Assessment of Sri Lankan Power Sector - October 2020 - K Seeds Investments

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

K SEEDS INVESTMENTS

Assessment of Sri

Lankan Power

Sector

October 2020

Contents 1. Overview of Sri Lankan Power Sector 1.1 Accessibility to power 05 1.2 Per Capita Electricity Consumption 06 1.3 Power Structure of Sri Lanka 07 1.4 Key Challenges Faced by SL Power Sector 07 2. Global Power Generation Trends 09 3. Power Generation System 3.1 Existing Power Generation System 12 3.2 Power Generation Expansion System 14 4. Cost of Production, Selling price and Demand for Power 4.1 Cost of Production 16 4.2 Selling Price 17 4.3 Average Selling Price Vs Average Cost at Selling Point 21 4.4 Comparison of Selling Prices 21 4.5 Demand for Power 22 4.6 Demand Projections 24 5. Power Distribution and Collection 5.1 Distribution of Power 26 5.2 Collection 27 6.Regulator of the Electricity Industry of Sri Lanka 28

7. Mini Hydro projects available in the industry

7.1 List of Mini Hydro Projects Undertaken by Listed Power

Companies in Sri Lanka 32

7.2 Small Hydro Power Developers Association (SHPDA) 34

7.3 Cyclin Impact on the Hydro Power projects 35

7.4 Approval of a mini-hydro project 38

7.5 Factors to consider by an investor who is looking to have

exposure to the mini hydro sector 39

8. Wind projects in the Industry 40

9. Solar Power projects in the Industry

9.1 Solar Power Projects Undertaken by CEB 45

9.2 Solar Power Plants Capacity Additions 45

9.2 Development of rooftop solar power 46

10.Thermal Projects

10.1 The Capacity Breakdown of the Sectors and the

Sources of Generating Thermal Power 48

10.2 Thermal Plant Specific Cost Comparison 54

11. Listed Power Generation Companies

11.1 Vidullanka PLC (VLL) 55

11.2 Resus Energy PLC (HPWR) 57

11.3 Vallibel Power Erathna PLC (VPEL) 58

11.4 Panasian Power PLC (PAP) 59

11.5 Laugfs Power PLC (LPL) 60

11.6 Laugfs Power PLC (LPL.X) 61

11.7 LVL Energy Fund PLC (LVEF) 62

11.8 Lotus Hydro Power PLC (HPFL) 63

12. Conclusion 64

13. References 65

1. Overview of Sri

Lankan Power Sector

Over the past 15 years, electric The production of nonconventional

power use has nearly doubled – renewable energy (NCRE) and

from 297 kwh per capita to 531 kwh liquefied natural gas (LNG) is

per capita, and 100 percent therefore a must in order to meet

electrification has been achieved in long-term energy demand in a

Sri Lanka. To meet the increasing sustainable and cost-effective way.

energy needs, Sri Lanka will need to The natural gas sector in the country

look beyond publicly funded has been slow to develop and the

projects, increase its share of exploration of domestic gas basins is

commercial financing and promote uncertain. The focus has now

increased involvement by the shifted to procurement of LNG to

private sector in the renewable fuel the power sector, but there is

energy sector to end the era of fossil lack of clarity on the demand for

fuel dominance in the energy sector. LNG beyond the power sector. In the

power sector, LNG is expected to

Given that the power sector in Sri fuel about 700 MW of old oil-fired

Lanka is heavily dependent on hydro power plants which are to be

plants, any change in the monsoon converted to gas-fired plants, and

pattern hurts the industry. At that about 1,600 MW of new gas plants

time, country will become are also planned in the long term

increasingly dependent on imported generation expansion plan (LTGEP).

fuel and eventually impact trade However, LNG procurement

and exchange rate balances. CEB methodologies and their cost

spending on liquid fuels was close to effectiveness are yet to be examined

USD 0.5 BN per year, and will in detail.

continue to rise.

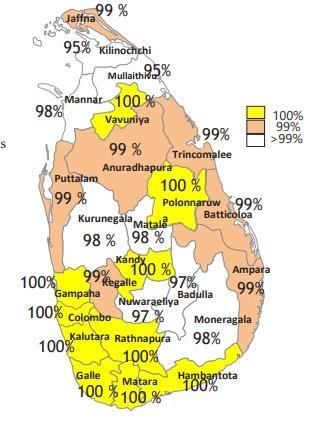

1.1 Accessibility to Power

During 2019 CEB reached out to all its prospective customers and hit an

electrification pace of 99.7 percent by the end of the year. Over the year the

number of buyers rose by 146,360 making the total number of customers as

6,500,641 at the year end. Throughout the year the CEB provided its customers

with electricity for the entire 24 hours of the day, except for occasional short-

term breakdowns.

FIGURE 01: ELECTRICITY ACCESSIBILITY

Source:Powermingov.lk

TABLE 01: ELECTRICITY FIGURE 02: SL PER CAPITA

CONSUMER BASE 2019 ELECTRICITY CONSUMPTION

Electricity Consumer 2018 2019 Increase in

Accounts accounts

2019

Domestic 5,543,137 5,651,452 108,315

Religious 39,422 40,724 1,302

General Purpose 704,173 739,122 34,949

Hotel 447 470 23

Industrial 62,570 64,241 1,671

Government 4,530 4,574 44

Agriculture - 56 56

Bulk Supply to LECO 1 1 0

Street Lighting 1 1 0

Total 6,354,281 6,500,641 146,360

Source: Statistical Digest 2019 Source: Generation Expansion Plan - 2019

FIGURE 03: ASIAN COUNTRIES

1.2 Electricity Per Capita

PER CAPITA ELECTRICITY

Consumption

CONSUMPTION:

The average per capita electricity

consumption in 2017 and 2018

were 626kWh per person and 650

kWh per person respectively.

Generally, it has been rising

steadily; however, in the period

2007 – 2009 amidst the slow down

of electricity growth, the per

capita consumption has stagnated.

A similar trend is observed during

2012 to 2013.

Figure 2 shows Sri Lanka's increase

in per capita electricity usage from

2004 through 2018. It is compared

to other Asian countries with

differences in per capita electricity

usage between 2004 and 2016 as Source: Generation Expansion Plan - 2019

shown in Figure 3.

1.3 Power Structure of Sri Lanka • A substantial amount of investment

Below figure depicts the key is needed to improve the existing

entities involved in the generation, power generation, transmission and

transmission and distribution of distribution system. Sri Lanka

power in Sri Lanka. therefore needs to promote greater

involvement of the private sector in

FIGURE 04: POWER the power sector. Sri Lanka will need

STRUCTURE to mobilize capital investments of

about USD 5.0 BN in generation, USD

1.1 BN in transmission, USD 229 MN

in distribution, and USD 512 MN in

proposed DSM programs to meet its

estimated demand for electricity in

2026. Such a large investment cannot

be financed only by public sector

funding.

• As the composition of world

electricity generation moves towards

renewable energy (RE), Sri Lanka

1.4 Key Challenges Faced by Sri

needs to look at ways of promoting

Lankan Power Sector

RE growth. While Sri Lanka is blessed

with numerous forms of renewable

• During adverse monsoon energy resources, there are no

seasons, costly power production research facilities within the country

methods using oil is mostly dedicated to RE growth.

adopted to offset low

hydroelectric power generation, • Slow roof-top solar production due

resulting in higher average power to lack of proper customer education

generation costs relative to other and limited options from commercial

countries. (~ 8.5 US cents / kWh in

2016, compared to ~ 5.5 in India banks for low cost financing. In spite

and ~ 6.5 in Bangladesh). of having regulations promulgating

rooftop solar adoption, Sri Lanka has

been unable to generate any gainful

momentum in the country's rooftop

solar deployment.

The high cost of rooftop solar • There are a large number of players

systems, combined with the lack of in the power sector and new

affordable financing or business licensees are on a tender basis for

models open to the public to build future projects. As a result, the

and use these systems, is one of

the primary reasons for this. entrance of new players would be

influenced by pricing and the benefit

will be marginal.

