As Oil Races Toward $100, Consumers Tell OPEC+ Enough Is Enough

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

As Oil Races Toward $100, Consumers Tell OPEC+ Enough Is Enough For the past year, oil consuming countries have become increasingly anxious at crude’s resurgence: first to $50 a barrel, then $75 and now to more than $85. And when Vladimir Putin, one of the leaders of the OPEC+ cartel, warned that $100 a barrel was a distinct possibility, the alarm bells really started ringing. Now, as quickening inflation pushes some central banks towards earlier-than-expected rate of interest hikes, the U.S. India, Japan and different consuming international locations are placing the strongest diplomatic strain on the cartel in years. Behind closed doorways, an intense marketing campaign is being waged to influence OPEC+ to hurry up its output will increase, in line with a number of diplomats and business insiders concerned within the contacts. The cartel, which meets just about on Nov. 4 to assessment coverage, is at the moment

boosting output at a price of 400,000 barrels a day every month. The personal efforts come on prime of current public appeals. The Biden administration is more and more alarmed by rising gasoline costs which have reached a 7-year excessive, and has been calling on OPEC+ for weeks to pump extra oil. Japan, the world’s fourth-largest oil client, took the uncommon step of including its voice to these calls in late October — a primary for Tokyo since 2008. India, the third-largest client, has additionally requested for extra crude. China has been silent in public, however is equally vocal in personal, diplomats stated. “We found ourselves in an energy crisis,” Amos Hochstein, the highest U.S. power diplomat, stated this week, reflecting a view broadly held view by large oil consuming nations. “Producers should ensure that oil markets and gas markets are balanced.” U.S., Japanese and Indian officers have spoken privately amongst themselves and likewise reached out to different large customers and oil-producing international locations. The calls began round three weeks in the past, however have intensified in current days after costs handed $85 a barrel. The Japanese “government is currently asking oil-producing countries to increase production in the Middle East,” in line with Tsutomu Sugimori, chairman of the Petroleum Association of Japan. “As the petroleum industry, we hope oil-producing countries, including OPEC, will take appropriate steps so as not to hinder a full-fledged recovery of the world’s economy.” So far, Saudi Arabia and others have refused to go faster, arguing the month-to-month 400,000 barrel-a-day additions are sufficient to fulfill the urge for food for oil in a world financial system nonetheless nursing the injuries of the pandemic. “We are not yet out of the woods,” Saudi Energy Minister

Prince Abdulaziz bin Salman stated on Bloomberg Television final week. “We need to be careful. The crisis is contained but is not necessarily over.” The prince’s feedback have been echoed in personal and public by others inside the OPEC+, an alliance of nations accounting for almost two-thirds of the world’s oil provide. Azerbaijan Energy Minister Parviz Shahbazov stated for instance there wasn’t a must rush quicker output will increase. “We have agreed on a very wise and smart program for months to come,” he stated. Saudi Arabia will most likely get its approach if it pushes to stay with a 400,000 barrel-a-day hike subsequent. For many OPEC+ officers they’re being made a scapegoat for a disaster they didn’t create. The downside, they argue, is just not oil however hovering pure gasoline and coal costs, which in flip have boosted electrical energy costs. Even if the cartel was to go quicker, that wouldn’t resolve these shortages, they stated. Some within the group who can be open to doing extra, nevertheless, if Saudi Arabia took the lead, a number of OPEC+ delegates stated, asking to not be named earlier than the assembly takes place. Shifting Mood For most of this 12 months oil-consuming nations accepted OPEC+ was doing sufficient. But after oil costs rose from $70 to greater than $85 a barrel and crude inventories in industrialized international locations declined sharply over the past couple of months, the temper has shifted. Now officers from consuming international locations consider the oil market is under-supplied. Many consuming international locations have been reluctant to name extra overtly for additional oil manufacturing simply earlier than a serious UN local weather change summit in

Glasgow, Scotland, referred to as COP26. But even that notion downside is beginning to fade. Jake Sullivan, the U.S. mational safety advisor, defined that Washington might combat in opposition to local weather change and guarantee there’s sufficient power to gasoline financial progress within the quick future. “Our view is that the global recovery should not be imperiled by a mismatch between supply and demand,” Sullivan stated on board Air Force One whereas en path to Rome for this week’s Group of 20 summit. “And action needs to be taken,” he stated, revealing that American diplomats have been in contact with “the largest consuming countries in the world to include China as well as India, Japan, Korea, the Europeans, and others.” President Joe Biden “will have those conversations at the G-20,” Sullivan stated. “We will see what comes as a result of those conversations.” Most Read from Bloomberg Businessweek ©2021 Bloomberg L.P.

