UNE Strategy 2021+ Environmental Scan and Analysis - 29 May 2020 Author Megan Aitken 0455 022 060

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

OPEN Council Meeting Page 111 of 327

Page |1

UNE Strategy 2021+

Environmental Scan and Analysis

29 May 2020

Author

Megan Aitken

Megan_a@rocketmail.com

0455 022 060

OPEN Council Meeting Page 112 of 327

Page |2

Contents

Highlights Summary........................................................................................................................ 4

New Technologies .............................................................................................................................. 4

Changes in Pedagogy .......................................................................................................................... 4

New educational models .................................................................................................................... 4

Changing Consumer Demand and Trends .......................................................................................... 5

1.0 Market Trends and Themes....................................................................................................... 6

Online education growth.................................................................................................................... 6

Case Studies: New Online Models ...................................................................................................... 7

Lifelong Learning ................................................................................................................................ 7

The Fourth Industrial Revolution........................................................................................................ 8

Job Pathways Based on Skills ............................................................................................................. 9

Changes in Workplace Training ........................................................................................................ 11

Case Studies: Workplace Education and Training ............................................................................ 12

2.0 Market Drivers and Opportunities .......................................................................................... 13

The Domestic Market ....................................................................................................................... 13

The International Market ................................................................................................................. 15

The Modern Learner ........................................................................................................................ 16

A Closer Look at Generation Z (1995-2015) ..................................................................................... 17

A look at Generation Alpha (Born after 2010).................................................................................. 19

3.0 Educational Models and Competitive Landscape ..................................................................... 20

Emerging Educational Models .......................................................................................................... 21

New Educational Approaches .......................................................................................................... 22

Case Studies: New Business Models in Practice ............................................................................... 22

Game Changers: ............................................................................................................................... 23

Job Placement Services ................................................................................................................... 23

Corporate Training .......................................................................................................................... 23

Immersive Media ............................................................................................................................ 23

Leveraging The Shared Economy .................................................................................................... 24

Leveraging Crowd Sourcing ............................................................................................................. 24

4.0 Strategic Digital Trends in Education ....................................................................................... 25

Longer Team: Top trends for universities 2022-2025 ...................................................................... 25

Short Term: Top trends for universities 2020-2022 ......................................................................... 27

Case Studies: New Technologies In Practice .................................................................................... 32

5.0 Impact of COVID-19 pandemic ................................................................................................ 34

OPEN Council Meeting Page 113 of 327

Page |3

Education sector............................................................................................................................... 34

Online learning ................................................................................................................................. 34

Businesses and the consumers......................................................................................................... 35

Economy ........................................................................................................................................... 35

Post Covid - A New Norm ................................................................................................................. 36

6.0 Trends in pedagogy and teaching models ............................................................................... 37

Digital Pedagogy ............................................................................................................................... 37

Adaptive Learning ............................................................................................................................ 38

Flipped Learning ............................................................................................................................... 39

Digital Courseware Design ............................................................................................................... 40

Case Studies: Digital Pedagogy in Practice ....................................................................................... 41

7.0 Evolving models for industry engagement............................................................................... 42

The Value of Better Partnerships ..................................................................................................... 42

Maturity of Australia’s Industry Engagement Model ....................................................................... 43

Case Studies: Industry Engagement Ecosystems .............................................................................. 44

8.0 Trends in physical and built education infrastructure .............................................................. 46

SmartCampus ................................................................................................................................... 46

Case studies: Smart Campus Stars ................................................................................................... 47

9.0 Regulatory Systems and Policies ............................................................................................. 48

Impact of Covid ................................................................................................................................ 48

Likely Regulatory Scenarios .............................................................................................................. 48

10.0 Research ............................................................................................................................... 49

Case Studies: Star Performers .......................................................................................................... 50

11.0 Mergers and Acquisitions ...................................................................................................... 50

Case Studies ..................................................................................................................................... 51

12.0 Change Management Models................................................................................................ 52

Kotter Model (2014) ......................................................................................................................... 53

Case Studies ..................................................................................................................................... 53

Recommended Reading ................................................................................................................ 55

OPEN Council Meeting Page 114 of 327

Page |4

Highlights Summary

New Technologies

• Investment in new learning technologies will surge as a result of Covid-19 so universities must continue to build

on their current online successes with more rigour and pace than ever before.

• Short term (2020-2023), there are eight different initiatives that are being implemented across universities

and should form part of any university strategy: Adaptive Learning; Blended/Flipped Learning Delivery;

Immersive and Multi-Media Courseware Design; Artificial Intelligence Analytics (Insights Driven Education);

Learning Gamification; Learner Spaces/Labs; Enhanced Learner Experience Systems (LMS, Enrolment and

CMS); Data and Cyber Safety and Security

• Priority should be given to a three-year artificial Intelligence and data warehouse strategy to leverage

student data across all phases of their journey (enrolment, learning experience, job placement). This enables the

implementation of technology tools such as chatbots, personalised learning and predictive nudge strategies.

• Trialling and implementing immersive media (AR/VR/holograms) and new digital design in courseware is

starting to emerge in selected Faculties. Investing in, or partnering with organisations, to transform existing

content using new technologies are now part of new digital era. Simulation tools reduce the overall cost and

volumes of learning, they provide more data points compared to traditional learning, and improve graduation

outcomes. While enhancing courseware assets through the use of 360 degree videos, interactive quizzes,

hotspots, ebooks, role playing tools, 3D models complement immersive media to provide a truly digitised

experience for students.