• There is a large gap between CEB

visionaries and industry

developers, which could slow

down the industry considerably.

Targets and objectives for the

power sector have not been

completely aligned among

stakeholders in the sector. The

2018 - 2037 long-term generation

plan was approved in June 2018

following lengthy deliberations

among sector stakeholders. Lack

of coordination between sectoral

entities can continue to delay

implementation of the project and

hinder commercial finance

mobilization.

• Sri Lanka lacks the domestic

potential to finance ambitious

commercial bank projects.

Without funding from multilaterals

and low-cost financing by

international banks, growth would

be difficult to achieve.

2. Global Power Generation Trends The energy world is changing… manufacturing industries. The last Regionally, over the coming years, 10 years have also witnessed a Asia Pacific is expected to be a drastic price drop as the experience leading contributor to the global and scope of renewable energy power generation market. Growing projects extended. demand for advanced power The global energy market has begun generation and distribution to evolve in encouraging ways, with infrastructure in Southeast Asian widespread renewable energy countries and constructive adoption and related technology government funding to develop the boding well for a sustainable future. power generation and distribution The global demand for new power networks in emerging economies generation capacity is being like India and China are the leading dominated by renewable drivers for the Asia Pacific power technologies. In many markets, solar generation market. power and wind power are rapidly In the coming years, steady growth the cheapest source of electricity, of the renewable energy sector is and most renewable energy sources likely to be a key feature of the Asia would be competitively priced at full Pacific power generation market, as cost. In 2019, as renewable the area is closer to the equator electricity production increased by than either North America or more than the growth in electricity Europe and thus has considerable demand, a new milestone was potential in terms of wind and solar reached, while fossil-fuel electricity generation. This is further aided by generation decreased. This is the the massive drop in renewable first time in decades that the energy costs and using electricity to production of fossil fuels has decarbonize the industry is decreased as the total generation of increasingly desirable, transport and electricity has increased.

FIGURE 05: RENEWABLES IN THE WORLD’S ENERGY MIX Source: IRENA Global Renewables Outlook Developed economies continued to be the early adopters of renewable energy technologies like wind, solar and biomass. Increasingly, however, in the 2010s, and particularly once costs have fallen to parity with fossil fuel alternatives, developing economies have chosen the baton up. Figure 6 shows that, for the first time in 2015, emerging economies accounted for the majority of global investment in renewable energy power, and have retained this since then. In 2019, out of a world total of $282.2 billion, they accounted for $152.2 billion, a 54 percent share. This was the same proportion as in 2018, but down from a 62 percent share in 2017. In 'other developing countries', except China and India, 2019 was the highest number ever for renewable capacity investment. This jumped 17% to $59.5 billion, and for 2016, it was double the equivalent amount.

FIGURE 06: GLOBAL INVESTMENT TRENDS IN RENEWABLE

ENERGY (in USD billions)

Source: UNEP, Bloomberg New Energy Finance

Further, a start-up based in New Zealand “Emrod” has developed a method of

transmitting electric power securely and wirelessly over long distances without

the use of copper wire, and is partnering with Powerco, the second largest

power distributor in the world to introduce it.

Emrod currently has a working prototype of its device, but will develop another

one for Powerco, with plans to produce by October 2020, and then spend

several months in laboratory testing before moving to a field trial. The prototype

system is said to be able to supply "quite a few kilowatts" of electricity, but can

be scaled up easily. Wireless transmission is, indeed, seen by Emrod as a key

enabling technology for renewable energy, which is often produced far from

where it is required. This kind of device could be a perfect way to get offshore

and remote renewable energy generation products into city grids without the

need for giant storage batteries and the like.3. Power Generation

System

3.1 Existing Power Generation along with the sources of power

System generation.

TABLE 02: POWER

The country's current generating GENERATION 2019

system is mainly operated by CEB

along with substantial private-sector

ownership. Until 1996 CEB owned

the entire electricity system. As of

1996, the private sector also

engaged in producing electricity to

meet the rise in electricity demand.

The country's existing generating

system has approximately 4,046

MW of installed capacity by 2019

including 610 MW non-dispatchable

plants operated by private sector

developers. CEB owns the bulk of

the dispatchable power, which

comprises 1,398.85 MW of hydro

and 1,504 MW of thermal Source: Statistical Digest 2019

generation capacity. Independent

Power Producers (IPPs) own However, the government of Sri

balancing dispatchable energy, Lanka, through the envisaged

which is totally thermal plants. renewable energy targets and

projected generation planning, has

Table 2 illustrates the breakdown of been pursuing a shift toward clean

contribution by CEB and IPP in 2019 power generation, including both

NCRE and LNG based generation.FIGURE 07: POWER GENERATION COMPOSITION OVER THE PAST YEARS Source: Revised LTGEP Sri Lankan Power System has operated maintaining 30%-60% share of renewable energy throughout the recent years. This trend will be continued in the future with the optimum amount of renewable energy integration to the system. FIGURE 08: RENEWABLE SHARE IN THE RECENT PAST Source: Revised LTGEP

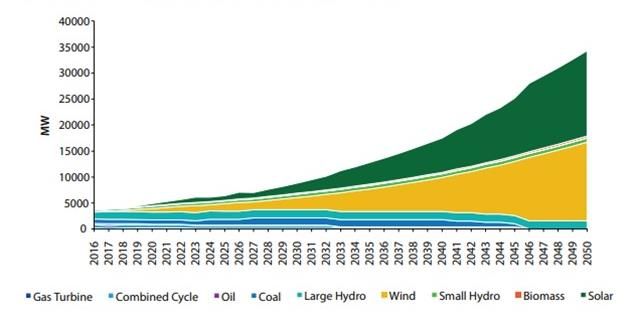

3.2 Power Generation • 4,199 MW of wind (1205 MW),

Expansion System solar (1389 MW) and gas (1605

MW) projects by 2037

FIGURE 09: SRI LANKA 2050

ELECTRICITY GENERATION

MIX: 100 PERCENT RE Additionally, base case also

estimates installation of 215 MW of

mini hydro, 85 MW of biomass, 822

MW of major hydro, 2.7 GW of coal

and 320 MW of oil-based generators

up to 2037.

Vision is to pave the way for Carbon

neutrality to be realized by 2050

according to the draft Energy Policy.

In 2016, the share of renewable

energy in power generation was

32%. Power generation facilities are

planned and implemented according

Source: Assessment of Sri Lankan Power Sector,

to CEB 's Long-Term Generation

UNDP Expansion Plan (2018-2037) to cater

for the growing electricity demand.

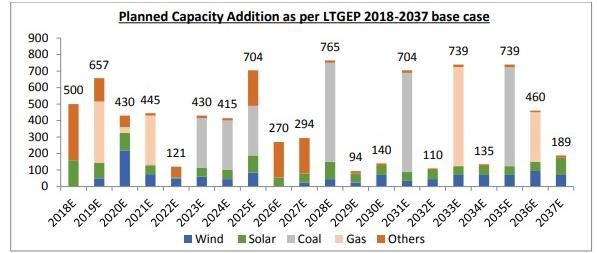

LTGEP 2018-2037 focuses on Main concern is given to the

diversifying the power mix and construction of optimal power

growing reliance on projects generating plants with minimum

relating to renewable energy and impact to the environment and all

gas. Base case under the 2018- plans are prepared to meet

2037 LTGEP provides for:

international obligations including

COP 21.

• 1,035 MW of wind (270 MW),

solar (360 MW) and gas (405

MW) projects by 2020

• 1,980 MW of wind (585 MW),

solar (690 MW) and gas (705

MW) projects by 2026FIGURE 08: PLANNED CAPACITY ADDITION AS PER LTGEP 2018-

2037 BASE CASE

Source: Assessment of Sri Lankan Power Sector, UNDP

Capital investment requirement is estimated based on the power generation

expansion plan. Total capital requirement includes capital costs expected to be

incurred for setting up the generation plants (including both conventional and

renewables). Additional investment will be required for operating plants and for

fuel related expenditure.

