odology employed here was pioneered by Jegadeesh and Titman ~1993!.

Following Jegadeesh and Titman ~2001!, stocks with share price lower than

five dollars are omitted in order to ensure that the results are not driven by

small, illiquid stocks or by bid-ask bounce.

Dispersion is defined as the standard deviation of earnings forecasts scaled

by the absolute value of the mean earnings forecast. If the mean earnings

forecast is zero, then the stock is assigned to the highest dispersion category.

Excluding observations with a mean earnings forecast of zero does not sig-

nificantly affect the portfolio returns. An alternative definition of dispersion

as the ratio of standard deviation of earnings forecasts to the book equity

per share does not significantly affect our results.

Each month, we assign stocks into five quintiles based on dispersion in

analyst earnings forecasts as of the previous month. After assigning stocks

into portfolios, stocks are held for one month. We calculate the monthly

portfolio return as the equal-weighted average of the returns of all the stocks

in the portfolio. The last column of Table II shows that this sort produces a

strong negative relation between average returns and dispersion in analysts’

earnings forecasts. The annual return on the D1 2 D5 strategy is 9.48 per-

cent, and is strongly significant. Of that D1 2 D5 spread, 68.4 percent comes

from the short side of the trade, that is, the difference between medium-

dispersion stocks and high-dispersion stocks. This evidence is strongly sup-

portive of the Miller ~1977! hypothesis laid out in Section I.

6

For example, only 14.5 percent of the firms in our sample are delisted for cause ~delist

codes of 400 and above on CRSP!, compared to 30.3 percent for the universe of CRSP stocks.Differences of Opinion 2121

Table II

Mean Portfolio Returns by Size and Dispersion

in Analysts’ Forecasts

Each month stocks are sorted in five groups based on the level of market capitalization as of

the third Thursday of the previous month. Stocks in each size group are then sorted into five

additional groups based on dispersion in analyst earnings forecasts for the previous month.

Dispersion is defined as the ratio of the standard deviation of analysts’ current-fiscal-year

annual earnings per share forecasts to the absolute value of the mean forecast, as reported in

the I0B0E0S Summary History file. Stocks with a mean forecast of zero are assigned to the

highest dispersion groups, and stocks with a price less than five dollars are excluded from the

sample. Stocks are held for one month, and portfolio returns are equal-weighted. The time

period considered is February 1983 through December 2000. The table reports average monthly

portfolio returns; t-statistics in parentheses are adjusted for autocorrelation.

Mean Returns

Size Quintiles

Small Large

Dispersion All

Quintiles S1 S2 S3 S4 S5 Stocks

D1 ~low! 1.52 1.45 1.50 1.51 1.48 1.48

D2 1.12 1.40 1.41 1.18 1.35 1.36

D3 0.99 1.20 1.32 1.11 1.36 1.23

D4 0.76 1.07 1.18 1.33 1.33 1.12

D5 ~high! 0.14 0.56 0.83 1.03 1.20 0.69

D1–D5 1.37 a 0.89 a 0.67 b 0.48 0.29 0.79 a

t-statistic ~5.98! ~3.12! ~2.41! ~1.55! ~0.94! ~2.88!

Mean Dispersion

Size Quintiles

Dispersion All

Quintiles S1 S2 S3 S4 S5 Stocks

D1 ~low! 0.010 0.011 0.012 0.014 0.014 0.012

D2 0.039 0.033 0.030 0.028 0.025 0.030

D3 0.081 0.062 0.053 0.047 0.039 0.053

D4 0.172 0.125 0.103 0.086 0.067 0.105

D5 ~high! 1.256 0.963 0.813 0.722 0.462 0.852

a,b

Statistically significant at the one and five percent levels, respectively.

Table II also presents two-way cuts on size and dispersion, to test if we are

simply capturing a size effect. Each month, we assign stocks to one of five

quintiles based on the level of market capitalization as of the third Thursday

of the previous month. We rank stocks in each size quintile into five further

quintiles based on dispersion in analyst earnings forecasts as of the previous

month. Each of the 25 resulting portfolios contains an average of 113 stocks,

if the Summary History file is used.7 Table II shows that the average monthly

7

We use conditional sorts here for consistency, since some of our later three-way sorts result

in portfolios that are very thin if we use independent sorts. Our results are not significantly

affected if we use independent sorts instead.2122 The Journal of Finance

Table III

Mean Portfolio Returns by NYSE Market Capitalization Deciles

Each month stocks in each NYSE-based market capitalization decile ~which is determined as of

