CAIRNHILL 16 AGENT SALES KIT - Not for circulation and not to send to consumers.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CAIRNHILL 16 AGENT SALES KIT

Not for circulation and not to send to consumers.

NAVIGATION

Project Info Location Vicinity Site Plan Schematic

Floor Plans Fittings Market Analysis Rental Analysis CMA

Limited Future CCR Resale VS No Oversupply ABSD Concerns

Freehold Supply Prices Trending New Launch In The Market

in District 9 Towards

$4000psf

2030: Double Orchard

The Price Masterplan

PROJECT INFO ß Back to navigation

• TSKY is a residential and mixed-use property developer in Singapore. As a JV

between industry veterans Tiong Seng and Ocean Sky, we are able to tap on

the expertise and experience of our parent companies as well as explore

better ways to design and build contemporary properties.

• When designing our properties, we always take the time to understand and

address how customer needs are changing. When building our properties, we

are able to always consider and evaluate new technology to create smart

spaces that work for people. With us, you will always enjoy properties with the

best of form and function.

ß Back to navigation

PROJECT INFO ß Back to navigation

PROJECT INFO ß Back to navigation

PROJECT TEAM ß Back to navigation

PROJECT INFO

Eco-luxury

Ecologically and socially responsible – prestigious Greenmark Gold Plus certification

Selection of environmentally friendly materials - Textured natural paint,

environmentally friendly Hybrid engineered wood flooring,

Green Initiatives – dedicated recycling chute, energy efficient fittings

Energy Efficient Fittings – LED lighting, energy efficient air conditioning system and applicances

Eco-friendly universal electric vehicle chargers for the residents to use

Curated artwork featured in the common spaces

ß Back to navigation

LOCATION ß Back to navigation

ß Back to navigation

CAIRNHILL ß Back to navigation

SCHOOLS

• Raffles Girls School

• Singapore Chinese Girls School

• ACS (Barker Road)

• ACS Junior

• River Valley Primary School

• St Margaret’s Primary School

ß Back to navigationMEDICAL

• Mount Elizabeth Hospital

• Paragon Medical Centre

ß Back to navigationTRANSPORT ß Back to navigation

SITE PLAN & FACILITIES ß Back to navigation

SITE PLAN

Common spaces/ facilities

The grand and lush entrance lobby at the first storey exudes

elegance and sophistication, welcoming the residents and guiding

them to the luxurious lift lobby.

Despite having a small site area, the landscape design for

Cairnhill Heights capitalizes on vertical greening with two

sky terraces and a landscaped roof top creating a landscape

experience which is magnified and makes the ground space feel

bigger than it is. A series of manicured geometric wave lines were

introduced onto the ground plane, breaking up the linearity of the

building architecture with parts of the groundscape disappearing

into the woods.

These lines were inspired by landforms displaying geometrically

repetitive movements and rhythmic folding patterns that slip and

slide. They are used to guide the forming of all landscape

components of the ground level, translating them into landscape

amenities such as swimming pool, water features, passageway,

planters, seatwalls, pavement patterns etc.

>40% landscape replacement area These amenities will cater to the diverse lifestyle aspirations of the

users and provide a holistic living environment for the residents.

ß Back to navigationSITE PLAN

Facilities - Ground floor

• Entrance drop-off featuring 16 water candles

as a strong focal and memorable physical address

for the development

• Lobby textured feature wall gives an illusion of

movement, which uplifts and inspires arrival.

• A 20m azure pool appears as it originates from the

woods, gently vanishing over an infinity edge beckoning

residents for a rejuvenating afternoon respite.

• An iconic 2-storey multipurpose pavilion with a feature

tree that overlooks to the pools and landscape

in the development.

• A kid’s pool with water bubblers.

• A long linear 3-4m tall green cage was proposed

creating a cosy, private secluded corner for a Jacuzzi

Pool with a trellis above it.

• Indoor gym – overlooking the landscape and pool.

ß Back to navigationSITE PLAN

2nd Storey Fitness Terrace

To allow users to enjoy fitness

activity in a natural setting, having a

holistic approach to wellness

ß Back to navigationSITE PLAN

7th Storey Reading Terrace

A landscape area with casual outdoor

furniture to allow users to Indulge and

contemplate in the surrounding greenery.

