Daily Grain / Livestock Marketing Outlook 5/7/2021 - A C Trading Co

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Daily Grain / Livestock Marketing Outlook

Written by: Jim Gerlach

5/7/2021

Early Call 8:45am EDT: Corn up 5, soybeans up 11, wheat up 10. Early Friday, Dow

Jones futures are trading higher, extending Thursday's new high with higher trading in

Europe with analysts expecting the Labor Department to show an increase of one

million jobs in Friday's nonfarm payrolls report (actual was 266,000). Thursday's

jobless claims fell to the lowest level since last year's pandemic, an encouraging sign the

U.S. economy is recovering. Meanwhile, COVID-19 cases in India continue to escalate.

Grain prices continue to advance on drought in Brazil, less than ideal U.S. crop weather

and new highs in U.S. basis levels, indicating a continuation of strong demand as end

users are still making money.

Grains: Soybeans for July delivery rose 1.8% to $15.71 ½, its highest close since

October 2012, on the Chicago Board of Trade Thursday. Dry conditions in North and

South America squeezed supply amid robust demand. Corn for July delivery rose 1.6%

to $7.20, its highest close since March 2013. Wheat for July delivery rose 1.5% to $7.55

¼, its highest close since February 2013. While rainfall is expected throughout much of

the U.S. Midwest this weekend, the northern Plains is only expected to receive moderate

rainfall. That's bad news considering the already existing dryness of the area. This was a

factor pushing grains higher across the board. Additionally, cold temperatures expected

this weekend carries the risk of frost. Drought conditions in Brazil also lifted grain

futures trading Thursday. Soybean futures led grains higher Thursday. A tight supply

globally and robust demand is supporting futures as they charge toward all-time highs.

The market is trending higher with the trade mostly orderly. With the U.S. on pace to

deplete bean supplies this summer along with the fact the U.S. is not set up to import

meaningful quantities of beans suggests the bean market is headed for more volatility

and higher prices in the coming months. The strong demand story surrounding soybean

oil also provided a lift for soybean futures Thursday and may keep providing them with

support. The edible oil markets remain hot amidst enthusiasm over the next generation

of renewable fuels. The edible oil markets breathed new life into the soybean market,

pushing new-crop contracts to new highs for this bull market, while the nearby contracts

1

remain just below recent eight-year highs. Tight supply of soybean oil is expected to

continue well into next year, according to the United Soybean Board. Export sales of

U.S. corn were far weaker than expected by traders, amid a large reduction in sales for

the 2020/21 marketing year. While not creating a lasting impact on corn futures trading,

the slim tonnage may be a sign that demand rationing has started.

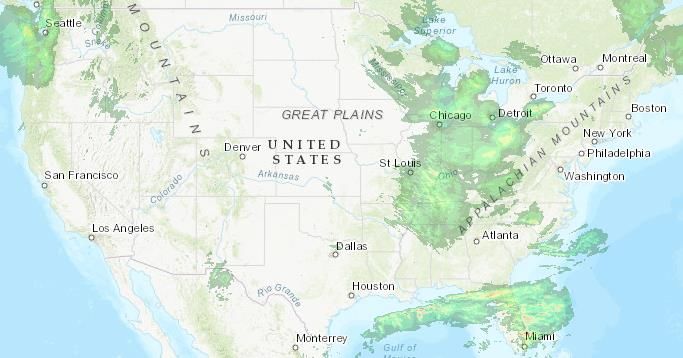

Rainfall yesterday was largely confined to the ECB and OH Valley, with modest

amounts generally from .25-.75” (see left map). Moderate coolness prevails across the

major U.S. crop areas through next Wednesday before easing. A band of rain affects the

northern Plains and especially the southern half of the Corn Belt this weekend, followed

by light showers in HRW wheat areas and the mid-South early next week (see 7-day

NOAA forecast map right), and then a fairly stormy period occurs within May 15-21.

About 50% of U.S. spring wheat receives 0.33” to 0.67” of rain Saturday (MT,

southwest half of ND, much of SD). 1-2” of rain affects much of IL, IN, MO, OH and

southern IA Sat-Sun, while 0.5-1” of rain affects the mid-South Sat-Sun, followed by

scattered t-storms Mon-Wed. Light rain is probable for HRW wheat in much of the

central and southern Plains Mon-Tue. In Brazil, little to no rain is foreseen for safrinha

corn in Goiás and Mato Grosso (about 60% of all safrinha crop production) as upper-

level high pressure marks a continuation of the dry season. Corn to the south will be

much drier than normal over the next two weeks, though 0.25” to 0.75” has been added

to the southern 15% of the belt next Wed-Thu when a cool front passes. 52%, 39%, 29%

of Brazil safrinha corn had under one-fourth normal rain the last 14, 30 and 60 days.

StatsCan released their March 31st grain/oilseed stocks data this morning, with wheat at

16.2mmt, canola at 6.6mmt, oats at 1.8mmt and barley at 2.8mmt. The average

estimates were 16.7mmt for wheat vs. 18.78mmt last year, canola at 6.7mmt vs.

10.55mmt last year and oats at 1.9mmt vs. 1.85mmt last year. Barley stocks were

estimated at 3.3mmt vs. 3.53mmt last year. Brazilian consultancy Datagro pegged their

corn crop at 105.5mmt vs. 109.3mmt previously, raising their soybean crop estimate to

136.3mmt from 135.5mmt previously (USDA at 109.0mmt and 136.0mmt,

2

respectively). However, many other private estimates for corn are 100mmt or lower.

