Demographic and Development Impact Analysis: Queensland Childcare Centres

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Demographic and Development

Impact Analysis:

Queensland Childcare Centres

Prepared on behalf of:

Australian Childcare Alliance (Qld)

Prepared by:

Kerrianne Meulman

Managing Director

Joshua Binkley

Consultant

Jacques de Wet

Research Assistant

August 2017

Job No. 17041

Urban Economics

Level 10, 87 Wickham Tce

Spring Hill QLD 4000

(ph) 07 3839 1400

mail@urbaneconomics.com.au

www.urbaneconomics.com.au

Warranty

This report has been based upon the most up to date readily available information at this point in time, as

documented in this report. Urban Economics has applied due professional care and diligence in accordance with

generally accepted standards of professional practice in undertaking the analysis contained in this report from

these information sources. Urban Economics shall not be liable for damages arising from any errors or omissions

which may be contained within these information sources.

As this report involves future market projections which can be affected by a number of unforeseen variables, they

represent our best possible estimates at this point in time and no warranty is given that this particular set of

projections will in fact eventuate.

TABLE OF CONTENTS

EXECUTIVE SUMMARY .......................................................................................................... ii

1.0 INTRODUCTION................................................................................................................ 1

1.1 BACKGROUND ........................................................................................................................ 1

1.2 STUDY OBJECTIVES AND METHODOLOGY ..................................................................................... 1

2.0 QUEENSLAND’S NETWORK OF CHILDCARE CENTRES ................................................................. 3

2.1 TRENDS AFFECTING THE CHILDCARE SECTOR ................................................................................. 3

2.2 THE STUDY AREAS ................................................................................................................... 6

3.0 ACA QLD MEMBER SURVEY............................................................................................ 12

3.1 SURVEY RESULTS ................................................................................................................... 12

3.2 REGRESSION ANALYSIS ........................................................................................................... 17

3.2.1 THE REGRESSION MODEL .................................................................................................... 18

4.0 DEMAND DRIVERS ......................................................................................................... 20

4.1 UTILISATION OF CHILDCARE IN QLD .......................................................................................... 20

4.2 POPULATION AND HOUSEHOLD GROWTH .................................................................................. 20

4.3 DEMOGRAPHIC & SOCIO-ECONOMIC CHARACTERISTICS................................................................ 26

5.0 DEVELOPMENT PIPELINE .................................................................................................. 34

6.0 OCCUPANCY RATES AND CENTRE VIABILITY.......................................................................... 37

7.0 RECOMMENDATIONS & CONCLUSIONS ............................................................................... 39

APPENDIX 1 – SURVEY QUESTIONNAIRE ....................................................................................... 41

REFERENCES ........................................................................................................................... 45

i|Pa g e

EXECUTIVE SUMMARY

• This Analysis has been prepared by Urban Economics on behalf of the Australian Child

Care Alliance (Qld) providing an independent analysis of the factors influencing

demand for, and supply of, child care in Queensland.

• This independent analysis particularly considers the impacts of and implications for

affordability and accessibility in delivering a viable network of child care centres for

families considering policy changes, key trends in the supply and delivery of places and

underlying demand parameters.

• An appetite for child care centre investment has emerged with the advent of national

and international operators taking control of independent operators. The larger

operators can be perceived to provide better certainty for investment yields and

leasing terms which in turn makes child care centres attractive propositions for

property investors and developers, one of the factors influencing activity in new

supply additions.

• Political and legislative changes to child care are also influencing the supply of, and

demand for, child care services in Australia. The ‘Jobs for Families Childcare Package’

is the most significant policy change to the childcare system in recent times, seeking

to “make child care more affordable, accessible and flexible.”

• A survey of member centres was undertaken in May 2017 as input to this analysis,

reporting an average occupancy rate for centres across Queensland of 76.3%

compared to 73.9% for the same period in 2016. Occupancy rates were diverse across

regions, even reflecting different occupancy rates within the same regions, indicative

that there were a range of factors at play in influencing centre performance including

catchment size, age of facilities, location, accessibility, operator etc.

• Population growth projections for the 0 to 4 age group in QLD suggest that an

additional 33,000 places or more than 420 child care centres would be required

between 2016 and 2036.

• Some 156 proposed, approved and under construction projects have been identified

across Queensland, with an ultimate capacity of around 16,600 additional places. If all

these proposed places proceed, half the projected demand over a 20 year period could

be provided within this development pipeline. By their very nature, supply additions

are “lumpy” rather than incremental like population growth or demand for child care

places, however, unchecked, this quantum of supply is likely to have implications for

some existing facilities and centres, at least for the short to medium term.

ii | P a g e

• In a typical market scenario, the price of a service such as childcare would respond to

both the level of demand and supply and specifically, price would be expected to

decrease with additional supply. Childcare in Australia however, is subsidised (a

dynamic which will shift with the Jobs for Families Package in 2018) and includes a

high level of fixed costs (predominantly wages). As such, prices are relatively inelastic,

and typically do not decrease with increased supply and competition; dispelling the

theory that increased supply will simply increase affordability for families. In fact, it is

a more tenable proposition that a centre which is substantially underperforming due

to an oversupply situation would cease operation; removing choice and accessibility

for the communities in which they locate.

• An indicator of oversupply of places is therefore considered to be when the occupancy

rates of centres within a local market is below 60% in rural and regional areas of

Queensland; and 70% in SEQ.

In ensuring the efficient and effective delivery of long day care places in Queensland, Urban

Economics therefore recommends:

❖ ACA Qld advocate at the local and state government level for the planning of child

care centres to consider the social, economic, community and planning need for new

facilities and the potential impacts that additional development may have on the

continuity of services in any given locality. Analysis of implications for occupancy rates

should be included.

❖ The application of a planning type threshold for long day care places of 30/100

children aged 0-4 years.

❖ Up to date occupancy data is sought from the Department of Education at the e.g.

Statistical Area Level 3 (SA3) geography, utilising data from the CCMS, and reported

on the MyChild website.

❖ ACA Qld continues its program of Member Surveys post July 2018 to discover any

effects of the Jobs for Families Child Care Package; having particular regard to facilities

in lower socio-economic areas.

iii | P a g e

1.0 INTRODUCTION

1.1 BACKGROUND

Urban Economics has been commissioned by Australian Childcare Alliance Queensland (ACA

Qld) to investigate the childcare sector within Queensland, analysing the perceived existing

oversupply of early education and long day care services in Queensland and the impacts of

this oversupply on reported low occupancy levels within facilities. This independent analysis

explores the risks and opportunities associated within the sector and will be utilised as an

advocacy tool to be presented to the Federal Government, media and financial institutions.

ACA Qld undertakes the role of advocating for its members which provide the opportunities

for families and their children to access early childhood education and care (ECEC). We have

previously undertaken analysis on behalf of ACA Qld in providing a submission to the

Productivity Commission in 2014, regarding the out of pocket cost of child care to families

and rebates and subsidies available for each type of care; utilising surveys undertaken by ACA

of families utilising these services.

Urban Economics is a specialist economic and market research consultancy teamed by

professionals with a passion for understanding how we live, work, play and educate within

our urban environments. We enjoy exploring vertical and horizontal integration and linkage

opportunities and critiquing the commercial realities underpinning these opportunities. Our

consulting experience has spanned the breadth of urban developments from child care to

aged care, and we are experienced in investigating economic development strategies and

opportunities across a broad spectrum of development scales.

1.2 STUDY OBJECTIVES AND METHODOLOGY

In undertaking this analysis, Urban Economics has undertaken a staged approach to the

research for this Study which seeks to:

• ‘Discover what is’ through a comprehensive supply analysis of child care facilities in

Queensland,

• Spatially illustrate the existing and future provision of child care services across QLD,

and the age profile of the communities in which they locate,

• Investigate the pipeline of child care developments across the State; and

• Determine the optimal provision of child care services relative to demographic, age

and working profiles within Queensland.

An overview of the approach is highlighted in the following graphic:

1|Page

Supply

Spatial Development Projections,

Analysis and

Analysis and trends and Planning and

Member

Mapping pipeline Thresholds

Survey

2|Page

2.0 QUEENSLAND’S NETWORK OF CHILDCARE CENTRES

This Chapter sets the scene for the analysis, establishing the Study Area, summarising key

trends in the childcare sector and identifying the network of centres across Queensland.

2.1 TRENDS AFFECTING THE CHILDCARE SECTOR

• FIGURE 2.1 summarises the Department of Education’s Child Care & Early Learning in

Summary data for Queensland between the December Quarter 2012 and September

Quarter 2016, noting the number of long day care services in the State. On average,

there were 27 new facilities per annum added to the supply network over this period.

