Determinants of Company Going Concern: Empirical Evidence in the Times of Covid-19 in Developing Capital Markets - Zenodo

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

Determinants of Company Going Concern: Empirical Evidence in the Times

of Covid-19 in Developing Capital Markets

Beryansyah1, MF. Arrozi2

1,2

Esa Unggul University

ABSTRACT: During the COVID-19 pandemic, various corporate sectors in Indonesia were affected by the pandemic, including

manufacturing companies. Where during the pandemic many companies are threatened with their business continuity. This

observation plan is to understand the influence of managerial ownership, financial distress and leverage on going concern companies

with profitability as a moderating variable. In this study going concern was measured by determining the Scott R formula. The

research methodology for testing and data analysis was using MRA (Moderating Regression Analysis). The population in this

observation is the manufacturing industry listed on the Indonesia Stock Exchange (IDX) in 2020. The sample collection was carried

out using the purposive sampling method with a total sample of 179 companies in 2020. The results of this observation prove that

financial distress has a negative effect on going concern and leverage. Positive impact on going concern. Meanwhile, managerial

ownership has no impact on going concern. Authorized profitability with return on assets is able to strengthen the influence of

financial distress and leverage on going concern. Observational findings in this observation normative accounting theory elevate

plans, skills and then determine how to meet the recognized goals. Normative accounting theory includes decisions about what to

do to fulfill the desires that have been mentioned. The implication of this research is that the implementation of Pecking order theory

explains that industries that get high profits will use relatively small liabilities because the industry will tend to set money in it. The

normative theory here tries to explain the explanations that are usually conveyed to the users of the accounting explanations that

will be presented.

KEYWORDS: Financial Distress, Leverage and Profitability, Managerial Ownership.

INTRODUCTION

The company is a one-way entity where the primary goal is to make a profit (profit oriented). Profit or profit here is a

measure of the effectiveness and efficiency of the company, so profit income is not guaranteed to have a long-term reputation.

Companies can operate for a long time so they can make projects, commitments or activities sustainable. This is based on the

principles of business continuity (going concern) which accommodates a company that can be expected to cancel in the future or

that the company will continue to be determined by time.

In 2020 many corporate sectors were affected due to the Covid Pandemic, in Indonesia the corona virus or pandemic could

be applied by the national government such as the destruction on Saturday 14 March 2020 to go through the century of disaster

emergency in Indonesia. Some companies also put their workers to work from home. All of these actions are intended to make the

Indonesian economy as well as the global economy significantly slow down (Report on Indonesian and World Economic

Development Bappenas, 2020).

Several sectors of Indonesian companies are experiencing the effects of the Covid Pandemic and the economy is slowing

down due to the COVID-19 (adhikara et al., 2022). Covid-19 also has a significant impact on the 2020 financial statements,

especially in the aspect of company income which has decreased due to the purchasing power of citizens and will have an impact

on inflation, and inventory measurement (Mala et al., 2021). The Central Statistics Agency (BPS) transmitted the results of the

impact of the Covid-19 pandemic and carried them out to 34,559 economic actors. The decline in income, due to Covid-19 has an

impact on business productivity.

In the midst of increasingly tight liquidity, the Company must consider Covid-19 in the reserves of a business in interim

financial reporting in the first half of 2020. Companies need to consider the Covid-19 situation in the company's risk management

in maintaining the company's profits to decline in 2020 due to Covid-19 19. Of course, when assessing this situation there is a

financial reporting perspective related to the third paragraph of PSAK 8. The spread of Covid-19 in Indonesia is the result of events

492 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

that occurred after the 2019 reporting period and no event could affect the presentation of the 2019 financial statements. However,

if Covid-19 19 that significantly threatens business continuity going forward due to the significant impact caused by Covid-19,

permanent companies will consider the company's valuation (going concern) when compiling the 2019 annual financial statements

(PSAK 8 paragraph 14).

The results of previous research on going concern have been carried out by Fernando (2018). It can be developed with

additional dependent variables, namely managerial ownership, and leverage, and does not include unearned revenue, working capital

turnover, cash flow of capital, and additional liabilities as independent variables. Including profitability as a moderating variable.

The difference in measuring going concern using the Scott Model, where previous research used the Zmijewski Model.

This study aims to find out, firstly, by choosing Good Corporate Governance (Managerial Ownership) as the dependent

variable, the researcher wants to find out whether there is a match between managerial theory and the events of this pandemic. Then

Financial Distress to measure whether the impact of this covid pandemic makes the company experience an indication of bankruptcy,

then Leverage is used to measure the amount of debt affecting the company's sustainability risk during the pandemic, then earnings

power as a moderating variable to calculate Return On Assets to see how effective the company's assets are in generating profit

during a pandemic.