Argentina’s farmers are expected to harvest 45mmt of soybeans and 50mmt of corn,

according to the Rosario Grains Exchange (USDA 47.5mmt and 47.0mmt,

respectively).

July corn is trading higher early Friday, continuing its push to new highs while the

seven-day forecast remains hot and dry for Brazil's safrinha corn crop, a damaging

prospect at pollination time. Brazil's FOB corn price for August closed at a new high

Thursday. May corn is trading roughly $.40 above the July contract and has had no

deliveries reported yet, signs that commercial demand for corn has eased a little but

remains active. Keep in mind this rally is not being fueled by speculative buying as non-

commercial net longs have been flat in 2021. This is a market where commercial

interests are still having difficulty securing the supplies they need. The Midwest is

covered with cash corn bids of $7 and higher. The 2021 renewable D6 RINs increased

to a new high of $1.70 ½ Thursday as it becomes increasingly difficult for refiners to

meet blending requirements. Meanwhile, corn planting continues in earnest with

moderate to heavy rains expected across the central and Eastern Corn Belt over the

weekend. Technically, the trends in July and December corn remain up with no sign of

turning lower yet.

July soybeans are up early Friday, with the oil side of the crush once again showing

bullish demand. July palm oil is trading over 4% higher at a new contract high, July

canola is at new all-time highs and July soybean oil is trading nearly a full cent higher

early Friday. Even in Brazil where this year's record harvest is still new, the FOB

soybean price for May increased to a new high Thursday. In China, there is no sign of

easing demand with July prices of soybeans and soybean oil near or at new highs early

Friday. Here in the U.S. cash soybean bids are largely $16 and higher in the eastern

Midwest, in the upper-$15s in the West. As with corn, non-commercial net-long

positions have been largely flat since last fall as the supply crunch is for real, although

there have been some deliveries. Late Thursday, the CME said there were 132 new

deliveries of May soybeans, 9 for May meal and 2 for May soybean oil. Soybean

planting is off to a fast start and rain in the forecast for this weekend and in the 8 to 14

day period will be helpful for new crops. Technically, the trends in both May and

November soybeans remain up with no signs of reversal yet.

3A CoBank analyst reiterated what I’ve been saying for some time regarding demand

rationing, or the lack thereof, in the grain/oilseed markets. “What we’ve got going on is

a fairly rare circumstance where pretty much everything in the supply chain is

profitable, so there hasn’t been any reason from a fundamental perspective, at least

domestically, for demand to drop off.” The poultry, cattle and pork industries are all

profitable, with hog prices hitting the highest prices in almost seven years. Beef packers

are cashing in fat profits, with margins near the record levels reached during the

pandemic. Even the beleaguered ethanol market is seeing the highest prices in six years

as the car makes a comeback as the preferred transport in the post-Covid era There are

rumors that China is seeking 1.5-2.5mmt of U.S. corn, which supported prices

yesterday, as did some talk that U.S. weather could turn hotter/drier after two more

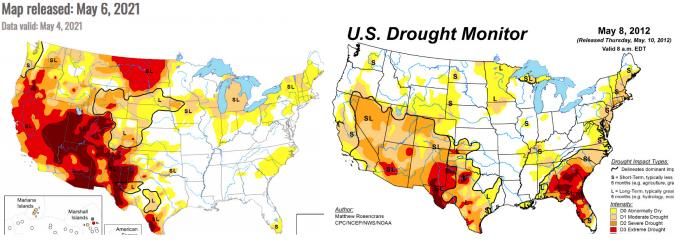

weeks of the cool/wet pattern. The latest U.S. drought monitor map vs. 2012 (see

graphic) shows the Dakotas/western NE/MI/and portions of IL-IN-OH drier than 2012.

RJO’s director of research Rich Feltes shared his thoughts on the upcoming WASDE

report, basically warning of the normal, WASDE bearish bias, but also suggesting post-

report weakness will be bought. My advice is for end users to use the USDA’s bearish

bias to buy call options at strike prices at the current highs should we break on USDA

news.

o Final U.S. corn yield clocked in below USDA’s May forecast in each of the last 2

years (last year by 6.5bpa) and in 5 of the last 11 years. Recall final 2012 U.S. corn

yield was 43bpa below the USDA May forecast. Final corn yield clocked in about 11bpa

below May in both 2010 and 2011. May to Final corn yield from 2014-2018 exceeded

the May forecast by 1-6bpa.

o Final U.S. soy yield clocked in below USDA’s May forecast in only 4 of the last 11

years. Final 2020 U.S. soy yield was 0.4bpa above the May forecast. Final 2019 soy

yield (recall wet/delayed spring) was 2.1bpa below the May forecast vs. a 4.2bpa May

4to final soy yield plunge in the 2012 drought year. May to final soy yields from 2014

thru 2018 exceeded the May forecast by 2.5bpa/2.5bpa/5.5bpa/1bpa/3bpa.

o A likely WASDE 9/22 U.S. corn carryover forecast in the 1.2-1.4 billion bu. area (if

realized) would be the lowest USDA May new crop corn carryover forecast since 2011.

o A likely WASDE 9/22 U.S. soy carryover forecast in the 110-130mb area (if realized)

would be the lowest USDA May new crop soy carryover forecast since 2011’s 145mb

forecast.

o One of the most anticipated WASDE updates on next Wednesday’s crop report will be

WASDE’s take on 2021 Brazil corn production (forecasted at 109mmt on the April crop

report). Suspect the trade is pricing a crop in the 95-100mmt range, although WASDE

may likely wait until June or July crop reports before slashing the crop appreciably.

