Alumni Network Southern Region webinar HK IPO market review for 2021 and the latest regulatory update - 25 January 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Alumni Network Southern Region webinar HK IPO market review for 2021 and the latest regulatory update 25 January 2022

Opening

Alumni Network Southern Region

Ryan Wu

Lead Client Service Partner, Strategic Clients

Alumni Network Southern Region

Deloitte China

Tel: +852 2740 8855

Email: rywu@deloitte.com.hk

© 2022. For information, contact Deloitte China. Presentation title 2

Disclaimer Any material or explanation (including but not limited to presentation slides or verbal explanation) (collectively “Material”) provided hereunder serves as a general guide instead of a basis for decision making and shall not be construed as any advice, opinion or recommendation given by Deloitte Touche Tohmatsu (“DTT”) on the presentation. In addition, the Material will be limited by the time available and by the information made available to (“DTT”), you should not consider the Material as being comprehensive as DTT may not become aware of all facts or information. Accordingly, DTT will not be in a position to make a representation, and will not make a representation as to the accuracy, completeness and sufficiency of the Material. You will rely on the contents of the Material at your own risk. This Material shall be kept confidential and any person other than DTT’s authorized personnel shall not, in any way, retain, use or disseminate this Material without DTT’s prior written consent. All duties and liabilities (including without limitation, those arising from negligence or otherwise) to all parties, including you are specifically disclaimed. All copyrights and other intellectual property rights contained in the Material are reserved by DTT. For the avoidance of doubt, the Material contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of the Material, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on the Material. The speaker's view, comment and speech are personal and do not constitute any position or opinion of DTT or otherwise represent DTT, or partners, principals, members, owners, directors, employees thereof. DTT does not endorse and is not responsible for any such personal expression in whatever form. Please take the view as the speaker's own only. © 2022. For information, contact Deloitte China. 3

Deloitte speaker

Edward Au

Managing Partner, Southern Region, Deloitte China

Edward Au is Deloitte China Southern Region Managing Partner. He is responsible for Deloitte China's

offices in Southern China, and with a focus on the development of the practice in the Greater Bay Area.

Edward is also Vice President of the Hong Kong Institute of Certified Public Accountants and contributes to

other organizations and the community in Hong Kong through his service including Financial Services

Development Council and Hong Kong Red Cross.

© 2022. For information, contact Deloitte China. 4

Deloitte speaker

Johnny Chu

Partner, Audit & Assurance, Deloitte China

Johnny is an audit partner and has extensive experience in serving listed and multinational companies. He

has been actively involved in various IPOs in Hong Kong and is a member of the Capital Market Service

Group in Deloitte China. Johnny has broad exposures to clients in many sectors but has focused

predominately in serving clients in consumer businesses and manufacturing industries.

Johnny is a member of our Capital Market Service Group, Southern China and has assisted many of his

clients to successfully list on Hong Kong Stock Exchange. He also provides advisory services to clients on IPO

plans and strategies as well.

© 2022. For information, contact Deloitte China. Presentation title 5

Agenda 1. Overview of global macroeconomic and geopolitical conditions in 2021 2. Review of IPO Market in 2021 - Global 3. Review of IPO Market in 2021 - Hong Kong 4. Outlook for IPO Market in 2022 - Hong Kong 5. Regulatory landscape for Hong Kong 6. HK SPAC Regime - overview 7. Q&A 8. Closing © 2022. For information, contact Deloitte China. 6

Hong Kong IPO Market Review for 2021 and Latest Regulatory Update Edward Au, Southern Region Managing Partner Deloitte China 25 January 2022

Review of IPO Market in 2021 ─ Global © 2022. For information, contact Deloitte China. 9

NASDAQ, NYSE, and Shanghai Stock Exchange were the top 3 exchanges globally by IPO proceeds

raised, followed by HKEX and Shenzhen Stock Exchange

Top 5 global stock exchanges by IPO proceeds

raised in 2021

NASDAQ

NYSE

352 IPOs Shanghai Stock

Exchange

Raising HKD782.2 110 IPOs

billion HKEX

Raising HKD454.2 249 IPOs Shenzhen Stock

billion Exchange

Raising HKD441.0 97 IPOs

billion

Raising HKD331.4 232 IPOs

billion

Raising HKD204.8

billion

Source: China Securities Regulatory Commission (CSRC), NASDAQ, Hong Kong Stock Exchange (HKEX), New York Stock Exchange (NYSE), Bloomberg and Deloitte’s analysis, as of 31 December 2021. All of the proceeds

include funds raised from the listings of real estate investment trusts, but exclude proceeds raised by investment trust companies, closed-ended investment companies, closed-ended funds, and special purpose

acquisition companies (SPACs).

