Access to Orphan Drugs in South Korea : Blind Spot of the Korean Health System - Interim Report - UAEM Korea

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Interim Report

Access to Orphan Drugs in South Korea

: Blind Spot of the Korean Health System

UAEM Korea

-1-

Table of Contents

Introduction

I. Background

A. Epidemiology of rare diseases in Korea

B. Characteristics of Orphan Drug Industry in Korea

C. Characteristics of Orphan Drug Supply in Korea

D. Cases of Supply Failure by Multinational Pharmaceutical Companies

E. Case Study: Gleevec

F. Case Study: Lipiodol

II. Stimulating the production of domestic pharmaceutical companies

A. Current Policies that Support the Development of Orphan Drugs in Korea

B. Policies that Support the Development of Orphan Drugs in Other Countries

C. SWOT Analysis on Domestic Orphan Drug Industry

D. Policy Suggestions

III. Establishing State-Owned Pharmaceutical Companies

A. Rationale

B. Public Pharmacy in Foreign Countries

C. Discussion on Public Pharmacy in Korea

D. Blueprints on Public Pharmacy

E. Alternatives

Conclusion

Appendix

I. List of designated rare diseases in Korea

II. List of designated orphan drugs in Korea

-2-Introduction

The South Korean government introduced social health insurance in 1977, achieving Universal

Health Coverage in 1989. (Kwon, Lee, & Kim, 2015) With 97% of the population under the

coverage of national health insurance, the Korean health system meets the health need of the

majority of the population. (IQVIA, 2018) Yet, the Korean health system shows weakness in

delivering healthcare for minority groups including rare disease patients. Rare disease patients in

South Korea have difficulty in accessing orphan drugs - treatments for rare diseases - primarily

due to the unstable supply. As pharmaceutical prices in Korea are used as reference prices in other

countries, including China, if transnational pharmaceutical companies receive prices lower than

what they demand, they often decide not to launch drugs or withdraw from supplying drugs in

Korea. (Choi, 2018) This tendency of transnational pharmaceutical companies, so-called ‘Korea

passing’, led to several cases of orphan drug supply failure in Korea. (Park, 2018) Not only that,

even when drugs are available in Korea, many times patients cannot afford orphan drugs.

Unreliable supply systems and high drug prices hinder the access to orphan drugs in Korea.

Sustainable Development Goal 3 states that we should "ensure healthy lives and promote well-

being to all at all ages" and one of the essentials targets for achieving Goal 3 is Target 3.B that

emphasizes the need to "provide access to affordable essential medicines and vaccines". As part

of such initiative, rare disease patients should be guaranteed the access to affordable orphan drugs

(UN, n.d.). To improve the access to orphan drugs, Korea should increase the domestic production

of orphan drugs and implement policies that relieve the economic burden on patients.

This paper consists of three sections, respectively focusing on establishing a sustainable supply

system of orphan drugs, ensuring affordable prices of orphan drugs, and suggesting the roles of

universities in this issue. Under Section A, ‘Supply’, there are three parts: Part I. Background, Part

II. Domestic Private Production, and Part III. State-owned Pharmaceutical Company. Part I will

provide the Korean context of rare diseases and orphan drugs. It will explore the cases of supply

failure in the past and characterize global and domestic orphan drug industries. Part I will serve as

a guide to those who have no prior knowledge in this issue. Part II will concentrate on stimulating

the domestic production of orphan drugs. Based on the characteristics of domestic orphan drug

industry, Part II will suggest policies to stimulate the growth of the industry, however, with utmost

-3-consideration to patients’ accessibility. Yet, entirely relying on a private sector for maintaining

sustainable supply has its own risks. Public investment may not be fully translated into public

return. The access to orphan drugs cannot be risked as they treat diseases that would otherwise

have catastrophic health consequence. Accordingly, governments should take greater part in

ensuring the access to orphan drugs. Part III will discuss the possibility of state-owned

pharmaceutical companies. Although the current President Moon failed to meet the promise to

establish a public pharmaceutical company, public provision of orphan drugs is still an attractive

option. Referring to successful experience in other countries, this paper will suggest

recommendations to lay the foundation for public pharmaceutical companies in the future.

The contents of Section B, ‘Affordability’, are to be specified. Some contents will include

establishing a national fund for orphan drugs and expanding the role of the Korea Orphan and

Essential Drug Center (KOEDC) as well as improving the current financial support to raise the

patients’ access to orphan drugs.

Section C, ‘Universities’, will cast light onto possible roles that can be played by universities in

innovating the access to orphan drugs in Korea. Moreover, universities consist of not only

professors, researchers, or administrators but also active student bodies. The section will discuss

how university students can contribute to improve the access to essential medicines in general.

-4-Figure 1 Access to Orphan Drugs in Korea

Figure 1 illustrates the overall structure of the paper. Problems pointed out in Section A,

‘Supply’, apply to the cases in which orphan drugs are not available through national health

insurance. Affordability, the main theme of Section B, is yet another huddle for accessing orphan

drugs. This is the case when orphan drugs are physically available, however expensive to the extent

that access is deteriorated.

Access to orphan drugs should be a pivotal goal for the government. Everyone has “the right to

health, the right to essential medicines”, and thus the right to orphan drugs. Orphan drugs

particularly require governmental intervention as they are mostly costly without alternatives while

rare diseases, if untreated, lead to catastrophic health outcomes. Also, orphan drug industry is

economically promising. The global orphan drug market is expected to increase at a 12%

compound annual growth rate (CAGR), reaching 224-billion USD by 2024. (IQVIA, 2018) This

is considerable given that the prescription drug sales are expected to increase at the rate of 6.9%

-5-(CAGR) from 2019 to 2024. (IQVIA, 2018) This global rise in demand for orphan drugs provides

an opportunity for domestic pharmaceutical companies to enter the growing market. On top of that,

orphan drug designation allows for numerous benefits such as market exclusivity, tax exemption,

and fast track for approval. Orphan drugs can be “Niche Busters”, drugs of which global sales are

between 100-million and 500- million KRW and the number of patients is between ten thousand

and one million. The market for developing blockbusters is already oversaturated. It is strategic

for domestic pharmaceutical companies to focus on developing potential niche busters.

The concepts of state-owned pharmaceutical companies and national fund for orphan drugs are

not new and so is the emphasis on domestic drug development. Yet, with the new socialist

initiatives in public health like Mooncare, the pharmaceutical industry and policies on orphan

drugs have changed. Based on up-to-date information, this paper will make amendments to

previously discussed ideas and suggest innovative solutions, especially with a keen eye on the role

of academic institutions. This research aims to shift the focus of the Korean pharmaceutical

industry from making profits to meeting the health needs of the population.

