University of Texas at Austin Energy Symposium 2013 Energy Innovation and Entrepreneurship - April 30, 2013

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

April 30, 2013

University of Texas at Austin Energy Symposium 2013

Energy Innovation and Entrepreneurship

NYSE: LPI

www.laredopetro.com

Forward-Looking / Cautionary Statements

This presentation (which includes oral statements made in connection with this presentation) contains forward-looking statements within the meaning of Section 27A of the Securities Act of

1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical fact, included in this presentation that address activities, events or

developments that Laredo Petroleum Holdings, Inc. (the “Company”, “Laredo” or “LPI”) assumes, plans, expects, believes or anticipates will or may occur in the future are forward-looking

statements. The words “believe,” “expect,” “may,” “estimates,” “will,” “anticipate,” “plan,” “intend,” “foresee,” “should,” “would,” “could,” or other similar expressions are intended to identify

forward-looking statements, which are generally not historical in nature. However, the absence of these words does not mean that the statements are not forward-looking. Without limiting

the generality of the foregoing, forward-looking statements contained in this presentation specifically include the expectations of plans, strategies, objectives and anticipated financial and

operating results of the Company, including as to the Company’s drilling program, production, hedging activities, capital expenditure levels and other guidance included in this presentation.

These statements are based on certain assumptions made by the Company based on management’s expectations and perception of historical trends, current conditions, anticipated future

developments and other factors believed to be appropriate. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond the control of the

Company, which may cause actual results to differ materially from those implied or expressed by the forward-looking statements. These include risks relating to financial performance and

results, current economic conditions and resulting capital restraints, prices and demand for oil and natural gas, availability of drilling equipment and personnel, availability of sufficient capital

to execute the Company’s business plan, impact of compliance with legislation and regulations, successful results from our identified drilling locations, the Company’s ability to replace reserves

and efficiently develop and exploit its current reserves and other important factors that could cause actual results to differ materially from those projected as described in the Company’s

Annual Report on Form 10-K for the year ended December 31, 2012, and other reports filed with the Securities and Exchange Commission (“SEC”).

Any forward-looking statement speaks only as of the date on which such statement is made and the Company undertakes no obligation to correct or update any forward-looking statement,

whether as a result of new information, future events or otherwise, except as required by applicable law.

The SEC generally permits oil and gas companies, in filings made with the SEC, to disclose proved reserves, which are reserve estimates that geological and engineering data demonstrate with

reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions and certain probable and possible reserves that meet the SEC’s

definitions for such terms. In this presentation, the Company may use the terms “unproved reserves”, “unbooked resource potential”, “estimated ultimate recovery”, “EUR” or other

descriptions of volumes of reserves, which the SEC guidelines restrict from being included in filings with the SEC. The Company does not choose to include unproved reserve estimates in its

filings with the SEC. “Unproved reserves” refers to the Company’s internal estimates of hydrocarbon quantities that may be potentially discovered through exploratory drilling or recovered

with additional drilling or recovery techniques. “Unbooked resource potential” is used by the Company to refer to the estimated quantities of hydrocarbons that may be added to proved

reserves, largely from a specified resource play. A resource play is a term used by the Company to describe an accumulation of hydrocarbons known to exist over a large areal expanse and/or

thick vertical section, which, when compared to a conventional play, typically has a lower geological and/or commercial development risk. Estimated ultimate recovery, or “EUR”, refers to the

Company’s internal estimates of per well hydrocarbon quantities that may be potentially recovered from a hypothetical future well completed as a producer in the area. Unproved reserves,

EURs and unbooked resource potential, may not constitute reserves within the meaning of the Society of Petroleum Engineer’s Petroleum Resource Management System or SEC rules and do

not include any proved reserves. Actual quantities that may be ultimately recovered from the Company’s interests will differ substantially. Factors affecting ultimate recovery include the scope

of the Company’s ongoing drilling program, which will be directly affected by the availability of capital, drilling and production costs, availability of drilling services and equipment, drilling

results, lease expirations, transportation constraints, regulatory approvals and other factors, as well as actual drilling results, including geological and mechanical factors affecting recovery

rates. Estimates of unproved reserves, EURs and unbooked resource potential may change significantly as development of the Company’s core assets provide additional data. In addition, the

Company’s production forecasts and expectations for future periods are dependent upon many assumptions, including estimates of production decline rates from existing wells and the

undertaking and outcome of future drilling activity, which may be affected by significant commodity price declines or drilling cost increases.

