Challenges and Opportunities for Conservation, Agricultural Production, and Social Inclusion in the Cerrado Biome

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Challenges and Opportunities for Conservation, Agricultural

Production, and Social Inclusion in the Cerrado Biome

Technical Annex: The Agriculture Sector, Agriculture Supply

Chains, and Transportation Infrastructure

August 2016

This technical annex accompanies the “Challenges and Opportunities for Conservation, Agricultural Production, and Social

Inclusion in the Cerrado Biome” report, developed for the Climate and Land Use Alliance by CEA Consulting.

The full report and associated materials can be found at: www.climateandlandusealliance.org/reports/cerrado/

v

Table of Contents

Introduction 3

Overview of agriculture in Brazil 6

Overview of agriculture in the Cerrado 12

Agriculture in Matopiba 16

Soy and the soy supply chain 27

The beef and milk supply chain 40

Pasture intensification 55

Agricultural certifications 61

Transportation infrastructure 65

2

AGRICULTURE

This section was produced in partnership with AgroIcone

3

Agriculture in the Cerrado

Historical background and overview

• Beginning in the mid 1970s, agricultural production in the Cerrado expanded greatly – through

a large scale national investment in agricultural research and development. Today, it is one of

the most intensive and productive agricultural regions in the world.

• In the twenty years between 1991 and 2011, the value of Brazil’s agricultural exports increased

ten-fold, from USD 7.9 billion to USD 81 billion.1 The Cerrado has been at the heart of this

growth. Today, the biome accounts for about 40 percent of the total GDP from Brazil’s

agricultural sector.2

Notes on this section:

• Much of the agricultural data is provided by state rather than biome, so much of the information presented here is not perfectly aligned to

the biome.

• Comprehensive information on the agricultural sector is limited by the fact that the latest Agricultural Census was published in 2006 and

there are no current plans for another census. As a result, a number of the charts in this chapter only provide data through 2006.

Sources: (1) FAOSTAT, 2015. (2) MMA, 2014.

4

Agriculture in the Cerrado

Soy

• Soy production has grown at a rapid clip in the past few decades. Planted area has tripled

since the mid 1990s and export value has quadrupled since 2006. Soy accounts for almost

40% of Brazil’s agricultural exports, by value.1

• Of the Cerrado states, Mato Grosso has by far the most land area planted with soy, but

Matopiba is growing in importance for soy production.2

Beef

• Brazil has the largest commercial cattle herd in the world and is the #2 producer and

exporter of beef globally. However, the majority of Brazil’s beef is consumed domestically. 3

• The processing segments of the supply chain is highly concentrated for both soy and beef.

• The beef sector is not growing as quickly as the soy sector. Slower growth and a trend

towards intensification could free up land for crop expansion onto former pasture lands.

Sources: Photos by CEA, from western Bahia. (1) MDIC, AgroIcone. (2) IBGE - Produção Agrícola Municipal, via AgroIcone. (3) USDA, 2015.

5

AGRICULTURE

OVERVIEW OF AGRICULTURE IN BRAZIL

6

Brazil is a top global producer and exporter of agricultural

commodities

Brazil’s agriculture, world share 2014/2015, %1

0% 20% 40% 60% 80% 100%

1

Orange juice

1 • Brazil is important to world food

production.

1

Sugar • Brazil leads world production

1

and export of orange juice,

2 sugar, and coffee.

Soybeans

2 • It is second for production and

4 export of soybeans, producing

Chickens

1 30% of the world’s soybeans

1 and accounting for almost 40%

Coffee Indicates

1 x of global soybean exports.

world rank

2 • Brazil is the world’s second top

Beef exporter of beef.

2

3

Corn Production

2

5 Exports

Cotton

3

4

Pork

4

Source: Data from USDA.

7

Agriculture exports account for over 40% of Brazil’s total exports by

value

Brazil’s trade balance

300

5 year increments 1-year increments

• Brazil has exported

250

about $100 billion

USD worth of

agricultural

200 commodities, on

an annual basis,

over the past few

US$ billion

150 years, and

imported about

$30 billion.

100 • Brazil’s total

exports are worth

about $230 billion

50 USD.

• The agriculture

sector is important

0 for maintaining

1990

1995

2000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Brazil’s trade

balance.

Brazil Exp Total Brazil Imp Total Agribusiness Exp Agribusiness Imp

Source: Ministério da Agricultura. Chart and text adapted from AgroIcone. 8

Agriculture is an important, but not leading, sector for foreign

investment

Foreign investment in Brazil

$12 Metallic mineral

extraction

$10 Oil extraction and

Brazil’s agriculture

related services sector averaged USD

$350 million in foreign

$8 Agriculture, livestock and investment per year

services related to these from 2007 to 2009,

activities

hitting almost USD

US $ Billion

Activities of suport the $500 million in 2008.

$6

mineral extracion

However, it lags far

behind mineral and oil

Silviculture, Forest

$4 exploitation extraction.

Non-metallic mineral

$2 extraction

Fishing and acquaculture

$0

Coal extraction

Source: Bacen, http://www.bcb.gov.br/rex/ied/port/ingressos/htms/index1.asp?idpai=INVEDIR, via AgroIcone.

9

Soy and beef are the commodities most linked to deforestation,

especially in Matopiba

Soy export value - all of Brazil

35

30 Soy

• Soy production has grown

US $ Billions

25

at a rapid clip in the last

20

Soybean oil few decades. Planted

15 Soybean meal area has tripled since the

10 Soybean mid-1990s. Soy accounts

5 for almost 40% of Brazil’s

agricultural exports, by

0

value.

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Beef export value - all of Brazil

8

7

6 Beef

Salted meat

US $ Billions

5

Casings

• Brazil has the largest

4 commercial cattle herd in

Offals

3 the world and is the #2

Processed meat

2

producer and exporter of

Fresh beef beef globally.

1

0

2006

1997

1998

1999

2000

2001

2002

2003

2004

2005

2007

2008

2009

2010

2011

2012

2013

2014

Source: MDIC, via AgroIcone. 10Pesticides, nutrient pollution, soil erosion, and genetic engineering are

significant concerns for Brazilian agriculture

• Pesticides are a major concern in the Cerrado because of the human and ecosystem health impact.

Brazil is now the world’s largest buyer of pesticides, and some pesticides that are outlawed in the

United States and/or Europe are still allowed in the Cerrado, with pesticide companies and users

arguing that the needs in the Cerrado’s tropical climate differ from those of more temperate regions.

However, cases such as an accidental crop-dusting of a school which sent 30 children and teachers to

the hospital have fueled a strong anti-pesticide movement.1

• Nutrient pollution from excess nitrogen and phosphorous from crop agriculture, is a growing concern

in the Cerrado. These nutrients can pollute surface and groundwater (aquifers) and causing algae

blooms that strangle aquatic ecosystems. Left unchecked, nitrogen pollution of drinking water sources

can lead to major health effects such as “blue baby syndrome.”2

• Soil erosion impacts the long-term productivity of crops and pastures. Unchecked overgrazing in

particular can cause erosion, compaction, and destruction, especially in sensitive riparian areas. Soil

erosion also leads to significant carbon loss in the Cerrado.

