BUILDING AN AFRICAN TRANSITIONAL ENERGY GROUP JULY 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BUILDING AN AFRICAN TRANSITIONAL ENERGY GROUP JULY 2021

Disclaimer and forward looking statements

These Presentation Materials do not constitute or form part of any invitation, offer for sale or subscription or any solicitation

for any offer to buy or subscribe for any securities in the Company nor shall they or any part of them form the basis of or be

relied upon in any manner or for any purpose whatsoever.

These Presentation Materials must not be used or relied upon for the purpose of making any investment decision or

engaging in an investment activity and any decision in connection with a purchase of shares in the Company must be

made solely on the basis of the publicly available information. Accordingly, neither the Company nor its directors makes

any representation or warranty in respect of the contents of the Presentation Materials.

The information contained in the Presentation Materials is subject to amendment, revision and updating in any way without

notice or liability to any party. The presentation materials contain forward-looking statements which involve risk and

uncertainties and actual results and developments may differ materially from those expressed or implied by these

statements depending on a variety of factors. All opinions expressed in these Presentation Materials are those solely of the

Company unless otherwise stated. No representation or warranty, express or implied, is made as to the fairness, accuracy

or completeness of the information or opinions contained herein, which have not been independently verified. The delivery

of these Presentation Materials shall not at any time or in any circumstance create any implication that there has been no

adverse change, or any event reasonably likely to involve any adverse change, in the condition (financial or otherwise) of

the Company since the date of these Presentation Materials.

The Presentation Materials are confidential and being supplied to you for your own information and may not be reproduced,

further distributed, passed on, or the contents otherwise divulged, directly or indirectly, to any other person (except the

recipient’s professional advisers) or published, in whole or in part, for any purpose whatsoever. The Presentation Materials

may not be used for the purpose of an offer or solicitation to subscribe for securities by anyone in any jurisdiction.

2

Executive Team

Adonis Pouroulis Julian Maurice-Williams Duncan Wallace Benoit Garrivier

Chief Executive Officer Chief Financial Officer Technical Director Transitional Power CEO

• One of the founders of • Chartered Accountant with • Geologist with 20 years of • 15 years of experience in

Chariot, has worked in the over 15 years of experience in experience in exploration and investment banking

sector for over 25 years the energy sector production • Structuring and carbon

business, dealing with large

• Influential in the founding, • Significant experience in • Successfully identified and utilities in Europe, China and

financing and growth of a financing, transactions and captured the Lixus Offshore Brazil

number of companies, listed markets area in Morocco

including Petra Diamonds • Founded iNca Energy in 2009,

• Previously with BDO LLP’s • Joined the board in July 2020 developing renewable energy

• Founder and chair of the Pella natural resources department projects in South Africa

Resources Group, an African totalling 330 MW of bid-ready

• Joined the board in July 2020 solar PV and 80 MW of bid-

focused natural resources and

energy group ready wind projects

• Co-founder of AEMP

• Member of the board since

IPO, CEO since July 2020

3

Building an African Transitional Energy Group

To create value and deliver positive change through investment in projects that are driving the energy revolution

Projected world population by world region Africa: Gross Domestic Product (US$)

WHY

AFRICA?

Asia

Africa ”Africa to propel

world’s population

towards 10bn by

2050”

Source: FT

Our Role

• Facilitates & balances shift to

renewables

• Reduces carbon footprint • Energy solution tailored for

• Promotes domestic self- Mining & Industry in Africa

sufficiency & energy security • Off grid remote locations

• Hybrid & renewables

• Environment • Strengthens social licence

• Local Communities to operate

• Employees

• Shareholders

Net NPV10* Pipeline

US$500m +500MW

4

Source: FT, UN, African Development Bank

*Internal estimate base case supported by audited 2C 361Bcf resource, 70mmscfd, 8-11$/mcf to power and industry

Positioned to Develop Energy Projects Across Africa

Moroccan offshore gas development with the potential to Renewable and hybrid energy project development in strategic

positively impact a growing economy, heavily reliant on partnership with Total-Eren, a leading player in renewable

energy imports and coal: energy, to serve mines in Africa:

• reduce carbon footprint • cleaner power generation / reducing carbon footprint

• promote energy self-sufficiency • reducing cost of energy supply

• catalyst for industrial growth • Africa’s largest hybrid solar plant on commissioning

• Operator 75% equity • right for up to 15% project equity in power projects

• Net NPV10* US$500m & IRR* > 30% • pipeline of projects +500MW equivalent to the Hoover Dam

Appraisal drilling Material Direct equity

unlocks the development Cashflows investment in projects

*Internal estimate base case supported by audited 2C 361Bcf resource, 70mmscfd, 8-11$/mcf to power and industry

5

Synergies & Scalability

c$1.5B +500 MW

2C Net Cash (Gross) pipeline

post-tax* equivalent to

Hoover Dam

c$500m 15 MW

2C Net

Essakane

NPV10*

(Gross)

Material upside Sub-Saharan total

beyond Anchois Chariot electricity supply,

development Portfolio Solar share

Chariot Historic

Interest

>3 Tcf Executives

Experience

1760 TWH

Morocco Solar 24%

Infrastructure- 2040**

led exploration

225 TWH

361 Bcf Solar 1%

Anchois 2C 2018**

Resource

*Internal estimate base case supported by audited 2C 361Bcf resource, 70mmscfd, 8-11$/mcf to power and industry

6

**Source: IEA, Africa Energy Outlook 2019, Electricity supply by type, source and scenario in sub-Saharan Africa

(excluding South Africa), 2018 and 2040

Transitional Gas: Anchois Gas Development

• Morocco is a premium SPAIN 2C Base Case

investment location with Pipelines

Net NPV10

world-class fiscal terms 1 Power Planned Pipelines

US$500m

3

Chariot 3D Seismic

• Growing power and 2 Industry IRR > 30%*

Rissana Offshore Existing CCGT

2

industrial demand 3 Spain (key terms agreed) Tangier

2C Base Case

1

underpin attractive local Lixus Offshore

Up to US$200m

markets Annual Revenue*

ALGERIA

• Favourably located with Anchois project

existing gas

SDX ConocoPhillips

Predator

Morocco Gas

infrastructure and for Market MOU from

RSD-1 1 Moroccan

export to Spain Kenitra

2

1 Government

• 75% equity & operator RABAT

1

10 Year Corporate

• Anchois has material gas 2 Mohammedia Sound

Tax Holiday

MOROCCO

2

Repsol

resources, low Casablanca

subsurface risk and can Access to

be developed through European

PORTFOLIO, GAS INFRASTRUCTURE & GAS

conventional technology MARKET OPTIONALITY Gas Market

ESG & Sustainability at Anchois

Reduction of 360,000 Morocco Power Consumption & GDP Growth Morocco Power Generation by Fuel in 2019

1990 to 2018 (40 TWh Total)

tonnes CO2 per year** 2000 Morocco Egypt Algeria

4% 16%

>90% of all primary 1500

KWh/Capita

energy imported 1000

12%

500 67%

Gas to fuel Industry & 1%

Economic Growth 0

2000 7000 12000 17000 Coal Oil Gas Hydro Renewables

GDP (PPP $US)/Capita

7

Sources: IEA, ONEE, BP Energy Statistical Review, Gas Strategies, ONHYM, WLPGA

*Internal estimate base case supported by audited 2C 361Bcf resource, 70mmscfd, 8-11$/mcf to power and industry

**Replacement of 300 MW of coal power generation with gas (c.50 mmscfd) using EIA estimate of 0.05 vs 0.09 tonnes of carbon per mmbtu (gas vs coal)