Work Cited

Choi, E. (2018). China referencing Korea’s pharmaceutical prices as

apprehended... Transnational Pharmaceutical Companies Getting

Cold Feet (“우려했던 중국의 한국약가 참조”..다국적사 초긴장). HIT News.

Retrieved from http://www.hitnews.co.kr/news/articleView.html?idxno=2830

IQVIA. (2018). IQVIA Market Prognosis 2018-2022: Asia / Australia - South Korea. London.

Kwon, S., Lee, T., & Kim, C. (2015). Republic of Korea Health Systems Review.

Park, S. (2018). Access to Medicines and Price Transparency: Beyond

the Trade-off (의약품 접근성과 약가 투명성 : 트레이드오프인가 ?). Health

and Welfare Policy Forum (보건복지포럼), (November), 63–78.

United Nations. (n.d.). Sustainable Development Goal 3. Retrieved from

https://sustainabledevelopment.un.org/sdg3

-6-I. Background

A. Epidemiology of rare diseases in Korea

1. Definition of rare disease and orphan drugs

Rare diseases refer to diseases that affect only a small percentage of the population; orphan

drugs, medicines to treat those diseases. Yet, specific definition of rare diseases and orphan drugs

differs across countries. In Korea, rare diseases refer to diseases with 20,000 patients or fewer.

(Ministry of Health and Welfare, 2015) Currently, 1,017 diseases are designated as rare diseases.

(Kim, 2019) The complete list is available in Appendix I. By the Rare Disease Management Act,

the Ministry of Health and Welfare compiles requests for rare disease designation and annually

updates the list. (Ministry of Health and Welfare) Orphan drugs are defined as drugs for treating

rare diseases or diseases without available treatment. (Korean Food and Drug Administration,

1998) To meet the legal definition of orphan drugs, for domestically produced drugs, the annual

total production cost should be five-billion KRW or lower; for imported drugs, the annual total

sales should be five-million USD or lower. (Korean Food and Drug Administration) There are 256

orphan drugs designated in Korea, as shown in Appendix II.

2. Demographics of rare disease patients

In December 2016, the number of rare disease patients was estimated to be about 4.7

million. (Ko, 2019) Among all rare disease patients, 47.1% of them resided in the Seoul

Metropolitan Area. (Ko) Other demographic factors - sex, age, and National Health Insurance tier

- of rare disease patients are described in Table 1.

-7-Table 1 Demographics of Rare Disease Patients in Korea

Data source: Analyzing the status of rare diseases and ways to improve support for rare diseases

patients in Korea

-8-3. Rare disease profile

Table 2 Examples of prevalent rare diseases and the number of patients

Data source: Analyzing the status of rare diseases and ways to improve support for rare diseases

patients in Korea

Among the five most prevalent rare diseases, the top two were diseases of the

musculoskeletal system and connective tissue. Yet, the most economically burdensome diseases

with highest copayment did not turn out to be the most prevalent diseases. Diseases with highest

annual copayment were as follows.

-9-Table 3 Examples of rare diseases with high annual copayment

Data source: Analyzing the status of rare diseases and ways to improve support for rare diseases

patients in Korea

B. Characteristics of Orphan Drug Supply in Korea

1. Characteristics of Global Orphan Drug Industry

- 10 -The global orphan drug industry was worth 154-trillion KRW in 2018, and it is anticipated

to be 292-trillion KRW in 2024. (Evaluate Pharma, 2019) This expected growth is ascribed to two

factors: technological development and legislative support for favorable business environment.

Technology to diagnose rare diseases has advanced enough that the rate of rare disease diagnosis

is faster than that of population growth of rare disease. Also, governments are actively supporting

the development of orphan drugs. The U.S. federal government supports orphan drug R&D;

Europe enacted a law for orphan drug in 2002 to encourage the development of orphan drugs;

while the Japanese government implemented the ‘Japanese Medicines Act’ to facilitate the

regulatory approval of orphan drugs. (Korea-China Science & Technology Cooperation Center,

n.d.) As a result, the number of applications for orphan drug designation is increasing while the

number of designations is decreasing which means that more and more pharmaceutical companies

seem to be interested in orphan drugs industry. Between 2000 and 2011, Food and Drug

Administration (FDA) designated 1,251 orphan drugs and approved 116 of them. In this period,

orphan drug designation in the USA increased continuously. (Korea Health Industry Development

Institute, 2019)

Using these benefits, orphan drug developers made a huge profit. Total revenue of top 50

orphan drugs that multinational pharmaceutical companies is about 9-billion USD in 2010. Yet,

between 2011 and 2016, the growth rate of total revenue was only 1.1%. This is because many

orphan drugs’ patents expired. The most profitable orphan drug was Remicade from Johnson &

Johnson. The multinational company first launched Remicade to treat Crohn’s disease; however,

it expanded the indication of the medicine afterwards. With the patent of Remicade expired, now

several generics for Remicade are available in the market. The second most profitable orphan drug

was Enbrel from Pfizer, a cure for rheumatoid arthritis.

There are several orphan drugs that are anticipated to be profitable. The most prominent

one is Humira from Abbvie and the second one is Avastin from Roche. The expected value of each

drug is 8.7-billion and 8-billion USD. On the other hand, chemotherapy is the field that is expected

to yield most profit. 566 medicines were chemotherapy medicines that Food and Drug

Administration (FDA) evaluated in 2016.

- 11 -2. Characteristics of Orphan Drug Industry in Korea

The number of patients with rare diseases in Korea is about 500 thousand. The number of

rare diseases is about 7,000, but only 950 diseases are supported by Ministry of Health and Welfare

(MOHW). Globally the whole medicine industry stagnated but orphan drug industry is growing

continuously. South Korea is of no exception. Orphan drug industry in Korea grows 13.75%

annually, and orphan biomedicine industry grows 26.5% annually.

Table 4 Orphan drug industry in Korea (products and price in KRW)

Whole products (million KRW) Production

Whole orphan drugs 252 (98,986) 20 (3,846)

Biologics 47 (62,795) 6 (2,880)

Medicine 205 (36,499) 14 (1,275)

Data source: (MFDS, 2019)

The number of orphan drug designation by Ministry of Food and Drug Safety (MFDS) is

increasing annually, and the rate of increase is about 1%. Recently, several Korean pharmaceutical

companies are trying to develop orphan drugs to be designated by FDA every year. Since 2015,

the number of orphan drugs that is developed by Korean pharmaceutical companies and designated

by FDA increased every year. There were 16 orphan drugs of this case in 2018.