• Genetic engineering is a concern for many Brazilians because of its possible effects on human health

and its potential to contaminate non-GMO crops. 60% of cotton, 54% of corn, and 91.8% of soy grown

in Brazil are now genetically engineered.3,4

Sources: (1) Prade 2015. (2) Neto et al. 2011. (3) Thuswol 2013. (4) Reuters Brasil 2014. 11AGRICULTURE

OVERVIEW OF AGRICULTURE IN THE CERRADO

12Cropland and pastureland currently account for almost half of the land cover in the Cerrado • The southern Cerrado states of Mato Grosso do Sul, Sao Paulo, and Goiás are dominated by pasture and croplands. • Minas Gerais and Mato Grosso are also used extensively for pasture and cropland. • The northern part of the biome is still largely covered with natural vegetation. Source: CEA and Greeninfo Network, using data from LAPIG Maps. 13

Agricultural production in the Cerrado states nearly doubled between

2005 and 2010

Total agricultural production in Cerrado states

900

800

Millions of tonnes

700

600

• Major increases in crop

500

production occurred in the

400 Cerrado states between 2005

300 and 2010.

200 • Soy is one of the main

100 growth crops in the Cerrado,

- and its planted area has

1990 1995 2000 2005 2010 2011 2012 2013

more than tripled since 1990.

• The southern Cerrado’s

Planted soy area by states - Cerrado planted soy area is far larger

than Matopiba’s, but both

20 São Paulo

18 are growing.

Minas Gerais

16 • Matopiba accounts for about

Mato Grosso do Sul

Millions of hectares

14 16% of planted soy area in

12 Goiás

the Cerrado.

10 Mato Grosso

8

Tocantins

6

4 Maranhão

2 Piauí

0 Bahia

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Source: Pesquisa Agrícola Municipal, via AgroIcone, April 2015. 14For sugarcane and soy, planted area (rather than productivity gains)

has driven yield growth in recent years

Soybean productivity in Cerrado and planted area Corn productivity in Cerrado and planted area

5 20 6 12

Planted area - million hectares

Planted area - million hectares

Productivity - thousand kg/ha

Yield: 108% Yield: 16% 18

Productivity - thousand kg/ha

5 Yield: 72% Yield: 39% 10

4 Area: 3% Area: 78% 16

14

Area: 3% Area: 28%

4 8

3 12

10 3 6

2 8

2 4

6

1 4 1 2

2

0 0 0 0

2003

2010

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2004

2005

2006

2007

2008

2009

2011

2012

2013

1999

2010

1990

1991

1992

1993

1994

1995

1996

1997

1998

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2011

2012

2013

Soybean planted area Soybean productivity Corn planted area Corn productivity

Sugarcane productivity in Cerrado and planted area

100 9

Yield: -2% Yield: 14% • Soybeans have the greatest planted area

Planted area - million hectares

90

Productivity - thousand kg/ha

8

80 Area: 31% Area: 113% in Brazil among the agricultural crops.

7

70 6 • Planted area for both soy and sugarcane

60 has more than doubled since 2000, while

5

50

4 yield has remained relatively constant.

40

30 3 • Corn yield have managed to grow

20 2 considerably since 2000.

10 1

0 0

2002

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Sugarcane planted area Sugarcane productivity

Data from Pesquisa Agrícola Municipal; charts adapted from AgroIcone. 15AGRICULTURE

AGRICULTURE IN MATOPIBA

16Farm size in the Cerrado

• Farms in Matopiba tend to be small, with the exception of Tocantins.

• Matopiba has about 50% more family farms than the southern Cerrado.

Average farm size of Cerrado states – 2006

500

450

Hectares

400

Matopiba

350

300

250

200

150

100

50

0

Mato Grosso Mato Grosso Goiás São Paulo Minas Gerais Tocantins Maranhão Bahia Piauí

do Sul

17Matopiba is dominated by small family farms while larger agribusiness

farms characterize the southern Cerrado

Number of farms (units)

Matopiba Southern Cerrado

1.2 1.2 • The total farm area

1.0 1.0 in Matopiba states is

Mato Grosso

0.8 0.8 do Sul 66.5 Mha. About

Tocantins Mato Grosso 30% (21 Mha) of this

Millions

Millions

0.6 0.6

Piauí Goiás area is in family

0.4 Maranhão 0.4 farms and about

São Paulo

0.2 Bahia 0.2 70% (45.5 Mha) is in

Minas Gerais non-family farms.

0.0 0.0

Family Not family Family Not family • Family farms

farming farming farming farming

account for about

85% of farm units in

Area (hectares) Matopiba.

• While non-family

Matopiba 140

Southern Cerrado farms cover twice

140

120 120 the area of family

São Paulo

100 100 farms in Matopiba,

Millions

80

Piauí

80 Minas Gerais non-family farms

Millions

60 Tocantins 60 cover almost seven

Mato Grosso do

40 Maranhão 40 Sul

times the area of

20 Bahia 20 Mato Grosso family farms in the

- -

rest of the Cerrado.

Family Not family Family Not family

farming farming farming farming

Source: IBGE - Censo Agropecuário. http://www.sidra.ibge.gov.br/bda/tabela/listabl.asp?c=1109&z=p&o=2&i=P 18Farmland is dominated by owner-farmers everywhere, though a

significant share of the land area is under administrator ownership

800

Number of farms in each ownership type by state, 2006

700

Matopiba states starred

600

Thousands of farms

500

Occupant

400

Administrator

300

200

Leessee/Partner

100 Owner

-

Bahia Minas Maranhão Piauí São Paulo Goiás Mato Mato Tocantins

Gerais Grosso Grosso do

Sul

50 Area of land in each ownership type by state, 2006

Matopiba states starred

40

Millions of hectares

30

Occupant

20 Administrator

Leessee/Partner

10

Owner

-

Mato Minas Mato Bahia Goiás São Paulo Tocantins Maranhão Piauí

Grosso Gerais Grosso do

Sul

Source: IBGE - Censo Agropecuário. 19Average land prices in the Cerrado have increased rapidly since 2009,