o Noteworthy that USDA’s initial May forecast of new crop U.S. soybean stocks has

overstated final stocks in 5 of the last 8 years, including a 285mb overstatement of final

9/21 U.S. soy stocks on the 5/20 crop report and a 450mb overstatement of final U.S.

soy stocks on the 5/19 crop report. USDA understatement of final U.S. soy stocks on the

May crop report occurred in only 11 of the last 38 years typically ranged from 50-

150mb.

o Noteworthy that USDA’s initial May forecast of new crop U.S. corn stocks has

overstated final stocks in 5 of the last 11 years, including whopping 1.966 billion bu.

overstatement of final 9/21 U.S. corn stocks on the 5/20 crop report and an over 500mb

overstatement of final 9/20 U.S. corn stocks on the 5/19 crop report.

o Be mentally prepared for WASDE next Wednesday to forecast: Hefty gains in 2022

Brazil corn/soybean production. Hefty gains in 2021 Ukraine corn/wheat production. A

hefty gain in 2021 EU wheat production. Only a nominal gain in 2021/22 Chinese soy

imports and a cautious take on 2021/22 corn imports. A Russian wheat crop smaller

than last year but still large historically. A hefty gain in 2021/22 world wheat feeding

and a conservative gain in world corn feeding. Modest cuts vs. last year in

Canada/Australia wheat crops. As chronicled in bullet points above, final U.S. yields

and stocks have varied widely from USDA’s initial May forecasts. Last point highlights

the reality that world 2021/22 forecasts likely lean negative. Additionally, USDA’s May

forecasts for combined 2021 U.S. corn/soybean acreage will likely fall short of final by

2-3 million acres (with corn likely understated the most). The trade following the crop

report will again focus on U.S. Midwest planting weather, early U.S. crop ratings,

safrinah corn, Chinese buying/execution on old crop corn, northern Plains dryness and

5the degree to which corn end users elect to extend new crop coverage. Given the array

of uncertainties that still lie ahead, suspect any negative initial take on May crop report

will trigger strong support.

One of the first things you learn when becoming a grain merchandizer is that

GENERALLY, basis and futures tend to pull against each other. In other words, when

basis is strong, futures tend to be weak and vice versa. That makes sense as when

futures are strong, board premiums entice grain movement and when futures are weak, a

strong basis entices movement. In rare instances, they will move together, which usually

indicates an abnormality in the market. Such is the case now as the U.S. national

average corn basis on April 30th was $.18 over the July futures, a new high not seen

since the second week in April of the 2012-13 crop year. Since the beginning of the

2020-21 crop year, average corn basis has been above the national average five-year

basis, similar to the way it ended the 2019-20 crop after recovering midsummer from a

first week of May pandemic low of $.32 under the July. Cash prices have been on fire

since mid-January when the National Corn Index reached a seven-year high, as basis

levels stayed firm in spite of rising futures. Demand at that time was picking up on the

West Coast as corn exports for the crop year 2020-21 started to pick up to Mexico,

Japan, Korea and China. The other factor strengthening U.S. corn prices was a slow

planting season for the safrinha corn crop in Brazil and currently dry weather likely

cutting yield potential's there. The majority of Brazil's growing regions now have soil

moisture readings of no more than 50% capacity. The only exception is a strip in far

western Mato Grosso do Sul that saw slightly increased soil moisture from weekend

showers.

Given that the supplies of corn in the U.S are dwindling amid strong export and

domestic demand, the markets are continuing to move to new highs. In the April 9

World Agricultural Supply and Demand Estimates (WASDE) report, USDA estimated

lower ending stocks for U.S. corn in 2020-21 at 1.352 billion bushels, a seven-year low.

Yet, demand has not budged. Besides export demand, domestic demand is driving the

strength in the basis and futures. Ethanol plants have been staging a strong recovery

versus the same time last year when the pandemic slowed or shuttered plants, with more

than one half of the nation's ethanol production capacity idled. As of April 2021, ethanol

production has recovered to approximately 90% of pre-pandemic levels or 950,000 bpd.

That means increased production created the need for cash corn, and as futures corn

prices rose, so did the basis, causing the overall cash price to surge as ethanol plants bid

for old-crop corn in additions to feeders and exporters. Here's a sampling of what the

spot cash corn price has done at various ethanol plants using daily data from the USDA.

In the Eastern Corn Belt, representing plants in Illinois, Indiana, Ohio and Michigan, the

truck cash price for April 30 was $6.78 versus $6.24 one week ago and $2.97 one year

6ago. In Nebraska, the truck cash price for April 30 was $6.67 versus $6.11 one week

ago and $2.79 one year ago. In Iowa, the truck cash price for April 30 was $6.38 versus

$6.02 one week ago and $2.49 one year ago. In South Dakota, the truck cash price for

April 30 was $6.70 versus $6.14 one week ago and $2.60 one year ago. So, the million-

dollar question is: Will we run out of old-crop corn to fill the needs of all interested

parties? At this point, everyone who uses corn is still making money, which means

demand rationing at current prices simply isn’t working…yet.

On the demand front, palm oil prices finished 4.7% higher in Asian trade, tracking

higher soybean oil prices on the Chicago Board of Trade. The soybean oil market's

rally, fueled by tight supply, led crude palm oil futures to hit new record high prices.