- 12 -∙ Figure 2 The number of orphan drugs exported

The size of orphan drug industry in Korea is also growing. The sales of orphan drug in

Korea increased from 21.6 billion KRW (2013) to 595 billion KRW (2017). This cannot be a

positive sign because the number of imported medicines also increased from 144 billion KRW

(2013) to 225 billion KRW (2017). This shows that Korea is dependent on import. In other words,

Korea orphan drug industry is being controlled by few multinational pharmaceutical companies.

Table 5 Production of orphan drugs by Korean

2013 2014 2015 2016 2017

(million KRW) 21,689 31,383 49,088 47,594 59,592

Increase rate (%) 44.7 56.4 -3.0 25.2

Data Source : (KHIDI, 2019)

Table 6 Importation of orphan drugs

2013 2014 2015 2016 2017

(billion KRW) 144 153 177 217 225

- 13 -Increase rate (%) 5.7 15.6 22.2 3.8

Data Source : (KHIDI, 2019)

C. Characteristics of Orphan Drug Supply in Korea

1. The number of approved medicines and ingredients in Korea

The number of approved orphan drugs is decreasing between 2014 and 2018. (Table 7)

Nonetheless, the number of domestically developed orphan drugs was much lesser than that of

imported orphan drugs.

Table 7 Approved orphan drugs (2014-2018)

2014 2015 2016 2017 2018

Total 20 49 14 18 17

Domestic 0 2 0 0 6

Imported 20 47 14 18 11

% Imported 100% 95.9% 100% 100% 64.7%

Data source: (MFDS, Drug Approval Report 2014-2018)

The total number of approved ingredients is decreasing but the percentage of imported

orphan drug ingredients is 100% in 2014, 2017 and 2018.

Table 8 Approved ingredients

2014 2015 2016 2017 2018

- 14 -Total 12 35 NA 18 9

Domestic 0 2 NA 0 0

Imported 12 33 NA 18 9

% Imported 100% 94.3% NA 100% 100%

Data source: (MFDS, Drug Approval Report 2014-2018)

NA = data not available

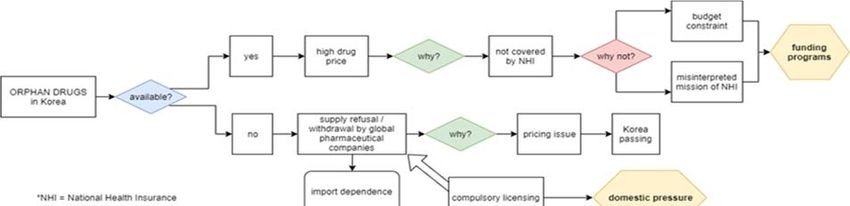

2. Supply problems of orphan drugs in Korea

As Korea heavily relies on imports from multinational pharmaceutical companies, the

supply of orphan drugs is unstable. Only 67.9% of imported orphan drugs were available at the

market. (Park, 2015)

Multinational pharmaceutical companies refused to supply their products due to the low

price suggested by the National Health Insurance Service (NHIS). Since Korea is listed as a

reference country for determining drug prices in other countries, such as China, Japan, and

countries in the Middle East, multinational pharmaceutical companies decide not to supply drugs

at prices lower than they demanded. So-called ‘Korea passing’ results in two phenomena.

First, even when drugs are designated as orphan drugs, drugs are not available at the market.

This case includes 33.5% of orphan drugs and 37.6% of orphan drug ingredients. Secondly, even

when orphan drugs are under the coverage of National Health Insurance (NHI), drugs are not

supplied at the market. 55.1% of orphan drugs were listed for reimbursement by NHI but not

available at the market. This gets worse because only 6.4% of approved orphan drugs were

produced domestically. (Kim, 2011) 93.2% of approved orphan drugs were imported.

There are several reasons why pharmaceutical companies do not supply the medicines.

First, some medicines could not be supplied due to technical problems or other problems. Amsidyl

for acute myeloid leukemia and Incodin for inflammation are examples of this case. Nonetheless,

Gleevec, Fuzeon, and Sprycel were not supplied since pharmaceutical companies decided not to,

for their profits. Furthermore, compulsory licensing for Gleevec and Fuzeon failed because of the

- 15 -refusal of pharmaceutical companies. There were 253 products of essential medicines that were

discontinued to supply for last 3 years.

Korea needs to encourage domestic production of orphan drugs not to be controlled by

multinational pharmaceutical companies. If Korea companies produce orphan drugs, the supply of

orphan drug will be stable.

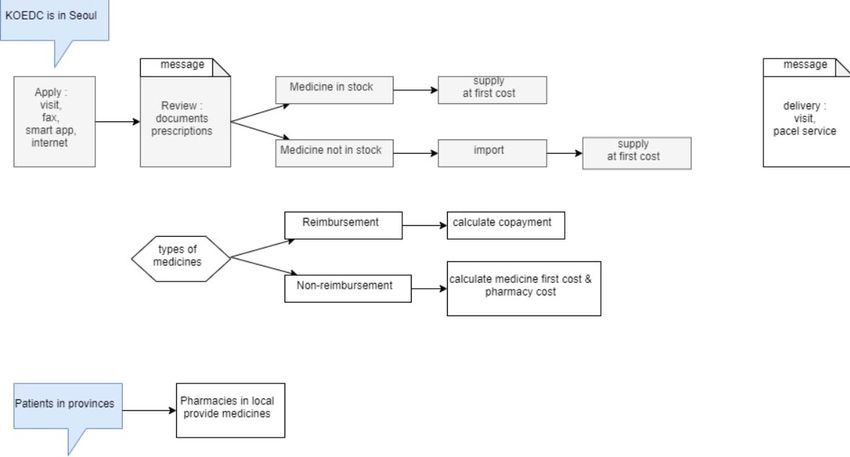

Now, Korea Orphan & Essential Drug Center (KOEDC) is supplying some medicines for

desperate patients.(Kim & Gwak, 2006) Patients can apply for orphan drugs they were prescribed

to KOEDC. Then KOEDC find those medicines and deliver to patients without their own profits.

Patients can visit KOEDC in Seoul, fax documents or use smart app of KOEDC. KOEDC reviews

those applied documents including prescription and decides whether to supply or not. If medicine

is in stock, KOEDC deliver this medicine immediately at the first cost. However, if medicine is

not in stock, KOEDC imports this medicine and delivers. The price of medicine can be different

by reimbursement. More specifically, patients can only pay copayment for reimbursement

medicine but in the case of non-reimbursement, patients need to pay medicine’s first cost and

pharmacy cost. Although KOEDC’s office is located in Seoul, patients in other provinces can

access to orphan drugs through local pharmacies.

