Alphatax UK Enterprise Release Notes - Version 21.1.1 - Tax Computer Systems

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Alphatax UK

Enterprise Release Notes

Version 21.1.1

Public

T: 01784 777 700 | E: enquiries@taxsystems.com | W: www.taxsystems.com

Contents

1. Introduction ............................................................................................................ 3

About version 21.1.1 .............................................................................................. 3

Technical support .................................................................................................. 3

2. Finance Act 2022 ..................................................................................................... 4

3. Returns and e-filing ................................................................................................. 5

Company tax return CT600 (2022) .......................................................................... 5

Partnership tax return SA800 (2022) ..................................................................... 12

Miscellaneous returns and e-filing changes ............................................................. 13

4. Interest restriction return API ................................................................................. 15

5. Miscellaneous changes ........................................................................................... 16

6. Optional modules .................................................................................................. 16

Accounts analysis ................................................................................................ 16

Tax accounting .................................................................................................... 16

7. Templates ............................................................................................................ 17

Public

21. Introduction

About version 21.1.1

Welcome to the version 21.1.1 patch edition of Alphatax UK. This release includes the following

features:

Table file changes following Finance Act 2022

Support for the CT600 2022 and associated e-filing schema

Updates for the latest versions of forms SA700 and SA800

Further amendments in relation to the introduction of the Interest restriction return API

Minor changes to resolve customer issues

Technical support

We provide a technical support help desk for users requiring assistance. The help desk can be

contacted by telephone between the hours of 9.00 am and 5.30 pm, Monday to Friday

excluding public holidays.

If you require help or further information, please contact the support team on:

UK: Tel: +44(0) 1784 777 666 Email: support@taxsystems.com

Ireland: Tel: +353 (0) 1661 9976 Email: support@taxsystems.ie

Please note: We recommend that you use the E-mail Support option from the Help menu in

Alphatax to send copies of the computation directly to Support.

Public

32. Finance Act 2022

We have made the following amendments to the table file held in Alphatax for this release. The

more involved tax rules changes required in response to Finance Act will be included in the

following V22.0 release.

The temporary increase in the rate of the annual investment allowance to £1 million had

been due to end on 31 December 2021 but Finance Act 2022 has extended this to 31

March 2023.

Legislatively, this change has been made by amending Finance Act 2019 where the

provisions for the temporary increase are held. S51A CAA 2001 itself – which provides for

the annual investment allowance – is unchanged.

Note that the FA 2022 legislation does not specify any different date for income tax rules.

Museums and galleries exhibition tax relief had been due to be withdrawn on 31 March

2022, but this relief has been made available for a further two years to 31 March 2024.

This sunset date is held within the definition of “qualifying expenditure” in s1218ZCG CTA

2009.

As a revenue raising measure, Finance Act 2022 has increased the rate of income tax

applicable to dividend income by 1.25% – from 32.5% to 33.75% – from 6 April 2022.

This rate is shared by the corporation tax rules of CTA 2010 Part 10 Chapter 3 which

apply a charge on loans made to participators of close companies, with s455 referring to

ITA 2007 s8(2).

For accounting periods straddling this date, Alphatax provides a Date of loan input in

the accessory statement of the Loans to participators statement to allow the correct rate

to be applied to any loans made.

Public

43. Returns and e-filing

Company tax return CT600 (2022)

HMRC have issued new versions of the forms CT600, CT600B and CT600L for 2022 which have

been included in this edition of Alphatax. These forms all act as direct replacements for the

preceding version and are used for accounting periods starting on or after 1 April 2015. In

addition, a new supplementary form CT600M has also been introduced in relation to freeport

capital allowances.

The changes to these forms are described below.

Exporter information

A new information question During the return period, did the company export goods

and/or services to individuals, enterprises or organisations outside the United

Kingdom (UK)? has been added to page 7 of the form. Tick boxes are provided for answers:

Goods; Services; or Neither.

A corresponding drop down input has been added to the Return details input statement.

Note however that the e-filing schema does not consider this box to be mandatory and we

have confirmed with HMRC that it may be left blank, which accordingly is the default applied

by Alphatax.

