ADOPTED BUDGET - City of Owosso

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021-22 ADOPTED

BUDGET

City Council

Christopher T. Eveleth, Mayor

Susan J. Osika, Mayor Pro-Tern

Janae Fear

Jerry Haber

Daniel Law

Nicholas Pidek

Robert J. Teich, Jr.

June 7, 2021 City Council Meeting

TABLE OF CONTENTS-FY2021-22 ADOPTED BUDGET

Page No.

Click on highlighted

text to view

General Appropriation Act

Executive Summary

Organizational Chart............................................................................1

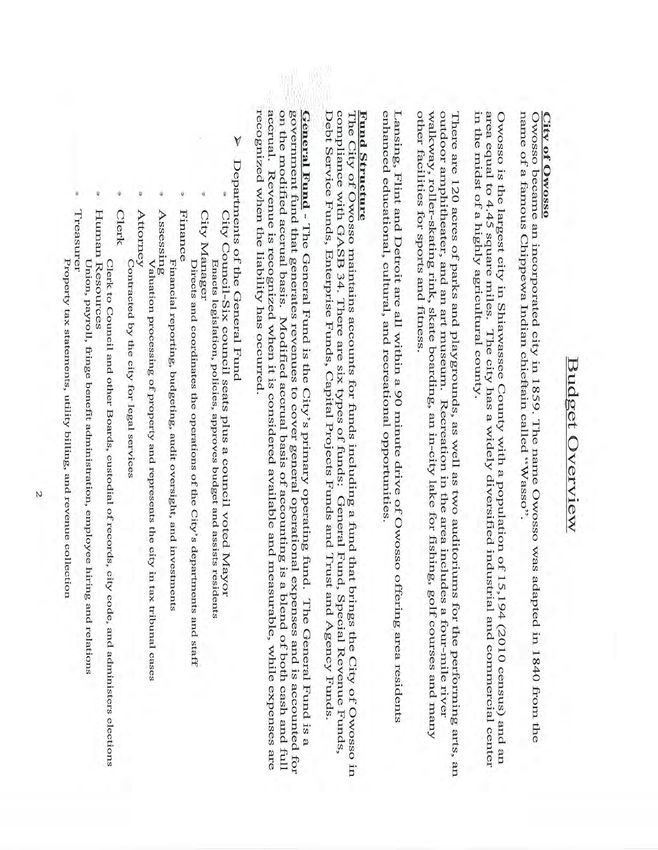

Budget Overview................................................................................2

Working Capital Schedule.................................................................... .5

Property Tax Illustration (FY2020-21) .......................................................6

General Fund Overview

Financial Summary..............................................................................7

General Fund Revenue..........................................................................8

General Fund Appropriations ...................................................................9

Other Governmental Funds

Special Revenue Funds.........................................................................10

Capital Improvement Funds....................................................................11

Special Revenue and Capital Improvement Funds Revenue..............................12

Special Revenue and Capital Improvement Funds Expenditures......................... 13

Debt Service Fund...............................................................................14

Enterprise Funds

Transportation and Utility Funds..............................................................16

Internal Service (Fleet) Fund.................................................................. 18

Component Units

Brownfield Authority...........................................................................19

Downtown Development Authority

Appendix

Detail by Fund.and Account-All budgets ..................................................20

2021-22 City Budget Adoption

City Manager Henne started the conversation saying he would like to have $30,000 added to

expenditures for the purpose of conducting a rate study. The cost would be split between the water,

waste water, and sewer enterprise funds.

Mayor Eveleth noted that he was still interested in adding some expenses to the budget for the castle for

power washing and repair of the outside lights. He said the castle is the City's brand and should be

looking as good as possible.

Councilmember Pidek indicated he had talked with the City Manager about a cybersecurity assessment

and would like to see $10,000 added to expenditures for said assessment.

Mayor Pro-Tern Osika asked for a report on the cybersecurity measures the City is currently taking. It

was noted that such a report exists but would not be publically distributed for security reasons.

City Manager Henne noted that the City's network engineer is working on getting an estimate for the

assessment now, but warned Council that he expected the cost to be more than $10,000.

It was asked how the assessment would be paid for. City Manager Henne said the money would come

from reserves with the cost spread out across multiple accounts.