© 2022. For information, contact Deloitte China. 10

Proceeds raised by the top 10 global IPOs in 2021 were up 36% from 2020’s level, with Chinese

Mainland and HK IPOs dominating the lists for both years

2021 2020

Rank Company Exchange Proceeds Rank Company Exchange Proceeds

(HKD100m) (HKD100m)

1 Rivian Automotive NASDAQ 1,069 1 SMIC SSE STAR Market 588

2 China Telecom SSE 576 2 JD.com HKEX 346

3 Kuaishou Technology HKEX 483 Beijing-Shanghai

3 SSE 344

High Speed Railway

4 Coupang NYSE 353

JD Health

4 HKEX 310

5 Didi NYSE 344 International Inc.

5 Snowflake NYSE 299

6 InPost SA AEX 304

6 Airbnb NASDAQ 297

7 Krafton Inc KRX 300

7 DoorDash NYSE 261

8 JD Logistics HKEX 283

8 NetEase HKEX 243

9 CTGR SSE 274

9 JDE Peet's BV AEX 219

10 BeiGene SSE STAR Market 271

10 Allegro.eu SA GPW 218

Total 4,257

Total 3,125

Source: CSRC, HKEX, NYSE, NASDAQ, Amsterdam Stock Exchange (AEX), Korea Exchange (KRX), Warsaw Stock Exchange (GPW), Bloomberg and Deloitte’s analysis, as of 31 December 2021.

Includes funds raised from listings of real estate investment trusts, but excludes proceeds raised from investment trust companies, closed-ended investment companies, closed-ended funds, and special purpose

acquisition companies (SPACs).

© 2022. For information, contact Deloitte China. 11Review of IPO Market in 2021 ─ Hong Kong © 2022. For information, contact Deloitte China. 12

Affected by regulations introduced for several Chinese Mainland industries, HK IPO proceeds raised

declined by 17% in 2021 and the number of IPOs dropped by 34%

No. of IPOs

34%

Proceeds raised 2021 97 IPOs

17%

Raising HKD331.4 bn

• In 2021, the number of mega and small IPOs

fell sharply, with the drop in mega IPOs the

major cause of the overall decline

• IPO activity slowed after Q2

• More companies went public under the new

146 IPOs

listing regime, including WVR IPOs and pre- 2020

revenue biotech and pharmaceutical Raising HKD 397.9 bn

companies

• There was just 1 GEM IPO

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 13There were a few more new economy IPOs in 2021 than there were in 2020, although proceeds raised

edged down by 4%

• The overall trend in new economy IPOs

remained the same, with health care & 44 IPOs HKD 226 billion 2021 No. of IPOs

pharmaceutical companies dominating volume 7%

and TMT taking the lead in proceeds raised Proceeds raised

• Proceeds from 8 mega IPOs in TMT reached

4%

•

more than 60% of total proceeds, vs. 5 in 2020

20 pre-revenue biotech and pharmaceutical

41 IPOs HKD 234.6 billion 2020

companies listed in 2021, vs. 14 in 2020

Industry distribution of new economy IPOs (by number) Industry distribution of new economy IPOs (by proceeds)

2021 2020 2021 2020

4% 2% 13% 3% 1%

5% 23%

32% 42% 40%

3% 44%

57% 46%

7% 61% 12%

5%

Financial Services Health Care & Pharmaceutical Consumer Business TMT Manfuacturing Property

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 14Hong Kong has emerged as the world’s second largest and Asia’s largest biotech fundraising hub. Its pre-

revenue biotech listings continue to grow

0 5 14 28 48

2017 2018 2019 2020 2021

No 18A listings and no

IPO funds raised

HKD18.0 billion

raised HKD 33.8 billion

raised

HKD 74.0 billion

raised

HKD 111.7 billion

raised

Source: HKEX and Deloitte’s analysis as at 31 December 2021

© 2022. For information, contact Deloitte China. 15Knowledge check

Do you know how many of the 10 biggest listed companies in Hong Kong by market

capitalization as of 24 January 2022 are new economy companies?

A 3

B 4

C 5

D 6

© 2022. For information, contact Deloitte China. 16Importance of the new economy sector to Hong Kong’s capital market is growing

Top 10 HK-Listed Companies by Market Capitalization

1 Tencent Holdings 4,512

2 Alibaba Gp - S W 2,556

3 Meitun - W 1,428

China Construction Bank 1,428

China Mobile 1,115

HSBC 1,099

AIA 1,065

4 JD.com - S W 905

Hong Kong Stock Exchange 600

5 NetEase - S 515

(HKD billion) 0 1,000 2,000 3,000 4,000 5,000

Source: AAStocks.com, Deloitte’s analysis, based on the market closing prices on 24 January 2022

© 2022. For information, contact Deloitte China. 17Overview of HK IPO market – 2021

The number of IPOs in Q4 continued to drop, hitting a recent-year low since 2012; proceeds raised in

2021 failed to surpass 2020’s level but still outperformed previous years

Lowest proceeds and number Highest proceeds in

Most IPOs in recent

of IPOs in recent years recent years

years (HKD billion)

70 300

7

60 250

12

33

50

17 200

13 8 1

25

Number of IPOs

40 20 2

1

Proceeds

5 2 150

49 8 1

30 5 19 59

5 1 10 20 17

2

3 7 29 46 100

20 3 5 9 16 40 42 2 3 38

3 5 27 5 38 35

4 3 2 39

6 9 30 31 31

1 16 27 16 27 24

10 23 18 15

24 19 22 20 18 20 32 20

50

5 19

10 10 12 13 10 18 16 11 13 14

26

6 13

0 0

HK MB IPOs HK GEM IPOs IPO proceeds

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 18Overview of HK IPO applications – 2021

Total IPO applications received in 2021 were up 37% from the same stage in 2020; there were 8% fewer

lapsed applications although withdrawn and returned applications increased

Total IPO applications 316 231 37%

received*

IPO applications being 42%

processed**

131 92

Lapsed applications (i.e.

approval in principle 8%

44 48

granted but not listed prior

to lapse of application)

1 1 0%

Rejected applications

Withdrawn applications 9 6 50%

2 0 N.A.