The contribution of this research is to improve the company's performance by always paying attention to the policies and

strategies adopted in determining the sustainability of the company's business. By paying attention to the debt owned by the

company, it reduces the risk of the company experiencing a bad financial condition which causes the company to fail to pay its debts

and cannot continue its business. The application of pecking order theory explains that companies that generate high profits, consume

relatively little debt, tend to use the company's internal funds for operational costs.

THEORY AND HYPOTHESES DEVELOPMENT

Normative Accounting Theory

Normative theory tries to explain the information that must be conveyed to users of accounting information and how that information

will be presented (Kabir, 2011). Normative theory is generated through a semi-exploratory process without testing the accounting

theory presented, which may or may not explain general accounting practice. On the other hand, empirical theory focuses on the

importance of empirical studies to verify whether the accounting theory presented in the accounting theory literature can explain the

dominant accounting practice (Budiarto, 1999). Accounting theory is an important part of practice. Normative accounting theory is

also claimed to be a prescriptive theory, which tries to answer the question of what should be. Here, accounting is believed to be a

regulatory practice that must be followed regardless of whether it is applied or practiced now or not. Normative theory seeks to be

able to justify what should be actualized, for example, there is a statement that explains the financial statements based on the asset

measurement method. Normative theory only interprets hypotheses that are put into practice without any hypothesis testing.

Bankruptcy Theory

Bankruptcy theory assumes that economic distress is a company's failure to lose income that is unable to cover expenses, namely

the company's profit margin in capital costs is not in line with the expected cash flow. Financial distress means it is difficult to

collect funds, both in the form of cash and working capital. As asset and liability management, it plays a very important role in

avoiding financial difficulties. Companies in countries experiencing financial difficulties will soon go bankrupt because financial

difficulties have become ill and then lead to rapid bankruptcy of those who are sick and bankrupt.

The Relationship of Managerial Ownership, Financial Distress and Leverage to Going Concern

Going Concern or business continuity is the root of the principle that presents the company's financial statements. The definition of

going concern is the ability of a company or entity to survive or operate in the long term where the sustainability of the company's

operations can be affected by financial or non-financial conditions such as poor management, decreased ability of the company to

pay debts, government policies, pandemics, inflation, etc.

Relationship of Managerial Ownership to Going Concern

Management ownership is a condition where a manager holds several shares issued in a company. In terms of stock management,

the position of managers and shareholders will be the same to increase company efficiency and maximize company value. In

addition, in ownership, the manager directly benefits from the decisions he makes because he becomes the owner of the company

493 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

directly by owning a number of shares in the company. According to (Januarti, 2009) it is concluded that managerial does not have

a significant influence on going concern audit acceptance. Meanwhile, the study (Linoputri, 2010) concluded that going concern

audit opinion had a negative effect on managerial ownership.

Relationship of Financial Distress to Going Concern

The soundness of a company is in a good financial position, the auditor does not issue a going concern opinion. According to

(Andari, Ni Made Meliani, 2017) management expects the company to face bankruptcy in the future, and its survival is also a

consideration. The financial situation of a company, that is, the company's financial position for a period of time, generates negative

net income for several years and eventually goes bankrupt, and the company's operating cash flow is no longer sufficient to take

corrective action to avoid bankruptcy.

Leverage Relationship to Going Concern

Companies with low levels of funding leverage tend to go bankrupt and remain vulnerable to corporate audit opinions. The

company's high leverage ratio is an indication of adverse conditions because most of the funds used come from debt. The fast

leverage ratio raises doubts on the auditor's side of the business continuity of a company to provide the auditor's opinion on the

business continuity. A high leverage ratio also makes it harder for businesses to get loans because lenders tend to display loans to

companies with declining leverage ratios.

The Relationship of Profitability to the Effect of Managerial Ownership with Going Concernn

Managerial ownership is share ownership by the management of the company. (Christiawan et al., 2007) argues that managerial

ownership is a condition where managers own shares in the company, meaning that managers are also shareholders in the company.

Managerial ownership also affects the profitability of the company, as we believe it can affect the company's operations and

ultimately its effectiveness in achieving its objectives. The relationship between financial performance and profitability will be

strengthened by the involvement of management. Because more executives will have an impact on the company, namely managers

tend to be more active in the interests of shareholders. This study is in accordance with research conducted by (Jensen & Meckling,

2019), showing that management ownership aligns the interests of management with those of shareholders, so that managers feel

the benefits of making decisions and the disadvantages of bad decisions.

Profitability Relationship to the Effect of Financial Distress with Going Concern

According to (Andre & Taqwa, 2014) financial distress can be explained by two extremes: shortterm liquidity problems that cannot

be resolved. Short-term financial difficulties are usually shortlived, but they can develop into serious problems. Where indicators of

financial distress can be collected from an analysis of cash flow, analysis of the company's strategy, and reports from the company's

finances.