ß Back to navigationSITE PLAN

Roof Terrace

A Teppanyaki themed outdoor dining with refined facilities

such as a wine cooler/ fridge, electrical/ gas operating hot plate,

granite counter top with sink and adequate seating.

A BBQ charcoal grill themed outdoor dining experience with facilities

such as grill pit, granite countertop with sink and adequate seating.

Linear water feature with bubblers and undulating planters at the

background that give an upscale touch to the development as a point of interest.

ß Back to navigationSCHEMATIC DIAGRAM ß Back to navigation

SCHEMATIC DIAGRAM

• Private lift access for all units

• Unit layout – meticulously designed with efficient use of space

• Wide frontage – Living Dining areas side by side with flexibility for reconfiguration

• Daylighting – full height curtain wall wraps around the corner of bedrooms to offer wide view angles

• High Ceiling – 3.2 and 2.8 for all units. Additional height (4.2m and 2.8m) for 14th Storey units.

• Luxurious fittings – imported kitchen, luxury branded kitchen appliances, rose gold luxury branded

sanitary fittings, etc

• Balcony Customised / bespoke sunshading screens provided for Type CS and Type D units along

West facing façade (optional)

ß Back to navigationUNITS BREAKDOWN ß Back to navigation

FLOOR PLANS ß Back to navigation

FLOOR PLANS: 2 BEDROOM ß Back to navigation

FLOOR PLANS: 3 BEDROOM ß Back to navigation

FLOOR PLANS: 3 BEDROOM + STUDY ß Back to navigation

FLOOR PLANS: 4 BEDROOM ß Back to navigation

FITTINGS & FIXTURES ß Back to navigation

FITTINGS & FIXTURES ß Back to navigation

MARKET ANALYSIS ß Back to navigation

WHAT’S IN THE VICINITY ß Back to navigation

RENTAL ANALYSIS

The Peak @ Cityvista

Description The Vermont Hilltops Helios Residences Vida

Cairnhill Residences

Est. TOP 2014 2013 2011 2011 2010 2009

1 BR $2800 $3050 - - - $2700

2 BR - $4200 $7050 $6000 - $3600

3 BR - $6500 $9500 $7400 $6650 -

4 BR - $8100 $14000 $9500 $9000 -

Median PSF $5.30 $5.25 $7.15 $4.90 $3.50 $4.90

HIGHEST PSF $6 $7.40 $16.92 $6.12 $4.81 $7

Estimated rental from past transaction. Source: SRX

ß Back to navigationRENTAL ANALYSIS