TABLE 03 :CAPITAL REQUIREMENTS OF POWER GENERATION

SEGMENTS

All Values in USD Power Generation

million

Solar Wind Gas Coal Others Total

Short term (till 360 351 631 - 424 1,767

2020)

Medium Term 690 761 756 1,100 1,724 5,041

(cumulative up

to 2026)

Long 1,389 1,567 1,881 2,700 2,056 9,564

Term(cumulative

up to 2037)

Source: Assessment of Sri Lankan Power Sector, UNDP4. Cost of Production, Selling Price, and Demand for Power 4.1 Cost of Production The average cost at selling point in 2017 and 2018 were Rs. 20.34 per 1 kWh and Rs.19.12 per 1 kWh respectively. Following table depicts the generation cost of one kwh for several power stations during 2016. TABLE 04: POWER GENERATION COST OF SEVERAL POWER STATIONS DURING 2016 Source: Generation Performance in Sri Lanka-2016

4.2 Selling Price Block Tariff

The average selling price per unit in Consumption blocks are based on a

2017 and 2018 were Rs. 16.26 per 1 30-day billing period and the number

kWh and Rs.16.29 per 1 kWh of units in a block would be prorated

respectively. according to the number of dates in

FIGURE 09: COST OF POWER VS each billing period.

END USER PRICING ( US

Cents/kWh) Domestic Low Users (if monthly

consumption is 60 units per

month or less than 60 units)

Consumption Energy Charge Fixed Charge

per month (LKR/kWh) (LKR/month)

(kWh)

0-30 2.50 30.00

31-60 4.85 60.00

Source: pucsl..gov.lk

Source: World Bank

Domestic-Users over 60 units per

month

4.2.1 End User Tariff Structure

Consumption per Energy Charge Fixed Charge

month (kWh) (LKR/kWh) (LKR/month)

Used for domestic purposes in

private residences. There are two

0-60 7.85 -

types of Domestic Tariff Categories.

61-90 10.00 90.00

1. Block Tariff 91-120 27.75 480.00

2. Time of Use Tariff (TOU): 121-180 32.00 480.00

The optional tariff for domestic More Than 180 45.00 540.00

consumers

Source: pucsl..gov.lkOptional Time of Use (ToU) Tariff Consumption per Energy Charge Fixed Charge

for Domestic Customers month (kWh) (LKR/kWh) (LKR/month)

Team of Use (ToU) Energy Fixed 0-30 1.90 30.00

Charge Charge 31-90 2.80 60.00

(LKR/kWh) (LKR/month 91-120 6.75 180.00

) 121-180 7.50 180.00

Off Peak (22.30-5.30 13.00 More Than 180 9.40 240.00

hrs) 540.00 Source: pucsl..gov.lk

Day (5.30-18.30 hrs) 25.00

Peak (18.30 -22.30 hrs) 54.00

3. Hotels

Source: pucsl..gov.lk

Customer Category H-1

2. Religious and Charitable This rate shall apply to supplies at

each individual point of supply

delivered and metered at 400/230

The tariff will be charged on Volt nominal and where the

Incremental Block Tariff basis. This contract demand is less than or

rate shall apply to supplies of equal to 42 kVA.

electricity to,

Energy Charge Fixed Charge Maximum

• places of public religious (LKR/kWh) (LKR/month) Demand

worship including private Charge Per

month(

residences of priests where such

LKR/kVA)

residences are associated with or 21.50 600

are within the place of public

religious worship,

Source: pucsl..gov.lk

• Homes for aged, orphanages Customer Category H-2

and homes for the handicapped, This rate shall apply to supplies at

which are specifically certified by each individual point of supply

the Director of Social Services as delivered and metered

charitable institutions, and the 400/230 Volt nominal and where

installation should not include any the contract demand exceeds

building used for commercial 42kVA.

purposes.Time Interval Energy Fixed Maximum Customer Category I-2

Charge Charge Demand Charge This rate shall apply to supplies at each

(LKR/k (LKR/mo Per month(

individual point of supply delivered

Wh) nth) LKR/kVA)

Peak 18.30- 23.50

and metered at 400/230 Volt nominal

22.30 and where the contract demand

Day 5.30-18.30 14.65 exceeds 42 kVA.

Off-peak22.30- 9.80 3,000 1,100

Time Energy Fixed Maximum Demand

5.30

Interval Charge Charge Charge Per month(

Source: pucsl..gov.lk (LKR/kW (LKR/mon LKR/kVA)

Customer Category H-3 h) th

Peak 20.50

This rate shall apply to supplies at (18.30-

each individual point of supply 22.30)

Day (5.30- 11.00

delivered and metered at 11,000 18.30)

Volt nominal and above. Off-peak 6.85 3,000 1,100

(22.30-

Time Interval Energy Fixed Maximum 5.30)

Charge Charge Demand Charge Source: pucsl..gov.lk

(LKR/kW (LKR/mon Per month(

Customer Category I-3

h) th) LKR/kVA)

Peak (18.30- 22.50 This rate shall apply to supplies at each

22.30) individual point of supply delivered

Day (5.30-18.30) 13.70 and metered at 11,000 Volt nominal

Off-peak(22.30- 8.80 3,000 1,100

and above.

5.30) Time Energy Fixed Maximum Demand

Source: pucsl..gov.lk Interval Charge Charge(LK Charge Per month(

(LKR/kW R/month LKR/kVA)

4.Industrial Consumers h

Peak 23.50

Customer Category I-1 (18.30-

22.30)

This rate shall apply to supplies at Day (5.30- 10.25

18.30)

each individual point of supply Off-peak 5.90 3,000 1,000

delivered and metered at 400/230 (22.30-

5.30)

Volt nominal and where the Source: pucsl.gov.lk

contract demand is less than or

5.General Purpose

equal to 42 kVA.

Consumptio Energy Fixed Maximum

Supply of electricity to be used in

n per Charge Charge Demand Charge shops, offices, banks, warehouses,

month(kWh (LKR/kWh (LKR/month Per month public buildings, hospitals, educational

establishments, places ofCustomer Category GP-1 Time Interval Energy Fixed Maximum

Charge( Charge(L Demand Charge

This rate shall apply to supplies at LKR/kW KR/mont Per month(

each individual point of supply h h) LKR/kVA)

Peak (18.30- 25.50 3,000 1,000

delivered and metered at 400/230 22.30)

Volt nominal and where the Day (5.30- 20.70

contract demand is less than or 18.30)

Off-peak 14.35

equal to 42 kVA. (22.30-5.30)

Source: pucsl..gov.lk

Consumption Energy Fixed Maximum

per Charge Charge Demand

month(kWh) (LKR/kWh (LKR/mo Charge Per 6.Government

) nth) month(

LKR/kVA) Supply of electricity to be used in

Less than or 18.30 240 - schools, hospitals, vocational

equal 300

More than 22.85 training institutions, and

300 universities, which are fully owned

Source: pucsl..gov.lk by the Government and funded

through the national budget and

Customer Category GP-2 provide their services free of charge

This rate shall apply to supplies at to the general public.

each individual point of supply Customer Category GV-1

delivered and metered at 400/230

Volt nominal and where the This rate shall apply to supplies at

contract demand exceeds 42 kVA. each individual point of supply

delivered and metered at 400/230

Time Interval Energy Fixed Maximum Demand Volt nominal and where the

Charge Charge Charge Per month(

(LKR/k (LKR/m LKR/kVA)

contract demand is less than or

Wh) onth) equal to 42 kVA.

