Toward a Comprehensive Affordable Housing Strategy for Canada - Steve Pomeroy by

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Toward a Comprehensive Affordable

Housing Strategy for Canada

by

Steve Pomeroy

Steve Pomeroy is President of Focus Consulting Inc.

October 2001

ISBN – 1-894598-94-6Table of Contents

Introduction 1

Defining The Problem – The Nature of Housing Need 2

Understanding the affordability issue 4

Shifting factors underlying affordability problems 5

Low levels of new construction 6

Lack of new rental construction worsens problem of affordability 7

Constrained access to affordable units 8

Erosion of the existing affordable housing stock 8

Consolidation – The context for housing policy 8

Responding to the need – Possible policy options 9

Supply Measures 10

Supporting public/nonprofit production 10

Incentives for private rental development 11

Creating a level playing field for rental development 13

Explanation of pooling provisions 13

Reducing development costs 14

Encouraging lower cost forms of development 15

Shifting patterns of ownership and facilitating not-for-profit ownership 16

Demand Measures 18

Rent supplement 18

Shelter allowance 19

Reform of welfare shelter benefits – A transitional shelter allowance 21

Some Concluding Observations – Toward a Comprehensive Housing Strategy 23

Glossary of Terms 28Introduction housing program, but provides a platform for

provinces/territories to add funding in order to

The issue of affordable housing and assist households in need. The Minister stated

homelessness has become increasingly promi- that he will continue to work with his provincial

nent in recent years, highlighted by deaths and territorial counterparts toward longer-term

of homeless individuals on the streets of major solutions.1

Canadian cities and efforts by municipalities and

housing advocates for action by the federal and The purpose of this paper is to present

provincial/territorial governments. an overview of the issues underlying the afford-

able housing problem and to set out a series of

Earlier this year, the federal government options that should be considered as part of a

announced a proposal for a new Affordable comprehensive national housing strategy.

Housing Program. Since then, discussions have

been under way with provinces and territories This paper is structured into four sections:

about program design and cost-sharing. The pro-

posal involves a capital grant of up to $12,500 • In Section 1, the nature of housing need

per unit, with the expectation that the provinces and contributing causes are described.

and territories will match this level. The grants

would be provided to both private and nonprofit • Section 2 describes one set of measures

corporations to help cover the cost of new rental intended to increase the supply of new

development. This investment is expected to housing and related ways to ensure that this

stimulate construction of 12,000 to 15,000 new new supply creates units that are afford-

units annually. able.

Following a meeting of housing minis- • Section 3 presents a similar discussion of

ters on August 16, 2001, the federal Housing ‘demand-side’ approaches – measures

Minister stated that the Canada Mortgage and intended to help households that pay too

Housing Corporation (CMHC) is prepared to much relative to their income better afford

increase the maximum federal grant level, but housing in which they already live.

within an overall budget cap of $680 million over

four years, and to allow the provinces and terri- • Section 4 offers some concluding obser-

tories some flexibility in program design. vations and emphasizes the need for a com-

prehensive policy, drawing from both the

This Affordable Housing Program is supply and demand options to create an

proposed as a short-term strategy, aimed at effective response to housing need and the

increasing new rental construction to address the predominant problem of affordability.

problem of low vacancy rates. It is not a social

Caledon Institute of Social Policy 1Defining the Problem – The Nature of Housing ‘Core housing need’ means that a house-

Need hold is experiencing at least one of three hous-

ing problems, based on established housing

The primary basis for social housing standards. Furthermore, the household has

policy is the presence of circumstances (housing insufficient income to resolve this problem with-

need) in which individuals or families are not out assistance.

able to meet their shelter needs through their own

resources. The appropriate choice of policy The three norm standards used in the core

instruments depends on the nature of the hous- need assessment are:

ing problem being addressed.