Assumptive 2 BR 3 BR 3 BR 4 BR

PSF + Study

$6 Est $4650 Est $6330 Est $7750 Est $10,400

$7 Est $5425 Est $7385 Est $9000 Est $12,200

$8 Est $6200 Est $8440 Est $10,300 Est $13,900

ß Back to navigationKYC

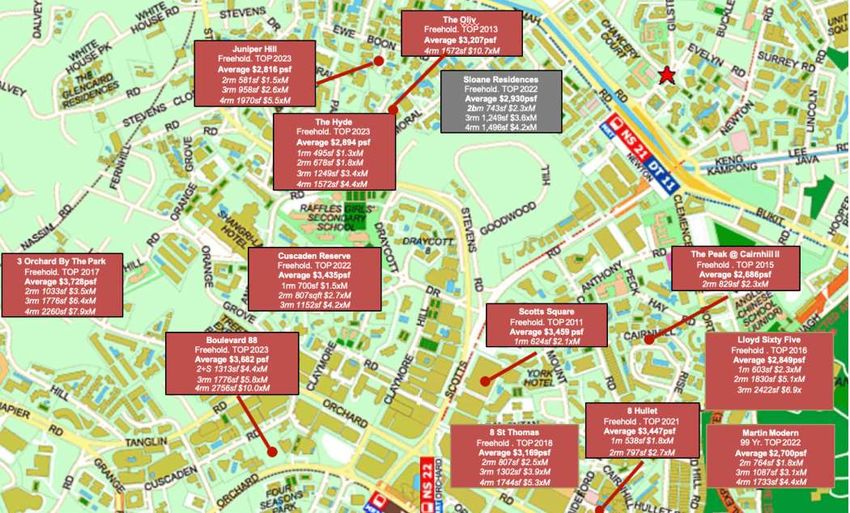

Dist Project Tenure Est TOP Total Unit 1rm Size 1rm Psf 1rm Quantum

9 Lloyd Sixtyfive ( TOP sales) FH 2016 76 603 $ 3,939 $ 2,375,000

9 8 Hullet FH 2021 44 538 $ 3,400 $ 1,829,200

9 The Scotts Tower (TOP Sales) 103yrs 2017 231 624 $ 3,425 $ 2,137,451

9 Scotts Square ( TOP sales) FH 2014 338 624 $ 3,525 $ 2,199,300

10 Fourth Ave Residences 99yrs 2022 476 484 $ 2,231 $ 1,080,000

10 Wilshire Residences FH 2013 85 463 $ 2,592 $ 1,200,000

10 Petit Jervois FH 2022 55 581 $ 2,754 $ 1,600,000

10 3 Cuscaden FH 2021 96 420 $ 3,733 $ 1,568,042

10 Cuscaden Reserve 99yrs 2022 192 700 $ 3,369 $ 2,358,000

10 The Hyde FH 2022 117 465 $ 2,802 $ 1,387,000

Dist Project Tenure Est TOP Total Unit 2rm Size 2rm Psf 2rm Quantum

9 Martin Modern 99yrs 2022 450 764 $ 2,596 $ 1,893,000

9 The Peak@Cairnhill II (TOP sales) FH 2015 60 829 $ 2,850 $ 2,363,000

9 Lloyd Sixtyfive ( TOP sales) FH 2016 76 1830 $ 3,011 $ 5,147,000

9 RV Altitude FH 2022 140 441 $ 3,256 $ 1,436,000

9 8 St Thomas ( TOP Sales) FH 2018 250 807 $ 3,173 $ 2,561,000

9 Hilltop Residences (TOP Sales) FH 2012 240 1335 $ 3,446 $ 5,000,000

9 8 Hullet FH 2021 44 797 $ 3,468 $ 2,764,293

9 The Scotts Tower (TOP Sales) 103yrs 2017 231 807 $ 3,716 $ 2,998,516

9 The Peak @ Cairnhill II (TOP Sales) FH 2015 60 829 $ 2,850 $ 2,363,000

10 Fourth Ave Residences 99yrs 2022 476 646 $ 2,195 $ 1,418,000

10 Wilshire Residences FH 2013 85 646 $ 2,554 $ 1,650,000

10 Juniper Hill FH 2022 115 581 $ 2,689 $ 1,592,000

10 3 Orchard By The Park ( TOP Sales) FH 2018 77 1066 $ 3,100 $ 3,305,000

10 120 Grange FH 2021 56 570 $ 3,242 $ 1,848,000

10 Boulevard 88 FH 2022 154 1313 $ 3,393 $ 4,455,000

10 Cuscaden Reserve 99yrs 2022 192 807 $ 3,423 $ 2,762,600

10 The Hyde FH 2022 117 678 $ 2,801 $.

1,899,000

Disclaimer: Prices are subjected to changes without notice, please confirm prices with respective projects IC. Last updated as of 11th Dec 2019

