ASI UK ETHICAL EQUITY FUND - May 2021 - OUR RESEARCH. YOUR SUCCESS - Rayner Spencer ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UND PROFILE

ASI UK ETHICAL EQUITY FUND

May 2021

OUR RESEARCH. YOUR SUCCESSCONTENTS

ASI UK ETHICAL EQUITY FUND____________________________________________4

IA UK ALL COMPANIES__________________________________________________5

ABERDEEN STANDARD INVESTMENTS______________________________________6

ASI UK ETHICAL EQUITY FUND____________________________________________7

Fund Management Team

Fund Objectives & Targets

Investment Philosophy

Investment Process

Ethical screen

Portfolio Construction Parameters

PAST & CURRENT POSITIONING/STRATEGY__________________________________13

Performance

SUMMARY & EVALUATION_______________________________________________17

ABOUT US____________________________________________________________18

Working with advisers

Working with providers

Ratings

Page 3ASI UK ETHICAL EQUITY FUND

OUR FUND PROFILES provide an in-depth review of our leading rated funds and are designed to give advisers, paraplanners and analysts an ‘under

the bonnet’ view of the fund. In providing more detailed commentary than a standard fund factsheet we believe our fund profiles set the standard for

the next generation of research notes, aiding in fund selection and in meeting the ongoing suitability requirements expected by the FCA, and helping

ensure firms deliver good client outcomes.

All of our rated funds are subject to rigorous and ongoing scrutiny on both a qualitative and quantitative basis. Our fund methodology is available for

download from the RSMR Hub – www.rsmr.co.uk

The ASI UK Ethical Equity Fund has been an RSMR Responsible rated fund since April 2012 and is listed within the RSMR Responsible classifications as

Ethical.

Originally launched in 1998, it is a UK equity fund that is bottom-up in composition. It draws on the wider UK equity team resource at ASI and has full FTSE

350 coverage. The fund adopts a co-manager structure, and one of the managers is the Deputy Head of UK Equities at ASI.

The fund adopts an ethical policy that is driven by the views of the fund’s investors and is applied with no compromises. A dedicated ESG Team manage

the ethical screening process of the fund with oversight of the ethical policy provided by the ASI Ethical Funds Advisory Group.

Due to the application of the ethical policy, many large cap names are excluded from the investable universe resulting in a portfolio that is constructed

across the UK market cap spectrum with bias towards mid-cap companies.

The fund is benchmarked against the FTSE All Share with a performance target of the FTSE Share +2%.

Stuart Ryan, Chartered FCSI, Chartered Wealth Manager, Head of Research, RSMR

Stuart graduated from the University of Wales Swansea with a degree in Law and commenced his career in finance

in 2004 at HSBC in Canary Wharf. He has gained wide range of experience in finance ranging from investment

management and investment banking to financial trading and market making.

Stuart worked for over 6 years at London based IFA Holden & Partners as Investment Manager leading the in-house

investment team. This included portfolio construction (including SRI & ESG portfolios), investment research, conducting

face-to-face meetings with both fund managers and clients and being a member of the internal investment committee.

He was subsequently the Performance & Risk manager at Redmayne Bentley based in Leeds and sat on the various

asset allocation committees as well as the Model Portfolio Service committee

Stuart is a Chartered Fellow of the Chartered Institute for Securities and Investment (CISI) as well as a Chartered

Wealth Manager.

Page 4IA UK ALL COMPANIES

The ASI UK Ethical Equity fund is classified in the Investment Association The uncertainty surrounding a ‘no deal’ with the European Union was

(IA) UK All Companies sector which comprises funds which invest at least finally removed in December 2020 increasing sentiment for the UK from

80% of their assets in UK equities, with the primary objective of achieving investors. This added to the Covid-19 vaccine breakthrough announced

capital growth. in November 2020 providing optimism with markets, including the UK,

responding accordingly.

As at March 2021 this is the second largest of the IA sectors, with over

£160bn of assets under management invested in circa 270 funds. Like many global economies, the UK experienced a dramatic decline in

Consequently, it encompasses a significant number of strategies and gross domestic product in 2020 as the pandemic spread and restrictions

methodologies, from passive FTSE trackers through to more specialist were imposed on citizens. The second quarter of the year saw a decline

funds, making a peer group comparison difficult. The sector tends to greater than 19% followed by a 16% increase in the third quarter. The

have consistent fund flows as many of the funds are used as core equity final quarter of 2020 saw a modest increase. The preliminary figure for

holdings in most asset allocations and resulting portfolios. the first quarter of 2021 indicates the UK economy declined less than

expected with economic forecasts for growth for the remainder of the

Although the UK economy is gradually reducing its global influence in

year upgraded to reflect the momentum in the economy.

