2022 SRB WORK PROGRAMME - srb.europa.eu - Single Resolution Board

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SRB WORK

PROGRAMME

2022

srb.europa.eu

Photo credits: Cover: iStockphoto/olaser Print ISBN 978-92-9475-280-2 ISSN 2529-671X doi:10.2877/56596 FP-AB-21-001-EN-C PDF ISBN 978-92-9475-281-9 ISSN 2529-6728 doi:10.2877/33489 FP-AB-21-001-EN-N More information on the European Union is available on the Internet (http://europa.eu). Luxembourg: Publications Office of the European Union, 2021 © Single Resolution Board, 2021 Reproduction is authorised provided the source is acknowledged. Printed by the Publications Office in Luxembourg

SRB WORK

PROGRAMME

2022

srb.europa.eu

2 Single Resolution Board I Work Programme 2022

Contents

SRB Work Programme 2022

Foreword3

Abbreviations5

Executive summary 6

1. Introduction 9

1.1. Mission statement 10

1.2. General policy context of the SRB’s work 10

2. The Single Resolution Board’s priorities for 2022 12

2.1. Achieving resolvability of SRB banks and LSIs 13

2.2. Fostering a robust resolution framework 20

2.3. Preparing and carrying out effective crisis management 25

2.4. Operationalising the Single Resolution Fund 26

2.5. The SRB as an organisation 27

3. Annexes33

Annex 1: SRB organisational chart 34

Annex 2: Resource allocation by activity for 2022 35

Annex 3: F

inancial resources and indicative procurement plan for

2022 (EUR) 36

Annex 4: Key performance indicators covering the 2022 cycle 38Single Resolution Board I Work Programme 2022 3

Foreword

The 2022 SRB Work Programme carry out the necessary reforms with

comes at a time when economies a view to have even more efficient

are rebounding from the deep European solutions. We need a single

recession triggered by the COVID‑19 banking and capital market to face

pandemic. Economic forecasts are the challenges of the future.

now painting a rosier picture than

expected some months ago, and Our resolution planning cycle for

banks have been resilient. However, 2021 is well on track, and we have

this should not make us complacent, already set clear priorities for the

and it certainly does not distract us 2022 cycle. Underpinning these prior-

from our goal: to ensure banks are ities, the SRB has developed guidance

fully resolvable by the end of 2023. for banks and our internal resolu-

tion teams, providing clear and solid

Our 2022 Work Programme is part of ground for banks to achieve resolva-

the 3-year strategy spelled out in our bility in line with the SRB Expectations

2021-2023 Multi-annual Programme. for Banks. Going forward, the focus is

The latter, together with the SRB on implementation and operationali-

Expectations for Banks, maps the sation, in line with the priorities that

path towards full resolvability of the we set last year.

banks under our remit by the end of

2023. The scars that the pandemic-in- To achieve this, we have set specific

duced crisis may have left in banks’ priorities for each bank in 2022 in

balance sheets are not yet clear. bespoke priority letters sent at the end

This makes our work on resolvabil- of September, as well as common prior-

ity and crisis readiness all the more ities for all. The focus in 2022 will be on

important to minimise any impact liquidity and funding in resolution, sep-

of potential bank failure on financial arability and reorganisation plans, and

stability and the public purse. information systems and Management

Information System capabilities.

For the same reasons, we believe the During the annual planning cycle, we

completion of the banking union – expect banks to make progress based

with the European Deposit Insurance on our guidance. Our resolvability heat

Scheme as the missing cornerstone of map will help gauge their performance

the review of the Crisis Management in doing so and ensure continuity in

and Deposit Insurance framework – our assessment.

remains a key priority for improving

the crisis toolbox and overall compet- Loss-absorption capacity is and will

itiveness of the European Union. The stay a key component of resolvability.

resolution framework has proven Many banks under the SRB remit have

effective, yet the toolbox can be been able to raise capital and debt

improved to better deal with failures instruments and thus build up the

of medium-sized banks and create necessary Minimum Requirements

a level playing field. The pandemic for own funds and Eligible Liabilities

has shown that European and inter- (MREL) issuances at record low

national decision-making bodies are interest rates. We encourage all banks

able to react quickly when needed, so to continue to build up their MREL in

we should not lose momentum and this favourable market.4 Single Resolution Board I Work Programme 2022

The SRB will further work on the oper- relevant judgments by the General

ationalisation of the resolution tools. Court and ensuring the transparency

As announced, we will take a careful of the calculation process with regard

look at operational requirements for to the contributions.

bail-in in resolution groups (Single

Point of Entry) and also expand our Of course, we do not do all this alone.

guidance on transfer strategies. Working hand-in-hand with national

The latter is reflected in minimum resolution authorities – which proved

requirements for own funds and so resilient during the pandemic –

eligible liabilities targets and closely is at the heart of our achievements.

relates to our work on separability. Our effective cooperation with other

European and international authori-

Crisis preparation is key for suc- ties, as well as the banking industry,

cessful bank resolution. In 2022, we also remains critical. We can all be

will conduct dry-run exercises to proud of how these efforts helped

test, among others, decision-mak- maintain financial stability for

ing procedures and coordination European citizens.

with external stakeholders. We will

integrate our new ICT tools into these On a personal note, I would like

exercises and put into practice the to share my appreciation of and

work carried together with national gratitude to our SRB Board Members

resolution authorities to develop and staff. 2022 will be my last year

national handbooks. serving as SRB Chair. We have come

a long way together since the early

The year 2022 will be a landmark for days of the SRB. We have been able

the Single Resolution Fund, given to navigate for more than a year

that the Common Backstop is set to on a remote virtual basis and are

enter into force early next year. This now preparing for a flexible, hybrid

will double the funds at our disposal working environment. I am proud of

to tackle bank failures. However, this how efficiently we have been able to

may not suffice if a systemic crisis adapt under such challenging and

occurs, so we still need a solution for fast-changing circumstances. Let us

the provision of liquidity in resolution. all work together to ensure we can

We will continue raising the annual deliver our priorities for 2022 and

ex-ante contributions to the Fund make all banks resolvable.

from banks, taking into account theSingle Resolution Board I Work Programme 2022 5

Abbreviations

ATC Advisory Technical Committee MAP Multi-Annual Programme

BRP Business Reorganisation Plan MIS Management Information Systems

BRRD Bank Recovery and Resolution Directive M-MDA MREL-Minimum Distributable Amount