• Being able to provide students with an enhanced learning platform (LMS) that is agnostic to the mode of

delivery (ie: it can be used for online and hybrid learning), offers intuitive digital features and digitally designed

courseware, as well as personalised learning will be key in the future. The real challenge is linking this seamless

digital experience to existing content management systems, enrolment systems and CRMs.

• Establishing an in-house innovation Lab/EdTech space should be considered to pilot and test new

technologies. This will develop an internal vanguard of change for the wider organisation to facilitate a more

modern approach to introducing new technology enhanced learning [Kotter 1996].

Changes in Pedagogy

• A coordinated digital-first pedagogy approach across all Faculties when designing courseware and curriculum

will be a competitive advantage in the new era of learning. Few universities have mastered a truly integrated

approach using digital design, adaptive learning, flipped classrooms/hybrid learning, and a sophisticated

learning platform.

• The university sector is rethinking the way it approaches credentials, and assessments – the aim is to digitise,

bring more mobility and validation to the system. Digital badging is relatively new in the university sector but

there is an opportunity to actively participate in this market through collaboration with other universities and

associated partners - to create a badging community, internationally or in the domestic market.

• The increasing demand for shortened educational products and need to have lifelong learning requires the

development of skills-based shorter educational suites of courses (stackable skillset, micro degrees, nano-

degrees ) by all universities. These can be used as pathways for further degree education, customised for use in

workplace learning, or as skills top-ups for existing students or post graduate students. A centralised Digital

Design function to support the development of digital first pedagogy and a more agile product development

process could facilitate this shift into developing micro-masters, nano-degrees, short course credentials.

• Courses that educate citizens for future roles (eg Cybersecurity) and courses that provide future focussed

skills/education to support workplace transition present new market opportunities. Universities’ self-

accrediting system allows them to move faster than other providers.

• Offering hybrid delivery (online and face to face) in a truly flipped classroom model will be the learning of the

future, and has the potential to increase student outcomes by up to 30per cent and reduce delivery costs by up to

10per cent. Academic capability needs improving and courseware need rapid digital transformation in order to

fit into this new model.

New educational models:

• In a new digital era, all universities will need to embark on double transformation where they reposition their

core business but also invest in the future business model.

• Many universities are developing a strategy to establish a deeper Industry Engagement Ecosystem which will

provide competitive advantage. The massive workplace transformation required in Australia following Covid-19,

combined with digital disruption, provides a unique platform for this model in the university sector. The overall

reputation of universities as quality providers of workplace learning and education will hold them in good stead.

This ecosystem moves being projects to a deep partnering model.

OPEN Council Meeting Page 115 of 327

Page |5

• As part of this effort, on-campus, in-residence programmes with companies, and establishing jointly owned

Capability Academies or Innovation Precincts are now taking hold. This will provide a stronger proposition for

future students who will leave university should a better learning opportunity be presented that also has

employment. There is room for a regional university to establish a regional Innovation Academy (eg University

of Maryland) or to develop regional Capability Precincts in partnership with others.

• Many universities are stepping up their B2B and B2G models by providing specific courses created for

workplace learning. There is an opportunity to create a strong, co-creation model with large and medium sized

organisation that includes the co-creation and dual branding of curriculums or white labelling. This is a growth

market.

• A number of universities are investing in the new digital experience. Revamping existing courseware and

legacy LMS systems is commonplace, however, the ability to embed AI, provide personalised learning and

extending the value chain to provide students with direct employment opportunities and add-ons to their

products/degrees is rare. While common in the US (Udacity model), this fully integrated model is yet to be

mastered by a domestic provider.

• A number of sandstone universities are deepening their partnerships with aggregators such as Coursera.

While these institutes enable universities to distribute existing product to a wider market, they now also provide

the sector with an opportunity to source multidisciplinary courses for existing students, curate global content to

reinvigorate existing courseware (eg Duke Model), or white-label their own content for a fee to support other

Coursera members.

• Some more advanced educational institute are looking to the shared economy and gig economy to leverage

improved operational efficiencies. Both trends can be leveraged when sourcing freelancers, hiring out university

venues, conducting digital testing, and seeking insights from analytics.

• The vast majority of universities now have a dedicated Innovation Academy, Digital Lab or Incubator Space

that brings together students and industry to collaborate, innovate, solve problems that can then be

commercialised. Clever collaboration with other universities and industries will be key.

Changing Consumer Demand and Trends

• The modern learner demands seamless and advanced digital technologies to be fully integrated into their

educational interactions. Most students believe that university courses need significant digital transformation.

• There is a recognised 8 second filter for Gen Z when reviewing/considering new universities, and a 4-5 min

attention span when learning. Digital presence and engaging courseware design need to be best-in-class.

• Personalising the student learning journey, collaborating with like-minded brands and providing students

with employment opportunities (projects with companies, internships, volunteering, using AI and algorithms to

match employers with students matching) will provide a distinct proposition to Gen Z learners.

• The need to have continuous lifelong learning, the emergence of portfolio (freelance) careers and the gig

economy are driving the demand for self-directed, affordable, accessible and time critical education. New

segments of learners and new learning propositions will challenge the dominance of undergraduate degree

programs, and continuous learning skills will become part of the mainstream university curriculum.