GDP terms, with the rise of the new emerging economies, it is still home

to some of the world’s leading companies and brands. Over time, the UK There are still uncertain waters to navigate until the economy is back

may gradually become a smaller part of an investor’s portfolio as other to pre-pandemic levels and the aftermath will be felt for some time.

markets increase in importance but for the time being it should remain a However, there is optimism building and with that, increased confidence

core part of a UK investors overall holding. with asset allocators to deploy capital into the UK market.

The UK stock market is one of the largest and most efficiently run. It is The events of 2020 have highlighted the need for active management

well understood and offers access to a huge variety of companies as where stresses were experienced across the full index and the wider

well as providing the ability to reduce currency risk by holding sterling economy. The ASI UK Ethical Equity fund offers an active solution for

assets. That said, the events surrounding the Covid-19 pandemic have clients who wish to gain exposure to the UK market without the inclusion

seen many companies in the UK market experience disruption, both of certain industries and sectors as well as providing a diversification

operational and financial. The UK market underperformed its global peers option for investors as part of their UK equity allocation.

during 2020 as the cloud of a potential hard Brexit compounded investor

sentiment against an already challenging backdrop. In addition, the

UK market, by its very construct, has very different sector constituents

compared to other global markets, which has proved a headwind during

the events of 2020 where indices comprised of technology names were

the natural beneficiaries.

Page 5ABERDEEN STANDARD INVESTMENTS

Standard Life Aberdeen plc is one of the world’s largest investment

companies, created in 2017 from the merger of Standard Life plc and

Aberdeen Asset Management PLC. Operating under the brand Aberdeen

Standard Investments, the investment arm manages £455.6bn (30 June

2020) of assets making it the largest active manager in the UK and the

second largest in Europe.

The company has developed a powerful global distribution with

institutional and retail clients located in over 80 countries, supported by

over 40 worldwide offices. They offer an extensive range of investment

services and have developed capabilities across a variety of asset

classes including equities, fixed income, commercial real estate and other

alternatives.

Page 6ASI UK ETHICAL EQUITY FUND

Managers Lesley Duncan and Rebecca Maclean holds a BA (Hons) Economics (University of Paisley) Post Grad IIMR (University

of Stirling) and an MPhil International Finance (University of Glasgow).

Structure OEIC

IA Sector UK All Companies Rebecca Maclean – Investment Director, UK Equities

Launched 1st August 1991

Rebecca has a career spanning 10 years, of which 7 have been at Aberdeen

Fund Size £345.0m (31.05.2021) Standard Investments. Rebecca is the deputy manager of the UK Ethical

Equity fund co-manager of the ASI UK Responsible Equity fund and holds

Fund Management Team responsibility for managing a number of UK equity segregated mandates.

The fund is managed by Lesley Duncan and Rebecca Maclean with Rebecca is also responsible for research coverage on the software sector

Rebecca as the deputy portfolio manager. Both are part of the wider UK as well as the business and support services sector within the UK equity

Equity Large Cap Team at ASI that provide full research coverage of the team. Rebecca holds a BA Experimental Psychology (University of Oxford),

FTSE 350 ex investment trusts. Currently the team comprise 15 investment MA International Relations (King's College London) and the CFA.

professionals led by Andrew Millington. Additional insight is also obtained

from the 8-strong ASI Smaller Companies team. Fund Objectives & Targets

Investment pods within the UK Equity Large Cap team cover areas such The ASI UK Ethical Equity Fund aims to deliver growth over the long term (5

as Core, Quality, Income and Responsible. Currently there are seven pods years or more) by investing in UK equities which meet the ethical criteria set

with five members within the Sustainable Investment Pod, namely Lesley out in the investment managers Ethical Investment Policy.

Duncan, Rebecca Maclean, Eleanor Jamieson, Wes McCoy and Peter Silver. The fund is benchmarked against the FTSE All Share with a performance

Rotations can occur within the equity pods, although Lesley and Rebecca target to achieve the return of the FTSE All Share plus 2% per annum over a

are core members of the Responsible Investment pod. rolling five-year period (before charges).

Peter Silver is the ESG analyst for the UK desk and feeds into the central Investment Philosophy

ESG team that produce the central thematic ESG research. Amanda Young In terms of investment philosophy, three core beliefs underpin the ASI

is Global Head of Responsible Investment. approach to equity investing.

