Autotech Seminar October 6, 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Autotech Seminar

October 6, 2021

REDEYE AUTOTECH SEMINAR - 2021

1

w

AGENDA AUTOTECH SEMINAR 2021

09:00 Introduction Redeye – Erik Rolander, Corporate Advisory

09:03 Redeye Autotech Report – Jesper Henrikson Equity Research

Block 1 Electrification

09:10 Polestar – Dennis Nobelius, COO

09:20 Garo – Patrik Andersson, CEO

09:30 Zaptec – Anders Thingbø, CEO

09:40 ChargeNode – Kristian Sandahl, CEO

09:50 Charge Amps – Anders Bergtoft, CEO

10:00 Paneldiscussions

10:25 Pause

Block 2 Autonomous Driving

10:35 Klimator – Rebecca Lewis-Lück, COO

10:45 Terranet – Pär-Olof Johannesson, CEO

10:55 Gapwaves – Lars-Inge Sjöqvist, CEO

11:05 Paneldiscussions

Block 3 Driver monitoring and safety

11:25 Smarteye – Martin Krantz CEO, Anders Lyrheden CFO

11:35 Acconeer – Lars Lindell, CEO

11:45 - 12:00 Paneldiscussions

REDEYE AUTOTECH SEMINAR - 2021

2

w

THE REDEYE TECHNOLOGY TEAM

Erik Kramming

Client Manager & Head of Technology

Erik has a Master of Science in finance from Stockholm University. His previous work has included a position

at Handelsbanken Capital Markets. At Redeye, Erik works with Corporate Broking for the Technology team.

Greger Johansson

Client Manager & Co-head Technology

Greger has a background from the telecom industry, both from large companies as well as from entrepreneurial

companies in Sweden (Telia and Ericsson) and USA (Metricom). He also spent 15+ years in investment banking

(Nordea and Redeye). Furthermore, at Redeye Greger advise growth companies within the technology sector

on financing, equity storytelling and getting the right shareholders/investors (Corporate Broking). Coder for two

published C64-games. M.Sc.EE and M.Sc.Econ.

Johan Ekström

Client Manager

Johan has a Master of Science in finance from the Stockholm School of Economics, and has studied e-com-

merce and marketing at the MBA Haas School of Business, University of California, Berkeley. Johan has worked

as an equity portfolio manager at Alfa Bank and Gazprombank in Moscow, as a hedge fund manager at EME

Partners, and as an analyst and portfolio manager at Swedbank Robur. At Redeye, Johan works in the Corporate

Broking team with fundamental analysis and advisory in the tech sector.

Erik Rolander

Client Manager

Erik has a Master’s degree in finance from Linköpings Universitet. He has previously worked at Remium as a

tech analyst and product manager for the equity research platform Introduce.se, which today is owned by ABG

Sundal Collier. At Redeye, Erik works with Corporate Broking for the Technology team.

Niklas Blumenthal

Client Manager

Niklas has studied business administration at Uppsala University and has over 20 years of experience in the

financial market. He has previously worked as client manager at Nordnet, CMC Markets, Remium and ABG

Sundal Collier. At Redeye, Niklas works with Corporate Broking in both Technology and Life Science teams.

Gustav Olin Månsson

Client Manager

Gustav has a Master’s degree in business administration from Karlstad University. He has previously

worked at PwC as an auditor towards listed entities. At Redeye, Gustav works with Corporate Broking for

the Technology team.

REDEYE AUTOTECH SEMINAR - 2021

3THE REDEYE TECHNOLOGY TEAM

Tomas Otterbeck

Head of Research

Tomas gained a Master’s degree in Business and Economics at Stockholm University. He also studied

Computing and Systems Science at the KTH Royal Institute of Technology. Tomas was previously responsible

for Redeye’s website for six years, during which time he developed its blog and community and was editor of its

digital stock exchange journal, Trends. Tomas also worked as a Business Intelligence consultant for over two

years.

Henrik Alveskog

Analyst

Henrik has an MBA from Stockholm University. He started his career in the industry in the mid-1990s.

After working for a couple of investment banks he came to Redeye, where he has celebrated 10 years

as an analyst.

Mattias Ehrenborg

Analyst

Mattias is an equity analyst within Redeye’s technology team, focusing on the renewable energy & cleantech

sector. He holds a BSc in Business and Economics from Uppsala University. Mattias has previously worked at

ABG Sundal Collier as a part of the Capital Goods team, primarily focusing on the renewable energy & cleantech

sector.

Douglas Forsling

Analyst

Douglas is an equity analyst in the technology team with a focus on the online gambling sector and fintech sec-

tor. He holds a Bachelor’s degree in finance and an unfinished Master’s degree in Operational Management and

Control from Stockholm University, School of Business. In addition, he has studied abroad in Hong Kong, Beijing,

and Oxford. He has had positions in SEB, Nordic Capital, and Danone. He has also produced a finance podcast

for nearly two years.

Forbes Goldman

Analyst

Forbes is an equity analyst within the technology team at Redeye. He holds a BSc in Business and

Economics from the Stockholm School of Economics and has also completed an academic exchange

semester in Mexico City.

Jesper Henrikson

Analyst

Jesper is an equity analyst in the technology team with a focus on telecom, automotive tech and more. He

holds a Master’s degree in Industrial Engineering and Management from Lund University, institute of technol-

ogy. In addition, he has studied abroad in Madrid. He has previously worked as an entrepreneur, management

consultant and business development manager at a B2B SaaS company. He has also run a stock-research blog

for nearly five years.

Mats Hyttinge

Analyst

Mats is an equity analyst in the technology & life science team at Redeye. He has an MBA and Bachelor degree

in Finance from USE in Monaco.

REDEYE AUTOTECH SEMINAR - 2021

4THE REDEYE TECHNOLOGY TEAM

Fredrik Nilsson

Analyst

Fredrik is an equity analyst within Redeye’s technology team. He has an MSc in Finance from

University of Gothenburg and has previously worked as a tech-focused equity analyst at Remium.

Mark Siöstedt

Analyst

Mark has a Master’s degree in Accounting and Finance from Lund University. He has a dual role within

Redeye as an editor (quality assurance and Top Picks) and as an equity analyst on the technology team.