Peak (18.30- 26.60 3,000 1,100

22.30)

Day (5.30- 21.80 Energy Charge Fixed Charge Maximum

18.30) (LKR/kWh) (LKR/month) Demand Charge

Off-peak 15.40

Per month(

(22.30-5.30)

LKR/kVA)

Source: pucsl..gov.lk 14.65 600

Customer Category GP-3

This rate shall apply to supplies at Source: pucsl..gov.lk

each individual point of supply

delivered and metered at 11,000

Volt nominal and above.Customer Category GV-2

Day (0530-1830 hrs) 30.00

This rate shall apply to supplies at Level 2

each individual point of supply AC

Peak (1830-2230 hrs) 55.00

delivered and metered at 400/230 Charging

Volt nominal and where the

contract demand exceeds 42 kVA. Off peak (2230-0530 hrs) 20.00

Energy Charge Fixed Charge Maximum Source: pucsl..gov.lk

(LKR/kWh) (LKR/month) Demand Charge

Per month( 4.3 Average Selling Price Vs

LKR/kVA) Average Cost at Selling Point

14.55 3000 1100

FIGURE 10: AVERAGE SELLING PRICE VS

AVERAGE COST OVER THE PAST YEARS

Source: pucsl..gov.lk

25

Customer Category GV-3 Avg Selling Price Vs Avg Cost 20

15

This rate shall apply to supplies at Average Selling

Price Per

each individual point of supply 10 Unit(Rs/kWh )

delivered and metered at 11,000 5 Average Cost Per

Unit (@ selling

Volt nominal and above. 0 point)(Rs/kWh )

Energy Charge Fixed Charge Maximum

(LKR/kWh) (LKR/month) Demand Charge Year

Per month(

Generally, average cost per 1 kwh at

LKR/kVA)

14.35 3000 1000

selling point is rising steadily;

however, in the period 2015 and

Source: pucsl..gov.lk

2018 it has been reduced by 24.7

percent, 6 percent respectively. An

Commission approved Electricity increasing trend is observed with

Tariff for the customers who are average selling prices per 1 kwh

charging their vehicles at CEB over the period.

owned charging stations. 4.4 Comparison of Selling Prices

Tariff Charge

Category

TOU Time Period

(LKR/kWh) SL selling prices of 1 kWh for

Day (0530-1830 hrs) 50.00

households and Businesses (as at

DC Fast

Dec. 2019) is compared to

Peak (1830-2230 hrs) 70.00

Charging benchmark countries depicted in

Off peak (2230-530 hrs) 30.00 Figure 11.FIGURE 11: SELLING PRICE COMPARISON WITH BENCHMARK

COUNTRIES

0.16

0.14

0.12

0.1

0.08

0.06

0.04

0.02

0

Country

Household, kWh Business, kWh

4.5 Demand for Power

Total power demand in Sri Lanka increased by 12,785 GWh in 2016 during the

period 2011-16 at a CAGR of 5.0 per cent. CEB has forecasted power demand to

rise to 50.978 GWh by 2044 at a CAGR of about 5.0 per cent.

FIGURE 12: POWER DEMAND EVOLUTION (2011-2016)

-

14000 12785

11786

12000 10624 11063

10026 10475

10000

8000

6000

4000

2000

0

2011 2012 2013 2014 2015 2016

Source: Sri Lanka Energy Infrasap,World Bank

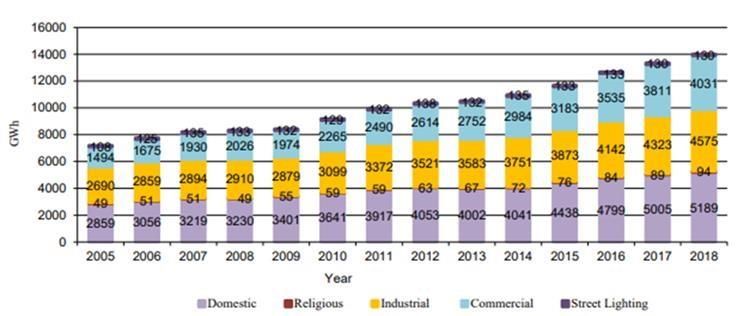

The sectoral contribution to the existing demand is highlighted below.FIGURE 13: SECTORIAL CONSUMPTION OF ELECTRICITY 2005-2018

Source: Generation Expansion Plan 2019

FIGURE 14: SECTORIAL CONSUMPTION OF ELECTRICITY 2018

Source: Generation Expansion Plan 2019

These Figures reveal that the cumulative industrial and commercial

(general purpose, hotel, government) sectors’ electricity consumption is

much more than the electricity consumption by the domestic sector.4.6 Demand Projections Development Project, Administrative

Cities Development Project, Multi

The Government has proposed Model Transport Hub (Pettah) and

and planned for large scale Science and Technology City) under

development projects, which will the Capital City and Colombo

lead to an increase of electricity Commercial City development

demand in the future. The major programs of Ministry of Megapolis and

development plans are mainly Western Development are indicatively

identified by Western Region estimated as 121MW for 2018-2022,

Megapolis Plan and Hambantota 399MW for 2023-2026 and 508MW

Port Development Plan in for 2027-2030 period.

Southern Region. The Western

Region Megapolis Plan identifies The Colombo Port City Development

following major areas for the Project is a major development

development. project under the Western Region

Megapolis Plan and indicate

• Multi Model Transport Hub cumulative electricity demand

(Pettah) requirement estimated as 30MW by

• Administrative Cities 2020, 177MW by 2025, 313MW by

Development Project 2030 and 393MW by 2040.

Hambantota Port Development Plan in

• Science and Technology City

Southern Region also estimated

• Maritime City Development approximately 400MW electricity

Project demand for the initial stage in the

• Colombo Central Business present development plan. The

District Electricity Demand Forecast 2020-

2044 was prepared considering the

• Housing Development phase development of the above

• Horana & Mirigama Industrial large-scale projects. During the

Township detailed planning stages, it is required

to identify the time-based load

• SME Industry requirement to determine the load

• Colombo Port City pattern which would impact on actual

electricity demand.

• Transport

Different demand forecast scenarios

• Tourism were planned in the power generation

The cumulative electricity demand expansion plan 2019, taking into

requirements for the identified account growth rate variations in the

projects (Maritime City baseline demand forecast, long-term

trend approach,end-user approach, and those listed FIGURE 15 : GENERATION

below.

FORECAST OF LOW, HIGH,

1. High Load Forecast - The forecast LONG TERM TIME TREND AND

developed considering 1% higher MAED WITH BASE

economic growth of the country

beyond 2022 and economic sector

change based on higher growth in

Industrial and Service sector in future.

2. Low Load Forecast - The forecast

developed considering 1% reduction

from the annual growth rate of Base

Load Forecast.

3. Long Term Time Trend Forecast -

The forecast developed purely based Source: Generation Expansion Plan 2019

on the time trend approach using the

past 25-year electricity demand FIGURE 16 :PEAK DEMAND

figures starting from 1993. FORECAST OF LOW, HIGH,

LONG TERM TIME TREND AND

4. MAED Load Projection – The MAED WITH BASE

projection derived from MAED

software by considering end user

energy demand data and identifying

technological, economic and social

driving factors influencing each

category of final consumption and

their relations to the final energy.

For the above four scenarios,

including the Base Load Forecast,

Figure 15 & Figure 16 graphically

displays the power production and Source: Generation Expansion Plan 2019

peak load forecast.5. Power Distribution and

Collection

4.5 Distribution of Power Division Province Area

North Western Chilaw,Kurunegala,Kuliyapi

tiya,Wariyapola,Puttlam

and Narammala

Major part of the country's Distribution

Division 1 North Central Anuradapura,Kekirawa and

electricity distribution is handled by Minneriya

CEB amounting to 88 per cent of the North Jaffna,Kilinochchi and

overall sales volume, while the rest Vavuniya

is managed by the subsidiary of CEB, Colombo City Colombo North, Colombo

South,Colombo West and

Lanka Electricity Company Ltd Colombo East

(LECO). Distribution licensees are

responsible for supplying end user Division Province Area

power and receiving end user

Eastern Ampara,Batticaloa,Trincomalee

revenue. and Kalmunai

Central Province Kegalle,Mawanella,Kandy

For ease of administration and Distribution

Division 2 City,Peradeniya,Kundasale,Katug

service, the entire CEB distribution astota,Galagedara,Matale,Damb

ulla,Nuwaraeliya,Ginigathena,Na

system is geographically divided into walapitiya

four Divisions; Distribution Division

Western Province North Gampaha,Kelaniya,Negombo,Ja-

1 (DD1), Distribution Division 2 ela,Divulapitiya and Veyangoda

(DD2), Distribution Division 3 (DD3),

and Distribution Division 4 (DD4).