Lesley Duncan – Deputy Head of UK Equities 1. Fundamental research provides information that can be used to exploit

Lesley has a career spanning 27 years, of which 25 have been at Aberdeen market inefficiencies – ASI are of the opinion that company fundamentals

Standard Investments. Lesley is the manager of the UK Ethical Equity fund determine a company’s share price, however this may be valued

co-manager of the ASI UK Responsible Equity fund and holds responsibility inefficiently in the shorter term. ASI believe that fundamental research

for managing a number of UK equity segregated mandates. Lesley is also provides invaluable information that allows them to identify opportunities

responsible for research coverage on the Household Goods and Builders and exploit these valuation inefficiencies.

Merchants sectors within the UK Equity team.

2. ESG assessment and corporate engagement enhance returns – ASI place

Lesley worked at Bothwell Asset Management as Trainee Analyst before joining ESG considerations and constructive engagement at the centre of company

Standard Life in 1995 as Trainee Investment Analyst on the UK desk. Lesley research. This can assist in mitigating risks and enhancing returns.

Page 73. Disciplined, active investment can deliver superior outcomes. ASI seek For the ASI UK Ethical Equity Fund, the starting point is the FTSE All Share

to construct high conviction portfolios that are comprised of the best to which the ethical policy of the fund is applied. This removes holdings

investment ideas. that are unacceptable to the fund. As at the end of 2020, applying the

ethical policy to the fund resulted in 47% of the index being unacceptable.

The ASI UK Ethical Fund applies the above beliefs with adherence to an

The remainder forms the investable universe of the fund which is further

investor led ethical criteria that applies both positive and negative screening.

divided into ‘acceptable’ and ‘preferred’. As at the end of 2020, the

investable universe comprised 37% preferred and 16% acceptable names.

Investment Process

‘we are looking for analyst recommended companies that pass the There is no formal target as to how many ‘preferred’ names are in the

screen, but we are looking for companies that have got strong ESG portfolio, instead the managers will seek to maximise this exposure as part

credentials too so that we have high conviction in them from both a of the wider management of the portfolio diversification whilst adhering to

financials and ESG perspective’ – Rebecca Maclean its objectives. The ethical screens are applied on a ‘no compromises’ basis

which leads to many large cap names being excluded from the portfolio.

The fifteen members of the UK Equity Large Cap team cover the FTSE To counter this, the portfolio has exposure across the market cap spectrum

350 ex-investment trust universe. Continuous research is conducted on utilising the UK Equity team’s full market coverage as well as input from

the companies within this universe with each member of the UK equity the Smaller Companies team.

team assigned individual sector responsibilities. No screen is applied

to companies in the FTSE 350 at this stage as the team has sufficient The team also use the ‘Matrix’ which is a quantitative tool that enables

resource to have full coverage of the universe and do not wish for any them to target companies that have the attributes that are believed likely

investment opportunities to be missed due to a screen. Team members to lead to future outperformance. This process was developed over 20

apply a Buy, Sell or Hold recommendation on every stock covered. Due to years ago and focuses on 13 key factors which are considered to be

the resource within the team, companies are met, regardless of whether drivers of out-performance with continuous back testing used to ensure

shares are owned, at least twice a year resulting in circa 750 meetings these factors remain relevant today.

annually. The UK Equity team also utilises other resources, such as the All investment ideas are subjected to peer reviews which is a fundamental

Smaller Companies team, that enables access to small cap investment part of the process. This occurs through regularly scheduled meetings

ideas, as well as attending meetings with the Corporate Credit team as well as on an ad hoc basis. The culmination of the wider team debate

enabling greater insight of a company from different perspectives. The leads to a ‘Conviction List’ of the team’s best ideas. This comprises

central ESG team can also provide additional insight into idea generation twenty names. The managers try to support this list where permitted, and

due to the thematic work that they undertake. Drawing on these multiple currently sixteen names in the portfolio are contained on this list.

sources forms the foundation of the idea generation within the team

with the best ideas selected for inclusion in the portfolio. As the manager Fundamental research on a company is undertaken by the sector analyst

explains ‘we are looking for analyst recommended companies that pass within the UK Large Cap team working alongside the desk based ESG

the screen, but we are looking for companies that have got strong ESG specialist. A full research note is written on a company, and is accessible

credentials too so that we have high conviction in them from both a via a proprietary research platform. The research note covers four key

financials and ESG perspective’. areas:

Page 81. Foundations – key elements of a company’s fundamentals are assessed if the investment thesis does not bare out.

including:

All stocks covered by the analysts are assigned a Q score ranking from 1

a. The evolution and growth of the business to 5. 1 indicates Best in Class with 5 indicating a laggard. Several metrics

b. The sustainable competitive advantage are used as part of this scoring system of which ESG forms a part. If a

company is awarded a Q1 score it will typically be demonstrating best in

c. Management’s track record of execution and managing risk

class in the ESG elements as well as the other metrics covered.