Information about capital allowances and balancing charges

Page 8 of the form CT600 2022 includes new boxes for trade or non-trade allowances or

charges in respect of:

Machinery and plant – super deduction, and

Machinery and plant – special rate allowance.

Corresponding fields have also been added in the Qualifying expenditure section on page 8.

Super deduction and Special rate allowances would previously have populated the Main pool

and Special rate pool allowance boxes on the form. Alphatax will now automatically populate

the new boxes as appropriate.

Public

5Losses, deficits, and excess amounts

The Company Tax Return guide 2022 has clarified that amounts entered in the Losses,

deficits and excess amounts arising boxes on page 9 of the form should include current

period amounts only and not any amounts brought forward from previous periods. In the case

of Management expenses and Non-trading losses on intangible fixed assets, in earlier editions

Alphatax included brought forward amounts which was in line with guidance we had previously

received from HMRC.

We have now applied the relevant changes needed to reflect the updated company tax return

guide. Boxes 830 and 850 will now return current period amounts arising only. These changes

will be applied by Alphatax for periods of account ending on or after 31 March 2020, with the

intention of covering all live submissions going forwards without unnecessarily affecting older,

settled returns.

CT600B

The supplementary form CT600B has been extended for 2022 to include a new page 3 for

Hybrids and other mismatches. The boxes present a series of indicators for certain aspects

of how the hybrids rules having impacted the computation period, followed by numerical

amounts relating to certain hybrid adjustments that may have been brought into account:

Public

6For this release we have made the following changes to our existing Hybrid and other

mismatches statement to support population of this form:

The input statement has been moved to appear within the CT600 supplementary forms

section of the contents tree and may now be enabled in computations via a new flag on

the Supplementary form summary input statement.

A new Additional CT600B analysis section is presented on the input statement with

fields that can be used to tick boxes B40 and B45 on the return. Boxes B50 to B75 will all

be derived automatically by Alphatax from existing entries on the statement.

We have added a new Surplus dual inclusion income allocation sub-statement which

allows for the allocation of any dual inclusion income surplus between group companies.

The relevant legislation here was inserted as a new Chapter 12A within Part 6A TIOPA

2010 by Finance Act 2021, and entries made for any surplus allocated to or from the

company will feed boxes B80 and B85 respectively.

CT600L

The research and development-related supplementary form CT600L has been amended for

2022 to include new sections of boxes for the following amounts:

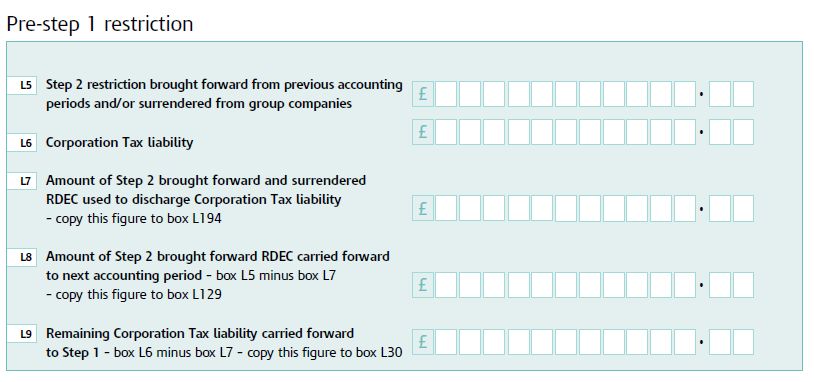

Pre-step 1 restriction

A new section has been added to the form to now reflect the correct legislative treatment of

Step 2 restriction amounts brought forward which, under CTA 2009 s104O(5), are offset

against the corporation tax liability of the following period in priority to any set off amount of

the later period.

The new boxes present the amount of any Step 2 restriction brought forward – including

amounts claimed from a group company under s104O(3) – and the offset against the

corporation tax liability for the period as taken from box 475. Any remaining Step 2 restriction

carries forward in box L65, whilst any remaining corporation tax liability feeds into the Step 1

offset of current period set-off amounts.