The key aim of creating the four Division Province Area

Divisions is to achieve benchmark Western

South II

Province Bandaragama,Homagama,Avi

ssawella Sri

competitiveness that can boost Distribution

Division 3

Jayawardenapura,and

consumer efficiency and supply Horana

quality.

Sabaragamuwa Ratnapura,Kahawatte,Ruwan

wella,Eheliyagoda and

Embilipitiya

Uwa Badulla,Diyatalawa,Monarag

alaDivision Province Area

Southern Province Ambalangoda,Galle,Hambant

hota,Matara,Tangalle,Akures

Distribution

sa(formally Weligama) and

Division 4

Baddegama

Western Province South I Ratmalana,Kalutara and

Dehiwala

Source:Powermingov.lk

5.2 Collection

The CEB's collection agents, Sampath

Bank, National Development Bank

(NDB), and National Savings Bank

(NSB), have introduced real-time

online (OLRT) monitoring of consumer

electricity bill payments over the year.6. Regulator of the

Electricity Industry of Sri

Lanka

Public Utilities Commission of Sri Lanka (PUCSL) is the economic, technical and

safety regulator of the electricity industry. The Commission regulates the

industry through licenses, regulations, rules and methodologies.

Economic

Regulation

PUCSL

Mandate

Technical Safety

Regulation Regulation

Price

Regulation

Safety Regulation

Technical & Safety

Economic Regulation

Regulation

Market Service

Regulation Quality Technical Quality

RegulationOUTCOMES OBTAINED BY PUCSL 1. Improved productivity & convenience for electricity consumers. 2. Affordable Price for consumers and sustainable financial stability for licensees. 3. Improved safety of every living being and properties of general public, licensees & operators. 4. Improved environmental conditions for humans, animals and plants.

7. Mini Hydro Projects in

the Industry

Sri Lanka is blessed at a local generation of colonial-era large-scale

location relative to rains in the tea plantations. Since then, until the

interior of, in addition to especially 1960s, the limited hydro capacity

around the central mountainous steadily expanded until the expansion

regions. Heavy rains and the sloping of the power grid to provide power.

nature of the land have resulted in a

CEB 's assistance to the development

series of small and large streams

carrying water throughout the year, of the Mini hydropower sector was

enabling a variety of reservoirs to given in the 1990s with the necessary

produce and meet significant assistance to the private sector, which

sections of the energy needs of the involved training & capacity building,

country. Although the government is pre-feasibility studies, and resource

carrying out large-scale power assessments. Beginning in 1997, the

generation projects, the private process for the purchasing of electricity

sector has been approved for from Small Power Producers (SPPs) by

projects with a capacity of under 10

the CEB was regularized by the

MW. Many local organizations are

pursuing potential locations and publication of the Uniform Power

selling the generated energy to the Purchase Agreement (SPPA), which

Ceylon Electricity Board when the included a scheme to measure the

green light is provided, building and purchase price based on the concept of

installing power plants. avoided costs. Further, 2006 National

Energy Policy established fuel

diversification and energy security in

Sri Lanka's history of small

electricity generation as a strategic

hydropower generation extends

over a century and is largely target and as part of this strategy the

associated with the power development of renewable energy

projects was established. In view ofthe above, the implementation of a Minihydro capacity is expected to three-tier tariff was introduced grow moderately over the next instead of the avoided cost-based twenty years in the long-term tariff with effect from 2008. Both generation expansion plan, as most of large-scale hydropower generation the attractive resources and sites facilities will remain under have already been established. government control for the near future, and the private sector will be responsible for the construction of small hydropower plants. Currently the technology specific cost reflective tariff introduced in 2012 is in force. The geo-climatic condition in Sri Lanka is favorable for the mini hydro development and several past studies have assessed the potential for the development of mini-hydro resources. A comprehensive study was conducted as part of the hydropower portion of the Ministry of Irrigation and Water Resources' Dam Safety and Water Resources Planning (DSWRP) project, focusing on the country's 13 river basins, and the study concluded that the country's total Minihydro capacity is 873MW. The total grid-connected Mini hydro capacity at the end of 2018 is 393.5 MW, comprising 368.5 MW built by the private sector and 25 MW under the multi-development project Moragahakanda Kaluganga Development by the relevant Ministry of Mahaweli Development and Environment with the Mahaweli Authority of Sri Lanka.

7.1 List of Mini Hydro projects undertaken by Listed Power Companies in

Sri Lanka

TABLE 05:LIST OF MINI HYDRO PROJECTS UNDERTAKEN BY

LISTED POWER COMPANIES

Power Project Ownership Generation Location River Catchment Plant Commissioning

Capacity Factor Year

Bambarabatuoya Vidullanka 3.2 Mw Rathnapura Kalu Ganga, 44% 1-Jun-2001

MHPP PLC Bambarabatuoya

Rideepana MHPP Vidullanka 1.75 Mw Badulla Badulu Oya 4% 15-May-2015

PLC

Lower Kothmale MHPP Vidullanka 4 MW Kotmale, Kothmale Oya 37% 25-Jun-2014

PLC Nuwara-Eliya

Madugeta MHPP Vidullanka 2.5 MW Neluwa, Gin Gange 46% 1-Nov-2013

PLC Galle

Wembiyagoda MHPP Vidullanka 1.3 MW Kalawana, Koswathu Ganga 40% 19-Mar-2013

PLC Ratnapura

Ganthuna MHPP Vidullanka 1.2 MW Ganthuna, Gurugodaya 38% 26-Mar-2010

PLC Aranayake,

Kegalle

Ethamala Ella Vidullanka 2 MW Matara Nilwala Ganga 44% 30-Sep- 2016

PLC

Batatotha MHPP Vidullanka 2.0 MW Kuruwita, Kuru Ganga 58% 6-Mar-2007

PLC Ratnapura

Udawela MHPP Vidullanka 1.4MW Badulla Badulu Oya 45% 29-Dec-2017

PLC

Upper agra oya Resus 2.6 MW Lindula, Agra Oya 39% 01-Feb-2006

hydropower project Energy PLC Thalawakele

Giddawa hydropower Resus 2.0 MW Giddawa, Huluganga 45% 01-Oct-2008

project Energy PLC Teldeniya

Upper magal ganga Resus 2.4 MW Dikellakanda. Magal Ganga 40% 01-Sep-2011

hydropower project Energy PLC Maliboda

Gomale oya Resus 1.4 MW Magala, Gomale Oya 30% 01-Aug-2016

hydropower project Energy PLC Maliboda

Moragaha oya Resus 1.5 MW Panvila, Moragaha Oya 35% 01-Mar-2017

hydropower project Energy PLC KandyRanawala oya Resus 1.2 MW Maliboda, Ranwala Oya 37% 29-Nov-2018