• Three quarters of Australian businesses are hiring people with different skills and workers need to double their

education and learning by 2040. Universities need to more closely align their offerings with the needs of the

workforce – to attract students, retain existing students and gain more Govt funding.

• When surveyed, students would leave if offered another course that provided employment opportunities and

many students remain unemployed or under employed four months after graduation. Add on employment

services, talent management services need to be part of the end-to-end university offering.

• With international student enrolments dropping, the focus will turn to the domestic market. Diploma, degree

courses are overlapping so there is an opportunity to capture a slice of the vocational market.

OPEN Council Meeting Page 116 of 327

Page |6

1.0 Market Trends and Themes

Online education growth

Higher education is being rapidly transformed by the growth in online learning, with an increasing

number of universities offering degrees online. Propelled by Covid-19, this market trend will continue to dominate

the sector – it is now an essential part of our educational infrastructure and becoming core business.

• The Australian online education market is anticipated to grow at a CAGR of over 8 per cent to $7 billion by

2024. Globally the CAGR is expected to be 7-10 per cent with some analysts predicting the sector will reach

USD$331 billion by 20251.

• In Australia, Ernst and Young found that 22 per cent of current students and 42 percent of future university

students have a preference for the majority of their studies to be delivered online, and 58 per cent of this

same cohort stated that the availability of online study played a role in their university choice.2

• The Grattan Institute found that there has been a 25 per cent increase in the past decade of students

deciding to study off-campus using mobile and PC technologies. In addition, 13 per cent of students

undertake what is known as multi-modal study – taking some course elements online and some face-to-

face.3

• Google’s Online Education Suite now has 100million users globally.4

As the e-learning market evolves, it is also becoming increasingly diversified with new competition, new products,

new teaching models. Current online offerings are trending toward short-term certificates (so-called micro-

credentials or nano degrees) with digital credentials, free offerings (MOOCs) as well as stackable degree programs in

which learners earn an academic credential by completing a self-paced sequence of topics. The learning is

asynchronous (self-paced) and student-centred.

• Globally, 77 per cent of the total education market is self-paced as a result of online education growing in

demand5

• The MOOC market (free online courses) will be worth a total of $60bn globally by 2029 and attracted 350

million enrolments in 2019. Lead by market leaders such as Coursera, edX, FutureLearn, these providers are

now partnering more closely with regional educational institutes to expand their market share. 6

• The digital badging market is expected to reach $291.28mn by 2026, growth at a CAGR of 18.81per cent

from 2019 to 20267. APAC is noted as the best market for future investment and growth in this sector.

The general penetration of mobile phones and internet access has contributed to the growing usage, particularly in

regional locations and among the working population.

• Australia has a mobile phone penetration rate that is the fourth highest in the world - 18.5 million mobile

phone internet accessors in 2019.8 This has resulted in rising demand for untethered access to online

education and post graduate studies where students can more easily fit their studies around busy working

and personal lives.

• The NBN is on track for full rollout by 2020 and will aid this growth by raising the number of internet

connections in regional and remote areas – citizens with this connectivity are twice as likely to enrol in

online education than non NBN connected users. 9 With increased speed of data transfer and a more stable

method of educational delivery, new channels and use of engagement tools such as high definition video

1

Australia Online Education Market By Technology Type, By Provider, By Application Type (Academic, Corporate & Government), By

Region, Competition, Forecast & Opportunities. Research and Markets Report, July 2019. Research and Markets.com.

2 Can the Universities of Today Lead Learning for Tomorrow, Ernst& Young, 2018. Accessed 12 May 2020. Ernst& Young.

3 Mapping Australian Higher Education. Andrew Norton. The Grattan Institute. September 2018.

4 Google Classroom Users Doubled as Quarantines Spread, BloombergQuint, Gerrit De Vynck and Mark Bergen, 9 April 2020.

5 Top 20 eLearning Statistics I 2019. Christopher Pappas. 24 September 2019. eLearning Industry.

6The Global MOOC Market is Forecast to Reach $20.8 Billion by 2023 from $3.9 Billion in 2018 - Analysis by Component, Course, User Type and

Region. BusinessWire, 2 Jan 2020.

7 Digital Badges Market by Offering (Platform and Services), End User (Academic (K-12 and Higher Education) and Corporate (SMEs and

Large Enterprises), and Region (North America, Europe, APAC, and Row) - Global Forecast to 2023 Report. MarketsandMarkets. August

2018.

8 Global Digital Badges Market By Offering, By End Use, By Geographic Scope, Competitive Landscape And Forecast. Verified Market

Research. April 2019.

9 Older Australians fastest-growing online learners. Media Release, 20 August 2018. NBN Connecting Australia.

OPEN Council Meeting Page 117 of 327

Page |7

streaming will emerge. This will also enable students to access personalised cloud networks to study from

home, conduct peer-to-peer learning, or access information from a global academy.

Key Insight

Covid-19 has propelled online learning and is viewed as the tipping point for universities to transition their

business models. Those universities that already have a strong foothold in online learning will be able to move

more quickly to maintain momentum. However, partnering and participating in aggregator models such as

Coursera should be considered in order to achieve scale and growth in an increasingly competitive and global

online education market.

Case Studies: New Online Models

Harvardx HBX is the online platform for Harvard Business School and is a faculty run, experimental

catalyst for improving teaching and online learning. In 2018, revenue grew by 58per cent

showing clear demand for online education.