This presentation includes financial measures that are not in accordance with generally accepted accounting principles (“GAAP”), including Adjusted EBITDA. While management believes that

such measures are useful for investors, they should not be used as a replacement for financial measures that are in accordance with GAAP. For a reconciliation of Adjusted EBITDA to the

nearest comparable measure in accordance with GAAP, please see the Appendix.

2

Technological Innovations Create Step Changes

Offshore Drilling

Rotary Drill Bit

.

Horizontal Drilling and

Hydraulic Fracturing

3

Horizontal Drilling & Hydraulic Fracturing: Unlocking Potential

Horizontal drilling, hydraulic fracturing and long-reach laterals Groundwater Water wells >1,000

aquifer feet

Multi-stage horizontal fracturing

Fracturing fluids and techniques

Steel casing and

Seismic and other geophysical analysis of drilling locations

cement to protect

groundwater

Reductions in environmental impacts (pad drilling, water

conservation and recycling, reformulation of additives, etc) Protective

steel casing

Shale fractures

10,000+ Feet

Horizontal Drilling and Hydraulic Fracturing Have Revolutionized the Oil and Gas Industry

4

Shale Gas Revolutionized North American Natural Gas Development

Large-scale application

of horizontal drilling

and hydraulic

fracturing techniques

in the shale plays

began in the early

2000s.

Since 2005, shale gas

production has been

increasing by about

50% per year.

5

Oil Shale Revolution Changing U.S. Energy Landscape

U.S. Avg Daily Oil Production (1970-2015)

11,000

10,000

9,000

Oil Shale

Thousand Barrels per day

8,000 Revolution

Begins!

7,000

6,000

5,000

4,000

3,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Source: EIA, Raymond James 6

Where is it Coming From?

7

Energy Independence Now a Real Speaking Point

North American Energy Independence

and Security are now possible

8

“L” Companies have Capitalized on the Changing Energy Landscape

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Colt Resources Corp. Lariat Petroleum, Inc. Latigo Petroleum, Inc. Laredo Petroleum, Inc.

Sold to JN Resources in 1996 Sold to Newfield in 2001 Sold to Pogo Producing Founded in October 2006

for $33.5 million for $333 m illion in 2006 for $750 million

Equity Investor: First Reserve Equity Investor: Warburg Pincus Equity Investors: Warburg Pincus Equity Investor: Warburg Pincus

JPMorgan

$3,620

($ millions)

Equity Utilized $2,750

Debt Utilized

Sales Price / Enterprise Value

$1,215

$750

$333 $360

$174

$13 $33.5 $710

$200

$100

$74 $160

Focus Areas:

A 20+-Year History of Generating Significant Value for Investors

9

The “L” Company Culture

INTEGRITY – Always do the right thing.

STEWARDSHIP – Take care of the company,

industry and environment.

RESPECT – Treat people everywhere the way you

want to be treated.

TEAMWORK – One company working together to

achieve common goals.

SUCCESS – Driven to succeed and plan for success.

10Critical Elements for “L” Companies

Plan for success from day one

Determine your strengths

Determine area of concentration

Develop a business plan

Secure “correct” equity funding

11The Private Equity Market

INVESTORS Advantages

• Pension funds Fast Access to Capital

• Endowments Strategic Advice

• Foundations Formal Structure

Bank holding

•

companies

Credibility

Private Equity Provider

• High-net-worth

individuals Disadvantages

• Investment banks

Fast Equity Dilution

• Corporations Strategic Advice

• Other investors Formal Structure

Investment Cycle

12Requirements for Private Equity Partners

Compatibility

Access to significant capital

Long-term investment cycle

Understand oil and gas industry risk and reward

Strategic advice / experience

Allow a strong outside board of directors

13Warburg Pincus: Strong Track Record Supporting E&P Companies

Warburg Pincus: Sample of their Worldwide Energy Companies:

Warburg Pincus’ philosophy of not “over leveraging” entities provides prudent balance sheet

stewardship

Management leverages Warburg Pincus’ relationships and industry contacts to support Company

Warburg Pincus has taken over 120 of their portfolio companies public

Laredo formed through a $600 million equity commitment from Warburg Pincus and members of

management

14Laredo Overview

NYSE: LPI

Market Cap: ~$2.4 Billion

Total Enterprise Value: ~$3.6 Billion

Total Company

Permian oil focused

Low-risk drilling inventory >10 years

Proved reserves: 188.6 MMBOE1

Average daily production: ~33.3 MBOE/D

during Q4-20121

Sound financial structure

• Rapidly growing cash flow from

operations

• Operational and financial flexibility

maintains capital options

1 Production and reserves reported on a two-stream basis. Reserves are gas price adjusted to reflect NGL benefit. Proved reserves per Ryder Scott evaluation at 12/31/12, at SEC pricing.