CCP Central Counterparty MPE Multiple Point-of-Entry

CDS Credit Default Swap MREL Minimum Requirement for own funds

CMDI Crisis Management and Deposit Insurance and Eligible Liabilities

CMG Crisis Management Group MS Member States

CMT Crisis Management Team NCWO No Creditor Worse Off

CoRes Resolution Committee NPL Non-Performing Loan

DGS Deposit Guarantee Scheme NRA National Resolution Authority

DMO Document Management Office OSD Operational Steps Documents

DORA Digital Operational Resilience Act OSI On-Site Inspections

EBA European Banking Authority PIA Public Interest Assessment

ECB European Central Bank RC Resolution College

EDIS European Deposit Insurance Scheme R4C Ready for Crisis

EfB Expectations for Banks RAP Resolvability Assessment Process

ESM European Stability Mechanism ReSG Resolution Steering Group

ESRB European Systemic Risk Board RPC Resolution Planning Cycle

FMI Financial Market Infrastructure RPM Resolution Planning Manual

FOLTF Failing or Likely to Fail RPO Resolution Planning Office

FORA Forward Looking Agenda RTS Regulatory Technical Standard

FSB Financial Stability Board RTT Resolution Tactical Team

G-SIB Global Systemically Important Bank SCC Standard Contractual Clauses

HR Human Resources SNE Seconded National Expert

IAAPN Inter-Agency Appeal Proceedings SPE Single Point-of-Entry

IADI International Association of Deposit Insurers SRB Single Resolution Board

ICF Internal Control Framework SRF Single Resolution Fund

ICT Information and Communication Technology SRM Single Resolution Mechanism

IGA Intergovernmental Agreement SRMR Single Resolution Mechanism Regulation

IMF International Monetary Fund SWD Solvent Wind-Down

IRT Internal Resolution Team TLAC Total Loss Absorbing Capacity

ITS Implementing Technical Standard TPLE Trilateral Principle Level Exercise

LSI Less Significant Institution XBRL eXtensible Business Reporting Language6 Single Resolution Board I Work Programme 2022

Executive summary

This document presents the 2022 resolvability assessment heat map

Annual Work Programme of the will allow tracking banks’ progress

SRB, setting out the agency’s objec- towards resolvability and also

tives and priorities, as year-2 of the benchmarking across banks, peer

Multi-Annual Programme (MAP)1 for groups and resolution strategies.

2021-2023. The SRB is committed Where the SRB, after consulting

to making banks resolvable by the the competent authorities, deter-

end of 2023. As part of this effort, mines that there are substantive

in 2022 the SRB will work with a impediments to the resolvability

view to enforcing and operationalis- of a bank, it will notify this deter-

ing the guiding principles laid down mination to the bank and make a

in the SRB Expectations for Banks2 recommendation on the appro-

(EfB) and the Minimum Requirement priate measures to address those

for own funds and Eligible Liabilities impediments. An anonymised

(MREL) policy3. In parallel, the SRB aggregated version of the heat

will continue evolving as an organ- map according to various dimen-

isation and work towards crisis sions is expected to be made

preparedness. The SRB priorities lie public closer to the end of the

in the following five strategic areas, phasing-in period of the EfB.

in line with the 2021-2023 MAP. ►► The operationalisation of reso-

lution plans, as part of the 2022

1) ACHIEVING RESOLVABILITY OF RPC. The Resolution Planning

SRB BANKS AND LSIS Manual (RPM) has been fine-tuned

In 2022, the SRB will implement the and serves as a guide for resolu-

following priorities to work towards tion-planning activities. It supports

banks’ resolvability by the end of the SRB guidance of banks in

2023: their implementation of the EfB,

ensuring coherence between

►► Continue the implementation the common and bank-specific

of the SRB EfB for 2022, among requirements, and consistency

others, through common and across banks.

bank-specific priorities, as part

►► The SRB will enhance the internal

of the Resolution Planning Cycle

framework on deep-dives and

(RPC). For 2022, the common pri-

on-site inspections (OSIs). It will

orities are: (i) liquidity and funding

update its deep-dive guidance

in resolution; (ii) separability and

and perform quality assurance

reorganisation plans; and (iii)

checks to ensure consistency. The

management information system

deep-dives are expected to be a

(MIS) capabilities. In addition,

significant step in improving the

the SRB has addressed banks

SRB’s expertise before launching

with bespoke priorities, to steer

fully-fledged OSIs. The deep

each bank’s progress towards

dives will provide guidance from

resolvability.

some material lessons learnt in

►► To foster a level playing field order to develop the SRB OSI

in the banking union, the SRB framework, which will cover the

1

https://www.srb.europa.eu/system/files/w/document/2020-11-30%20SRB%20Multi-Annual%20

Work%20Programme%202021-2023.pdf

2

https://www.srb.europa.eu/system/files/media/document/efb_main_doc_final_web_0_0.pdf

3

https://www.srb.europa.eu/system/files/media/document/mrel_policy_may_2021_final_web.pdfSingle Resolution Board I Work Programme 2022 7

whole spectrum of the resolvabil- Functions at regional level, the crit-

ity assessment process (RAP). icality of transactional accounts,

and the assessment of protection

The SRB will continue its close of covered depositors / Deposit

cooperation with the national reso- Guarantee Schemes (DGS) and, on

lution authorities (NRAs) in Internal the analytical side, by enhancing

Resolution Teams (IRTs) regarding network and contagion models.

significant institutions, and to ensure ►► Expand the policy work on

the implementation and consistent Financial Continuity by introduc-

application of the Less-Significant ing the operational guidance for

Institutions (LSI) Guidelines and the the assessment of the identifica-

relevant SRB policies and guidance. tion and mobilisation of collateral

The SRB will continue to provide for the RPC 2022.

empirical analysis and support to

►► Continue the development and

NRAs when performing tasks for the

increase the consistency of the

LSIs under their direct responsibility.

SRB MIS architecture, as well as the

deployment of data warehouse

2) FOSTERING A ROBUST

automated tables and dashboards

RESOLUTION FRAMEWORK

in resolution planning.