∙ Figure 3 Application of medicine through KOEDC

- 16 -D. Cases of Supply Failure by Multinational Pharmaceutical Companies

Table 9 The list of orphan drugs that failed to be supplied

Year Producer Disease Current status

2001 gleevec Chronic myeloid leukemia Price renegotiated

2004 Fuzeon HIV/AIDS Free supply through KOEDC

2007 Sprycel Chronic myeloid leukemia Supply without refund

2008 Prezista HIV/AIDS Free supply through KOEDC

2009 Elaprase Hunter syndrome Resupply after tariff exemption

(Mucopolysaccharidoses Ⅱ)

2009 Naglazyme Mucopolysaccharidoses Ⅳ Supply with refund

2009 Myozyme Pompe disease Supply with refund

2009 NovoSeven hemophilia Price renegotiated

2018 Syprine Wilson disease Generic supplied

2018 Lipiodol transarterial chemoembolization Price renegotiated

2018 Xolair Allergic asthma Price negotiation failed

2019 Radicut Lou Gehrig’s disease (ALS) Supply refused

E. Case Study: Gleevec

Gleevec, so-called ‘miracle cancer drug’, is a treatment for chronic myeloid leukemia. It

was developed by Novartis, a multinational pharmaceutical company. In 2001, Novartis decided

- 17 -not to supply Gleevec as the price negotiation with Korea Ministry of Health and Welfare (MOHW)

was not successful. At the first price negotiation, Novartis requested 25,000 KRW per tablet, while

MOHW suggested 17,862 KRW per tablet. Novartis wanted a similar price in Korea since other

countries including Japan, Germany and USA accepted high price of Gleevec. Desperate patients

demanded compulsory licensing of Gleevec, but the Korean government did not take such

responsibility. Novartis decided to supply Gleevec to 230 patients for free just for two months. In

2003, the government and Novartis preceded the second price negotiation for Gleevec and settled

on 23,045 KRW which was 83% of the world’s average Gleevec price. After the second

negotiation, patient copayment of Gleevec was 497,770 KRW per month. In 2014, the price of

Gleevec decreased and Gleevec was supplied at 11,077 KRW per tablet. Since 2013, generics of

Gleevec, such as Supect, have been developed in Korea. (Jung, 2017)

F. Case Study: Lipiodol

Lipiodol is a contrast agent that is usually used for transarterial chemoembolization (TACE)

to cure liver cancer. It was developed by Guerbet, a French multinational pharmaceutical company.

In 2018, Guerbet demanded Health Insurance Review & Assessment Service (HIRA) to increase

the price of Lipiodol. At first, lipiodol was set as 52,560 KRW per ampule in 1999; however, now

Guerbet is demanding for five times of its first price. Otherwise, Guerbet said it won’t supply

lipiodol in Korea in 2018 which might cause an emergent situation in major hospitals. Then

government had a negotiation to set the price of Lipiodol at a reasonable level and finally the price

was set as 3.6 times of is first price. In 2012, Lipiodol was under shortage prevention program but

access to lipiodol was not improved. Still Guerbet insisted Lipiodol’s price for 260,000 KRW.

As experience, the price of medicine goes lower gradually after the end of its patent but

the price of lipiodol is continuously increasing. Furthermore, Lipiodol is an ‘Old truck’ which

means that has only an approval in France in 1965 not in Korea. This was possible because Guerbet

is a well-known company for its contrast agent. The usage of lipiodol enlarged 7 times than its

first usage for last 50 years.

Korean government considered to produce Lipiodol domestically but concluded that

producing it is impossible. The reason for this is that materials of Lipiodol are so rare. In this

- 18 -situation, congress and experts had a conversation to set up control tower of essential medicines

but they did not conclude anything.

- 19 -Work Cited

Jung, C. R., Lee, J. W., & Ko, K. (2017). A Critical Study of the Arguments for and against a Moratorium

on Glivec (글리벡 급여정지를 둘러싼 찬반논쟁에 대한 비판적 고찰). Korean J Med

Ethics

(한국의료윤리학회지), 20(3), 257-275.

Kim, H. E., & Gwak, H. S. (2006). Current Status and Expectations of Orphan Drugs in Korea – In point

of supplying medicines for the rare diseases (국내 희귀의약품의 현황 및

과제 – 희귀질환에

대한 의약품 공급을 중심으로). Kor. J. Clin. Pharm. (한국임상약학회지), 16(2), 107-

112

Kim, J. (2019). Adding 91 More Diseases to the National List of Rare Diseases

with Designation 국가관리대상 희귀질환 91 개 추가 지정. Ministry of Health and

Welfare Press. Retrieved from

http://www.mohw.go.kr/react/al/sal0301vw.jsp?PAR_MENU_ID=04&MENU_ID=0403&page=1&

CONT_SEQ=351196

Kim, T. W. (2011). Analysis of Distribution and Supply System of Orphan Drugs

(희귀의약품 유통현황

분석 및 공급방안 고찰). 숙명여자대학교 임상약학대학원.

Ko, K. (2019). Analyzing the status of rare diseases and ways to improve support for rare diseases

patients in Korea.

Korea-China Science & Technology Center (한중과학기술협력센터). Current

status of orphan drug in

major asia countries (희귀의약품에 대한 아시아 주요국가의 현황).

Korean Food and Drug Administration. Regulation on Orphan Drug Designation. , (1998).Ministry of

Health and Welfare. Rare Disease Management Act. , (2015).

Korea Health Industry Development Institute (한국보건산업진흥원). (2019).

Analysis of domestic and

foreign Orphan drug industry and development status(국내외 희귀의약품

시장 및 연구개발

현황 분석). 한국보건산업진흥원 보건산업브리프, 283.

- 20 -Park, S. (2015). Discontinued Orphan Drugs in Korea: Policy Suggestions.

(희귀의약품의 공급 중단

실태와 정책과제). 보건복지포럼.

II. Stimulating the production of domestic pharmaceutical companies

A. Current Policies that Support the Development of Orphan Drugs

Drug Preclinical Clinical Regulatory Other

Discovery Approval (After

I II III IV approval)

R&D funding

Expedited

approval

Reduction in

user fee

Exemption of

review fees for

item approval

Exemption of

data

- 21 -Assignment of

project

managers

Reduced

requirement

for GMP

assessment

Preliminary

regulatory

review

Accelerated

safety

evaluation

Extension of

re-

examination

Market

exclusivity

Tax deduction

Exemption of

data for

re-

examination

Green = economic incentives

- 22 -Blue = regulatory incentives

R&D funding: The Ministry of Health and Welfare provides the R&D grant for pre-clinical and

clinical I and II studies to selected companies, universities or other research institutes. The duration

of R&D grant is either two or three years.