City Manager Henne went on to note that estimates are being sought to replace the footlights at the

castle. He further noted that the expenses discussed this evening may be able to be absorbed by the

small surplus in the OHC budget, negating the need to change the budget before approval

Motion by Councilmember Pidek to adopt the General Appropriations Resolution approving the 2021-

2022 City Budget, with $30,000 added to expenditures for the purpose of conducting a water/sewer rate

study (with funding to come from enterprise funds) and $10,000 added to expenditures for a cybersecurity

assessment (with funding to come from reserves) as detailed below:

RESOLUTION NO. 97-2021

GENERAL APPROPRIATIONS ACT (BUDGET)

A resolution to establish a general appropriations act for the City of Owosso; to define the powers and

duties of the city officers in relation to the administration of the budget; and to provide remedies for refusal

or neglect to comply with the requirements of this resolution.

WHEREAS, pursuant to Chapter 8, Section 5 of the Owosso City Charter, the City Council has received

the proposed budget for the fiscal year beginning July 1, 2021 and held a public hearing on May 17,

2021, and;

WHEREAS, the City Council has held other sessions to discuss the proposed budget;

NOW, THEREFORE, BE IT FURTHER RESOLVED THAT the City Council of the City of Owosso hereby

adopts the FY2021-22 budget and sets the tax rates as shown below.

Section 1: Title

This resolution shall be known as the Owosso General Appropriations Act.

Section 2: Chief Administrative Officer

The City Manager shall be the Chief Administrative Officer and shall perform the duties of the Chief

Administrative Officer enumerated in this act.