Danesh Zare

Analyst

Danesh has a Master’s degree in mechanical engineering from the Royal Institute of Technology. He has

previously worked as a Calculation Engineer for more than 6 years, holding positions at both Scania and Volvo

Trucks. He also produced a finance podcast for nearly two years. Danesh joined Redeye in 2020 and works as

an equity research analyst, covering companies in the tech-sector, with a focus on gaming companies

Niklas Sävås

Analyst

Niklas has more than ten years experience from the financial industry working within banking and financial

technology. He started his first company in 2016 focused on consultancy and investments. Niklas has a dual

role within Redeye where he splits his time between the podcast Investing By The Books, Redeye Academy and

as an analyst on the technology team. He has a bachelor degree in Business and Economics from SLU.

Hjalmar Ahlberg

Analyst

Hjalmar is an equity analyst within the technology team focusing on gaming and online gambling sectors.

He holds a Master’s degree in finance and has previously worked within the banking industry with focus on

equity research covering various sectors.

Jacob Svensson

Analyst

Jacob Svensson is an equity analyst within the technology team, focusing on software companies. He holds

a BSc in Business Administration and a Master’s in Finance from Lund University and has previously worked

within the banking industry and asset management.

Viktor Lindström

Analyst

Viktor is an equity analyst in the technology team, focusing on gaming and cleantech sectors. He holds a

Master’s degree in Finance from University of Gothenburg. Previously, he held positions at Carnegie Investment

Bank and Consensus Asset Management.

REDEYE AUTOTECH SEMINAR - 2021

5Technology Selected Transactions

REDEYE AUTOTECH SEMINAR - 2021

6TECHNOLOGY SELECTED TRANSACTIONS

RECENT

FEBRUARY 2021 FEBRUARY 2021 FEBRUARY 2021 MAY 2021 FEBRUARY 2021

IPO Private Placement Private Placement IPO Private Placement

Selling Agent SEK 40m SEK 30m SEK 60m 53 MSEK

SEK 201m

2017–2020

DECEMBER 2020

Private Placement

52 MSEK

NOVEMBER 2020 OCTOBER 2020 OCTOBER 2020 OCTOBER 2020 MARCH 2020

Directed Issue + Rights Issue Rights Issue Directed Issue Rights Issue Rights Issue

204 MSEK 50 MSEK 66 MSEK 57 MSEK 36 MSEK

DECEMBER 2019 NOVEMBER 2019 OCTOBER 2019 JUNE 2019 MAY 2019

Pre-IPO IPO Rights Issue Rights Issue Directed Issue + Rights Issue

18 MSEK 26 MSEK 51 MSEK 40 MSEK 139 MSEK

MAY 2019 APRIL 2019 APRIL 2019 MARCH 2019 JANUARY 2019

Rights Issue Dual Listing Rights Issue IPO IPO

Co-Lead Manager 10 MSEK 102 MSEK 80 MSEK Joint Bookrunner

135 MSEK 120 MSEK

NOVEMBER 2018 OCTOBER 2018 OCTOBER 2018 OCTOBER 2018 JUNE 2018

Rights Issue Direced Issue Directed Issue Right Issue Private Placement

25 MSEK 43 MSEK 21 MSEK 39 MSEK 108 MSEK

JUNE 2018 JUNE 2018 MAY 2018 APRIL 2018 FEBRUARY 2018

Rights Issue Private Placement IPO Private Placement Private Placement

Join Lead Manager 50 MSEK 30 MSEK 20 MSEK 20 MSEK

127 MSEK

NOVEMBER 2017 NOVEMBER 2017 NOVEMBER 2017 OCTOBER 2017 APRIL 2017

IPO IPO Private Placement 22 MSEK IPO

60 MSEK 180 MSEK 9 MSEK 60 MSEK

REDEYE AUTOTECH SEMINAR - 2021

7Table of content

Key drivers 9

Transactions in the sector 14

Valuation metrics 16

Share performance 17

Covered Companies 16

– Acconeer

– Gapwaves

– Smart Eye

REDEYE AUTOTECH SEMINAR - 2021

8KEY DRIVERS

The automotive market is currently in a tech revolution that has barely started. Most notably, the cars of

the future will be electrified, autonomous, connected, smart and shared, as we will elaborate in the different

sections below.

Environmentally friendly electric cars Europe leading the way for new

All major car OEMs have an electric vehicle strategy and most EV registrations – USA lagging

of them are looking to go fully electric. The installed base of In Europe, EV sales exploded in 2020. In 2019, only 3% of

electric vehicles is expected to exceed 100 million vehicles cars sold in Europe was electric – in 2020 this figure incre-

around 2029, as indicated in the graph below. ased to 10%. Overall Europe’s car market contracted 22% in

2020. Yet, new electric car registrations more than doubled

Expected installed base for 2030 has to 1.4 million.

increased by 10% in two years

The estimated total installed base of electric vehicles (EVs) in China was previously the leader in share of electric vehicles

2030 is 140 million vehicles. This is a 10% increase in estima- sold, amounting to 5% already in 2018. Since then, China’s

tes from 2019. growth of EVs has stagnated and the share of EVs amounted

to 6% in 2020. The US market is clearly lagging both China

and Europe. The share of new vehicles being electric has

been steady at 2% since 2018.

Expected installed base of electric vehicles (million vehicles) Electric car registrations per region, 2015-2020

150 1500

1200

120

Thousands

900

90

600

60

300

30 0

Europe USA China Others

0 2015 2016 2017 2018 2019 2020

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Source: IEA, Redeye Research

Source: IEA, Redeye Research

REDEYE AUTOTECH SEMINAR - 2021

9KEY DRIVERS

Smart connected cars Sharing economy & ridesharing

Cars are becoming connected “computers on wheels” as they Owning a car will be less common in the future. Instead, cars

get equipped with internet access/W-LAN, allowing cars to will be shared and rented as a service. The market for so

communicate and share information with each other. This called ride-hailing services (platforms connecting passengers

opens endless opportunities for personalization, IoT and with private drivers) is growing rapidly, albeit with a small dip

driver-car-interaction. One example is controlling household in 2020 due to Covid-19. One good illustration of this trend is

electronics from the car, e.g., closing windows, the fridge the vertical takeoff in the number of Uber rides. Uber reached

telling the car that it is out of milk and much, much more. 10 billion trips in 2018 and 23 billion trips by the end of 2020.

The global connected car market is expected to be worth At the peak, before Covid-19 struck, almost 21 million Uber

over USD 200 bn in 2025, as indicated in the graph below: rides were made each day.