Making the most of our energy wealth Lebanon is presented with the most serious challenges it has faced in the past decade. The economy is struggling, the internal security situation is deteriorating and the country’s neighbors pose real threats. In these circumstances the very fact that the country continues to operate can be seen as a success. And amidst everything, there are opportunities — not just in newfound offshore oil and gas but also within the country’s ingenious population. As we head into 2013, what can be done to help the country unite, to overcome its challenges and ultimately to grow? Over the course of this week, eight influential figures will address seven important topics, each suggesting one proposal to help the country move forward. In this article, the World Energy Council’s Roudi Baroudi calls for measures to protect the country’s offshore oil and gas from corruption. My one hope for Lebanon in 2013 is that all of its various

political leaders and factions take and/or allow the necessary steps for sound and sustainable development of the country’s newly promising energy sector. Why? Because virtually all of the measures involved a) are just common sense; b) require little or no investment of scarce public resources; and c) happen to be the same changes required to reform, rebuild and genuinely reconcile Lebanon as a whole. On the overall energy front, the first change would have to be one of mindset. For too long, the sector has been treated by officials, their relatives and their cronies as a cash-cow for themselves rather than as an essential ingredient in building and operating a modern nation-state. From heavy industry to the average family, everyone is affected by the chronic power shortfall. We are more than a decade into the 21st century: doing homework by candlelight should be the stuff of tales told by grandparents, not the current experiences of schoolchildren also learning to use computers. Imagine if those tasked with formulating and implementing energy policy were concerned at last with basic public goals: namely, how best to deliver affordable, reliable and sustainable energy (electricity, LPG “cooking gas”, gasoline, diesel oil, fuel oil) to all Lebanese. In turn, this new attitude could quickly convince Lebanese politicians of the need to follow the law by forming a regulatory authority for electricity, and one for the nascent oil and gas industry as well. This would go hand in hand with a government newly determined to ensure transparency, for instance by disseminating all available general information and specific knowledge about the process(es) by which the future of the oil and gas sector is being planned and managed. The same enlightened leadership would seek out and adopt the best practices at every stage of its oil and gas venture, starting at the beginning. For example, Lebanon should spend

its taxpayers’ money wisely by restricting its paid advertising to globally recognized industry publications and highly regarded professional and financial publications like the Economist and the Financial Times, and using the websites of the World Bank and the European Commission – for free – in order to ensure the broadest possible international awareness of the country’s hydrocarbon potential. The government could then consult the latter two bodies and other reputable institutions to help understand the experiences of other emerging energy powers and avoid making the same costly mistakes. Thus animated, not just by the need to closely monitor oil and gas developments, but also by its duty to keep the public informed, the Ministry of Energy and Water would secure timely and professional analysis of the seismic studies immediately following their completion – then, based on these findings, publish the next steps approved by the government in order to pursue development of the fields. In addition, with the seismic results in hand, the ministry could commission a well-known and qualified international consulting firm to prepare a comprehensive energy master-plan encompassing the entire industry and each of its sub-sectors. The electricity subsector component would be based on a long- term, least-cost expansion of generation and transmission which would take into account feasible grid interconnections with other countries in the region, the role of renewable energy, and integration of the environmental and climate change dimensions to demonstrate Lebanon’s strategy for reducing its carbon footprints in its production and use of energy. When it comes to the implementation of specific projects, the ministry would act diligently to ensure not only that all necessary environmental impact studies were being carried out, but also that the implementation of mitigating measures was done in accordance with both international best practice and

the requisite environmental and social guidelines applicable in Lebanon. The same spirit of respecting the law and pursuing the national interest also would cause Lebanese politicians, whatever their party loyalties, to avidly support the continued reform of the judiciary, an acceleration of nominations to fill judicial vacancies, and other measures designed to strengthen the rule of law. All of these steps would magnify the impact of the others by helping to ensure that pieces of legislation passed by Lebanon’s Parliament are no longer regarded as idle suggestions to be ignored at will. All of the foregoing – flowing from the original wish that Lebanon’s main political actors would stop obstructing oil and gas progress – would ensure a dynamic and profitable energy sector capable of alleviating many national problems, especially poverty. Properly managed, oil and gas would supply ample revenues for decades to come, providing the Lebanese state and Lebanese society with the resources they need to finally end the twin evils of systematic inequality and sectarian resentment. If we really want our grandchildren not to be doing their homework by candlelight, then real change is needed. With simple steps and more enlightened leadership, we can start to make it happen in 2013. Roudi E. Baroudi is an independent energy and environmental consultant and Secretary General of the World Energy Council – Lebanon Member Committee

What green artificial intelligence needs Long before the real-world effects of climate change became so abundantly obvious, the data painted a bleak picture – in painful detail – of the scale of the problem. For decades, carefully collected data on weather patterns and sea temperatures were fed into models that analysed, predicted, and explained the effects of human activities on our climate. And now that we know the alarming answer, one of the biggest questions we face in the next few decades is how data-driven approaches can be used to overcome the climate crisis. Data and technologies like artificial intelligence (AI) are expected to play a very large role. But that will happen only if we make major changes in data management. We will need to move away from the commercial proprietary models that currently predominate in large developed economies. While the digital world might seem like a climate-friendly world (it is better to Zoom to work than to drive there), digital and Internet activity already accounts for around 3.7% of total greenhouse-gas (GHG) emissions, which is about the same as air travel. In the United States, data centres account for around 2% of total electricity use. The figures for AI are much worse. According to one estimate, the process of training a machine-learning algorithm emits a staggering 626,000lb (284,000kg) of carbon dioxide – five times the lifetime fuel use of the average car, and 60 times more than a transatlantic flight. With the rapid growth of AI,