ß Back to navigationKYC

Dist Project Tenure Est TOP Total Unit 3rm Size 3rm Psf 3rm Quantum

9 Lloyd Sixtyfive ( TOP sales) FH 2016 76 2422 $ 2,889 $ 6,996,000

9 Martin Modern 99yrs 2022 450 1087 $ 2,860 $ 3,108,900

9 8 St Thomas ( TOP Sales) FH 2018 250 1302 $ 3,069 $ 3,996,000

9 Hilltop Residences (TOP Sales) FH 2012 240 1550 $ 3,548 $ 5,500,000

9 The Scotts Tower (TOP Sales) 103yrs 2017 231 1227 $ 3,829 $ 4,697,792

9 TwentyOne Angullia Park (TOP Sales) FH 2014 54 2260 $ 3,995 $ 9,028,000

10 Wilshire Residences FH 2013 85 840 $ 2,651 $ 2,227,000

10 Juniper Hill FH 2022 115 958 $ 2,730 $ 2,615,000

10 Boulevard 88 FH 2022 154 1776 $ 3,302 $ 5,864,000

10 Cuscaden Reserve 99yrs 2022 192 1152 $ 3,658 $ 4,214,000

10 The Hyde FH 2022 117 1,249 $ 2,799 $ 3,496,000

Dist Project Tenure Est TOP Total Unit 4rm Size 4rm Psf 4rm Quantum

9 Martin Modern 99yrs 2022 450 1733 $ 2,588 $ 4,485,000

9 8 St Thomas ( TOP Sales) FH 2018 250 1744 $ 3,174 $ 5,536,000

9 Hilltop Residences (TOP Sales) FH 2012 240 2465 $ 3,550 $ 8,750,000

9 The Ritz-Carlton Residences ( TOP sales) FH 2011 58 2831 $ 3,900 $ 11,040,000

9 Le Nouvel Ardmore (TOP Sales) FH 2014 43 3961 $ 4,494 $ 17,800,000

10 Wilshire Residences FH 2013 85 1270 $ 2,700 $ 3,430,400

10 The Oliv@Balmoral ( TOP sales) FH 2013 23 3337 $ 3,207 $ 10,700,000

10 Juniper Hill FH 2022 115 1970 $ 2,797 $ 5,511,000

10 White house Residence ( TOP sales) FH 2013 12 3100 $ 2,951 $ 9,149,400

10 3 Orchard By The Park ( TOP Sales) FH 2018 77 2260 $ 3,500 $ 7,910,000

10 Boulevard 88 FH 2022 154 2756 $ 3,651 $ 10,063,200

10 The Hyde FH 2022 117 1572 $ 2,799 $ 4,400,000

Disclaimer: Prices are subjected to changes without notice, please confirm prices with respective projects IC. Last updated as of 11th Dec 2019

ß Back to navigationCMA

Disclaimer: Prices are subjected to changes without notice, please confirm prices with respective projects IC. Last updated as of 11th Dec 2019

ß Back to navigationMARKET SENTIMENTS ß Back to navigation

ß Back to navigation

ß Back to navigation BUSINESS TIMES: 6 Jun 2019 Source: URA, ERA Research

GLS CONFIRMED LIST

Source: URA, ERA Research

ß Back to navigationTODAY: 11 AUG 2018 Source: URA, ERA Research

ß Back to navigationSource: URA, ERA Research ß Back to navigation

UPCOMING SUPPLY IN D9 & D10

Potential no. of

Location / Project Name Developer Land Cost (psf / ppr)

units

The Avenir 376 Hong Leong / Guocoland / Hong Realty $1,806

The Iveria (Riviera Point) 51 Macly Group $1,461

The Atelier (Makeway View) 154 Bukit Sembwang Estates $1,626

Hyll on Holland

179 FEC Properties $1,654 - $1,703

(The Estoril & Hollandia)

Van Holland (Toho Mansion) 97 Koh Brothers $1,805

15 Holland Hill (Olina Lodge) 128 Kheng Leong $1,712

Leedon Green (Tulip Gardens) 670 Yanlord / MCL Land $1,790

City Towers 190 Cheung Kong $1,847

One Holland Village 200+ Far East $1,888

Cairnhill 16 (Cairnhill Heights) 42 Tiong Seng / Ocean Sky $1,914

Cairnhill Mansions 200 Low Keng Huat $2,311

Eden 20 Swire Properties $2,526

14/14A Nassim Road 86 Shun Tak $2,744

Park House 120 Shun Tak $2,910

KOPAR @ Newton

435 CEL $1,192

Kampong Java Road (GLS)

Total 2,948+

Source: URA, ERA Research

ß Back to navigationß Back to navigation

SURGE IN LUXURY HOME SALES

>$3500PSF

Source: URA, ERA Research

ß Back to navigation“We have not seen those

numbers (of foreigners buying

super luxury homes in

Singapore) since the first

quarter of 2007.”