FIGURE 2.1: Long Day Care Services - Queensland

1,500

1,480

1,460

1,440

1,420

1,400

1,380

1,360

1,340

1,320

1,300

Source: Department of Education

• The Australian Bureau of Statistics (ABS) estimated that as at June 2016, there were

some 2,194 child care service businesses operating within Queensland; of which 879

were employing businesses. TABLE 2.1 outlines child care business counts by their

employment sizes in Queensland between 2008 and 2016. Whilst the number of

services is known to have increased over this period, industry consolidation is

hypothesised to have compressed the number of businesses. Non-employing

businesses primarily include family day care services and sole traders which have

steadily increased.

3|Page

TABLE 2.1: Child Care Service Businesses by Employment Ranges - Queensland

Non 1-19 20-199 200+

Total

Employing Employees Employees Employees

Jun-08 1,147 450 651 12 2,260

Jun-09 1,125 366 433 9 1,933

Jun-10 1,190 340 442 18 1,990

Jun-11 1,218 517 306 9 2,050

Jun-12 1,140 519 321 10 1,990

Jun-13 1,104 498 341 9 1,952

Jun-14 1,187 536 330 8 2,061

Jun-15 1,275 535 327 7 2,147

Jun-16 1,314 565 306 8 2,194

Source: ABS

• Political and legislative changes to child care continue to influence the supply of, and

demand for, child care services in Australia. The ‘Jobs For Families Childcare Package’

is the most significant change to the childcare system in recent times. Initiated by the

Productivity Commission’s Inquiry into Childcare in 2015, the package seeks to “make

child care more affordable, accessible and flexible.”

• The issue of affordability remains debated with reports that the average daily fees for

child care in Brisbane will rise to $157, $175 in Melbourne and $223 per day in Sydney

by 2020, highlighting concerns with the initiatives within the JfF package.

• “End-of-trip” facilities such as showers and bike storage which were once not common

within CBD offices are now considered a standard inclusion by building owners to

attract and retain tenants. It is also now considered that ‘lifestyle” facilities such as

childcare and co-working spaces are being demanded by workers and businesses in

CBD’s or near their place of work.

• Following the collapse of ABC Learning Centres in 2008/09, childcare facilities have

predominantly been operated by not-for-profit groups such as Goodstart and smaller

‘mum and dad’ operators. In more recent times, corporate, and for-profit operators

such as G8 Education and Affinity have emerged, consolidating numerous child care

brands and facilities within their operations. The long-term leases and security

provided by child care centres as real estate investment products have similarly

attracted sophistication in the development of the sector and specialisation from

property funds such as Folkestone Education Trust and Arena REIT.

• Centre occupancy rates are a key metric in determining the viability of an operation.

Whilst there is no ‘one size fits all’ measurement for occupancy rates, 70% occupancy

is often adopted as the target break-even point for a long day care centre. Data

released by larger and sophisticated operators through annual reports suggest that an

occupancy rate over 80% and above is targeted for profitable centres.

4|Page

• A 2016 report by Colliers International estimated that average occupancy rates across

Australia were 70% although, regional areas were noted to have occupancy rates

averaging between 50% and 70%, whilst metropolitan areas were in the order of 80%.

Workforce Trends

• There is significant interplay between increasing casualisation of the workforce and

increases in the rate of female workforce participation rates as illustrated in FIGURE

2.2. This trend however has ‘plateaued’ in recent times, attributable to numerous

factors such as an ageing workforce and increasing unemployment rates generally.

FIGURE 2.2: Employment Profile – Australia

90% 12%

80%

10%

70%

Unemployment Rate

60% 8%

Participation

50%

6%

40%

30% 4%

20%

2%

10%

0% 0%

Oct-1999

Oct-1979

Oct-1984

Oct-1989

Oct-1994

Oct-2004

Oct-2009

Oct-2014

Jun-1981

Jun-1986

Jun-1991

Jun-1996

Jun-2001

Jun-2006

Jun-2011

Jun-2016

Feb-1988

Feb-1978

Feb-1983

Feb-1993

Feb-1998

Feb-2003

Feb-2008

Feb-2013

Full Time Part Time Female Participation

Male Participation Unemployment Rate

Source: ABS

• Whilst employment overall continues to grow, casual and part-time job creation has

outpaced full-time employment; accounting for 56% of all new jobs over the past

decade. Similarly, unemployment rates have been reported within a healthy range of

below 6% over this period, a rate which is being maintained by part-time and casual

workers.

Commercial Property Investment Trends

• An appetite for child care centre investment has emerged with the advent of national

and international operators taking control of independent operators. The larger

operators can provide better certainty for investment yields and leasing terms which

can make child care centres attractive for property investors and developers.

5|Page• Self-managed super funds (SMSF) and ‘mum and dad’ investors/owner operators

attracted to sub-$5million price point of many centres coupled with long leases to

operators are competing with institutional and corporate real estate; driving record

yields for centres (particularly in metropolitan areas) across Australia.

• As at May 2017, construction activity analysts Cordell listed more than 150 mooted,

proposed and under construction childcare centre developments across Queensland.

• The commercial office market (particularly in the Brisbane CBD) has recently had a

peak in vacancy rates, prompting building owners to include additional shared and

flexible spaces as well as tenancy mixes which include childcare, in seeking to attract

commercial tenants to fill vacancies.

• Child care centres are also increasingly integrated within mixed use developments.

Whilst once the focus of education precincts, integration of child care facilities into

mixed use precincts is becoming more common, with movements to also integrate

with other forms of development such as Aveo’s Springfield Retirement Village.

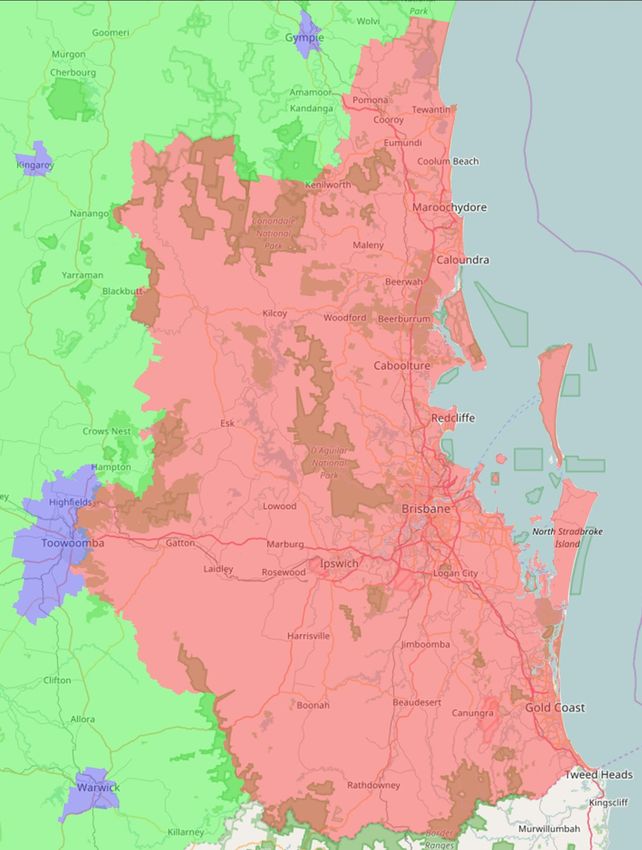

2.2 THE STUDY AREA

The Study Area is defined as the entire State of Queensland which has been geographically

apportioned into three markets utilising Statistical Area Level 2 (SA2) boundaries, including:

• South East Queensland – 317 statistical areas within the bounds of the Noosa,

Sunshine Coast, Somerset, Moreton Bay, Brisbane, Logan, Redland, Lockyer Valley,

Scenic Rim and Gold Coast local government areas (LGA).

• Regional Townships – 136 statistical areas which envelop the main urban areas of

regional towns including Toowoomba, Gympie, Bundaberg, Gladstone, Rockhampton,

Mackay, Townsville and Cairns.

• Rural Balance – 70 statistical areas which define the non-urban, rural and balance

areas of the State.

The segments and regions are illustrated in FIGURES 2.3 and 2.4 and a breakdown of the

distribution of centres, places and population by region is outlined in TABLE 2.2.

Urban Economics has identified approximately 1,500 centres across Queensland which

provide typical long day care and early childhood education services. This excludes other

types of centre-based care such as kindergartens, preschools and outside school hours care

(OSHC). In total, these centres have around 117,000 licensed places or an average of 78-places

per centre.