these emissions are expected to rise sharply. And Blockchain, the technology behind Bitcoin, is perhaps the worst offender of all. On its own, Bitcoin mining (the computing process used to verify transactions) leaves a carbon footprint roughly equivalent to that of New Zealand. Fortunately, there are also many ways that AI can be used to cut CO2 emissions, with the biggest opportunities in buildings, electricity, transport, and farming. The electricity sector, which accounts for around one-third of GHG emissions, advanced the furthest. The relatively small cohort of big companies that dominate the sector have recognised that AI is particularly useful for optimising electricity grids, which have complex inputs – including the intermittent contribution of renewables like wind power – and complex usage patterns. Similarly, one of Google DeepMind’s AI projects aims to improve the prediction of wind patterns and thus the usability of wind power, enabling “optimal hourly delivery commitments to the power grid a full day in advance.” Using similar techniques, AI can also help to anticipate vehicle traffic flows or bring greater precision to agricultural management, such as by predicting weather patterns or pest infestations. But Big Tech itself has been slow to engage seriously with the climate crisis. For example, Apple, under pressure to keep delivering new generations of iPhones or iPads, used to be notoriously uninterested in environmental issues, even though it – like other hardware firms – contributes heavily to the problem of e-waste. Facebook, too, was long silent on the issue, before creating an online Climate Science Information Center late last year. And until the launch of the $10bn Bezos Earth Fund in 2020, Amazon and its leadership also was missing in action. These recent developments are welcome, but what took so long? Big Tech’s belated response reflects the deeper problem with using AI to help the world get to net-zero emissions. There is a wealth of data – the fuel that powers all AI systems – about what is happening in energy grids, buildings, and

transportation systems, but it is almost all proprietary and jealously guarded within companies. To make the most of this critical resource – such as by training new generations of AI – these data sets will need to be opened up, standardised, and shared. Work on this is already underway. The C40 Knowledge Hub offers an interactive dashboard to track global emissions; NGOs like Carbon Tracker use satellite data to map coal emissions; and the Icebreaker One project aims to help investors track the full carbon impact of their decisions. But these initiatives are still small-scale, fragmented, and limited by the data that are available. Freeing up much more data ultimately will require an act of political will. With local or regional “data commons,” AIs could be commissioned to help whole cities or countries cut their emissions. As a widely circulated 2019 paper by David Rolnick of the University of Pennsylvania and 21 other machine-learning experts demonstrates, there is no shortage of ideas for how this technology can be brought to bear. But that brings us to a second major challenge: Who will own or govern these data and algorithms? Right now, no one has a good, complete answer. Over the next decade, we will need to devise new and different kinds of data trusts to curate and share data in a variety of contexts. For example, in sectors like transport and energy, public- private partnerships (for example, to gather “smart-meter” data) are probably the best approach, whereas in areas like research, purely public bodies will be more appropriate. The lack of such institutions is one reason why so many “smart- city” projects fail. Whether it is Google’s Sidewalk Labs in Toronto or Replica in Portland, they are unable to persuade the public that they are trustworthy. We will also need new rules of the road. One option is to make data sharing a default condition for securing an operating license. Private entities that provide electricity, oversee 5G networks, use city streets (such as ride-hailing companies), or seek local planning permission would be required to provide

relevant data in a suitably standardised, anonymised, and machine-readable form. These are just a few of the structural changes that are needed to get the tech sector on the right side of the fight against climate change. The failure to mobilise the power of AI reflects both the dominance of data-harvesting business models and a deep imbalance in our public institutional structures. The European Union, for example, has major financial agencies like the European Investment Bank but no comparable institutions that specialise in orchestrating the flow of data and knowledge. We have the International Monetary Fund and the World Bank, but no equivalent World Data Fund. This problem is not insoluble. But first, it must be acknowledged and taken seriously. Perhaps then a tiny fraction of the massive financing being channelled into green investments will be directed toward funding the basic data and knowledge plumbing that we so urgently need. – Project Syndicate • Geoff Mulgan, a former chief executive of NESTA, is Professor of Collective Intelligence, Public Policy and Social Innovation at University College London and the author of Big Mind: How Collective Intelligence Can Change Our World.

Saudi energy minister dismisses calls for extra OPEC+ barrels MOSCOW, Oct 14 (Reuters) – OPEC leader Saudi Arabia dismissed calls for speedier oil output increases on Thursday, saying its efforts with allies were enough and protecting the oil market from the wild price swings seen in natural gas and coal markets. “What we see in the oil market today is an incremental (price) increase of 29%, vis-à-vis 500% increases in (natural) gas prices, 300% increases in coal prices, 200% increases in NGLs (natural gas liquids) …,” Saudi energy minister Prince Abdulaziz bin Salman told a forum in Moscow on Thursday. The Organization of the Petroleum Exporting Countries and allies led by Russia, collectively known as OPEC+, have done a