d. Past treatment of minority shareholders

e. The balance sheet and financials The portfolio construction process has now been enhanced so that only

stocks with a Q3 ESG rating or above can be added to the fund. Prior to this

f. ESG risks and opportunities of the company in question

the fund was permitted to own companies that were assigned an ESG Q

2. Dynamics – Factors are assessed for changes that impact the price of a score of 4 and above to reflect the engagement that would be undertaken

stock. This includes areas such as: with companies held. This has now changed so that new companies in the

portfolio are only held if they score an ESG Q score of 3 and above.

a. Internal change

i. Management change As part of this enhancement, the existing portfolio was assessed and where

a company was assigned a Q4 ESG score, engagement with the company

ii. Corporate restructuring or consolidation

was undertaken to determine if the score would improve. If it was decided

iii. New product innovation this score would not improve the company was removed from the portfolio.

iv. New market entry This impacted a handful of names held with companies removed including

b. External change JD Wetherspoon, Mitchells & Butler and St James Place.

i. Regulatory or political change As the Q scores are dynamic, if a company’s Q score were to move from

ii. Technology change a 2 to a 4 (although this has yet to occur), this company can still be held

iii. Competitive dynamics in the portfolio as is not an automatic sell based on the score downgrade.

However, the position cannot be added to. Instead, engagement would take

iv. Consumer preference/behaviour

place with the company and it would be added to the priority engagement

v. Perception change list where formalised specific timescales are set for specific issues to be

3. Financials and valuation – thorough analysis is undertaken to assess the addressed. The priority engagement list is another process enhancement

strength and weakness of a company’s financials. This includes the balance that has been put in place.

sheet, cash flow and accounting. The market perception of future prospects A house ESG score was also implemented across all desks at ASI during

and value of the company are also compared to the ASI forecast of future the latter part of 2020 and early 2021. This is a proprietary assessment

financials and the stock price ASI believe the company should trade at. tool to understand the ESG risks within the portfolio. The tool uses

4. Investment insight and risk – The investment thesis for the company data points from third party providers that are entered into an in-house

is elaborated on covering areas such as difference of view versus market model that ranks the risk of a particular theme to a company in terms of

consensus. This assessment is combined with downside risk implications materiality to that sector. The output from this is a house score for the

Page 9portfolio that provides an extra way of identifying companies that may such as airlines and airports have been increasingly highlighted in the

require engagement in the portfolio to understand why a company has responses. However, airline stocks are still permitted in the portfolio as

received a certain score. There are also tools with regards to carbon the engagement overlay is fundamental to the process. Companies are

footprint analysis as well as climate change scenario analysis of the selected in the portfolio that are going above and beyond within their

portfolio. The third-party data provider data is used to aid the proprietary respective industries to address fundamental ESG issues. As the manager

model as opposed to dictating the output as the team are in regular explains, ‘the engagement part of our process adds a layer and depth to

contact with the companies they cover and have access to data that may how we think about the stocks in which we invest’.

not be available to the third-party provider.

The screen applied is both negative and positive with a ‘no compromises’

The application of these additional ESG metrics is part of the ongoing approach. A formal corporate governance policy is in place with regards to

process to hold companies that are on a journey to go above and beyond active engagement and voting at AGMs. The whole process is supported by

in terms of ESG considerations for their respective industries. the wider ESG resource at ASI with eight equity team desk ESG specialists

and twenty central ESG stewardship team members.

Ethical screen

The dedicated ESG team manages the ethical screening process with the Positive

fund’s Ethical Investment Policy covering both the positive and negative The positive criteria are used to favour companies that benefit society and

criteria applied. The areas screened are reflective of the wider views of the environment. The UN Global Compact is used to define the following

investors in the fund with the criteria regularly reviewed (both positive four areas where positive business practices and standards are sought:

and negative) via surveys and consultations. Oversight of the process is

1. Environment – Companies are invested in that have a positive impact

undertaken by the Ethical Funds Advisory Group (comprising independent

on the environment, through strong policies, processes and management,

external members as well as key internal members).

recognising the finite resources available in the world. Companies are

The annual investor survey informs the ethical policy adopted by the also sought that contribute to environmental protection and enhancement

fund. The survey enables trends to be monitored as well as identifying through their products and services, such as environmental technologies,

areas of potential interest for further research. The team prefer to see a renewable energy (such as wind, solar, geothermal, tidal), pollution

trend before making major changes as they are cognisant that the media mitigation, energy and resource efficiency, environmental protection and

can influence short term views. The fossil fuel element of the policy was conservation of biodiversity and natural resources.