Exemption of data required for approval: Before sales or import, pharmaceutical companies should

submit data from clinical trials. In the case of Orphan drug, companies do not have to submit those

data. Additionally, Orphan drug also gets exemption in submitting data used to clarify its safety:

results of clinical study can be utilized to show its pharmacological action. In particular, if orphan

drug is necessary in urgent situation, results of Phase 2 clinical trial can substitute results from

Phase 3.

Accelerated safety evaluation: Orphan drug is the subject of accelerated evaluation, and the data

necessary for drug approval can be submitted after the drug has been marketized.

Extension of re-examination period: Although market exclusivity is not separately granted, re-

examination period - a period in which the safety of drug is re-evaluated - is nearly synonymous

with market exclusivity, since generics of orphan drugs are banned during a re-examination period.

The re-examination period of orphan drugs is 10 years, which is longer than that of non-orphan

drugs, 4~6 years.

Exemption of data for re-examination: After launching a drug on the market, a pharmaceutical

company should submit the data on the safety of the drug. In the case of orphan drugs, such data

can be omitted.

Tax Deduction: 20% of income tax or corporate tax is deduced by the Ministry of Health and

Welfare. In the case of Small and Medium-sized enterprises, 30% of income tax or corporate tax

is deducted. This does not specifically target orphan drugs but also to medicines that are included

in newly growing industry such as gene medicine, antibody drug conjugate, cell therapy products

using stem cell, and biosimilar and in the category of original technology. In other words, there is

no financial aid only for Orphan drug.

Support for clinical trials: When pharmaceutical companies can be supported for clinical trials

such as writing down the plan of clinical trial, collecting subjects necessary for clinical trials and

enforcement of joint clinical trial globally

- 23 -Preliminary regulatory review: The approval of orphan drug sales and import can be prioritized

over those of other drugs.

Reduction in fees: Fees, which are required to submit an application for approval, get pre-review

and approval, are reduced.

B. Policies that Support the Development of Orphan Drugs in Other Countries

1. Orphan Drug Act in U.S. (1983)

There are many causes that pharmaceutical company should consider before developing

orphan drugs. Given the size of orhan drug in past, it was an uneasy job to be engaged in orphan

drugs, leading few companies to monopolize the market of orphan drugs. For relieving the

hardness of developing orphan drugs, U.S. government established Orphan Drug Act (ODA) in

1983 to boost R&D of Orphan drugs in pharmaceutical companies. ODA can be categorized in

two: (1) financial support (2) institutional support.

Financial support usually occurs in the form of exemption in costs such as getting

exemption of application for marketing. All orphan drugs are exempted from the cost of applying

for marketing. When it comes to tax, company can charge to deduct 50% of federal income tax.

This is carried for 20 years or until profit is generated. User fees for NDA (Non-Disclosure

Agreement) or BLA are also waived that are necessary in application, approval which is

approximately $2,000,000. Funds needed in R&D is also supported in various ways. Costs which

are indirectly or directly needed for clinical trials, are supported up to $14,000,000 annually.

Company can get financial support with this OPGP. In 1st clinical study, 0.2 million dollars per

year is supported for three years and 0.4 million dollars per year are supported for 2nd and 3rd

clinical study up to 4 years. This program also includes financial aid for office.

Even with the financial support, due to risks in being assigned as orphan drug, R&D of

orphan drug was not activated to sufficient extent. To shorten time necessary in R&D, FDA

- 24 -implemented policies such as: Fast-track (being started from 1988), Accelerated approval (1992),

Priority review (1992), Breakthrough therapy (2012). In addition, FDA assigns 10~15 companies

that can get support from FDA in every year.

Institutional support usually occurs in the form of shortening periods necessary for being

allowed. Orphan drugs are the target of Fast-track review and applicants can also request for Fast-

track review. Also, for orphan drugs, period required for approval process is shortened. Maximum

day necessary for approval is 60 days which is directly related to fast-track.

Although there is no precise statement that those policies can be applied to “orphan drug”,

U.S. applied supports in procedure also to orphan drug, considering the fact that orphan drugs are

suitable to conditions that is needed before applying that policies.

In addition, laws that can protect benefits of pharmaceutical companies are legislated such

as market Exclusivity, which bans permission of same or similar medication that can be used to

same diseases for seven years from the day when medicines get market authorization. There is a

law that can accelerated marketing procedures. Since 2007, drug developer can use application

procedure not only for FDA but also for EMEA (European Medicines Agency) to get marketing

approval. If the drug is designated as orphan drug both in U.S and EU, a single annual report can

be submitted instead of submitting reports individually.

To orphan drugs, government recognizes the necessity of using them before getting

marketing approval. Therefore, patients can use orphan drugs before marketing approval which

are also suitable to following conditions: ⑴ medicine that are for fatal disease, ⑵ If there is no

substitute, ⑶ If drugs are on clinical study or on active phase (Right before marketing approval)

2. EU

There is an “emergency licensing system” which allows medicine to be used with limit,

even if there is not enough data on efficiency in terms of safety. Similar to ODA in U.S., financial

support and institutional support also exist in EU.

In the case of financial support and institutional support for development, Orphan drug can

get financial support from EMEA in terms of application for approval and post-approval activities.

- 25 -Fee for plan of clinical trial and follow-up investigation are supported: in the case of SMEs, 100%

of cost is deducted and 75% is deducted to non-SMEs. Entire cost necessary for approval is

exempted. Particularly to SMEs, whole cost used in post-activities is supported for an year of

marketing approval. Companies are supported 100% when they got review after submitting

application for getting marketing authorization.

Different from other medications, patients can use orphan drugs without approval even in

3rd phase of clinical study or in the middle of approval. However, the speed of access is various

depending on the market size of each country in EU.

50% fee is exempted for application before getting authorization in terms of marketing.

Samely, 50% exempted fees are applied to annual post-authorization activities. In addition, fee

will be reduced for review fee and preauthorization inspection fee.

Market exclusivity that protects pharmaceutical companies for getting enough benefits also

exist in EU. Permission of same or similar medication that can be used for same diseases are not

allowed for 10 years from the day when medicines get permission of marketing. However, if the

drug is not suitable to the criteria which designated drugs as orphan drugs initially or if

unreasonable profits are generated, then market exclusivity can be withdrawn.

3. Japan

In Japan, there are financial support in the form of deduction, tax exemption. Orphan drugs

can get not only 10% deduction of corporate tax but also additional 6% of tax reduction in research

and R&D cost. 50% of expenses for conducting clinical trials is also supported. There is a financial

support in the marketing stage such as exemption of tax in terms of MAA (Marketing

Authorization Application).