Returned applications

2021 2020

Source: HKEX, Deloitte's analysis, as of 31 December 2021.

*Includes investment vehicles applying to list under Chapters 20 and 21 of the MB Listing Rules, applications for transfer from GEM to MB, applications from deemed new applicants under Rule 8.21C or Rule 14.84 of

the MB Listing Rules, and very substantial acquisitions regarded as reverse takeovers under Rule 14.06(6) of the MB Listing Rules or Rule 19.06(6) of the GEM Listing Rules.

**Figures for 2020 and 2021 include IPO applications that were accepted between 1 January and 31 December in 2020 and 2021.

© 2022. For information, contact Deloitte China. 19Overview of HK IPO market – 2021

Boosted by 5 mega IPOs (4 of which were new economy IPOs with WVR structures), proceeds raised by the

top 5 IPOs increased by 14% to HKD139.8 billion from HKD123 billion in the same period of 2020

W

1. Kuaishou

W Technology – W

(HKD48.3 billion)

1. JD.com – SW

(HKD34.5 billion)

2. JD Logistics 2. JD Health

(HKD28.3 billion) (HKD31.0 billion)

W 3. Baidu – S W

(HKD23.9 billion)

3. NetEase – S

(HKD24.3 billion)

W 4. Bilibili – S W

(HKD23.2 billion) 4. YUM China – S

(HKD17.3 billion)

W 5. XPeng – W

(HKD16.0 billion)

2021 2020

5. CBHB – H shares

(HKD15.9 billion)

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 20Overview of HK IPO market – 2021

Chinese Mainland companies accounted for more than 80% of HK IPOs and over 90% of total proceeds;

fewer overseas companies went public in HK; there were more loss-making IPOs due to an increase in pre-

revenue biotech listings

Number of IPOs by location of issuer P/E multiples of HK IPOsHK IPO valuation analysis – 2021

Nearly half of IPOs were priced at above the mid-point of their indicative ranges, and 35% were priced

below their mid-point, a decline of 12 percentage points from 2020’s level

2021 2020

Top of range

4% 6%

Above mid-point of range 2% 6%

1% 24%

33% Mid-point of range

25% Below mid-point of range

Bottom of range

35%

Below range

17%

10% 17% Fixed price

5%

Others 4%

11%

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 22Analysis of HK IPO’s public offering subscriptions – 2021 5 most over-subscribed IPOs in 2021

Public offering subscriptions were generally better than Issuer

Over-subscription

rate

they were in 2020. The top 5 over-subscribed IPOs in 1H,

New Horizon Health – B 4,133x

most of them new economy companies, remained the top 5

Angelalign Technology 2,079x

at the end of the year

Yidu Tech 1,634x

Cheshi 1,275x

99

(2020: 94%)

Kuaishou Technology – W 1,204x

% of IPOs over-subscribed Best performing IPOs by over-

subscription rate

4,133x 4,500

Among those over-subscribed, 3,600

Over-subscription rate

(2020: 58%)

56 % were over-subscribed by

1,949x

2,700

1,800

900

over

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

20

x 2021

New Horizon

Health – B

2020

Ye Xing Gp

0

© 2022. For information, contact Deloitte China. 23Industry representation of HK’s IPOs in 2021 (by number)

Health care & pharmaceutical and property took the lead, with representation of the former up sharply

from 2020, resulting in varying reductions in the representation of nearly every other sector except

consumer business

2021 2020

Energy & Resources

1% Financial Services 3%

19% 1% 5%

19%

Health Care &

14%

Pharmaceutical

33%

Manufacturing

17% Property 17% 10%

Consumer Business

8%

21% TMT 32%

Others

Source: HKEX, Deloitte’s analysis as of 31 December 2021.

© 2022. For information, contact Deloitte China. 24Industry distribution of HK’s IPOs in 2021 (by proceeds)

TMT was well ahead thanks to 7 large or mega IPOs, followed by health care & pharmaceutical

2021

TMT 140.5 3%

Consumer Business 58.3

Property 15.8 22%

Kuaishou, Baidu,

Manufacturing 35.4 42% Bilibili, Linklogis

Health Care & Pharmaceutical 72.0 and Trip.com

drove TMT into 11%

Financial Services 9.1 the lead

5%

Energy & Resources 0.3 17%

(HKD billion) 0 - 50 100 150

Energy & Resources Financial Services Health Care & Pharmaceutical Manufacturing Property Consumer Business TMT

2020

TMT 109.7

6% Consumer Business 62.0

27% TMT proceeds Property 94.3

24% Source: HKEX, Deloitte’s analysis as

boosted by Manufacturing of 31 December 2021.

10.9

listings of

NetEase, JD.com, Health Care & Pharmaceutical 97.6

GDS and XDF.CN 3% Financial Services 22.3

16%

Energy & Resources 1.1

24%

(HKD billion) 0 40 80 120

© 2022. For information, contact Deloitte China. 25Knowledge check

Which one below is NOT a key highlight of the HK IPO market in 2021?