but land in Matopiba is still relatively inexpensive

Agricultural land average price in Cerrado states, 2009 - 2014

30

+12%

25

Thousands R$/hectare

Matopiba

+21% +22%

20

+16%

+21%

15 +20%

10 +24% +9%

+16%

5

0

X% PI MA BA TO MT MS MG GO SP

Compound

Annual Pasture land average price in Cerrado states, 2009 - 2014

+14%

Growth 16

Rate

Thousands R$/hectare

14

Matopiba

12 +20%

10 +18% +16%

8

+19%

6 +23% +12%

4

+25%

+12%

2

0

PI MA TO BA MT MS MG GO SP

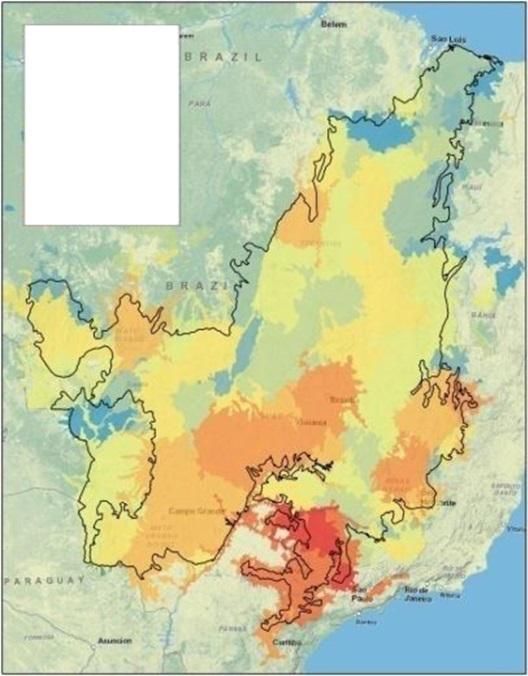

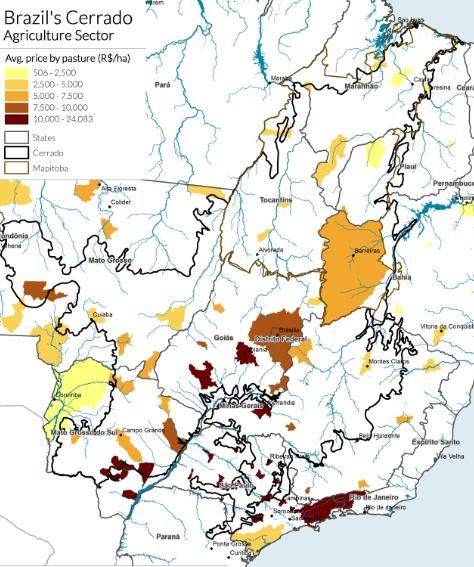

Source: Agrianual. Charts adapted from AgroIcone. 20Cheaper land prices in Matopiba make it an attractive area for

agricultural expansion

Avg. price by pasture (R$/ha)

506 - 2,500 Map of land prices in the Cerrado, 2012

2,500 - 5,000

5,000 - 7,500

Lower

7,500 - 10,000

10,000 - 24,083

States

Cerrado

Matopiba

Higher

Pasture land price map made by GreenInfo Network with data from

Agrianual, provided to CEA by AgroIcone. The Agrianual land price

database is incomplete, explaining why the map only shows select

areas. Land prices map on the right-hand side is from WWF, 2013. 21Currently, about 10% of the major agricultural crops and 20% of the

cattle produced in the Cerrado come from Matopiba

Soybean Sugarcane 1%

Bahia

3%

2% Maranhão 0%

4% 5% 3% 0%

7% 10%

Piauí • Mato Grosso dominates

11% Tocantins 10% soybean and corn

18% Goiás

3% production and also has the

Mato Grosso

6% largest cattle herd.

Mato Grosso do Sul

60%

10%

• Sao Paulo dominates

Minas Gerais

sugarcane production.

47%

São Paulo • Goiás and Mato Grosso do

Sul are leaders for corn and

soy.

Corn Cattle head • Maranhão is the only

Matopiba state with

3% 1% Bahia

1%

significant sugarcane

8% 4% Maranhão 8% 8% production; Matopiba also

1%

6%

Piauí has little corn production.

14% 15% 18% 6%

Tocantins • Cattle and soy dominate in

Goiás Matopiba.

Mato Grosso 16%

15%

Mato Grosso do Sul 16%

39% Minas Gerais

21%

São Paulo

Source: Pesquisa Agrícola Municipal, via AgroIcone. Link: http://www.sidra.ibge.gov.br/bda/tabela/listabl.asp?c=1612&z=p&o=28. 22Soy and corn production are growing in the Cerrado

Soybean production in Matopiba by state

3.0

2.5

2010

• The three “micro

2.0

regions” with the highest

Millions

2011

1.5 soy and corn production

2012

in Matopiba are Gerais

1.0 2013

de Balsas (Maranhão),

2014

0.5 Alto Parnaiba Piauiense

(Piauí) and Barreiras

0.0

Maranhão Tocantins Piauí Bahia (Bahia).

• In recent years, soy

production has grown

3.0 Corn production in Matopiba by state most rapidly in Tocantins.

2.5 • Corn production has

2010

grown rapidly in

2.0

Maranhão, Piauí, and

Millions

2011

1.5 Bahia.

2012

1.0 2013

2014

0.5

0.0

Maranhão Tocantins Piauí Bahia

Source: IGBE, via AgroIcone 23Grain storage capacity is a gap in the region and is concentrated in

Western Bahia

Storage facilities in Matopiba

Storage capacity by area

0 – 60 t

60 – 150 t

150 – 300 t

300 – 1,000 t • The Barrieras (Bahia)

microregion is has the

1.000 – 3,307 t

most developed

Warehouse agricultural storage

capacity, followed by

Gerais de Balsas

(Maranhão). Regions

are shown in blue on

the map.

Source: EMBRAPA, 2014, via AgroIcone. 24Matopiba states receive far less agricultural credit than southern

Cerrado states

Rural credit distributed in 2013

20

• Minas Gerais and Sao

Paulo receive by far the

18

most lending of the

Cerrado states, receiving

16

about R$18 billion in

14

2013.

• Mato Grosso and Goiás

12 comprise a second tier,

each receiving around

Billions R$

10 R$12 billion in 2013.

• Aside from Bahia,

8 Matopiba Matopiba states each

received less than R$2

6

billion in 2013.

4

2

0

MG SP MT GO MS BA TO MA PI

Source: Bacen: http://www.bcb.gov.br/pt-br/sfn/credrural/sicor/matrizinformacoes/Paginas/pgRegiaoUf.aspx, via AgroIcone 25The Matopiba states have lower Human Development Index (HDI)

scores than states in the southern Cerrado

HDI in Cerrado municipalities (2010)3

• The Human Development Index (HDI)

is a blended metric that integrates

0.44 – 0.58

health, education, and income

indicators. It was created by the 0.58 – 0.64

United Nations Development Program, 0.64 – 0.69

in 1990.1 0.69 – 0.74

• HDI is a 0-1 scale. In 2010, the country 0.74 – 0.85

with the highest score was Norway

(0.94) and the lowest was Niger (0.32).

• Matopiba states (Maranhão, Tocantins,

Piauí and Bahia), in the northern part

of the biome, have lower HDI scores

than southern Cerrado states.

Sources: (1) UNDP, 2013. (2) World Bank 2015. (3) CEPF 2015 26AGRICULTURE

SOY AND THE SOY SUPPLY CHAIN

27Soybean production is concentrated in southern Cerrado, Mato Grosso, and

western Bahia; high yield areas are dispersed

Soybean crop production in 2013 Soybean crop yield in 2013

Source: Produção Agrícola Municipal via AgroIcone 28Soy prices have skyrocketed

Average price in R$/ton by crop

900

750 • Growth in soy prices has far

outpaced sugarcane and

600

corn, leading it to be the

fastest expanding crop in

Price crop (R$)

the Cerrado.

450 • Sugarcane prices have

hardly increased since 1995

300 • Corn prices have fluctuated

since 2009, with modest

overall growth.

150

0

1995 2000 2005 2009 2010 2011 2012 2013

Sugarcane Soybean Corn

Source: data from Pesquisa Agrícola Municipal; chart adapted from AgroIcone. 29Soy production of Tocantins and Maranhão have comparable yields to

the rest of the Cerrado; Bahia and Piauí lag behind

Soy yield by state in the Cerrado, 2013 (kg/ha)

3,500

Matopiba

3,000

2,500

kg / hectare

2,000

1,500

1,000

500

0

Goiás São Paulo Mato Minas Mato Tocantins Maranhão Bahia Piauí

Grosso Gerais Grosso do

Sul

Source: IBGE - Produção Agrícola Municipal, via AgroIcone 30Crushing industry: Process Industrial soy oil derivatives: The

whole soybeans into meal and refined oil can be further processed

into margarines, mayonnaise, and

Soy supply chain oil. Soybean meal in the

domestic market goes to the vegetable fats, which are intended

feed industry. Other processed primarily for the domestic market

products can also be sold to the through wholesale distributors and

food, chemical and retailers.

pharmaceutical industries.