Strong April export data provided further support for palm oil prices. On China's Dalian

exchange, September corn was up 1.5%, July soybeans were up 2.1%, September

soybean meal was up 1.4% and September soybean oil was up 1.5%. Due to a massive

surge in Covid-19 cases, Indian edible oil refiners have sharply reduced expected

imports for May and June given social restrictions cause demand at outside eateries to

decline. Current ideas are for May/June imports of 650,000mt, down from previous

ideas of 850,000mt. Under normal conditions, India consumes about 1.9mmt of edible

oil monthly, with palm oil accounting for about 2/3rd of the total. Some 73% of the all-

time record 17.4mmt of soybeans exported from Brazil in April were bound for China,

with the states of Mato Grosso and São Paulo as the main origins, official customs data

showed on Thursday. Cargos heading to China totaled 12.6mmt, the highest volume on

record and 2mmt higher than last year. Other major destinations were the EU, whose

Brazilian bean imports amounted to 1.6mmt in April, as well as Mexico and Turkey,

with just over 400,000mt each. Brazil’s April exports were bolstered by delayed

harvested beans arriving at ports later than previously anticipated and the pushing of

volumes that were expected to have reached the seaborne market earlier in April. With

record shipments registered in April, Brazilian bean exports reached 33mmt year to

date, 1.1mmt higher on the year and also a historical record for the first four months of

the year. Year-to-date volumes bound for China also reached an all-time high at

23.9mmt, 2.9% higher on the year. Brazil’s ag exporter association Anec maintained

their 32.0mmt 2021/22 corn export forecast despite the drought, which would still be

down from last year’s 33.6mmt forecast (35.1mmt according to the Brazilian

government). They see soybean exports at 83.0mmt vs. last year’s official 81.6mmt

estimate and just short of the 2018/19 record of 83.7mmt. Argentine farmer soybean

sales remain tepid at 16.4mmt vs. 20.8mmt at this time last year, according to their ag

ministry. Farmer sales of corn are at 24.5mm vs. 23.65mmt at this time last year. South

Korea tendered for 276,000mt of corn for Jul-Aug shipment.

7Hogs: Cash hogs are called steady to somewhat lower. As packers look to the weekend,

they may back off on their cash hog buying sprees and let the weekend pass before

jumping wildly into the market again. USDA’s National Average Afternoon Base Hog

price was $.51 weaker to $116.42. The May 4th CME Lean Hog Index was $107.89, up

by another $.52. The weekly USDA Export Sales report showed 48,240 MT of pork

sales during the week ending 4/29. That was up 35% on week and the fourth largest

weekly sale of the year. China imported 922,000mt of all meat in April 2021, up 6.9%

from the same month in 2020 according to Chinese customs data. Pork cutout futures

closed mixed as June dropped back a nickel but the other nearbys were as much as $.22

stronger. USDA’s National Pork Carcass Cutout Value was $1.95 stronger on Thursday

to $113.86 on slow movement of 216 loads. The primal cuts were mostly higher, though

picnics pulled back by $2.50. Estimated packer margins were $-26.23/head for non-

integrators and $99.92/head for integrators vs. $-29.07 and $95.58 the previous day.

Weekly kill is down 0.1% vs. last week, but up 56.9% vs. last year’s plant shutdowns.

Hog futures struggled for a while Thursday, but like a child outside a candy store,

traders eventually had to come in and buy as lower futures were too enticing. Only the

October contract closed slightly lower, which sets the stage for higher futures Friday.

Saturday slaughter is estimated at 15,000 head. I didn't think the lean hog contracts

would close higher Thursday afternoon as the market has had a full speed ahead attitude

this week, so it seemed logical that traders may want to let the market trade steady

before taking prices any higher. However, the lean hog market decided to do what it has

recently become quite accustomed to and that's trading higher. June lean hogs closed

$0.05 higher at $114.47, July lean hogs closed $0.17 higher at $114.65 and August lean

hogs closed $0.12 higher at $109.92. Thursday's pork cutout value closed higher with

nearly every cut seeing $2.00 advancements, other than the picnic ham, which closed

$2.50 lower and the rib, which only saw an advancement of $0.58 Thursday afternoon.

Pork net sales of 48,200mt reported for 2021 were up 36% from the previous week and

up noticeably from the prior four-week average. The three primary buyers were Mexico

(19,400mt), China (15,000mt) and Japan (4,700mt). Thursday's actual slaughter data

shared that for the week ending May 24, live carcass weights fell by 1 pound to average

290 pounds and dressed carcass weights remained steady at 217 pounds.

It stands to reason live cattle futures would have closed higher Thursday due to ever

increasing boxed beef prices. However, the disconnect between cash and boxed beef is

large with packer profits around $719 per head. Yet, they have been able to procure

cattle this week at mostly steady prices averaging $119.12. Consumers want beef and

packers need to keep the market supplied. However, high prices may be having an

impact on the export market. Technically, live cattle futures are attempting to build a

level of support with futures moving in a fairly sideways pattern over the past two

8weeks. The live cattle contracts managed to close fully higher and Thursday's boxed

beef prices continued to soar, but the cash cattle market neglected to see any more bids

renewed, and even more depressing, Thursday's slaughter is only estimated at a sorry