Alphatax will automatically populate these new fields from existing entries in the computation.

Public

7Note that in previous editions, as part of application controls to not change older periods, we

had included a flag Apply changes to the order of RDEC credit offset against CT liability

made in e-filing taxonomy applicable from 1 April 2022? on the Submission options

input statement. This flag may now need to be removed if it had been used before to allow a

re-submission.

Step 7 – Amounts extinguished by s104S

A new box L123 has been added within the Step 7 section for Amounts extinguished by s104S (2)(b)

CTA 2009. This section of the legislation extinguishes any entitlement to a payable R&D expenditure

credit under Step 7 where a company is not a going concern at the time of the claim.

We have re-introduced our associated input on the Research and development expenditure credits

(CT600L) input statement.

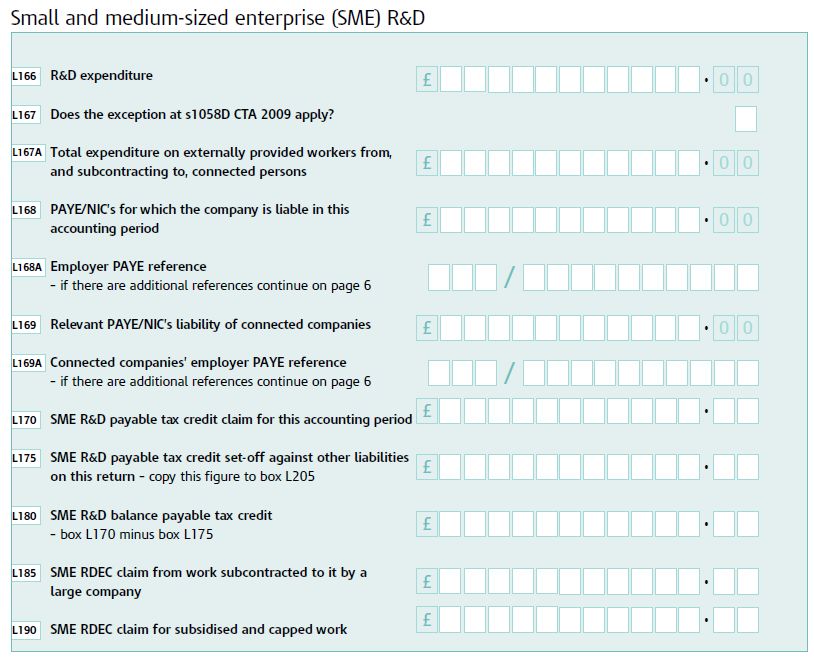

Small and medium-sized enterprise (SME) R&D

The existing SME section of the form has been considerably extended to capture additional

information relating to any claim. The amount of R&D expenditure is now included, along with

details of the tax credit calculation. As part of this, an amount for PAYE and NIC liabilities and

an employer PAYE reference number for the company are now required entries.

For this edition, we have now added a new Research and development SMEs (CT600L) input

statement to draw together the entries that will be populated in these boxes, including

highlighting where inputs should be made in existing inputs elsewhere in the computation. The

main example of this is the PAYE and NIC liabilities for payment periods ending in

accounting period input which has always been located on the Income tax summary input

statement.

Note that the SME area of the form continues to only be relevant where a tax credit is being

claimed in the computation, and not for the 130% enhanced deduction, in accordance with the

Company Tax Return guide.

Public

8CT600L e-filing issues

HMRC have introduced a new XML e-filing schema V1.97 to reflect the 2022 updates to the

CT600, and this includes additional validation rules relating to the CT600L. These rules resolve

certain issues from the previous schema but have introduced new ones. We have been in

discussions with HMRC on these issues, and they have acknowledged some (but not all) of

them on their Changes and issues affecting the Corporation Tax online service page.

The following issues with the population of the CT600L remain unresolved at the time of this

release. Note that in every case we have kept the existing, correct presentation in the

computation unchanged.