6|PageTABLE 2.2: Distribution of Child Care Services

Centres 2017 Places 2017 Population 2016

# % # % # %

SEQ 1,036 69.3% 84,448 72.2% 3,297,983 68.1%

Regional 369 24.7% 27,951 23.9% 1,128,160 23.3%

Rural 91 6.1% 4,522 3.9% 417,160 8.6%

QLD 1,496 116,921 4,843,303

Source: Urban Economics, ABS

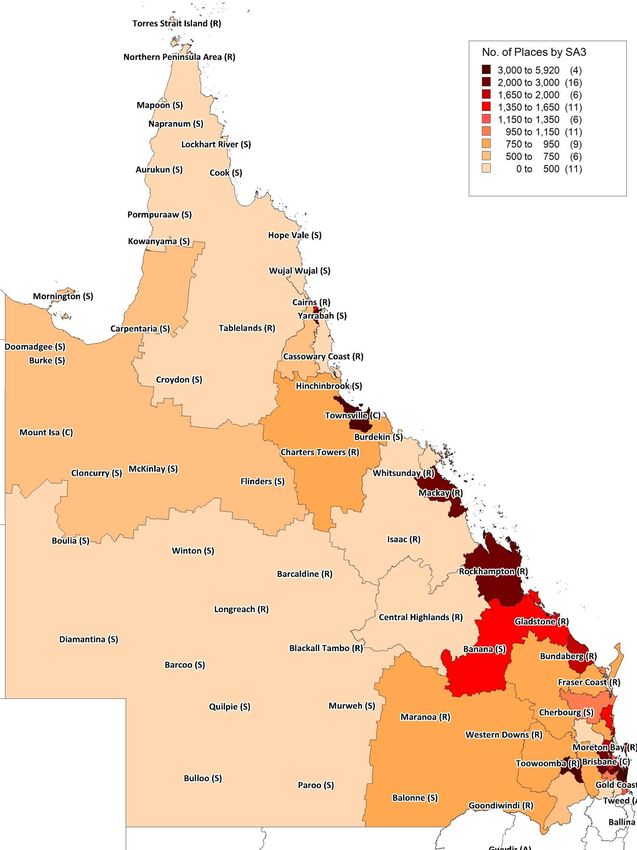

FIGURES 2.5 and 2.6 thematically illustrate the supply of childcare centres by SA3 in SEQ and

the state.

7|PageFIGURE 2.3: The Study Area - Queensland

8|PageFIGURE 2.4: The Study Area – South East Queensland

9|PageFIGURE 2.5: Childcare Places in SEQ by Statistical Area Level 3 -SEQ

10 | P a g eFIGURE 2.6: Childcare Places in QLD by Statistical Area Level 3

11 | P a g e3.0 ACA QLD MEMBER SURVEY

3.1 SURVEY RESULTS

In collaboration with ACA Qld, Urban Economics conducted an online survey of member

centres. The survey opened on 31st May 2017 and closed on Friday the 30th of June, collecting

a total of 218 member responses, which were primarily from centres within South-East

Queensland. Although there were some centres which self-classified as ‘rural’, the results of

these responses have ben redistributed for analysis to the Regional Study Area. In total 173

(81%) member responses were received from centres within SEQ and 45 (19%) were received

from regional centres. The Survey questions are provided in APPENDIX 1.

Responses from centres in SEQ represented more than 14,860 daily places or an average

centre size of 86 places per facility. Regional centres represented 3,515 places or

approximately 78 places per facility.

FIGURE 3.1: Daily Places by Surveyed Study Area Responses

Regional

19%

SEQ

81%

Respondents which indicated the number of licensed places by age group defined an age

structure which included; birth to 2 years (20.3%), 2-3 years (26.8%) and 3 years to school age

(52.9%). This structure is further detailed by study area in FIGURE 3.2.

12 | P a g eFIGURE 3.2: Proportion of Places by Study Area and Age Group

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

SEQ Regional

Birth to 2 yrs 2 to 3 yrs 3 yrs to School Age

TABLE 3.1 lists the number and proportion of centres by the age of the facility. Significantly,

more than 80% of respondent centres were 5 or more years old and almost 65% were at least

10 years old. It is inferred that with the emergence of sophistication surrounding child care

centres as real estate investments, property investors will continually seek to ‘refresh’ their

assets either through redevelopment and expansion of existing centres, or construction of

new centres; contributing to the perception of significant new supply in the pipeline.

TABLE 3.1: Age of Centres

Under

1 to 2 2 to 5 5 to 10

12 10+

yrs yrs yrs

mths

# 3 5 21 26 112

SEQ

% 1.8% 3.0% 12.6% 15.6% 67.1%

# 1 5 2 11 24

Regional

% 2.3% 11.6% 4.7% 25.6% 55.8%

# 4 10 23 37 136

TOTAL

% 1.9% 4.8% 11.0% 17.6% 64.8%

Adopting reported trends for occupancy rates at metropolitan compared to regional and rural

child care centres, it could be hypothesised that the daily rate would show a similar level of

variability or elasticity. The evidence is stronger, however, to suggest that the daily rate is

‘pegged’ to government subsidies creating a ‘floor’ in price, with prices only increasing in

areas of extreme demand and/or where the perception of quality is above the norm. TABLE

3.2 outlines the median and average daily rates for respondent’s facilities within SEQ and the

Regional Study Area, indicating limited variation in price based upon location alone. This

dynamic is further explored in the regression analysis of Section 3.2.

13 | P a g eTABLE 3.2: Median and Average Daily Rates

3 to

Birth to 2 to 3

School

2 yrs yrs

age

Median $91.5 $89.0 $86.0

SEQ

Average $89.5 $89.2 $87.3

Median $90.0 $88.0 $87.0

Regional

Average $87.6 $86.2 $84.8

The Survey queried the enrolments for each facility by day. The results reveal that on average,

respondent child care centres in SEQ had an occupancy rate of 76.7% whilst responding

regional centres were at 74.4% occupancy in May 2017. The average occupancy rate for

respondent centres across Queensland in May 2017 was 76.3% compared to 73.9% for the

same period in 2016.

Occupancy rates for centres were diverse within competitive areas. In some instances, a

centre which was over-subscribed and included a waiting list was within the same postcode

as a centre with an occupancy rate in the order of just 40%, indicating that access to, and

availability of services may be a limiting factor in the selection of a facility and that there are

a range of other factors that are determinants in demand and therefore occupancy rates and

performance of centres.

For instance, cross-tabulation of occupancy rates and the age of respondent’s centres reveals

that facilities which are older than 2 years have an occupancy rate in the order of 75%. Only

five respondent centres were less than 2 years old for which occupancy rate data was

available; these centres reported an average occupancy rate of 87%, but noting statistical

limitations of the small sample size for this group. Anecdotally, newer centres may have a

perception of higher quality for parents and be locating in areas of heightened growth and

demand; providing heightened reported occupancies.

Less than 10% (21) of respondent facilities reported having a waiting list across all age groups

at the time of the survey. 28% reported having a waiting list for any particular age group.

Waiting lists were mostly for infants (birth to 2 years) which comprised 44% of lists; followed

by lists for 2 to 3 year olds (31.5%) and the remainder for 3 years to school age.

Qualitative responses were sought from respondents regarding the opportunities, constraints

and issues surrounding child care as an industry. These responses are summarised in TABLES

3.3-3.5 below. It is noted that issues regarding funding and legislation within the sector are a

key concern of operators.

14 | P a g eTABLE 3.3: Q14 – What do you consider are the key opportunities and prospects facing the

child care sector?

Responses Frequency

Early education for next generation 5

Increase in staff qualifications 4

School Readiness 3

Positive outcomes and framework 3

Children not attending 1

None 4

New funding for childcare 3

Introduction of new family package 3

New assessment and ratings 1

Lower ratio's, strain on costs 2

Increasing community awareness of early education importance 11

Oversupply of spaces/centres 6

Loss of access 2

Improved recognition of importance 7

Lack of staff due to poor pay and conditions 3

LDCPDP 1

More indigenous using child care 2

Loss of connection due to technology 1

Greater need due to parents needing to work longer hours/days 1

Detrimental effect of jobs for family package 2

Poor wages for educators 2

Capped rebate of $7,500 1

Poor quality RTO's flooding the industry 1

Bleak future with changes too schooling 1

Increased fees are getting unaffordable for families 1

Funding for Kindergarten 1

Accreditation process 1

Increasing costs gas, electricity etc 1

TABLE 3.4: What factors or issues (if any) do you believe are influencing or constraining your

centre at this point in time?