MITx MITx offers online courses through edX that can be audited to provide students with a verified

certificate from MIT for an extra cost. The model provides self-paced learning, online

discussion groups, wiki-based collaborative learning, online assessments and laboratories. In

2018, MITx shared 111 MOOCs as teasers to their paid degree offerings, with 26 being run for

the first time.

EdEx EdEx is a collaborative organisation of institutes partnering to offer 2,500+ courses to

students globally including MIT, Harvard and Berkshire universities. The platform has 120

institutional partners globally and an offering for business customers. Arizona State Uni is

currently partnering with EdEx to offer all first-year students with free MOOC courses and

students can then “Pay for Your Result” - accreditation for a fee. EdEx invented the

MicroMasters.

Udacity Udacity has over 100,000 graduates and partners with companies to offer online nanodegrees

(demand for which is now 75per cent of their student cohort). Co-created curriculums offer

students a digital badge and employment matching on completion. They have 50 enterprise

clients and half of these are in the Fortune Top 500. Udacity invented the nano-degree.

Lifelong Learning

The need for lifelong and continuous learning is changing the nature of our education sector.

• With the average worker needing to sustain a 50-60-year career over a 100-year lifespan, learners will be

increasingly required to update, refresh and retool to navigate complex career structures. 10

• It is anticipated that the average Australian worker will change jobs 2.4 times over the next two decades,

and 60 per cent will seek a totally new role in a new industry in the next decade. As a consequence, the ‘half-

life of a learned skill today is 5-years’ – ie: much of what students learnt 10 years ago is obsolete and half of

what they learnt 5 years ago is now irrelevant.

• On average, Australians will need to spend 33 per cent more time on education and training across their

lifetime by 2040 which equates to an additional three hours per week on training to keep pace with

workplace changes.

• This ‘skills gap’ within Australia is costed at circa $2bn – the cost to future proof Australia’s workforce

(totalling 600 billion additional hours of education and training).

• The nature of employment is also changing. This is shifting from permanent to casual, and seeing new fields

emerge such as portfolio and gig-workers; presenting universities with new market segments that have

very distinct needs. In Australia, one third of our workforce consists of freelancers and an estimated

700,000 workers moonlight as freelancers whilst also being full time employed.

10 Careers and Learning, Real Time, All the Time. Human Capital Trends Report. Bill Pelster, Dani Johnson, Jen Stempel, Bernard van der

Vyver. 28 February 2017. Deloitte.

OPEN Council Meeting Page 118 of 327

Page |8

These factors combined have spurred a rise in consumers seeking alternative credentials that offer short, low-cost

online courses delivered in bite-sized chunks, that can be stacked together to achieve mastery in a larger concept.

These courses provide learners with a digital certification / badges that show proficiency in particular industries or

knowledge areas, helping them to accredit further learning.

Key Insight

The need to have continuous lifelong learning, the emergence of portfolio (freelance) careers and the gig

economy are driving the need for self-directed, affordable, accessible and time critical education. New

segments of learners and new learning propositions will challenge the dominance of undergraduate degree

programs, and continuous learning skills are likely to become part of the mainstream university curriculum.

The Fourth Industrial Revolution

The Fourth Industrial Revolution is here and represents entirely new ways in which technology becomes embedded

within societies and (in the future) human bodies, with tools such as AI and big data. Examples include genome

editing, new forms of machine learning and intelligence, cryptographic methods such as the blockchain, robotics and

automation.

The main drivers of the Revolution are:

1. Demographic and Socio: 44per cent - changing nature of work, flexible work

2. Technological: 34per cent - mobile internet, cloud technology, big data

The World Economic Forum’s Future of Jobs Report11 found that by 2022/23:

• 133 million new jobs will be created to meet the demands of the Fourth Industrial Revolution.

• 35 per cent of core skills will change. Skills such as emotional and social intelligence, creative thinking,

collaborative, and complex problem-solving tasks will be in demand - skills that machines and automation

cannot replicate.

• This will create new roles called ‘super-jobs’: machine-powered, data-driven roles that require human

support. These skills are required in addition to a student’s technical or academic qualifications.

11 The Future of Jobs Report. World Economic Forum. 2018

OPEN Council Meeting Page 119 of 327

Page |9

The McKinsey Report12 in Australia also found:

• One third of Australia’s workforce will need to reskill to future-proof their employment.

• 50 per cent of companies believe that automation will decrease their numbers of full-time staff and, by

2030, robots will replace 800 million workers across the world.

Education is at the forefront of enabling the workforce to successfully transition to a future way of working and

prepare for thesenew emerging roles. This ‘job transitioning process’ will be the greatest challenge of our time,

according to the World Economic Forum13.

• By 2026, without any retraining, 16 per cent of all displaced workers in developed countries will find

themselves unskilled for current work opportunities, and another one in four will find that they have up to

three potential job transitions to choose from.

• With reskilling, over 95 per cent of displaced workers could move into growing, high income jobs. However,

this requires that 70 per cent of affected workers retrain in a new job “family” or career

• Coordinated efforts by educators, businesses, policymakers are required to mobilise this effort in Australia.

The ability to map pathways for employees and job roles will be key for universities and education

providers to develop new courses, skill sets and products.