Global connected car market (USD bn)

250

200

150

100

50

0

2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Redeye Research, various industry sources

Uber: Number of trips (billion)

25

20

15

10

5

0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Trips per year Accumulated

Source: Uber, Redeye Research

REDEYE AUTOTECH SEMINAR - 2021

10KEY DRIVERS

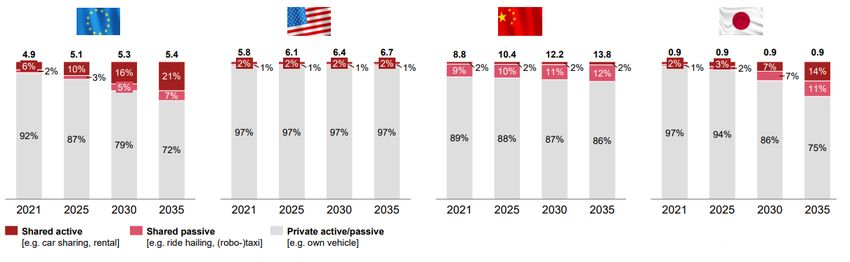

Preference towards shared mobility still varies across the Looking into expectations for 2035, Europe and Japan are

major markets; EU/Japan expected to lead by 2035 expected to travel one out of four kilometers through shared

Today, China and Europe are far ahead of USA and Japan mobility, while China will only grow to 14% while USA expec-

in shared mobility. While China and Europe have market ted to remain at 3%.

penetration of shared mobility of 11% and 8% respectively,

Japan and USA are both only at 3%.

Market penetration by mobility mode (in ‘000 trillion person-kilometer scaled to %)

Source: PwC, Autofacts, Strategy&

REDEYE AUTOTECH SEMINAR - 2021

11KEY DRIVERS

(Semi)-autonomous cars & driver assistance Safety-standard organizations mandating more

All car OEMs are investing in autonomous car technologies, technology to enable higher grade of autonomy

although the 100% autonomous cars will arrive later than As for the safety implications, safety-standard organizations

OEMs previously expected. The investments are related to worldwide are continuously mandating more technology to

many different areas. Various sensors are needed for the car decrease the 1.2 million road fatalities and 50 million traffic

to detect what is going in its surroundings. Artificial Intelligen- injuries that occur every year. About 94 percent of these car

ce (AI) then helps the cars to understand this information and crashes are related to human error, which drives the need for

make adequate maneuvers. Advanced Driver-Assistance Systems (ADAS), i.e. technology

that helps the driver in the driving process. Like self-driving

Some of the OEMs are moving directly to level 4 (high auto- cars, ADAS also require an increasing number of sensors

mation) where the car drives by itself almost the whole time. and AI.

Others believe it is important to first develop semi-autono-

mous level 2+ or level 3 (conditional automation) cars where

the driver is expected to intervene from time to time. Regard-

less which one of these approaches the car OEMs prefer, the

whole car industry has agreed on the long-term importance

of moving towards autonomous cars due to e.g. higher safety

and lower transportation costs.

REDEYE AUTOTECH SEMINAR - 2021

12KEY DRIVERS

2021 has seen first ever deployments of L3 and L4 Trust towards autonomous cars is declining – driven by

– but above 20% share expected only after 2030 worries of cybersecurity threats and recent accidents

In 2021, Honda became the first carmaker to sell a vehic- According to the Digital Auto Report 2021 by Strategy&, trust

le equipped with certified level 3 self-driving technology. towards autonomous cars is declining in several important

Though we already have the first L3 cars on the roads, it markets. In a consumer survey, people in Germany, USA and

will take time before penetration becomes relevant. In 2030, China answered on whether they personally would use a fully

Europe is estimated to reach 29% of L3 or higher of new autonomous car. The share of consumers saying they would

vehicles sold. The same figure for the USA is 16%, 34% for not use an autonomous car increased to 62% in Germany

China, and 29% for Japan. Fully automated cars, i.e., level 5, (36% previous year), 64% in the USA (36% previous year), and

are expected to arrive in 2035, but only at a modest 1% share 14% in China (9% previous year). Trust is however increasing

of all new cars sold. All this according to PwC Autofacts and in Japan, with 28% saying no vs 37% last year.

Strategy&.

The global semi-autonomous vehicle market demand was

valued at 14.2 million units in 2020. NVIDIA estimates that in “In general, willingness to use fully automated cars

2025, there will be 40 million semi-autonomous vehicles, of has declined, especially in Germany and the US.

which 6/7 with Level 2, and the remaining 1/7 of Level 3 or 4. Trust in automated driving is seen as susceptible

Grandviewresearch.com estimates the market to expand to to change, and consumer attitudes might fluctuate

60 million units in 2028. Nvidia also estimates that there will rapidly as critical headlines emerge, e.g. following

be only 1 million Robotaxis in 2025. accidents and cybersecurity threats.”

Addressable market of semi-autonomous vehicles by 2025 (million vehicles)

40

35

30

25

20

15

10

5

0

L2+ (incl. Autopilot) L3/L4 Robotaxis

Source: NVIDIA

REDEYE AUTOTECH SEMINAR - 2021

13TRANSACTIONS IN THE SECTOR

M&A – slightly fewer deals and lowest Looking at the chart below, it is noteworthy that the valua-

multiples since 2015 tions of the deals in 2H 2020 were the lowest since 2015

About 90 M&A transactions were completed in 2020 and the -especially when looking at EBITDA multiples. After three

deal flow has continued in 2021. The largest acquisition of years of EBITDA multiples ranging between 13 and 17, it was

2021 is the ongoing acquisition of Veoneer, which has recei- down at 10 in 2H’20, a level which was normal in 2014-1016.

ved bids from both Magna and Qualcomm. The latest bid is Sales multiples have remained rather constant, hovering

from Qualcomm and amounts to USD 4.6 bn. between 1.7–2.1 the last five years, except for two outliers

in 1H’17 and 2H’18.