A 2 out of global top 10 IPOs in funds raised

B Listed 1st homegrown tech unicorn

C New records in WVR and biotech listings

D Top 3 in IPO funds raised in the world

Increased weight of new economy IPOs and their funds raised in the

E market

© 2022. For information, contact Deloitte China. 26Outlook for IPO Market in 2022 – Hong Kong © 2022. For information, contact Deloitte China. 27

Industry distribution of active HK listing applications in 2021

There were around 58% more active MB listing applications in 2021 than in 2020, mostly from health

care & pharmaceutical, followed by TMT and property; GEM continued to be dominated by consumer

business, with a further reduction in the number of applications

MB GEM

Consumer Business

Energy & Resources

14%

25% 25%

3% Financial Services

3% 37%

Property

TMT

12% 21%

Manufacturing

25%

Health Care & 13%

22%

Pharmaceutical

Others

Number of applications: 141 Number of applications: 8

Source: HKEX, Deloitte’s analysis, as of 31 December 2021.

© 2022. For information, contact Deloitte China. 28Number of active HK listing applications from overseas companies in 2021

Malaysian companies dominated HK listing applications from overseas businesses, and most overseas

applicants were manufacturing companies

Overseas applicants by country Overseas applicants by industry sector

20% 20% 20%

40%

MB

20%

40% Number of applications: 5

40%

Consumer Business Property

Manufacturing TMT

Malaysia Singapore Vietnam

Health Care & Pharmaceutical

GEM

Number of applications: 1

100% 100%

Source: HKEX, Deloitte’s analysis, as of 31 December 2021.

© 2022. For information, contact Deloitte China. 29In 2022, the HK market’s liquidity will be affected by the Fed's balance sheet reduction and interest rate

hikes, and China concept stocks will accelerate their HK listings, with overall performance expected to

remain robust

More high-growth Asian More China concept stocks to

companies to seek HK listings return and list in HK

More HK local unicorns to Sustainability and ESG

go pubic companies to go public

HK in a strong position to attract listings of innovative industry

and new economy companies

Enhanced listing regime for Promoting sustainable and

SPAC listing regime Ongoing geopolitical issues Maturing market ecosystem Staying relevant green finance

overseas issuers

Clarification of dual primary More technology companies Chinese companies HK has been Asia’s largest, Continuous Further developing sustainable

listing regulations and will be attracted to list in HK, have to consider more and the world’s 2nd largest, enhancement and financial products to bring more

requirements for opening including SPAC M&A targets farsighted and prudent biotech fundraising hub, reform of listing growth opportunities for issuers and

secondary listings. from privatized China fundraising solutions with related fund investors regimes and rules investors, and subsequently support

and strategies. Chinese Mainland's "30-60" goals of

Concept Stocks. to support the development

peak emissions by 2030 and carbon

of new economy enterprises.

neutrality by 2060.

© 2022. For information, contact Deloitte China. 30Regulatory landscape – Hong Kong © 2022. For information, contact Deloitte China. 31

In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

“Fast Interface for New Issuance” (FINI)

issuers, including secondary listing and dual

platform accessible by market

primary listings

participants to handle subscription,

pricing, allotment, payment, listing Hong

approval and stock admission

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The Mainboard (MB) listing requirements have been

The regulators identified a list of features increased to HKD80 million for the three-year track

that may prompt them to make further record period to align better with the market

inquiries regarding a new listing. capitalization requirements raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on Corporate Governance (CG)

is heavy on investors protection measures

and ESG and expected practice.

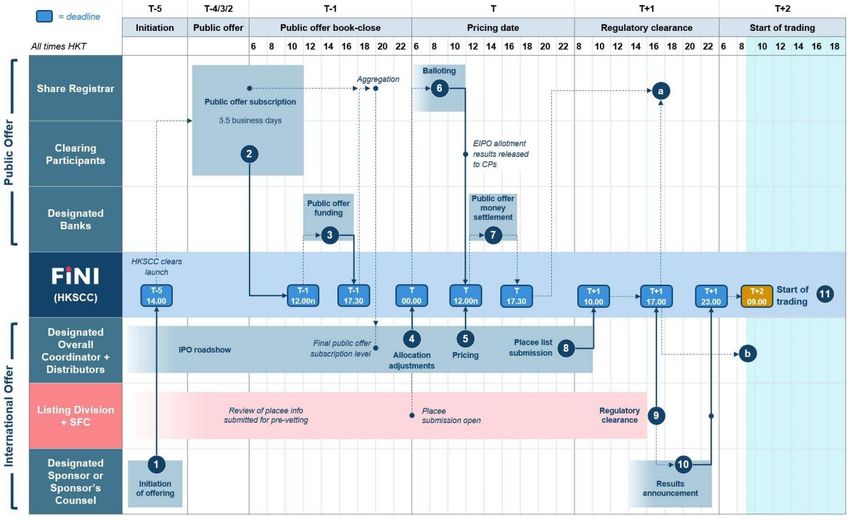

© 2022. For information, contact Deloitte China. 32T+2 Settlement Under FINI Plan

Modernising Hong Kong’s IPO Settlement Process

FINI

(Fast Interface for

New Issuance)

A secure web-based

portal for market

participants and

authorities to interact

digitally and

seamlessly for end-

to-end IPO settlement

process in Hong Kong

Expected to launch in

Q4 2022 at the

earliest

Source: Fast Interface for New Issuance (FINI): Concept Paper Conclusions – Modernising Hong Kong’s IPO Settlement Process published by HKEX on 6 July 2021

© 2022. For information, contact Deloitte China. 33In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

FINI platform accessible by market

issuers, including secondary listing and dual

participants to handle subscription,

primary listings

pricing, allotment, payment, listing

approval and stock admission Hong

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The MB listing requirements have been increased to

The regulators identified a list of features HKD80 million for the three-year track record period to

that may prompt them to make further align better with the market capitalization requirements

inquiries regarding a new listing. raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on CG and ESG and expected

is heavy on investors protection measures

practice.