“remarkable” job acting as “so-called regulator of the oil market,” he said. “Gas markets, coal markets, other sources of energy need a regulator. This situation is telling us that people need to copy and paste what OPEC+ has done and what it has achieved.” Asked about calls by major consumers like the United States for OPEC+ to increase production further to cool off rising oil prices, Prince Abdulaziz said: “I keep telling people we are increasing production.” He said OPEC+ would be adding 400,000 barrels per day (bpd) in November, and then again in the following months. At its meeting earlier this month, OPEC+ stuck to its agreement of increasing production by 400,000 bpd a month as it unwinds production cuts. “We want to make sure that we reduce those excess capacities that we have developed as a result of COVID,” he said, adding that OPEC+ wanted to do it “in a gradual, phased-in approach”. Prince Abdulaziz said that while OECD oil inventories were on track to normalise at the end of this year, 2022 was looking “a bit of a challenging year”. OPEC+ figures show the oil market is set for a surplus of about 1.4 million bpd next year. Additional reporting by Katya Golubkova and Olesya Astakhova in Moscow, and Ahmad Ghaddar in London Editing by Jason Neely and Mark Potter Our Standards: The Thomson Reuters Trust Principles.

China’s Energy Crisis Is Hitting Everything From iPhones to Milk NEW DELHI: The hit from China’s energy crunch is starting to ripple throughout the globe, hurting everyone from Toyota Motor Corp to Australian sheep farmers and makers of cardboard boxes. Not only is the extreme electricity shortage in the world’s largest exporter set to hurt its own growth, the knock-on impact to supply chains could crimp a global economy struggling to emerge from the pandemic. The timing couldn’t be worse, with the shipping industry already facing congested supply lines that are delaying deliveries of clothes and toys for the year-end holidays. It

also comes just as China starts its harvest season, raising concerns over sharply higher grocery bills. China’s export growth unexpectedly surged in August, with port disruptions due to fresh outbreaks of the delta virus having limited impact on trade. “If the electricity shortages and production cuts continue, they could become yet another factor causing global supply- side problems, especially if they start to affect the production of export products,” said Louis Kuijs, senior Asia economist at Oxford Economics. Slower growth Economists have already warned of slower growth in China. At Citigroup, a vulnerability index indicates that exporters of manufactured goods and commodities are particularly at risk to a weakening Chinese economy. Neighbors like Taiwan and Korea are sensitive, as are metal exporters such as Australia and Chile, and key trading partners such as Germany are also somewhat exposed. As for consumers, the question is whether manufacturers will be able to absorb higher costs or will pass them along. “This is looking like another stagflationary shock for manufacturing, not just for China but for the world,” said Craig Botham, chief China economist at Pantheon Macroeconomics. “The price increases by now are pretty broad- based — a consequence of China’s deep involvement in global supply chains.” UN index of global food costs is at the highest in a decade Beijing has been scouring for power supplies as it tries to stabilize the situation. The impact on the global economy will depend on how quickly those efforts bear fruit. Many Chinese factories reduced production for this week’s “Golden Week” holiday, and economists are closely watching whether power shortages will return as they ramp up again. Already, though, some industries are under pressure, and the damage they’re seeing could quickly fan out to other sectors. Paper Consider paper. Production of cardboard boxes and packing

materials was already strained by skyrocketing demand during the pandemic. Now, temporary shutdowns in China have hit output even harder, leading to a possible 10% to 15% reduction in supply for September and October, according to Rabobank. That will add further complications to businesses already suffering from the global paper shortage. Food The food supply chain is also at risk as the energy crisis makes harvest season more challenging for the world’s biggest agricultural producer. Global food prices have already jumped to a decade high, and worries are mounting that the situation will worsen as China struggles to handle crops from corn to soy to peanuts and cotton. In recent weeks, several plants were forced to shut or reduce output to conserve electricity, such as soybean processors that crush beans to produce meal for animal feed and oil for cooking. Prices for fertilizer, one of the most important elements of agriculture, are skyrocketing, slamming farmers already buckling under the strain of rising costs. The processing industry is set to be more severely affected than staples such as grains and meat, Rabobank analysts wrote in a report this week. In the dairy sector, power cuts could disrupt the operation of milking machines, while pork suppliers will face pressure from tighter supply of cold storage. Wool Outside of China, Australian sheep farmers are bracing for weaker demand just as they seek to sell their wool at auctions. The industry saw Chinese mills reduce production by up to 40% due to power cuts last week, Australian Broadcasting Corp reported. Tech The tech world could also see a dramatic hit, given that China is the world’s biggest production base for gadgets from

iPhones to gaming consoles, and a major center for the packaging of semiconductors used in autos and appliances. Several companies have already experienced downtime at their Chinese facilities to comply with local restrictions. Pegatron Corp, a key partner for Apple, said last month it began to adopt energy-saving measures, while ASE Technology Holding Co, the world’s biggest chip packager, halted production for several days. The overall impact on the tech sector has so far been limited because of customary shutdowns around the week-long holiday. Should the energy crunch worsen, it could hit production ahead of the crucial year-end shopping season. Industry giants including Dell Technologies Inc and Sony Group Corp can ill afford another supply shock after pandemic- induced turmoil fomented a global chip shortage that will extend well into 2022 and beyond. Automakers Any further deterioration of the semiconductor market would also add headaches for automakers, who have already seen production crunched by the chip shortage. The industry, which is high on the list of protected sectors in times like these, has thus far largely been spared from the effects of the power crisis. Still, there have been some isolated instances. Toyota, which produces more than 1 million vehicles a year in China at plants centered around Tianjin and Guangzhou, has said some of its operations have been impacted by the power shortages.