tightened in 2019 with the output of the 2020 survey seeing this extended

2. Human Rights & community – Companies are sought that respect and

further to include support services with exposure to fossil fuels. This

support the human rights of those affected by its business, particularly

amendment to the ethical policy was applied to the portfolio and resulted

those companies upholding the highest standards of business conduct in

in the removal of Wood Group in the first half of 2021.

countries with a weak rule of law. The fund seeks to invest in companies

‘the engagement part of our process adds a layer and depth to how we that offer products and services that provide access to some of the world’s

think about the stocks in which we invest’ – Lesley Duncan most basic rights, such as water, sanitation, education, healthcare, food,

shelter and energy, in a bid to enhance livelihoods and society. In addition,

Environmental factors have increasingly been more prominent in the

companies are also sought that have strong relationships within their

past few investor surveys, for example carbon intensive industries

Page 10communities and ensure that their business activities provide positive fund invests. In circumstances where engagement results in concerns still

benefits to the local environment in which they operate. remaining over corporate behaviour or oversight, disinvestment from a

company will occur.

3. Employment – Companies are sought that have strong labour practices,

where employees are valued and treated with respect and dignity.

Negative

Companies that demonstrate strong policies, practices and reporting on

issues such as equal opportunities, diversity, freedom of association, right Negative criteria are used to avoid investing in companies which are

to collective bargaining, training, education, and wellbeing will be favoured. involved in certain industries and activities which have been identified by

In addition, the fund favours companies implementing strong safety, health investors in the fund as a concern:

and welfare policies, particularly those involved in hazardous activities. The following covers a select number of the screens applied.

4. Anti-bribery and corruption – Companies are favoured that uphold z UN Global Compact non-compliance (failure of one or more of the ten

the highest standards of business ethics and demonstrate strong anti- principles of the UN Global Compact)

corruption policies including oversight, commitment and anti-corruption

z Weapons

practices. The fund seeks to invest in companies that have adopted and

z Nuclear (more than 5% of revenue)

embedded a code which encourages employees to follow principles

of good business behaviour and positive corporate culture. This code z Alcohol production (more than 10% of revenue)

should be publicly available and actively communicated to all employees, z Animal testing

suppliers and stakeholders. z Animal husbandry (e.g. intensive farming)

Corporate Governance z Fur

The fund adopts a formal governance policy with active voting at z Pornography (more than 3% of revenue)

annual general meetings of the companies held. Issues such as board z Tobacco

independence, excessive remuneration and audit issues are considered.

z Gambling (more than 10% of revenue)

The fund adopts a policy of voting: z Poor business practices that harm society (e.g. predatory lending)

z against the Chair of any company where the board fails to have set z Environmental protection (includes highly carbon intensive activities and

policy, have oversight or take responsibility for environmental, social, oil & gas extraction)

health & safety and human rights issues. The full positive and negative criteria that forms the ethical policy for the

z against members of any health, safety and environment committee where fund is available on the ASI website.

insufficient oversight has resulted in poor performance in these areas.

Portfolio Construction Parameters

Engagement The fund is benchmarked against the FTSE All Share, although the

An active engagement policy is undertaken with companies on a number application of the ethical policy leads to a natural overweight to mid-cap

of environmental, social and governance issues. The engagement seeks companies in the portfolio.

the adoption of good corporate behaviour by the companies in which the

Page 11The fund is bottom up in composition with an active share typically above

80% and a tracking error between 4-10%.

The number of holdings is typically within the range of 50-100 stocks with

turnover in the region of 20-25%.

Position sizes are considered on an absolute basis (as opposed to relative

to the index) with the majority of the holdings between 1% and 3.5% in

size. 5% is the upper position size limit.

A maximum of 30% can be held in any one sector of the FTSE All Share

Index with cash in the portfolio around 5%.

Page 12PAST & CURRENT POSITIONING/STRATEGY

Like many investors, at the start of 2020 the portfolio was positioned for a This was the approach taken with Boohoo as the company was previously

robust UK recovery post the general election and Brexit resolution and this was held in the portfolio. In July 2020 Boohoo was subject to a media

reflected in the overweight positioning to the consumer staples sector. The investigation into modern slavery. These allegations were taken very

onset of the Covid-19 pandemic created the opposite environment although the seriously by the managers, and they spoke to the Boohoo on the Monday

application of the ethical policy did assist as the fund did not hold sectors such morning after the news broke to get a greater understanding of the issue.