the third Thursday of the previous month! are sorted into five groups based on dispersion in

analyst earnings forecasts for the previous month. Dispersion is defined as the ratio of the

standard deviation of analysts’ current-fiscal-year annual earnings per share forecasts to the

absolute value of the mean forecast, as reported in the I0B0E0S Summary History file. Stocks

with a mean forecast of zero are assigned to the highest dispersion groups, and stocks with a

price less than five dollars are excluded from the sample. Stocks are held for one month, and

portfolio returns are equal-weighted. Only portfolios in the largest seven deciles are reported

since there are fewer than eight stocks on average within each size0dispersion portfolio for

size deciles 1 to 3. The time period considered is February 1983 through December 2000. The

table reports average monthly portfolio returns; t-statistics in parentheses are adjusted for

autocorrelation.

Mean Returns

NYSE Market Capitalization Deciles

~Average Number of Stocks in Each Portfolio!

Dispersion 4 5 6 7 8 9 10

Quintiles ~27! ~47! ~68! ~91! ~119! ~149! ~189!

D1 ~low! 1.21 1.22 1.34 1.42 1.50 1.47 1.45

D2 1.41 1.51 1.26 1.39 1.38 1.18 1.31

D3 1.38 1.31 1.41 1.04 1.30 1.16 1.20

D4 0.72 0.91 0.96 1.11 0.88 1.08 1.18

D5 ~high! 0.61 0.53 0.33 0.32 0.49 0.64 1.03

D1–D5 0.60 0.69 1.01 a 1.09 a 1.01 a 0.84 b 0.41

t-statistic ~1.48! ~1.86! ~3.08! ~3.61! ~3.93! ~2.33! ~1.49!

a,b

Statistically significant at the one and five percent levels, respectively.

return differential between low- and high-dispersion portfolios declines as

the average size increases. While the return differential between the low-

and high-dispersion stocks is positive and highly significant for the smaller

stocks, it becomes insignif icant for stocks in the two highest market-

capitalization quintiles.8 In particular, the D1 2 D5 strategy for the smallest

quintile earns an enormous 16.4 percent annual return on average. Thus, it

does not appear that we are simply picking up a size effect, since the two-

way sorts still produce a strong negative relation between average returns

and dispersion for the first three quintiles.

However, I0B0E0S-based market-capitalization quintiles might be mislead-

ing because the universe of I0B0E0S firms is comprised of only relatively

large firms—especially among the firms covered by at least two analysts. To

be consistent with reporting convention, we also form portfolios using NYSE-

based market capitalization deciles. Table III reports returns on these port-

8

Results do not change significantly when data are restricted to stocks covered by at least

three analysts.Differences of Opinion 2123 folios. There are not enough stocks in the three lowest deciles to produce representative average portfolio returns for these classes of stocks. The re- turn differential for the fifth through ninth NYSE size deciles turns out to be statistically significant, indicating that the dispersion result holds for even relatively large stocks. A. Sorting by Size and Book-to-Market In this section, we triple-sort on size, book-to-market ~BE0ME ! ratio, and dispersion to test if we are merely picking up a book-to-market effect in returns. Since low-book-to-market stocks tend to have higher levels of mar- ket capitalization, we try to control for the strong size-related pattern ob- served in Table II ~namely, that within small stocks, we see a huge return differential between low- and high-dispersion stocks! by sorting on size and book-to-market. Stocks are first sorted into three categories based on the level of market capitalization at the end of the previous month. Within each size category, the stocks are sorted into three groups based on the book-to- market ratio, and finally into three dispersion groups within each resulting group. Book equity ~BE ! is defined as the COMPUSTAT book value of stock- holders’ equity, plus balance sheet deferred taxes and investment tax credit ~if available!, minus the book value of preferred stock. Depending on avail- ability, we use redemption, liquidation, or par value ~in that order! to esti- mate the book value of preferred stock. To insure that the book equity figure is known to the market before the returns that it is used to explain, we match the yearly book equity figure for all fiscal years ending in calendar year t 2 1 with returns starting in July of year t. This figure is then divided by market capitalization ~ME ! at month t 2 1 to form the BE0ME ratio, so that the BE0ME ratio is updated each month. Finally, within each size and book-to-market group, stocks are sorted into three further subdivisions based on dispersion in earnings-per-share forecasts as of the previous month. Table IV presents the returns on the resulting 27 portfolios. Note that each portfolio contains an average of 55 stocks. The return differential be- tween low- and high-dispersion stocks is still significant in four of the nine categories, indicating that the dispersion effect is not simply capturing a book-to-market effect. Again we observe the strong size pattern first de- picted in Table II, with small stocks exhibiting the largest return differen- tial. However, no clear pattern emerges with respect to book-to-market ratios. While the return differential between low- and high-dispersion stocks is larger for value stocks ~those with high BE0ME ratios!, this result is not over- whelming. On the other hand, the lower half of the table is more revealing. In particular, value stocks have much larger average dispersion in forecasts than growth stocks, implying that book-to-market ratios are positively re- lated to dispersion in analysts’ forecasts. Despite having lower average values of dispersion, growth stocks in the high-dispersion portfolios earn returns almost as low as value stocks, indi- cating that the same amount of dispersion in analysts’ earnings per share