115,000 head. Boxed beef prices continue to scale higher and higher as consumers are

faced with short supplies amid the nation's prime grilling season, all while feedlots have

cattle to sell and packers could run faster chain speeds, but instead feedlots are left

without bids and consumers are faced with higher beef prices once again. June live

cattle closed $1.05 higher at $115.47, August live cattle closed $0.75 higher at $118.47

and October live cattle closed $0.37 higher at $123.47. Thursday's slaughter is estimated

at 115,000 head, 4,000 head less than a week ago. Beef net sales of 16,900mt reported

for 2021 were down 28% from the previous week and 18% from the prior four-week

average. Thursday's actual slaughter data share that for the week ending April 24, both

steer and heifer carcass weights saw decreases. Steers averaged 896 pounds (down 2

pounds from the previous week) and heifers averaged 825 pounds (down 12 pounds

from the previous week). Boxed beef prices closed at year another new high for the

move, with choice up $1.59 ($306.37) and select up $3.18 ($289.36) with a movement

of 100 loads. We are now over $40 higher than the all-time high (with the exception of

last year’s brief spike due to plant closures). Cash is called steady. It's most likely that

Friday won't see much for cash cattle trade as it's looking like the week's business is

essentially done. The $0.06 to $0.10 rally in the nearby corn contracts didn't allow for a

kind closes in the feeder cattle contracts Thursday afternoon. May feeders closed $1.00

lower at $130.47, August feeders closed $1.82 lower at $143.40 and September feeders

closed $1.92 lower at $145.55.

Hog supplies coming to market in the last few weeks are a bit higher than one would

have expected based on the USDA survey. We think slaughter this week may be around

2.4 million head. Using that number, hog slaughter in the last four weeks has averaged

3.8% higher than the comparable four week period in 2019 (we leave 2020 comparisons

out due to COVID skewing the data). Looking at the inventory survey from March, the

supply of hogs in the 120-179 pound category was 2% lower than in 2019. Is the survey

really that far off? Maybe and maybe not. Probably a better way to look at things is to

compare the inventory of the two market hog categories: +180lb. and 120-179. The

March survey had the number of hogs in these two groups at 28.151 million, +1.4% vs.

2019. Weekly hog slaughter since the first week of March has been a total of 24.910

million, 2.5% higher than last year. So while the supply is a bit higher, it is not that far

off. One could argue that strong pork demand is causing packers to pull some supply

forward in order to fill orders from retail and food service customers. While this may

have caused some margin erosion, in the short term the packer is looking to keep

customers happy. One indication that we may be seeing some hogs being pulled forward

is the decline in hog carcass weights. Carcass weight of producer owned hogs are down

92 pounds or 0.9% in the last month and they are also 1.5 pounds lower than the same

period in 2019.

I’ve spoken extensively about record beef/pork prices (discounting last year’s plant

closures, when prices briefly spiked), but chicken demand is also huge. After a year

promoting takeout wings and crispy chicken sandwiches, restaurants including KFC,

Wingstop Inc. and Buffalo Wild Wings Inc. say they are paying steep prices for scarce

poultry. Some are running out of or limiting sales of tenders, filets and wings, cutting

into some of their most reliable sales. Independent eateries and bars have gone weeks

without wings, owners say. Chicken breast prices have more than doubled since the

beginning of the year, and wing prices have hit records, according to market-research

firm Urner Barry. "The overall supply is constrained. That affects every part of the bird,

" Wingstop Chief Executive Charlie Morrison said in an interview earlier this week.

Wingstop said it is paying 26% more for bone-in chicken wings this year. Mr. Morrison

said the company is speaking daily to chicken suppliers that are struggling to raise

production because they are having trouble getting enough workers. Similar constraints

are weighing on other companies across different industries and around the country.

At the start of 2021, chicken looked like a bargain for U.S. restaurants. Closures and

dining room restrictions had contributed to swollen stockpiles of chicken in cold-storage

facilities. Boneless skinless chicken breast, the poultry industry's flagship product, last

year averaged around $1 a pound, according to Urner Barry. Now boneless chicken

breast is trading at $2.04 a pound, the firm said. Over the past decade, the price

averaged about $1.32 a pound. One reason for the higher prices is the chicken sandwich

wars of recent years. Fast-food chains including McDonald's Corp., Popeyes Louisiana

Kitchen Inc. and Wendy's Co. have introduced new crispy and spicy offerings. More

chains plan to introduce new chicken sandwiches in the coming months, including a

hand-breaded version that Burger King plans to sell nationally by this summer. Chris

Testa, president of United Natural Foods Inc., said this week the supermarket distributor

is seeing chicken prices increase partly because of higher demand from restaurants.

Consumers paid about $3.29 a pound for boneless chicken breasts in March, up 3 cents

since January and 11% higher than a year earlier, according to the U.S. Bureau of Labor

Statistics. KFC, owned by Yum Brands Inc., developed a sandwich earlier this year that

is selling more than twice as quickly in the U.S. as an older version, the company said.

"Our main challenge has been keeping up with that demand," Yum CEO David Gibbs

said last week.

KFC late last month told U.S. restaurant owners to remove chicken tenders and

Nashville Hot chicken items from online menus because of tight supplies, according to a

company message. KFC's suppliers aren't always delivering full orders of chicken, and

10restaurants are also limiting sales of the new KFC Chicken Sandwich, according to

people familiar with the matter. The company asked owners to remove in-store

promotions for the chain's $30 fill-up bucket, a multipiece chicken deal that generated a

surge in sales during the pandemic, the people said. "We look forward to getting back to

business as usual, once we get past this period of industry supply constraints," a KFC

spokeswoman said. Chicken-wing prices have gotten a pandemic boost, too. Prices for

jumbo wings have risen to a record $2.92 a pound, Urner Barry said. Chili's owner

Brinker International Inc., Applebee's and other sit-down chains introduced online-only

wing brands during the pandemic, in part because they are easier to package and deliver

than other entrées. Fast-food restaurants' servings of wings grew 33% in the 12 months

ended in March compared with the same year-earlier period, according to market-

research firm NPD Group Inc.