as energy however the mid-cap bias of the fund did counter this. A follow up call took place the next day where the decision was made to

divest from the company across all funds. In the eighteen-month period

In the wake of the pandemic, positions were added to that the managers

prior to divestment, dialogue had taken place seven times between ASI

felt were undervalued and the position in Euromoney was an example

and the company with regards to supply chain issues.

of this. Although travel was restricted, using a 2-5-year time horizon the

managers felt the company would be a beneficiary once travel increased Post divestment ASI have continued to engage with the company on

due pent-up demand. The same view was taken with WH Smith with sustainability matters engaging with them on a variety of issues. In addition,

their outlets in railway stations and airports. Countryside Properties and the issue of fast fashion had previously not been cited by investors as

Unite are examples of companies already held where the managers part of the annual engagement survey, although questions have now been

have participated in capital raising to strengthen their balance sheets. added on this area as well the sustainability of supply chains.

Countryside Properties was added to due to the structural regeneration

Looking at other examples of engagement with companies held, Fever-

element of the business whereas Unite was due to the need going forward

Tree has been engaged on the issue of lack of disclosure and sustainability

for student accommodation.

resource at the company. The output from that engagement has been

Software stocks are an area where the managers are focusing post improved disclosure by the business and the appointment of a dedicated

the pandemic and this is the current largest overweight in the portfolio sustainability manager. John Laing has been engaged with to tackle the

(Rebecca is the analyst on this sector). The recurring revenue streams issues of ESG integration and supply chain transparency in the business.

are the attraction, and as such these types of businesses were added to This engagement has seen the appointment of a new ESG Director as

the portfolio in 2020. Examples of holdings added in this sector include well as ASI setting milestones for the company to meet with regards to

Blancco Technology Group which was introduced to the portfolio due to disclosure and impact analysis.

the environmental aspect. The company facilitates the reduction in landfill

Although the managers have their own respective sectoral responsibilities,

waste by reducing the need to physically destroy information technology

biases do not come through into the portfolio as individual companies

hardware. The company develops secure data erasure products which

are selected on the strength of the investment case in the context of the

erase more data from a device than by restoring factory settings (as data

broader portfolio. The only bias that tends to come through in the portfolio

can still be obtained). Instem is another software name held that provides

construction is towards growth names. This is because the managers have

IT solutions for medical testing without the use of animals. Aptitude

a preference for stocks that have a structural aspect to them, this has

Software was added pre-pandemic.

been a long-term theme in the fund and includes attributes such as having

The fund does own companies that would be considered 100% best in a strong market positioning, the ability to grow faster than the market, and

class within the portfolio but the managers will also own companies that a form of uniqueness. Names such as ASOS, Moonpig, Instem, Coats and

they feel can be improved by engaging on ESG issues as active owners. Autotrader are examples of current holdings that display these attributes.

Page 13Cineworld was a portfolio holding and the position had performed very The following pie chart illustrates the sectoral exposures on an absolute

well. The position has now been removed from the portfolio due to basis as at the 31st March 2021:

concerns over a proposed Long-Term Incentive Plan for management.

Utilities, Unclassified, Cash & Other,

3.60% 1.80% 2.80%

WH Smith has also been exited due to price appreciation with the Industrials,

25.20%

proceeds redeployed into other areas that were presenting opportunity Telecommunic

ations, 3.60%

such as ASOS. ASOS plays into an area the managers are keen on –

moving from the high street to online retail, with the company being Consumer

moved onto the Conviction List as well. ASOS offers a global reach due to Staples, 4.30%

its roll out model. ASOS also scored well in terms of ESG credentials and Real Estate,

its supply chain. 4.70%

Dixon Carphone has also been removed as the managers felt the company

had benefitted from the increased requirement for electronic goods due to

remote working, but that this trend had played out.

The fund has participated in two IPOs in 2021 so far, Moonpig and Technology,

14.10% Consumer

Trustpilot. Moonpig was included due to increased visibility of earnings for

Discretionary,

growth as the company is enabling the addition of gifting to the greeting 22.60%

cards they sell. Trustpilot was included as it is seen as more independent Financials,

than other competitors in this space and as valuable to companies due to 17.30%

its strong network effect. Source: ASI (30/04/2021). Numbers may not add up to 100% due to rounding or the

exclusion of cash. The fund is actively managed, and its composition will vary. Fund

Support services exposure has been amended with Ferguson being details and characteristics are as of the date noted and subject to change.

sold out due to the valuation being less attractive with names such as

Active overweight positions versus the benchmark include information

Homeserve and Ashtead added to benefit from the cyclical recovery in

technology, health care, communication services, and consumer staples

2021 that have yet to reach fair value.

with underweight positions in real estate, financials, energy, consumer

Howden Joinery is largest holding and is held due to its attractive earnings discretionary and utilities. Underweight exposure can be a by-product of

growth which is underpinned by its depot opening plan combined with its the ethical policy.

gain in market share. The company also has a strong balance sheet and is

In terms of outlook, the managers see the continued roll out of vaccines

cash generative.

underpinning a more optimistic outlook for the global economy. There is

The ethical policy of the fund permits around 53% of the FTSE All Share to be improved investor sentiment towards UK equities with the pre-existing

invested in due to the ethical policy being tightened in 2019 for fossil fuels. gap between value and growth investment styles beginning to converge.