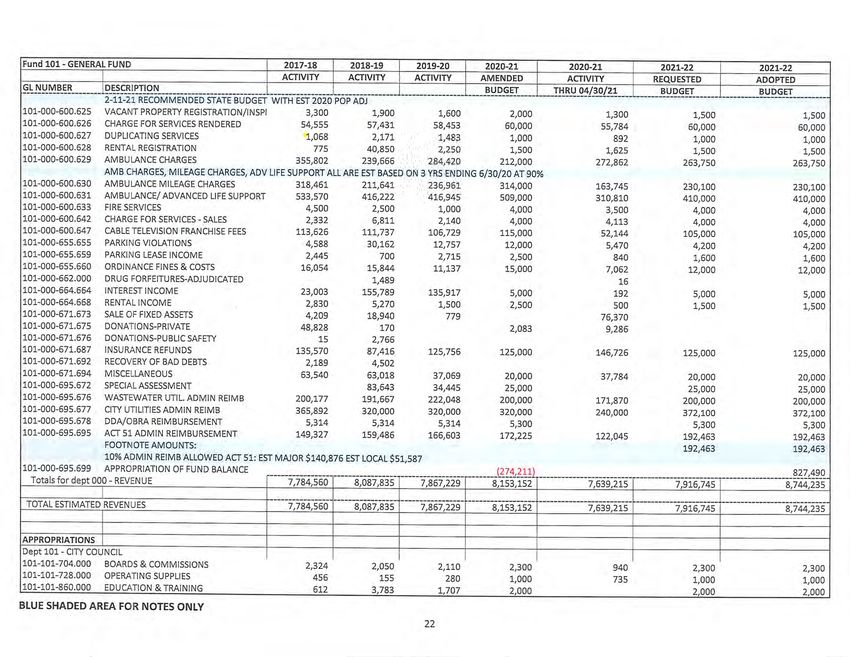

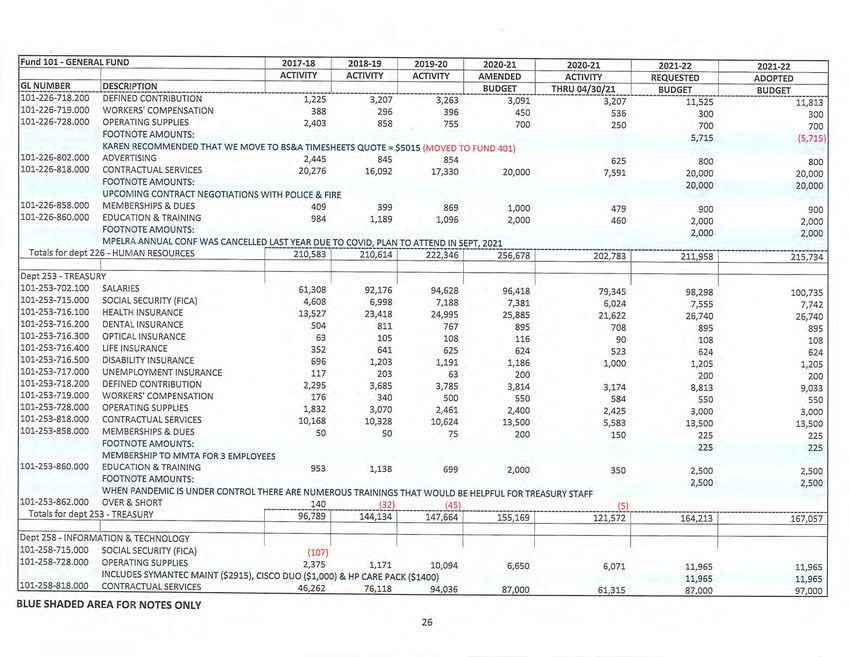

Section 3: Fiscal Officer The Finance Director shall be the Fiscal Officer and shall perform the duties of the Fiscal Officer enumerated in this act. Section 4: Estimated Expenditures The following amounts are hereby appropriated for the operations of the City Government and its activities for the fiscal year beginning July 1, 2021 and ending June 30, 2022: General Fund City Council $ 5,300 City Manager 262,583 City Attorney 118,000 Finance 306,305 Assessing 183,407 City Clerk 299,570 Human Resources 215,734 Treasury 167,057 Information Technology 134,965 Building & Grounds 140,540 General Administration 352,776 Police 2,263,812 Fire 2,012,337 Building & Planning 344,476 Public Works 660,310 Leaf & Brush 231,500 Parking 33,000 Community Development 85,599 Parks 203,293 Transfers Out 723,671 Total General Fund $ 8,744,235 Major Streets Fund Public Works $ 2,159,372 Local Streets Fund Public Works $ 1,452,844 Parks and Recreation Sites Fund Culture and Recreation $ 50,000 CDBG Revolving Loan Fund Economic Development $ 1,500 Historical Sites Fund Culture and Recreation $ 31,428 Historical Commission Culture and Recreation $ 129,500 General Obligation Debt Fund Debt Service $ 968,145 Capital Improvement Fund Capital Improvements $ 820,453 Capital Improvement Streets Fund Street Improvements $ 1,174,084

Transportation Fund Transportation $ 88,089 Sewer Fund Public Works $ 2,270,405 Water Fund Public Works $ 4,841,757 Waste Water Treatment Fund Public Works $ 5,172,229 Fleet Fund Public Works $ 605,553 DDA Construction Fund Economic Development $ 20,000 Brownfield Authority Economic Development $ 464,538 Section 5: Estimated Revenues The following are estimated to be available for the fiscal year beginning July 1, 2021 and ending June 30, 2022, to meet the foregoing appropriations. General Fund Property Taxes $ 3,711,670 License and Permits 385,580 State Contributions 1,774,482 Charges for Services 1,225,850 Interest and Rent Income 6,500 Fines and Forfeits 17,800 Transfers In 794,863 Other Financing Sources- Fund Balance 827,490 Total General Fund $ 8,744,235 Major Streets Fund Intergovernmental Revenue $ 1,748,073 Special Assessments 249,094 Transfers In 674,084 Interest Income 150 Total Major Streets Fund $ 2,671,401 Local Streets Fund Intergovernmental Revenue $ 516,274 Special Assessments 61,000 Transfers In 842,424 Interest Income 50 Other Financing Resources-Fund Balance 33 096 Total Local Streets Fund $ 1,452,844 Parks and Recreation Sites Fund Other Financing Resources-Fund Balance $ 50,000