For chicken producers, restaurants' growing poultry appetite is driving a windfall and

helping offset surging grain prices, which inflates companies' cost to raise chickens.

Pilgrim's Pride Corp., the second-largest U.S. chicken company by sales, last week

reported $100 million in quarterly profit, a nearly 50% increase on year and surpassing

expectations. Analysts surveyed by FactSet also anticipate strong profits for Tyson

Foods Inc. and Sanderson Farms Inc. when they report quarterly results over the next

several weeks. "Demand for wings is more than we can currently fill," said Mike

Cockrell, chief financial officer for Sanderson, which supplies chicken to chains,

including Buffalo Wild Wings and TGI Fridays, and food service distributor Sysco

Corp. Chicken producers had about 4% more broiler chicken eggs in incubation

facilities on April 1 versus a year earlier, according to U.S. Department of Agriculture

data, though total chicks hatched over the first three months of the year trailed 2020's

first-quarter total. Commercial chicken breeds are raised for about seven weeks before

they are slaughtered. Pilgrim's CEO Fabio Sandri said last week staffing shortages have

affected which products Pilgrim's plants can produce. Pilgrim's expects chicken's strong

run to continue, he said. "Grilling season is just around the corner, when chicken

demand is seasonally the strongest historically."

Weather: There is a trough in the East with a ridge over the Rockies and another trough

moving into the West. The eastern trough will be slow to move through the East this

weekend though a portion of it will remain behind. The western trough may sit in the

West for a few days before moving eastward next week and be replaced by a ridge.

Another trough may move into the Northwest late next week while the ridge slides into

the middle of the country. The U.S. and European models are fairly similar in the upper

levels but have differences in how widespread rainfall will be next week. The European

model is favored, which for now is a drier solution overall. For the outlook period,

temperatures on Wednesday will be below normal east of the Rockies and above normal

11in the West. Temperatures are likely to remain in this pattern through the end of the

week but rise in the Central and East next weekend. A system will ride along a frontal

boundary across the south in the middle-to-end of next week. Another system will move

into the Northwest late next week and into the Plains over the weekend.

North American Weather Highlights: Drought continues in the northern Plains.

Temperatures have fallen below freezing a couple of days this week and may do so this

weekend into next week as well, which could damage any emerged corn or wheat.

Moderate showers are expected through Sunday for a good portion of the region, being

very beneficial for soil moisture where it occurs. Northeast North Dakota is not likely to

receive much precipitation, however. Soil moisture has improved for much of the

central/southern Plains region over the last week. A couple of systems will bring good

chances for periods of widespread moderate showers through next week. All shower

activity will benefit developing to reproductive wheat and emerging corn and soybeans.

Temperatures will be below normal for the next week, limiting overall growth.

Scattered showers have fallen across the Midwest over the last several days, increasing

soil moisture for much of the region. The northwest could use more showers, though. A

system will bring more rainfall over the weekend, mostly across the south, while the

north stays drier for the next week. Some chilly temperatures, including frost potential,

is possible across the north and east through much of next week, which may be

damaging to emerging crops. This is not a high likelihood nor is it widespread, however.

Moderate showers have moved through the Delta recently, benefiting emerged crops.

The rain has delayed planting activities. More moderate showers are expected this

weekend and next week to benefit germination and early growth. Recent showers in the

Southeast will benefit emerging cotton but have caused planting delays. More moderate

to heavy showers are expected next week to benefit germination and early growth.

Temperatures below normal and dry conditions in the Canadian Prairies normally slow

planting but reports from Saskatchewan and Manitoba note increased activity. Showers

have been and will continue to be more consistent across the southwest through the

weekend, benefiting soil moisture there. Eastern and northern areas will continue to be

on the cool and dry side for the next week. More widespread showers may wait until

next weekend.

Global Weather Highlights: Heat and dryness in Brazil have been the theme over the

last couple of weeks, forcing developing to reproductive corn to deplete subsoil

moisture across the region. A front moving northward through southern Brazil has

brought moderate showers to Rio Grande do Sul for developing winter wheat but did

not bring much shower activity north into Parana or Mato Grosso do Sul for corn.

Overall heat and dryness continue for another week, causing stress and damage to corn.

Recent showers in Argentina have disrupted the corn and soybean harvest somewhat,

12but primed soils for winter wheat planting, which picks up in the next couple of weeks.

Another system is set to bring more widespread showers Sunday into next week.

Periods of showers will continue to delay harvest. Recent cold temperatures in Europe

across the north and east have been concerning for winter grains over the last couple of

weeks, but estimates are for mostly minor damage. More widespread showers this week

will help increase soil moisture but delay spring planting. The cooler temperatures will

rise this weekend into next week. Favorable conditions are found across the south for

reproductive to filling winter grains. Scattered showers continue to maintain overall

above-normal soil moisture in the Black Sea. Warmer temperatures have also moved in,

promoting growth. A couple of systems will bring more showers to the area, but with

falling temperatures, causing mixed conditions for wheat. The showers could cause

more delays for corn planting. Recent showers in Australia this week will benefit early

growth for winter crops but has caused some planting delays for wheat and canola and

harvest delays for cotton and sorghum. Dryness over the next week should be beneficial

overall. Conditions have been mostly favorable across China so far this spring, though it

has been overly wet across the south for rice and sugarcane and cool across the

northeast for corn and soybean planting. Systems will continue to move through the

region over the next week with shots of precipitation and roller-coaster temperatures,

though the northeast is likely to remain mostly below normal. This may continue to

have a delaying impact on corn and soybean planting. Periods of showers that have

continued this spring have kept conditions favorable for much of the winter crops in

northwestern India as they move through reproduction and fill. Scattered showers have

started to develop occasionally over the interior of India well in advance of summer

planting season for cotton and soybeans, which starts with the monsoon in June.