At the stage of marketing, there is market exclusivity in Japan, however, it is different from

the notion in USA or in EU. After permission of medicine, same medicine which are used to treat

same disease are not allowed. 10 years are guaranteed as market exclusivity period. Re-

examination period, which takes a similar role to market exclusivity, is lengthened from six years

to ten years.

- 26 -Support that are provided during research includes free consultation which companies can

get in any stage of research and development. Also, it takes 12 months to be authorized for general

pharmaceutical firms, but in case of Orphan drug, it takes ten months to get authorization.

Generally, 12 months are necessary for reviewing but only to orphan drug, review period is ten

months.

C. SWOT Analysis on the Domestic Orphan Drug Industry

Strength Opportunity

- “Rights-attached health-committed - Increasing size of global orphan drug

president” market

(Open Society Foundations, 2019) - Possibility to seek for M&A with

- Increasing financial or administrative overseas pharmas

support for orphan drug development - Potential to cooperate with other

- Orphan drugs industry considered as governments due to overlapping

alternatives of blockbuster model interests

- Growing awareness of domestic - Korea watched by international

pharmaceutical companies to develop society, expected to act as a ‘bridge’

orphan drugs between developing/developed

- Shifting focus to open innovation to countries

strengthen internal capacities

- Advanced GMP facilities

Weakness Threat

- Relatively small pool of patients to - More comprehensive provision of

carry out clinical trials exclusive benefits to orphan drug

- Tendency to aim for FDA approval industry in other countries, such as

from developmental stage(Domestic the U.S.

- 27 -market not big enough) - More competitiveness of

- Cultural factors that draw back transnational pharma industries

facilitation of M&A with external - Varying degree of registration

entities standards that inhibit overseas market

- Scattered academic centers and entrance

limited capacity to carry out big-scale

projects

- 28 -D. Policy Suggestions

1. Pool patients for clinical trials

One of the major obstacles in orphan drug R&D is the difficulty in recruiting enough patients

for clinical trials. The orphan drug R&D in Korea usually stops at the first phase of clinical trials

and stops at the second phase of clinical trials in the US. This is mostly because, by definition,

patients of rare diseases are low in number. In this sense, clinical trial is the greatest bottleneck for

orphan drug development. A possible solution is to form a network of countries that could share

rare disease patients for clinical trials. Since the bottleneck issue is not confined to Korea, the other

countries would be interested in forming a network as well. In the network, patients from different

countries could be recruited for the same clinical trial.

A similar effort for collaborative international clinical trials exists in Europe. The European

Society for Paediatric Oncology proposed an international clinical trial model where hospitals in

different countries in Europe could run the same clinical trials for childhood cancer. For childhood

cancer, there were small groups of patients as well and this problem would be resolved with the

collaborative clinical trial platform amongst the EU countries (Kearns, n.d.). This was facilitated

within the EU system where they can have a standardized regulation for clinical trials (European

Society for Paediatric Oncology, n.d.).

In the case of Korea, such a network could be formed under the Korea National Enterprise for

Clinical Trials (KoNECT), which already has experience of forming networks with other countries

(Korea National Enterprise for Clinical Trials, n.d.). The network would consist of countries that

has similar national health system as Korea such as the National Health Insurance. Therefore,

similar government agencies from the member of countries could be in charge of the network to

allow easier cooperation. Countries such as Thailand, Taiwan, Japan, and the Philippines could be

examples of member countries for this network. The international clinical trials would be

organized at the international coordination center to set up the conditions and guidelines for the

clinical trial to be carried out. The information on the clinical trials would be sent to the national

coordination center at each participating member. The national coordination center would organize

- 29 -clinical trials at different hospitals in the country. Then, the data from the clinical trials would be

collected and stored at the international coordination center for the member countries to access

when needed. The possible limitation of this network would be the differing clinical trials

regulation amongst the member countries. Also, there will be difficulties in forming a joint

regulation and agreement amongst the member countries on how international clinical trials will

be run.

2. Impose rules to secure domestic supply during re-examination period for reliable supply

Currently, re-examination period is ten years for orphan drugs without alternatives and four or

six years for orphan drugs with alternatives. (Ministry of Food Drug and Safety, 2017) During the

re-examination period, generics cannot be made which practically gives those drugs market

exclusivity. However, it can be problematic if this hinders adept supply in response to demands,

for example when the pharmaceutical industries decide upon a higher price which becomes an

obstacle to access to treatment. On top of that, imported products account for the majority of

domestic orphan drugs which renders drug importers most beneficiaries of market monopoly.

Therefore, appropriate policy measures should be taken to secure the supply of orphan drugs

during the re-examination period. In order to secure supply stability, countries that grant market

exclusivity on orphan drugs such as the US, EU, and Taiwan are depriving pharmaceutical

companies of market exclusivity when their drugs are not sufficiently supplied to meet demand

quota. (Lee, 2019) Thus, it is implying the stability of supply as part of the market exclusivity

system of orphan drugs. To be more specific, Taiwan allows for exemption during market

exclusivity period when the supply does not meet demand, or when the central government decides

that the price is set too high. Korean re-examination policy should also consider imposing these

measures to secure domestic supply of orphan drugs.

3. Divert from closed model of R&D to open innovation system through active M&A

- 30 -Considering the global trend, M&A is an essential factor to increase competitiveness and secure

mid-to-long-term development capacity. As of 2018, the number of bio/pharma industry M&A

deals have reached 1,438 which is the highest in 10 years. Big pharmas are continuing to invest in

bioventures and seeking Open-innovation by M&A. When looking at the outbound 1 figure, 0F

Korean outbound has reached $18 million which is relatively small compared to other countries’

figures. The number of cases account for only 7% of the total deals, whereas Hongkong reached

52% and Japan reached 39%. In 2018, there were 38 domestic M&A out of 41 total established

M&A. (Lim, Chang, & Eom, 2014) Closed-R&D model with limited self-capacity is being shifted

to open-innovation system in which revolutionary ideas and new technologies are shared within

similar sectors. Pharma industry is trans-boundary in nature, since countries’ borders are

meaningless when it comes to taking actions for treating disease. No pharmaceutical industries

limit their supply market to their own countries. Therefore, Korean pharmaceutical industry should

actively take part in cross-border M&A to set ground for a long-term growth.