A

Production Soybean Industrial oil

Inputs Originators Distribution

81.7 m ton crushers derivatives

West Distributors:

Seeds Salad

Central Link the

46.8% Private crushing and

Warehouse companies Wholesale soy

Fertilizers South Dressing

A

derivatives

37.1% industries to

A A A A the final

Pesticides Margarine

Southeast Agricultural consumers.

cooperatives Retail

6.4%

A

Machinery Northeast Mayonnaise

A Coop-

6.4% Trading eratives Institutional

companies Market

Other North Other

3.3% A

A

A

Originators: Transact

International A A A

with producers /

market US$ Feed industry Domestic

cooperatives in order to

22.8 billion Meat industry Market

acquire soybeans and

sell to the foreign

A

market and to the Other

crushing industry. This industries Note:A Values, when mentioned, for 2013. Source: Ministério

a step can be skipped. da Agricultura; IBGE - Produção Agrícola Municipal. 31Strategic Importance of this Sector

oy Complex – 2013

Brazilian soy supply chain by the numbers

million tons

Exportations

Export 12 million

Meal Meal 15.0 tons

Domestic market

29.328 million tons Dom. Consumption

16 million tons

Production

Production Crushing

Processing 14.2

82 million tons

82.3 36 million tons Export

38.5 Exportations

Oil 1 million tons

Oil 1.7

7 million tons Domestic market

7.4 Dom. Consumption

6 million tons

5.7

Biodiesel

2.0

Exportations Biodiesel

38.5 2 million tons

Export

43 million tons

ABIOVE 7

Source: ABIOVE & MDIC-Secex, via AgroIcone. 32Bunge, Cargill, ADM, and Louis Dreyfus dominate Brazilian soy trading

Active crushing units in Cerrado by company, 2014 • There are around 30 companies or

Company Units Location Company Units Location Company Units Location cooperatives trading soy in the

Bunge 6 BA, GO, MS, MT, PI Agrex 1 GO Oleoplan 1 BA Cerrado region, with 42 soybean

Cargill 5 BA, GO, MG, MS, MT Amaggi 1 MT Olvebasa 1 BA crushing units between them,

ADM 4 GO, MG, MS, MT Araguassú 1 MT Olvego 1 GO

including 10 inactive units.

Caramuru 3 GO, MT Cereal 1 GO Producampo 1 MT • The top 10 companies with the largest

Granol 3 GO, SP Clarion 1 MT Selecta 1 MG installed crushing capacity represent

Algar Agro 2 MA, MG Correcta 1 MS Sodru 1 SP

Brejeiro 2 GO, SP Dureino 1 PI Sperafico 1 MT

55% of the total industry capacity in

Comigo 2 GO Grupal 1 MT Tauá 1 MT Brazil.

Louis • In 2014, Bunge, Cargill, ADM, and

Dreyfus 2 GO, MT Lasa 1 GO

Sina 2 SP Noble 1 MT

Louis Dreyfus exported USD$ 17

billion (Bunge - $6 billion; Cargill - $4

billion; Louis Dreyfus - $3.5 billion;

ADM - $3.3 billion). These four

Major exporting companies by value companies exported 55% (USD$ 17.2

21

billion) of the total soy complex

18

exported by Brazil in 2014 (USD$ 31.4

15

billion).

Billion USD

12

• In recent years, the Brazilian soybean

9

crush industry has become more

6

concentrated due to mergers and

3

acquisitions in the late 1990s, when

0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

international companies bought small

and medium national industries.

ADM Bunge Cargill Louis Dreyfus

Sources: Table - ABIOVE. Chart - MDIC-Secex. Both graphics and slide text adapted from AgroIcone. 33Soybean crushing capacity is concentrated in the southern Cerrado

and the far Southern region of Brazil

Soybean crushing capacity

200

175 • In the past 10 years crushing

capacity has increased by 37%

Thousand tons/day

150

125 in Brazil, from 132 to 180

100 thousand tons/day.

75 • In the same period, crushing

50 capacity in the Cerrado

25 increased by 48%, from 104 to

0 109 thousand tons/day.

2002

2005

2008

2011

1997

1998

2000

2001

2003

2004

2006

2007

2009

2010

2012

2013

2014

• MT/MS/GO comprise 41% of

Brazil Cerrado

Brazilian soybean crushing

capacity, while states in the far

South comprise 38%.

Crushing capacity in 2014 • Matopiba’s crushing capacity is

45 currently very limited.

40 • Since 2004, crushing capacity

35

has increased about 96% in MT,

Thousand tons/day

30

25

50% in RS, 37% in GO, and 45%

20 in MS.

15

10

5

0

MT PR RS GO SP MS MG BA SC PI AM MA

Source: ABIOVE. Charts adapted from AgroIcone, slide test partially adapted from AgroIcone. 34Whole soybean exports are growing while soybean meal and oil

exports are declining

Brazilian soy exports by type1

50 • In the 1990’s, soybean meal

45 was the main soy product

40

35

exported by Brazil.

• Starting in 2000, China began to

Million tons

30

25 invest it its own crushing

20

15 capacity and started to import

10 more grain than meal.

5

0

• Domestic consumption of

soybean meal has increased

2007

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2008

2009

2010

2011

2012

2013

2014

significantly in the last decade,

Soybean Soybean meal Soy oil mainly due to expansion and

concentration of Brazilian meat

Brazilian soybean destination2 production.

90 • Since 2005 an increasingly

75 greater proportion of Brazilian

Million tons

60 soybeans have been exported,

45

while the amount consumed

domestically fluctuates

30

considerably year over year.

15

0

2001

1997

1998

1999

2000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Domestic Consumption Exports

Sources: (1) Data source: MDIC, chart adapted from AgroIcone. (2) Data source: Pesquisa Agrícola Municipal / MDIC-Secex, chart adapted from AgroIcone. This graph is for soybeans, in

particular – does not include soybean meal or soy oil. Some slide text adapted from AgroIcone. 35Domestic consumption of soybean meal has increased, while major

international buyers have gained a preference whole soybeans

Whole soybean export Soy oil export destinations, • China imports the vast

destinations, 2014 2014 majority of Brazilian

soybeans (71% in

2014).

China India

3%

2% 15% 15% • India and China each

Spain 33% China

7% import about one third

4% Netherlands Bangladesh

of Brazil’s soybean oil

5% Thailand 7% Algeria exports.

United States 8% Cuba

71% • As of 2014, the main

Other Other

30% Brazilian soybean meal

importers are the

Netherlands, France,

Germany and Thailand.

Brazilian soybean meal export Brazilian soybean meal export • China used to buy

destinations in 1998 destinations in 2014 more soybean meal

from Brazil, but it has

7% 11% invested in its own

crushing capacity and

37% 19%

Germany

39% 14% now imports the

2% France lower-value whole

9%

Thailand soybeans.