Macros: The macro markets were mixed as of 8:30am EDT, with Dow futures steady,

the U.S. dollar index is down 0.6%, crude oil is down 0.4% and gold is steady. The S&P

500 on Thursday closed 0.82% higher. The DJIA gained 0.93%, while the Nasdaq 100

gained 0.82%. Bullish factors included the decline in U.S. weekly initial unemployment

by 92,000 to a 13 ½ month low of 498,000, showing a stronger labor market than

expectations of 538,000, and an easing of the pandemic in the U.S. after new U.S. Covid

infections fell to 46,853 on Wednesday, a 6 ¾ month low. I try to stay away from Covid

politics, but I simply cannot help myself when I saw the following headline. A

University of Chicago study shows that stay at home orders did not lower

infections/deaths but rather boosted both. What’s sad is that many pre-pandemic

contingency planning predicted as much. Back to the news. The Fed provided a clear

warning about stock prices and frothy risk areas such as SPACs, meme stocks, and

cryptocurrencies in its semi-annual financial stability report released after the stock

market closed Thursday afternoon. Fed Governor Lael Brainard, in a statement released

with the report, said, "Vulnerabilities associated with elevated risk appetite are rising.

13The combination of stretched valuations with very high levels of corporate indebtedness

bear watching because of the potential to amplify the effects of a re-pricing event." A

"re-pricing event" in non-Fed language is otherwise known as a stock market crash. The

Fed report said that valuations for some assets are "elevated relative to historical norms

even when using measures that account for Treasury yields. In this setting, asset prices

may be vulnerable to significant declines should risk appetite fall." Fed Chair Powell

said himself at his April FOMC post-meeting press conference that some parts of the

markets "are a bit frothy, and that's a fact." Dallas Fed President Kaplan on April 30

said, "We're now at the point where I'm observing excesses and imbalances in financial

markets. I'm very attentive to that, and that's why I do think at the earliest opportunity I

think it will be appropriate for us to start talking about adjusting those purchases." Mr.

Kaplan yesterday repeated his call for discussions on QE tapering, saying that he would

like those discussions to begin "sooner rather than later." He said the economy would be

"much healthier" if the Fed were to start "weaning off these purchases."

A recent survey by Bloomberg found that 14% of the analysts surveyed expect the Fed

to start tapering its QE program in Q3, and 45% of the analysts expect tapering to begin

in Q4. Opportunities for the Fed to announce the tapering could come as soon as the

July or September FOMC meetings or at the Fed's late-August Jackson Hole conference.

The consensus is for the tapering to last 7-12 months. However, the market is still not

expecting the Fed to start raising rates until early 2023. The Bloomberg survey found a

consensus for two 25 bp rate hikes in 2023 that would bring the funds rate target up to

0.50%/0.75% from the current level of 0%-0.25%. The stock market is clearly on watch

for any events that could spark a sharp sell-off since there have recently been some

unexplained stock market drops. The majority of Fed officials have been dovish and

have been trying to reassure the markets that a rate hike is a long way off. However, if

inflation should start to show a sharp and persistent rise, then the Fed would have no

choice but to start QE tapering and lean towards a rate hike. That could easily spark a

sharp sell-off in stocks as the punch bowl is taken away sooner than expected.

Global shares mostly rose Friday, tracking a rally on Wall Street as investors awaited

the release of jobs data. France's CAC 40 slipped nearly 0.1% in early trading to

6,352.44 while Germany's DAX added 0.7% to 15,303.46. Britain's FTSE 100 added

0.4% to 7,107.22. U.S. futures were steady with the contract for the Dow industrials

rising less than 0.1% to 34,463.50. The S&P 500 future rose less than 0.1% to 4,197.88.

China reported its trade with the United States and the rest of the world surged by

double digits in April as consumer demand recovered, but growth appeared to be

slowing. Trade data released Friday show global exports rose 32.3% over a year ago to

$263.9 billion, in line with March but down from the explosive 60.6% rise in the first

two months of 2021. China's trade gains look especially dramatic in comparison with a

14year ago, when global economies shut down to fight the coronavirus. The positive

indicators are coming amid worries about renewed tensions between the U.S. and China

over trade. Japan's benchmark Nikkei 225 recouped early losses to edge up nearly 0.1%

and finish at 29,357.82. Australia's S&P/ASX 200 added 0.3% to 7,080.80, while South

Korea's Kospi gained 0.6% to 3,197.20. Hong Kong's Hang Seng gyrated much of the

day ending nearly 0.1% lower at 28,610.65, while the Shanghai Composite dropped

0.7% to 3,418.87. Japan has decided to extend its state of emergency to curb the spread

of COVID-19 infections, which kicked in last month in some urban areas, with people

asked to stay home and restaurants to close early. The emergency will continue through

the end of the month, instead of ending May 11, officials said.

Stocks have mostly pushed higher on expectations of an economic recovery and strong

profits this year. Massive support from the U.S. government and the Federal Reserve,

and increasingly positive economic data, have also encouraged investors to push stock

prices to all-time highs. Jobs growth is key to a sustained economic rebound, but it has

lagged other areas of the economy such as retail sales and consumer confidence.