Pre-step 1 restriction

• Validation rule 9631: For periods beginning before 1 April 2022, the HMRC schema does

not allow box L65 to be populated for current period Step 2 amounts arising (box L55)

unless there is also an existing brought forward amount present (based on box L9). This

issue then affects box L70 onwards, and ultimately the claim in box 880. We have

reviewed this and determined that there is no way that we can populate the form in this

case that does not break the amount of the claim in both the computation and the tax

return form. We have made HMRC aware of this issue and await a resolution. In the

meantime, customers may need to discuss paper filing with HMRC (this is not a scenario

they have listed on their issues page).

Public

9• Computations with only a Step 2 brought forward amount being offset against

corporation tax (with no current period R&D claims) are not able to complete the relevant

Pre-step 1 restriction section on the form CT600L. This is because validation rule 9710

requires that one of either the Step 1 or SME sections must be included (and various

other validation rules within those sections mean that we cannot print zero entries to get

past this). To enable e-filing to succeed, we have removed the amount offset from box

530 in such a scenario, and the CT600L will not be printed.

• For computations with a Step 2 brought forward amount which exceeds corporation tax

of the period, the remaining amount to carry forward in box L8 feeds into the RDEC

carried forward section of the form in box L129. Validation rule 9775 however, via box

L140, requires this amount to be double counted for the purposes of box L150. To allow

e-filing to pass, Alphatax will follow the validation rules and apply this double counting.

However, HMRC have advised that they intend to resolve this issue in the future and so

we have also added a flag Remove double counting of box L129 value in box L150

on CT600L on the Submission options input statement (we will remove the need for this

flag in a future release once HMRC have addressed the issue).

Income tax deductions

• Validation rule 9630: This rule requires that box L62 is the positive-only difference

between boxes L15 and L30. In our view though, this does not correctly consider income

tax being offset against the corporation tax liability within the Step 1 calculation in box

L35. Alphatax will populate this box in line with the required validation rules.

• Validation rule 9631: This error can also arise where income tax suffered is being offset

against corporation tax of the period, and Step 2 restriction brought forward is present.

The new Pre-step 1 restriction section does not account for the income tax deduction in

the way that the Step 1 section does. HMRC have advised that they intend to amend

their validation rule to cater for this scenario and recommend waiting to file affected

returns.

Note that where there are Step 2 brought forward amounts present, this error code will

not appear, but the offset of Step 2 amounts brought forward against corporation tax will

still be presented incorrectly on the CT600L and in box 530.

Small and medium-sized enterprise (SME) R&D

• Computations for accounting periods beginning on or after 1 April 2022 claiming an

enhanced expenditure deduction, but not a tax credit, cannot complete the form CT600L,

or accordingly box 660 of the CT600. This is because of the combination of validation

rules 9604 – which states that box 660 may only be completed where box L166 is

completed – and 9780 – which states that L166 may only be completed where you are

claiming a tax credit in box L170 or SME RDEC in boxes L185 and L190. We have advised

HMRC of this issue and the have said they will be removing validation error 9604 (and

the related 9605) in a future update.

• Validation error 9635: We believe that box L168 - PAYE/NIC’s for which the

company is liable in this accounting period - is intended for the purposes of applying

the cap on payable SME R&D tax credits under s1058 CTA 2009, however validation rule

9635 also makes this a required entry where an SME RDEC claim is being made for

subcontracted or subsidised work in boxes L185 or L190.

• Validation error 9635: Similarly, the PAYE/NIC entry is also required for periods of

account beginning before 1 April 2022, even though the legislative cap does not apply.

HMRC have advised that they will be adding an application control to this rule in a future

update.

Public

10• Validation error 9638: Companies claiming SME RDEC for subcontracted or subsidised

work in boxes L185 or L190 cannot complete the CT600L for periods beginning on or

after 1 April 2021. This is because validation error 9638 requires that box L166 is

completed where the SME section of the form is used. We have advised HMRC and await

their response.

CT600M

HMRC have introduced a new supplementary form CT600M in relation to freeport capital

allowance qualifying expenditure. The form presents two tables to capture details of the

freeport rules in relation to structures and buildings allowances or 100% first year allowances.

These allowances were recently introduced by Schedule 21 of Finance Act 2021.