SCMP: 25 Sep 2019

Source: URA, ERA Research

ß Back to navigationUPCOMING PRICES TRENDING

TOWARDS $4000 PSF

$3136.97

The Avenir (D9, CS) $2,727.80

$1,806

$3,187.80

Crystal Tower (D10, CS) $2,772.00

$1,840

$3,198.27

City Towers (D10, CS) $2,781.10

$1,847

$3,259.56

One Holland (D10, GLS) $2,834.40

$1,888

Cairnhill Heights (D9, CS)

$3,494.28

$3,038.50

??

$2,045

$3,805.24

Royal Oak Residences (D10, CS) $3,308.90

$2,253

$3,893.44

Cairnhill Mansion (D9, CS) $3,385.60

$2,312

$3,990.62

Cuscaden Reserve (D10, GLS) $3,470.10

$2,377 $4,787.45

Park House (D10, CS) $4,163.00

$2,910

Est Selling $PSF Breakeven Price Sold

ß Back to navigation

Source: URA, ERA Researchß Back to navigation

DEVELOPER’S PRICING PHASE STRATEGY

First Mover Advantage

1) Developers will launch in phases

2) Prices will increase for every phase

ß Back to navigationß Back to navigation

New launch:

Approx $17xx psf

Resale:

Approx $13xx psf

ß Back to navigationNew launch:

Approx $22xx psf

Resale:

Approx $22xx psf

ß Back to navigationCONCLUSION

1. First-mover advantage

2. Newer facilities and more attractive features

3. Lower cost of maintenance and repairs

4. Wider range of unit choices

5. Prices will increase for every phase

ß Back to navigationCCR NEW LAUNCHES

RESALE CONDOS

44% PRICE GROWTH.

38% PRICE GROWTH.

New Launches median

price growth $531 psf

Resale Condos median price

growth $383 psf

Ave. size = 1,330 sqft

Price growth disparity

Source: URA, ERA Research and Consultancy

$196,840

ß Back to navigationCCR RESALE CASE STUDY:

THE SAIL (COMPLETED 2008)

Address Area (sqm) Transacted Unit Price ($psf) Sale Date

Price

2 Marina Boulevard 62 $1,274,000 Dec 2014

#1X-XX $1,792

2 Marina Boulevard 62 $1,368,000 $2,123 Feb 2019

#1X-XX

Profit: $94,000

Source: URA, ERA Research and Consultancy

ß Back to navigationCCR NEW LAUNCH CASE STUDY:

MARINA ONE RESIDENCES (LAUNCHED 2014)

Address Area (sqm) Transacted Unit Price ($psf) Sale Date

Price

21 Marina Way 65 $1,496,700 $2,139 Oct 2014

#1X-XX

21 Marina Way 65 $1,700,000 $2,430 Feb 2019

#1X-XX

Profit: $203,300

216% more than resale condo!

Source: URA, ERA Research and Consultancy

ß Back to navigationRCR NEW LAUNCHES

RESALE CONDOS

33% PRICE GROWTH.

28% PRICE GROWTH.

New Launches median

price growth $352 psf

Resale Condos median price

growth $197 psf

Ave. size = 1,050 sqft

Price growth disparity

$162,750

Source: URA, ERA Research and Consultancy

ß Back to navigationRCR RESALE CASE STUDY:

THE METROPOLITAN CONDOMINIUM (COMPLETED 2009)

Address Area (sqm) Transacted Unit Price ($psf) Sale Date

Price

8 Alexandra View 130 $1,870,000 $1,336 Oct 2014

#3X-XX

8 Alexandra View 130 $2,012,000 $1,438 Feb 2019

#3X-XX

Profit: $142,000

Source: URA, ERA Research and Consultancy

ß Back to navigationß Back to navigation

DEVELOPER’S TRACK RECORD

• Atra in D3

• Parc Emily in D9

• Hilltops in D9

• Wilkie Studio in D9

• The Wharf Residence in D9

• Volari @ Balmoral in D10

• Sloane Residences in D10

• The Panorama in D20

• Eco Sanctuary in D23

• …and many more

ß Back to navigationNO OVERSUPPLY IN THE MARKET ß Back to navigation

UNSOLD INVENTORY LEVELS

BELOW AVERAGE

35

ß Back to navigationUNSOLD INVENTORY WILL START FALLING AS

HOME SALES OUTPACE THE SHARP

SLOWDOWN IN LAND ACQUISITIONS.