2124 The Journal of Finance

Table IV

Mean Portfolio Returns by Size, Book-to-Market, and Dispersion

Each month stocks are sorted into three groups based on the level of market capitalization at

the end of the previous month. Each size group is then sorted into three book-to-market groups.

The book-to-market ratio is computed by matching the yearly BE figure for all fiscal years

ending in calendar year t 2 1 to returns starting in July of year t; this figure is then divided by

market capitalization at month t 2 1 to form the book-to-market ratio, so that the book-to-

market ratio is updated each month. Each size and book-to-market group is further sorted into

three dispersion groups. Dispersion is defined as the ratio of the standard deviation of analysts’

current-fiscal-year annual earnings per share forecasts to the absolute value of the mean fore-

cast, as reported in the I0B0E0S Summary History file. Stocks with a mean forecast of zero are

assigned to the highest dispersion groups, and stocks with a price less than five dollars are

excluded from the sample. Stocks are held for one month, and portfolio returns are equal-

weighted. The sample period is February 1983 through December 2000; t-statistics in paren-

theses are adjusted for autocorrelation.

Mean Returns

Low Book-to-Market Medium Book-to-Market High Book-to-Market

Small Mid Large Small Mid Large Small Mid Large

Dispersion Cap Cap Cap Cap Cap Cap Cap Cap Cap

Low 1.35 1.42 1.40 1.64 1.50 1.32 1.50 1.58 1.42

Medium 1.27 1.40 1.20 1.29 1.11 1.27 1.13 1.46 1.37

High 0.73 1.28 1.38 0.67 0.86 1.12 0.70 1.10 1.34

Low–high 0.63 b 0.14 0.02 0.96 a 0.64 b 0.21 0.80 a 0.48 0.08

t-statistic ~2.10! ~0.47! ~0.06! ~4.09! ~2.37! ~0.96! ~4.09! ~1.70! ~0.25!

Mean Dispersion

Low Book-to-Market Medium Book-to-Market High Book-to-Market

Small Mid Large Small Mid Large Small Mid Large

Dispersion Cap Cap Cap Cap Cap Cap Cap Cap Cap

Low 0.04 0.03 0.02 0.05 0.03 0.02 0.10 0.04 0.03

Medium 0.08 0.05 0.03 0.09 0.05 0.04 0.21 0.11 0.07

High 0.49 0.34 0.20 0.56 0.37 0.26 1.04 0.86 0.59

a,b

Statistically significant at the one and five percent levels, respectively.

forecasts would cause lower returns for growth stocks than value stocks.

This is not surprising, given that the same amount of disagreement about

earnings per share should translate into a higher level of disagreement about

the intrinsic value of a growth stock as compared to a value stock. This, in

turn, would translate into a higher price run-up for growth stocks, and

lower subsequent returns. However, low-dispersion growth stocks earn lower

returns than low-dispersion value stocks because of the famous value pre-

mium, and that translates into lower spreads between low- and high-

dispersion portfolios for growth stocks.Differences of Opinion 2125

Table V

Mean Portfolio Returns by Size, Momentum, and Dispersion

Each month stocks are sorted into three groups based on the level of market capitalization at

the end of the previous month. Each size group is then sorted into three momentum groups;

momentum is computed based on past returns from t 2 12 to t 2 2, where “Losers” is an

equal-weighted portfolio of stocks in the worst-performing 33 percent. Each size and momen-

tum group is further sorted into three dispersion groups. Dispersion is defined as the ratio of

the standard deviation of analysts’ current-fiscal-year annual earnings per share forecasts to

the absolute value of the mean forecast, as reported in the I0B0E0S Summary History file.