Research (Hapsari, 2014) shows that profitability has a negative influence on financial distress. Efficient wealth management makes

it possible to cover all the costs of running a business and has a significant profit yield. A study from (Srikalimah, 2017), states

against similar results that profitability has a negative impact on financial difficulties.

The Relationship of Profitability to the Effect of Leverage with Going Concern

The leverage ratio is a measure of the long-term ability that is used to assess the company from fulfilling obligations (Andre &

Taqwa, 2014). A high leverage ratio can lead to high financial risk when risks arise.

Profitability is the company's ability to make profits, namely high profits, the faster the tax liability and high leverage, the lower the

company's profitability. The existence of a significant influence displays the existing leverage from the main factors that influence

the profitability of the company.

Hypothesis Development

Based on the literature review and the results of previous studies, the hypotheses are formulated as follows:

H1: Managerial ownership, financial distress, and leverage affect going concern with profitability as a moderating variable.

H2: Managerial Ownership has a positive effect on Going Concern

H3: Financial Distress has a negative effect on Going Concern

H4: Leverage has a negative effect on Going Concern

H5: Profitability strengthens the positive effect of Managerial Ownership on Going Concern

494 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

H6: Profitability weakens the negative effect of Financial Distress on Going Concern H7: Profitability strengthens

the positive influence of Leverage on Going Concern

RESEARCH METHODS

Research design

The research design uses causality hypothesis testing, namely to test the effect between two variables. The approach used

is the quantitative method, namely the use of numbers as variable indicators. According to (Efferin, 2018) the quantitative approach

is an approach that uses procedures, hypotheses, field trips, data analysis and data conclusions to measure aspects, computations,

methods and certainty of numerical data.

Variable Operational Definition

Going Concern in this study is the dependent variable, according to (Indonesian Institute of Certified Public Accountants,

2011) interpreting going concern as the ability of a business to maintain business continuity in the right period of time. More than 1

year. The year from the date of the audited financial statements. In this study, the method used in predicting going concern uses the

Scott model (Scott, 1981) that interest payments are generated from earnings before interest and corporate taxes and changes in

equity in this case are dividend payments.

Managerial ownership is a condition where managers take part in the company's capital structure or use other terms, the

manager has a dual role as manager and shareholder in the company. In accounting theory, the motivation of managers will choose

the amount of profit management in the company. Motivation that is not in sync will form the amount of profit management that is

out of sync

According to Andari, et al., (2017), financial distress (financial distress) begins when the company is unable to meet

payments and the company cannot complete its obligations based on cash flow projections.

According to Petrus et al., (2018) Leverage ratio is the company's ability to meet short-term and long-term financial

obligations and or the company's good size in paying off debt.

ROA is a method of calculating the financial performance of a company by comparing the net profit generated by the

company with the company's total assets. ROA reflects how much a company earns from the financial resources it invests. The

reason the author uses ROA to assess the financial performance of a company is that the ROA ratio is very important in financial

analysis which is a comprehensive method. ROA ratio analysis is a method of analysis that is commonly used to assess the level of

effectiveness of the company's operations as a whole. According to (Priyanto, 2013). Understanding ROA is a type of profitability

that is able to assess the company's ability in terms of obtaining profits based on the assets used.

RESULTS AND DISCUSSION

Research result

Descriptive Statistics

The statistical descriptive results show the tendency of individual taxpayers as shown in table 4.2

Table 4.2 Descriptive Statistics

495 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

The table above shows the composition of the shareholding owned by Managerial at 6.2%. The higher the managerial

ownership value, the higher the influence of management interests. With a mean value of 6.41 on financial distress, it shows that

the company does not experience bankruptcy potential. The company's high leverage ratio indicates a loss, because most of the

money the company develops comes from debt. Profitability shows that the average value of the sample study has an ROA of 27.2%,

which means that the company gets the main performance from its operational activities. Based on the statistical results, descriptive

going concern has a mean value of 45 billion and is positive. This explains that the company's playing value as the research sample

has a positive EBIT so that it is a going concern.

Normality test

The use of the normality test is used to process data from research results using the Kolmogorov-Smirnov test method, as

explained in the previous chapter that the normality test can be used to see the residual model in research with a normally distributed

Table 4.3. Normality

One-Sample Kolmogorov-Smirnov Test

Unstandardized Residual

N 68

Mean 0E-7

Normal Parametersa,b

Std. Deviation 2.04051907

Absolute .083

Most Extreme Differences Positive .083

Negative -.083

Kolmogorov-Smirnov Z .688

Asymp. Sig. (2-tailed) .731

a. Test distribution is Normal.

b. Calculated from data.