3Q’18 Potential Supply low at ~45,000 compared to historical high of ~68,000 (2Q’11)

Assuming a 5y cycle, annual new units launch rate of ~9,000 units

80,000 160

Non-Landed Residential Units in the

URA Residential Price Index

70,000 140

60,000 120

50,000

100

40,000

Pipeline

80

30,000

60

20,000

10,000 40

0 20

Planned Private Resi & EC Units with and without Pre-requisites for sale and unsold Period URA Property Price Index

ß Back to navigationSHARP SLOWDOWN IN LAND

ACQUISITIONS

No more new projects Fewer new projects

from Enbloc Sales from GLS

ß Back to navigationPIPELINE SUPPLY ALREADY

STARTING TO DROP

Falling Pipeline Supply Fewer confirmed GLS list

(From En bloc & GLS) (Condo & EC)

ß Back to navigationPRIVATE HOUSING SUPPLY BELOW

HISTORICAL HIGH & SET TO FALL.

• Developers likely keep pricing firm and pace their launches for 2019

• 15y average annual new sales of ~12,200 units

• > than annual new launch rate of ~9,000 units

Uncompleted & Completed

25,000 $1,800

Private Residential Units

$1,600

20,000 $1,400

$1,200

15,000 $1,000

Sold

$800

10,000

$600

$400

5,000

$200

0 $0

New PrrivateHome Sales

Buying opportunities

Source: URA, ERA Research

ß Back to navigationABSD ß Back to navigation

ABSD IS HAPPENING EVERYWHERE

Hong Kong

30%

New South British

Wales Columbia

8% 20%

Highest ABSD Rate Singapore

for Foreigners 20%

United Toronto

Kingdom

15%

12%

Vancouver

15%

Source: Christie White Paper 2018, Wealth Seminar – Calvin Sin

ß Back to navigationSINGAPORE PROPERTY PRICES INCREASED

2.6X TO 3X IN LAST 15 YEARS!

$3,000

$2,500 CCR New Home Price PSF TRIPLED in last 15 years ($899psf - $2,704psf) – Fuelled by foreigner Demand

Median Price PSF

$2,000

RCR New Home Price PSF increased 2.8x in last 15 years ($615psf - $1,736psf)

$1,500

$1,000

$500

OCR New Home Price PSF increased 2.6x in last 15 years ($506psf - $1,331psf)

$0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018YTD

Period

OCR Median Price PSF RCR Median Price PSF CCR Median Price PSF

Source; URA, ERA Research

ß Back to navigationMORGAN STANLEY:

PROPERTY PRICE TO DOUBLE BY 2030

ß Back to navigation2017

(Morgan Stanley)

ß Back to navigationProperty prices is

forecast to rise by

5% each year on a

per square foot

(psf) basis from

2018 to 2030.

-Morgan Stanley

Source: Business Times, 14 Apr 2017

ß Back to navigationYear Price ($psf)

2017 $1,000.0

2018 $1,054.8

2019 $1,112.6

IN ORDER FOR PRIVATE 2020 $1,173.6

RESIDENTIAL PROPERTY 2021 $1,237.9

2022 $1,305.7

PRICE TO DOUBLE BY 2023 $1,377.3

2030, THERE MUST BE 2024 $1,452.7

2025 $1,532.4

5.48% P.A. GROWTH. 2026 $1,616.3

2027 $1,704.9

2028 $1,798.3

2029 $1,896.9

2030 $2,000.8

ß Back to navigationOVERALL PRIVATE PROPERTY PRICE INDEX HAS BEEN

ON UPTREND SINCE 2017

All residential properties price index

(exclude EC)