Enhanced structures and buildings allowances in Freeports

Freeport qualifying expenditure benefits from a higher structures and buildings allowance rate

of 10% under CAA 2001 s270(2A)(a). Page 2 of the CT600M must now be completed for each

building or structure for which a claim is being made.

Our V21.0 edition introduced a new Freeport qualifying expenditure? to the accessory

statement of the Structures and buildings allowances statement to allow this rate to be

claimed.

Alphatax will now complete the details of the Total amount of qualifying expenditure and

Total Structures and Building Allowance (SBA) claim amount on the CT600M for each

item of expenditure based on the existing fields.

Note that the Company Tax Return guide and rubric on the form indicate that the allowance

box should be populated for each period in which an allowance is being claimed. However,

HMRC’s e-filing validation rule 9654 does not allow for this. We have raised this with HMRC,

and they have advised that they will be removing this rule in the future, but for this release

Alphatax will only populate these boxes in the period in which the building if first brought into

qualifying use (refer to box 771).

For this edition, we have introduced further accessory statement inputs to allow the Address

of business operation to be completed. We have also amended the narrative for the existing

Name of freeport field, which was previously used for XBRL tagging only but is now also

returned on the CT600M (with the name converted to an index number as listed in the

Company Tax Return guide).

In addition, we have reversed a change that we had made in the previous edition which meant

that the Date of first non-residential use field was not needed where the Date of

qualifying expenditure was completed instead. As was the case previously, the Date of first

non-residential use will now be a required entry for allowances to be claimed, in line with

the wording of s270(2A) and as captured on the form CT600M.

Enhanced capital allowance (ECA) for plant machinery in Freeports

Expenditure on plant and machinery for use primarily in a freeport tax site qualifies for a 100%

first year allowance under CAA 2001 s45O. Page 3 of the CT600M must now be completed for

each item of expenditure for which a claim is being made.

Our V21.0 edition introduced a new Expenditure on which FYAs at 100% are claimed

(freeport tax sites) input on the trade Plant and machinery main pool input statement to

allow for this allowance to be claimed.

Public

11For this edition, we have now introduced a new Summary of freeport assets sub-analysis

statement, nested under the Plant and machinery main pool input statement, which requires

users to reconcile any freeport 100% FYA claimed to items of expenditure for the purposes of

the CT600M.

The form captures details of the freeport location (as an index), the address, the FYA claimed,

and any disposal value. There is also a tick box to state whether an Enterprise Zone claim has

been made.

Non-resident company tax return SA700 (2022)

This edition of Alphatax includes the recently released form SA700 (2022) – Tax return for a

non-resident company or other entity liable to Income Tax.

There are no changes to the boxes on this year’s edition of the form.

Miscellaneous non-resident company tax return changes

We have resolved an issue with a carried forward calculation which stopped transitional

rules being applied correctly in some circumstances for the period after a non-resident

company had transitioned to corporation tax rules from 5 April 2020.

The For companies with no rental income, additional information field had been

removed from the Additional information input statement in a previous edition, reflecting

property income being removed from the form for 2020-21 onwards. This input was

being hidden where it already contained a value however, so we have now resolved this

issue to allow users to remove any existing entry.

Partnership tax return SA800 (2022)

This edition of Alphatax include the recently released form SA800 (2022) – Partnership Tax

Return and all supplementary pages. The associated e-filing schema is also included.

The changes to this year’s edition of the form are:

A new information question During the return period did the partnership export

goods and or services to individuals, enterprises or other organisations outside

the UK? has been added to page 2 of the form. Tick boxes are provided for answers:

Goods; Services; or Neither. A corresponding drop down input has been added to the

Return details input statement. Note however that the e-filing schema does not consider

this box to be mandatory and we have confirmed with HMRC that it may be left blank,

which accordingly is the default applied by Alphatax.

New boxes have been added in the capital allowances summary for Zero-emission car

allowance across the main pages and all supplementary forms (UK property, foreign,

and extra trading), and for Freeport Structures and Buildings Allowance on the

trading and UK property pages. Alphatax already provided inputs for these allowances to

be claimed in the computation and will now feed these amounts into the relevant boxes

on the return.