Clean Energy Has Won the Economic Race For decades, spectacularly inaccurate forecasts have underestimated the potential of clean energy, buying time for the fossil-fuel industry. But as two new analyses from authoritative institutions show, renewables have already convinced the market and are now poised for exponential growth. DENVER – For decades, we at the Rocky Mountain Institute (now RMI) have argued that the transition to clean energy will cost less and proceed faster than governments, firms, and many analysts expect. In recent years, this outlook has been fully vindicated: costs of renewables have consistently fallen faster than expected, while deployment has proceeded more rapidly than predicted, thereby reducing costs even further. Thanks to this virtuous cycle, renewables have broken through. And now, new analyses from two authoritative research institutions have added to the mountain of data showing that a rapid clean-energy transition is the least expensive path

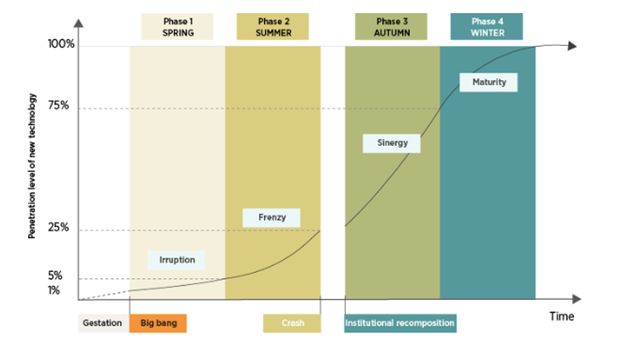

forward. Policymakers, business leaders, and financial institutions urgently need to consider the promising implications of this development. With the United Nations Climate Change Conference (COP26) in Glasgow fast approaching, it is imperative that world leaders recognize that achieving the Paris climate agreement’s 1.5° Celsius warming target is not about making sacrifices; it is about seizing opportunities. The negotiation process must be reframed so that it is less about burden- sharing and more about a lucrative race to deploy cleaner, cheaper energy technologies. With the world already suffering from climate-driven extreme weather events, a rapid clean-energy transition also has the virtue of being the safest route ahead. If we fail at this historic task, we risk not only wasting trillions of dollars but also pushing civilization further down a dangerous and potentially catastrophic path of climate change. One can only guess why forecasters have, for decades, underestimated the falling costs and accelerating pace of deployment for renewables. But the results are clear: bad predictions have underwritten trillions of dollars of investment in energy infrastructure that is not only more expensive but also more damaging to human society and all life on the planet. We now face what may be our last chance to correct for decades of missed opportunities. Either we will continue to waste trillions more on a system that is killing us, or we will move rapidly to the cheaper, cleaner, more advanced energy solutions of the future. New studies have shed light on how a rapid clean-energy transition would work. In the International Renewable Energy Agency (IRENA) report The Renewable Spring, lead author Kingsmill Bond shows that renewables are following the

same exponential growth curve as past technology revolutions, hewing to predictable and well-understood patterns. Accordingly, Bond notes that the energy transition will continue to attract capital and build its own momentum. But this process can and should be supported to ensure that it proceeds as quickly as possible. Policymakers who want to drive change must create an enabling environment for the optimal flow of capital. Bond clearly lays out the sequence of steps that this process entails. Examining past energy revolutions reveals several important insights. First, capital is attracted to technological disruptions, and tends to flow to the areas of growth and opportunity associated with the start of these revolutions. As a result, once a new set of technologies passes its gestation period, capital becomes widely available. Second, financial markets draw forward change. As capital moves, it speeds up the process of change by allocating new capital to growth industries, and by withdrawing it from those in decline. The current signals from financial markets show that we are in the first phase of a predictable energy transition, with spectacular outperformance by new energy sectors and the de- rating of the fossil-fuel sector. This is the point where wise

policymakers can step in to establish the necessary institutional framework to accelerate the energy transition and realize the economic benefits of building local clean- energy supply chains. As we can see from market trends highlighted in the IRENA report, the shift is already well underway. Reinforcing the findings from the IRENA report, a recent analysis from the Institute for New Economic Thinking (INET) at the Oxford Martin School shows that a rapid transition to clean energy solutions will save trillions of dollars, in addition to keeping the world aligned with the Paris agreement’s 1.5°C goal. A slower deployment path would be financially costlier than a faster one and would incur significantly higher climate costs from avoidable disasters and deteriorating living conditions. Owing to the power of exponential growth, an accelerated path for renewables is eminently achievable. The INET Oxford report finds that if the deployment of solar, wind, batteries, and hydrogen electrolyzers continues to follow exponential growth trends for another decade, the world will be on track to