* Flash estimate

Source: URA, ERA Research & Consultancy

ß Back to navigationNATIONWIDE PRIVATE PROPERTY PRICE

ANNUAL GROWTH RATE > 5%

FOR YEAR 2018 & 2019

CCR RCR OCR

All Private Nationwide Non- Non- Non-

Residential* Non-landed* landed* landed* landed*

2018 + 7.9% + 8.3% + 6.7% + 7.4% + 9.4%

1Q - 3Q

2019 + 2.1% + 2.7% + 0.1% + 6.0% + 2.1%

*Note: Rate of annual growth of property price index

Source: URA, ERA Research & Consultancy

ß Back to navigationPRICES FOR NEW LAUNCHES

ARE CONSISTENTLY INCREASING IN PAST 5 YEARS

Median unit price ($psf) of New Launches

+1.9%

+12.0%

+4.0%

+8.1%

Source: URA, ERA Research & Consultancy

ß Back to navigationMEDIAN PRICES FOR NON-LANDED PROPERTIES IN ALL

MARKET SEGMENTS INCREASED > 5% LAST YEAR

+7.9%

+6.9%

+9.9%

Source: URA, ERA Research & Consultancy

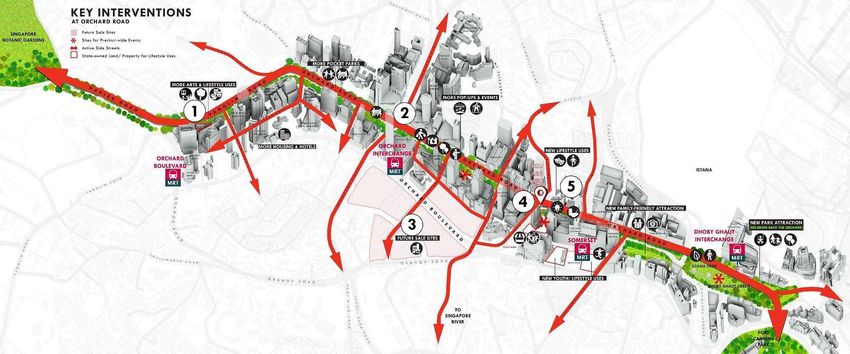

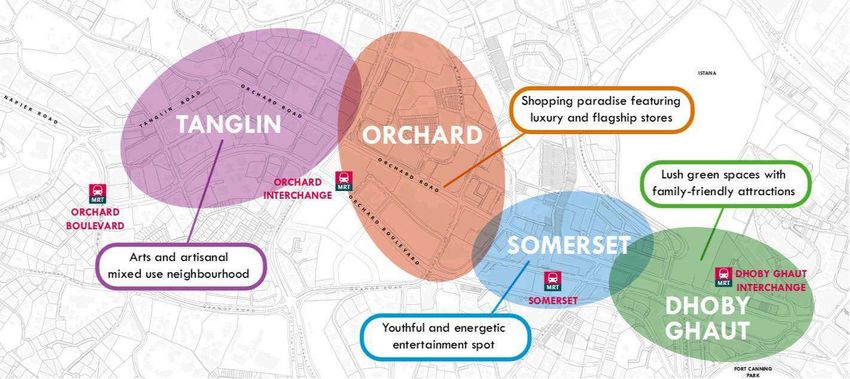

ß Back to navigationORCHARD MASTERPLAN ß Back to navigation

MP 2019 - ORCHARD • To transform Orchard Road into a lifestyle destination • Offer experiences to bring out the unique identity of its four sub-precincts - Tanglin, Orchard, Somerset and Dhoby Ghaut • There are opportunities to introduce new retail concepts, lifestyle attractions and events to enhance the unique experience of each sub-precinct. ß Back to navigation

MP 2019 - ORCHARD ß Back to navigation

NEW LIFESTYLE EXPERIENCE AT

TANGLIN

The conserved Tudor Court can

house a greater diversity of uses,

including arts and cultural

offerings. The covered canal

behind can be turned into an

attractive courtyard space

enlivened with public art and

outdoor dining, making it a focal

area for local residents and hotel

guests.

ß Back to navigationNEW MIXED USE DEVELOPMENTS AT

ORCHARD INTERCHANGE

The vacant State Land parcels at

Orchard Boulevard present

opportunities for exciting mixed-use

developments above the upcoming

Thomson-East Coast Line Orchard

Interchange MRT, which can also be

connected to Orchard Road via

bustling side streets.