3. Focus more on development of biopharmaceuticals, which are high value-added products

The global pharmaceutical market is expected to grow by an annual average of 5.9% from 2016

to 2021, to $1.46 trillion by 2021. (Evaluate Pharma, 2019) With the development of

biotechnology, the emergence of innovative biopharmaceuticals such as stem cell therapies and

gene therapies has shifted the focus of global new drug development from synthetic drugs to

biopharmaceuticals. Biopharmaceuticals generally have better efficacy and fewer side effects than

synthetic drugs, resulting in high success rates in the overall process. Also, the conversion rate of

biopharmaceuticals by clinical stage is also higher than that of synthetic drugs. The probability of

transition from phase 2 to phase 3, is 34.4% for biopharmaceuticals, 32.9% for vaccines and 26.5%

for synthetic drugs from 2006 to 2015. Thus, it can be encouraged to focus on development of

biopharmaceuticals.

1

Outbound refers to M&A case in which domestic entity takes over overseas entity. (Lim et al.,

2014)

- 31 -In Korea, biopharmaceutical exports have soared from 2015, reducing the trade deficit of the

entire pharmaceutical industry. A number of pharmaceutical companies, including Bukwang

Pharm, Reyon Pharm, and Handok Pharm, are investing in bio-venture companies that are

developing new drugs and are striving for an open innovation strategy. Of these, Bukwang Pharm

invested KRW 3.9 billion 10 years ago in Anthrogen, a stem cell drug development company,

bringing financial benefits of KRW 883 billion. This case can be benchmarked by other

bioventures or pharma industry for the purpose of smoother orphan drug development and

inducing higher benefit.

- 32 -Work Cited

Anthony K et al., (2014), The current status of orphan drug development in Europe and the US,

Intractable & Rare Diseases Research, (January), 2-6

Enrique Seoane-Vazquez et al., (2008), Incentives for orphan drug research and development in

the United States, Orphanet Journal of Rare Diseases, 5-6.

European Society for Paediatric Oncology. (n.d.). Clinical Trials in Paediatric Oncology.

Retrieved from siope.eu/european-research-and-standards/clinical-trials-in-paediatric-

oncology/%0A

Evaluate Pharma. (2019). Orphan Drug Report 2019.

Lee, S. & Lee, J (2013), Rare Disease Research and Orphan Drug Development, For.J.Clin.

Pharm, Vol 23, No.1, 4-8.

Lee, Y. (2019). Domestic and Overseas Orphan Drug Industry and Analysis of Current R&D

Status. In KHIDI Brief (Vol. 283).

Lim, D., Chang, J., & Eom, Y. (2014). Samjong INSIGHT (Vol. 65).

Ministry of Food Drug and Safety. (2017). Guide to Drug Approval System in Korea.

Open Society Foundations. (2019). Access to Medicines and Innovation in South Korea.

(January), 1–23.

Park, S (2015), Discounted Orphan Drugs in Korea: Policy Suggestion, Health and Welfare

Policy Forum (보건복지포럼), (February), 67.

Kearns, Pamela. (n.d.). Clinical Trials in Europe: The Framework and Perspective [PDF

Document]. Retrieved from

https://pdfs.semanticscholar.org/7224/0e90898c31de5357480a7af1fc03ec2368c6.pdf

Kearns, Pamela. (n.d.). Towards more and better cure - the critical role of collaborative clinical

trial platforms [PDF document]. Retrieved from https://www.siope.eu/wp-

content/uploads/2017/11/Kearns_ICCD_2018.pdf

Korea National Enterprise for Clinical Trials. (n.d.). Establishment of

North East Asia Network (동북아 네트워크 구축). Retrieved from

https://www.konect.or.kr/kr/contents/business_new_6/view.do

Kwak, S. & Jeong, S (2019), Analysis of Orphan Drug market and R&D status in Korea, KHIDI

Brief, Vol 283, 4-5.

- 33 -III. Establishing State-Owned Pharmaceutical Companies

A. Rationale

'Public pharmacy' is a pharmaceutical company established and operated by the government to

efficiently and systematically conduct the production, distribution, and management of national

essential drugs and orphan drugs. The importance of stable medicine supply has emerged with the

advent of public health risks such as swine flu, Severe Acute Respiratory Syndrome (SARS), and

the Middle East Respiratory Syndrome Coronavirus (MERS-CoV) as well as the risk of new

infectious diseases and bioterrorism. Besides, the need for government's active intervention has

been pointed out through the experience of private pharmaceutical companies rejecting the supply

of orphan drugs and the unstable supply of shortage prevention drugs. In this regard, the discussion

over public pharmacy has emerged as a solution that can ensure the sustainable production and

supply of essential and orphan drugs.

B. Public Pharmacy in Foreign Countries

1. Status quo

Table 10 Publicity of the Global Pharmaceutical Production and Supply System

Data source : (Kim, Kim, & Lee, 2015)

- 34 -* s: The public ownership of the means of pharmaceutical production

* p: The public funding of pharmaceutical expenditures

* i: The control of prices and intellectual property rights of pharmaceuticals

2. Case Comparison (Kim et al., 2015)

2.1. The U.S.

Both the U.S. and Korea completely depend on the market for the

production of medicines due to the absence of public pharmacies.

However, unlike the U.S., the Korean pharmaceutical industry is not as

developed as that of the U.S., which leads Korea to rely on imports. The

size of the pharmaceutical market in Korea was 16.3 billion USD while

the size of the pharmaceutical market in the U.S. was 373.3 billion USD,

which means the size of Korea’s pharmaceutical market is only 4.4% of

the U.S. (KHIDI (한국보건산업진흥원), 2019)

2.2 Thailand, Indonesia

Korea, Thailand, and Indonesia share similarities in that the history of the national social

security system and the pharmaceutical industry is not long. Also, all three countries have high

control over price and intellectual property rights. Moreover, the need for compulsory licensing

has emerged in three countries. Thailand conducted compulsory licensing on seven medicines from

2006 to 2007 because price negotiations on HIV/AIDS treatments with pharmaceutical companies

broke down while the burden of government on healthcare expenditure was growing. Indonesia

conducted compulsory licensing in 2004, 2007, and 2012 for a total of nine items (including

HIV/AIDS and hepatitis B treatments). In 2012, the Decree of the President of the Republic of

Indonesia proposed the urgent need to control HIV/AIDS and hepatitis B and to expand

accessibility on Antiretroviral (ARV). Considering that the free access system on ARV was first

- 35 -implemented in 2004, the implementation of compulsory licensing in Indonesia would have been

inevitable for the feasibility and sustainability of the system under limited financial resources.

Unlike Thailand and Indonesia, compulsory licensing was rejected by the government in Korea.