OMS/ODA Fund Interest $ 500 Other Financing Resources-Fund Balance 1 000 Total OMS/DOA Fund $ 1,500 Historical Sites Fund Other Financing Resources-Fund Balance $ 129,500 Historical Commission Fund Interest/Rental Income $ 14,400 Other Revenue 1,500 Transfers In 17 000 Total Historical Comm. Fund $ 32,900 Debt Service Fund Property Taxes $ 891,685 DOA Contribution 76 460 Total Debt Service $ 968,145 Capital Improvement Fund Transfers In $ 698,103 Other Financing Resources-Fund Balance 122,350 Total Cap Improvement Fund $ 820,453 Capital Improvement Streets Fund Other Financing Resources-Fund Balance $ 1,174,084 Transportation Fund Transportation $ 40,000 Sewer Fund Charges for Services $ 2,052,000 License and Permits 500 Interest and Penalties 29,000 Total Sewer Fund $ 2,081,500 Water Fund Charges for Services $ 3,941,000 License and Permits 20,000 Interest and Penalties 43,200 Other Revenue 28,000 Total Water Fund $ 4,032,200 Waste Water Treatment Fund Charges for Services $ 2,442,210 Other Financing Sources-Loan 3,037,900 Interest Income 2,000 Other Revenue 5 000 Total Waste Water Treatment Fund $ 5,487,110 Fleet Fund Interest/Rental Income $ 705,000 DDA Construction Fund Other Financing Sources-Fund Balance $ 20,000

Brownfield Authority

Property Taxes $ 445,417

Other Income 19 121

Total Water and Sewer Fund $ 464,538

Section 6: Millage Levy

The City Council shall cause to be levied and collected the general property tax on all real and personal

property within the city upon the current tax roll an amount equal to 16.5548 mills per $1,000 of taxable

value consisting of 12.8448 mills for operating, 1.0000 mill to operate a solid waste recycling program,

.1500 for Transportation and 2.5600 mills for debt.

Section 7: Adoption of Budget by Reference

The general fund budget of the City of Owosso is hereby adopted by reference, with revenues and activity

expenditures as indicated in Sections 4 and 5 of this act.

Section 8: Appropriation not a Mandate to Spend

Appropriations will be deemed maximum authorizations to incur expenditures. The fiscal officer shall

exercise supervision and control to ensure that expenditures are within appropriations, and shall not issue

any city order for expenditures that exceed appropriations.

Section 9: Periodic Fiscal Reports

The fiscal officer shall provide the City Council monthly reports of fiscal year to date revenues and

expenditures compared to the budgeted amounts.

Section 1 O: Limit on Obligations and Payments

No obligation shall be incurred against, and no payment shall be made from any appropriation unless

there is a sufficient unencumbered balance in the appropriation and sufficient funds are or will be

available to meet the obligation.

Section 11: Budget Monitoring

Whenever it appears to the fiscal officer or the City Council that the actual and probable revenues in any

fund will be less than the estimated revenues upon which appropriations from such fund were based, and

when it appears that expenditures shall exceed an appropriation, the fiscal officer shall present to the City

Council recommendations to prevent expenditures from exceeding available revenues or appropriations

for the current fiscal year. Such recommendations shall include proposals for reducing appropriations,

increasing revenues, or both.

Section 12: City Council Adoption

Motion supported by Councilmember Law.

Roll Call Vote.

AYES: Councilmembers Pidek, Law, Fear, Haber, Teich, Mayor Pro-Tern Osika, and Mayor

Eveleth.

NAYS: None.

I hereby certify that the foregoing document is a true and complete copy of a resolution authorized by the

Owosso City Council at the regular meeting of June 7, 2021.

Downtown Development Authority General Appropriations Resolution

Motion by Mayor Pro-Tern Osika to adopt the General Appropriations Resolution to authorize the levy of

the Downtown Development Authority millage for the 2021-2022 fiscal year as follows:

RESOLUTION NO. 98-2021

GENERAL APPROPRIATIONS RESOLUTION FOR

THE DOWNTOWN DEVELOPMENT AUTHORITY

FOR FY 2021-22

WHEREAS, the Authority board met to consider a proposed budget for fiscal year 2021-22, and after

deliberations and public input approved a budget; and

WHEREAS, the Owosso City Council held a public hearing on the proposed budget on May 17, 2021;

and,

WHEREAS, it is the intent of the Downtown Development Authority to levy a tax for general operating

purposes pursuant to Public Act 197 of 1975; and

WHEREAS, the general property tax laws, specifically MCL 211.34(d) provide for an annual compound

millage reduction calculation applied to the maximum millage rate of two mills authorized by MCL

125.1662; and

WHEREAS, the millage reduction commonly known as the "Headlee" rollback results in a maximum

operating millage rate of 1.9001 for which the Authority is authorized to levy,

NOW, THEREFORE, BE IT RESOLVED THAT the City Council of the City of Owosso hereby

sets the tax rates and adopts the FY2021 budget for the Downtown Development Authority as

shown below.