hydropower project Energy PLC Deraniyagala

Upper hulu ganga Resus 1.9 MW Panwila, Kandy Hulu Ganga 35% 25-July-2019

hydropower project Energy PLC

Rathganga MHP Panasian 3 Mw Ratthurugala, Rathganga 45% 2004

Power PLC Ratnapura

Manelwala MHP Panasian Walapane,Nuwa Kurundu Oya 38% 2008

Power PLC ra Eliya

Padiyapelella MHP Panasian 3.5 Mw Padiyapelella, Beliul Oya 43% 2017

Power PLC Nuwara Eliya

Erathna mhpp Vallibel 9.9 MW Kuruwita, Kuru Ganga N/A 2004

Power Rathnapura

Erathna PLC

Denawaka ganga mhpp Vallibel 7.2 MW Malwala, Denawaka Ganga N/A 2012

Power Rathnapura

Erathna PLC

Kiriwaneliya mhpp Vallibel 4.65 Norton Bridge, Maskeli Oya N/A 2011

Power MW Nuwara Eliya

Erathna PLC

Ginigathhena Laugfs 0.7 MW Ginigathhena N/A N/A 2017

Power PLC

Ranmudu Oya Phase 1 Laugfs 0.5 MW Balangoda N/A N/A 2017

Power PLC

Ranmudu Oya Phase 3 Laugfs 0.55 Balangoda N/A N/A 2017

Power PLC MW

Belihul oya LVL Energy 2.2 MW Balangoda Horton Plains 47% May 2002

Fund PLC

Assupini ella LVL Energy 4.0 MW Gampola and Maha Oya 47%. November

Fund PLC Mawanella 2005

Kadawala LVL Energy 6 MW Watawala and N/A 25% March 2008

Fund PLC Kadawala

Neluwa LVL Energy 2.2 MW border of Galle Gin Ganga 33% January 2008

Fund PLC and Kalutara

Theberton LVL Energy 1.3 MW Kiriwaneliya N/A 41% September

Fund PLC 2015

Campion LVL Energy 1.2 MW Bogawantalawa Kehelgamuwa Oya 45%. May 2017

Fund PLC

Bambarapana LVL Energy 2.5 MW Bambarapana, Uma Oya 41%. February 2018

Fund PLC Badulla7.2 Small Hydro Power 6 Zyrex Power (Pvt.) Ltd. N/A

Developers Association (SHPDA) 7 Elpitiya Plantations 4.46 Mw

The Small Hydro Power Developers

8 Lotus Hydro Power Plc. 4.9 Mw

Association (SHPDA), representing

(Formerly known as Hydro

the major local power generators Power Free Lanka / Browns

of renewable energy in Sri Lanka, Hydro Power Plc.)

seeks to jointly work with relevant

state authorities to formulate and 9 Natural Power (Pvt.) Ltd. N/A

implement appropriate national 10 Dunsinane Power Co. (Pvt.) N/A

Ltd.

renewable energy policies. SHPDA 11 Midland Energy (Pvt.) Ltd. N/A

members currently supply 12 Vallibel Power Erathna Plc. 21.85 Mw

approximately 10% of the nation’s 13 Serendib Energy (Pvt.) Ltd. N/A

demand, saving millions of dollars in 14 Weswin Power (Pvt.) Ltd. N/A

foreign exchange to the country 15 Agraoya Hydro Power N/A

annually. Moreover, small (Pvt.) Ltd.

16 Santak Power (Pvt.) Ltd. N/A

hydropower projects, while being 17 Energy Reclamation (Pvt.) N/A

environmentally friendly, have Ltd.

stimulated tangible economic 18 Hydro Trust Lanka (Pvt.) 4 MW

progress among rural Sri Lankan Ltd.

communities. Table 06 includes the 19 WKV Hydrotechnics (Pvt) 43.4 Mw

Ltd.

members of Small Hydro Power 20 Samangiri Hydro Electrical N/A

Developers Association. Co. Pvt

21 Hynford Water Power N/A

TABLE 06: MEMBERS OF SMALL (Pvt.) Ltd.

HYDROPOWER DEVELOPERS 22 Resus Energy Plc. 13 MW

ASSOCIATION (Formerly known as

Hemas Power Plc.)

Company Installed 23 Falcon Valley Hydro N/A

capacity in mini 24 Bogo Power (Pvt.) Ltd. N/A

hydro projects 25 Vidullanka Plc 32.35 Mw

1 Access Energy (Pvt.) Ltd. N/A

2 Eco Power (Pvt.) Ltd. 58.2 Mw 26 Mark Hydro (Pvt.) Ltd / N/A

3 Recogen Haycarb (Pvt.) N/A Mark Marine Services Pvt.

Ltd. Ltd.

4 Hydrodynamics (Pvt.) Ltd. N/A 27 Royali Power (Pvt.) Ltd. N/A

5 Saman Jala Viduli Co. N/A 28 Branford Hydro Power N/A

(Pvt.) Ltd. (Formerly (Pvt.) Ltd.

known as Hydro Tech

Lanka Dickoya)29 Hayleys Power Ltd. 9.5 MW 7.3 Cyclin impact on the hydro power

(Formerly known as projects

Hayleys Industrial

Solutions)

30 Panasian Power Plc. 8.9 Mw

Although an assessment of a project's

31 Waltrim Hydropower 6.6 MW technological viability would be

(Private) Ltd. Formerly straight forward, the climate

known as Sunshine Power

conditions could be highly

(Pvt.) Ltd.

32 Terraqua International N/A complicated.

(Pvt.) Ltd. The climate of Sri Lanka is marked by

33 Sujalashakthi (Pvt.) Ltd. N/A

34

the southwest monsoon and

Wellawaya Hydro Power N/A

Pvt. Ltd. northeast monsoon. The Climate

35 Castle Power House (Pvt.) 11.85 Mw experienced during the 12 months

Ltd. period in Sri Lanka can be

36 Energy Generators (Pvt.) N/A characterized in to 4 climate seasons

Ltd.

37 Laugfs Power Ltd. 1.75 Mw

as follows.

38 Ceylex Engineering Pvt. 7.5 MW

Ltd. (LTL Power) 1. First Inter-monsoon Period (March

39 Magalganga Power (Pvt.) N/A to April)

Ltd.

40 Bhoruka Power Lanka N/A Arm and uncomfortable conditions,

(Pvt.) Ltd. with thunderstorm-type rain,

41 Hiran Power (Pvt.) Ltd. N/A

42 Nilwala Vidulibala N/A

particularly during the afternoon or

Company (Pvt.) Ltd. evening, are the typical weather

43 Eskey Power Generators N/A conditions during this season. The

Pvt. Ltd. distribution of rainfall during this

44 Fair Energy Developers N/A period shows that the entire South-

Pvt. Ltd.

45 Campion Hydro Pvt. Ltd. N/A

western sector at the hill country

46 Escas Owala Pvt. Ltd. N/A receiving 250 mm of rainfall, with

47 Mossiville Hydro Power N/A localized area on the South-western

Pvt. Ltd. slopes experiencing rainfall in excess

48 Aqua Power Pvt. Ltd. N/A of 700 mm (Keragala 771 mm). Over

49 Meunex Nahawathura N/A most parts of the island, the amount

Hydro Power Pvt Ltd.

50 Hydro Jet Power Pvt. Ltd. N/A

of rainfall various between 100 and

250 mm, the notable exception being

the Northern Jaffna Peninsula (Jaffna-

78 mm, Elephant pass- 83 mm).5-month long period. Lowest figures are

recorded from Northern and

Southeastern regions.

Source: http://www.meteo.gov.lk/

2. Southwest Monsoon Period

(May to September)

Source: http://www.meteo.gov.lk/

Windy weather during this

monsoon eases off the warmth

that prevailed during the 1st Inter 3. Second Inter-monsoon Period

monsoon season. Southwest (October to November)

monsoon rains are experienced at

any time of the day and night, The thunderstorm-type of rain,

sometimes intermittently mainly particularly during the afternoon or

in the Southwestern part of the evening, is the typical climate during

country. Amount of rainfall during this season. But unlike in the Inter-

this season varies from about 100 monsoon season, the influence of

mm to over 3000 mm. The highest weather system like depression and

rainfall received in the mid- cyclones in the Bay of Bengal is

elevations of the western slopes common during the second

(Ginigathhena- 3267 mm, Intermonsoon season. Under such

Watawala- 3252 mm, Norton- conditions, the whole country

3121 mm). Rainfall decreases experiences strong winds with wide

rapidly from these maximum spread rain, sometimes leading to

regions towards the higher floods and landslides. The second

elevation, and in Nuwara-eliya, it Intermonsoon period of October –

drops to 853 mm. The variation November is the period with the most

towards the Southwestern coastal evenly balanced distribution of rainfall

area is less rapid, with the over Sri Lanka. Almost the entire island

Southwestern coastal belt receives in excess of 400 mm of rain

experiencing between 1000 mm during this season, with the

to 1600 mm of rain during this Southwestern slopes receivinghigher rainfall in the range 750 the minimum is in the Western

mm to 1200 mm (Weweltalawa coastal area around Puttalam (Chilaw-

Estate in Yatiyantota recording 177 mm) during this period.