The application of the ethical policy does lend to a mid-cap bias in the portfolio Due to this, the managers see a better environment going forward for

with the managers finding the best ideas in the mid-cap space currently. fundamental stock picking.

Page 14Performance

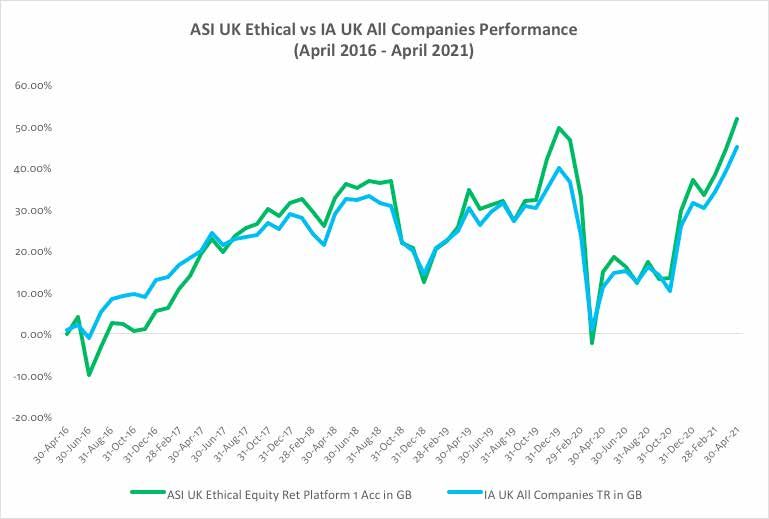

The adoption of an ethical policy has not hindered performance over the

medium to long term. Over the five-year period spanning April 2016 to

April 2021, the ASI UK Ethical Equity Fund has delivered 51.56% on a total

return basis. This compares to 44.75% over the same period by the IA UK

All Companies sector, again on a total return basis.

The line chart below illustrates this performance.

ASI UK Ethical vs IA ALL Companies Performance

(April 2016 – April 2021)

Source: ASI (31/04/2021) & RSMR. Figures shown are for the Platform 1 Acc share class in sterling.

Page 15Reflecting on more recent performance, the onset of the pandemic did see The portfolio still maintains a strong overweight to information technology

the fund fall further than the sector due to the mid-cap bias as a result which has benefited performance. Software names such as Kainos Group

of the ethical policy applied. The lack of Oil & Gas exposure (due to the have benefitted against the economic backdrop due to the visibility of

screens) was a positive during this period as was exposure to sectors earnings. CVS Group has benefitted from increased pet ownership during

such as Software and Life Assurance. However, the fund held overweight the pandemic.

positions in Housebuilders, Support Services and Travel & Leisure,

Although many names have performed well, there is still further

areas that were significantly impacted by Covid-19 and the restrictions

appreciation expected. As the manager reiterates ‘we always come back

that were put in place for the wider economy. In addition, the lack of

to valuation’ in terms of the portfolio and fundamentals.

exposure to Pharmaceuticals (again due to the screen), dampened relative

performance.

Performance improved throughout the summer with Q4 experiencing a

strong rally for the fund, as well as the wider UK market, post the vaccine

breakthrough announcement in November.

‘we always come back to valuation’ – Lesley Duncan

Q1 2021 has continued to see performance improve of both the fund

and wider sector as the vaccine roll out commenced within the UK.

Overweight positions in consumer discretionary names started to perform

with the housebuilders experiencing increased demand for family homes

as structural changes take place. Hybrid working and increased working

from home has seen demand increase for different types of space for

residential homes, benefiting the exposure in the fund.

Cyclical positions such as Joules Group and Greggs have benefitted on

the UK high street, an area that has been under increasing pressure.

Both companies have adapted their business models in response to the

pandemic. The former experienced increased online sales and the latter

trialling a delivery service to drive sales.