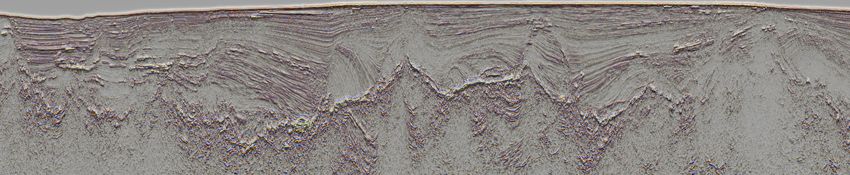

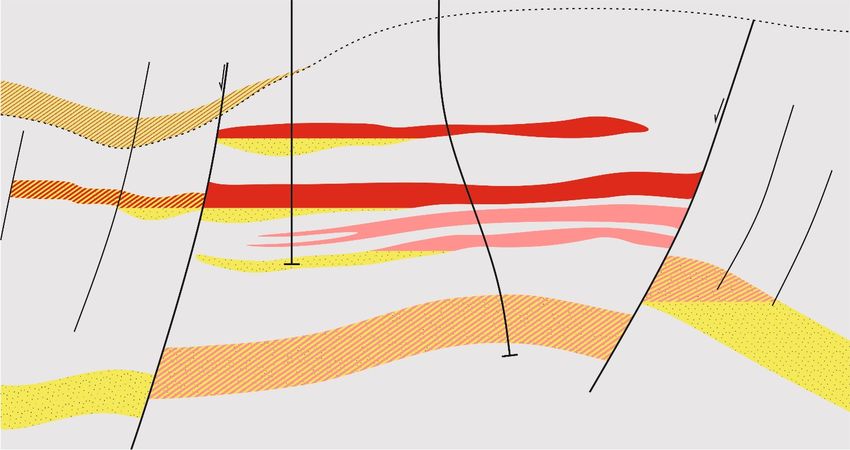

Transitional Gas: Appraisal Well – Unlocking the Development

Anchois-1 Potential

PLIOCENE Discovery Appraisal Well

A Sands Excellent Quality 2020

Well Location Reprocessed 3D

B Sands

MIOCENE Seismic Data

Plie prospect

A Sand 115 Bcf High Reservoir Porosity

C, M & O & Permeability

A&B Sand

Appraisal

+128 Bcf B Sand 247 Bcf well High Quality Gas

97% Methane

No CO2 / H2S

Gas in ANCHOIS

well

Gas identified in C&M Sands FOOTWALL

ANCHOIS Exploration

185 Bcf PROSPECT Minimum

0

additional fault deepening Maximum 4.0 km2

blocks DEEP 8.7 km2

Water-bearing, good

quality M sand

PROSPECT

-ve

O Sand 147 Bcf

Anchois-1

O Sand 358 Bcf

CONTINGENT RESOURCES PROSPECTIVE RESOURCES

Proven fault block Additional fault Low risk: gas/reservoir Exploration prospects in PSDM (CHARIOT 2020)

(1C & 2C) blocks (~3C) proven by Anchois-1 (2U) undrilled, O Sand (2U)

1,800 Contingent Prospective

Target to drill appraisal well in 1,600

Q4 2021 - close to discovery 1,400

well 1,200 Capitalising on low rig rates

1,000

Bcf

Re-confirm and test existing

800

Appraisal well to progress

600

discovery, very low risk 400 gas sales agreements and

200 project finance

-

Potential upside with drilling of 1C/1U 2C/2U 3C/3U

deeper low risk gas sands, Appraisal well to be

audited chance of success 2C RESOURCE 2U RESOURCE suspended as producer

up to 64% 361 BCF 60 690 Bcf

MMBOE 115 MMboe

8

Sources: Estimates of Gross Contingent & Prospective Resources from NSAI Independent Resource Assessment 2020

Transitional Gas: Anchois Gas Development

SUBSEA-TO-SHORE DEVELOPMENT Engineering

• Simple & standard construction

& development

• Pre-FEED completed

• Development collaboration

agreement signed with market

leading gas developers

Onshore Central

Processing Facility

2C Development 2C Development

Gas Flowline

70 mmscfd Capex US$300m

Future Drilling & Control Umbilical >30% IRR* Repaid in

Transitional Gas: Material Upside Beyond Anchois Development

Lixus Mio-Pliocene Portfolio 2C/2U (Bcf)