The tick box for declaring disguised remuneration income (also referred to as the

loan charge) has been removed from this year’s edition of the form, reflecting the fact

that – aimed at loans outstanding on 5 April 2019 – this was a temporary settlement

scheme. The corresponding input has been removed from the trade Accounts

adjustments input statement in Alphatax.

Public

12 Similarly, tick boxes for declaring that capital allowance claims include enhanced

capital allowances for designated environmentally beneficial plant and

machinery have been removed from the form. Enhanced capital allowances were

previously available under Schedule A1 CAA 2001 which was abolished by FA 2019 in

relation to expenditure incurred on or after 1 April 2020.

Miscellaneous partnership tax return changes

The 2020-21 edition of the SA800 introduced a declaration box for the nominated partner to

confirm that any coronavirus support scheme payments received have been included as

taxable income.

To draw attention to this new field, we included a diagnostic test to confirm that users had

entered either Yes or No for this question. HMRC guidance subsequently confirmed that this

box did not need to be considered where the partnership had not received any such payments.

We have accordingly now removed the diagnostic test and removed No as a possible entry for

the input provided by Alphatax. Users will not be able to leave this entry as blank where it is

not relevant for their partnership.

Miscellaneous returns and e-filing changes

The 2021 detailed profit and loss account taxonomy introduced three new ‘sub-tags’,

which sat below existing tags in the structure of the taxonomy: Revenue from off

payroll working which is a sub-tag of Turnover/revenue; and Coronavirus Job

Retention Scheme income and Other Coronavirus grants which are sub-tags of

Government grant income.

As the tags defined in the taxonomy do not provide a complete reconciliation for the

corresponding parent, and to retain compatibility with older Alphatax periods or any links

or templates that may be in use, we added the corresponding new inputs as standalone

fields meaning that any amounts entered need to also be included within the

corresponding parent tag as well. In this release we have now added an additional

narrative to clarify this:

Public

13When populated correctly, the input statement will appear to not cast. In report mode

however, these sub-tags are separated out and returned outside of the main profit and

loss account.

We have resolved a rounding issue in the calculation of the 50% SR allowance which was

leading to an Inconsistent duplicate facts error when e-filing in some scenarios.

HMRC’s XBRL schema allows for a maximum of 40 iterations of the same item tag, which

leads to filing failures for computations where a large number of footnotes have been

entered. We have now added an error message that will appear during assembly to warn

users of this issue. Users are able to control which footnotes are tagged via the existing

Footnote XBRL tagging dialog which also appears during assembly.

Further to a change in the previous release, we have included an additional fix to resolve

an e-filing failure related to the UKResidentDefault dimension being applied to the

AdjustmentsExemptDividendsOrDistributionsPerAccounts tag. This tag is included on the

trade Accounts adjustments report statement where exempt ABGH dividends have been

entered. This dimension relates to property business items only but was incorrectly

appearing for trades in some circumstances.

We have further resolved a more general issue, also introduced as part of this previous

fix, which in some limited cases would cause dimensions from different hypercubes to be

applied to a tag, which would lead to an e-filing failure.

Public

144. Interest restriction return API

In July 2021, HMRC made available a new API that can be used to submit interest restriction

returns, as well as nominated company appointments and revocations, electronically via tax

software. At the time, it was proposed that this would become the mandatory submission

mechanism for returns submitted from April 2022 onwards. HMRC modified their position in the

March 2022 agent update however. The proposal is now that electronic submission of these

returns is to be made mandatory from September 2022, but this will involve a choice of two

routes: using either the API from tax software, or the existing 'G-form' provided online by HMRC.

From September 2022 though, HMRC will no longer accept returns that are sent by email, post

or attached to company tax returns.

In Alphatax, we included full support for this API submission mechanism in our Group module in

the preceding V21.1 release. We default to assuming that the API will be used, and this enables

a small number of additional inputs or report statement disclosure changes, in line with HMRC’s

API schema. A flag Disable API disclosure on the Interest restriction return? flag is

provided on the Group configuration options input statement that allows users to revert to the

previous disclosure where the G-form route is being used for submission.