Total number of deals & valuation multiples in Autotech, 2014-2020

70 35

60 30

50 25

Valuation multiples

Number of deals

15,5 17,2

40 15,5 15,5 20

13,4

13,4

11,2 17,2

30 11,0 15

9,6 9,6 10,4

9,6

8,2

20 10

4,7

10 3,1 5

1,3 1,4 2,1 2,1 2,1 2,1 2,1 2,0 1,7 1,8 2,1 1,8

0 0

1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H

2014 2015 2016 2017 2018 2019 2020

Transaction count Trailing 30-month median EV/S Trailing 30-month median EV/EBITDA

Source: Hampleton Partners

REDEYE AUTOTECH SEMINAR - 2021

14TRANSACTIONS IN THE SECTOR

Below is a list of some of the largest deals of the past five years:

Major M&A deals 2016-2021

Target Acquirer Price (bn USD) EV/Sales multiple

Mobileye Intel 15,3 39x

Harman Samsung 8,0 1x

Wabco ZF 7,4 2x

Veoneer Qualcomm/Magna 4,6 2x

Plus BlackRock, Hennessy, DeShaw 3,3

Careem Uber 3,1

BCA Marketplace BBD Bidco 2,4 1x

Fleetmatics Verizon 2,4 6x

Yinlong Gree 1,9

Wallbox Kensington (SPAC) 1,5 30x

SAFT Total 1,1 1x

99 Taxis DiDi 1,0

NEVS Evergrande 0,9 34x

Telogis Verizon 0,9 7x

Affectiva Smart Eye 0,7 15x

ABC Technologies Apollo 0,4 5x

Xevo Lear 0,3 1x

Source: Redeye Research, various industry sources

REDEYE AUTOTECH SEMINAR - 2021

15VALUATION METRICS

Valuations of the listed autotech companies forecast for the corresponding period for the tier-1s is 1%,

In the tables below, we have summarized the valuations of as indicated in the following table. This leads to on average

car OEMs, tier-1s and autotech-related tier-2/3 players. 34% higher P/E ratios for the tier-1s (median used due to

Car OEMs are expected to grow sales on average 4% during Tesla being such an outlier), while EV/S multiples are actually

2019-2021 according to Factset consensus, while the higher for OEMs.

Valuations of Listed Autotech Companies: OEMs & Tier-1s

Company Mkt P/E EV/EBITDA EV/Sales CAGR Sales

cap sales (SEKbn)

OEMs (SEKbn) 20 21E 22E 20 21E 22E 20 21E 22E 19-21E 2020

GM 615 10 8 7 12 11 9 1,2 1,1 1,0 1% 1127

Ford 442 32 8 7 20 13 11 1,2 1,1 1,0 -1% 1170

Volkwsagen 1275 17 10 9 8 7 7 1,1 1,2 1,1 1% 2339

BMW 535 14 5 6 13 8 8 1,4 1,3 1,2 3% 1039

Daimler 779 21 6 6 12 8 8 1,2 1,1 1,0 1% 1619

Toyota 2461 12 10 9 14 11 10 1,7 1,5 1,4 0% 2281

Honda 476 9 8 7 10 9 8 0,9 0,7 0,7 -1% 1104

Nissan 192 -5 20 9 70 13 10 1,1 0,8 0,8 -2% 659

Suzuki 184 16 13 12 7 6 5 0,7 0,6 0,5 0% 266

Hyundai 386 38 9 8 17 11 11 1,1 1,1 1,1 3% 811

Renault 95 -1 13 4 17 10 8 1,2 1,0 1,0 -3% 456

PSA 541 15 5 5 2 2 2 0,3 0,3 0,3 14% 910

Tesla 6292 329 148 105 128 83 60 24,1 16,4 12,1 36% 290

Average 1098 39,0 20,2 14,9 25,4 14,7 12,1 2,9 2,2 1,8 4,1% 1083

Median 535 14,9 8,8 7,1 13,4 9,6 8,0 1,2 1,1 1,0 0,5% 1039

Tier-1s (SEKbn) 20 21E 22E 20 21E 22E 20 21E 22E 19-21E 2020

Continental 232 36 15 10 8 4 4 0,8 0,7 0,6 -3% 396

Magna 205 20 11 9 8 6 5 0,7 0,7 0,6 0% 301

Veoneer 35 -4 -12 -21 -14 -18 -62 1,5 2,1 1,8 1% 13

Hyundai Mobis 386 38 9 8 17 11 11 1,1 1,1 1,1 3% 811

Aptiv 356 78 40 28 23 18 15 2,8 2,6 2,3 6% 120

Denso 478 48 17 14 12 7 7 1,2 1,1 1,0 1% 414

Valeo 59 -7 19 9 8 4 3 0,7 0,5 0,5 0% 172

Visteon 26 109 48 19 19 13 9 1,4 1,1 0,9 3% 23

Alps Alpine 20 -73 14 10 6 3 3 0,4 0,3 0,3 -2% 60

Faurecia 57 -15 10 7 6 4 3 0,6 0,6 0,5 1% 154

Aisin Seiki 97 11 7 6 5 4 3 0,5 0,5 0,4 1% 296

Average 177 21,9 16,2 8,9 8,7 5,2 0,1 1,1 1,0 0,9 0,9% 251

Median 97 20,0 13,8 9,0 7,9 4,5 3,7 0,8 0,7 0,6 0,7% 172

Source: Factset, Redeye Research

REDEYE AUTOTECH SEMINAR - 2021

16VALUATION METRICS • SHARE PERFORMANCE

In group 2 in the table below, we have included the Swedish, digit EV/sales multiples. However, they are not profitable yet,

smaller, pure-play companies (and in some cases their which we believe is related to the immature autotech market.

competitors). As one would expect, these players have a From 2023 and beyond we expect the autotech winners to

significantly faster expected sales growth and higher, double begin turning profitable and enjoy high margins.

Valuations of Listed Autotech-related Companies: Tier-2/3

Company Mkt P/E EV/EBIT DA EV/Sales CAGR Sales

cap sales (SEKbn)