Over the past few years, the SRB has

established and published its core

To ensure the adequate reflection

policies, so the focus has now shifted

of the new policies in the resolution

to operationalising the existing

plans, the SRB will conduct a system-

guidance. The key areas for work in

atic quality review of all resolution

2022 are:

plans, to ensure up-to-date and har-

monised drafting practices for banks

►► Update and enhance the MREL

under the SRB’s direct remit.

policy by (i) reviewing the no-cred-

itor-worse-off (NCWO) approach;

In 2022, the SRB will continue to

(ii) implementing upcoming

provide informed inputs to the leg-

European Banking Authority (EBA)

islative and policy discussions of

regulatory technical standards

relevance to resolution and the

(RTS) timely into the SRB policy;

banking union. The SRB is actively

and (iii) reviewing the MREL cali-

engaged and stands ready to support

bration for transfer strategies.

legislators in the ongoing review of

►► Deepen the operationalisation the Crisis Management and Deposit

of the single point of entry (SPE): Insurance (CMDI) framework and

through work on (i) the identi- the European Deposit Insurance

fication of legal and practical Scheme (EDIS) discussions. At inter-

obstacles to the implementation national level, the SRB contributes

of bail-in, including issues identi- to the development of resolution-re-

fied during the April 2021 dry-run lated international standards at the

as well as other issues stemming Financial Stability Board (FSB), and to

from the national and European bilateral dialogues with non-EU juris-

legislative framework; (ii) reso- dictions on financial services.

lution powers in the execution

of SPE strategies; (iii) the use of 3) PREPARING AND CARRYING OUT

arrangements, including contrac- EFFECTIVE CRISIS MANAGEMENT

tual, safeguarding the availability With a view to enhancing crisis prepar-

of sufficient resources to support edness, in 2022 the SRB will conduct

subsidiaries, where necessary. dry-run exercise testing, among

►► Introduce additional policy others, decision-making procedures

enhancements for the Public and coordination with external stake-

Interest Assessment (PIA), i.e. holders. In particular, the SRB will

for the assessment of Critical conduct a technical dry-run exercise8 Single Resolution Board I Work Programme 2022

involving at least one resolution unit, parallel, the SRF will carry out the

one bank and one NRA, with aiming annual exercise of calculating and

at testing bail-in execution, among collecting ex-ante contributions. As

others, as well as some aspects of the SRF continues to increase (over

governance in crisis, with the involve- EUR 52 billion as at June 2021),

ment of senior management. The the SRB continues to improve the

latter, as part of the overall goal of management of these funds. The

operationalising the resolution tools, 2022 Investment Plan will be imple-

will put into practice the work carried mented by two external investment

out together with NRAs to develop managers, and the SRB will review its

national handbooks. Dry-run will also investment strategy.

provide an opportunity to integrate

the new SRB ICT platform, Ready for 5) THE SRB AS AN ORGANISATION

Crisis (R4C), and to align it with other The SRB is now a mature institution

existing data projects and platforms. that has successfully coped with the

Lessons learned will be incorporated operational challenges posed by the

into the SRB crisis management pro- COVID‑19 pandemic, proving the

cedures and templates, ensuring importance of sound business conti-

consistent approaches and best nuity planning. The SRB will continue

practices among IRTs. working towards a ‘digital SRB’, imple-

menting its 2022 ICT strategy and

4) OPERATIONALISING THE SRF development programme. The SRB

In early 2022, the Common Backstop will also work to strengthen talent

to the Single Resolution Fund (SRF) retention by developing dedicated

will enter into force. This requires the learning and career opportunities.

SRB to implement its collateral policy Lastly, in 2022 the SRB will implement

and the methodology for the assess- the post-pandemic ‘new normal’

ment of its repayment capacity. In hybrid working arrangements.Single Resolution Board I Work Programme 2022 9

1

Introduction4

4

This publication is not intended to create any legally binding effect and does not in any way substitute the legal requirements laid

down in the relevant applicable European Union and national laws. It may not be relied upon for any legal purposes, does not

establish any binding interpretation of EU or national laws and does not serve as, or substitute for, legal advice. This document may

be subject to further revisions, including due to changes in the applicable EU legislation. The SRB reserves the right to amend this

publication without notice whenever it deems appropriate, and it shall not be considered as predetermining the position that the

SRB may take in specific cases, where the circumstances of each case will also be considered.10 Single Resolution Board I Work Programme 2022

1.1. Mission statement

The SRB is the central resolu- within the SRB’s remit be failing or

tion authority within the banking likely to fail, and also fulfil the other

union. Together with the 21 NRAs criteria for resolution, the SRB will

of the participating Member States draft and adopt a resolution scheme

(MS), it forms the Single Resolution and the relevant NRAs will implement

Mechanism (SRM). Its mission is the resolution accordingly. In addition

to ensure an orderly resolution of to resolution planning and decisions

failing banks with minimum impact for significant institutions, the SRB

on the real economy, the financial also performs an oversight function

system and the public finances of the with regard to LSIs. The SRB is also

banking union’s MS and beyond. in charge of the industry-funded SRF,

which was established to provide

The role of the SRB is proactive: ancillary financing to ensure the

rather than waiting for resolution effective application of resolution

cases to manage, the SRB focuses on schemes.

resolution planning and enhancing

resolvability in close cooperation The SRB’s values: the SRB strives to

with NRAs. The SRB drafts and adopts be a trusted and respected resolution

resolution plans for the banks under authority with a strong resolution

its remit and regularly updates capacity in the SRM, thus avoiding

these plans. In this context, the SRB future bail-outs. The SRB aims to be

determines the preferred resolution a centre of expertise in bank resolu-

strategy for a bank. This strategy sets tion. Its three values are: (i) Excellence

out the resolution tools and powers in Resolution, (ii) Integrity and (iii) EU

to be applied in the event of resolu- spirit.

tion and sets the MREL. Should a bank

1.2. General policy

context of the SRB’s

work

Due to the COVID-19 pandemic, stability, and the extraordinary

2020 and 2021 tested the global and temporary – regulatory and fiscal

EU financial regulatory framework – relief measures adopted in 2020

developed after the Great Financial were necessary. However, the case

Crisis, which has proved to be fit for such flexibility is fading away as

for purpose overall. Following the the European economy recovers, so

financial turmoil of March 2020, these measures will be progressively

the monetary and fiscal response withdrawn.

to the crisis, the decisive reaction

by regulators, and the robustness The SRB is part of an evolving policy

of banks together kept a potential and regulatory context, and stands

severe economic recession at bay. ready to engage as a key stake-

The banking union has played a holder in broader EU financial policy

major role in safeguarding financial discussions.Single Resolution Board I Work Programme 2022 11

The year 2022 will undoubtedly As economies recover from the

include regulatory activity aimed at COVID‑19 pandemic, governments

addressing the remaining gaps in the will gradually withdraw the unprece-

European financial regulation. The dented public support granted over

European Commission is expected to the past few years. This will require

present a legislative proposal on the a careful and targeted approach.

review of the CMDI framework. The The impact on non-performing loans

review concerns three legislative texts (NPLs) for the moment is limited, yet

for handling bank failures, including the outlook remains uncertain and

the SRB’s founding regulation, which vulnerable. The Commission’s Action

directly affects the Board’s activities Plan on NPLs sets out ambitious

on the medium term. The priorities options for addressing any resur-

include enhancing the toolkit to deal gence, and the SRB remains a

with medium-sized banks, the pro- committed partner in policy discus-

gressive harmonisation of national sions on this front. Should NPL issues

insolvency procedures and the contribute to a bank failing and being

alignment of the 2013 Banking resolved, the resolution framework

Communication with the revised Bank provides for adequate tools and

Recovery and Resolution Directive funding to resolve problems arising

and Single Resolution Mechanism from NPLs.