Answer Frequency

Cost of quality program 1

Population growth in area 2

Lack of family input 3

Increased Fees 17

Increased Wages 6

Reduced child/educator ratio's 5

Competition/New centres 24

Special offers (Free days, weeks etc) 1

People on benefits not working 1

15 | P a g eLack of qualified/suitable staff 11

Lack of local professional development opportunities 3

Uncertainty about impact of Jobs for Families Package 3

Lack of employment in area for parents 6

Cost, no grants for profit centres 1

Poor quality RTO's 1

Poor media coverage 1

Family income 1

Inconsistent assessor ratings 2

Over regulated by government 1

Lack of planning for future centres 2

Limited space and leases for buildings 1

Private school kindergartens 1

Families running out of CCR due to costs and cuts 1

Effect of paid maternity leave on nursing rooms 1

Of the respondents who completed this question, 21% indicated that they were concerned

about the number of new centres opening within their area. A number further indicated that

they would be required to upgrade their centres to remain competitive but this was likely to

be unsustainable given their financial structures. Others blamed the local planning

authorities for unregulated testing of demand versus supply and therefore the approvals

process was considered ineffective.

TABLE 3.5: Are there any other factors or issues that you would like to raise concerning the

operation of your centre or the industry as a whole?

Answer Frequency

Too many unnecessary centres being built 8

Lack of pay for educators 5

Increase in behaviour, illness, health management 2

Not at this time 6

Rural area's not able to share opportunities 1

Quality of assessment standards 4

Introduction of subsidy 1

Changes to family assistance for non-working parents 2

Frequent changes to legislation, leads to stress in workplace 3

Requirement for qualified staff, limited wage allowance 5

Increased costs 3

Economic downturn in community 2

Unfair grants for non-for-profit centres 2

Concern over new jobs for family package 5

Concern for equal care 3

Too much government regulation 4

Reported occupancy % not always accurate 2

Lack of direction for industry future 1

Bias for non-profit centres 3

16 | P a g eLack of respect of industry and educators 1

Lack of networking for educators 1

Low socio-economic factors 1

Assessors who are not child care trained or experienced 2

Less unnecessary paperwork 1

Poor RTO quality 4

Reduced ratios increasing costs and expense for families 2

Stigma towards male early educators 1

3.2 REGRESSION ANALYSIS

Urban Economics conducted a regression analysis on the results provided by the ACA Qld

Member Survey to develop an understanding of the relationships involved between certain

variables and the average price level of daily care associated with a childcare centre.

Regression Analysis is a statistical measure that attempts to determine the strength of the

relationship between one dependent variable and a series of other changing variables (known

as independent/explanatory variables).

The analysis was carried out in a methodical manner. An initial regression was run using each

survey question as an explanatory variable, however the results were inaccurate due to the

variables resemblance to one another brought about by the sub-group questions (0-2yrs, 2-

5yrs, etc.).

This lead to the data being sorted via question type, culminating any sub-groups into a single

variable (Eg. Total Places). A standard method for estimating a regression model (Standard

Least Squares Estimation) was run, assuming it was the best estimation method (Best Linear

Unbiased Estimator), to which the model was then tested for regression properties such as;

inconsistent variance in the model, model covariance unequal to zero, cointegration of

explanatory variable with one another and the cointegration of explanatory variables with

the error term.

The regression model was found to have many of these properties and so a more appropriate

method of estimation was used (Robust Least Squares Method with Huber-White covariance

under Heteroskedastic consistent standard errors).

Each of the explanatory variables were then tested for significance at the 5% level and were

omitted if their effect was deemed insignificant. The following are the explanatory variables

that were found to have a significant effect on Average Price:

• Total Number of Enrolments across all sub-groups

• Total Number of Daily Attendances across all sub-groups

• Total Number of Places

• Breakeven Point under 80%

• Built within the last 2 years

• Waiting List

17 | P a g e3.2.1 THE REGRESSION MODEL

The equation of the regression model is stated as:

y = b 0 + b1 x1 + b2 x2 + b3 x3 + b4 x4 + b5 x5 + b6 x6

Whereby:

y = Average Price b0 =82.924

x1 = Total Number of Enrolments across all sub-groups b1 = -0.033

x2 = Total Number of Daily Attendances across all sub-groups b2 = 0.046

x3 = Total Number of Places b3 = 0.045

x4 = Breakeven Point under 80% b4 = -2.007

x5 = Built within the last 2 years b5 = 1.847

x6 = Waiting List b6 = 2.316

Leading to the inferences outlined below:

• If the total number of enrolments increases by 1 person, the average price will

experience a $0.03 decrease in price.

• If the total number of daily attendees increases by 1 person, the average price will

experience a $0.05 increase.

• If the total capacity of a child care centre increases by 1 person, the average price will

experience a $0.05 increase.

• If a Childcare centre’s breakeven point is under 80% occupancy, the average price will

experience a $2.01 decrease.

• If the Childcare Centre was built within the last two years, the average price will

experience a $1.85 increase.

• If the waiting list of a Childcare centre increases by 1 person, the average price will

experience a $2.32 increase.

The developed regression model featured a final R2 value of 15% meaning; the six variables

can explain only 15% of the variation in Average Price. An R2 value of below 40% is expected

when dealing with any field that attempts to predict human behaviour. Such a value therefore

renders this model inappropriate for forecasting, however the coefficient relationships

(stated above) are legitimate due to their significance at the 5% level. Factoring in variables

such as locality, proportion of 0-4 years of age in surrounding region, fixed and current costs,

price of substitute services, etc. would increase the R2 value and allow for forecasting.

The values of coefficients themselves are small due to the inelastic nature of the childcare

market, causing prices to be ‘sticky’ and therefore do not vary by approximately more or less

than $10-15. A $0.05 increase per daily attendee is an example of this as its very slight change

is not seen in price level until more than 100 children attend in a single day, pushing the price

up by $5 (assuming all else remains constant) only for the childcare centre to be at maximum

capacity in any case.

18 | P a g eThe results of the regression analysis highlights that the childcare economy is largely market

lead, whereby change in supply and demand is made through significant changes in market

variables rather than the force of external factors e.g. price is determined by equilibrium. This

is seen in the above relationships whereby an increasing waiting list signals increased demand

and so places a significant change on price, or where the prospect of a new centre sees an

increase in price due to the perceived idea that it offers a better service compared to

local/older competition.

Note that this regression is indicative of only a sample (160 child care centres for which there

was robust data) and does not consider locality or other area defining aspects, but rather

displays the positive or negative relationship the tested explanatory variables have on the

average daily price of childcare in a broad and generic scenario.

Demand is just as important as supply within the childcare market and is as dependent if not

more; on quality, as it is on price. This inference is adopted within Chapter 6 which explores

occupancy rates and centre viability.

19 | P a g e4.0 DEMAND DRIVERS

4.1 UTILISATION OF CHILDCARE IN QLD

The Department of Education and Training’s Early Childhood and Child Care in Summary for

the June Quarter 2016 estimated that some 159,030 children utilised long day care services

in Queensland, and the State included 1,482 long day care services in the period and around

116,000 licenced places. This suggests that on average, more than 107 children can be

attributed to each centre or ratio of 1 place for every 1.37 children utilising long day care

services.

Similarly, as at June 2016, Queensland included an estimated 324,000 children aged 0-4.

Assuming that this age group were the only users of long day care services, and allowing for

double counting of children which may present at more than one facility; between 45% and

50% of children aged 0-4 in Queensland utilised long day care services through the June

Quarter 2016.

4.2 POPULATION AND HOUSEHOLD GROWTH

Between 2006 and 2016, the population of SEQ increased from an estimated 2.67million

persons in 2006, to around 3.3million persons in 2016, or approximately 2.1% p.a. over this

period; compared to QLD which increased from 4.01million persons in 2006 to 4.84million

persons in 2016 at approximately 1.9% p.a. The dynamic is outlined in TABLE 4.1, whereby

SEQ is increasing its share of the State’s population compared to the Regional and Rural Study

Areas.