Group 1 (SEKbn) 20 21E 22E 20 21E 22E 20 21E 22E 19-21E 2020

Xilinx 333 59 44 39 31 33 29 9,2 10,2 9,4 4% 28

Infineon 480 57 34 27 17 17 14 4,2 4,7 4,3 14% 91

NXP 493 34 21 19 18 16 15 5,9 6,1 5,7 6% 79

Renesas 181 46 20 16 11 8 7 3,4 2,6 2,3 8% 62

ST 350 38 23 21 15 13 11 3,2 3,2 3,0 9% 94

Intel 1895 10 11 12 6 7 7 2,9 3,2 3,2 -2% 717

Melexis 41 59 34 31 26 21 19 6,3 6,3 5,8 11% 5

Synopsys 438 60 49 44 29 37 33 8,9 12,3 11,2 8% 35

Nvidia 4819 90 54 49 42 43 39 19,3 21,8 19,5 34% 152

Average 1003 50,5 32,3 28,6 21,9 21,7 19,4 7,0 7,8 7,2 10,2% 140

Median 438 57,1 33,8 27,1 18,3 16,8 15,0 5,9 6,1 5,7 8,1% 79

Group 2 (SEKm) 20 21E 22E 20 21E 22E 20 21E 22E 19-21E 2020

Seeing Machines 4912 -4 -28 -42 -18 -25 -43 4,1 12,9 11,2 21% 259

Acconeer 1535 -8 n/a n/a -30 -20 -44 37,7 84,3 16,1 157% 10

Neonode 485 -11 -8 -14 -19 -10 1 9,3 6,1 1,2 71% 55

Diadrom 104 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a 39

Terranet 437 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a 0

Gapwaves 1376 -35 n/a n/a -38 n/a n/a 66,8 54,0 32,0 32% 16

Smart Eye 4255 -47 -49 -58 -76 -43 -106 52,1 31,2 10,3 85% 65

Average 1872 -20,9 -28,4 -38,0 -36,2 -24,5 -48,1 34,0 37,7 14,2 73,3% 63

Median 1376 -10,7 -27,7 -42,0 -30,1 -22,5 -43,6 37,7 31,2 11,2 70,9% 39

Source: Factset, Redeye Research

One year share price performance (%)

Looking at the one-year stock performance (see

the graph beside), all segments have performed 120%

well. The field is tight between OEMs, tier-1s and 100%

large tier-2/3 players, while small tier-2/3 players 80%

have performed even stronger.

60%

40%

20%

0%

OEMs Tier-1s Large tier-2/3s Small tier-2/3s

Source: Bloomberg

REDEYE AUTOTECH SEMINAR - 2021

17Covered Companies

REDEYE AUTOTECH SEMINAR - 2021

18REDEYE AUTOTECH SEMINAR - 2021

19Acconeer ACCON

Company page Publication date

https://www.redeye.se/company/acconeer September 30 2021

Redeye Rating

COMPANY QUALITY FAIR VALUE RANGE CATALYST POTENTIAL

Last price

Impact Timeframe

73.1

Major Long

Moderate Mid

Minor Short

3 2 2 Base

Bear Bull

People Business Financials 21.0 44.0 82.0 Turn page for catalyst specifics

Snapshot Financials

Acconeer Redeye Estimates

OMXS30

2019 2020 2021E 2022E 2023E

60

Revenue, MSEK 6 10 18 94 341

40

Growth -49.6% 72.6% 90.6% >100% >100%

20

EBITDA -68 -65 -49 -35 58

0

EBITDA margin Neg Neg Neg Neg 17.0%

Volume EBIT -68 -65 -64 -37 55

1 000k

500k EBIT margin Neg Neg Neg Neg 16.4%

0

Nov Jan Mar May Jul Sep Pre-tax earnings -68 -68 -64 -37 55

Net earnings -68 -68 -64 -29 43

Marketplace First North Stockholm Net margin Neg Neg Neg Neg 12.9%

CEO Lars Lindell Dividend/Share 0.00 0.00 0.00 0.00 0.00

Chairman Thomas Rex EPS adj. -3.59 -3.58 -2.72 -1.22 1.81

P/E adj. N/A N/A N/A N/A N/A

Share information

EV/S N/A N/A N/A N/A N/A

Share price (SEK) 73.1

EV/EBITDA N/A N/A N/A N/A N/A

Number of shares (M) 23.4

Market cap (MSEK) 1,709 Last updated: 2021-07-23

Net debt (MSEK) -82

Owner Equity Votes

Analyst

Bengt Adolfsson 11.6% 11.6%

Avanza Pension 9.6% 9.6%

Jesper Henrikson

jesper.henrikson@redeye.se Smbc Nikko Securities Inc. 7.9% 7.9%

Swedbank Försäkring 4.3% 4.3%

Nordnet Pensionsförsäkring 3.7% 3.7%

Conflict of interests

Mikael Egard 2.5% 2.5%

Jesper Henrikson owns shares in Acconeer: No

Mats Ingvar Ärlelid 2.4% 2.4%

Redeye performs/have performed services for the Company and receives/have

received compensation from the Company in connection with this. Lars-Erik Wernersson 2.4% 2.4%

Skandinaviska Enskilda Banken S.A 1.2% 1.2%

DTX i Sverige AB 1.1% 1.1%

REDEYE AUTOTECH SEMINAR - 2021

20Company description

Acconeer is a semiconductor company in Lund, Sweden, who went public in radar will be the go-to technology for CPD. Acconeer has won three CPD design

December 2017. It develops and sells radar sensors, with a fabless business wins for a total contract value of SEK 90-120m. We believe the OEM is a small

model, to manufacturers of electronics. The manufacturing partners are some premium car manufacturer, suggesting that CPD is a multi-billion SEK market

of the World's largst (Global Foundries & Amkor). Acconeer has developed a for Acconeer. We think larger premium OEMs could yield three times larger

radar with a minimal footprint (5x5x1 mm) that is 10 times smaller and comes initial contracts of SEK 270-360m, and this is just the premium market. The top

at a 10 times lower cost, compared to competing radars. Its real claim to fame 8 largest mass market manufacturers are 2-5 times larger than that, meaning

though is that the power consumption is 50 times lower than competition. As incredible potential.

for competitive disadvantages, radar technology is complex in general and

requires a lot of education of the customer but at the same time Acconeer is Large design wins to drive the share price

company of minor size that competes with giants. Acconeer needs to start

The key differences in our case scenarios are related to automotive and

building revenue sources in order to be seen as a reliable supplier for larger

smartphones. While news of orders gradually will de-risk the case we assume

companies. The growth strategy is based on a few important pillars such as

certain deals are key catalysts. They are more worth than others and have the

selling on Digi-Key, World's largest online distributor (450 000 customers) and a

potential to substantially move the shares; especially more larger deals within

vast, global network of local, niche distributors. The company's current focus

automotive. With sales ramping, a big news pipeline, and enough cash until

areas are robotics, smart presence, child presence detection, parking sensors,

year 2023 in a worst case scenario, we argue that the neglected Acconeer

level measurement (incl.waste management) and automotive.

stock provides solid risk/reward.