15Concentrated Asset Portfolio Focused in Permian Basin

Permian

China Grove

Tulsa

Headquarters

Midland

Basin

Permian

Delaware Garden City

Basin

Permian Basin – ~203,500 net acres 1

• ~85% of total company reserves

• ~69% of Q4-2012 total production

• ~92% working interest - average

1 Acreage totals as of 12/31/12. 16Consistent Growth in Reserves and Production

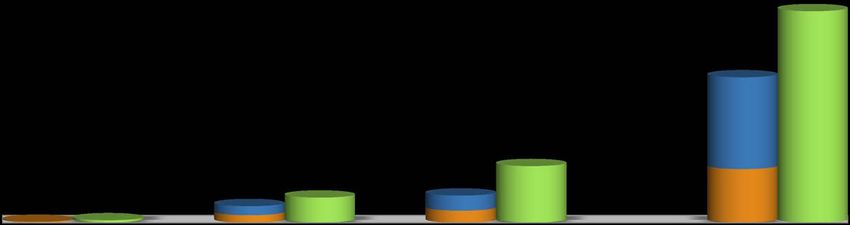

Permian oil is driving repeatable growth

Reserves Production 34.5-35.9

200 188.6 35

180 30.9

30

156.5

160

136.6 48% 25 23.7 19.0

140

120 64% 17.3

20

MBOE/D

MMBOE

67%

100

14.3 14.5

80 15

9.8

60 44.2

52.5

10 9.8

52% 16.2

40 89% 13.6

36% 4.2 8.4

92% 33% 5 9.2

20

8% 11% 3.7 4.5

- 0 0.5 1.4

2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 2013 E

Successful transition to 2013

higher value oil reserves 25% growth in oil production

Targeting 15% total production growth

Reserves reported on a two-stream basis with gas price adjusted to reflect NGL benefit; per Ryder Scott evaluation at 12/31/12, at SEC pricing.

Production data includes production from Broad Oak Energy, Inc. on a combined basis and presented on a two-stream basis. 17

CAGR in MBOE/D production from 2008 through midpoint of projected 2013.Permian Basin: Multiple Targets of Opportunity

Howard

Mitchell

Martin

Midland

Sterling

85+ miles

Glasscock

Reagan

LPI Acreage Tom Green Commercial horizontal

LPI Horizontal Wells

Upton

Upper Wolfcamp

development has been

Middle Wolfcamp Irion proven for all four zones

Lower Wolfcamp

Cline

from >60 wells

20+ miles

1 Well counts as of 2/28/13

2 Based on 2012 and 2013 completions with at least 30 days of production history as of 2/28/13 18Identified Resource Potential – De-risked Acreage To-Date

1800 Identified Resource Potential1

1,415 + 1,600 +

1600

De-risked Resource Potential of greater

than 1,600 MMBOE

1400

1200

Additional upside to resource potential for

continued delineation of:

1000 • Hz Upper Wolfcamp

Hz Middle Wolfcamp

MMBOE

•

• Hz Lower Wolfcamp

800 • Hz Cline

600 15+ year of development opportunities

400

Development of our identified resource

189 potential will require access to additional

200 capital

0

• Debt capital markets

Estimated Total Additional Identified • Equity capital markets

Proved Reserves De-risked De-risked

12/31/12 Resource Resource

Potential Potential

1 De-risked acreage and resource potential totals as of 2/28/13

19Laredo’s Debt Financing

Strong bank group

$825 million Revolving Credit Facility from commercial banks

Comprehensive risk management program

Public debt

$550 million HY 9.5% Senior Notes due 2019

$500 million HY 7.375% Senior Notes due 2022

Laredo’s Bank Group Includes:

20Laredo’s Initial Public Offering

Advantages to public equity Disadvantages to public equity

Access to capital Expensive and time consuming

Increased liquidity Restrictions

Public currency for acquisitions Broader shareholder base

Enhanced benefits for current employees Reduced control

21What Are The Next Innovations in Oil and Gas?

Horizontal Drilling and

Hydraulic Fracturing

Offshore Drilling

?

Rotary Drill Bit

.

22NYSE: LPI www.laredopetro.com

You can also read