TABLE 4.1: Population Growth

2006 2012 2013 2014 2015 2016 P.A. 2006-2016

SEQ 2,671,361 3,076,351 3,135,324 3,187,936 3,238,395 3,297,983 2.1%

Regional 954,843 1,080,359 1,100,859 1,114,889 1,123,343 1,128,160 1.7%

Rural 381,788 411,495 415,576 417,100 417,006 417,160 0.9%

QLD 4,007,992 4,568,205 4,651,759 4,719,925 4,778,744 4,843,303 1.9%

Source: ABS

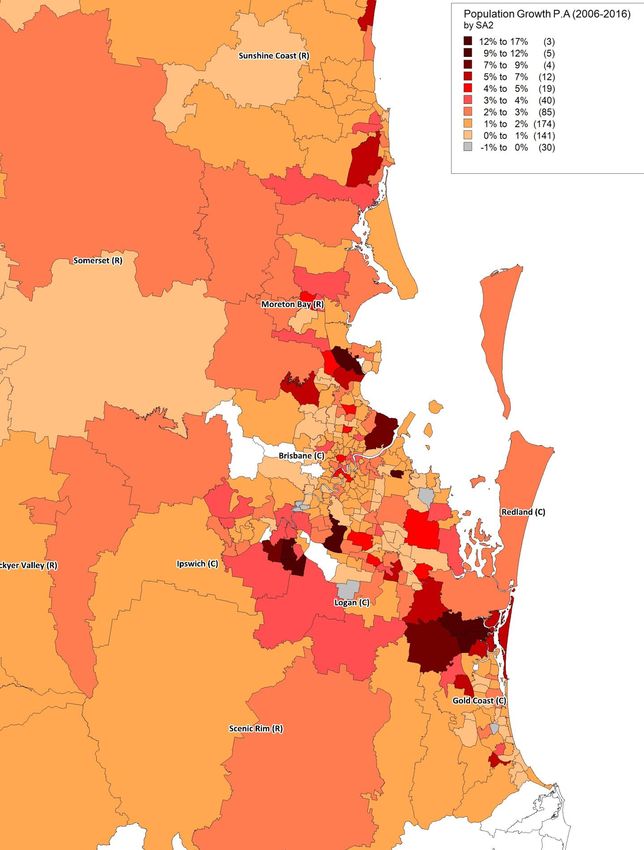

Just as population growth has not been evenly distributed across QLD, some areas of SEQ

experienced significant increases in population and new household formation, whilst others

have recorded very little growth, and in some areas, declining populations. TABLE 4.2 lists the

fastest growing statistical areas in QLD between 2006 and 2016, all of which are within SEQ

and Townsville, with the exception of Gracemere.

Notably, these growth localities correspond with the existing supply of child care facilities

across QLD, particularly in the northern Gold Coast growth corridor and within the Moreton

Bay Region around North Lakes-Mango Hill, as illustrated in FIGURES 4.1 and 4.2.

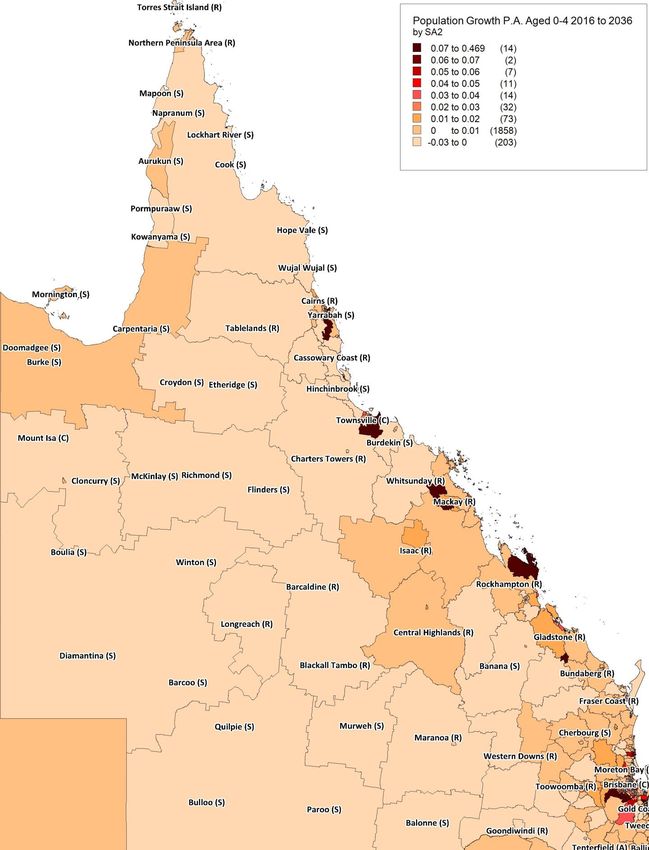

20 | P a g eFIGURE 4.1: Average Annual Population Growth by SA2 – SEQ

21 | P a g eFIGURE 4.2: Average Annual Population Growth by SA2 – QLD

22 | P a g eTABLE 4.2: Top 20 Fastest Growing SA2’s in QLD – 2006-2016

SA2 2006 2016 % Growth 2006-2016

Pimpama 1,728 8,161 16.8%

North Lakes - Mango Hill 9,157 30,772 12.9%

Coomera 4,134 13,324 12.4%

Springfield Lakes 4,969 14,088 11.0%

Pallara - Willawong 1,780 4,738 10.3%

Deeragun 8,946 23,088 9.9%

Wakerley 3,983 9,603 9.2%

Bellbird Park - Brookwater 5,025 11,981 9.1%

Upper Coomera - Willow Vale 14,777 32,058 8.1%

Bohle Plains 3,039 6,481 7.9%

Redbank Plains 9,530 20,067 7.7%

Hope Island 5,651 10,591 6.5%

Peregian 5,247 9,826 6.5%

Ormeau - Yatala 10,988 20,195 6.3%

Murrumba Downs - Griffin 8,457 15,452 6.2%

Caloundra - West 10,022 17,964 6.0%

Gracemere 6,206 10,948 5.8%

Oonoonba 3,618 6,377 5.8%

Cashmere 10,741 18,676 5.7%

Bethania - Waterford 5,974 10,265 5.6%

Source: ABS

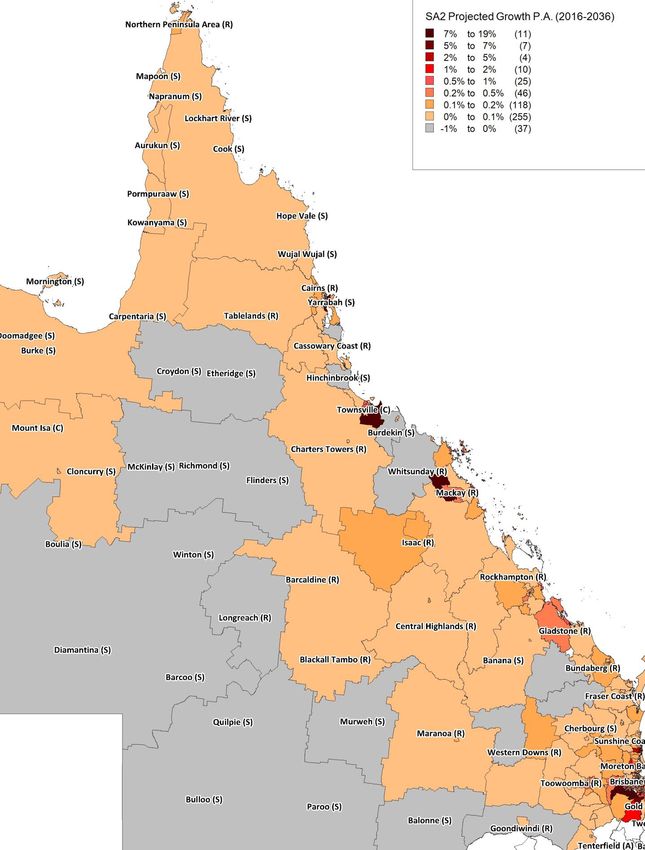

Population projections prepared by the Queensland Government Statisticians Office (QGSO)

outline where population growth is anticipated to be greatest towards 2036. FIGURE 4.3

graphically displays the projected level of population growth within the SA2’s of QLD.

TABLE 4.3 lists the top 20 fastest growing SA2s projected for this period.

23 | P a g eTABLE 4.3: Top 20 Projected Population Growth by SA2’s in QLD – 2016-2036

#2016 %PA 2016-

SA2 Name 2016 2021 2026 2031 2036

-2036 2036

Ripley 3,764 17,700 43,056 74,582 104,610 100,846 18.1%

Eagle Farm - Pinkenba 553 1,766 2,786 6,718 9,388 8,835 15.2%

Rosewood 12,145 15,945 25,474 40,187 61,867 49,722 8.5%

Coomera 12,577 19,632 33,184 47,852 63,762 51,185 8.5%

Townsville - South 4,489 7,840 12,022 16,203 20,778 16,289 8.0%

Pimpama 6,033 10,688 16,843 20,657 25,931 19,898 7.6%

Greenbank 13,294 18,092 30,064 40,071 55,959 42,665 7.5%

South Brisbane 6,920 11,731 17,664 23,250 28,406 21,486 7.3%

Upper Caboolture 3,317 5,157 8,256 10,993 13,539 10,222 7.3%

Gordonvale - Trinity 8,939 13,286 19,818 26,456 34,746 25,807 7.0%

Morayfield 5,348 7,191 10,002 13,743 18,995 13,647 6.5%

Bellbird Park - Brookwater 12,368 15,896 23,449 32,973 42,633 30,265 6.4%

Jimboomba 23,569 31,260 44,847 60,849 79,824 56,255 6.3%

Chambers Flat - Logan

4,396 5,163 7,148 9,184 14,817 10,421 6.3%

Reserve

Fortitude Valley 6,223 9,378 12,216 16,071 20,851 14,628 6.2%

Caloundra - West 17,921 25,973 34,722 49,448 59,535 41,614 6.2%

Springfield Lakes 13,769 18,162 26,841 35,312 45,331 31,562 6.1%

Rochedale - Burbank 5,016 6,197 7,348 10,930 15,578 10,562 5.8%

Landsborough 10,301 12,743 19,009 24,675 30,991 20,690 5.7%

Newstead - Bowen Hills 9,672 14,921 19,303 23,596 27,904 18,232 5.4%

Source: QGSO

The ‘south-west corridor’ of SEQ, which comprise the very large satellite communities of

Yarrabilba, Greater Flagstone, Echo Ripley and Greater Springfield, denotes particularly high

levels of growth. Other notable growth areas include masterplanned areas of Townsville and

Cairns as well as near-city localities such as Newstead, Fortitude Valley, South Brisbane and

Eagle Farm (Hamilton).