Page 16SUMMARY & EVALUATION

The ASI UK Ethical Equity Fund is a UK equity fund that is bottom up in underperforming when the sectors that are screened out are favoured

construction with ideas for the fund are generated from various sources by the market (e.g. oil & gas). However, the fund can demonstrate

at ASI (e.g. the UK Large Cap team, the ESG team, the Smaller Companies outperformance when the sectors that are screened out are encountering

team) with peer review an integral part of this process. Turnover is low a headwind.

with a high active share and a tracking error of between 4-10%.

In addition to providing a UK equity solution for investors that require the

The fund utilises an investor driven survey to determine the ethical policy ethical policy that is adopted, the fund can also be used to diversify the UK

adopted. The output from this survey is a combination of both positive equity allocation within a portfolio due to the ethical policy, although the

and negative criteria which are applied to the initial investable universe, mid-cap bias will need to be factored into the allocation decision.

excluding companies that do meet the requirements of the policy. The

dedicated ASI ESG team manage the ethical screening process of the

fund with oversight of the ethical policy provided by the ASI Ethical Funds

Advisory Group.

Like all investment funds, it is important investors are aware of the

approach of the proposition. This is especially applicable when assessing

funds that apply some form of ethical screen (whether positive or

negative) to the underlying portfolio construction. This is to ensure that the

individual investor’s requirements are taken into consideration and there

are no underlying holdings that could cause concern. It is also important

to understand that the ASI UK Ethical Equity Fund will not only own best in

class companies as the managers will also consider companies that pass

the ethical criteria that are on a positive ESG journey where engagement

will form an integral part of ownership.

The co-manager structure benefits from the experience of both Lesley

(who is deputy Head of UK Equities) and Rebecca who both have individual

sector responsibilities as members of the UK Equity Large Cap team. The

individual sectoral responsibilities of the managers do not lead to sectoral

biases forming in the portfolio as the managers are focused on the

strength of a given investment case in the context of the broader portfolio.

The only bias at the portfolio construction stage is towards growth names

as the managers have a preference for stocks that have a structural

aspect to them, this has been have been a long-term theme in the fund.

The application of the ethical policy has not hindered performance over

the medium to long term, although the screens can result in the fund

Page 17ABOUT US

Established in 2004 RSMR provides research and analysis to firms working Ratings

across the UK’s personal financial services marketplace.

Our innovative ratings are now recognised as market leading and cover

Our work is completed with total impartiality, without any conflict of a broad area of investment solutions including single strategy funds, SRI

interest and delivered to a high professional standard by a team of funds, Multimanager and multi-asset funds, DFMs and investment trusts.

experienced and highly qualified people. Our familiar ‘R’ logo is now recognised as a trusted badge of quality by

advisers and providers alike and a ‘must-have’ when selecting funds. Our

Working with advisers ratings are founded on a strict methodology that considers performance

We provide specialist research, analysis and support to a diverse range and risk measures but places a greater emphasis on the ability of fund

of financial advisers and planners helping them to deliver sound advice managers to continue to deliver performance in the years ahead. based on

to their clients, backed by rigorous and structured research and due our in-depth face-to-face meetings with fund managers across the globe.

diligence. We understand financial services and we will work alongside you to deliver

The main regulatory body in the UK, the FCA, states that personal tailored solutions that are right for your clients and your business.

recommendations made by advisers should be ‘based on a comprehensive Our research. Your success.

and fair analysis of the relevant market’ and this has led to closer scrutiny

of the whole advice process. Our solutions are designed to help advisers

meet these challenges whilst recognising that advisory firms require a

range of flexible options that best meet their own business needs and

those of their clients.

Working with providers The data and information in this document does not constitute advice

or recommendation. We do not warrant that any data collected by us,

We work with all the leading fund groups, life and pension companies

or supplied by any third party is wholly accurate or complete and we

and platform operators across the financial services sector offering will not be liable for any actions taken on the basis of the content or

straight forward and pragmatic advice to help add value and improve their for any errors or omissions in the content supplied.

business performance and efficiency whilst treating customers fairly in line All opinions included in this document and/or associated documents

with FCA requirements. constitute our judgement as at the date indicated and may be changed

at any time without notice and do not establish suitability in any

individual regard.

©RSMR 2021. All rights reserved.

Page 18Number 20 Ryefield Business Park Belton Road Silsden West Yorkshire BD20 0EE Tel: 01535 656 555 Email: enquiries@rsmgroup.co.uk www.rsmr.co.uk OUR RESEARCH. YOUR SUCCESS Rayner Spencer Mills Research Limited is a limited company registered in England and Wales under Company Registration Number 5227656. Registered Office: Number 20, Ryefield Business Park, Belton Road, Silsden, BD20 0EE. RSMR is a registered trademark.

You can also read