3D PSDM

LIXUS

coverage

OFFSHORE 5,000 Rissana

Offshore

4,500 ~8,476 sq km

Maquereau

West 4,000

Maquereau

Merluche North 3,500

Anchois

Maquereau Discovery

Central 3,000

Maquereau

South 2,500

2,000 Lixus Offshore

Oursin ~2,390 sq km

Plie Turbot Pageot

Anchois 1,500

Crevette 1,000

Espadon Meduse 500

Moule St Pierre Kenitra

-

Tombe

Anchois Gas Chariot

Discovery (CR/PR) Prospects Anguille Rabat

Anchois Satellite Lead

Prospects (post-Nappe)

Other Lixus Lead

Prospects (sub-Nappe) Casablanca

LIXUS LICENCE GAS DISCOVERY

LIXUS 2C / 2U RESOURCES (BCF) RISSANA LICENCE

AND PROSPECTS

2C+2U 3 Tcf 3.5 x Area of Lixus

Further material gas sands in Lixus Licence

0.5 billion boe

licence – similar seismic attributes to Low Commitment

discovery Captured further prospective

acreage in Rissana Licence 1,000km 2D Seismic

10

Sources: * Estimates of Gross Contingent & Prospective Resources from NSAI Independent Resource Assessment 2020 & 2019 and Internal Company Estimates

**Estimates of Gross Prospective Resources from NSAI Independent Resource Assessment 2018 on former Mohammedia & Kenitra licences

+ Subject to Award of Rissana Offshore licenceTransitional Power: Rationale for Acquisition of New Business