The Kolmogorov-Smirnov test above shows residual data which has a normal distribution. The results of this normality test explain

that the Kolmogorov-Smirnov value is significant at 0.731 > 0.05, which is in accordance with the assumption of normality.

Data Multicollinearity Test

The multicollinearity test is to see the results of the tests contained in the regression model found, namely the independent

variables of the regression model by analyzing at the VIF level (Variant Inflation Factors). Then the VIF value ofInternational Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

Table 4.4 explains that the model used gives all independent variables to the value of VIF 0.05 then

there will be no auto-correlation and if the probability value isInternational Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

Hypothesis Testing before Moderation

Hypothesis testing is done either simultaneously or partially. The calculation results are in table 4.6 below.

Table 4.6. Coefficient of Determination Test Table (R2)

Model Summaryb

Model R R Square Durbin-Watson

Adjusted R Std. Error of the

Square Estimate

1 .485a .235 .160 2.02915 1.434

a. Predictors: (Constant), LVPF, KM, FD, KMPF, FDPF, LV

b. Dependent Variable: LNGC

Based on regression testing, the Adjusted R2 value is 0.160, indicating that managerial ownership, financial distress, leverage, and

profitability have an influence on going concern by 16% and the remaining 84% is influenced by other variables contained in this

study.

Table 4.7. Uji F Table (Simultan)

ANOVAa

Model Sum of Squares df Mean Square F Sig.

77.326 6 12.888 3.130 .010b

Regression

251.165 61 4.117

Residual

1 Total 328.490 67

a. Dependent Variable: LNGC

b. Predictors: (Constant), LVPF, KM, FD, KMPF, FDPF, LV

Based on the regression test in table 4.6, the F-count is 3,130 with a significance (0.010 < 0.05). The results of the Simultaneous

Effect Test of F show that the p-value is lower than the significance value (0.05) so that the conclusion from Ha1 is accepted, namely

that there is managerial ownership, financial distress, leverage, and profitability on going concern simultaneously.

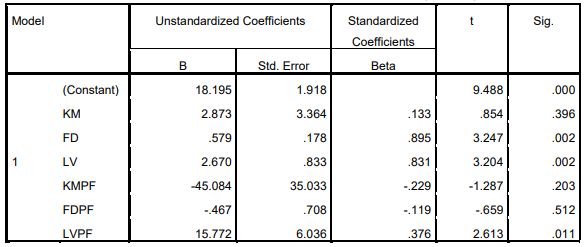

Table 4.8. T Test Results (Partial)

a. Dependent Variable: GC

498 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

Based on the results contained in table 4.7 above, it can be made an equation of multiple regression, namely:

GC = 18,195 + 2,873 KM + 0,579 FD + 2,670 LV - 45,084 KM*PF - -0,467 FD*PF

- 15,772 LV*PF + 2.02915

DISCUSSION

Effect of Managerial Ownership, Financial Distress, Leverage and Profitability on Going Concern

Based on the test of the F-count regression model of 2.796 significance (0.000International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

The Effect of Profitability weakens the positive influence of Managerial Ownership on Going Concern

In accounting theory, the motivation of managers determines the amount of profit earned by the company. Different motives

bring different benefits. Stock managers in a company are involved in setting policies and making decisions about accounting

practices that apply to the companies they manage. While going concern or the survival of the company is always associated with

the ability of management to hold the company. If the economic situation of a company is uncertain, then a pandemic situation like

this requires management to be able to make decisions so that the company can continue to run its business.

Profitability can moderate the influence of managerial ownership on business continuity. Where this is caused by the

existence of stock management in the company who cannot make decisions where it will affect performance in achieving the goal

of making a profit. Managerial ownership equalizes the interests of management with shareholders, so that managers can feel directly

from the benefits that result from decisions. This study is in accordance with research conducted by (Jensen & Meckling, 2019),

showing that management ownership aligns the interests of management with those of shareholders, so that managers feel the

benefits of making decisions and the disadvantages of bad decisions.

The Effect of profitability weakens the negative influence of Financial Distress on Going Concern

Financial distress is a company's financial statements in a condition where the situation is not good. Therefore, usually the

profits obtained by the company can no longer be used in submitting loans, funding operations and completing responsibilities with

existing profits.

Profitability can moderate the effect of financial distress on the company's business continuity. This is due to an indication

of bankruptcy by a company, one of which is a factor that is influenced by the high and low profits of a company, the company's

profit, the indication of bankruptcy experienced by the company is considered low, making the company continue to be able to

continue its business. The results of research from (Srikalimah, 2017), state against similar results that profitability has a negative

impact on financial difficulties. If the company gets a high profit, then the profit can be used by the company, so that financial

difficulties will not occur.