Stocks with a mean forecast of zero are assigned to the highest dispersion groups, and stocks

with a price less than five dollars are excluded from the sample. Stocks are held for one month,

and portfolio returns are equal-weighted. The sample period is February 1983 through Decem-

ber 2000; t-statistics in parentheses are adjusted for autocorrelation.

Mean Returns

Losers Winners

Small Mid Large Small Mid Large Small Mid Large

Dispersion Cap Cap Cap Cap Cap Cap Cap Cap Cap

Low 0.92 1.02 1.27 1.29 1.45 1.36 1.79 1.79 1.54

Medium 0.47 0.69 1.12 1.11 1.32 1.18 1.84 1.80 1.58

High 0.09 0.63 0.93 0.82 1.22 1.06 1.56 1.81 1.73

Low–high 0.82 a 0.40 0.35 0.48 a 0.23 0.30 0.23 20.02 20.19

t-statistic ~3.65! ~1.56! ~1.46! ~2.76! ~1.12! ~1.61! ~1.17! ~20.10! ~20.83!

Mean Dispersion

Losers Winners

Small Mid Large Small Mid Large Small Mid Large

Dispersion Cap Cap Cap Cap Cap Cap Cap Cap Cap

Low 0.10 0.05 0.03 0.04 0.03 0.02 0.03 0.02 0.02

Medium 0.21 0.10 0.06 0.09 0.05 0.04 0.06 0.15 0.04

High 1.18 0.85 0.55 0.61 0.33 0.22 0.39 0.28 0.25

a,b

Statistically significant at the one and five percent levels, respectively.

B. Sorting by Size and Momentum

Our final portfolio strategy entails a three-way cut on size, momentum,

and dispersion, to rule out the possibility that the momentum effect docu-

mented in Jegadeesh and Titman ~1993! is driving our results. Stocks are

first sorted into three categories based on the level of market capitalization

at the end of the previous month. Within each size category, the stocks are

sorted into three groups based on past returns from t 2 12 to t 2 2 ~as in

Fama and French ~1996!!. Lastly, within each size and momentum group,

stocks are sorted into three further subdivisions based on dispersion in

earnings-per-share forecasts as of the previous month.

Table V presents the returns on the resulting 27 portfolios. Again the

return differential between low- and high-dispersion stocks is still strongly2126 The Journal of Finance

significant in two of the nine categories, indicating that the dispersion effect

is not simply capturing a momentum effect. However, a clear pattern emerges

with respect to momentum, as the return differential between low- and high-

dispersion stocks is strongest in stocks that have performed poorly over the

past year ~“losers”!. For example, the D1 2 D3 strategy for the smallest

quintile of losers earns a 9.84 percent average annual return.

III. Regression Tests

Fama and French ~1996! show that sorting stocks on variables such as BE0ME

~the book-to-market ratio!, E0P ~the earnings-to-price ratio!, or C0P ~the cash-

f low-to-price ratio! can produce a strong ~in their case, positive! ordering of

returns across deciles. They also argue, however, that estimates of three-

factor time-series regressions indicate that the three-factor model captures these

patterns in average returns. The regression intercepts are uniformly small,

and the Gibbons, Ross, and Shanken ~~1989!, hereafter, GRS! tests never

come close to rejecting the hypothesis that the three-factor model describes

average returns. Along these lines, we employ similar tests to see if the

three-factor model can capture the return patterns observed in Tables II to V.

A. Multifactor Time-Series Tests

Fama and French ~1996! argue that many of the CAPM average-return

anomalies are related, and that they are captured by the three-factor model

in Fama and French ~1993!. In the model, R M 2 R F is the excess return on

a proxy for the market portfolio, SMB is the difference between the return

on a portfolio of small stocks and the return on a portfolio of large stocks,

and HML is the difference between the return on a portfolio comprised of

high book-to-market stocks and the return on a portfolio comprised of low

book-to-market stocks. The variable HML represents the value premium;