Investment case Main bear point:

• Strong unique product offering & scalability from unmatched cost • Acconeer’s minor size is a disadvantage that likely explains why major

• Automotive has the largest potential players like Google want to go with Infineon. Acconeer needs to start

• Large design wins to drive the share price building revenue sources in order to become reliable as a long-term

• Main bear point supplier for large customers.

Strong unique product offering & scalability

Catalyst types

from unmatched cost Larger deals to drive the share price

Acconeer’s radar of 5x5x1 mm is the tiniest radar on the market, which means Today's valuation has discounted a bunch of deals for Acconeer but since lead

unmatched cost. Other radars are more than three times larger, suggesting that times are long we assume the deals will start to gradually come. Smaller

they have at least three times higher cost. The real claim to fame though, and customers are moving faster. While news of orders gradually will de-risk the

the truly disruptive element in Acconeer’s offering, is the power consumption, case we assume certain larger deals are key catalysts. They are more worth

which is more than 10 times lower than competing radars. Combining these than others and have the potential to substantially move the shares; especially

characteristics and its fabless business model with the largest manufacturing big deals within automotive like Child Presence Detection.

partners in the World (Amkor & Global Foundries), Acconeer is poised to scale

rapidly with high gross margins as soon as sales kick in. Acconeer is ready to

ride the structural growth in large market segments within e.g. IoT, automotive

and robotics respectively. We believe automotive will be the company's most

important market.

Automotive has the largest potential

Acconeer is working on ten use cases in automotive with its tier-1 partner Alps

Alpine. The most exciting area is child presence detection (CPD) since it is

being mandated by Euro NCAP from 2022-2023, meaning it will become

standard in Europe. Moreover, CPD regulation in US is underway. Thus, most

OEMs are procuring or are about to procure CPD. In essence, it is the same type

of case as Smart Eye ~2 years ago. We believe Acconeer has a strong

competitive advantage in CPD as Acconeer's radar can detect a sleeping baby,

behind a blanket, by sensing its pulse or breathing, meaning, i our opinion, that

REDEYE AUTOTECH SEMINAR - 2021

21Gapwaves GAPW B

Company page Publication date

https://www.redeye.se/company/gapwaves September 29 2021

Redeye Rating

COMPANY QUALITY FAIR VALUE RANGE CATALYST POTENTIAL

Last price

Impact Timeframe

48.8

Major Long

Moderate Mid

Minor Short

4 4 2 Base

Bear Bull

People Business Financials 20.0 76.0 115.0 Turn page for catalyst specifics

Snapshot Financials

Gapwaves Redeye Estimates

OMXS30

2019 2020 2021E 2022E 2023E

70

60 Revenue, MSEK 20 22 40 51 116

50 Growth >100% 7.7% 80.4% 28.7% >100%

40

EBITDA -30 -36 -30 -29 6

30

EBITDA margin Neg Neg Neg Neg 5.4%

Volume EBIT -35 -42 -35 -35 0

2M

1M EBIT margin Neg Neg Neg Neg 0.1%

0

Nov Jan Mar May Jul Sep Pre-tax earnings -35 -44 -35 -35 0

Net earnings -35 -44 -35 -35 0

Marketplace First North Stockholm Net margin Neg Neg Neg Neg 0.1%

CEO Lars-Inge Sjöqvist Dividend/Share 0.00 0.00 0.00 0.00 0.00

Chairman Jonas Ehinger EPS adj. -1.32 -1.61 -1.29 -1.28 0.00

P/E adj. N/A N/A N/A N/A N/A

Share information

EV/S 28.5 70.5 N/A N/A N/A

Share price (SEK) 48.8

EV/EBITDA -19.0 -42.5 N/A N/A N/A

Number of shares (M) 30.7

Market cap (MSEK) 1,497 Last updated: 2021-09-29

Net debt (MSEK) -78

Owner Equity Votes

Analyst

Cécile Schilliger 21.8% 57.8%

HELLA 10.1% 3.1%

Forbes Goldman

forbes.goldman@redeye.se Avanza Pension 4.8% 1.5%

Lars-Inge Sjöqvist 3.7% 8.9%

Nordnet Pensionsförsäkring 2.8% 0.9%

Conflict of interests

BNP Paribas Sec Serv Luxembourg 2.7% 0.8%

Forbes Goldman owns shares in Gapwaves: No

Alfred Berg Fonder 2.7% 0.9%

Redeye performs/have performed services for the Company and receives/have

received compensation from the Company in connection with this. SIX SIS AG 1.8% 0.6%

Bright Peter Leo Ebenezer 1.8% 0.5%

Jian Yang 1.7% 5.1%

REDEYE AUTOTECH SEMINAR - 2021

22Company description Counter Points

Competitors catching up

Gapwaves offers wireless communication solutions based on the GAP

waveguide technology, which stems from the research of the late founder Per- While competition may be limited at this point, it is expected to increase.

Simon Kildal. The company’s great potential is found in the millimeter wave Huber+Suhner is the only competitor that is currently using a similar waveguide

antennas that can be applied in expansions of current radio link networks, technology. However, with limited success due to volume production issues

automotive radars and eventually 5G deployments. according to Gapwaves' CEO.

Nevertheless, other competitors could arise that could affect Gapwaves’

Investment case prospects. Another competing technology is, of course, regular patch antennas,

even though they do not have the same technological benefits as do waveguide

• Attractive application areas within both automotive and telecom for

antennas. We believe that the potential customers with in-house capabilities to

Gapwaves' 4-10x more power-efficient antennas.

develop similar products, such as the large system integrators, like Ericsson

• Contracts with several automotive customers with potential to yield SEK

and Nokia, pose perhaps the most serious threat.

250m in annual sales.

Uncertainties regarding 5G networks and the telecom opportunity

• The trends towards self-driving cars and increased safety regulations as

well as the coming 5G transformation creates huge market potential. Even though the 5G transformation is starting to happen, there is still

significant uncertainty regarding how the next generation networks will look

Several promising application areas for Gapwaves' like and how rapid the deployment will be, especially in the higher frequencies.

differentiated technology As of now, Gapwaves has one smaller customer within the telecom segment,

Gapwaves' product offering is based on the company's patented waveguide and it remains for Gapwaves technology to prove itself for this application

technology and includes antennas that can be used in, for example, telecom commercially.

equipment and for automotive applications. There are several benefits to this Rapid technological development

technology. One of them is that the antennas become 4-10x more power-

Technological development moves quickly in the industries that Gapwaves

efficient, and the power losses are thereby reduced. The technology also

focus on, as noted above. Within both the automotive and telecom equipment

increases the output power and the antenna directivity, i.e., the capability to

industries, the next generation is always around the corner, and products

concentrate the radiation in one direction. These characteristics are especially

become obsolete rather fast. Hence, the life cycle of Gapwaves’ product

interesting in the coming 5G transformation of the telecom networks, where,

offering is limited, and the company must address this issue with product

for example, the antenna directivity will be crucial to attaining higher capacity in

development to have a sustainable business.

the networks.