24 | P a g eFIGURE 4.3: Projected Average Annual Population Growth by SA2 – QLD

25 | P a g e4.3 DEMOGRAPHIC & SOCIO-ECONOMIC CHARACTERISTICS

The results of the 2011 ABS Population and Household Census (the most recent complete

Census results available) and some results of the 2016 Census have been utilised to examine

the demographic and socio-economic characteristics of the Study Area. Additional data has

also been sourced from the Department of Employment and subsequent ABS data.

Relevant demographic data is displayed thematically and graphically in FIGURES 4.4 to 4.7

where appropriate including:

• Female workforce participation;

• Children aged 0-4;

• Births;

• Labour force;

• Unemployment rate;

• Places of work; and

• Median household income (2016 Census)

The level of female workforce participation within a community is a known determinate of

the need to access child care services. TABLE 4.4 lists the top 20 statistical areas within

Queensland for female workforce participation as at the 2011 Census.

The majority of these areas are noted within inner-Brisbane and areas linked to typical

industries of the female workforce such as Shailer Park and Kirwan - West (retail). Conversely,

areas with lower female workforce participation include those with larger populations of

older persons and concentrations of retirees such as on Bribie Island, and areas with

universities such as St Lucia and Robertson. Interestingly, universities typically include

childcare facilities which cater to the significant working populations they support,

highlighting the trend for families to access facilities proximate to their place of work.

TABLE 4.4: Top 20 Female Workforce Participation

Male Female TOTAL

Norman Park 81.3% 74.4% 77.8%

Red Hill (Qld) 77.4% 74.4% 75.9%

Alderley 77.8% 74.0% 75.9%

Auchenflower 76.2% 73.9% 75.0%

Newstead - Bowen Hills 78.7% 73.8% 76.4%

Wakerley 85.3% 73.1% 79.0%

Brinsmead 79.5% 73.0% 76.2%

Eatons Hill 82.3% 72.8% 77.5%

Paddington - Milton 79.6% 72.6% 76.0%

Cashmere 82.5% 72.2% 77.3%

Sheldon - Mount Cotton 80.4% 72.1% 76.2%

Windsor 75.9% 72.0% 73.9%

Springfield Lakes 86.2% 71.9% 78.7%

Morningside - Seven Hills 78.8% 71.6% 75.1%

26 | P a g eWeipa 81.8% 71.6% 77.1%

Mount Louisa 79.6% 71.6% 75.6%

Kirwan - West 79.9% 71.3% 75.4%

Redlynch 78.4% 71.1% 74.6%

Wilston 76.9% 70.8% 73.8%

Shailer Park 79.6% 70.8% 75.2%

Source: 2011 ABS Census

Despite Australia’s ageing population, the number of young children aged 0 to 4 is projected

to increase within QLD toward 2036, particularly within SEQ and regional centres. Rural areas

are anticipated to include declining numbers of young children, which is in line with negative

growth in these areas overall.

Adopting existing levels of long day care utilisation, and average sized facilities; some 33,000

additional places across more than 420 facilities would be required within QLD between 2016

and 2036 due to population growth alone.

TABLE 4.5: Children Aged 0-4 Population Growth

2011 2016 2021 2026 2031 2036 P.A. 2016-2036

SEQ 199,476 216,499 229,369 248,946 268,984 290,067 1.5%

Regional 75,990 78,491 80,938 85,432 90,115 95,103 0.9%

Rural 28,864 28,316 27,658 27,664 27,971 28,445 -0.1%

QLD 304,330 323,305 337,965 362,043 387,069 413,615 1.2%

Source: QGSO

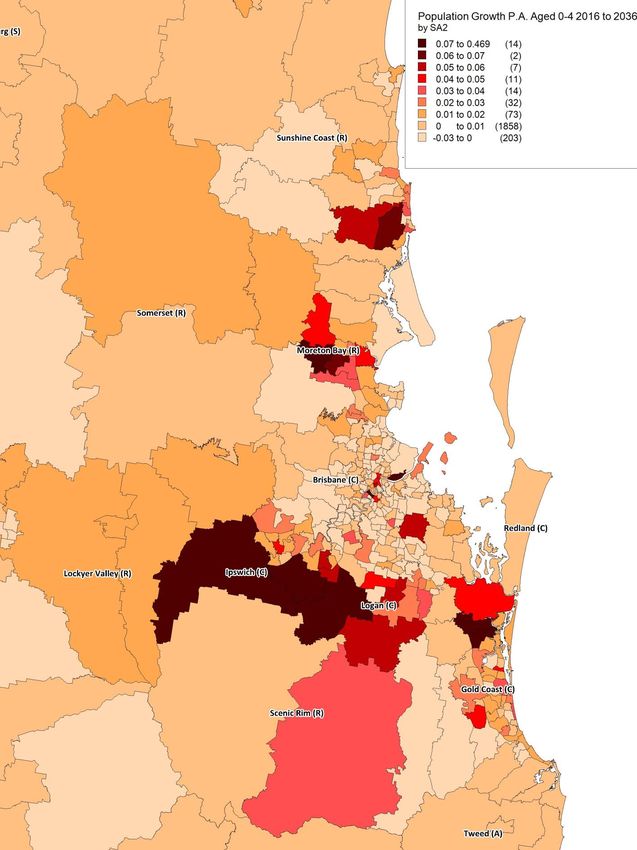

FIGURE 4.4 illustrates the projected average annual growth in the 0-4 age group by SA2 within

SEQ; highlighting the prevalence of this growth within the major growth communities of the

northern Gold Coast, Logan and Ipswich. Other growth areas within this age group are

projected in areas with low existing bases of children such as South Brisbane and Eagle Farm

(Hamilton).

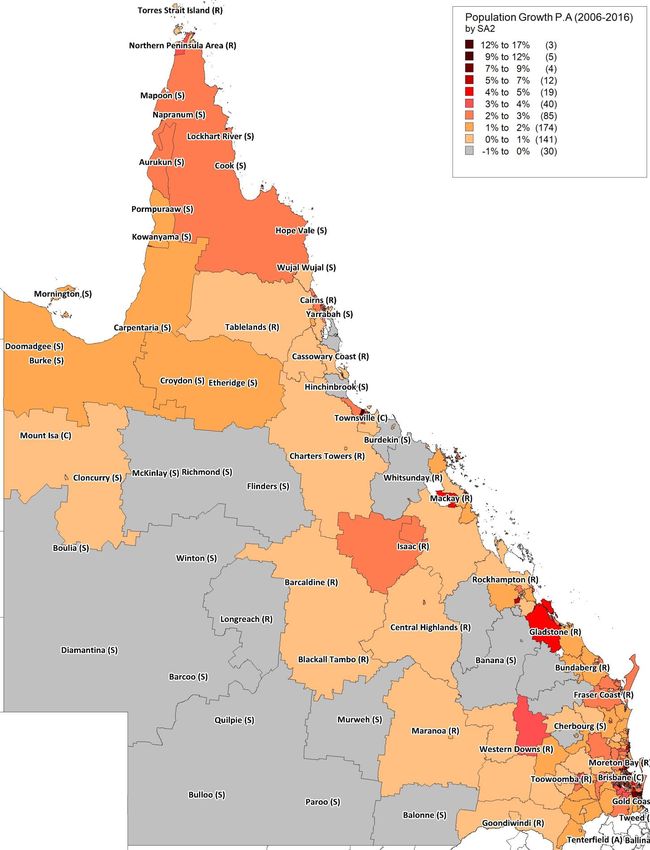

Conversely, growth across QLD is limited to major regional towns such as Rockhampton,

Gladstone, Mackay, Townsville and Cairns whilst rural areas are generally projected to include

declining populations of young children as illustrated in FIGURE 4.5. Similarly, early results

from the 2016 ABS Census indicate that the population of children aged 0-4 within QLD has

in fact declined since the 2011 Census, suggesting demand may not be as high as estimated.