1219 mm)

Source: http://www.meteo.gov.lk/

Source: http://www.meteo.gov.lk/

Seasonal Rainfall

4. North-East Monsoon Period

(December to February) The rainfall pattern is influenced by

the monsoon winds of the Indian

The dry and cold wind blowing Ocean and Bay of Bengal and is

from the Indian land-mass will marked by four seasons. The first is

establish a comparatively cool, but from mid-May to October, when

dry weather over many parts winds originate in the southwest,

making the surrounding pleasant bringing moisture from the Indian

and comfortable weather except Ocean. When these winds encounter

for some rather cold morning the slopes of the Central Highlands,

hours. Cloud-free skies provide they unload heavy rains on the

days full of sunshine and pleasant mountain slopes and the

and cool night. During this period, southwestern sector of the island.

the highest rainfall figures are Some of the windward slopes receive

up to 250 centimeters of rain per

recorded in the North, Eastern

month, but the leeward slopes in the

slopes of the hill country and the

east and northeast receive little rain.

Eastern slopes of the The second season occurs in October

Knuckles/Rangala range. The and November, the inter-monsoonal

maximum rainfall is experience at months. During this season, periodic

Kobonella estate (1281 mm), andsqualls occur and sometimes

tropical cyclones bring overcast tape. Whenever a developer finds a

skies and rains to the southwest, potential site for a hydropower

northeast, and eastern parts of the project, they must examine the

island. During the third season, feasibility and apply an application for

December to March, monsoon construction to the sustainable

winds come from the northeast, energy Authority (SEA), which would

bringing moisture from the Bay of grant a provisional approval (PA).

Bengal. The northeastern slopes of With the PA, the developer will now

the mountains may be inundated

be applying for a CEB Letter of Intent

with up to 125 centimeters of rain

during these months. Another and Central Environmental Authority

inter-monsoonal period occurs (CEA) environmental approval.

from March until mid-May, with The CEA will refer the application to

light, variable winds and evening another authority serving as Agency

thundershowers. for Project Approval (PAA). The PAA

sets in scope meetings and

government agencies from which the

developer needs to seek project

approval, which will include no

objections from the Grama Sevaka

and Divisional Secretary calling public

meetings. PAA will also provide Terms

of Reference (TOR) for an initial

report on environmental assessments

(IEER).

Source: http://www.meteo.gov.lk/

The developer shall submit the IEER

7.4 Approval Process of a mini- to PAA along with other approvals to

hydro Project be reviewed by the Technical

Assessment Committee (TEC)

Obtaining recognition and appointed by PAA.

approval of a mini-hydro power

project requires lengthy Environmental clearance for the

inspections as outlined below, Energy Permit (EP) shall be given to

and going through loads of red CEA if approved.The developer is required to begin physical construction at the proposed site upon receipt of EP. The developer would submit Public Utility application from the Public Utilities Commission of Sri Lanka (PUCSL) for Energy License and apply for signing a Power Purchase Agreement with the CEB. 7.5 Factors to consider by an investor who is looking to have exposure to the mini hydro sector If an investor is going to purchase an already established plant, the historical generation of the plant or the plant factors need to be considered. Once the technical feasibility of undertaking the project is done, marginal cost and benefit analysis needs to be performed. If only marginal cost of generating 1 Mw is less than the additional revenue it generates, the project is feasible. Most of the locations of the projects are inaccessible and developers need to create roads or upgrade existing footpaths to allow vehicles and equipment for construction. Power generators are very heavy and the operation of the plant requires daily access after completion, therefore proper roads are required.

8. Wind Projects in the

Industry

More than a century ago, wind generating electrical energy.

turbines first appeared. In the

1830s, after the invention of the Depending on the size of the turbine

electric motor, engineers began

trying to harness wind energy to and the length of its blades, the

generate electricity. Wind power amount of power which can be

generation took place in the United harnessed from the wind is

Kingdom and the United States in determined. The output is

1887 and 1888, but in Denmark, proportional to the rotor's

where horizontal-axis wind turbines dimensions and to the wind speed

were built in 1891 and a 22.8-metre cube. In principle, as wind speed

wind turbine began operation in doubles, the capacity for wind

1897, modern wind power is power increases by a factor of eight.

considered to have been first

developed.

Wind-turbine capacity has increased

Using the kinetic energy created by over time. Typical turbines had a

air in motion, wind is used to nominal capacity of 0.05 megawatts

produce electricity. Using wind

turbines or wind energy conversion (MW) and a 15-metre rotor

devices, this is converted into diameter in 1985.

electrical energy. Wind first hits a

turbine’s blades, causing them to The turbine potential of today's

rotate and turn the turbine latest wind power projects is around

connected to them. This converts 2 MW onshore and 3-5 MW

kinetic energy into rotational energy offshore. Commercially available

by rotating a shaft connected to a wind turbines with rotor diameters

generator and, by electromagnetism of up to 164 meters have achieved a

capacity of 8 MW. In iron smeltingfucentury B.C., Sri Lanka is the capacity is economically exploitable.

country which first used wind for The Ceylon Electricity Board has

industrial use. established these possible exploitable

wind resources and, along with the

The National Renewable Energy expansion of transmission networks,

Laboratory (NREL) of the USA has prioritized their growth activities.

developed the All Island Wind Energy Harnessing the exploitable wind

Resource Atlas of Sri Lanka in 2003, power potential is then subjected to

suggesting nearly 5,000 km2 of windy various technical constraints such as

areas with good-to-excellent potential power systems stability, power

for wind resources in Sri Lanka. Of the system operation, seasonality and

total windy area, approximately 4,100 variability. This technical potential is

km2 is on land and about 700 km2 is defined by the renewable energy grid

in lagoons. The windy land represents integration study conducted by the

about 6 percent of Sri Lanka's total Ceylon Electricity Board.

land area (65,600 km2). Using a

conservative estimate of 5 MW per In the next 20-year period, Mannar

km2, nearly 20,000 MW of potential and Northern areas will be focused

installed capacity could be provided for wind power development at large

by this windy property. The total scale and the Puttalam, Eastern and

theoretical wind capacity rises to central highland areas are will

approximately 24,000 MW if the contribute to small to medium scale

windy lagoons are included. wind power resource development.