23% Netherlands

12% 26%

China

1%

Others

Source: MDIC-Secex, via AgroIcone. 36Globally, the Unites States and Brazil dominate soybean exports and

China now accounts for nearly 65% of soybean imports

Soybean exporters

120

• US (49 million tons) and Brazil (46

100 million tons) are the largest

80 exporters of soybeans, globally,

Million tons

60

followed by Argentina (8 million

tons) and Paraguay (5 million tons)

40

as of 2014/15.

20

• Brazil soybean exports increased

0 by 128% in last decade, followed

by Paraguay (67%) and US (63%).

Argentinian exports decreased by

United States Brazil Argentina Paraguay Other 16%.

Soybean importers • In the last decade China’s soybean

120 imports have increased by 187%,

100

while imports by Japan and the EU

have decreased by 32% and 13%,

80

Million tons

respectively.

60

40

20

0

China European Union Mexico Japan Other

Source: chart data from USDA, charts adapted from AgroIcone. Slide text adapted from AgroIcone. 37Growth in soybean production is expected to continue at a fast pace

• From 2014 to 2024, the Brazilian

Soybean long-term projection government predicts an increase in

120

soybean production of 37%, reaching 118

million tons by the 2023/24 growing

season.

100

• In the same period, domestic consumption

80

and exports are expected to increase by

about 26% and 44% respectively.

Million tons

60 • The increase in domestic consumption will

be caused by higher demand from the feed

40 industry and for biodiesel production.

• The planted soybean area is expected to

20 increase by 10 million hectares over the

next 10 years, reaching 40 million hectares

0 in 2024.

o The planted area is expected to increase,

mainly in the Matopiba states.

o In Mato Grosso, soybean area is expected

Production Consumption Exports to expand, primarily over degraded

pasture areas.

Source: Chart data from Ministério da Agricultura, chart adapted from AgroIcone. Slide text partially adapted from AgroIcone. 38Soybean meal and oil production are projected to grow more slowly;

oil will likely remain mostly domestically consumed

Soybean meal long-term projection

40 Soybean Meal

35 • Between 2013/14 and 2023/24,

30 soybean meal production is expected

Million tons

25

20

to increase by about 25%, reaching 35

15 million tons in 2023/24.

10 • Growth is expected to be primarily

5 driven by domestic consumption.

0

• The Brazilian government estimates

that in 2023/24, about 54% of soybean

Production Consumption Exports

meal production will be consumed

domestically, and 45% will be exported.

Soybean oil long-term projection

Soybean Oil

10

9 • Between 2013/14 and 2023/24, the

8

7

Brazilian government estimates an

Million tons

6 increase of about 26% in soybean oil

5

4 production, reaching 9 million tons in

3 2023/24.

2

1 • Domestic consumption and exports are

0 expected to increase by about 23%

and 18%, respectively.

Production Consumption Exports

Source: Chart data from Ministério da Agricultura, chart adapted from AgroIcone. Slide text partially adapted from AgroIcone. 39AGRICULTURE

THE BEEF AND MILK SUPPLY CHAIN

40The cattle herd is dispersed throughout Brazil, with significant stocks in

the Cerrado and Amazon

Cattle herd in Brazil, beef and dairy, 2013

• Cattle for beef and milk are

major agricultural products in

Brazil for both domestic

consumption and export.

• Cattle, especially beef cattle, is

present in the frontier areas,

and pasture is often the first

productive use of lands

converted from natural

vegetation.

• Soy and other crops are more

profitable uses of land, so

often recently deforested land

spends a few years as

Legend pastureland before being

90 to 54,175 head converted to cropland.

54,176 to 118,456 head

118,457 to 222,810 head

222,811 to 547,022 head

547,023 to 3,766,176 head

No data

Source: IBGE - Pesquisa Pecuária Municipal. 41Beef cattle are dispersed around the country, while dairy cattle are

concentrated in southeastern Brazil

• While cattle for beef in Brazil are spread throughout the Cerrado (especially south & west) and the

Amazon, cattle for dairy are concentrated in the southeast part of Brazil.

• Consequently, dairy cattle are likely a less direct driver of deforestation; the soy used in their feed is likely

the main driver of deforestation from the dairy industry.

Beef cattle in Brazil Milk cows in Brazil

291 to 10,095 head 30 to 5,023 head

10,096 to 19,736 head 5,024 to 9,679 head

19,737 to 39,965 head 9,680 to 17,299 head

39,966 to 72,142 head 17,300 to 29,614 head

72,143 to 172,988 head 29,615 to 49,229 head

172,989 to 450,002 head 49,230 to 82,928 head

450,003 to 3,648,728 head 82,929 to 467,000 head

No data No data

Source: IBGE – Censo Agropecuário & IBGE – Pesquisa Pecuária Municipal 42Beef production is expected to grow 20% by 2040; milk production is

projected to grow 30% in that timeframe

Beef long-term projection for Brazil Beef projections

14 • Roughly 2% growth per year is expected in

12

beef production through 2024.

Million tons

10

• Between 2014 and 2024 Brazilian beef

8

consumption is expected to increase by

6

4

16%, from 7.7 million to 9 million tons.

2 • In the same period, a growth of about 40%

0 in exports is expected, from 2.1 million to

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2.9 million tons. This represents, on

Production Consumption Exports average annual growth rate of 3.4%.

Milk projections

Milk long-term projection for Brazil

• Between 2013/14 and 2023/24,

60 1,200

projections show an increase of about 30%

50 1,000 in milk production, from 36 million to 46

Thousand tons

Million tons

40 800 million tons.

30 600 • Brazilian milk consumption is expected to

increase by about 27% in the next 10

20 400

years, from 38 million to 48 million tons.

10 200

• Exports will increase by about 34% in the

0 0 same period, reaching 191 thousand tons.

• Import projections show a decrease by

about 9% in the period, from 1.1 million to

Production Consumption Imports Exports 991 thousand tons.

Source: Ministério da Agricultura. Charts and some text adapted from AgroIcone. 43Brazil has one of the largest commercial cattle herd in the world

• 5 countries share 79% of the world’s

cattle: India (367 million head), Brazil

World cattle herd

(258 million), China (151 million), USA

1400

(125 million) and the EU (117 million).

1200

• Brazil has the largest commercial herd

in the world (much of India’s herd is

1000 outside of the market).

• Between 2000 and 2013 the Brazilian

Million animals

800 cattle herd increased by nearly 40%,

while India’s expanded by only 9%.

600 During that same time the other major

cattle-producing countries declined:

400

o China, -7%

o USA -10%

200

o EU -10%

0 • The total world cattle herd decreased

2000 2002 2004 2006 2008 2010 2012 2014 by 3% between 2000 to 2014 from

1.32 billion head to 1.28 billion head.

India Brazil China USA European Union Other

Source: data from USDA, chart adapted from AgroIcone. Slide text a partially adapted from AgroIcone. 44The US, Brazil, EU, and China lead in beef consumption

World beef production

60 Production

• Brazil ranks second in global beef production.

50

• In 2014 Brazilian production represented 16% of

40 world production, 32% higher that its share in

Million tons

30 2000 (12%).

20

• From 2000 to 2014, US and EU production

decreased by around 10%, while production in

10

Brazil, China and India increased by 49%, 34% and

0 170% respectively. These five countries accounted

2000 2002 2004 2006 2008 2010 2012 2014

for two-thirds of global beef production in 2014.

USA Brazil European Union China India Other

Consumption

World beef consumption

60 • World beef consumption increased by 9%, from

2000 to 2014, reaching 58 million tons.