The Effect of Profitability strengthens the positive influence of Leverage on Going Concern

Pecking order theory explains that companies that generate high profits will use relatively little debt because companies

will tend to use their internal funds. Profitability is the ability possessed by the company to make a profit. If the profit earned is

large, the amount of tax liability paid is also higher, if the leverage is higher, the profitability of the business will weaken. A

significant influence explains the leverage of a primary factor and affects business profitability.

Profitability can moderate the effect of leverage on the company's business continuity. This is caused by companies that

are able to form high profits that will affect the high level of business success in fulfilling financial responsibilities both in the short

and long term, the output of this study shows how businesses are able to manage debt to earn profits and also to pay off their debts.

According to research (Kusumaningrum, 2019) companies with a high rate of return on an investment tend to use a fairly low level

of debt. Where the rate of return allows the company to fund most of the funding needs obtained internally.

RESEARCH FINDINGS

This research has some interesting findings, so that the company has a lot of debt, so the company is also at high risk of not being

able to continue its business. This is in accordance with the pecking order theory, which explains that a business can generate high

profits, will carry out relatively little debt so that businesses that have low debt will tend to be able to continue their business. So in

this study it proves that normative accounting theory takes goals, attitudes and determines methods in achieving existing goals.

Normative accounting theory provides resolutions regarding what must be done to achieve goals. Normative accounting theory in

going concern as a qualitative characteristic of financial statements which states that the company's ability to survive or be able to

operate in the long term where the company's business continuity is influenced by financial conditions, one of which is the decline

in the company's ability to pay debts.

Furthermore, the results of the study found that Adjusted R2 from before moderation had a value of 0.097 and increased to

0.160 when moderation occurred. So, comprehensively the profitability moderating variable will strengthen the company to be a

going concern.

500 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

CONCLUSION

Management ownership, financial difficulties and leverage simultaneously affect business continuity. Ownership does not have a

positive effect in determining the sustainability of the company's management. Financial difficulties have a negative impact on the

sustainability of the company's business. A business's poor financial position during a pandemic can indicate that a business cannot

continue as a going concern. Leverage has a positive impact in determining the sustainability of a company's business. Profitability

weakens the impact of management ownership on the company's business continuity. Profitability reduces the negative impact of

financial difficulties on the company's business continuity. Profitability increases the positive effect of leverage on the company's

business continuity.

RECOMMENDATION

Recommendations for this research: it is recommended and expected to use study objects that focus on other industries and increase

the study time span more than the current research period, namely 5 years (period 2016 – 2021), add independent variables that

affect going concern, for example audit quality and change moderation apart from profitability, so that it can provide a broader

explanation regarding indications of going concern in a company, using a proxy approach to corporate governance measurement

methods such as using data from IICG and IICD in the form of scoring or the ASEAN Corporate Governance Scored (ACGS) in

order to be able to assess the implementation of GCG comprehensively. Comprehensive and accurate, as well as using corporate

governance measurements with proxies such as audit quality and managerial ownership.

Then it is recommended to test the going concern variable using other proxies such as the Altman Z-Score, and to test the

financial distress variable using the latest Altman Z-Score formula, in 2014.

REFERENCES

1. Adhikara, Arrozi, MF, Maslichah, Nur Diana, M. Basjir, 2022, Organizational Performance in Environmental Uncertainty

on the Indonesian Healthcare Industry: A Path Analysis, Academic Journal of Interdisciplinary Studies, Vol 11, No 2,

ISSN : 2281-4612

2. Alamsyah, M. F. (2019). The effect of profitability, company size and market value on share prices in the metal and mineral

mining sub-sector on the Indonesian stock exchange. 11(2), 170–178.

3. Aminah. (2015). INFLUENCE OF PROFIT MANAGEMENT ON FINANCIAL PERFORMANCE IN MANUFACTURING

COMPANIES IN 2011-2012. 6(1).

4. Aminy, M. M. (2019). Journal of Enterprise and Development. 1(1), 1–6.

5. Andari, Ni Made Meliani, I. G. B. W. (2017). FINANCIAL DISTRESS IN BANKING COMPANIES Ni Made Meliani

Andari 1 Faculty of Economics and Business Udayana University, Bali, Indonesia The progress of a country is closely

related to the country's economic system. The good or bad of a country's economy. 6(1), 116–145.

6. Andre, O., & Taqwa, S. (2014). The Effect of Profitability, Liquidity, and Leverage in Predicting Financial Distress

(Empirical Study of Various Industrial Companies Listed on the Stock Exchange in 2006-2010). Journal of the Forum for

Accounting Research, 2(1), 293–312. http://ejournal.unp.ac.id/index.php/wra/article/view/6146

7. Annisa Livia Ramadhani, Khairunnisa., S. M. . (2019). THE EFFECT OF OPERATING CAPACITY, SALES GROWTH

AND OPERATION CASH FLOWS ON FINANCIAL DISTRESS (Empirical Study on Agricultural Sector Companies Listed

on the Indonesia Stock Exchange 2013-2017). 5, 75–82.