achieve net-zero-emissions energy generation within 25 years. In its own coverage of the report, Bloomberg News suggests as a “conservative estimate” that a rapid clean-energy transition would save $26 trillion compared with continuing with today’s energy system. After all, the more solar and wind power we build, the greater the price reductions for those technologies. Moreover, in his own response to the INET Oxford study, Bill McKibben of 350.org points out that the cost of fossil fuels will not fall, and that any technological learning curve advantage for oil and gas will be offset by the fact that the world’s easy-access reserves have already been exploited. Hence, he warns that precisely because solar and wind will save consumers money, the fossil-fuel industry will continue to try to slow down the transition in order to mitigate its own losses. We must not allow any further delay. As we approach COP26, it is essential that world leaders understand that we already have cleaner, cheaper energy solutions ready to deploy now. Hitting our 1.5°C target is not about making sacrifices; it is about seizing opportunities. If we get to work now, we can save trillions of dollars and avert the climate devastation that otherwise will be visited upon our children and grandchildren.

Aramco warns world’s spare oil supplies are falling rapidly Saudi Aramco said oil-output capacity across the world is dropping quickly and companies need to invest more in production. It’s a “huge concern,” Chief Executive Officer Amin Nasser said in an interview in Riyadh, Saudi Arabia’s capital. “The spare capacity is shrinking.” His comments come with crude prices having soared 70% this year to around $85 a barrel. Many major consumers, including the U.S., Japan and India, have called on producers to pump more. The supply deficit in oil markets could worsen in 2022 if the

coronavirus pandemic eases and more people fly, he said. Declining rapidly “If there’s aviation pick up next year, that spare capacity will be depleted,” he said. “It’s now getting to a situation where there’s limited supply — whatever is left that’s spare is declining rapidly.” Several oil and gas traders have criticized governments and climate activists for calling on companies to stop investing in fossil fuels, saying that will cause shortages of energy in the coming decade. Aramco, the world’s biggest oil company, is investing billions of dollars to raise its daily capacity to 13 million barrels from 12 million. It expects to complete the project by 2027. Many Wall Street banks and OPEC+ members doubt there will be supply shortages next year. JPMorgan Chase & Co. has said oil markets will shift to a supply surplus of 1 million barrels by March from a deficit of around 1.5 million barrels now. Saudi Arabia’s energy minister told Bloomberg on Saturday there could be a “huge uplift” in crude inventories in 2022. “We still have Covid,” Prince Abdulaziz bin Salman said, justifying OPEC+’s refusal to ease deep supply cuts it began last year any faster. “We still have jet fuel limited in terms of growth. If you do more now, you’re accelerating the problem.” The Organization of Petroleum Exporting Countries and its partners are increasing daily output by 400,000 barrels each month. The 23-nation group, led by Saudi Arabia and Russia, next meets on Nov. 4 to decide whether to change strategy. Written By Salma El Wardany and Matthew Martin

How China Plans to Become Carbon-Neutral by 2060 China’s industrialization has occurred at a breathtaking pace, lifting hundreds of millions out of poverty and transforming the country into the world’s factory floor. That’s also made it the biggest emitter of carbon dioxide, the main greenhouse gas driving climate change. The most-populous nation has set itself the ambitious goal of becoming carbon-neutral by 2060, a challenging target given it hasn’t even reached its emissions peak. To get there, President Xi Jinping wants to transition away from an economy reliant on coal and other fossil fuels by switching to renewable energy and developing new technology to capture emissions. 1. What is carbon neutral? It means cutting as much of your carbon dioxide emissions as possible and then offsetting what you can’t eliminate. For a country, this could mean switching to renewable energy such as

solar power instead of coal and investing in projects that absorb carbon dioxide, such as reforestation. Carbon neutral has become a goal of companies and countries alike to address public concerns about the impact emissions have on the climate. 2. What is China’s goal? Even though China is the world’s second-largest economy, it’s still classified as a developing nation and hasn’t reached its emissions peak. That’s forecast to come by 2030, with Xi committing to carbon neutrality by 2060, 10 years after the U.S. deadline set by President Joe Biden. If China pulls it off, it would be the fastest decline from peak emissions among major economies, speedier than Europe’s goal of 70 years and the US target of 40 years. China’s plan, which the country’s climate envoy said includes all greenhouse gases and not just carbon dioxide, would boost global efforts to limit the rise in temperatures and potentially give it greater sway in global matters. 3. What needs to be done? China has to find replacements for the fossil fuels that have powered its economy and rapid urbanization. A key early step was taken in July when China opened the world’s largest carbon trading market, creating a framework for how emissions are priced and regulated in the country. It’s already pushing the expansion of electric vehicles and automation while investing in nuclear power, which doesn’t emit greenhouse gases. There is more spending on research into technologies such as storage batteries and using hydrogen as a fuel to complement low- emissions energy sources. The government will have develop more wind and solar power projects so that coal-fired plants play a smaller role in generating electricity. Local authorities have been told to develop regional plans to lower emissions and some have already taken measures to curb what they perceive as wasteful uses of electricity, such as Bitcoin