© 2022. For information, contact Deloitte China. 34HK’s new secondary listing rules – Chapter 19C (Main Board)

In effect since 30 April 2018

Chinese concept stocks

“Innovative” company?*

(1) New technologies; (2) innovations; and/or (3) a new business

model, which also serves to differentiate the company from

existing players

What is an “innovative”

Qualifying primary stock exchanges company?

New York Stock Exchange, Nasdaq or London Stock Exchange Main Market • Its success is demonstrably attributable to the

(“premium” only)

application, to the company’s core business, of (1),

(2) and/or (3);

Good track record of regulatory compliance • R&D is a significant contributor to its expected

At least two full financial years value and constitutes a major activity and expense;

• Demonstrable success attributable to its unique

features/IP; and/or;

Expected market capitalization at time of listing* • Outsized market cap./intangible asset value relative

If below HKD40 billion, needs at least HKD1 billion of revenue in most recent audited

to tangible asset value

financial year and HKD10 billion expected market cap at time of secondary listing

* These only apply to secondary listing with a WVR structure upon the consultation conclusion for Qualified to seek listing under Chapter 19C

“Listing Regime for Overseas Issuers” published in November 2021. 19C.03 Rules 8A.04 to 8A.06 do not

apply to a qualifying Issuer seeking a secondary listing under Chapter 19C.

© 2022. For information, contact Deloitte China. 35Listing regime for Overseas Issuers

The enhanced overseas listing regime provides flexible dual primary listings with WVR and VIE

Structures, and Expansion of Secondary Listing regime

Recognised

jurisdictions • No distinction

• Codification and consolidation of and

requirements of the two routes acceptable

• Codification of all secondary listing jurisdictions

related JPS provisions into Chapter

19C of the Listing Rules

• Non-WVR Greater China Issuers

seeking a secondary listing are no

longer required to demonstrate that

they are innovative companies and Enhanced

have the option of meeting a regime

minimum market capitalisation at

listing of either HKD3 billion or Shareholder • 1 common set of Core Standards

HKD10 billion Secondary

protection applicable to all issuers regardless of

• Codification of JPS Automatic Waiver listings

standards their places of incorporation

eligibility requirements with minor

modifications

• An issuer will be regarded as having a Dual primary

primary listing on the Exchange upon listings • Grandfathered Greater China Issuers and Non-Greater China Issuers

its delisting from the stock exchange with Noncompliant WVR and/ or VIE Structures may apply directly for

on which it is primary listed a dual primary listing and retain the non-compliant structures

• Codification of some conditional Common Waivers for dual-primary

© 2022. For information, contact Deloitte China. listed issuers and the principles for granting Common Waivers 36Knowledge check

Do you know how many overseas listed China concept stocks have returned to list in

HKEX since the new listing regime (i.e. April 2018)?

A 16

B 17

C 18

D 19

© 2022. For information, contact Deloitte China. 37The secondary listing and dual-primary listing regimes of HK are well received among US-listed Chinese

technology companies

2018 August 2019 November December

6 13 20 27 4 11 18 25 2 9 16 23 30

BeiGene, Ltd. – B (06160) Alibaba Group Holdings Ltd. –

S W (09988)

2020 June July August September October November

1 8 15 22 29 6 13 20 27 3 10 17 24 31 7 14 21 28 5 12 19 26 2 9

NetEase, Inc. – S (09999)

JD.com, Inc. – SW (09618)

Yum China Holdings, Inc. – S

(09987)

Huazhu Group Ltd. – S (01179)

Zai Lab Ltd. – S B (09688)

ZTO Express (Cayman) Inc. – SW

(02057)

Baozun Inc. – SW (09991)

GDS Holdings – SW (09698)

New Oriental Education &

Technology Group Inc. – S

(09901)

Source: HKEX and Deloitte’s analysis as at 31 December 2021

© 2022. For information, contact Deloitte China. 38The secondary listing and dual-primary listing regimes of HK are well received among US-listed Chinese

technology companies (cont’d)

2021 March April July August December

1 8 15 22 29 5 12 19 26 5 12 19 26 2 9 16 23 30 6 13 20 27

Autohome Inc. – S (02518)

Baidu, Inc. – S W (09888)

Bilibili Inc. S W (09626)

Trip.com – S (09961)

Xpeng Inc. – W (09868)

Li Auto Inc. – W (02015)

Weibo Corp. - S W (09898)

Total funds raised: HKD

Source: HKEX and Deloitte’s analysis as at 31 December 2021

336 billion

© 2022. For information, contact Deloitte China. 39In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

FINI platform accessible by market

issuers, including secondary listing and dual

participants to handle subscription,

primary listings

pricing, allotment, payment, listing

approval and stock admission Hong

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The MB listing requirements have been increased to

The regulators identified a list of features HKD80 million for the three-year track record period to

that may prompt them to make further align better with the market capitalization requirements

inquiries regarding a new listing. raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on CG and ESG and expected

is heavy on investors protection measures

practice.