In Korea, the need for compulsory licensing on Gleevec (treatment for leukemia) in 2002-2003

and Fuzeon (treatment for HIV/AIDS) in 2008-2009 has been drawn by civil and patient

organizations but rejected by KIPO (Korean Intellectual Property Office). KIPO said that both

cases are not particularly necessary for the public good. This is due to the political and economic

contexts that require Korea to meet stricter legal and institutional requirements as a high-income

country joining OECD. Also, Thailand and Indonesia own public pharmaceutical companies while

Korea does not. Thailand established a public pharmacy in 1966 named Government

Pharmaceutical Organization (GPO) where most medicines for national major diseases are

produced. Thailand saved 3.1 billion baht (about 100 billion KRW in 2016) of its drug budget due

to GPO. Indonesia has four public pharmaceutical companies and three of them focus on the

production of generics.

2.3 Poland

Both Korea and Poland are high-income countries that joined OECD relatively recently. Due to

this political context, there is pressure from the international community to meet the legal

requirements of high-income countries even though the history of the capitalist system is short,

and the level of pharmaceutical development is not high.

However, while the publicness remains in Poland as a historical legacy of the socialist system,

the production of healthcare services and pharmaceuticals in Korea heavily relies on the market.

C. Discussion on Public Pharmacy in Korea

1. History

- 36 -In Korea, discussion over the establishment of public pharmacy came up to the surface, but it

soon faded away. In June 2017, the passing of the National Essential Drug Supply and

Management Act triggered the controversy. Three months later, legislation on the establishment

of a public pharmaceutical company was proposed to the National Assembly but it was rejected

due to its cost-effectiveness.

While Korean Medical Association (KMA), Korea Alliance of Patients Organization, and

Korean Federation Medical Activist Groups for Health Rights (KFHR) supported the

establishment of public pharmacy, Korea Institute for Health and Social Affairs (KIHASA) and

the Ministry of Health and Welfare (MOHW) expressed skepticism.

The discussion concluded with an alternative idea: a control tower that can organically connect

existing production facilities and provide a timely supply of essential medicines.

2. Evaluation

The biggest reason for bill rejection is mostly related to the cost-effectiveness of public

pharmacy. There is a widespread concern that public pharmacy can break the market order by

providing medicines at a low price, which can be regarded as an excessive market intervention by

the government. Also, some raise concerns that the stable supply of medicines for public health

emergencies can still be achieved by private pharmaceutical companies. Since there are about 200

private pharmaceutical companies in Korea and the utilization rate of manufacturing facilities is

only 70% (Jin, Lee, & Yu, 2017), it is more cost-effective to conduct private consignment

production by using the idle production facilities of private companies, rather than establishing the

public pharmacy. Regarding a request for consignment production of orphan drugs from

government organizations, 68% of the respondents (26 private pharmaceutical companies) showed

a positive attitude. (Jin et al., 2017) Moreover, some points out that it is rather more urgent to

expand the R&D investment for private pharmaceutical companies considering the low domestic

vaccine self-sufficiency rate (50% in 2017, 14 out of 28 items) and at the same time strengthen the

role of existing organizations such as Korea Orphan & Essential Drug Center (KOEDC).

However, public pharmacy is still an attractive option in that it can improve the publicity of

essential and orphan drugs’ accessibility to a meaningful extent. The public pharmacy can

- 37 -contribute to improving drug accessibility by producing low-profit drugs that private

pharmaceutical companies are reluctant to produce. Also, independent R&Ds with utilitarian value

can be conducted. Last but not least, the public pharmacy can prevent supply withdrawal of

essential drugs, thus enabling the stable supply of national essential medicines for emergencies.

D. Blueprints on public pharmacy

1. Operating Plan

If a public pharmaceutical company was founded in Korea, it would be established and operated

under the Ministry of Health and Welfare. It would include labs, farms, distribution centers as

affiliated facilities.

The function of the public pharmacy would include the production and import of public

pharmaceuticals (including Vaccines, Shortage prevention drugs, orphan drugs, essential

medicines, Foreign aid medicines, Medicines for public health emergency), the production of

compulsory licensing drugs, the import of parallel import drugs, the investigation/promotion of

the demand and management of public pharmaceuticals, and the domestic/international

cooperation related to public pharmaceuticals.

Public pharmacy would be mostly financed by National Health Promotion Fund. Also, revenue

from the public pharmacy’s business and donations would assist the operation of public pharmacy.

(Kwon, 2017) Several regulations would be made to maximize the publicness of pharmaceuticals:

a provision that profit should not exceed a certain percentage of production cost.

2. Different Types of Establishment

- 38 -Table 11 Types of Public Pharmacy

3. Concerns

The biggest concern on public pharmacy is its cost-effectiveness and sustainability. Those who

oppose the public pharmacy points out that the continuous operation cannot be guaranteed since it

cannot generate a minimum profit for operation.

The primary reason for its low cost-effectiveness derives from the types of drugs that public

pharmacy produces. Public pharmacy would mainly deal with four types of medicines: low-priced

rare drugs, high-priced rare drugs, generics, and vaccines. First, low-priced rare drugs are unlikely

- 39 -to generate profits from exports due to low price-competitiveness compared to that of China. Also,

in case of high-priced rare drugs, it is uncertain whether the production will be possible since

compulsory licensing, a precondition for producing high-priced rare drugs, is rarely executed due

to the concerns about trade conflicts and international pressures. (Although high-priced drugs do

not necessarily mean that they are patented, they tend to be priced higher.) Moreover, there is a

criticism that the production of generics in public pharmacies can destroy the market order of the

Korean pharmaceutical industry. Because the main source of income for Korean private

pharmaceutical companies is generics, the public pharmacy can shake the private sector to its core

if they provide them at a relatively low price. Whether public pharmacy should produce generics

or not is a huge dilemma in that generics can improve the sustainability of public pharmacies but

at the same time, destroy the market order of the private sector. Finally, in the case of vaccines,

some point out that there will be no meaningful improvement in its development, production, and

supply even if a public pharmacy is established. It’s because the government has already provided

enormous support on vaccines to the private sector, and government organizations such as the

Ministry of Food, Drug, and Safety (MFDS) and Centers for Disease Control and Prevention Korea

(KCDC) are already involved in consignment production, supply management, and R&D.

E. Alternatives

1. Non-profit Social Enterprise

A non-profit organization (NPO) named “One World Health”, an organization exempt from

federal income tax under section 501(c)(3) of Title 26 of the United States, fills the gaps left by

governmental, temporary, and narrowly focused healthcare efforts. (OneWorld Health, 2020) One

World Health, funded by Bill & Melinda Gates Foundation and the UK government, is providing

treatment for neglected diseases in developing countries.

The mission of this organization is to conduct R&D and medicine dissemination on neglected

diseases. To achieve this goal, One World Health established a cooperative system with companies,

- 40 -You can also read