high book-to-market stocks are value stocks, and low book-to-market stocks

are growth stocks. Similarly, the variable SMB represents the size premium.9

Believers in the three-factor model suggest that it is an equilibrium pric-

ing model in the spirit of Merton’s ~1973! intertemporal capital asset pricing

model ~ICAPM!. In an ICAPM framework, investors care about market risk,

but they also care about hedging against more specific aspects of their in-

vestment consumption decisions. For example, investors may wish to hedge

against the relative prices of consumption goods. In this view of the three-

factor model, SMB and HML are viewed as portfolios that proxy for factors

that are of special hedging concern to investors, and bi , s i , and h i are factor

loadings or sensitivities, and E~R Mt ! 2 R Ft , E~SMBt !, E~HML t ! are ex-

pected risk premiums. The main testable implication of the model in this

setting is that ai 5 0 for all assets. We test this hypothesis using a formu-

lation of the Hotelling t 2 test ~GRS ~1989!!. Extensions of the model ~see,

9

See Fama and French ~1996! for details on the construction of these factors.Differences of Opinion 2127 e.g., Carhart ~1997!! add a momentum factor to this model, included to cap- ture the medium-term continuation of returns documented in Jegadeesh and Titman ~1993!. We include the variable UMD to capture the momentum pre- mium; it equals the difference between the return on a portfolio comprised of stocks with high returns from t 2 12 to t 2 2 and the return on a portfolio comprised of stocks with low returns from t 2 12 to t 2 2. Table VI reports estimates of three- and four-factor time-series regres- sions for monthly excess returns on five equal-weighted portfolios formed on dispersion in analysts’ forecasts. The estimated intercepts indicate that the three-factor model leaves a large negative unexplained return for the portfolio of stocks in the highest dispersion quintile. The loadings indicate that low-dispersion stocks behave like big, value stocks ~they load less on SMB but heavily on HML!, while high-dispersion stocks behave like small, value stocks. An important point to mention, however, is that these load- ings give a potentially misleading picture of the risk characteristics of these stocks, because they are highly variable. For example, in results not reported here, we find that in the sample period from 1983 to 1999, high- dispersion stocks load very heavily on HML, while low-dispersion stocks load more on growth. However, in the year 2000, these patterns were strongly reversed, as high-dispersion stocks behaved very much like growth stocks. The GRS test rejects the hypothesis that the three-factor model explains the average returns on the five dispersion quintiles. The rejection of the three factor model is testimony to the explanatory power of the regressions ~the average of the five regression R 2 is 0.932!, so that even small intercepts are distinguishable from zero. Note, however, that the intercept on the high- dispersion quintile is a nontrivial 0.58 percent. Table VI also reports estimates of the four-factor time-series regression for monthly excess returns on the dispersion quintiles. Again, the estimated intercepts indicate that the model leaves a large negative unexplained re- turn for the portfolio of stocks in the highest dispersion quintile. Meanwhile, the estimated intercept on the lowest dispersion quintile is positive and mar- ginally significant. The pattern of loadings is identical to the pattern found in the three-factor regressions, except that the stocks in the highest disper- sion quintile now behave like small, distressed losers ~they load more on SMB, HML, and less on UMD!. This lowers the negative unexplained return for the portfolio of stocks in the highest decile, but the model still predicts higher postformation returns on these stocks. The GRS test again rejects the hypothesis that the four-factor model explains the average returns on the dispersion quintiles. Thus it appears that neither model can account for the return patterns displayed in Tables II to V. B. Explaining Dispersion In this section, we run a series of Fama and MacBeth ~1973! cross- sectional regressions in order to illustrate the relation between dispersion in

2128 The Journal of Finance

Table VI

Time-Series Tests of Three- and Four-Factor Models

for Dispersion Equal-Weighted Quintiles

This table reports estimates of the Fama–French three-factor model, as well as a four-factor

model, E~R it 2 R Ft ! 5 biM ~R M 2 R F ! 1 s i SML t 1 h i HML t 1 m i UMDt , for monthly excess

returns on the equal-weighted dispersion quintiles. The market premium ~R M 2 R F ! uses the

CRSP NYSE0AMEX0Nasdaq value-weighted index. The variables HML and SMB are created

using the same methodology as Fama and French ~1996!. The momentum premium ~UMD! is

the difference between the return on a portfolio comprised of stocks with high returns from

t 2 12 to t 2 2 and the return on a portfolio comprised of stocks with low returns from t 2 12

to t 2 2. The dispersion equal-weighted quintiles are formed as in Table II. The sample period

is February 1983 to December 2000. Stocks with a price less than five dollars are excluded from

the sample, and t-statistics ~Newey-adjusted! are in parentheses.