© 2022. For information, contact Deloitte China. 40Uplifted MB Profit Requirements for Listing

Effective on 1 January 2022

1. Profits test

Profits in the last 3 financial years >HKD80 million

Preceding 2 years' aggregate profits >HKD45 million

Most recent year's net profit >HKD35 million

Market capitalization at time of listing >HKD500 million

2. Market capitalization/revenue test

Market capitalization at time of listing >HKD4 billion

Main Board Most recent audited financial year's revenue >HKD500 million

3. Market capitalization/revenue/cash flow test

Market capitalization at time of listing >HKD2 billion

Most recent audited financial year's revenue >HKD500 million

Preceding 3 financial years’ aggregated positive cash flow from operating activities >HKD100 million

Increase in minimum public float value at the time of listing increased to HKD125 million.

Main Board new applicants must meet one of the three financial criteria above.

HK’s Listing

Framework

Aggregated positive cash flow from operating activities for the 2 years prior to listing >HKD30 million

Market capitalization at time of listing >HKD150 million

Substantially the same management for 2 years

The removal of the streamlined process for GEM transfers to the Main Board (including that a sponsor

GEM must be appointed at least two months before the submission of a listing application)

Increase in minimum public float at time of listing to HKD45 million

A mandatory public offering requirement (at least 10% of total offer size) for all GEM IPOs

An extension of the post-IPO lock-up requirement on controlling shareholders to 2 years

© 2022. For information, contact Deloitte China 41In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

FINI platform accessible by market

issuers, including secondary listing and dual

participants to handle subscription,

primary listings

pricing, allotment, payment, listing

approval and stock admission Hong

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The MB listing requirements have been increased to

The regulators identified a list of features HKD80 million for the three-year track record period to

that may prompt them to make further align better with the market capitalization requirements

inquiries regarding a new listing. raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on CG and ESG and expected

is heavy on investors protection measures

practice.

© 2022. For information, contact Deloitte China. 42SFC and HKEX Joint Statement on New Listing

Features of problematic IPOs which may lead to enquiries by regulators

Small market capitalisation Unusual underwriting

The applicant’s market capitalisation barely

meets the minimum threshold under the

commission

Unusually high underwriting or

Listing Rules#.

placing commissions or other listing

expenses##.

Highly concentrated

Very high P/E ratio shareholding

Very high price to earnings (P/E) ratio Shareholding is highly concentrated in a

taking into account the applicant’s limited number of shareholders,

fundamentals (including its profit particularly where the value of the

forecast) and the valuation s of its peers. public float is small and the spread of

shareholders barely meets the minimum

thresholds set out in the Listing Rules.

# This is also a characteristic of shell companies identified in the “Guidance on IPO Vetting and Suitability for Listing” (HKEX-GL68-13A) (i) small market capitalization

## This is also a characteristic of shell companies identified in the “Guidance on IPO Vetting and Suitability for Listing” (HKEX-GL68-13A) (iii) involve fund raising disproportionate to listing expenses (i.e. a high

proportion of the listing proceeds were used to pay listing expenses)

Source: Joint statement on IPO related misconduct by Securities and Futures Commission and HKEX on 20 May 2021.

© 2022. For information, contact Deloitte China. 43In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

FINI platform accessible by market

issuers, including secondary listing and dual

participants to handle subscription,

primary listings

pricing, allotment, payment, listing

approval and stock admission Hong

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The MB listing requirements have been increased to

The regulators identified a list of features HKD80 million for the three-year track record period to

that may prompt them to make further align better with the market capitalization requirements

inquiries regarding a new listing. raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on CG and ESG and expected

is heavy on investors protection measures

practice.

© 2022. For information, contact Deloitte China. 44SPAC Listing Regime

SPAC IPO volume and proceeds in the US in 2021 are still well above previous years’ levels

(Number of IPOs)

SPAC IPO volume SPAC IPO proceeds

(USD million)

700 180,000

600 613 160,000 162,394

140,000

500

120,000

400

100,000

248 83,379

300 80,000

200 60,000

40,000 13,608

100 46 59 10,752

34 20,000 10,049

7 15 9 12 20 13

0

1 10 36 503 1,082 491 1,455 1,750 3,902 3,499

0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

• Supported by active capital markets and the Fed's continued monetary easing, SPAC transactions set high in 2021

More certainty than traditional

Less time to list Low listing costs

IPOs

Source: SPACInsider, as of 3 January 2022; includes additional proceeds from exercise of over-allotment options.