The switch to API disclosure was applied in Alphatax for group periods of account ending on or

after 1 April 2021 in line with the timeline originally announced by HMRC. To not change existing

computations, we have left this application date as it was. However, in this release, we have

made the following changes to reflect the latest proposals:

The Disable API disclosure on the Interest restriction return? flag was previously

designed to be hidden after April 2022 on the basis that the API route was to become

mandatory, but we have now amended the display rule so that this flag will be available

indefinitely going forward, reflecting the continued availability of the g-form as an

alternative route for submission.

The HMRC API schema closely follows the legislative requirements of TIOPA 2010 Sch 7A

para 20, but there are certain notable deviations. The Alphatax reports have been

designed to accurately reflect this schema to provide clarity over the contents of the

return. Accordingly, we have now added a heading “API facsimile” to the report

statements produced by Alphatax where this filing approach is in use, reflecting the fact

that these statements should not be submitted as an IRR under the g-form route. We

have also added an FAQ to the Interest restriction return Help page which explains some

of these differences in more detail.

Similarly, for all group periods, the Interest restriction return statement is now titled

Interest restriction summary initially, until the Interest restriction return ready for

submission? flag has been set to Yes.

Miscellaneous corporate interest restriction changes

We have resolved a display rule issue, created by the API disclosure changes introduced

in the previous release, which caused the statement Worldwide group is not subject

to interest restrictions in the return period to not display for abbreviated returns.

We have resolved an issue whereby the View – Submissions menu was not available for

Enterprise users who had not submitted the API interest restriction return themselves.

Public

155. Miscellaneous changes

Following changes by the Bank of England to their base rate, there have been three

changes in recent months to the HMRC interest rates for late payment and repayment of

corporation tax. This edition of Alphatax includes these latest rates affecting the Interest

on tax payments report statement, which is produced by Alphatax where the Date for

interest calculations field is populated on the Corporation tax payments input

statement.

For the previous edition, as part of changes introduced to correct the tax treatment of

SME R&D tax credits, we replaced the various RDEC flags on the accessory statement for

Corporation tax payments with a single drop-down input. An error with the display rules

though meant that certain categories were not displaying in some circumstances, the

main example being for investment companies claiming RDEC credits from group

members. We have now resolved this issue.

6. Optional modules

Accounts analysis

• A new Right of use assets per accounts statement had been introduced in the previous

release to allow separate disclosure of leases following changes introduced by IFRS 16.

This change was previously only available for computations applying IFRS but has now

also been enabled for companies applying FRS 101.

• We have introduced new diagnostics where the Enable reordering of accounts

analysis brought forward balances? option has been set in the Accounts analysis

options statement and the reordered brought forward balances entered do not equal the

amounts brought forward from the previous period.

Tax accounting

We have resolved a recently introduced issue which stopped users from being able to enter

negative amounts in certain brought forward input cells, primarily on the Tax account

summary input statement.

Public

167. Templates

Capital allowance updates

We have resolved a minor presentation issue on certain templates whereby recently introduced

columns for super-deduction capital allowances were incorrectly using the display rule dates

that apply to the also recently introduced freeport structures and buildings allowances for the

underline and currency column headings.

The following statement templates have now been corrected:

1. Assets – Fixed asset trading additions.tut

2. Assets – Additions with pre-trading capital expenses.tut

3. Division – Fixed asset trade additions.tut

Public

17Alphatax® software may not be copied, photocopied, reproduced,

translated, or reduced to any electronic medium or machine-readable

form, in whole or in part, without the express written permission of:

Tax Computer Systems Limited

Magna House, 18 – 32 London Road,

Staines-Upon-Thames, TW18 4BP

T: 01784 777 700

E: enquiries@taxsystems.com

W: www.taxsystems.com

Registered Office:

Magna House, 18-32 London Road, Staines-Upon-Thames, TW18 4BP

Registered in England & Wales number 05347048

Copyright © 2022 Tax Computer Systems Limited

Public

18You can also read