Regulation (BRRD/SRMR) framework.

The third pillar of the banking union, The SRB is also closely monitoring

EDIS, is still pending, but needs to the digitalisation of financial services

remain the target for an efficient CMDI and the related policy initiatives,

framework. A political agreement on including the Digital Operational

a credible stepwise and time-bound Resilience Act (DORA) and its

calendar towards European deposit relevant provisions for banks. The

insurance is needed to avoid perpet- SRB stands ready to play its role,

uating the use of public funds in the given the importance of data and

national handling of banking crises. MIS for resolvability. Sustainability

and green financing are also key

The Common Backstop to the SRF developments that are here to stay,

will enter into force in early 2022. and the SRB welcomes the progress

After several years of political nego- made these topics. In addition, the

tiations and operationalisation of the SRB supports the work being made

backstop, its entry into force is an on the Capital Markets Union, and

important milestone for the SRB as encourages further efforts towards

an organisation and reinforces the its completion.

credibility of the banking union’s res-

olution framework. Nevertheless, the Finally, in parallel with the entry into

Common Backstop is not a panacea force of the EU regulatory framework

and may not suffice to tackle the for the recovery and resolution

failure of a major Global Systemically of central clearing counterparties

Important Bank (G-SIB) or a systemic (CCPs), the SRB will continue to ensure

crisis from a liquidity viewpoint. A its contribution to and coordination

structural solution for the provision with all other participants of the CCP

of large‑scale liquidity in resolution is Resolution Colleges.

still to be found.12 Single Resolution Board I Work Programme 2022

2

The Single Resolution

Board’s priorities for

2022Single Resolution Board I Work Programme 2022 13

The SRB’s work in 2022 pivots around few years provides clarity and solid

the SRB’s commitment to make banks grounds for banks to achieve resolv-

fully resolvable by the end of 2023. ability in the different dimensions

This is part of a multi-annual effort set laid down in the EfB. The SRB has

in the SRB Expectations for Banks and opted for a transparent and ongoing

MREL policy. The 2021‑2023 MAP set relation with banks, and clearly sets

the stage for this exercise with clear out what is expected from them in

goals. The multiple guidance that 2022 to reach the goal of resolvability

the SRB has developed over the past by the end of 2023.

2.1. Achieving

resolvability of SRB

banks and LSIs

In 2022, the SRB will implement the

priorities in the strategic area of

2.1.1.

resolvability of SRB banks and LSIs, Implementation

along the priority streams of the

2021-2023 MAP. They concern:

of the SRB

Expectations for SRB

(i) the implementation of the SRB

banks

EfB for 2022, among others,

through common and bank-spe-

On 1 April 2020, the SRB published

cific priorities, as part of the RPC;

its EfB, which is the key reference

(ii) further operationalisation of the document for banks to build their

resolution plans when updating capabilities, under the SRB guidance,

plans and MREL as part of the 2022 in order to demonstrate that they

RPC, supported by banks’ testing are resolvable by the end of 2023

exercises under SRB guidance to in each of the areas for the suc-

demonstrate resolvability; cessful execution of their resolution

(iii) the conduct of resolvability strategies.

assessments, feeding into a

newly created SRB heat map, and The EfB are subject to a gradual

decisive action where no suffi- phase-in. The figure below shows

cient progress is made; the periods over which banks are

(iv) the enhancement of the SRM expected to build up their capabilities

internal framework on deep- in respect of the specific dimensions

dives and OSIs; of the EfB, with the beginning of 2024

as the latest deadline.

(v) the strengthening of the oversight

function of LSI.14 Single Resolution Board I Work Programme 2022

Figure 1: EfB phase-in over 2020-2023

2020 2021 2022 2023

Governance Governance arrangements supporting resolution preparedness

Loss- Fulfil intermediate MREL Fulfil final MREL targets

MREL: targets by 1 January 2022

absorbing & by 1 January 2024

recapitalisation

capacity Operationalisation of bail-in (bail-in playbooks)

SRB Expectations for Banks

Liquidity and Ability to estimate Capabilities: (1) to measure, report and forecast

funding in liquidity and funding liquidity in resolution; and (2) to identify and monitor

resolution needs in resolution assets (collateral) to obtain funding in resolution

Operational Assessment of operational continuity risk & actions to mitigate risks and measures to improve preparedness

continuity in for resolution

resolution &

access to FMI

Identification, mapping and assessing of dependencies & FMI contingency plan

services

Information MIS for bail-in execution

systems &

data

requirements MIS for valuation

Communication Communication plan

Separability &

restructuring Separability and business reorganisation measures

In 2020, the SRB communicated For 2022, the SRB has set the following

annual working priorities common three common priorities to banks

to all banks under the SRB’s remit (see further details in section 2.2.1):

to facilitate a structured and for-

ward-looking implementation of the (i) liquidity and funding in resolution;

EfB. Using a sequential approach (ii) separability and reorganisation

and annual priorities that build on plans;

each other, with the IRTs monitoring

(iii) information systems and MIS

progress, the SRB is committed to

capabilities (for bail-in and

achieving resolvability of all banks5

valuation data).

under its remit by the end of 2023.

As in previous years, these priorities

For 2020 and 2021, the SRB commu-

are complemented by bank-specific

nicated common priorities focusing

priorities defined by the respective

on (i) bail-in operationalisation, in

IRT. The SRB communicated them

particular banks’ playbooks and MIS

to banks through ‘priority letters’ at

capabilities; (ii) operational continuity

the end of September 2021. In this

in resolution; (iii) access to Financial

context, based on the guiding princi-

Market Infrastructures (FMIs); (iv)

ples laid down in the EfB and MREL

liquidity and funding in resolution;

policy, the SRB provided banks with

and (v) availability of data required

additional operational guidance on

for valuation.

the arrangements banks should work

on in the course of 2022, as it did for

IRTs closely monitored banks’

the working priorities identified for

progress in implementing these

2020 and 2021.

priorities in the course of the reso-

lution planning activities and, where

The SRB is systemically enhancing

necessary, the SRB communicated

its guidelines to ensure that banks

areas of insufficient progress that

steadily make progress in their

could jeopardise the overall objective

laid down in the EfB.