Factor Sensitivities

Alpha Adj. R 2

Portfolio ~%! RM 2 RF SMB HML UMD ~%!

D1 ~low-dispersion! 0.13 1.06 0.32 0.26 88.42

~0.88! ~39.78! ~3.17! ~2.83!

0.27 1.06 0.33 0.21 20.13 89.18

~2.14! ~43.33! ~4.17! ~2.50! ~22.01!

D2 0.03 1.06 0.40 0.22 92.64

~0.30! ~44.13! ~5.76! ~2.95!

0.17 1.06 0.41 0.17 20.12 93.35

~1.57! ~56.96! ~7.98! ~2.44! ~22.81!

D3 20.07 1.08 0.49 0.15 95.08

~20.82! ~42.71! ~6.59! ~2.91!

0.09 1.07 0.51 0.09 20.14 95.94

~1.26! ~52.92! ~9.46! ~1.98! ~24.12!

D4 20.18 1.11 0.67 0.14 96.47

~22.56! ~52.79! ~12.74! ~3.31!

20.03 1.10 0.68 0.08 20.14 97.17

~20.40! ~63.19! ~19.12! ~2.00! ~25.21!

D5 ~high-dispersion! 20.58 1.15 0.88 0.13 93.74

~24.78! ~38.53! ~16.16! ~3.19!

20.35 1.15 0.91 0.05 20.20 94.92

~22.62! ~45.66! ~26.12! ~1.11! ~25.18!

GRS~3F! 5 5.51

GRS~4F! 5 2.62

analysts’ forecasts and various fundamentals. We also explore how disper-

sion in forecasts is distinct from other common measures of risk, such as

standard deviation of returns, market b, earnings variability, and so forth.

The goal is to determine what exactly makes dispersion in analysts’ fore-

casts such an important valuation indicator.Differences of Opinion 2129

Specifically, we attempt to disentangle the effect of dispersion in analysts’

forecasts from stock fundamentals and additional measures of risk by per-

forming a series of yearly cross-sectional regressions of dispersion ~mea-

sured seven months before the end of the fiscal year! on various lagged firm

characteristics. Aside from the fiscal year-end lagged values of market cap-

italization, book-to-market ratio, sales-to-assets ratio, and debt-to-book ra-

tio, we include momentum ~the return from t 2 12 months to t 2 2 months!,

market b ~estimated using the past 36 to 60 months of data!, residual cov-

erage, the standard deviation of daily returns over the past 250 days ~lagged

one month!, the average adjusted volume over the past 250 days ~lagged one

month!, the average adjusted turnover over the past 250 days ~lagged one

month!, the mean age of the forecasts, and a measure of earnings variability

~s~eps!!. Residual coverage is the residual from yearly regressions of ln~1 1

analyst coverage! on ln~M ! and ln~B0M !. A firm’s adjusted volume is the

daily volume from the last 250 days, divided by the mean volume of the

firm’s exchange; adjusted turnover is defined similarly. Finally, s~eps! is

the standard deviation of earnings per share, divided by the absolute value

of mean earnings per share over the past five years; s~eps! is lagged one

year. We run the regressions yearly, rather than monthly, because the dis-

persion measures for each stock are highly autocorrelated.

The results, reported in Table VII, cast doubt on the interpretation of

dispersion in analysts’ forecasts as a proxy for risk. Dispersion is strongly

positively related to market b, earnings variability, and standard deviation

of past returns. Since these variables are commonly used measures of risk,

we expect them to be positively related to returns. Therefore, the negative

relation between dispersion and future returns is hard to explain within a

traditional risk-based framework. Confirming the evidence presented in

Tables II to IV, dispersion is positively related to BE0ME, and negatively

related to size and momentum. Additionally, dispersion is positively related

to leverage, turnover, and volume, but negatively related to sales and the

mean age of the forecasts. Controlling for firm size, we find that dispersion

is positively correlated with analyst coverage, indicating that there is a high

demand for additional opinions in situations where earnings are difficult to

forecast. Based on these results, we feel that the correct interpretation of

dispersion in analyst earnings forecasts is as a proxy for differences in opin-

ion among investors. For example, turnover is often used as a proxy for

differences of opinion, and we find these two measures to be strongly posi-

tively related in our cross-sectional regressions.