Areas of projected increases in the 0 to 4-year-old population are confirmed within analysis

of births data by SA2. TABLE 4.6 lists the top 20 statistical areas for births between 2010 and

2015, outlining substantial quantums of new children within expanding residential areas.

27 | P a g eFIGURE 4.4: Projected Children Aged 0-4 – 2016-2036 – SEQ

28 | P a g eFIGURE 4.5: Projected Children Aged 0-4 – 2016-2036 – QLD

29 | P a g eTABLE 4.6: Top 20 Most Births by SA2 – 2010 to 2015

2010 2011 2012 2013 2014 2015 2010-2015

Upper Coomera - Willow Vale 488 510 572 550 569 544 3,233

Mount Isa 503 420 458 456 436 488 2,761

Forest Lake - Doolandella 461 435 448 431 466 429 2,670

North Lakes - Mango Hill 305 366 438 421 460 484 2,474

Caboolture 381 397 428 417 421 418 2,462

Deeragun 295 347 390 456 492 473 2,453

Dakabin - Kallangur 373 434 415 426 413 381 2,442

Redbank Plains 355 397 440 427 395 422 2,436

Caboolture - South 377 427 416 396 408 378 2,402

Hills District 389 384 364 355 333 344 2,169

Southport 349 360 353 369 373 341 2,145

Deception Bay 369 356 325 342 358 282 2,032

Calamvale - Stretton 299 290 347 355 365 340 1,996

Inala - Richlands 295 304 307 287 320 340 1,853

Pacific Pines - Gaven 308 297 306 312 325 298 1,846

Springfield Lakes 277 286 286 322 327 336 1,834

Ormeau - Yatala 299 310 317 271 315 280 1,792

Jimboomba 308 313 278 271 280 337 1,787

Woodridge 297 286 307 300 289 275 1,754

Nerang - Mount Nathan 311 303 285 286 295 253 1,733

Source: ABS

TABLE 4.7 outlines the SA2s with the largest quantum of employed persons within QLD

according to Small Area Labour Market (SALM) data as at June 2016. These localities are

dominated by areas with high proportions of dual income working families which would have

a heightened propensity to access child care services. Mount Isa is the only locality outside of

SEQ with a significant employed workforce which also includes an above average supply of

child care services; highlighting the increased provision of these services in areas catering for

industries (such as mining) in regional and rural areas.

TABLE 4.7 Top 20 Employed Persons by SA2 – June 2016

Labour Unemployed Employed

Force Persons Persons

Upper Coomera - Willow Vale 17,315 807 16,508

Southport 17,712 1,476 16,236

Forest Lake - Doolandella 16,370 670 15,700

North Lakes - Mango Hill 15,349 619 14,730

Hills District 14,275 462 13,813

Surfers Paradise 14,304 949 13,355

Robina 13,432 497 12,935

Calamvale - Stretton 12,924 564 12,360

Dakabin - Kallangur 13,082 1,113 11,969

Pacific Pines - Gaven 11,452 522 10,930

Mount Isa 11,805 907 10,898

30 | P a g eCaboolture 12,415 1,564 10,851

Coorparoo 11,213 441 10,772

Narangba 10,872 335 10,537

Noosa Hinterland 11,070 592 10,478

Ormeau - Yatala 10,869 407 10,462

Nerang - Mount Nathan 11,330 913 10,417

Mudgeeraba - Bonogin 10,786 441 10,345

Cashmere 10,633 302 10,331

Helensvale 10,452 393 10,059

Source: Small Area Labour Market data

There is a noted trend for families seeking to access child care services nearer to their place

of work as opposed to where they live. Urban Economics notes an ABS survey which indicates

that 12% of families who utilise long day childcare, ensure that these facilities are in close

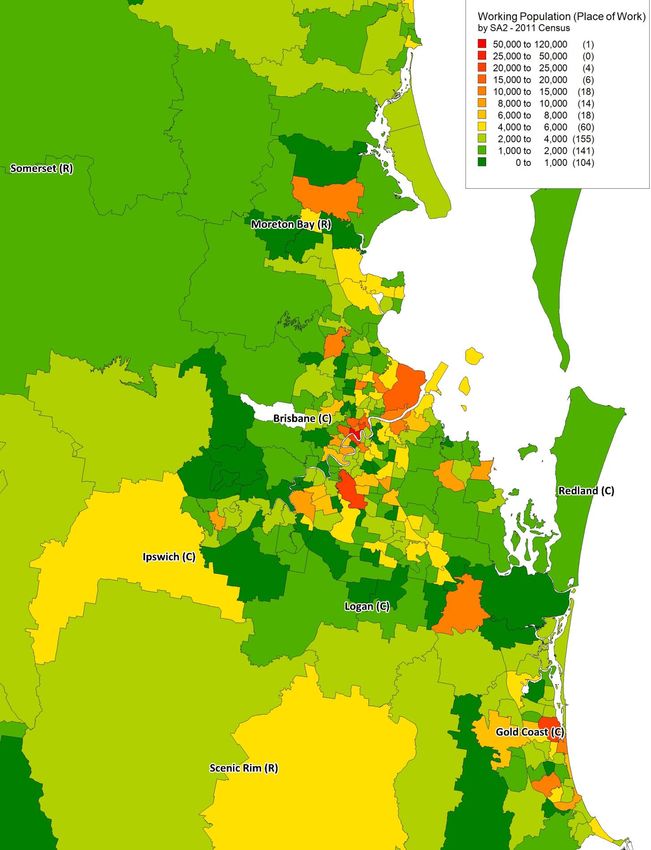

proximity to their place of work. With this in mind, FIGURE 4.6 illustrates the working

populations of SEQ by SA2 (place of work); indicating localities where workers may create an

additional layer of demand for access to service.

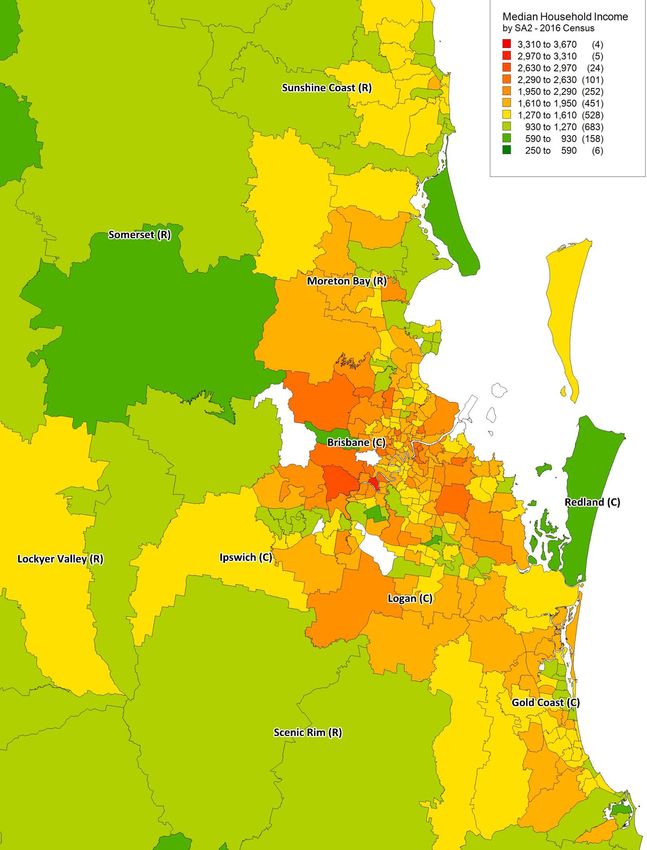

FIGURE 4.7 illustrates median household incomes within SEQ as at the 2016 Census.

Heightened incomes indicate a heightened propensity to afford child care services but

conversely, typically correspond with areas with lower proportions of young children. Higher

household incomes are however commensurate with growth areas which support dual

income working families

31 | P a g eFIGURE 4.6: Workers by SA2 2011 Census – SEQ

32 | P a g eFIGURE 4.7: Median Household Incomes 2016 Census - SEQ

33 | P a g e5.0 DEVELOPMENT PIPELINE

It is recognised that development activity within the childcare sector has increased and

become more sophisticated as noted within the various trends outlined in Chapter 2. The

following summarises the development pipeline of childcare centres across Queensland,

utilising data extracted from Corelogic’s market intelligence platform Cordell Connect in May

2017.