5

For banks that are switched from insolvency to resolution preference in 2021 or later, an

adequate phase-in of 3 years would be granted to implement the SRB EfB.Single Resolution Board I Work Programme 2022 15

operational preparedness in all key In 2022, the SRB will monitor the

areas of the EfB. adherence of the SRB banks with the

BRRD2 MREL targets, which become

The EfB timeline specifies that banks binding as of 1 January 2022. If

have to establish MIS capabilities to breaches are detected, the legislative

deliver the liability data for bail-in framework provides the SRB with two

at short notice by the end of 2022. formal tools for addressing them:

Against this background, banks are by imposing restrictions relating to

expected to test their MIS capabilities the MREL-Minimum Distributable

for bail-in data through a dry-run. Amount (M-MDA) or, in situations

The latter will test banks’ bail-in where the shortfall impedes the

playbooks, which are to be submitted resolvability of institutions, by trig-

by the end of 2021, in line with the EfB. gering the substantive impediments

Banks will have to provide a report procedure with all the possible

on the outcome of the dry-run which, measures listed in the BRRD. Both

once reviewed by IRTs, will serve as SRB polices are already in place.

input for cross-cutting analysis.

Finally, the SRB will conduct the pre-

Additionally, through the above-men- paratory work for 2023, which is the

tioned 2022 priority letters, the SRB final year for the phase-in of the

formally identified areas of closer EfB, again with a view to providing

monitoring where a bank needs to support and guidance to banks in

make significant progress to ensure order to become fully resolvable.

resolvability by the end of 2023.

In such cases, additional evidence

should be provided by banks in

2.1.2.

order to enable the SRB to assess Operationalisation

the existence of impediments to

resolution. Depending on how sig-

of resolution plans

nificant these impediments are, the for SRB banks

SRB will ask the bank concerned

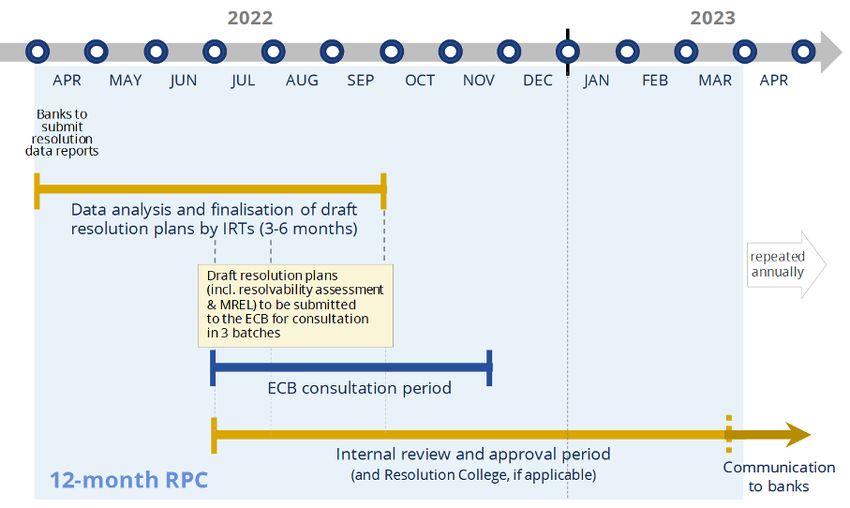

to address them either through The 2022 RPC starts in April 2022 and

corrective actions, under close mon- runs until March 2023 (cf. Figure 2

itoring by the IRT during the following below). However, this process

12-month period, or by starting the remains subject to a lengthy consul-

formal procedure for addressing sub- tation cycle that may lead to delays

stantive impediments provided for in beyond the SRB’s control. The SRB

the legal framework. This assessment and the NRAs, through the IRTs, are

will be conducted taking into account, carrying out the annual update of the

among others, the gradual phase-in resolution plans, using data with the

of EfB banks’ multi-annual work reference date 31 December 2021.

programme (delivered to the SRB The annual RPC benefits from regular

in January 2021 and to be updated lessons-learned exercises, to ensure

by the end of 2021) and the banks’ that each RPC is conducted more effi-

annual resolvability progress reports. ciently than the previous one.16 Single Resolution Board I Work Programme 2022

Figure 2: Timeline of the 2022 RPC for SRB banks

All SRB resolution plans will best-practice guide for the resolu-

be consulted with the ECB and tion plans and resolution strategies,

subject to internal quality control has been amended to require a

(cf. section 2.2.2.), which enables the clear comply-or-explain approach

2022 RPC to substantially improve when deviating from the estab-

the quality of the resolution plans. lished policies. This further ensures

The Single Rulebook is constantly compliance with the rulebook, high

evolving (as the EBA develops new standards and consistency in resolu-

RTS), and this makes the quality tion planning for SRB banks.

control process a dynamic assess-

ment – to ensure compliance with the Table 1 below provides an overview

evolving detailed rules. of the number of SRB banks for which

the SRB expects to adopt resolution

The Resolution Planning Manual plans and MREL decisions as part of

(RPM), which provides IRTs with a the 2022 RPC.Single Resolution Board I Work Programme 2022 17

Table 1: Overview of quantitative objectives planned for the 2022 RPC

Number of resolution Group resolution plans

MREL decisions expected to be

groups expected for the expected to be adopted

adopted during the 2022 RPC

2022 RPC [1] during the 2022 RPC

MS of which:

of which:

Simplified

Total with Total [3] External [5] Internal [6]

Obligations

Resolution [4]

Colleges [2]

AT 8 3 8 0 7 20

BE 6 2 6 0 5 8

BG 0 0 0 0 1 3

CY 3 0 3 0 3 2

DE 21 8 21 0 19 21

EE 1 0 1 0 1 0

EL 4 1 4 0 4 0

ES 11 2 10 0 11 6

FI 3 1 3 1 3 2

FR 13 4 11 2 10 29

HR 0 0 0 0 3 5

IE 6 3 6 0 2 11

IT 12 2 12 0 12 50

LT 1 0 1 0 1 0

LU 4 1 4 0 3 12

LV 1 0 1 0 1 0

MT 3 1 3 0 2 1

NL 7 1 7 2 7 7

PT 4 1 4 1 5 5

SI 3 0 3 0 3 4

SK 0 0 0 0 2 3

Total 111 30 108 6 105 189

Host cases Number of Resolution plans expected to be MREL decisions expected to be

[7] host cases adopted during the 2022 RPC adopted during the 2022 RPC

SE 6 2 6

BE 1 1 2

BG 1 1 1

[1] W

ithout prejudice of any change in the composition of the banking sector affecting the

number of groups within the SRB’s remit from the date of publication of this document.