IV. Robustness Checks

To ascertain that the persistently high returns we have documented thus

far are not caused by a statistical f luke or an obvious explanation, we em-

ploy additional trading strategies and regression tests to demonstrate

robustness.2130 The Journal of Finance

Table VII

FM Regressions of Dispersion in Analysts’ Forecasts

on Lagged Firm Characteristics

Fama and Macbeth ~1973! cross-sectional regressions are run every fiscal year from 1983 to

2000. Dispersion in analysts’ forecasts ~measured seven months before the end of the fiscal

year! is regressed on b ~estimated using the past 36 to 60 months of data!, M ~the lagged fiscal

year-end market capitalization!, B0M ~the lagged fiscal year-end book-to-market ratio!, R 212:22

~the return from t 2 12 months to t 2 2 months!, RCov ~the residual from yearly regressions of

ln~1 1 analyst coverage! on ln~M ! and ln~B0M !!, s~R! ~the standard deviation of daily returns

over the past 250 days, lagged one month!, Vol ~the average adjusted daily volume from the last

250 days, lagged one month!, Turn ~the average adjusted turnover from the last 250 days,

lagged one month!, D0B ~the lagged fiscal year-end debt-to-book ratio!, S0A ~the lagged fiscal

year-end sales-to-assets ratio!, s~eps! ~the one-year lagged standard deviation of earnings per

share divided by the absolute value of mean earnings per share over the past five years!, and

Age ~the mean age of the forecasts!. A firm’s adjusted volume is its volume divided by the mean

volume of the firm’s exchange, while a firm’s adjusted turnover is its turnover divided by the

mean turnover of the firm’s exchange. Newey–West t-statistics are in parentheses. Stocks with

a price below five dollars are excluded.

b ln M ln B0M R 212:22 RCov s~R! Vol Turn ln D0B ln S0A s~eps! Age

0.131

~4.49!

20.046

~26.59!

0.075

~3.26!

20.309

~25.22!

0.135

~4.86!

0.141

~4.95!

0.005

~2.99!

0.044

~8.20!

0.039

~3.00!

20.034

~24.25!

0.005

~2.71!

20.023

~21.37!

0.112 20.025 0.058 20.282 0.114

~3.81! ~27.19! ~2.66! ~25.40! ~5.67!

20.030 0.005 0.089 20.221 0.087 0.185

~21.41! ~0.81! ~3.29! ~26.04! ~5.07! ~3.66!

0.080 20.028 0.059 20.295 0.089 0.002 0.039

~2.51! ~26.98! ~2.53! ~25.78! ~4.33! ~1.79! ~3.42!

0.067 20.030 0.032 20.288 0.088 0.002 0.046 0.039 20.031 0.004 20.020

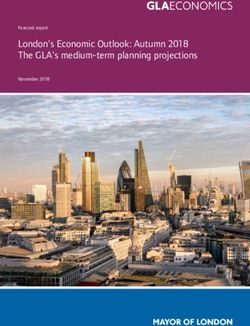

~1.90! ~27.85! ~1.55! ~26.23! ~3.86! ~1.24! ~3.23! ~2.23! ~23.30! ~2.89! ~20.80!Differences of Opinion 2131 Figure 1. Robustness checks: Lags in portfolio formation. At the end of each month, all stocks in the I0B0E0S universe are ranked into deciles based on dispersion in analysts’ earnings per share forecasts ~defined as the ratio of the standard deviation to the absolute value of the mean forecast!. Stocks in each dispersion decile are assigned into equal-weighted portfolios with a certain lag and held in the portfolio for one month. The difference in returns between the lowest- and highest-decile portfolios is calculated. The chart plots the mean monthly return differential, with the broken lines indicating the 95 percent confidence interval ~adjusted for autocorrelation!. A. Lag in Portfolio Formation We try waiting several months before assigning stocks to portfolios. The rationale for this is that even though I0B0E0S updates earnings forecasts frequently, the updates may not become available to the general public until much later. As shown in Figure 1, when the lag gets longer, returns clearly drop, as information becomes stale—prices on stocks in the portfolio may have already fallen due to selling by disappointed optimists. If the lag is longer than five months, the return difference is no longer statistically sig- nificant, even for the lowest market-capitalization quintile. B. Different Holding Periods We also try holding a stock in the portfolio for longer than one month. At the end of each month, stocks are ranked into deciles based on the disper- sion in analyst earnings per share forecasts and assigned into portfolios without a lag. The stocks are then held in the portfolio for T months, with 10T th of each portfolio reinvested monthly. Portfolio returns are equal weighted. Figure 2 shows the results of the strategy for different holding periods. For relatively short holding periods, the results are similar to that of the one-month holding strategy. This is because essentially the same stocks are selected by both strategies every month due to persistence in analyst fore-