50

• In the last decade, Brazilian beef consumption

40 increased by 29% and Chinese beef consumption

Million tons

30 increased by 48%. On the other hand, the US, and

20

EU Argentina consumption decreased by about

10%, 8% and 2%, respectively.

10

• In 2014, Brazil, China, US, EU, and Argentina

0 together consumed 63% of the total world beef.

2000 2002 2004 2006 2008 2010 2012 2014

USA Brazil European Union China Argentina Other

Source: data from USDA, chart adapted from AgroIcone. Slide text a partially adapted from AgroIcone. 45Since 2000, Brazil’s beef exports have increased five-fold, while China

emerged as a major importer

World beef exporters

10 Exporters

• The main beef exporters in 2014 were India

8

(2.1m tons), Brazil (1.91m), Australia (1.85m),

Million tons

6

USA (1.17m) and New Zealand (0.6m).

4

• According to the USDA, from 2000 to 2014,

2 beef exports increased considerably in India

0 and Brazil, by about 505% and 291%,

respectively.

India Brazil Australia USA New Zealand Other

World beef importers Importers

8 • Main beef importers in 2014 were the US

7

(1.34 m tons), Russia (920 thousand tons),

6

Million tons

5 Japan (740 thousand tons), Hong Kong (650

4 thousand tons) and China (417 thousand

3

2

tons).

1 • Between 2000 and 2014, China had the

0 largest increase in beef imports, about

2,506%, albeit off of a small base.

USA Hong Kong Russia Japan China Other

Source: data from USDA, chart adapted from AgroIcone. Slide text a partially adapted from AgroIcone. 46Most Brazilian beef is consumed domestically; Russia and Hong Kong*

account for nearly half of Brazilian beef imports

Brazilian beef destination

10

9

• About 80% of Brazilian beef

8 production is consumed

7 domestically, and 20% is exported,

Million tons

6

5 although exports have been

4 growing slightly faster than

3

2

domestic consumption.

1 • Beef production increased about

0

2000 2002 2004 2006 2008 2010 2012 2014 50% from 2000 to 2014, reaching

nearly 10 million tons.

Domestic Consumption Exports

• The main beef exporting states in

Top export destinations for Brazilian beef 2014 were SP (439 thousand tons),

1.8 MT (279 thousand tons), GO (228

1.6 thousand tons), MS (165 thousand

1.4 tons) and RO (134 thousand tons).

1.2

Billions USD$

1.0

• Key end buyers in 2014 were Hong

0.8 Kong (25%), Russia (20%),

0.6 Venezuela (11%) and Egypt (11%).

0.4

0.2

0.0

*It isn’t clear from the data what the final

destination is for exports to Hong Kong. It

may serve as an intake port for beef

consumption in mainland China, or may

be part of a processing and re-export

Source: MDIC via AgroIcone.

hub.

47Brazil’s cattle herd has been fairly stable over the last 10 years

250 Head of cattle in Brazil

200 • States with at least part of

their area in the Cerrado

150

are home to about 60% of

Non-Cerrado states

Millions of cattle

100

Brazil’s cattle herd. (Note

Cerrado states that this graph shows Cerrado

50 states, not the Cerrado Biome.)

• In 2013 Mato Grosso had

0 over 28 million head,

1990

1995

1991

1992

1993

1994

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Minas Gerais 24 million,

Goiás and Mato Grosso do

Sul about 21 million, and

160 São Paulo and Bahia each

Head of cattle in Cerrado states had about 10 million head.

140 Piauí

• Tocantins and Maranhão

120 Maranhão had about 8 million head

100 Tocantins in 2013, while Piauí had

Millions of head

80

São Paulo less than 2 million.

Bahia

60

Mato Grosso do Sul

40

Goiás

20 Minas Gerais

0 Mato Grosso

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Source: IBGE - Pesquisa Pecuária Municipal, via AgroIcone. 48Beef cattle supply chain

Suppliers: Primary Industrialization: Marketing:

Activities related to producers: Primary processing Wholesalers & exporters

animal health, Companies or Slaughter and initial These actors often also

nutrition, and farmers that breed break-down of animals. provide storage & delivery.

genetics. and fatten the

Secondary processing Retailers

animals. Often there

Incorporates meat into Sell beef directly to

are multiple steps in

food products or consumer. Retailers include

this part of the

further processes meat grocery stores, restaurants,

chain.

products. and food services providers.

Suppliers Primary Industrialization Marketing Consumption

producers

Primary Wholesaler

processing or Exporter

Input Agricultural industrial-

Suppliers companies iztion Final

Retailer

customer

Secondary Collective /

Carrier Farmers

processing institutional

agents

indutrial- food

ization companies

Source: Ministério da Agricultura, via AgroIcone. 49The top three beef cattle companies in Brazil – JBS, Marfrig, and

Minerva – control 36% of slaughter capacity

The top 3 Brazilian beef cattle companies

% of beef cattle Number and location of

Company slaughter slaughterhouses2

capacity1

• Total: ~50 total units in Brazil

• Cerrado: ~20 units in or near the Cerrado

22% • Matopiba: 1 unit in Maranhão; 4 units in

Pará near the Cerrado (Tocantins), 1 unit

near Belém

• Total: ~20 total units in Brazil

• Cerrado: ~10 units in or near the Cerrado

9% • Matopiba: No identified units in

Matopiba states

• Total: ~8 units in Brazil

5% • Cerrado: ~5 units in or near the Cerrado

• Matopiba: 1 unit in Tocantins

Sources: (1) Valor Economico, 2011 via AgroIcone. (2) ABIEC website, accessed September, 2015. http://www.brazilianbeef.org.br/mapadasplantas.asp. 50Slaughterhouses are concentrated in southern Cerrado states,

although Rondonia and Para have significant slaughter capacity

Major slaughterhouses

• Slaughterhouses have settled near the Pasture

producing regions, mostly in the southern Slaughterhouse

Cerrado states. Matopiba region

Protected areas and

• There are 260 slaughterhouses registered in indigenous lands

the SIF (Federal Inspection Service). In MT State boundaries

there are 37; in MS - 35; SP - 30; MG - 29; GO -

26; RO - 18.

Number of slaughterhouses

6 Southern Cerrado Matopiba

5

4

Millions

3

2

1

0

Sources: Map via AgroIcone. Some text adapted from AgroIcone. Chart data from Ministério da Agricultura via AgroIcone. 51Brazil’s dairy sector (production value USD$37 m) is almost as important

economically as its beef sector (production value USD$50 m)

Production value of beef and dairy in Brazil, 2012

• Fresh or chilled cattle meat in 2012

was valued at $34 million USD.

1% Frozen cattle meat was valued at

1% 0%

$12 million USD. Together they

2% account for over 90% of the value of

beef cattle production, and 53% of

15%

overall cattle production (including

dairy).