mining. The ruling Communist Party of China has an overarching goal of creating a “great modern socialist country” to ensure a prosperous life for its citizens. That’s a mantra that has required continuous economic growth and led to increased pollution. Breaking the link between growth and emissions will require policies that take aim at fossil fuels and encourage development of renewable energy. Monetary policy will need to be adjusted if the transition causes inflationary pressure. Beijing will also need to support vulnerable sectors and regional economies during the decarbonization process. For example, the coal industry in Shanxi contributes 20% of the province’s revenue, according to PingAn Securities chief economist Zhong Zhengsheng. 5. What will be the economic impact? Services and high-technology will have to boost their contribution to the economy, a move that could unleash investment demand of as much as 300 trillion yuan ($46.3 trillion), according to the People’s Bank of China. The central bank has said a big chunk of the funds will come from market investors but a policy framework encouraging private investment will be important. That is in addition to cleaner air, improved road safety and prevention of potential climate damage that the World Bank said could be worth 3.5% of gross domestic product by 2030. Such benefits have to be weighed against the impact on ordinary Chinese people of an economic restructuring that phases out jobs in carbon-emitting sectors, with the coal mining and processing industry employing 3.5 million workers alone. 6. Who are the biggest losers? China’s 2,200 electricity utilities powered by fossil fuels, a group that accounts for almost half of the carbon China spews into the atmosphere and 14% of the world’s total, are among

the first to feel the impact through the country’s carbon market. Power is one of the eight industries that account for nearly 90% of its carbon emissions, a group that also includes steel, construction materials and transport, according to a report by China International Capital Corp. Eliminating their dependence on fossil fuels will require a move to cleaner sources such as wind and solar and spending on mitigation measures or carbon offsets. Regional Chinese economies that rely heavily on fossil fuel production, such as Shanxi and Inner Mongolia provinces, will also be affected. 7. Who stands to benefit? Electric-vehicle makers are one of the high-profile beneficiaries of China’s plan thanks to government subsidies. Beijing has set a target of having new-energy vehicles account for 20% of sales by 2025 compared with 6% in 2020. Utilities that make the shift to renewable sources will also benefit, along with providers of services such as emission measurement and carbon trading, according to Nannan Kou, head of China research for BloombergNEF. Other winners could include makers of photovoltaic systems, recycling firms and producers of new materials and non-ferrous metals for electric vehicle assembly. 8. What role will the central bank play? China’s goal of carbon neutrality is shared across China’s key institutions and is a top priority for the PBOC. The central bank removed so-called clean-coal projects from its definitions of green bonds while pledging to revamp tools so it can offer cheap funds for banks to encourage more environmentally focused loans. Regulators also plan to adjust the rules on capital adequacy and how it counts green assets. At the end of March, China’s outstanding green loans stood at 14 trillion yuan, an amount set to expand at a rapid pace. 9. Will private banks play a role?

Banks will need to change who they lend to and balance how their loans mesh with Beijing’s climate ambitions. The high capital cost of building power plants, steel mills and factories mean companies in those sectors often carry significant financing needs and any rapid change could affect their ability to manage credit risks, according to Zhou Xuedong, executive vice president at National Development Bank and a former senior PBOC official. He said a climate-change stress test for financial institutions will be necessary. This story has been published from a wire agency feed without modifications to the text. Rising LNG imports provide scant relief for Europe power

crisis Reuters/London Europe’s imports of liquefied natural gas (LNG) are picking up as winter approaches but there is little relief for the region’s power crunch because competition with Asia for supplies is so intense. Power and gas demand has spiked due to low inventories and surging requirements in Asia and Europe as economies recover from the Covid-19 crisis. Cold weather in the northern hemisphere has also increased demand for power, prompting buyers to be more active on the spot market to bridge supply gaps and driving LNG prices to record levels. Wholesale gas markets are reflecting that, with benchmark European TTF values hitting all-time highs. Asian spot LNG prices hit a record peak of above $56 per million British thermal units (mmBtu) earlier this month. Prices have since retreated slightly to around $30 per mmBtu, but are still up 500% from last year. Northwest Europe’s LNG imports over the January-September period were down by 5.5mn tonnes from levels seen a year earlier, but have picked up since the start of the winter gas season which runs from October to March, when there is higher demand. Competition between Europe and Asia and a spike in global gas prices saw European TTF and Asian JKM LNG benchmark prices chase each other higher, with the latter priced at a premium to TTF, drawing more supply to Asia rather than Europe. As a result, northwest Europe is unlikely to see a strong flurry of LNG supply to help ease prices. “Our latest balance calls for net LNG deliveries to Northwest Europe, in Belgium, France, Netherlands and the UK, this winter to average 114mn cubic metres per day, roughly in line with year ago levels of 116mn cubic metres per day,” said Luke