So far, there has been limited interest in the product technology from potential

telecom customers, leading us to believe that in the near term, the case is more

Catalyst types

about the automotive opportunity. The company has received a number of low- Announcement of a breakthrough automotive agreement

volume development agreements from several automotive customers. It has Gapwaves has customer relationships with several automotive Tier 1 parts

two high-volume agreements to date – licensing agreements with Veoneer and suppliers. The most critical catalyst for the share price is that a Tier 1 customer

HELLA. We expect Gapwaves will start receiving significant royalties in 2023. moves forward with volume production.

Gapwaves has sparked interest from other verticals, and that the application

5G market take-off & telecom customers

areas for its antenna units continues to expand. This is nonetheless validated

The transformation of the telecom industry, moving from 4G to 5G technology,

by orders, and follow-up orders from Uhnder and Smartmicro, among others.

is expected to take place in the coming years, and this shift has partially

Gapwaves is tapping into large industries, such as last-mile-delivery (LMD) and

already begun. Gapwaves will be well-positioned to attract customers from this

the internet of things (IoT), which present significant greenfield opportunities.

segment in addition to automotive, meaning a significant upside potential in

the stock.

Huge market potential in core segments

In the coming years, strong growth is expected in both primary application Follow-up orders from existing customers and new customer wins

areas for Gapwaves' technology. Thus, it is easy to see that the potential Gapwaves has attracted significant attention from automotive and new radar

markets for Gapwaves' products are enormous. Within automotive, the growth verticals. It is essential that these customers continue to place follow-up

is in the short term driven by increased regulation to improve safety and, in the orders, and increase volumes.

long run, the trend towards self-driving cars, which increases the need for

sensors drastically. The coming shift within the telecom sector to 5G

technology will lead to a surge in demand for suitable equipment for the denser

networks that the new technology will require. Both of these market

developments constitute exciting opportunities for Gapwaves going forward.

REDEYE AUTOTECH SEMINAR - 2021

23Smart Eye SEYE

Company page Publication date

https://www.redeye.se/company/smart-eye September 20 2021

Redeye Rating

COMPANY QUALITY FAIR VALUE RANGE CATALYST POTENTIAL

Last price

Impact Timeframe

190.2

Major Long

Moderate Mid

Minor Short

5 4 2 Base

Bear Bull

People Business Financials 170.0 340.0 405.0 Turn page for catalyst specifics

Snapshot Financials

Smart Eye Redeye Estimates

OMXS30

2019 2020 2021E 2022E 2023E

250

Revenue, MSEK 57 61 104 314 741

200

Growth 7.8% 8.3% 70.2% >100% >100%

150

EBITDA -61 -51 -97 -39 336

100

EBITDA margin Neg Neg Neg Neg 45.4%

Volume EBIT -77 -75 -114 -69 296

1 000k

500k EBIT margin Neg Neg Neg Neg 40.0%

0

Nov Jan Mar May Jul Sep Pre-tax earnings -78 -75 -114 -69 296

Net earnings -78 -75 -114 -55 233

Marketplace First North Stockholm Net margin Neg Neg Neg Neg 31.5%

CEO Martin Krantz Dividend/Share 0.00 0.00 0.00 0.00 0.00

Chairman Anders Jöfelt EPS adj. -5.18 -4.54 -5.80 -2.78 11.80

P/E adj. N/A N/A N/A N/A N/A

Share information

EV/S 29.8 27.3 N/A N/A N/A

Share price (SEK) 190.2

EV/EBITDA -27.6 -32.4 N/A N/A N/A

Number of shares (M) 19.9

Market cap (MSEK) 3,791 Last updated: 2021-08-27

Net debt (MSEK) -219

Owner Equity Votes

Analyst

Sellers Of Affectiva 10.2% 10.2%

Ålandsbanken I Ägares Ställe 9.3% 9.3%

Jesper Henrikson

jesper.henrikson@redeye.se Swedbank Robur Fonder 7.5% 7.5%

Första AP-fonden 6.9% 6.9%

Mats Krantz inklusive närstående 6.5% 6.5%

Conflict of interests

Handelsbanken Fonder 5.6% 5.6%

Jesper Henrikson owns shares in Smart Eye: Yes

Niclas Eriksson med närstående 5.0% 5.0%

Redeye performs/have performed services for the Company and receives/have

received compensation from the Company in connection with this. Martin Krantz 4.8% 4.8%

Anders Jöfelt 4.7% 4.7%

Avanza Pension 4.6% 4.6%

REDEYE AUTOTECH SEMINAR - 2021

24Company description

Smart Eye provides eye tracking software for especially automotive

Impatient & short term focused stock market

applications but addresses customers in defence, aircraft and academic Smart Eye’s first design wins with new customers are in general worth a lot

research as well. In the Research Instruments segment, where Smart Eye has more than what meets the eye as they are platform based. The platforms will

a market share of 4-5 percent, it provides systems consisting of hardware, usually (although not automatically) yield additional new car models for every

software and accessories. Our investment case, however, is fully based on year over the platforms’ lives of about 10 years. In addition, each car model

the Automotive Solutions segment, which is an OEM business where lives around seven years. For Smart Eye this creates a very foreseeable and

Smart Eye provides tier 1 automotive suppliers with algorithms and software stable revenue stream for many years to come as the large switching costs

for embedding eye tracking in products that are later sold to the car OEM provide solid barriers to entry. The stock market however, as always, only sees

manufacturers. When a car model with Smart Eye's technology is launched the coming few quarters, meaning significant potential for patient, long term

Smart Eye will receive a royalty based license fee per car. Within Automotive investors.