Looking to harness network to increase

SPA Signed in March 2021 for pipeline of projects

Purchase of AEMP

Group – Renewable and Hybrid

Developer for Mines in Africa

Consideration $2 Million in

Share Capital

✓ Joint Venture with

✓ Right for up to 15% Project Equity

✓ 500 MW Pipeline of Mining Projects

✓ Experienced Team

✓ Successfully Completed 1st Solar Existing project

Hybrid Project for Gold Mine

Pipeline Project

✓ Chariot Network = Additional Pipeline

Business Interest

of Management

11Transitional Power: Scalability, Leverage & Returns

Current Pipeline Example: 50 MW Solar Project***

SIZE OF PRIZE

500 MW equivalent electricity

production of the Hoover Dam

20 GW equivalent to c.50% of annual

70% 30% 85%

UK electricity consumption Debt Equity

Recent comparable 15%

transaction values renewable

electricity projects at • Target returns > 15% ROE

c.$1.8million per MW** • c.US$50 M Capex

• Take or Pay Long Term contracts = low

• Chariot’s equity risk

share = c.US$2 M

+20 GW*

Sub Saharan Africa mining

• Additional revenues earned from

management & on project completion

power demand 2020 Conveyor belt of projects

Commencement of construction

500 MW

Target

Dec 21 Dec 22

Revenues 6-9 months from signing

Sources:*World Bank

12

**https://www.total.com/media/news/press-releases/total-farms-down-2-portfolios-of-renewable-assets-in-France

***Internal estimate, representative project size, assumed US$1M / MW capex,Transitional Power: Existing Operations

Essakane Solar 15 MW Solar

• Largest hybrid PV-HFO plant in Africa and one of the largest Generation

in the world 130,000

• Together with Total Eren, AEMP has successfully developed, PV Panels

financed and built, and now operates, a 15 MW solar PV

Commenced

plant coupled with a 57 MW HFO power plant for operations

IAMGOLD's Essakane mine in Burkina Faso 2018

• AEMP holds equity of 10% in project

DEVELOPMENT CONSTRUCTION OPERATION &

SCOPING FINANCING

UNCERTAINTIES MAINTENANCE

ESG & Sustainability at Essakane

6 million Reduction of 100% of ongoing

2019 TSM

litres fuel saved 18,500 tons CO2 project staff are

Environmental

per year per year nationals

Excellence

Award

Supplies off-grid gold 1% of project Carbon credits registered

mine with competitive revenues dedicated with UN - funding of

and carbon-free to community additional community

electricity investment projects

13Timeline & Value Triggers

Additional Gas Prospectivity / 3Tcf Lixus & Rissana upside

Strategic Partnering APPRAISAL Strategic Partnering FIRST

FID

DRILLING GAS

Anchois 361Bcf Unlocked

FEED Debt

Finance

Drilling Rig Gas Sales Reserves Gas Sales CONSTRUCTION

Signed MoUs Report Agreements

v v v v v v v v v v

2021 2022 2024

Essakane Operating

AEMP

COMPLETES CONSTRUCTION Operating

NEXT

PROJECT

SIGNED CONSTRUCTION Operating

ADDITIONAL

PROJECT

SIGNED

Additional Projects / 500+ MW Project Pipeline

14Highlights – Significant Value Upside

● Unique & ● Transitional Gas ● Transitional ● Scale & Synergy ● Team & Network

Sustainable High Value Gas Power ◆ 7 X Upside in 2U Gas ◆ Team with Proven

African Development in Clean Power for Resource Record of Project

Transitional Morocco ◆ 500MW+ Pipeline of Delivery

Mining & Industry

1

Energy Group ◆ Net NPV10 Power Projects ◆ Continent Wide

◆ Strategic Partner

◆ Negative Net

US$500m* ◆ Synergies Inception Business Interest &

◆ High Return

CO2 Projects ◆ Project Finance to Completion Network

Project Portfolio

◆ Delivering

& Developers ◆ Investment in Other

Positive Impact Transition Energy

Highlights

2

◆ Acquisition of Transitional Power completion

◆ Appraisal drilling targeting Q4 2021 ◆ Subsequent power projects:

● Signing

◆ Potential reserves upgrade

◆ Gas sales agreements ● Construction

◆ Project finance ● Operation

◆ FID & development ◆ Further signing of pipeline

Upcoming ◆ Other transitional energy projects

Catalysts

*Internal estimate base case supported by audited 2C 361Bcf resource, 70mmscfd, 8-11$/mcf to power and industry

15Mission & Principles

Mission To create value and deliver positive change through investment

in projects that are driving the energy revolution

Values

Positive Impact:

• Environment

• Local Communities

• Employees

• Shareholders

Collaboration

• Mutual Benefit

• Balance

• Knowledge Growth

Integrity

• Technical Excellence

• Trusted

• Transparent

Pioneering

• Enterprising

• Agile

• Challenge Convention

Respect:

• Engagement

• Honesty

• Culture

16APPENDICES

Management Team

Julian Maurice-Williams Adonis Pouroulis Duncan Wallace

Chief Financial Officer Chief Executive Officer Technical Director

Benoit Garrivier Pierre Raillard Laurent Coche David Brecknock

Transitional Power CEO Head of Gas & Morocco Business Development, Drilling Manager

• 15 years of experience in Country Director Transitional Power • 22 years experience

investment banking • Over 25 years’ operational and • Over 20 years’ experience in • Expert deepwater drilling manager

• Structuring and carbon business, management experience in energy international development sector

dealing with large utilities in industry, specific expertise in the and sustainability, public and • Managed deepwater and ultra-

Europe, China and Brazil development of natural gas private sector across Africa deepwater drilling operations in

projects in Africa Morocco, Brazil, Cote d’Ivoire,

• Founded iNca Energy in 2009, • Senior VP Sustainability (Africa) for

developing renewable energy • Previously Orca Energy Group, AngloGold Ashanti Gabon and Egypt

projects in South Africa totalling Head of Business Development. • Managed Chariot’s 2018

• Previously led large-scale energy

330 MW of bid-ready solar PV and Key role in development of Songo

programmes for the UNDP in East campaign

80 MW of bid-ready wind projects Songo gas field, located offshore

and Western Africa for over a

Tanzania, which is analogous to

• Co-founder of AEMP Chariot’s Anchois gas project

decade

• Co-founder of AEMP

• Held leadership roles at African

Petroleum Corporation, Perenco

and OneLNG

18Non Executive Directors

George Canjar Robert Sinclair Chris Zeal Andrew Hockey

Non-executive Chairman Non-executive Director Non-executive Director Non-executive Director

• Over 40 years with Shell, • Over 52 years’ experience in • Over 30 years’ experience • Over 35 years’ experience in

Carrizo, Davis Petroleum and finance as a Chartered across a wide range of sectors the oil & gas industry, with