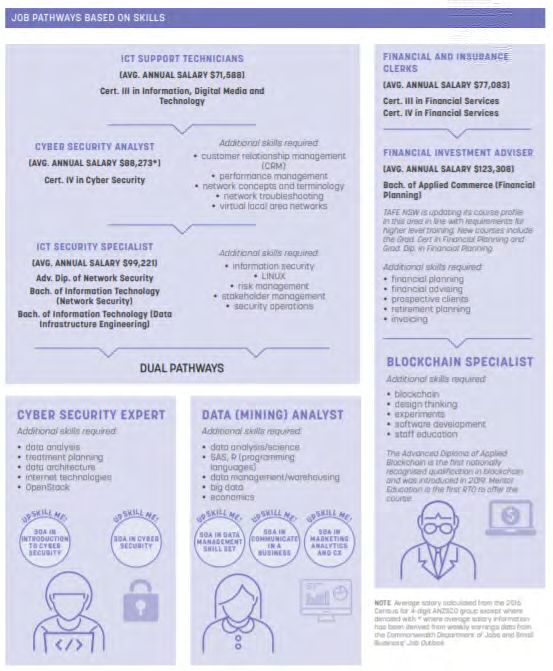

Job Pathways Based on Skills

Whereas traditional pathways programmes focussed on moving a student from vocational training through to degree

qualifications, new pathways focus on moving students based on skill sets. This poses a significant risk to the

university sector.

• Universities will need to adapt to an interdisciplinary system, where they offer a range of relevant skillsets

rather than one specific field. This will require an unbundling of existing products (bite sized content, easily

digestible), introducing new products that are relevant to new skills (mini degrees in emerging areas), and

developing new forms of accreditation (badging), and better aligning their offerings to changes in the

workplace.

• As their own accrediting organisations, universities have a speed-to-market advantage over competing

vocational or private providers. Universities should look to partner with organisations to review the future

of work, and design courses and degree programmes that support organisations as they transform their

workforce and find new talent for emergent roles.

• Faethm and other providers are emerging to work alongside organisations using AI analytics to predict the

impact of emerging technology on any job, workforce, company, industry, location or economy. As a result,

this enables companies and governments to validate and prioritise digital transformation agendas, re-skill

employees for the future, develop better strategies and policies, and make smarter investment decisions.

• In this new world, as per the example below, a Finance and Insurance Clerk can move up the skills chain to

become a Blockchain Specialist without the need for a degree, and an ICT Technician can move to become a

cybersecurity expert or data analyst using skills based training alone.

12 Jobs Lost Jobs Gained – What the future of work will mean for jobs, workers and skills. James Manyika. McKinsey Report. 28 November

2018.

13 The Future of Jobs Report. World Economic Forum. 2018

OPEN Council Meeting Page 120 of 327

P a g e | 10

Educational Pathways based on skill-sets alone

Source: TAFE NSW, Reskilling and Vocational Training Report. January 2020

In this new sector, Ernst & Young identified the following future skillset clusters with the greatest growth (2019):OPEN Council Meeting Page 121 of 327

P a g e | 11

Changes in Workplace Training

With traditional education perceived as being expensive and unable to meet real-time requirements of employees,

there has been a dramatic shift in workplace education. A number of organisations are investing in unaccredited

employee education or co-creating courseware with educational institutes to develop staff capabilities. Moreover,

there has been a marked shift in workplace education away from just digital learning, to experiential learning in the

workplace.

• Globally, this corporate educational market is worth an estimated $31bn with a CAGR of 11 per cent14

• In the online education sector in Australia, non-formal education accounted for 12.4per cent of sector

revenue in 2019, around $632.4 million.15

• Over 48 per cent of all employers in Australia use unaccredited training and 72 per cent use informal

training for their employees, rivalling the traditional use of university education training.16

• The development of specific Capability Academies (eg Optus has developed an in house CX academy) that

offer continuous learning in specific areas and in the flow learning within the organisation is growing.

• Specialist learning precincts are emerging to meet this growing demand. These precincts involve

Government, universities and TAFEs coming together to develop real-time training and education needs (eg

Western Sydney Aerotropolis, Sydney’s Innovation Precinct,

Key Insight

With 50 per cent of organisations in Australia planning to spend more on training in the coming year, there is

already a high propensity to spend in this market. While perceived credibility should give universities a market

advantage, cumbersome and inflexible offerings and higher fees are obstacles that need to be addressed prior to

a dedicated strategic approach being actioned.

Preferred providers – Workplace Training, Australia

Source: Developing the Workforce for a Digital Future. AI Group. 2018.

14 Work-Related Training and Adult Learning. Australian Bureau of Statistics. 2018.

15 Online Education Growth and Market Report. IBISWorld 2019.

16 Unaccredited Training – Why Employers Use it and Does It Meet Their Needs. Ian White, Navinda De Silva. NCVER. 10 December 2018.OPEN Council Meeting Page 122 of 327

P a g e | 12

Case Studies: Workplace Education and Training

Optus Optus CX Academy

This is the first of several strategies to build and improve Optus customer experience and

service outcomes. Partnering with academics and trainers, the academy was born out of a

strategic focus to improve customer experience. The program takes employees through a

variety of customer experience [CX] masterclasses designed to drive the best end to end

experience outcomes for customers. Over 300 employees nationally have been trained on

Lean Process Improvement, Customer Journey Mapping and Human Centred Design. Optus is

planning to have these courses formally accredited and recognised.