39%

Fresh or chilled cattle meat

Frozen cattle meat

Cattle edible offal

27%

Dairy production

Preparation of the milk

Leather & skin of cattle

14% Cattle fat, sheep or goats

1% Cattle fat, raw sheep or goats

Spoils raw, inedible

Source: IBGE – Pesquisa Industrial Anual – Produto, via AgroIcone. 52The dairy industry is less concentrated than the cattle industry

Top 10 companies in milk purchased (thousand liters)1 Distribution of dairy companies in Brazil2

Company 2013 2014

1 DPA/Nestlé 2,033,000 2,000,000

2 BRF 1,377,264 1,424,626

3 CCPR/ ITAMBÉ 1,056,264 1,222,373

4 LATICÍNIOS BELA VISTA 828,630 1,032,098

5 CASTROLANDA, BATAVO e CAPAL 548,674 765,938

6 EMBARÉ 527,721 563,952

7 AURORA 499,500 518,900

8 DANONE 448,716 457,690

9 CONFEPAR 411,037 418,975

10 JUSSARA 330,380 348,125

• In recent years, the dairy industry has become more concentrated, with some companies gaining

market share in both the purchase of milk and in end markets.

• Main international companies in this sector are DPA/Nestlé and Danone; they represented 28% of the

total milk bought by the top 10 companies of this sector in 2014.

• BRF is the second largest company in milk purchased and the largest Brazilian national company in the

sector.

• Most dairy processing is located in the largest milk producing states of MG, GO, PR and RS.

Sources: (1) Associação Brasileira dos Produtores de Leite via AgroIcone. (2) G100 Associação Brasileira de Pequenas e Médias Cooperativas e Empresas de Laticínios. (3) Slide text adapted

from AgroIcone. 53Brazil’s dairies lag behind other major milk producers in terms of yield

• World milk yield increased by

World dairy milk yield in 2014 21% from 2000 to 2014,

12

reaching over 4 tons/cow.

10

• From 2000 to 2014 the milk

Tons/cow

8

6 yield growth was most

4 significant in Ukraine (94%),

2 Argentina (43%), EU (34%), and

0

USA (22%). In Brazil the yield

improved 17% during this

period.

• Brazil’s dairy productivity is

lower than other major milk

producing countries.

Data source: BGE - Pesquisa Pecuária Municipal; charts and text adapted from AgroIcone. 54AGRICULTURE

PASTURE INTENSIFICATION

55Pasture intensification can spare land, provide room for expansion of

crops, and improve cattle productivity

• Pasture intensification increases productivity from a given unit of land through improved

forage quality, instead of expanding production by expanding the land footprint.

• Pastures intensification can: 1) reduce the land footprint needed to produce cattle, thus

reducing pressure on forests, 2) free up land that soy and other crops can expand onto, thus

reducing pressure on forests, and 3) reduce the enteric fermentation emissions associated

with the cattle herd by improving their diets.

• In general, Brazil has relatively low density of cattle per hectare (less than one head of cattle

per hectare) spread out over ~160 Mha1 (roughly 20% of Brazil’s total area). There is

considerable room for intensification and efforts are already being made on the part of the

government, trade associations, and NGOs, to intensify through restoration of degraded

pastures. Current cattle production is mostly low-density2

Sources: (1) IBGE, Agricultural Census, 2006.

(2) Tollefson 2010. 56The land sparing effects of pasture intensification could be very

significant

In theory, intensification has a high GHG mitigation

potential because it helps avoid cattle-driven Change in LULUCF GHGs caused by cattle

deforestation. Increasing the productivity of pastures intensity tax or subsidy policy scenarios (2030)2

might save 250-450 Mt CO2e per year by 2030.

• Strassburg et al. 2013 modeled intensification on

Brazil’s 115 Mha of cultivated pasturelands and

found that intensification might prevent land use

change emissions of ~400 Mt CO2e per year

(assuming continuation of current deforestation

trends), while reductions in enteric fermentation

could mitigate ~50 Mt CO2e per year in 2030. 1

• Cohn et al. 2014 did a similar analysis, investigating

the effects of a government subsidy for intensive

cattle production or a tax on extensive cattle

production.2

o Both a tax and subsidy yield ~400 Mt CO2e per

year by 2030 from decreases in deforestation in

Brazil. (middle graph)

o Intensification driven by subsidies would

presumably increase the herd size and thus

enteric fermentation emissions, while

intensification driven by taxes would

presumably decrease herd size and thus enteric

fermentation – both effects would be marginal

(Cattle intensification and use of mixed systems can meet the demand

for land from expanded crop production in Brazil

• According to one modeling effort, future crops will demand an area of 33.5 Mha across all of

Brazil. (By way of comparison, the area of the entire Cerrado is 200 Mha). If these crops

were distributed across mixed agropastoral (crop-livestock) and silvopastoral (crop-planted

forest) systems, then the area might be significantly larger (~60 Mha).

• This need could be accommodated

using the existing footprint of Future demand for land from crops and planted forest (Mha) can

be met by expanding onto land spared by intensification of cattle

agriculture by intensifying agriculture

and then expanding onto newly freed- 1

up lands. 6

• According to this modeling effort,

Brazilian cultivated pasturelands are

only at 32-34% of their potential 8

productivity currently.

• Increasing productivity to 49-52% of

its potential would allow for

agricultural production without

expanding the overall footprint of 18

agriculture.

• This would save 14.3 Gt CO2e, almost

all in avoided deforestation.

-34

Cattle Soybean Maize Sugarcane Planted Total

forest

Source: Strassburg et al., 2014. 58The Cerrado has significant pastureland that is suitable for crop

production

Pastureland suitable for agriculture*

Pampas Pantanal Caatinga Atlantic Forest Cerrado Amazon

20

18

16

14

Million hectares

12

10

8

6

4

2

0

Source: Soares-Filho, et al, 2014. *Without considering climatic or land-use zoning restrictions, per biome (colors) and state (horizontal axis). 59In theory, no additional vegetation needs to be cleared

• Assuming very modest levels of cattle Possible land use scenario in 2040 that avoids

intensification and use of mixed crop- further conversion of natural vegetation

livestock and crop-forestry systems,

demand for agricultural products in 2040

can be met without expanding the overall

footprint of agriculture (see right).

• An alternative scenario where cattle

production is concentrated in high

productivity areas would potentially even

free up additional land to be reforested.

• The challenge is that, while such an

allocation may make sense at the national

level, it may not reflect the needs of

individual landowners, each of whom are Sugarcane

likely to seek to maximize their own Reforestation

Agropastoral (AU/ha)

economic gain from the land that they 0.00-1.00

control. This may involve expanding 1.01-2.00

2.01-5.35

production into areas of native vegetation. Silvipastoral (AU/ha)

0.00-1.00

1.01-2.00

2.01-5.35

Traditional Cattle Ranching (AU/ha)

0.00-1.00

1.01-2.00

2.01-5.35

Source: Strassburg et al., 2014.

60AGRICULTURE

AGRICULTURAL CERTIFICATIONS

61The Roundtable for Responsible Soy (RTRS) certification has the

backing of global soy traders, but has had limited impact to date

RTRS was established in 2006 and is a multi-stakeholder initiative of the mainstream soy

industry, including retailers, producers, the feed industry, NGOs, and banks.1

• RTRS has over 150 members from more than 120 countries. Its RTRS-certified soy program

was launched in 2011.

• RTRS has a goal of reaching 10 million tonnes of certified responsible soy worldwide by 2017. 2

Brazil’s total soy production in 2014 was 90 million tones. In 2014, 1.5 million tonnes of RTRS-

certified soy were produced, accounting for less than 1% of global soy trading.3

• RTRS soy cannot be produced on land deforested after 2009. RTRS also promotes increasing

productivity and other best agricultural practices.4

• The price premium for RTRS soy is very low, and little public pressure has been exerted on this

segment of the supply chain (traders) , which reduces the incentive for buyers to buy RTRS-

certified soy.