Hess supervising exploration, Accountant, of which over 42 and retained by over 20 specific expertise in the

development and engineering have been spent in the FTSE100 companies including development and production of

projects. Global experience Guernsey financial services British Gas, Cairn Energy and gas assets in the UKCS sector

from offshore SE Asia to North industry Tullow Oil

American onshore. • Founder & NED of Fairfield

• Formerly Managing Director of • Previously Managing Director Energy Ltd and previous

• Broad functional experience Artemis Trustees Limited, a at Jefferies Hoare Govett ( a experience with Eni, Fina,

across the E&P sector with Guernsey-based fiduciary division of Jefferies Inc.) LASMO, Triton Energy and

specific expertise in deal services group specialising in corporate Monument

structuring, risk analysis, broking and investment

strategic modelling and finance • Extensive experience of banking • Currently CEO of Independent

offshore trusts and corporate Oil & Gas, a UK-based

• Currently focused on entities and financial planning • Director at Ventus 2 VCT plc, a Development and Production

transitional energy solutions for both individuals and company invested in Operator with assets in the

including natural gas, corporations renewable energy Companies Southern North Sea gas basin

renewables and battery in the UK

solutions.

19Transitional Power: Partner Information

Total Eren is an Independent Power Producer which develops, finances, builds and operates

over the long-term renewable energy power plants globally.

2012 - founded by Pâris Mouratoglou and David Corchia

Shareholders 2019 %

2015 - €195 million capital increase from a diversified consortium of financial Eren Groupe Majority

investors

Total S.A 30%

2017 - Total S.A. acquires an indirect interest in EREN RE by subscribing to a Bpifrance 12.3%

capital increase of €237.5 million. EREN RE changes its name to Total Eren.

Tikehau Capital and FFP 7%

2019 - Total Eren acquires NovEnergia. Total S.A. increases its stake in Total Next World Group 4.4%

Eren to reach a total of almost 30% (directly and indirectly).

Key Figures

>€320 million in 100 power >3,300MW gross >2,000MW gross

revenue 2019 (including plants in operation capacity of renewable capacity of projects under

newly acquired energy assets in operation development

or under construction

NovEnergia’s revenue) or under construction

in 18 countries

>€1 billion in >450 >3,600 GWh of 5GW Global gross

equity capital (Dec 2019) installed capacity targeted

employees in electricity generated in

2020 by 2022

France and worldwide

20

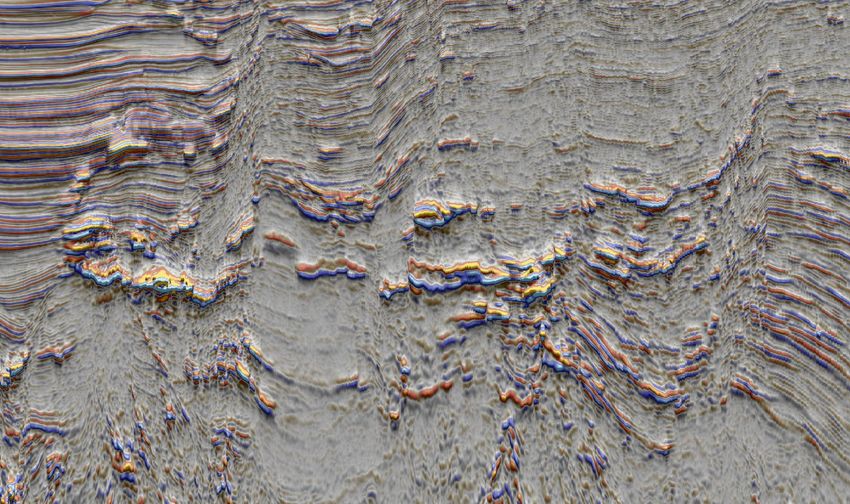

Sources: https://www.total-eren.com/en/in-brief/Lixus Offshore Prospects & Leads – 2020 PSDM