RMIT New course to meet demand for DevOps professionals and Launch of the Centre for

Digital Enterprise

Developed in partnership with Thoughtworks and Devops Agile Skills Association (DASA),

the course has been designed to upskill those in technology and management roles looking to

understand the benefits and processes of integrating DevOps within their business. The

Centre for Digital Enterprise is a partnership between RMIT University, Wodonga TAFE and

Sunraysia Institute of TAFE, working together to support both city and regional businesses. It

provides training and support for all businesses wishing to develop their management and

skills for technology in the workplace.

Westpac Westpac launches major new broker education platform

The new Broker Academy has been developed by Westpac Group in conjunction with global

training digital disruptor GO1.com and in consultation with industry partners, including the

Commercial & Asset Finance Brokers Association of Australia (CAFBA) and the Institute of

Strategic Management (ISM). It aims to provide one of the most comprehensive integrated

online learning and business knowledge platforms available to help support finance brokers

in Australia. The online education portal connects brokers with up to 5,000 CPD-approved

courses ranging from compliance, sales, marketing, contract law negotiation, management,

wellbeing and hard and soft skills training.

Australia Post Establishment of AusPost Tech Academy

Following an induction and 12-week technology bootcamp run by Coder Academy, students

will spend two weeks on an operational placement at a mail facility, parcel facility and Post

Office before starting rotations within the Melbourne headquarters.

There are 4 x 5-month rotations over two years. One rotation in the business area offers your

choice tertiary education courses.

Those market areas posing the largest opportunities are medium and large organisations, and state

government agencies.OPEN Council Meeting Page 123 of 327

P a g e | 13

Source: Deloitte Digital, 2019.

2.0 Market Drivers and Opportunities

Today’s student is a highly connected, mobile, and sophisticated online citizen that dictates how educational

providers need to deliver their products and services.

The Domestic Market

When combining population and demographic-driven data, demand for higher education in Australia is projected to

grow by an additional 50,000 undergraduate enrolments by 2020, and 156,000 by 2030. In total, this would see

demand for an additional 81,000 places in 2020 and 219,000 places in 2030.17 The majority of this market growth

and opportunity remains in undergraduate programmes.

Those universities with online operations also have a national footprint, therefore, an opportunity to market to

interstate students exists. In this regard, the largest school leaver populations are NSW followed by Qld and Victoria.

Projections for 2030

Enrolment Growth By State and Age Enrolment Growth by Product

17 Future Demand for Higher Education in Australia. go8Univeristies.OPEN Council Meeting Page 124 of 327

P a g e | 14

Source: ABS (Australian Demographic Statistics, Education and Work Survey). Future Demand for Higher Education in Australia,

go8Univeristies.

Overall, children growing up in regional or remote areas with the same academic ability as their metropolitan peers

continue to be much less likely to attend university due to accessibility issues. There is an opportunity for a strong

online university to spearhead this market and create a superior NSW wide regional educational offering, and partner

to provide students in these communities with internet access.

The micro-degree/skills set/Diploma market presents an opportunity for dual sector universities to significantly

increase their domestic market share. There is a growing overlap in earnings and outcomes between bachelor and

diploma courses and these two categories are beginning to merge – indeed, many universities currently offer

Diploma courses, and TAFE is now offering bachelor degrees that have integrated recognised prior learning units.

There is an opportunity to capture a larger slice of this vocational/Diploma market from vocational providers.

This market segment could provide an opportunity for universities to capture more domestic students, in the wake of

declining international students with Covid-19.

A recent Ernst & Young report18 found that Australian university completion rates continue to fall. The 9-year

completion rate has fallen from 75per cent in 2009 to an estimated low of 66per cent in 2017. This indicates that

almost one in three students who enrol in bachelor and above courses do not complete their studies. There are 1

million university enrolments in 2017 and approximately 357,000 will not graduate in 9 years.

With expected growth in bachelor’s degrees, there is a need to better support low ATAR students attending

universities due to their current failure rates19. A new category of degree course that better supports their ability to

complete is required – eg: micro degrees, nano-degree, stackable skill sets as RPL for degree pathways.

The rate of full-time employment following undergraduate degrees is declining, making degrees less attractive

for students wanting employment immediately after or during their studies. There is a clear mismatch in university

offerings/courses and what the labour market requires. In the past two decades, unemployment and

underemployment for graduates four months after graduation has increased to 28per cent in 2017. This means there

were approximately 63,000 graduates unemployed or underemployed four months after graduation. At the same

time, for most students, employment is cited as a factor in their decision to enrol in a higher education course - for

bachelor-degree students, about 85 per cent give a job-related consideration as their main reason for study.

18The Productivity Uplift from Better Outcomes for our University Students. 18 September 2019. Ernst& Young.

19 Risks and Rewards. When Is Vocational Training a Good Alternative To Higher Education. August 2019. Grattan Institute.OPEN Council Meeting Page 125 of 327

P a g e | 15

The International Market

The international market has been significantly impacted by Covid-19, however, according to Austrade, the onshore

international sector (should it return to normal) could generate up to 940,000 new enrolments by 2025 (which

equates to a compounding annual growth rate of 3.8 per cent). 20China is set to remain Australia’s largest source

market, followed by India and Vietnam.