Source: URA, ERA Research

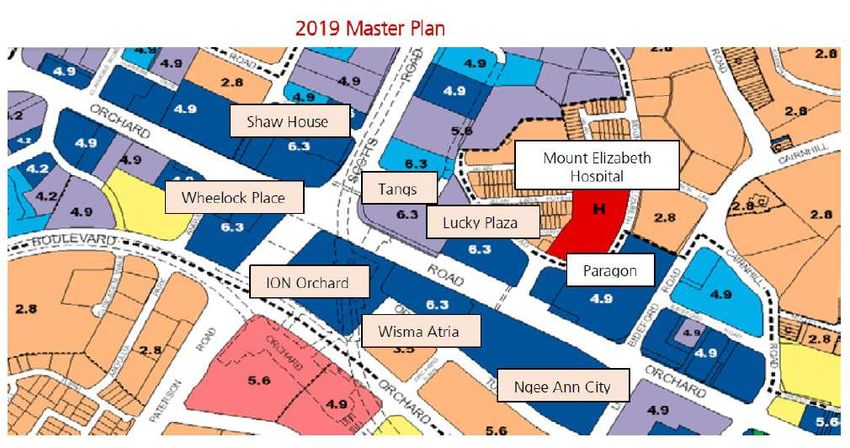

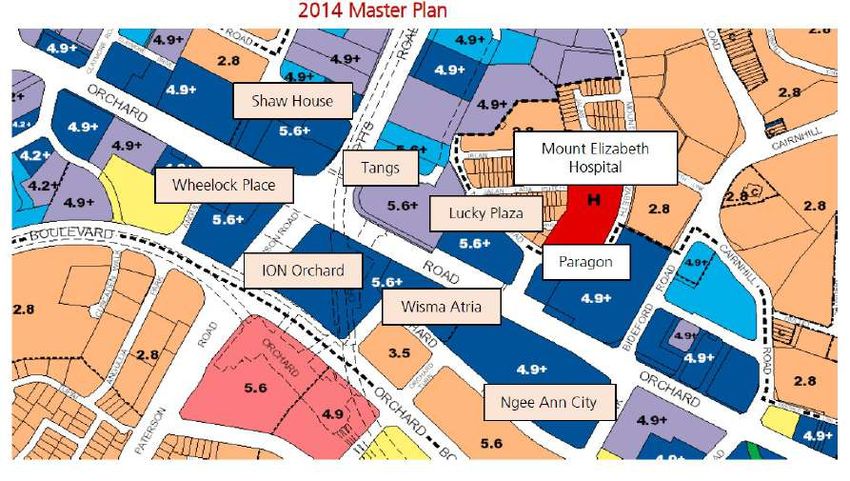

ß Back to navigationINCREASE IN PLOT RATIOS: ORCHARD

Source: URA, DBS, ERA Research

ß Back to navigationHIGHER REVISED PLOT RATIOS

– ORCHARD / SOMERSET / DHOBY GHAUT

Source: URA, DBS Bank, ERA Research

ß Back to navigationFUTURE MIXED-USE DEVELOPMENT

IN ORCHARD

• Housing – there will be a future mixed-use

development at the upcoming Thomson-East Coast

Line Orchard Interchange MRT station

ß Back to navigationMP 2019 - ORCHARD ß Back to navigation

MP 2019 - NEW EVENT SPACE AT SOMERSET

The car park at Grange Road

has hosted retail and F&B

events.

With rapid evolving trends and

demand for more events, the

car park can be transformed

into a dedicated events space

with dining and

entertainment to form a

cluster of lifestyle offerings

with the Design Orchard

showcase across the street.

ß Back to navigationMP 2019 - AN OASIS IN THE CITY AT

DHOBY GHAUT

Source: URA, ERA Research

The existing green open spaces above Dhoby Ghaut MRT station

provide respite from the hustle and bustle of Orchard Road.

The large mature trees, wide open spaces and pleasant shade stand in

contrast with the surrounding hotels and shopping malls

ß Back to navigationCONCLUSION

Wherever transformation is, it attracts

foreign and local investors’ attention.

More Attention = More Demand

ß Back to navigationYou can also read