NOW THEREFORE, BE IT FURTHER RESOLVED THAT, the tax levy for the fiscal year commencing

July 1, 2021 shall be the rate of 1.9001 per $1,000 of taxable value of the 2021 assessment roll for the

district as approved by the Board of Review.

Section 1: Estimated Expenditures

The following amounts are hereby appropriated for the operations of the Owosso Downtown

Development Authority and its activities for the fiscal year beginning July 1, 2021 and ending June 30,

2022:

Downtown Development $224,450

Section 2: Estimated Revenues

The following are estimated to be available for the fiscal year beginning July 1, 2021 and ending June

30, 2022, to meet the foregoing appropriations.

Property Taxes $202,000

other Revenue 24,580

Total General Fund $226,580

Motion supported by Councilmember Pidek.

Roll Call Vote.

AYES: Mayor Pro-Tern Osika, Councilmembers 1eich, Haber, Fear, Pidek, Law, and Mayor

Eveleth.

NAYS: None.

I hereby certify that the foregoing document is a true and complete copy of a resolution authorized by the

Owosso City Council at the regular meeting of June 7, 2021.

. .-;,.�,

-

//..ff '-'.,_/� ,"\:,

\.

1r and, c·t1 y C erk

. K'kl .,.,,...

"

- /'-..

-�f' \\

I --:>:- •

Executive Summary - FY 2021-22 Budget

The Fiscal Year 2021-22 budget is the result of the dedicated work of a number of city staff members

and elected/appointed officials. Thanks are due to the Owosso City Council and the City's Department

Heads for their assistance in developing this budget. In addition, the staff of the City's finance

department provided valuable support in preparing revenue and expense projections, while the entire

workforce of the City has been supportive in trusting and following the City's leadership efforts.

This document represents a diligent effort to provide an affordable, hi-quality, and safe environment for

our employees, residents, business owners, and visitors. It is designed to provide a transparent view of

the City's current funding practices, historical financial health, and our projections for future revenues

and expenditures.

It will be important for the City of Owosso to identify factors that encourage better than average

improvement in the coming years. Fiscally, city officials have made conservative financial decisions that

serve to preserve Owosso's financial future. Financial policies have been put into place that serve as

triggers for needed financial decisions rather than risk having these tough decisions deferred. Most

importantly, the city understands that good financial health directly impacts our ability to deliver quality

public service to our residents.

This executive summary will highlight a number of the key issues affecting the City's finances. This

summary will also outline many financial and administrative decisions that officials have made to

appropriately address the needs of our taxpayers in light of the financial constraints within which our

city must operate. A more in-depth analysis of the revenues and expenses proposed for the fiscal year is

provided later in the document. Any questions regarding this budget document should be addressed to

the City Manager's office.

State Economic and Policy Impact

The State Legislature and Governor have made significant changes to Michigan local revenue sharing

over the last 18 years. There are two types of revenue sharing: Constitutional and Statutory.

Constitutional revenue sharing mandates that 15% of the 4% portion of Michigan's 6% sales tax is

distributed to cities, villages and townships on a population basis. This formula cannot be changed by

the legislature since it is part of the state's constitution. Statutory revenue sharing can be changed by

the legislature and has been changed and renamed a few times. Currently, it is called the City, Village,

and Township Revenue Sharing (CVTRS) program.

Because CVTRS funding is decided by the State Legislature, it has become an attractive source of funding

to balance the state's budget since the great recession. This means that cities like Owosso have seen a

dramatic decrease in its CVTRS revenue over the last 18 years. In Owosso's case, over $10 million has

been diverted away from the City by the State of Michigan since 2003. That is an average of $750,000

per year that should have been allocated to Owosso's revenue sharing payments to fund basic services

that was instead diverted to fund other State budget priorities.In addition to CVTRS payment reductions, property taxes continue to hit the glass ceiling of the Headlee

Amendment (1978) and Proposal A (1994). These two state tax policies limit the amount of revenue

that can be collected from property taxes - many cities' principal means of funding basic services (i.e.

police departments, fire departments, parks, general administration, and certain community

development efforts).