2132 The Journal of Finance Figure 2. Robustness checks: Holding periods. At the end of each month, stocks are ranked into deciles based on dispersion in analysts’ earnings per share forecasts and assigned into portfolios without a lag. The stocks are then held in the portfolio for T months, with 10Tth of each portfolio reinvested monthly. Portfolio returns are equal-weighted. The difference in re- turns between the lowest- and highest-decile portfolios is calculated. The chart plots the mean monthly return differential, with the broken lines indicating the 95 percent confidence interval ~adjusted for autocorrelation!. cast dispersions. However, for longer holding periods, returns of this strat- egy are lower because stocks remaining in the portfolio too long may no longer satisfy the portfolio selection criteria. C. Sorting Based on Dispersion in Two-Years-Ahead Earnings Forecasts Here we sort stocks based on the dispersion in the following fiscal year’s earnings forecasts ~not reported here!. There are fewer observations of the two-years-ahead earnings forecasts in I0B0E0S, and, therefore, slightly fewer stocks in each portfolio. Still, because the current and the next fiscal year’s earnings-per-share forecasts are highly correlated, the forecast dispersions are also highly correlated, and the results are similar, although the return differential is somewhat lower. D. Subperiod Analysis We calculate mean monthly returns for the portfolio for the subperiods 1983 to 1991 and 1992 to 2000. As reported in Table VIII, the return differ- ential is significant for all size quintiles for the period of 1983 to 1991. For the 1992 to 2000 time period, it is significant only for the smallest size quintile. As can be seen from the second part of the table, average disper- sions of stocks in portfolios have also decreased in the later time period. This indicates that the overall magnitude of the disagreement has declined, possibly because investors have become better at valuing stocks. At the same

Differences of Opinion 2133

Table VIII

Subperiod Analysis

Each month stocks are sorted in five groups based on the level of market capitalization as of

the third Thursday of the previous month. Each size group is then sorted into five subgroups

based on dispersion in analyst forecasts. Dispersion is defined as the ratio of the standard

deviation of analysts’ current-fiscal-year annual earnings per share forecasts to the absolute

value of the mean forecast, as reported in the I0B0E0S Summary History file. Stocks with a

mean forecast of zero are assigned to the highest dispersion groups, and stocks with a price less

than five dollars are excluded from the sample. Stocks are held for one month, and portfolio

returns are equal-weighted. The table reports the average monthly return differential between

stocks in the lowest- and highest-dispersion quintile in each size group over the indicated time

periods; t-statistics in parentheses are adjusted for autocorrelation.

Mean Returns

Small Large

All

Time Period S1 S2 S3 S4 S5 Stocks

1983–2000 1.37 a 0.89 a 0.67 b 0.48 0.29 0.79 a

~5.98! ~3.12! ~2.41! ~1.55! ~0.93! ~2.88!

1983–1991 1.54 a 1.41 a 0.94 a 0.86 b 0.66 1.16 a

~6.11! ~5.28! ~3.56! ~2.62! ~1.95! ~4.63!

1992–2000 1.21 a 0.37 0.40 0.11 20.08 0.41

~3.14! ~0.77! ~0.83! ~0.21! ~20.16! ~0.86!

Mean Dispersion

Size Quintiles

Dispersion All

Quintiles S1 S2 S3 S4 S5 Stocks

Time period: 1983–1991

D1 ~low! 0.013 0.014 0.016 0.018 0.017 0.015

D5 ~high! 1.434 1.148 0.986 0.938 0.487 1.008

Time period: 1992–2000

D1 ~low! 0.008 0.008 0.009 0.010 0.010 0.009

D5 ~high! 1.081 0.780 0.642 0.509 0.437 0.698

a,b

Statistically significant at the one and five percent levels, respectively.

time, trading costs have come down, and firm-related information has be-

come more readily available. All these factors may have contributed to the

decline in the return differential over time.

E. Evaluation of Other Explanations

Hong et al. ~2000! suggest that negative momentum in stock returns—the

empirical finding that past losers continue to earn below normal returns in

the future—is caused by the slow price adjustment to negative information.

They empirically document that negative momentum is more pronounced forYou can also read