© 2022. For information, contact Deloitte China. 45SPAC Listing Regime

The SPAC listing regime will encourage more listings of tech and innovative companies in HK

Establishment of a De-SPAC target Listing of successor

Listing of a SPAC Shareholder vote Close of acquisition

SPAC search company

A de-SPAC target must Must meet all the new

value at least 80% of the listing requirements of

Must raise at least Requires a In case a SPAC is

SPAC IPO proceeds Main Board

HKD1 billion majority of unable to announce a

Investment companies

Apply the cannot be eligible to SPAC’s de-SPAC transaction The IPO sponsor must

Takeover Code to become de-SPAC targets shareholders within 24 months, or be a corporation or

a SPAC during its Have at least one at a general complete one within authorized financial

listing independent PIPE investor meeting, 36 months, it must be institution, licensed or

as an asset management where SPAC liquidated and must registered under the

A SPAC’s board must promoters and return all the funds it

firm to manage assets of at SFC Ordinance for

have at least two their close raised to its

least HKD1 billion or funds Type 6 regulated

Type 6 or Type 9 associates shareholders. The

of at least HKD1 billion activities, i.e. advising

SFC-licensed must abstain SPAC will then be

Require a valuation on corporate finance

individuals. That delisted

validation of the target by

includes one Independent PIPE

independent third parties,

director investment has been

such as outside PIPE

representing the strengthened for a

investors

licensed SPAC stronger regulatory

promoter Require an independent

financial advisor determine check on the terms and

the independence of a PIPE valuation of the de-SPAC

investor in a de-SPAC transaction

transaction

Open to all

Only professional investors will be allowed to participate investors types

including retail

© 2022. For information, contact Deloitte China. 46SPAC Listing Regime

Lifecycle of SPAC in HK

≥ 75 professional Promoters

investors

2a. Fundraising Promoter shares

Public shares 1. Formation of a SPAC by a promoter

via an IPO (≤20%) and

(≥80%) and • The SPAC then issues promoter shares to

Issue price of at warrants

warrants the promoter at nominal consideration

least HKD10/ share (unlisted)

SPAC

2b. Deposit of IPO proceeds Escrow

into a ring-fenced escrow

account

PIPE 3. Acquisition of the target within 36 100% of the

Target months of SPAC IPO with possible

gross IPO

investors extension of up to 6 months

• The target must have a market value proceeds

4. Coordination of a SPAC promoter with the of at least 80% of the funds raised by

external PIPE investors to raise capital from the SPAC from its IPO

hedge funds, private equity firms, management

firms, and family offices to ensure sufficient

funds for the acquisition Successor 5. Completion of combining the SPAC business with

the target through merger, acquisition, reorganization,

© 2022. For information, contact Deloitte China. company or similar 47SPAC Listing Regime The first filing for SPAC listing in Hong Kong on 17 January 2022 © 2022. For information, contact Deloitte China. 48

In 2021, extensive reforms successively introduced in HK capital market creating a new landscape and

expanding the range of fundraising opportunities for businesses

1 T+2 IPO Settlement Plan 2 Listing Regime for Overseas Issuers

Relaxed listing requirements for overseas

FINI platform accessible by market

issuers, including secondary listing and dual

participants to handle subscription,

primary listings

pricing, allotment, payment, listing

approval and stock admission Hong

Kong

3 Uplifted MB Profit Requirements for

4 SFC and HKEX Joint Statement on Listing

New Listing The MB listing requirements have been increased to

The regulators identified a list of features HKD80 million for the three-year track record period to

that may prompt them to make further align better with the market capitalization requirements

inquiries regarding a new listing. raised in 2018.

Capital

Market

5 SPAC Listing Regime 6 IPO Applicants’ CG and ESG Practice

Disclosure

A regime tailored to the particular risks and

The Exchange has provided guidance on prospectus

requirements of the Hong Kong market and

disclosure requirements on CG and ESG and expected

is heavy on investors protection measures

practice.

© 2022. For information, contact Deloitte China. 49IPO Applicants’ CG and ESG Practice Disclosure

Corporate governance measures – Statement on compliance culture

Comprehensive disclosure on

how the issuer instils a strong corporate culture that fully adopts and prioritizes compliance and governance

measures of integrity

(w)e have compliance policies in place that clearly

Board’s attitude or commitment towards lawful,

1 define the company’s compliance requirements,

including business ethics, vendor access and the

ethical and responsible operation of the acceptance and provision of travel and entertainment

businesses. and gifts. We have also established an ethics

Measures to ensure such culture is embedded

2 committee under the oversight of the audit committee

to supervise matters related to FCPA compliance. Our

whistle blowing policy and the related reporting

in the organisation mechanism provide a confidential and protected

Measures to ensure such culture is

3 channel for reporting suspected compliance violations.

Regardless of position or location, we require all

[employees] to comply with our anti-corruption

embedded in the organisation compliance policies and attend related trainings to

embrace the highest standard on integrity.

Leading practice - An information technology company set up a dedicated committee to

oversee compliance matters and established compliance policies.

© 2022. For information, contact Deloitte China. 50IPO Applicants’ CG and ESG Practice Disclosure

Corporate governance measures – Board’s oversight and involvement and diversity

Board diversity policy

Systems and/ or mechanisms

in place to continually

evaluate the appropriateness

and effectiveness of the

board diversity policies

Gender diversity

Single gender board

applicants who have made a

commitment in the listing

document should appoint a

“Over-boarding” INEDs director of a different gender

in accordance with such

Tightened scrutiny of commitment.

the explanations and

replace over-boarding

INEDs A1 submission filed on or

after 1 July 2022 with single

gender board will not be

accepted.