A B

Nappe

Nappe

Mud/Salt

Diapir

Sub-Nappe Prospectivity

Anchois Mini-Basin Pliocene & Miocene Anchois Satellite Prospects

LIXUS

3D PSDM OFFSHORE

coverage

5-10km from Anchois, with same

reservoir and attributes

Mio/Plio U/C B

2019 PSTM evaluation 600 Bcf*

A A

Other Lixus Prospects

B

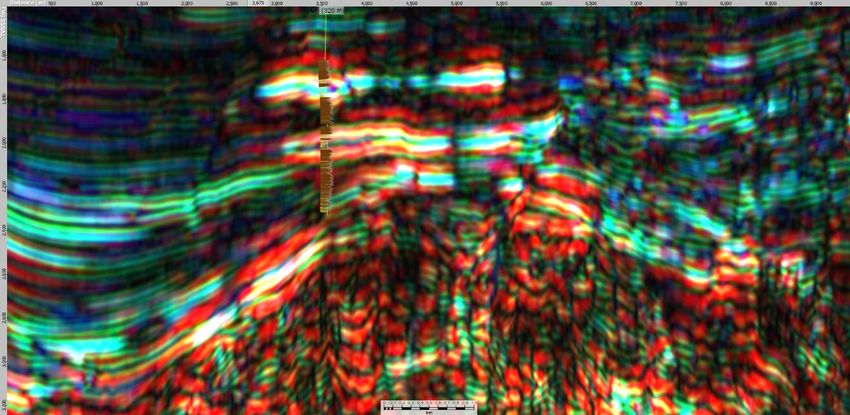

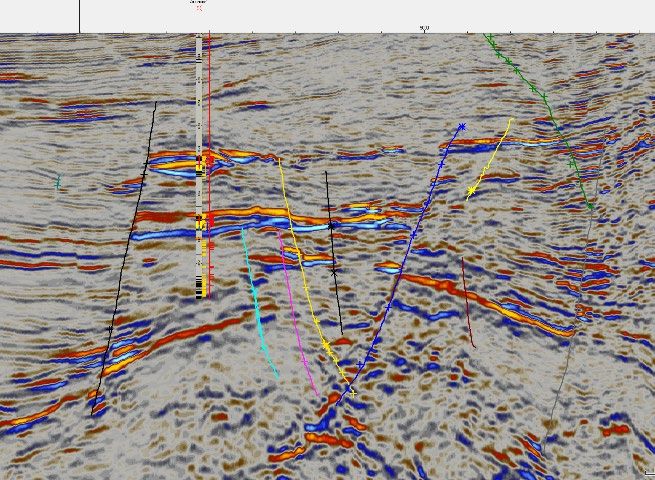

A Shallower water of 70 toAnchois Field – PSDM Interpretation, Resources & Appraisal

Anchois-1 Legacy PSTM Anchois-1 New PSDM Anchois Discovery – B Sand

Increase in A & B resources

Improved mapping of gas sands

Identification of new targets

A Sands

A Sands

Anchois-1

B Sands

B Sands 3.2 to 4.8 km2

PSTM (2010)

Maximum Minimum

C Sands O Sands 4.0 km2

0

C Sands 8.7 km2

M Sands

(Water-

Wet)

-ve

Footwall Anchois-1

Prospect: New

O Sands

Target

PSDM (CHARIOT 2020)

Candidate Appraisal Location Anchois – Resources & New Target Sands

Anchois-1

Anchois-1 Anchois Footwall

2020 KPSDM

Spectral Low Frequency Gas- Prospect

Decomposition Bearing Response

RGB Display 114 Bcf

A GWC 2C Resources 361 Bcf

247 Bcf

B GWC

A Sands

C & M 185 Bcf

GWC O GWC

Water-Bearing

Response 147 Bcf

B Sands

O GWC

358 Bcf 2U Resources 690 Bcf

Frequency (Hz)

Thin gas 5

Top Nappe

pay

25 15

C, M &

O Sands Reprocessed seismic data improvements and new interpretation techniques,

such as spectral decomposition, have identified additional undrilled gas sands

C & M Sands are equivalent to gas pay and reservoir proven in the Anchois-1 well

M Sands (Water-Wet)

O Sands comprise two targets below Anchois-1 TD and in adjacent fault block

22

Sources: Estimates of Gross Best Estimate Contingent & Prospective Resources from NSAI Independent Resource Assessment 2020Anchois Development & Production Growth Analogues