What these challenges mean is that financing Owosso's basic services will remain a challenge in the

future if new revenues - or state tax reform - are not on the horizon.

Retirement Costs

MERS Pension System

The 2020 MERS actuarial report has been received. The city's funded ratio for the defined benefit

groups is 86%. This is better than most cities in the state but is due to a better than expected rate of

return over the last few years. The health of the city's retirement system will depend upon continued

positive investment performance which is never guaranteed. The city's annual required contributions

will continue to grow and account for 4% of all city expenses. This number will grow because the annual

contribution amount rises much quicker than the rate of inflation and increases in revenue to the city.

Capital Improvements and Purchases

This will be the 3rdyear that the City has operated under a 6-year capital improvements plan. That plan

was approved by Planning Commission and City Council in early 2021. The purpose of the capital

improvements plan is to list and prioritize all needed capital projects city wide. The plan is not a

commitment of current or future funding - rather a plan to help guide staff and council decisions on

needed improvements in the city.

For FY 21-22 the city will be funding these capital projects:

• General Fund: $829,953 for improvements and capital purchases

o Land Improvements

• $54,301 - Gould St special assessment

■ $30,000 - new overhead street lights downtown

o Building Improvements

■ $220,980 for city hall/river retaining wall replacement

■ $10,000 for city hall finance wing carpet

■ $30,000 for Library building air conditioning

replacement

■ $72,000 to replace overhead doors in DPW shop

building

• $10,000 for security and accessibility tech in city hall

■ $10,000 for boiler repair in Public Safety Building

o Equipment" $44,369 for police body worn cameras

" $34,950 for Fire/EMS defibrillator

o Computers

11

$12,500 for City wide computer replacement (phased)

• $18,000 for city hall wireless accessibility upgrades

• $5,015 for BS&A timesheets application

11

$7,000 for laserfiche server replacement for Clerk's

office

o Vehicles

• $38,690 for police cruiser (additional $17,500 pd by

grant)

" $30,058 for detective vehicle replacement

• $100,000 into 401 fund for possible FY 22-23 ambulance

replacement

• Major Street Fund $289,500

o $50,000 for street patching program

o $50,000 for sidewalk replacement and maintenance program

o $15,000 for surveying and engineering services

o $144,500 for chip sealing

o $30,000 for tree maintenance and removal

• Local Streets Fund $240,000

o $50,000 for sidewalk rehab

o $50,000 for street patching

o $30,000 for storm sewer repairs

o $142,000 for chip seal projects

o $30,000 for tree maintenance and removal

• Local Street Projects $662,000

o $162,000 for Maple Avenue reconstruction

o $500,000 for crush-and-shape street repaving projects

• Parks Millage Fund $50,000 for various park system improvements

• Historic Millage Fund $129,500 for historic sites/assets improvements

• Sewer Fund: $97,920

o $24,920 for IT and geodatabase items

o $12,000 for emergency sewer repairs

o $10,000 for engineering assistance when/where needed

o $51,000 for lift station related maintenance and monitoring

items

• Water Fund: $1,173,730

o $677,600 for lead service line replacements (state mandated)

o $350,000 for lead service line identification (state mandated)o$41,130 in IT improvements, annual cross connection program,

and misc engineering expenses

o $105,000 for Maple St water main replacement

• Drinking Water Plant: $674,650

o $14,000 to inspect and clean SW reservoir

o $40,000 for permitting and misc engineering

o $110,000 for backwash lagoon dredging

o $52,000 for replacement of high service pump and controls

o $195,900 for Palmer well No. 3 rehab

o $40,000 for treatment plant well No. 1 rehab

o $222,750 for SCADA phase 2 project

• Waste Water Plant: $55,000

o $20,000 for east tower pump rehab

o $35,000 for tertiary pump and motor replacement

• Waste Water Plant SRF: $3,037,000 for solids handling and roof project (debt)

• Fleet Fund: $270,000

o $10,000 for pavement saw

o $210,000 for aerial bucket truck

o $50,000 for 3/4 ton pickup (2)

Street Projects

This year the city's street reconstruction program will include $1 million in street projects. This includes

Maple, Gould, Glenwood, Garfield, Lincoln, McMillan, Park, Pearce, and South. Most of these projects

are simple crush-and-shapes except for Gould and Maple. These projects are being funded through a

combination of street bond sales, special assessments, Federal grants, and Act 51 receipts.