Economists expect the April jobs data to show employers hired 975,000 workers last

month as the economy accelerated out of the pandemic and vaccines rolled out

nationwide. The unemployment rate is expected to drop to 5.8% from 6%. In energy

trading, benchmark U.S. crude fell 4 cents to $64.67 a barrel in electronic trading on the

New York Mercantile Exchange. Brent crude, the international standard, lost 1 cent to

$68.08 a barrel. In currency trading, the U.S. dollar inched down to $109.15 Japanese

yen from $109.19 yen. The euro cost $1.2081, up from $1.2062.

Summary: July corn closed up $.10 ¼ at a new contract high of $7.18 ¾ Thursday,

persistently pushing higher with support from a seven-day forecast for central Brazil

that remains hot and dry. For months, many voiced concerns about the consequences of

Brazil's late soybean harvest and now those concerns have proven correct. Brazil's

safrinha corn crop is pollinating in hot and dry weather and crop estimates are falling

from USDA's 4.3 billion bushels (bb) to some less than 4.0 bb. USDA offers its next

update on Wednesday, May 12. Confirming the situation, Brazil's FOB corn price for

August was up 2% to a new high of $293.25/mt ($7.44/bu.) Thursday. U.S. December

corn closed up $.20 ¾ at a new high of $6.25 ½. The Buenos Aires Grain Exchange said

22% of Argentina's corn was harvested, down from the five-year average of 32%. Here

in the U.S., corn planting has been active for well over a week and Monday afternoon's

Crop Progress report is apt to show another big jump. Activity will slow in the southern

and southeastern Corn Belt when moderate to heavy rains arrive this weekend. A broad

coverage of light rains over the Corn Belt will be largely beneficial to crops in the 8- to

14-day forecast. Thursday's U.S. Drought Monitor showed a mix of minor changes.

Drier areas around Iowa and northern Illinois were offset by moisture improvement in

15parts of the Eastern Corn Belt. There are several reasons for USDA's estimate of U.S.

corn ending stocks to come down in Wednesday's WASDE report and export sales are

one of those. From a technical view, the trends remain actively up for both, July and

December corn.

July soybeans closed up $.27 ¼ at $15.69 ½ Thursday, supported by another bullish

performance from the oil side of the crush. July Malaysian palm oil set the tone earlier

Thursday, gaining 4.2% and posting a new contract high. July canola is the bullish star

of the moment, benefitting from a dry seven-day forecast for the northwestern U.S.

Plains and western Canadian Prairies. July canola is trading up 3.2% at a new all-time

high. July soybean oil followed with a new high close of 64.35 cents, a gain of 0.89 cent

on the day. Oil still represents the minority share, accounting for 46% of the soybean

crush, but has been an important part of increasing the return for crushing soybeans and

keeping demand active, even during this time of tight U.S. supplies. Export demand has

shifted to Brazil, but the U.S. is still getting some business. USDA said 6.1mb of

soybeans were sold for export last week with unknown and Japan listed as top buyers.

Unknown was also the top buyer of 7.1mb of new-crop soybeans sold. Last week's

soybean shipments totaled 9.7mb with no mention of imports in USDA's report. In

China, demand for soybeans remains strong with the July contract on the Dalian

exchange closing up 2.5% at the equivalent of $18.18 a bushel. July soybean oil on the

Dalian posted a new closing high. Late Thursday, the Buenos Aires Grain Exchange

said 53% of Argentina's soybeans were harvested, down from the five-year average of

66%. The exchange's crop estimate remains at 43.0mmt, down from USDA's estimate of

47.5mmt. From a technical view, the trends for July and November soybeans remain up

with no signs of breaking lower yet.

July KC wheat closed up $.09 ¾ at a new closing high of $7.26 ¾ after a quiet start

Thursday morning. U.S. wheat prices continue to benefit from corn's bullish influence,

but also have their own weather concerns early in 2021. Thursday's weather map

showed light showers around the Great Lakes, but was mostly dry over the rest of the

U.S. There is a chance the HRW wheat crop could benefit from moderate rain amounts,

starting this weekend, but it is not clear yet how much of the crop will participate. A

larger forecast area of light rain amounts is expected to be somewhat helpful in the 8- to

14-day forecast. Mostly minor changes were seen in Thursday's U.S. Drought Monitor.

For winter wheat, it is interesting to note drought levels increasing in the Pacific

Northwest and not much rain in the seven-day forecast. Spring wheat areas are also

expected to stay mostly dry the next seven days in both the U.S. and Canada. A few

exceptions include parts of Montana and Alberta. On the demand side, it doesn't look

like U.S. wheat exports will reach USDA's 985mb goal by the end of May. USDA

reported net cancellations of 3.5mb of previous sales for last week. The cancellations

16could have shifted to new-crop sales as 2021-22 sales totaled 14.7mb. Shipments totaled

21.5mb last week, leaving 159mb to export to reach USDA's export goal by the end of

May. Outside of North America, crop conditions are mostly favorable in major wheat

regions, a bearish contrast to North American weather concerns. Technically, the trends

remain up for July contracts of winter wheat and for September Minneapolis wheat.

A/C Trading Co. does not accept orders to buy or sell by e-mail, text or any other form of social media. This material has been

prepared by a sales or trading employee or agent of A/C Trading Co. and is, or is in the nature of, a solicitation. By accepting this

communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and

agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME

JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION

INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO

THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE

PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS

COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is

substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or

indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from

trades and statistical services and other sources that A/C Trading Co. believes are reliable. We do not guarantee that such information is

accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is

subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

17You can also read