With respect to banking groups for which the resolution strategy follows multiple-points-

of-entry (MPE) (i.e. application of resolution measures at the level of several resolution

entities located in MS), resolution groups are counted separately within a banking group.

This means that for countries where the number of banking groups exceeds the number

of resolution plans, it cannot be concluded that the SRB did not prepare RPs for certain

banks. The difference might be due to the fact that IRTs follow an MPE strategy for banks

in this country.

[2] Including European Resolution Colleges.

[3] T

he number of resolution plans is lower than the number of SRB banks, among others, due

to the fact that some SRB banks are part of another banking group under the SRB’s remit

and therefore are included in the respective group resolution plan.

[4] T

his figure is provisional, as the number of simplified obligations is subject to case-by-case

approval by the SRB Executive Session.

[5] At the resolution group level (i.e. including decisions for the sub-consolidated level).18 Single Resolution Board I Work Programme 2022

[6] T

he figures by country represent all subsidiaries of banking groups located in that country

(including subsidiaries of banking groups headquartered in another banking union MS)

not subject to a sub-consolidated MREL. Figures include cooperatives, in particular groups

subject to solidarity mechanisms in national legislation, which might be subject to a

dedicated MREL approach in the upcoming cycles.

[7] T

he host cases are in principle banking groups whose parent is headquartered in the

European Union but is not under direct responsibility of the SRB. Numbers are aggregated

under the MS of the banking group’s parent undertaking.

In 2022, the IRTs will perform an procedure for the removal of sub-

assessment of the bank recovery stantive impediments, as foreseen by

plans and provide comments to the the legal framework.

ECB. This assessment will, in turn,

provide input for the IRTs’ resolu- The SRB will further enhance public

tion planning activities and generally confidence by communicating how

enhance the IRTs’ crisis preparedness successfully banks manage to remove

in view of a potential transition from barriers to resolvability over time.

the recovery to the resolution phase.

2.1.4. The

2.1.3. Resolvability enhancement of the

assessment internal framework

and removal on deep-dive and

of impediments on-site inspections

for SRB banks (OSI) for SRB banks

In 2022, the resolvability assessment

Following the targeted pilot projects

heat map, implemented for the first

carried out by the IRTs in the 2021

time in the 2021 RPC, will capture

RPC, in 2022 the SRB will extend

the banks’ progress and allow bench-

the sample of the banks that will

marking against the 2022 priorities

be subject to deep-dives by their

(primarily separability, reorganisation

IRTs. The deep-dives will be carried

and the identification of collateral in

out by the IRTs as part of their res-

resolution). The results will be based

olution planning activities and will

on the IRTs’ resolvability assessments

constitute an extension of the IRT’s

included in the 2022 resolution plans

usual off-site activities. The deep-

and banks’ work programme commit-

dives are expected to be a significant

ments for the RPC.

step towards improving the SRB’s

expertise before launching ful-

This assessment, based on a set of

ly-fledged OSIs. All the deep-dive

harmonised criteria, is aimed at clas-

reports will be subject to consistency

sifying banks’ progress according to

analyses to ensure that the same

each resolvability condition and the

approach is applied to all banks’ deep

impact the latter has on the feasi-

dives and to pave the way to run

bility of the resolution strategy, or,

fully-fledged OSIs in the upcoming

where insufficient progress is noted,

years. Moreover, in 2022 the SRB will

helps to identify impediments in a

update its deep-dive guidance, based

consistent way, at different degrees

on the lessons learned from the 2021

of materiality. Where the progress

exercise. The deep-dives will be used

demonstrated by the bank shows

as a tool to further improve resolu-

that the bank is not likely to achieve

tion planning work and to check the

resolvability in line with the SRB’s

progress achieved by the banks in

expectations, the SRB will initiate the

line with the SRB EfB.Single Resolution Board I Work Programme 2022 19

yearly updates. Therefore, besides

2.1.5. Oversight the quantitative increase, the LSIs’

of less significant resolution plans notified by NRAs

provide more in-depth analyses and

institutions (LSIs) a higher degree of operationalisa-

tion, enabling the SRB to enhance its

The SRMR provides a clear division of expertise and oversight with regard

tasks between the SRB and NRAs with to LSIs. This development is expected

regard to the type of entities within to continue in 2022.

its scope. While the SRB is ultimately

responsible for drawing up plans Taking into account the above, the

and adopting all resolution-related SRB will continue to enhance the

decisions for significant institu- consistent application of high res-

tions and cross-border groups (both olution standards among the LSI

referred to as ‘SRB banks’), NRAs are resolution plans received from the

in charge of the same tasks for LSIs NRAs, with the ultimate goal of

in the banking union. With regard to ensuring their high quality and the

LSIs, the SRB maintains an oversight LSIs’ resolvability. For this purpose

function to ensure the consistent and to process efficiently a large

application of resolution standards number of notifications, the SRB will

within the banking union. Therefore, closely cooperate with the NRAs on

NRAs must submit to the SRB any a bilateral and/or multilateral basis

draft resolution measure they intend (e.g. at least two meetings of the LSI

to adopt for the LSIs under their Taskforce with all NRAs at staff level

direct responsibility, and the SRB may will take place in 2022). In particular,

express its views. a round of bilateral meetings with all

NRAs will take place in September-

According to the NRA data (April 2021), October 2022. Such bilateral and

the number of LSIs under their direct multilateral engagements involve

responsibility for which resolution ex-ante discussion of the NRAs’ policy

planning is required stands at 2 165. stances to be included in the draft

The resolution planning coverage resolution plans and other resolution

conducted by NRAs has been consist- planning approaches, with the aim of

ently increasing in the past few years, ensuring alignment with the SRB LSI

rising from 17.6% in 2017 to 51.7% Guidelines and thereby coherence

in 2018, and then to 85.3% in 2019 across the NRAs’ approaches, while

and 91.3% in the 2020 RPC. It is now remaining proportional. This was also

expected to reach 93.4% in the 2021 made possible by an increase in the

RPC and increase further in the 2022 number of SRB staff responsible for

RPC, progressively reaching 100%. In overseeing LSIs.