8. Aprilasuci, M., & Palenteng, D. (2017). Bankruptcy Analysis Using the Altman Z-Score Method ( Case Study in Charoen

Pokphand Indonesia Tbk , Pt . Japfa Comfeed Indonesia Tbk , and Pt . Sierad Produce Tbk Period 2013-2017 ). 03(02),

17–25.

9. Arga Fajar Santosa, L. K. W. (2007). Analysis of Factors Affecting the Tendency of Accepting Going Concern Audit

Opinions.

10. Arma, E. (2017). The effect of profitability, liquidity, and company growth on the acceptance of audit opinion. Padang

State University, Profitability, Liquidity, and Corporate Growth, 1–30.

11. Astuti, P., & Pamudji, S. (2015). Analysis of the Effect of Going Concern Opinion, Liquidity, Solvency, Cash Flow,

Company Age And Company Size Against. 4, 1–11.

501 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

12. Ballesta, J. P. S., & García-Meca, E. (2005). Audit qualifications and corporate governance in Spanish listed firms.

Managerial Auditing Journal, 20(7), 725–738. https://doi.org/10.1108/02686900510611258

13. Baridwan, Z. (2000). Development of Accounting Theory and Research. Indonesian Journal of Economics and Business,

15(4), 486–497. https://core.ac.uk/download/pdf/297708794.pdf.

14. Baxter, W. T. (2014). Accounting theory. Accounting Theory, 3, 1–357. https://doi.org/10.4324/9781315885490

15. Budiarto, A. (1999). Relation of Accounting Research to Teaching and Practice of Positive Theory Approach. Indonesian

Journal of Accounting and Auditing, 3(1), 29–48.

16. Carcello, J., & Neal, T. (2000). Audit Committee Composition and Auditor Reporting. The Accounting Review, 75.

https://doi.org/10.2139/ssrn.229835

17. Carolina, V., Marpaung, E. I., & Primary, D. (2018). Financial Ratio Analysis to Predict Financial Distress Conditions

(Empirical Study on Manufacturing Companies Listed on the Indonesia Stock Exchange 2014-2015 Period). Maranatha

Journal of Accounting, 9(2), 137–145. https://doi.org/10.28932/jam.v9i2.481

18. Christiawan, Jogi, Y., Tarigan, & Joshua. (2007). Managerial Ownership: Department of Accounting Economics, Faculty

of Economics - Petra Christian University, 9, 1–8.

19. Dewi, R. J. T., Khairunnisa, & Mahardika, D. P. . (2017). Analysis of the Effect of Liquidity, Leverage, and Operating

Capacity on the Financial Distress of Mining Companies (Study on Mining Sector Companies Listed on the Indonesia

Stock Exchange 2013-2015 Period). E-Proceeding of Management, 4(3), 2648-2653 ISSN : 2355-9357.

20. Diwanti, N. S., & Purwanto. (2020). The Influence Of Financial Ratios And Good Corporate Governance Towards

Financial Distress On Islamic Banks In Indonesia. Journal of Management Studies, 5(1), 1–17.

21. Efferin. (2018). Accounting Research Methods. Journal of Chemical Information and Modeling, 53(9), 1689–1699.

22. Febriyan, Ari Hadi Prasetyo, F. (2019). INFLUENCE OF OPERATIONAL CASH FLOW, LIQUIDITY, LEVERAGE,

DIVERSIFICATION, AND COMPANY SIZE ON FINANCIAL DISTRESS

23. (Empirical study on multi-industrial sector companies listed on the IDX 2014-2016). Journal of Accounting, 8(1).

https://doi.org/10.46806/ja.v8i1.579

24. Fernando. (2018). THE EFFECT OF GOING CONCERN ON THE PROPERTY COMPANY LISTED IN INDONESIA

STOCK EXCHANGE Fernando ( kweefernando@gmail.com ) Master of Accounting at Esa Unggul University Jak.

25. Ghozali. (2011). Multivariate Analysis Application With SPSS Program.

26. Ghozali. (2016). Quantitative and qualitative research design for accounting, business, and other social sciences.

27. Hanifah, O. E., & Purwanto, A. (2013). THE EFFECT OF CORPORATE GOVERNANCE STRUCTURE AND

FINANCIAL INDICATORS ON FINANCIAL DISTRESS CONDITIONS (Study on Manufacturing Companies Listed

on the Stock Exchange. Diponegoro Journal of Accounting, 2, 1–15.