Cassiopea-Argo, Sicily Channel Poseidon, Gulf of Cadiz Corrib, NW Ireland

• ENI Operated • Repsol Operated • Vermillion Operated (developed by Shell)

• >600 Bcf Resources • 150 Bcf Resources • 600 Bcf Resources

• 5-600m WD, 60km flowline, 5 wells • 75-150m WD, 30km offshore • 350m WD, 80km offshore

• Development ongoing, 600 M$ CAPEX • Peak production 51 mmscfd in 2002 • CPF capacity 260 mmscfd

• Peak production 200 mmscfd

Anchois development plan uses well-established industry technology, with multiple international analogues

Tanzania Ivory Coast Egypt

Historical Gas Production & Consumption Historical Gas Production & Consumption Historical Gas Production & Consumption

350 300 7000

300 250 6000

250 5000

200

200 4000

MMscfd

MMscfd

MMscfd

150

150 3000

100

100 2000

50 50 1000

0 0 0

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Production (MMscfd) Consumption (MMscfd) Growth Production (MMscfd) Consumption (MMscfd) Growth Production (MMscfd) Consumption (MMscfd) Growth

Evidence from other African countries with developed gas resources demonstrates that once in production, internal gas markets

(both industrial and power) develop to exploit that resource with strong growth in gas production.

23Lixus Offshore: Independent Resource Assessment

Contingent Gas resources* (Bcf)

Probability of

Prospective Gas resources (Bcf)

Field / Prospect Geologic Success

1C* 2C* 3C* Mean (Pg)

1U 2U 3U Mean

Anchois Discovery

Anchois A sand* 65 114 175 117 N/A

Anchois B sand* 136 247 375 252 N/A

Anchois Contingent Resource* 201 361 550 369 N/A

Anchois Prospective

Anchois Deep (C sand) 60 164 284 168 64%

Anchois Deep (M sand) 9 21 36 22 38%

Anchois Deep (O sand) 225 358 481 362 37%

Anchois Footwall (O sand) 90 147 212 149 46%

Anchois Remaining Recoverable Resource 585 1051 1563 1070

Anchois Satellites

Anchois N 140 308 492 297 43%

Anchois W 45 89 134 86 35%

Anchois NW 10 29 51 28 34%

Anchois SW 42 101 165 98 28%

Anchois WSW 22 61 110 60 23%

Sub total 259 588 952 569

Additional Lixus Prospects

Maquereau N 91 311 628 311 25%

Maquereau C 73 267 559 276 25%

Maquereau S 59 205 432 216 23%

Tombe 60 154 280 153 19%

Turbot 38 281 709 303 16%

Sub total 321 1218 2608 1259

Total Remaining Recoverable Resource 1165 2857 5123 2898

24

Source: Estimates of Gross Contingent & Prospective Resources from NSAI Independent Resource Assessment 2019, 2020Morocco

Exploitation Concession

25 years 31% corporate 10 year corporate

(extendable tax after 10 year tax holiday

by 10 years) tax holiday no taxation of profits in

first 10 years of

production

3.5% royalty applies Royalty, rental, training, exploration,

to gas from Anchois production and bonus expenditures

(>200m water depth) are all tax deductible

Key Figures

Morocco Energy Consumption and GDP Growth (2000 to 2017)

• GDP: US$119.7 billion; Annual Growth 2.5%

• Population 36.4 million; Inflation 1.1% (2018) 1,000

• Major Industries: automotive parts, phosphate 800

mining and processing, aerospace, food processing,

kWh/capita

600

leather goods, textiles, construction, energy, tourism. 400

• Constitutional monarchy; Robust Economy; Good 200

Trade Relations 0

4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500 8,000

• Country risk profile: BBB- GDP/capita

25

Sources: https://data.worldbank.org, https://www.cia.gov/the-world-factbook/, IEA.Corporate Snapshot

Market Statistics

Listing AIM, London

Ticker Symbol CHAR

Issued Shares (at 23 July 2021) 636,723,079

Share Price (at 23 July 2021) 5.70p

Market Capitalisation (at 23 July 2021) US$50m

Total Director / Employee share awards (at 31

10,241,655

December 2020)

26You can also read