Cottell, LNG analyst at S&P Global Platts. Asia is home to the world’s three biggest LNG buyers, China, Japan and South Korea, who tend to keep buying throughout the winter. European gas storage levels were well below where they should have been at the start of the winter season on October1, pushing European buyers to compete aggressively for spot cargoes. “Competition from Asia for flexible Atlantic Basin LNG is expected to be robust, with Northwest Europe facing challenges in competing with largely price insensitive Northeast Asian buyers who have continued to procure spot cargoes despite record high JKM,” said Samer Mosis, manager of global LNG analytics at S&P Global Platts. Usually, when Asian LNG and TTF prices are so closely coupled, US LNG sellers would favour sending cargoes to Europe to save shipping time and costs, said Robert Songer, LNG analyst at commodities intelligence firm ICIS. But that is not the case this year. ICIS’s LNG Edge shipping platform shows that China, Japan and South Korea have all imported more US LNG than in any previous year, while Atlantic Basin importers like Spain, France and the UK have all seen smaller portions of US cargoes. North American LNG exporters have been adding to capacity because of demand in major Asian economies. US exports of LNG are expected to average 9.7bn cubic feet per day (Bcf/d) this year, 3.2 Bcf/d higher than the 2020 record high of 6.5 Bcf/d. This year, the United States’ exports of LNG are also expected to exceed its annual pipeline exports of natural gas for the first time, the US Energy Information Administration (EIA) said in a report. But with the bulk of US exports destined for Asia, Europe’s best hope for significantly boosting supplies may be a mild winter in China, which is hard to predict, analysts said. “As long as unexpected cold from the La Nina (weather) system doesn’t see China keep outbidding Europe for cargoes, there is certainly some avenues for more gas to land in Europe in the

coming months,” said Ryan McKay, commodity strategist at TD Securities. Wall Street hails a new era of oil prices: Higher for longer Could the era of cheap oil supply be gone for good? That’s the conclusion of some of the biggest commodities desks on Wall Street, where banks have been lifting their long-term price forecasts, often by $10 or more. While the US shale boom brought about a “lower-for-longer” mantra, the market is now fixated on climate change and the dwindling appetite to invest in fossil fuels. Instead of growing supply, companies are under pressure to limit their spending, causing a structural under-investment in new production that — the argument goes — will keep oil prices

higher for longer. “My advice to clients is that you want to stay long oil until you know where that equilibrium price is” that brings new supplies online, said Jeff Currie, head of commodities research at Goldman Sachs Group Inc. “We know it’s above these levels because we haven’t had a big uptick in capex and investment.” The notion of a supply gap is nothing new. Since prices crashed in 2014, analysts have talked up the potential for demand to outstrip production as a result of underinvestment. But the rout in energy prices from Covid-19, combined with pressing environmental concerns, offer reason to think this time is different. The number of oil and gas drilling rigs globally may have recovered from the lows of when oil prices turned negative last year, but they are still down more than 30% on the start of 2020. Current figures are about as low as they were in 2016, according to Baker Hughes Co., despite headline crude prices being near a seven-year high. Future View Among the banks seeing higher prices for longer, Goldman says $85 for 2023. Morgan Stanley bumped what it calls its long- term forecast up by $10 to $70 this week, while BNP Paribas sees crude at almost $80 in 2023. Other banks including RBC Capital Markets have talked up the prospect of oil being at the start of a structural bull run. Such estimates imply that a commodity vital to the global economy has become structurally more expensive. Oil price expectations underpin hundreds of billions of dollars of equity valuations for major international oil companies like Royal Dutch Shell Plc and BP Plc. There’s an ever-dwindling appetite to lend on the part of

investors too. In the last week alone, the largest French banks said they would curb the financing of the shale oil and gas industry from early next year. Ecuador recently had to double the amount of banks that could provide it with credit guarantees as financial institutions shunned crude harvested from the Amazon. Unsustainable Not everyone supports the idea that prices can be stay at elevated levels. Citigroup Inc. said in a report this month that crude below $30 and above $60 looks unsustainable in the long-term. A prolonged price above $50 could add 7 million barrels a day of extra supply, the bank’s analysts including Ed Morse wrote in a note. “Mid-term, cost indicators keep pointing to a fair-value range between $40-$55 a barrel,” they said. But others see a tide that’s turning, especially given changes in the U.S., which has effectively become a swing producer in recent years. On one front, publicly listed U.S. shale companies remain constrained in growing production. When EOG Resources Inc. said in February that it planned to grow output its shares fell the most of any company on the S&P 500. There have been few, if any, similar comments from producers since. Alongside that, the impact of field declines is growing clearer. In November, the Permian Basin was the only onshore U.S. field to show meaningful year-on-year production growth. All others were either flat or down, according to an Energy Information Administration report. Similarly, while some of the key OPEC+ producers find themselves with spare capacity that they can dip into next year, others including Nigeria and Angola are already showing signs of struggling to lift production further.

“People have become very comfortable with the idea that shale will be there and we’re not resource constrained,” said David Martin, head of commodities desk strategy at BNP Paribas. “That’s a question mark in my mind.” And in a world spending less money on fossil fuels, questions then turn to demand, which doesn’t look like peaking any time soon. The International Energy Agency said earlier this month that spending on fossil fuels is lower than needed if current demand growth continues. It only sees oil demand starting to decline in the 2030s under current policies. However, Morgan Stanley estimates that supply could stop expanding by 2025, leaving a sizable gap. “We are running at net-zero type capex levels, whilst at the same time demand is not following the net-zero trajectory,” said Martijn Rats, an oil strategist at the bank. “Demand will be above 100 million barrels a day for the rest of the 2020s, but on the supply side we’re not going to produce that with current investment levels.” This story has been published from a wire agency feed without modifications to the text.

You can also read