With the onset of Corona to continue through the next 24 months, growth will slow and the focus will be on growing

in the domestic market. However, there are opportunities when a Post-Covid new norm emerges, as identified by

Austrade in a commissioned report21:

• As developing countries expand their educational offerings in-country, Australian universities have the

potential to support this growth through the provision of online content for licencing fees, with careful

consideration to intellectual property protection.

• There is also an opportunity to capture a slice of the international VET market. The largest VET onshore

enrolments in 2025 are forecast to come from India (16 per cent), Thailand (eight per cent) and South

Korea (seven per cent). Should dual sector universities tap into this market, there is an opportunity to

increase enrolments through the offering of short courses/skill sets /Diploma courses as degree pathways.

• Roughly five million students are studying abroad today and the major driver of student mobility to date has

been unmet demand for higher education in developing countries. A growing number of students in these

countries are choosing to stay within the region to study as a result of Covid-19. As Asia increases its

capacity to absorb students from the region and expands its recruitment of international students, countries

such as Australia may well see demand for places slow, especially from major sending markets such as

China and India. Pursuing greater diversification in international enrolments will become ever more

important. In addition, the number of Chinese university-aged students will be notably smaller 15 years

from now: demographers expect China’s population of 20-24-year-olds to decline by 20per cent from 2010

to 2020.

• Beyond Covid-19, regional mobility schemes are an opportunity for Australian universities to continue to

maintain international momentum. The ASEAN International Mobility for Students (AIMS) programme, the

Erasmus programme in Europe and bilateral mobility arrangements, including Mexico’s Proyecta

100,000 initiative and the corresponding 100,000 Strong in the Americas programme will gain traction.

• International students have an expanding array of educational options that are (a) close to home and (b)

more affordable than those in Australia so a new, collaborative regional model with mobile credentials,

cross-university curriculums and transferrable learning is required. There is an opportunity for Australian

universities to partner with like-minded educational institutes to create more mobility with students, co-

create courses, white label content.

20 Growth and opportunity in Australian international education. Austrade. Deloitte Access Economics and EduWorld. 2016

21 Ibid.OPEN Council Meeting Page 126 of 327

P a g e | 16

Key Insight

Industry Mismatch: There is a mismatch between the field of study and industry demand in the Australian

university sector. In 2018, approximately 43per cent of graduates were not in a job that fully utilised their

education; indicating that this mismatch is an underlying issue. More than half of Australian graduates do

not believe their degree is ‘very important’ for their current employment yet up to 85 per cent of students

choose their university based on it being able to provide employment and career prospects. There is a

market opportunity for a university to provide industry specific degree courses, diplomas or micro-degrees

and link this to a sophisticated employment matching service.

Completion Rates: One in three current students in Australian universities are unlikely to complete and

this is likely to rise given that significant new demand for bachelor’s degrees from low ATAR students.

Developing a suite of micro degree/stackable skillsets on top of existing degree courses, and student

support services such as bootcamps, mental health support, and work placement services should be

considered. Improving student choice is also a contributing factor so providing more detailed career

information as part of an improved ‘entry conversation’ process is required.

Domestic Market: With international markets in decline, the competition for an increased share of the

domestic market will intensify. Capturing a slice of the vocational Diploma market could have merit, as will

the identification of new, interstate market opportunities.

International Market: New and enhanced student mobility and joint-credentials schemes with Asian

partner universities will be key post Covid-19 as more students will opt to learn at home and not abroad.

Given demographic trends, the focus should be on the rising middle class in smaller, developing nations.

The Modern Learner

A study conducted by Deloitte and Bersin22 found the following characteristics of the modern learner:

Overwhelmed, impatient and distracted: The average person spends 25 per cent of their time on emails, checks

their phone 150 times a day and gives content around seven seconds to decide if it’s relevant to them. The average

person spends two hours a day on their smartphone and will only put aside 24 minutes a week for learning.

Keen to learn: The modern learner is keen to be better educated for the sense of personal satisfaction and

achievement it provides. Glassdoor data reveals that among Millennials, the “ability to learn and progress” is now the

principal driver of a company’s employment brand.

Want personalized, timely, quality content: The majority of learning is done in the moment of need and is

expected to be personalised. Google reports that mobile searches that include the term “best” and “____for me” have

grown by 80 and 60 per cent respectively, in the last two years. Students expect providers, including universities to

provide them with customised and personalised services similar to other sectors such as Financial Services. Over 70

per cent of online users will leave portals if they are not optimised for them and their needs. Learners like to learn

anytime and anywhere - 30 per cent learning whilst they travel to and from work and 41per cent opting to learn at

their desks.

Self-paced and workplace learning are highly valued: The majority of students prefer to learn through on-the -job

experience. Collaboration and knowledge sharing also rank highly as a result of turning to others for advice being

more widely available through the use of social networking tools. With respect to classroom learning, while 63 per

cent of students find it a useful form of learning, only 31 per cent find it particularly important or essential. Self-

paced e-learning is considered essential by around 49 per cent of students.

Most value quality, ease of use and relevance in online learning: Students most value quality, ease of use and

navigation, and relevance and timeliness in their online or hybrid study.

22 Leading in Learning. Josh Bersin, Bersin by Deloitte. 29 March 2018. Deloitte.OPEN Council Meeting Page 127 of 327

P a g e | 17

Source: Leading in Learning. Josh Bersin, Bersin by Deloitte.