Sri Lanka Sustainable Energy

Sri Lanka is blessed with quality wind Authority has identified resource

energy primarily in the coastal region locations for large scale wind power

of the northwest, the northern and development in Mannar, Jaffna

central highlands. There is a slightly peninsula, Kokilai and Puttalam areas.

higher potential for wind power in There is both public and private

areas exposed to the southwestern participation in the production of

monsoon. For different factors, such these tools, and competitive pricing

as overlapping land uses, accessibility strategies are increasingly being

and environmentally sensitive issues, sought in the production of these

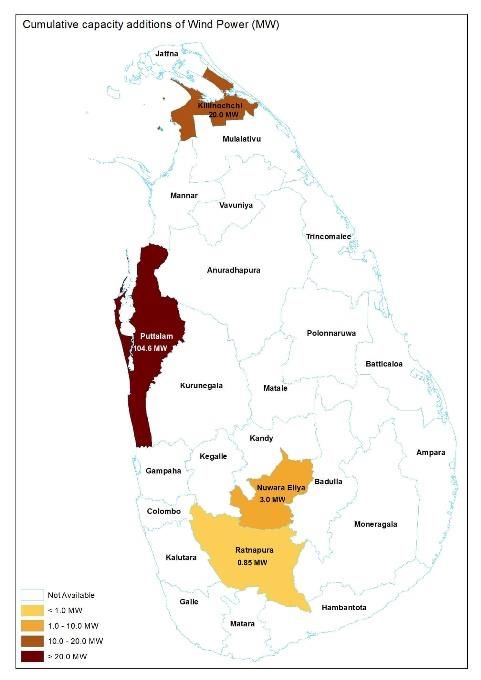

only a fraction of the overall available power projects at present.FIGURE 17 : CUMALATIVE CAPACITY ADDITION OF WIND POWER Source: www.energy.gov.lk TABLE 07 : WIND RESOURCE REGIMES AND EXPECTED ANNUAL CAPACITY FACTORS Wind Regime Annual Capacity Factor(%) Northern 34.1 Mannar 36.7 Puttalam 32.1 Eastern 27.3 Central Highland 19.1 Source: Generation Expansion Plan 2019

TABLE 08: CEB OWNED WIND 2021 - 50 400

POWER STATIONS (10 MW X 5Nos. -

Power Station Capacity (in MW) Year of Trincomalee,

Commissioning Monaragala,

Mampur 10.000 May,2010 Kilinochchi…)

Seguwanthivu 10.000 May,2010 2022 - 290 290

Vidatamuna 10.000 July,2010

Pooneryn 240

MW Mannar 50

Willpita 0.150 Oct,2010

MW

Nirmalapura 10.000 Oct, & Jul,2012 2023 - 160 MW 160

Uppu Daluwa 10.000 July,2012

(Mannar 60

Madurankuliya 10.000 July,2012

MW, Mannar

Ambewaka-Ace 3.000 Aug,2012 mainland 100

Wind MW)

Total Wind 73.040 As at Dec,.2012 2024 - 50 50

(Kokilai - 50

MW)

Source : Powermin.gov.lk 2025 5 130 135

(Puttalam - 100

Wind power plants with a total MW, Jaffna - 30

capacity of 210 MW will be added MW)

in 2020, 2022 and 2023. Other Total 5 800 805

wind power plants will be added

Source: Renewable Energy Development Plan Phase I

giving priority to the areas with

high wind energy resource

potential identified in the RE

resource inventory. A pilot project

on offshore wind energy will be

connected to the national grid in

2025.

TABLE 09 : WIND POWER

CAPACITY ADDITION

Capacity (MW)

Offsho Onshore Total

re

2019 - 20 95

(Chinaka -10 MW

x2 Nos.)

2020 - 100 100

(Mannar-100 MW)9. Solar Power Projects in

the Industry

Solar power generation has come a countries such as Bangladesh,

long way from its inception and is making solar rooftop projects more

now becoming a very competitive appropriate for Sri Lanka.

renewable energy source. Solar

power can be generated using many

methods and the most common and While the government of Sri Lanka

environmentally friendly alternative has not been able to promote solar

is photovoltaic (PV) panels. rooftop projects until recently,

several private companies have

Both rooftops and solar farms will

install PV panels. Solar farms are successfully carried out their own

desirable choices for countries with projects in their factories and office

large open land areas, such as the buildings. At their fabric park in

Middle East, Australia and North Thulhiriya, MAS Holdings has

America. But it isn't a feasible choice completed a 1 MW solar rooftop

for an island nation and a project. With a 1.3 MW rooftop

biodiversity hotspot like Sri Lanka solar project to power the famous

with restricted land resources. HNB buildings of Colombo, 249 HNB

Rooftop solar systems, on the other customer centers throughout the

hand, reuse existing government

rooftops and private office island and seven solar-only

buildings, factories, and residential branches, Hatton National Bank

houses. They have no negative followed up.

environmental consequences, can

be easily installed in a very short

time. Excess power from on rooftop

solar panels can be fed back to the

national grid. Rooftop solar projects

also provide the benefit of being

able to install grid off in rural areas,

as seen in9.1 Solar Power Projects other than solar parks. Monaragala,

Undertaken by CEB Pooneryn, Polonnaruwa and

Mahiyanganaya have been identified

TABLE 10: CEB OWNED SOLAR for establishing solar parks.

POWER STATIONS Out of these, 100 MW from

Monaragala and 130 MW from

Power Capacity Year of Commissioning

Station (in MW) Pooneryn will be added by 2021. 100

Battaramull 0.018 Jan,2002 MW each will be added from

a Polonnaruwa, Monaragala and

Gannoruwa- 0.500 April,2011

Mahiyanganaya in the period 2023-

2

Thiruppane 0.123 July,2011 2025. Apart from these, Maduru Oya

Gannoruwa- 0.737 Aug.,2011 floating solar project will be added in

1 2021. Solar roof top systems will be

Total Solar 1.378 As at Dec,.2012 added through the Soorya Bala

Sangramaya project.

Source: Powermin.gov.lk

TABLE 11 : SOLAR POWER

9.2 Solar Power Plants Capacity CAPACITY ADDITION

Additions Ca

pa

cit

According to Renewable Energy y

Development Plan Phase I 2019- (M

W)

2025, 25 projects of 1 MW X 60 Large Roo Float Total

Nos.solar power tender were added ftop ing

in 2019, and the balance will be 2019 25 70 - 95

added in 2020. Projects under 1 MW (1 MW x 25 Nos.)

2020 129 30 - 159

X 90 Nos. solar power tender will be (Valachchenei - 10 MW,

added in 2020, 2021 and 2022. Vaunathivu – 10

Further, the already tendered 10 MW, Pooneryn – 80 MW, 1

MW X 29 Nos.)

MW projects of Valachchanai and 2021 270 30 100 400

Vaunathivu will be added in 2020. (Monaragala – 100 MW,

Apart from these, a total capacity of Pooneryn – 50 MW,

1 MW X 50 Nos., 70 MW

360 MW will be added from 2021 to from other projects)

2025 from this type of projects2022 90 26 15 31

penetration on small scale and top

(1 MW x 20 Nos., 70

MW from other roof.

projects)

2023 180 MW 25 15 220 In Sri Lanka, in 2010, the Ministry of

(Monaragala – 100 MW,

80 MW from other

Power and Renewable Energy, Ceylon

projects) Electricity Boards (CEB) and Lanka

2024 170 MW 40 50 265 Electric Company (LECO) launched the

(Polonnaruwa – 100

MW, 70 MW from other

'Energy Banking Facility' for such

projects) micro-scale generating facilities,

2025 170 MW 104 20 294 generally known as the 'Network

(Mahiyanganaya – 100 Energy Metering Facility' for

MW, 70 MW from other

projects) electricity consumers. This scheme

Total 1034 330 200 1564 requires any user of electricity to

engage as a producer in the

Source: Renewable Energy Development Plan Phase I production of electricity from a

source of renewable energy for their

own use and in the export of any

9.3 Development of Rooftop Solar surplus energy. The installed capacity

Power of the generating facility shall not

surpass the customer's contractual

Roof top solar systems are beginning requirement. Consumers are not

to play a prominent role in providing charged for energy exports, but are

electricity consumers with energy compensated (in kWh) for consuming

needs and it is an efficient type of the same amount of energy over

embedded generation located at the subsequent billing periods. No

end user. financial compensation is paid out for

the consumer's surplus energy

With the availability of rooftop exported. Taking into account the

spaces, rooftop solar PV installations difference between the import and

can significantly reduce land use and the export of energy, the electricity

environmental issues, especially in bill is prepared. At present, under a

urban and suburban areas. Several net metering scheme amounting to

schemes are introduced around the 106 MW of solar power, the country

world to create an enabling has around 14,700 such installations.

environment for photovoltaicYou can also read