In total, some 156 proposed, approved and under construction projects have been identified

across Queensland, with an ultimate capacity of around 16,600 additional places or an

average of approximately 106-places per centre. As noted in Chapter 4, population growth

projections for the 0 to 4 age group in QLD suggest that an additional 33,000 places or more

than 420 typical facilities would be required within the state between 2016 and 2036. If all

these places proceed, half the projected demand over a 20 year period could be provided

within this development pipeline.

There are varying estimations of the likelihood that childcare development projects within

the pipeline will actually proceed although a breakdown of project statuses from the data

suggests that:

• 34% of projects have ‘Commenced’;

• 2% are in ‘Early’ planning;

• 11% are ‘Firm’;

• 47% are ‘Possible’; and

• 6% have an ‘Unknown’ status.

Conservatively assuming that just 50% of the mooted projects will proceed, the current

pipeline would account for more than a quarter of the total additional supply needed over

the period 2016-2036. Furthermore, it is noted that there was an actual decline in the real

numbers of children aged 0 to 4 years within Queensland between 2011 and 2016, suggesting

that there may be some revisitation of the population projections prepared by the State, as

is typically undertaken every two to three years and post the release of Census data.

Therefore, it could be argued that if growth rates in Queensland continue to moderate, the

number of children 0 to 4 years may be less than projected and influence the demand for

child care places.

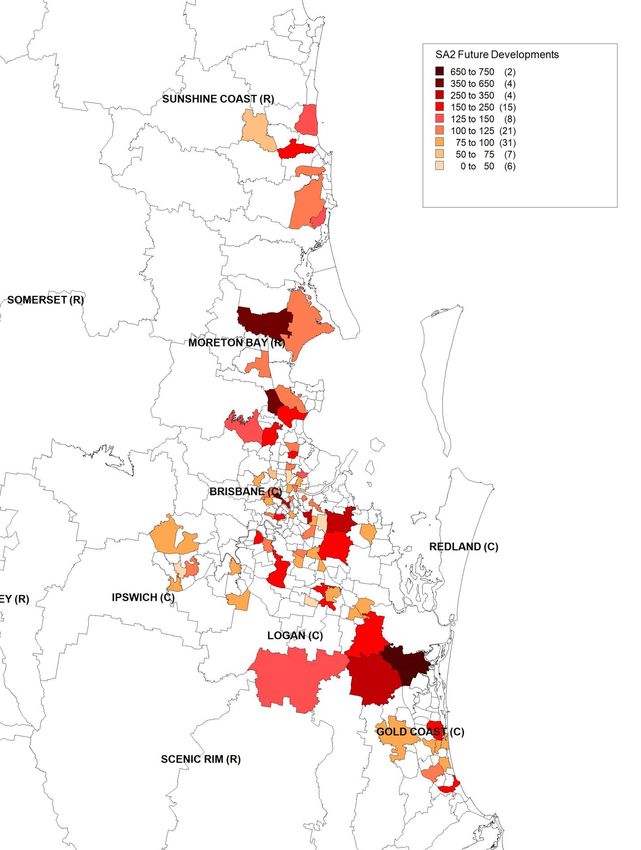

FIGURE 5.1 illustrates the development pipeline of centres across SEQ, highlighting the focus

of new projects within the south-east corner. Approximately 80% of the mooted future supply

of places are within SEQ with the balance in the Regional Study Area.

34 | P a g eMuch of the future supply is proposed within residential growth areas which as noted in

Chapter 3, already include the greatest supply of facilities in many instances. E.g. Coomera.

Given the projected growth scenarios of these areas, it is expected that additional facilities

are planned within these areas although, there is a potential for an oversupply of facilities

should these growth scenarios not eventuate. It is noted that these statistical areas are

geographically diverse in size and growth profile which are not directly comparable, but do

provide an indication of future supply.

Interestingly, a significant proportion of the development pipeline is proposed within

established areas of SEQ and as illustrated within FIGURE 4.1, on the fringe of inner-Brisbane.

A range of factors may be attributed to this dynamic such as:

• Gentrification within these localities;

• Proximity of these areas to places of employment; and

• Speculative development targeting areas with older and lower quality centres.

Supply by its very nature is “lumpy” in its growth. Unlike population growth which is typically

exponential, the addition of new places is dependent on new centres or expansion of existing

centres, much the same that a new commercial office building or shopping centre is lumpy

not incremental in its development. As a result, there will be periods of supply additions as

well as periods of undersupply of places because of the very nature of centre development

and growth. There is currently a market appetite for new child care centres as a relatively

affordable investment stream that makes them palatable to small to medium investors and

SMSF’s, institutions etc in much the same way that there has been strong interest and uptake

in investment in new service stations across Queensland.

This supply proliferation is promoted by government inquiries that promote a sense of

urgency in the need for child care places and affordability around child care, early childhood

educational facilities that are promoting their courses and again a sense of urgency around

the need for early educators, as well as the activities of child care groups themselves as they

seek to gain critical mass. Balancing the needs of children and families against the “informed”

sources is typically market-led, but unlike shopping centres or service stations in Queensland

for instance, is faced with less planning legislative tools and mechanisms to “check” growth.

35 | P a g eFIGURE 5.1: Development Pipeline Places by SA2 - SEQ

36 | P a g e6.0 OCCUPANCY RATES AND CENTRE VIABILITY

This Section critiques the potential impact of childcare centre supply in relation to occupancy

rates, and the ongoing viability of centres.

The regression modelling outlined in Chapter 3 provides some insight into the causal

relationship between the supply of child care places and centre viability. Whilst there is some

evidence that competitive supply is a determining factor, the results are much stronger for

the explanation that quality and demand determine occupancy rates and the subsequent

viability of facilities.

In a typical market scenario, the price of a service such as childcare would respond to both

the level of demand and supply and specifically, price would be expected to decrease with

additional supply. Childcare in Australia however, is subsidised (a dynamic which will shift

with the Jobs for Families Package in 2018) and includes a high level of fixed costs

(predominantly wages) as outlined in TABLE 6.1. As such, prices are relatively inelastic, and

typically do not decrease with increased supply and competition; dispelling the theory that

increased supply will increase affordability for families. In fact, it is a more tenable proposition

that a centre which is substantially underperforming due to an oversupply situation would

cease operation; removing choice and accessibility for the communities in which they locate.

TABLE 6.1: Performance Benchmarks - Child Care Services – 2014/15

Annual turnover range

Key benchmark range $65,000 – $200,001 – More than

$200,000 $600,000 $600,000

Total expenses/turnover 52% – 63% 72% – 86% 78% – 87%

Average total expenses 58% 79% 83%

$65,000 – $200,001 – More than

Benchmark Range

$200,000 $600,000 $600,000

Labour/turnover 23% – 45% 38% – 51% 44% – 52%

Rent/turnover 9% – 14% 7% – 12% 7% – 11%

Motor vehicle expenses/turnover 5% – 7% 1% – 3% 1%

Source: ATO

• 70% occupancy is the oft quoted break-even point for a child care centre (Ibisworld

industry report) however; the Productivity Commission in its 2015 Review explained

that increased costs may now place this figure closer to 80%.

• Affinity Education for the 2014/15 financial year noted that expenses were equivalent

to 84.2% of turnover comprising; employment (59.1%), building occupancy (13.9%),

direct expenses (9.6%) and other (1.6%); highlighting the large proportion of fixed

costs and low margin nature of the business. Affinity owned centres reported an

occupancy rate of 84% in 2014/15.

• The Australian Childcare Alliance’s 2015 Member Survey reported an average

occupancy rate of 76% across reporting member centres.

37 | P a g e• G8 Education reported an occupancy rate of 80.85% in 2016 and 81.88% in 2015

across its portfolio; indicating that profitable operations are those with occupancies

above 80%.

• A study of government involvement within the child care sector in the UK states that

an 80% occupancy is the rate of viability for a child care centre (Penn, 2007).

• 76% occupancy rate reported by the respondents to the survey for 2017 and 40% of

respondents who answered the question identified that the 70-80% range was the

breakeven point for their centre.

Adopting the abovementioned assumptions and results of the Member Survey, Urban

Economics considers that the average breakeven point for childcare centres is in the order of

75%. Centres will continue to operate with occupancy rates above 60% in some instances

however; most will exit the market, cut staff or resources or not enter with occupancy rates

near or below this point.

On this basis, a significant oversupply of places is considered to be when the occupancy rates

of centres within a local market is below 60% in rural and regional areas of Queensland; and

70% in SEQ.

38 | P a g eYou can also read