A Closer Look at Generation Z (1995-2015)

Generation Z students are leading the change in how education and learning is delivered and consumed. They are a

driving force in the innovation of new learning tools as well as teaching styles. They have unlimited access to

resources and are behind universities creating more learner-centric environments, where students become the

directors of their own futures. As the first generation of digital natives, they are familiar with engaging digital

platforms and quick to recognise poor digital design, becoming disengaged by a poor online experience.

According to Ernst & Young23, Australian students would opt out of their degrees if there was another viable, more

relevant pathway to employment and progressing their careers.

• A total of 42 per cent of students say their current degree requires transformation in light of new digital

technologies and disruption in their workplace. This increases to 51 per cent for international students, and

56 per cent for business and management students. The risk to universities is that they become untethered

from industry and continue to offer irrelevant education to equip students for a rapidly changing workplace

in the Fourth Industrial Revolution.

A study conducted by Barnes and Noble College24 shows that today’s students refuse to be passive learners.

• Gen Z are not interested in simply showing up for class, sitting through a lecture, and taking notes that they

will memorize for an exam later on. Instead, they expect to be fully engaged and to be a part of the learning

process themselves. Gen Z students tend to thrive when they are given the opportunity to have a fully

immersive educational experience and enjoy the challenges of being a part of it. Just over half of Gen Z

students (51 per cent) surveyed said they learn best by doing while only 12 per cent said they learn through

listening. These same students also mentioned they tend to enjoy class discussions and interactive

classroom environments over the traditional dissemination of information. There is also a strong preference

towards a collaborative learning environment – this generation of learners are comfortable learning

alongside other students, even outside of their own school.

As a digital generation, Generation Z expect personalised learning and digital learning tools to be deeply

integrated into their education. For them, technology has always been a fully integrated experience in every aspect of

their lives and their view is that education should not be any different.

23

Can the Universities of Today Lead Learning for Tomorrow, Ernst& Young, 2018. Accessed 12 May 2020. Ernst& Young

24 Gen Z: Exploring High Schoolers Expectations for Higher Ed. Barnes and Noble College.OPEN Council Meeting Page 128 of 327

P a g e | 18

• Gen Z believe that universities should be able to seamlessly connect academic experiences to their personal

data to provide personalised experiences.

• Additionally, they expect learning tools to be available on-demand and with low barriers to access. For

them, learning is not limited to the classroom and should be able to be an ‘anytime, anywhere’ activity.

Access to unlimited new information has created a more self-reliant and career driven student.

• In the Barnes and Noble survey, as many as 13 per cent of Gen Z already have their own business and many

are even taking this entrepreneurial spirit to drive changes in university curriculum. Part of this change is

due to the fact that they have more access to more information than the generations before them. By the

time this generation has reached higher education, they are already well versed in current events, music

popular culture, and global trends. They are well aware of the world around them and are already beginning

to think through what their place in it will be.

Gen Z are impatient, like gamification and want organisations to ‘keep it real’

• 47 per cent of consumers research products and services online prior to consuming and when they search,

60 per cent will hang-up if their call is unanswered within 45 seconds. In addition, 42per cent percent of

Gen Z respondents in a recent study said they would participate in an online game for a campaign; 43per

cent would write a product review.25

• 60 per cent of Gen Z shoppers will not use apps or websites that load slowly or are difficult to navigate and

63 per cent of Gen Z members prefer real people to celebrities when it comes to advertisements.26

Gen Z is not only eager for more personalized products but also willing to pay a premium for products that

highlight their individuality.

• 58 percent of consumers say they are willing to pay more for personalized offerings and will also pay a

premium for products that embrace causes they identify with. As we enter the “segmentation of one” age,

there is an opportunity for universities to leverage advanced analytics to improve their insights from

existing student databases27.

Key Insights

Mastering online presence. Nearly half of Gen Z shoppers research their purchases online before stepping into a

store or on a campus and once online, there is an eight second brand filter. Online information, ratings, prices and

student testimonials need to be consistently and easily available online. Partnerships with like-minded brands

will also be well considered by Gen Z.

Digital platforms provide new low-cost ways to individually tailor courses and career information, but more

research is needed to understand how people respond to it and how it can be best delivered to support course

choice. Comparative sites are now starting to emerge in industries such as insurance, travel and home loans. SEEK

is establishing a ‘trip advisor’ online portal to compare educational offerings, prices and service levels (judged by

students, for students).

Personalised learning. More than half of all modern learners indicate a strong desire for adaptive and

personalized learning, 80 per cent like learning at their own pace, and 90 per cent prefer to learn through

collaboration with their peers and tutors. An advanced adaptive learning platform and new approaches to

teaching are required. While some universities offer digital content and connected learning, no university has

developed a fully integrated personalised platform that truly meets the needs of the modern learner.

For Gen Z, price and quality need to align. In the future, different pricing models may need to apply to different

delivery methods, to give Gen Z greater transparency. Repackaging curriculums or de-bundling products will

demand more transparent pricing where instructional access or F2F learning is more expensive than an online

webinar – universities could be forced to adopt this model in the future.

25

Move Over Millennials: Generation Z Is The Retail Industry's Next Big Buying Group. Matthew Shay. Forbes. 12 January 2017

26

What brands need to know about GenZ. Kate Beckman. 17 March 2017. BazaarVoice.

27

Online learning in Australian higher education: Opportunities, challenges and transformations. Cathy Stone. Student Success Volume 10,

Issue 2, pp. 1-11. August 2019.Student Success JournalYou can also read