Supply and demand of RTRS soy6

• RTRS recently completed a map to guide future 1.4

expansion of soy in Brazil and Paraguay. These 1.2

Millions of tonnes

maps identify High Conservation Value (HCV) 1.0

0.8

areas with a vision towards incorporating them 0.6

into sourcing standards; discussions of how to 0.4

use this map are ongoing. 0.2 * *

0.0

• Amaggi is a leader in RTRS certifications; as of 2011 2012 2013 2014

2014, 42% of RTRS certified soy came from Stock/credits left over from previous year

Amaggi and its suppliers.5 Production

* Indicate incomplete data

Sales (report was issued in 2014)

Sources: (1) WWF, 2015. (2) ResponsibleSoy.com, 2015. (3) IISD.org, 2015. (4) RTRS, 2011. (5) Juliana Lopes interview, Amaggi. (6) WWF, 2014. 62RTRS’ mapping effort for responsible soy expansion is very detailed

Guide for responsible soy expansion

RTRS members must embed in procurement and investment strategies

RTRS criteria for soy

expansion

Not permitted

Areas have value;

depends on HCVA

assessment

Law adequate

No native

vegetation, law

adequate

63In addition to RTRS there are several other initiatives and certifications

that have emerged for soy in Brazil

Alianca da Terra is a Brazilian NGO focused on sustainable farming

• Alianca da Terra (ADT) maintains a Registry of Social-Environmental Responsibility (RSR).

The main goal of the RSR is to help guide landowners through the key criterion of the RTRS

certification.2

• In 2008, ADT began working with ADM on the “Doing it Right” program, which is focused

on entering ADM’s suppliers into the RSR. Today it has registered over 500 properties.2

• ADM and Alianca da Terra have also joined the SojaPlus program (see below).3

SojaPlus is the Brazilian soy industry’s main soy sustainability initiative4

• Launched in 2011, the Soja Plus program is the result of a partnership between ABIOVE

(the Brazilian Vegetable Oil Industry Association) and APROSOJA (the Mato Grosso State

Soybean and Corn Producers Association). The initiative was started in Mato Grosso but

aims to eventually expand to Minas Gerais, Mato Grosso do Sul, and Paraná.5

• SojaPlus is a comprehensive sustainability and best practices program. It is not centered

around a certification program, but nonetheless offers certification to participating farms

through a third party audit.5

• The main activities of SojaPlus involved farm trainings and rural assistance with technology

and best agricultural practices.6

Sources: (1) Alianca da Terra, 2015. (2) IFC, 2015. (3) ADM, 2013. (4) ABIOVE, 2010. (5) Silva, 2015. (6) ABIOVE 2010. 64AGRICULTURE

TRANSPORTATION INFRASTRUCTURE

65Brazil is making significant investments in transportation infrastructure

in the Cerrado

Lack of transportation infrastructure has been a limiting factor for agriculture in the Cerrado

• It is generally cheap to produce agricultural crops in the Cerrado, but relatively expensive

to bring them to market. As transportation infrastructure improves, it has the potential to

improve the economics of production and speed the expansion of agricultural

development near transportation corridors.

Brazil’s Logistics Investment Program (LIP), first announced by President Rousseff in 2012, will

lead to significant investment in road and rail transport in the Cerrado and elsewhere in Brazil. 1

• Scope: R$198 billion. R$ 69 billion from 2015-2018, and $129 billion after 2018.

• R$ 66b will be spent on roads; R$ 86b on railways, R$ 37 on ports, and R$ 8.5 on airports.

The third phase of Brazil’s Growth Acceleration Program (PAC-3) focuses on expanding

investment in infrastructure to stimulate the productive sectors, including: 2

• a host of new hydropower plants

• the completion of the North-South railway

• support for a East-West railway (to connect Brazil to the Pacific Ocean)

• expansion of the highway system

Sources: (1) McKenna, 2012. (2) KPMG. “Investing in Brazil: A land of opportunities,” November, 2012, http://bit.ly/22JwQTl. 66Brazilian roads are currently the backbone of agricultural transport in

the Cerrado

Brazil’s major roadways

• There are 213,000 km of paved roads

in Brazil; another 21,00 km are under

currently construction.

• Roads help make land accessible and

usable at a lower cost, driving

deforestation in the surrounding

areas.

Share of total road length among Cerrado states2

14% Mato Grosso

Mato Grosso do Sul

6% 30%

Goais

3% Minas Gerais

6% Sao Paulo

Maranhao

7% Tocantis

21%

9% Piaui

4% Bahia

Sources: Ministério dos Transportes, via AgroIcone. Pie chart data source: DNIT. Chart adapted from AgroIcone. 67Cerrado highways: existing, planned, and under construction

Legend

CAR-FIP priority municipalities

Existing highways

Planned highways PAC plans for highway expansion

Highways under construction include:1

Indigenous area • the construction and paving of

Federal protected area BR-235 in Piauí

Federal sustainable use area • the paving of BR-163 in Mato

State protected area

State sustainable use area

Grosso

• the construction of the BR-158

and BR-242 in Mato Grosso

• the duplication of the BR-080

in Goiás

• construction of the BR-350 in

Mato Grosso do Sul

• the construction of the BR-080

passages in Mato Grosso and

Goiás.

Source: map – MMA. “Marco de Gestão Ambiental e Social – MGAS.” 2014. (1) “Transportes 2014 e Resultados 2011 a 2014,” Ministério dos Transportes. 68Cerrado railways: existing, planned, and under construction

Legend

CAR-FIP priority municipalities

Existing railways

Planned railways

Railways under construction

Indigenous area

Federal protected area • Ambitious railways

Federal sustainable use area schemes, including a

State protected area

State sustainable use area

north-south trunk link

being constructed

through Tocantins and

Goiás, would link

Cerrado breadbaskets

to demand centers and

ports on both the East

and West coasts of the

continent.

Sources: map – MMA. “Marco de Gestão Ambiental e Social – MGAS.” 2014. 69There are plans to greatly increase rail capacity in the Cerrado in

support of agricultural transport

Planned expansion of Cerrado’s

Railroad infrastructure is slated to expand throughout the Cerrado, main North-South railway1

including through two high-profile projects.

Bacarena

The North-South railway1

Acailandia

• The partially-complete North-South railway will be a major route for

grain export from the Cerrado. Legend

• Between 2011 and 2014 over 900km of railway was constructed. Existing railways

Planning stage

Under construction

Palmas

Completed

Twin Ocean Railroad In operation

• China recently proposed a Brazil’s existing and planned railways4

5,300km, USD$10 billion railway N-S trunk line Ouro Verde

that would cut across the Minas de Goiás

Anapolis

Gerais, Goiás, Mato Grosso, the

Southern Amazon, and Peru.

Feasibility studies are underway.2

Estrela D’Oeste

• The railway would slash the cost of

shipping agricultural products to Panorama

Asia. Part of proposed

Twin Ocean route

• Critics worry that it would threaten

uncontacted Amazon tribes and the Chapeco

rainforest.3 Dashed lines =

planned railways

Rio Grande

Sources: (1) Ministério dos Transportes, 2014. (2) Lee, 2015; (3) Watts, 2015. (4) Ministério dos Transportes, via AgroIcone. 70You can also read