© 2022. For information, contact Deloitte China. 51IPO Applicants’ CG and ESG Practice Disclosure

ESG Disclosures – Climate-change related issues

1 Leading practice

Prospectus disclosure

Climate change-related issue oversight

Board’s overall responsibility and details of any

policy to address climate related issues

An Applicant addressed the climate-

related transition and physical risks by:

Climate-related risks and opportunities (i) identifying policy actions around

Actual and potential impact on business, strategy

and financial performance climate change that would ‘continue

to evolve … and pose varying levels of

Climate-related risks and opportunities financial and reputational risk’ to the

Identification and assessment over the short,

medium and long term, their impact, and steps Applicant; and

taken to mitigate such risks (ii) explaining measures implemented to

Climate-related risks

mitigate the potential impact of

Quantitative information on the metrics and climate change on the Applicant’s

targets used to assess and manage

‘premises, operations, supply chain,

transport needs, and employee safety.’

© 2022. For information, contact Deloitte China. 52Speaker enquiries

Edward Au

Managing Partner, Southern Region, Deloitte China

Tel: +852 2852 1266

Email: edwau@deloitte.com.hk

© 2022. For information, contact Deloitte China. 53HK SPAC Regime - overview 25 Jan 22 Information Classification: Confidential

What is a SPAC?

• Special Purpose Acquisition Companies or “SPAC”, are also known as a “blank check company”, is a company with no commercial operations that is formed to

raise funds through an IPO for the purpose of acquiring an existing private company within a set timeframe.

• The HKEX has published its consultation conclusion in December 2021 and the new SPAC regime under Chapter 18B is effective from 1 January 2022

© 2022. For information, contact Deloitte China. Presentation title 55Life Cycle of a HK SPAC

1 2 3 4 5

Formation IPO of SPAC Target search Approvals IPO of Target

• Promoter forms SPAC • SPAC submits listing • SPAC identifies suitable • Needs approval from • The successor

application to HKEX target both investors and company is listed on

• Promoter usually are HKEX before stock exchange

professional investors • SPAC issues • Target needs to meet all completion

with corporate finance shares/warrants to listing requirement and

experience professional investors has a value of at least • Submits listing

80% of the proceeds document for De-

• Promoter subscribes • Funds raised are kept raised (i.e. HK$800M) SPAC target for HKEX

for shares/warrants in in an escrow account approval similar

SPAC • Transaction needs to be requirement to RTO

• Minimum fund raised done within 3 years

is HK$1B

• HKEX may grant

extension of 6 months

© 2022. For information, contact Deloitte China. Presentation title 56Benefits to De-SPAC targets

1 Deal certainty at acceptable price

•

•

Price is negotiated with the promoter

No underwriters involvement or book building process

2 Expertise of promoter

• Promoter are experts in the sectors and may be able to provide more accurate

valuation of businesses

• Promoters may take up management role in the entity after De-SPAC

3 Dual track approach to listing

• Target company can concurrently apply for listing using traditional IPO and negotiate

with SPAC promoters at same time

© 2022. For information, contact Deloitte China. Presentation title 57Benefits to investors

1 Shareholder votes on De-SPAC

• Details of the De-SPAC transactions are presented to the shareholders for

approval at a general meeting

2 Redemption option

• Shareholders can elect to redeem its shares even if voting in favor of the De-SPAC

transaction

3 Mandatory PIPE investment

• Require third party investors to invest a minimum of 25% of value of the target if the

value is less than HK$2B

• A third party support on the valuation of the De-SPAC target

© 2022. For information, contact Deloitte China. Presentation title 58Speaker enquiries

Johnny Chu

Partner, Audit & Assurance, Deloitte China

Tel: +852 28526374

Email: johnchu@deloitte.com.hk

© 2022. For information, contact Deloitte China. Presentation title 59Questions and answers © 2022. For information, contact Deloitte China. 60

Latest update

“An essential guide to SPAC listings in Hong Kong”

Presented by Deloitte China’s Capital Market Services

Group, the guide is for companies that are considering a

special purpose acquisition company ("SPAC") listing, and

introduces the new listing regime for SPACs in Hong Kong,

its lifecycle and key features.

Access the brochure here, or scan below:

© 2022. For information, contact Deloitte China. 61Upcoming Event

March Alumnus x INED Workshop

Topic on Sino-US relations

Speaker: Xu Sitao

Chief Economist, Partner, Deloitte China

© 2022. For information, contact Deloitte China. 62© 2022. For information, contact Deloitte Advisory (Hong Kong) Limited. 63

Thank you!

Keep us updated on your enterprise status under pandemic

© 2022. For information, contact Deloitte China. 64About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more. Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our global network of member firms and related entities in more than 150 countries and territories (collectively, the “Deloitte organization”) serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 345,000 people make an impact that matters at www.deloitte.com. Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which are separate and independent legal entities, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Hanoi, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Osaka, Seoul, Shanghai, Singapore, Sydney, Taipei and Tokyo. The Deloitte brand entered the China market in 1917 with the opening of an office in Shanghai. Today, Deloitte China delivers a comprehensive range of audit & assurance, consulting, financial advisory, risk advisory and tax services to local, multinational and growth enterprise clients in China. Deloitte China has also made—and continues to make—substantial contributions to the development of China's accounting standards, taxation system and professional expertise. Deloitte China is a locally incorporated professional services organization, owned by its partners in China. To learn more about how Deloitte makes an Impact that Matters in China, please connect with our social media platforms at www2.deloitte.com\cn\en\social-media. This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities. © 2022. For information, contact Deloitte China.

You can also read