Long Term Debt

Historically, Owosso has been debt-adverse. However, in 2016 the voters approved a $10 million streets

project bond to address he city's crumbling roadways and City Council approved $2 million to update all

water meters in the City's water system. In the ten years between 2006 and 2016, the city's long-term

debt has hovered between $2.2 and $3.4 million. With the 2016 streets bond, 2018 water meter

replacement program, and now the DWRF and SRF state revolving loan programs, long term debt has

increased to $23.5 million for FY 21-22 and will continue to increase with more state revolving loan fund

projects for utility improvements. With most of this new debt taken on during periods of low interest

rates or as a part of state-sponsored debt programs that carry historically low interest rates, this means

that the city is being strategic with its new debt obligations.Staffing

For FY 21-22, the city will add an executive secretary position to the building department and promote

the building department office manager position to planning and zoning director. In 2021, the City

eliminated the Historical Commission Director contractual position. Total FTE for the City stands at 95

with an addition of 29 part time/seasonal and 7 contractual employees.

Health Insurance Costs

The City of Owosso offers health, vision, and dental insurance based on the hard-cap model allow under

Public Act 152 of 2011. Every October, the State Treasurer releases a maximum amount that

municipalities may fund employee healthcare based on three categories: single coverage, individual &

2-person coverage, and family coverage. The cap amounts for calendar year 2021 are as follows:

• Single: $7,304.51/year

• 2-person: $15,276.01/year

• Family: $19,921.45/year

The city offers a health plan that is funded completely by these hard caps but also gives employees the

option to upgrade for an additional cost borne by the employee. If an employee elects to get coverage

elsewhere, the city pays that employee to not take the city's health coverage. This payment is less than

the cost of insuring the employee and is a useful tool to reduce overall healthcare cost to the city. The

total cost of health care for the city in FY 21-22 (including costs for employees not taking the city's plan)

will be $1,320,999 ($871,510 of that cost is allocated to the General Fund). This is a 3.7%increase from

FY 21-22. In the last 10 years, the cost of health insurance has risen 46%- an average of 7%per year.

Projected Unrestricted General Fund Balance at 6.30.2022

The amount of a city's unrestricted General Fund balance is an often-used measurement of overall

financial health for the community. While Owosso does track and consider many other factors to

determine overall fiscal health, it is still important to monitor the General Fund's unrestricted fund

balance amount. It is the policy of the City of Owosso that the minimum General Fund unrestricted fund

balance shall be 25%when compared to overall General Fund expenditures for the fiscal year (after

accounting for general admin costs in other funds). It is projected that this budget will generate a year

end unrestricted General Fund balance of $2,169,791-or 25%of total General Fund appropriations for

FY 21-22. This meets the city's minimum unrestricted General Fund balance policy.

Future Years' Expectations

It will be important for the City to project its revenues and expenditures long-term in order to make

sound fiscal decisions on an annual basis. That work is assisted with the Munetrix financial tracking

system, the 6-year capital improvements plan, four utilities-related asset management plans, a fund

balance policy, and the city's willingness to look for new revenue sources (i.e. medical marijuana

facilities state tax disbursements and new grant opportunities). However, current laws regulating our

property tax system-which represents the city's largest General Fund revenue source-make it difficultfor communities like Owosso to grow their tax revenues to fund adequate basic services. In short,

Owosso's property tax revenues have only just rebounded to match what the city was collecting before

the great recession - but during the same period, costs have steadily gone up. The city has met those

challenges by greatly reducing the amount of staff positions but the work is not done. Accordingly, it is

important that the city's leadership continue to explore appropriate combinations of expense reduction,

service efficiency, and revenue enhancements to ensure that our residents and business owners

continue to receive the services that they need at a cost that is reasonable.

Conclusion

There are a number of issues that continue to affect Owosso's finances - some positive and some

negative. The city's leadership will be persistent in its efforts to provide a high level of fiscal

management that focuses on reducing unnecessary costs and improving revenues while providing

excellent services at an affordable cost to our taxpayers. Accordingly, this FY 2021-2022 budget is

respectfully submitted.

Nathaniel R. Henne - City ManagerYou can also read