28. Hapsari, E. I. (2014). Journal of Management Dynamics. Jdm, 5(2), 171–182.

29. Haryanto, Y. A. (2019). The Effect of Profitability, Solvency, Liquidity, and Market Ratios on Going Concern Audit

Opinions on Manufacturing Companies on the Indonesia Stock Exchange. Diponegoro Journal of Accounting, 8(4), 1–13.

30. Herawaty, V. (2008). The Role of Corporate Governance Practices as Moderating Variables of the Effect of Earnings

Management on Company Value. The Role of Corporate Governance Practices as Moderating Variables From the Effect

of Earnings Management on Firm Value, 10(2), 97–108. https://doi.org/10.9744/jak.10.2.PP.97-108

31. HT ALI, H. (2018). Predicting the Financial Distress Condition of Go-Public Companies Using Multinomial Logit

Analysis. Cereals For, 51(1), 51.

32. Ige, O. M., & Onadeko, B. O. (2001). An open study to evaluate the safety and efficacy of zafirlukast (“Accolate”) in

patients with mild to moderate asthma in Ibadan, Nigeria. West African Journal of Medicine, 20(4), 220–226.

33. Indonesian Institute of Certified Public Accountants. (2011). PSA No. 30 SA Section 341. Professional Standards for

Certified Public Accountants, 30, 2.

34. Irwanto, F., & Tanusdjaja, H. (2020). The Effect of Profitability, Liquidity, and Solvency on Audit Opinions Regarding

Going Concern (Study on Manufacturing Companies Listed on the IDX for the 2015-2017 Period). Journal of

Multiparadigm Accounting Tarumanagara, 2(1), 298–307.

35. Ittonen, K. (2012). Information Asymmetries and Investor Reactions to Going Concern Audit Reports.

502 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

36. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1698595.

37. Januarti, I. (2008). ANALYSIS OF FINANCIAL RATIO AND NON-FINANCIAL RATIO AFFECTING AUDITORS

IN GIVING AUDIT OPINIONS GOING CONCERN ON AUDITEE

38. (Empirical study on Manufacturing Companies listed on the JSE in 2000 - 2005). In Maksi (Vol. 8).

39. Januarti, I. (2009). Analysis of the Influence of Company Factors, Auditor Quality, Company Ownership on the Acceptance

of Going Concern Audit Opinions (Manufacturing Companies Listed on the Indonesia Stock Exchange). Journal of

Diponegoro University, 1–26.

40. Jensen, M. C., & Meckling, W. H. (2019). Theory of the firm: Managerial behavior, agency costs and ownership structure.

Corporate Governance: Values, Ethics and Leadership, 77–132. https://doi.org/10.2139/ssrn.94043

41. Julius, F. (2014). INFLUENCE OF FINACIAL LEVERAGE, FIRM GROWTH, PROFIT AND CASH FLOW ON

FINANCIAL DISTRESS. 1164–1178.

42. Kabir, M. H. (2011). Positive Accounting Theory and Science: A Comparison. SSRN Electronic Journal, April 2011.

https://doi.org/10.2139/ssrn.1027382

43. Kholis, N. (2014). Analysis of Ownership Structure and Its Role on Company Earnings Management Practices. Addin,

8(1), 203–222.

44. Kusumaningrum, Y. (2019). ANALYSIS OF THE INFLUENCE OF COMPANY SIZE, LIQUIDITY AND LEVERAGE

ON THE ACCEPTANCE OF AUDIT OPINIONS OF THE GOING CONCERN. 8(2009), 1–12.

45. Liana, D. (2014). Financial Ratio Analysis To Predict Financial Distress Condition of Manufacturing Companies Listed

on the Jakarta Stock Exchange. Indonesian Journal of Accounting & Auditing, 7(2), 1–27.

46. Lie, C., Wardani, R. P., & Pikir, T. W. (2016). Effect of Liquidity, Solvency, Profitability, and Management Plan on Going

Concern Audit Opinion (Empirical Study of Manufacturing Companies on the IDX). 1(2), 84–105.

47. Linoputri, F. P. (2010). The Effect of Corporate Governance on the Acceptance of Going Concern Audit Opinions.

Undergraduate Thesis of Accounting Department, Faculty of Economics, Diponegoro University, Semarang, 1–88.

48. Mada, B. E., & Laksito, H. (2013). The Influence of Corporate Governance Mechanisms, Head's Reputation, Debt Default

and Financial Distress on the Acceptance of Going Concern Audit Opinions. Diponegoro Journal of Accounting, 2(4), 84–

97.