particular cases, some LSIs are not

covered by resolution planning due The LSI Guidelines are applied on a

to a number of technical factors such comply-or-explain basis, taking into

as entry into force of new regulatory account the principle of proportion-

frameworks and compliance with ality, while making reference to the

new policies, ongoing changes in the policies and guidance developed for

LSIs’ corporate structure and the fact SRB banks where there is no reason

that there is a number of newcomer to deviate (i.e. on grounds of speci-

LSIs for which no full information is ficity of the LSIs’ situation or national

yet available. specificities). The SRB and NRAs are

continuing to work in close cooper-

For the vast majority of LSIs under ation to ensure implementation and

the NRAs’ direct responsibility, NRAs the consistent application of the LSI

have already prepared at least one Guidelines as well as the propor-

iteration of the resolution plan, and tional application of the relevant SRB

in some cases have written several20 Single Resolution Board I Work Programme 2022

policies and guidance, in compliance SRB’s LSI risk management and

with Article 6 of the Guidelines. The strengthens crisis preparedness.

SRB also provides empirical analysis In particular, it allows the SRB to

and support to NRAs when perform- prepare in a timely manner when the

ing tasks for LSIs under their direct first signs of financial deterioration

responsibility. of an LSI emerge and provide prompt

feedback to the relevant NRA at the

Within the framework of the LSI moment of crisis, when the SRB will

oversight function, the SRB maintains have to assess the draft resolution

the Early Warning System for LSIs measure to be adopted by the NRA.

requiring closer monitoring, as laid In 2022, the SRB will further enhance

down in the Cooperation Framework6. its engagement with NRAs to ensure

This procedure contributes to the the overall LSI crisis preparedness.

2.2. Fostering a robust

resolution framework

the Resolution Committee (CoRes)

2.2.1. Development and relevant expert networks.

of SRB policies

MINIMUM REQUIREMENT FOR

Over the last few years, the SRB has OWN FUNDS AND ELIGIBLE

established and published its core LIABILITIES (MREL)

policies, so its focus is now shifting As part of the work on its resolution

from the completion and fine-tuning priorities, in 2022 the SRB will update

of the existing guidance towards oper- and further enhance its MREL policy.

ationalising the resolution strategy This is a key part of the work to opera-

and a more bespoke implementa- tionalise its resolution tools and both

tion of its policies, particularly to the Multiple Point-of-Entry (MPE) and

cater for diverging national laws. The Single Point-of-Entry (SPE) strategies.

latter justifies the SRB’s push towards This will be done, inter alia, by:

developing national handbooks and

the work on bank-specific playbooks, ►► Reviewing the NCWO approach:

with a tailored, ready-to-use and the SRB will enhance its NCWO

operational perspective. approach, and investigate possible

changes to the balance sheet when

The SRB will continue to integrate in approaching resolution. It will also

its policy work programme for 2022 assess discretionary exclusions to

the guidance from standard-setting feed into a new SRB policy and the

bodies at international and European NCWO approach for 2023.

level (the FSB and EBA). In particu- ►► Following-up any regulatory devel-

lar, the SRB will implement, where opments concerning the RTS on

relevant, RTS and ITS that the EBA will deductions for internal MREL in

deliver on execution of the rules of daisy chains.

the Banking Package. As in previous

►► Reassessing the MREL calibration

years, SRB policy work will be done in

for transfer strategies7, in par-

close cooperation with NRAs, through

ticular with a better link to the

6

https://www.srb.europa.eu/system/files/media/document/decision_of_the_srb_on_cofra.pdf

7

As explained in the 2021 MREL policy, the SRB tailors the adjustment factor to bank-specific

characteristics within a 10% corridor range with an upper limit of 25% and a lower limit of

15%.Single Resolution Board I Work Programme 2022 21

resolvability assessment progress EXPECTATIONS FOR BANKS (EFB)

(heat map) and the different reso- – GUIDANCE ON THE WORKING

lution strategies. PRIORITIES FOR 2022

►► Broadening further the scope of ►► Liquidity and funding in resolution

non-resolution entities subject

to internal MREL. The SRB will Building on the 2021 work on liquidity

continue lowering the materi- and funding in resolution, in 2022 the

ality threshold of relevant legal SRB will phase in EfB principle 3.3 and

entities, reducing it from 3% to 2% assess banks’ capabilities to identify,

in 2022. mobilise and monetise assets that

►► Implementing the new ‘permis- can be used as collateral in resolution.

sions regime’ as of 1 January 2022. Banks will be asked to focus on asset

The SRB will assess applications classes that are less likely to be used

according to the latest draft RTS in the recovery phase: non-marketable

and refine its policy in the case of assets (in particular credit claims) and,

changes when the RTS becomes a in general, assets not eligible for the

delegated regulation. ordinary central bank monetary facil-

►► Fine-tuning will also be made on ities. To support the resolution plan,

MPE, e.g. by reviewing the meth- assessment banks will be requested:

odology on the use of ‘surplus’ in (i) to identify and quantify the amount

third countries resolution groups. of collateral they hold for different

asset classes; (ii) to describe the

OPERATIONALISING SINGLE POINT operational steps (including the time

OF ENTRY (SPE) horizon and governance processes)

With a view to operationalising and to mobilise these asset classes; and

enhancing the credibility of the SPE (iii) to identify and address challenges

approach, the SRB will give further (legal, regulatory, operational, etc.) to

consideration to the practical aspects mobilise each asset class cross-border

of the implementation of the SPE in resolution (both within the EU and

strategies, including identification outside the EU).

of the legal and practical obstacles

to the transferability of funds from Solvent wind-down (SWD) of trading

the point of entry to its subsidiaries. books refers to approaches that may

Leveraging on the lessons learned be used for exiting trading activities in

from the resolution college dry-run an orderly manner and avoiding any

in April 2021, the SRB will follow up risks to financial stability. Such a tool is

on key elements, including: (a) the relevant for banks under business as

reliance on single versus multiple usual (i.e. as a recovery option), as an

failing or likely to fail (FOLTF) decla- element of the resolution strategy, and

rations in the case of a cross‑border as part of the post‑resolution Business

group crisis; (b) the identification of Reorganisation Plan (BRP). The

proper mechanisms (cf. Article 59 vs planning for these phases is closely

Article 63 of the BRRD) to ensure the interlinked. The policy will focus par-

transfer of subsidiaries’ losses to the ticularly on the context of resolution,

point of entry; and (c) the treatment under both the dimensions of financial

of losses of viable subsidiaries in the continuity and business reorganisation

resolution scheme. post-resolution. The main objectives

are (i) to adequately prepare, develop

As regards the extent of financial and maintain banks’ capabilities for

support in resolution, the SRB will the planning of a SWD in resolution,

give consideration, inter alia, to the whether as part of the resolution

usage of contractual arrangements strategy, or as actions implemented in

for making available resources to the post-resolution phase restructur-

subsidiaries, where necessary. ing context and (ii) to execute the SWD22 Single Resolution Board I Work Programme 2022

plan within a reasonable timeframe. by banks in a ‘BRP analysis report’).