Solutions Smart Eye has won designs from about half of the customers that

has procured eye tracking thus far. The automotive market has high barriers Design wins to move the share price

to entry as it is costly and time consuming to develop products that meet the

We expect a steady news flow going forward with design wins from already

customers' high standards and switching costs are high, meaning important

won procurements as well as RFQ’s worth SEK billions in progress for the next

competitive advantages for Smart Eye.Listing: Stockholm Stock Exchange

quarters, which should drive the share price.

(First North) since year 2016.Locations: HQ in Sweden. Offices in Detroit,

China and Japan.

Catalyst types

Investment case VW win

The Volkswagen procurement will be finished imminently. Volkswagen sells

• In pole position within eye tracking for mandated driver monitoring

almost 11 million vehicles per year and is the World's second largest car OEM

• Impatient & short term focused stock market

(second only to Toyota), meaning significant catalyst potential if Smart Eye

• Design wins to move the share price

would win Volkswagen.

In pole position within eye tracking for Design wins in China

mandated driver monitoring We believe there are design wins overdue in China where Smart Eye's tier-1

partner has been selected and only paperwork remains before Smart Eye is

Due to EU and Euro NCAP's decisions to mandate driver monitoring, the market

officially nominated.

for driver monitoring systems (DMS) is about to explode. This expected growth

is a known fact for the stock market but we believe many do not understand Design wins and follow-up orders in general

Smart Eye’s strong positioning. Smart Eye has devoted ~20 years of 100 The major key catalyst in general is won contracts from the many RFQ’s worth

percent focus to and investments in this very niche. The company is in pole in total SEK 6 billion, which should drive the share price. In addition, we expect

position with an unmatched 84 design wins for 13 car OEMs. As for barriers to follow-up orders from existing customers

entry, the technology needs to cope with e.g. changing light conditions, tunnels,

sunshine, darkness, vibrations etc. and at the same time never fail. Competition

is therefore basically limited to one other tier-2 player aside of the tier-1

customers’ own solutions. However, we believe it is unlikely that the customers

in the long run are willing to put up with all investments and maintain the focus

necessary for in house sourcing. Smart Eye states that, being platform

independent and hardware agnostic, it has a competitive edge as its

technology can be locked late in the development process.

REDEYE AUTOTECH SEMINAR - 2021

25REDEYE AUTOTECH SEMINAR - 2021 26

Disclaimer Important information Redeye AB (“Redeye” or “the Company”) is a specialist financial advisory boutique that focuses on small and mid-cap growth companies in the Nordic region. We focus on the technology and life science sectors. We provide services within Corporate Broking, Corporate Finance, equity research and investor relations. Our strengths are our award-winning research department, experienced advisers, a unique investor network, and the powerful distribution channel redeye.se. Redeye was founded in 1999 and since 2007 has been subject to the supervision of the Swedish Financial Supervisory Authority. Redeye is licensed to; receive and transmit orders in financial instruments, provide investment advice to clients regarding financial instruments, prepare and dissemi- nate financial analyses/recommendations for trading in financial instruments, execute orders in financial instruments on behalf of clients, place financial instruments without position taking, provide corporate advice and services within mergers and acquisition, provide services in conjunction with the provision of guarantees regarding financial instruments and to operate as a Certified Advisory business (ancillary authorization). Limitation of liability This document was prepared for information purposes for general distribution and is not intended to be advisory. The information contained in this analysis is based on sources deemed reliable by Redeye. However, Redeye cannot guarantee the accuracy of the information. The forward-looking information in the analysis is based on subjective assessments about the future, which constitutes a factor of uncertainty. Redeye cannot guarantee that forecasts and forward-looking statements will materialize. Investors shall conduct all investment decisions independently. This analysis is intended to be one of a number of tools that can be used in making an investment decision. All investors are therefore encouraged to supplement this information with additional relevant data and to consult a financial advisor prior to an investment decision. Accordingly, Redeye accepts no liability for any loss or damage resulting from the use of this analysis.. Potential conflict of interest Redeye’s research department is regulated by operational and administrative rules established to avoid conflicts of interest and to ensure the objectivity and independence of its analysts. The following applies: • For companies that are the subject of Redeye’s research analysis, the applicable rules include those established by the Swedish Financial Supervisory Authority pertaining to investment recommendations and the handling of conflicts of interest. Furthermore, Redeye employees are not allowed to trade in financial instruments of the company in question, from the date Redeye publishes its analysis plus one trading day after this date. • An analyst may not engage in corporate finance transactions without the express approval of management and may not receive any remuneration directly linked to such transactions. • Redeye may carry out an analysis upon commission or in exchange for payment from the company that is the subject of the analysis, or from an underwriting institution in conjunction with a merger and acquisition (M&A) deal, new share issue or a public listing. Readers of these reports should assume that Redeye may have received or will receive remuneration from the company/companies cited in the report for the performance of financial advisory services. Such remuneration is of a predetermined amount and is not dependent on the content of the analysis. Redeye’s research coverage Redeye’s research analyses consist of case-based analyses, which imply that the frequency of the analytical reports may vary over time. Unless otherwise expressly stated in the report, the analysis is updated when considered necessary by the research department, for example in the event of significant changes in market conditions or events related to the issuer/the financial instrument. Recommendation structure Redeye does not issue any investment recommendations for fundamental analysis. However, Redeye has developed a proprietary analysis and rating model, Redeye Rating, in which each company is analyzed and evaluated. This analysis aims to provide an independent assessment of the company in question, its opportunities, risks, etc. The purpose is to provide an objective and professional set of data for owners and investors to use in their decision-making. Redeye Rating (2021-04-08) Rating People Business Financials 5p 20 15 3 3p - 4p 96 77 36 0p - 2p 6 30 83 Company N 122 122 122 Duplication and distribution This document may not be duplicated, reproduced or copied for purposes other than personal use. The document may not be distributed to physical or legal entities that are citizens of or domiciled in any country in which such distribution is prohibited according to applicable laws or other regulations. Copyright Redeye AB. REDEYE AUTOTECH SEMINAR - 2021

redeye.se

Redeye is the next generation investment banking company, specialized in Life Science and Technology.

Clients are innovative and fast-growing companies based in the Nordics but with a global reach. Redeye is a

leading provider of Equity Research, Corporate Broking, and Corporate Finance in these sectors. The research

is built on a value-based investment philosophy and with a unique Rating model. Redeye was founded in

Stockholm 1999 and is regulated by the Swedish Financial Authority (Finansinspektionen).

REDEYE AUTOTECH SEMINAR - 2021You can also read