49. Mahaningrum, A. A. I. A., & Merkusiwati, N. K. L. A. (2020). Effect of Financial Ratios on Financial Distress. E-Jurnal

Accounting, 30(8), 1969. https://doi.org/10.24843/eja.2020.v30.i08.p06

50. Mala, Fath, Chajar Matari, Joel Faruk Sofyan, Muhammad Fachrudin Arrozi Adhikara, Sapto Jumono,

51. 2021, THE RELATIONSHIP BETWEEN BANKING INTERMEDIATION AND REAL ECONOMIC GROWTH (A

CASE STUDY OF INDONESIA FOR THE PERIOD 2007–2019), JOURNAL OF SOUTHWEST JIAOTONG

UNIVERSITY, Vol. 56 No. 6, ISSN: 0258-272, pp 551 – 563. Mhd, H. (2014). Ppgb 2005 azhar maksum.

52. Petrus, K. B., Bisnis, F., Kristen, U., Wacana, D., Wahidin, J., & Yogyakarta, S. (n.d.). LEVERAGE

53. AND AUDIT OPINIONS GOING CONCERN. 157–173.

54. Priyanto, S. (2013). THE EFFECT OF LIQUIDITY, SOLVENCY AND PROFITABILITY ON STOCK PRICES OF

COMPANIES IN THE JAKARTA ISLAMIC INDEX IN THE INDONESIA STOCK EXCHANGE (IDX) PERIOD 2009

– 2013. 91–102.

55. Rimawati, I., & Darsono, D. (2017). Effect of Corporate Governance, Managerial Agency Costs and Leverage on Financial

Distress. Diponegoro Journal of Accounting, 6(3), 222–233.

56. Sakai, H., & Asaoka, H. (2003). The Japanese Corporate Governance System and Firm Performance: Toward Sustainable

Growth.

57. Sari, I. R. A. Y. (2016). Faculty of Economics and Business, University of Muhammadiyah Surakarta 2016.

58. Sari, L. A. (n.d.). DEBT TO EQUITY RATIO, DEGREE OF OPERATING LEVERAGE STOCK BETA AND STOCK

RETURNS OF FOOD AND BEVERAGES COMPANIES ON THE INDONESIAN STOCK EXCHANGE. 2(2), 1–12.

59. Sintyawati, Ni Luh Ary, M. R. D. S. (2018). Ni Luh Ary Sintyawati Made Rusmala Dewi S THE INFLUENCE OF

MANAGERIAL OWNERSHIP, INSTITUTIONAL OWNERSHIP AND LEVERAGE ON AGENCY COSTS IN

MANUFACTURING COMPANIES. Unud Management E-Journal, 7(2), 993–1020.

503 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504International Journal of Current Science Research and Review

ISSN: 2581-8341

Volume 05 Issue 02 February 2022

DOI: 10.47191/ijcsrr/V5-i2-22, Impact Factor: 5.825

IJCSRR @ 2022 www.ijcsrr.org

60. Srikalimah. (2017). JOURNAL OF ACCOUNTING & ECONOMICS FE. UN PGRI Kediri Vol. 2 No. 1, March 2017.

Journal of Accounting & Economics FE. UN PGRI Kediri, 2(1), 43–66.

61. Sugiyono. (2014). Educational Research Methods Qualitative Approach. Educational Research Methods Qualitative

Approach.

62. Thio, P. (2004). Consideration of the Company's Going Concern in Giving Audit Opinions. 1(1996), 46– 55.

63. Tjeleni, I. E. (2013). THE INFLUENCE OF MANAGERIAL AND INSTITUTIONAL OWNERSHIP ON DEBT POLICY

IN MANUFACTURING COMPANIES IN THE INDONESIA STOCK EXCHANGE. 1(3), 129–139.

64. Wahyudin, M. (2012). To Know the Guidance of Good Corporate Governance in Indonesia (Indonesian).

65. SSRN Electronic Journal, July. https://doi.org/10.2139/ssrn.1679131

66. Wahyuningtyas. (2010). USING PROFIT AND CASH FLOWS TO PREDICATE FINANCIAL DISTRESS ( CASE

STUDY ON NON-BANK COMPANIES LISTED ON THE INDONESIA STOCK EXCHANGE FOR THE PERIOD OF

2005-2008).

67. Widarjono. (2010). Applied multivariate statistical analysis.

68. Widiarti, A.; A. (2002). dynamics dynamics dynamics. Journal of Economics and Management Dynamics, 11(2).

Cite this Article: Beryansyah, MF. Arrozi (2022). Determinants of Company Going Concern: Empirical Evidence in the Times

of Covid-19 in Developing Capital Markets. International Journal of Current Science Research and Review, 5(2), 492-504

504 *Corresponding Author: MF. Arrozi Volume 05 Issue 02 February 2022

Available at: ijcsrr.org

Page No.-492-504You can also read