The policy will be introduced in 2022, Although banks will not be requested

alongside operational guidance for to develop a fully-fledged BRP on a

banks with significant trading activities going-concern basis, they will nev-

and guidance on the first principles for ertheless be required to establish

IRTs. The final chapter of the guidance proper governance arrangements

will be drafted in 2022, for its applica- and provide an analysis of the main

tion in 2023. components of the BRP.

►► Separability and reorganisation ►► Management information systems

(MIS) capabilities

In 2022, the SRB will prioritise the EfB

dimension of ‘Separability & restruc- The SRB will request all SRB banks

turing’ and will request banks to to focus on the EfB dimension of

prepare business reorganisation and Management Information systems

separability analysis reports. (MIS) and data requirements.

Specifically, banks are expected to

To further operationalise the imple- complete the establishment of MIS

mentation of other resolution tools in capabilities for bail-in data by the end

addition to bail-in (i.e. transfer strate- of 2022. Banks will have to provide

gies), the SRB will continue to develop evidence, based on testing, as part

policy and guidance on separability. of the bank-specific deep-dives (for

Separability is defined in this context more information, see section 2.3.1.

as the bank’s ability to implement on crisis preparedness). SRB banks

a transfer of (i) legal entities, (ii) are expected to perform a simula-

business lines, or (iii) portfolios of tion of bail-in by the end of 2022. The

assets and liabilities at short notice outcome of the 2022 simulations will

to a third party. In particular, the be analysed through a monitoring

priority will be to work on separabil- report at the beginning of 2023. The

ity in order to operationalise partial latter will provide an overview of the

transfer tools (for relevant banks). banks’ progress on bail-in readiness

This work will need to be completed and promote a level playing field in

by the end of the 2023 RPC in line the banking union. Due to the utmost

with the phase in for this resolvability importance of valuation data for the

dimension in the EfB. preparation and implementation

of the resolution strategy, the SRB

Another priority for the 2022 RPC and expects banks to focus on MIS capabili-

beyond will consist in ensuring that, ties for valuation data and consistently

when open-bank-bail-in is defined implement the projects launched in

either as the preferred resolution previous cycles in order to achieve

strategy or as a variant, banks have complete MIS by the end of 2023.

the capability to draft BRPs that

would have to be delivered within PUBLIC INTEREST ASSESSMENT

1 month following bail-in execution (PIA) AND FINANCIAL STABILITY

(as required by the legislation and as ANALYSIS

detailed by principle 7.3 of the EfB). After the introduction of the policy

Since this requirement is intrinsically and guidance for the consideration of

linked to the use of the bail-in tool, it system‑wide events in the PIA for res-

is important that the relevant banks olution planning in the 2021 RPC, 2022

are capable to produce such a plan will see the introduction of further

to ensure their financial soundness policy enhancements for the PIA

and long-term viability. The SRB will including the assessment of Critical

develop internal guidance to support Functions at regional level, the critical-

the IRTs in assessing such capabil- ity of transactional accounts and the

ities (that are to be demonstrated assessment of protection of coveredSingle Resolution Board I Work Programme 2022 23

depositors / DGS. Moreover, work will quality review of the resolution

be initiated to enhance the reporting plans based on its methodology

criticality of capital market functions. developed in 2020, which has been

further improved in 2021 by taking

The analytical part of the work on into account the work on the resolv-

PIA and financial stability focuses ability assessment heat map. This

on a main deliverable taking the methodology examines the plans in

form of dashboards to support IRTs two phases, in order to foster har-

in their consistent assessments monised practices for banks under

in resolution planning. A similar the SRB’s remit and allow systematic

analysis is produced when perform- benchmarking of plans against policy

ing the PIA in a crisis case, and can developments. This leads to the year-

also be used for ad-hoc analysis and on-year improvement of the quality

briefs. Each dashboard is based on of the plans and their compliance

tools and models covering multiple with the evolving Single Rulebook

aspects of the PIA. In the 2022 RPC, (cf. Banking Package and related

specific focus will be on contagion Implementing Technical Standards

and network models, also looking (ITS), Regulatory Technical Standards

at contagion to non-bank financial (RTS), etc.). Finally, wherever the

institutions, e.g. the insurance sector, quality control identifies a need to

as well as a common framework to update or fine-tune SRB policies,

assess the real economic impact of the SRB works accordingly to revise

a bank failure and indirect contagion them8.

channels such as market analysis via

bonds and credit default swaps (CDS).

2.2.3. Monitoring of

In 2022, the SRB will finalise its com- and contributing to

putational workbench project, thus

providing a robust and modern

external policy and

platform for data-driven and econo- regulatory activity

metric analysis. The new platform will

enable the SRB to enhance its financial In 2022, the SRB will engage closely

stability models, including network with the European Commission,

contagion models and models European Parliament, Council of the

assessing impact on the real economy. European Union, the ECB and the

In terms of resolution reporting and EBA on relevant regulatory and policy

data exchange, the SRB will introduce issues. The priority topics for 2022 in

new tools supporting the MREL and terms of external policy and regula-

Total Loss Absorbing Capacity (TLAC) tory activity include:

calculations, improve its data quali-

ty‑checking procedures and extend its ►► the review of the CMDI framework;

data exchange with the ECB. ►► the discussions on strengthen-

ing the banking union, especially

2.2.2. Quality focused on the agreement of a

work plan for EDIS (closely linked

assurance of to the above) and cross-border

resolution plans and integration;

►► ongoing discussions on the

benchmarking provision of liquidity in resolution;

In line with its mandate, the SRB will ►► discussions regarding other leg-

continue to conduct a systematic islative files on financial services,

8

This is done in cooperation with NRAs and can be particularly important with new and

complex policies, after they have been implemented for the first time, such as – to give just

one example – the SRB’s updated approach to PIA for systemic-wide-events.You can also read