• Suitability: This standard uses national

Housing need in Canada has been defined occupancy standards to determine if house-

in terms of adequacy, suitability and afford- holds have a sufficient number of bedrooms

ability. These three problems are the basis for based on the family composition (effectively

the definition of housing need established by the a crowding measure).

federal housing agency, the Canada Mortgage

• Adequacy: A standard that measures hous-

and Housing Corporation, and are used in defin-

ing condition to determine if the dwelling

ing and measuring need by all provinces and ter-

is safe, has basic plumbing and is in a rea-

ritories. This need measure is called core hous-

sonable habitable state of repair.

ing need.

• Affordability: A standard based on a ratio

of housing expenditures to total household

Table 1 income; a household paying more than 30

Core Housing Need 1996 percent of its income for housing is consi-

dered in need.

Total 1,725,655

Renters 1,172,270 68% If a household is found to be below one

Owners 553,385 32 or more of these standards, a second test is

applied to determine if its income is sufficient to

Unattached

Individuals 878,415 51%

afford a suitable and adequate dwelling in its

community within 30 percent of the household’s

Single female 245,950 28 income. This measure uses the median rent of

Single male 149,330 17 an appropriately sized private rental unit and

Living with others 52,705 6 converts the rent to an annual income required

Families

to afford this unit based on spending 30 percent

847,235 49%

of income for rent.2 A household with gross

Two parents with income below this level, and living below any

144,030 17

children

13

of the three housing standards, is defined as

110,140

Couples, no children being in core housing need.

Female lone parent 144,030 17

Male lone parent 16,945 2

1 This formal housing need measure is

Multiple family 8,475

based on data collected by Statistics Canada

Source: CMHC; 1996 Census through the Census and during the intercensal

Caledon Institute of Social Policy 2period through another Statistics Canada survey. In the 1990s, heightened awareness about

Prior to 1996, the Household Income, Facilities homelessness added a new dimension to these

and Equipment database was used; since 1996, housing need categories – absolute homelessness

the Survey of Household Spending has been used and households at risk. To date, there are no

to collect data, but CMHC has not published official statistics measuring the extent of these

updated housing need data since the 1996 Cen- problems.

sus. Thus 1996 Census data remain the most

recent official basis for housing need statistics, Absolute homelessness means living

and are used here to indicate housing need. without four walls and a roof, and perhaps more

important, without a door that one can lock to

CMHC reports that a total of 1.7 million create private living space and security. The

households or 7.6 percent of the total were in number of chronically homeless persons is not

core housing need in 1996. This figure com- accurately known, as there is no easy way to

pares to 1.2 million households or 12.2 percent count this population. Proxy counts of shelter

of the total in 1991. and soup kitchen use as well as efforts by street

workers suggest, however, that this group is

These core need problems are divided growing and becoming more diverse. Home-

almost evenly between unattached individuals lessness is acknowledged as a complex social

(51 percent) and families (49 percent). Single issue – related to mental and physical illness, but

females make up more than one-quarter (28 per- often exacerbated by a lack of access to afford-

cent) of all households in need. able housing and appropriate support services.

Seniors comprise just over one-fifth of ‘At risk’ has emerged as a term in the

households in need, distributed between unat- 1990s to identify families and individuals that

tached individuals and family couples. Among have formal shelter, but whose circumstances are

families, lone parents are the largest category in precarious. They are deemed at risk for one of a

need. range of reasons – the cost of shelter consumes

such a large part of their income that they are

More than two-thirds of households in vulnerable to rent arrears and eviction; they are

need are renters (68 percent), even though renters temporarily living with a friend or relative but

comprise only 35 percent of the population. Most have no permanent place of residence; they are

often, renters experience an affordability pro- personally at risk of physical or mental abuse;

blem; owners in need tend more often to exper- or they have disabilities that may cause them to

ience adequacy problems (e.g., poor condition lose their shelter.

of dwelling).

One measure used to help determine the

Affordability is, by far, the most serious number of households at risk is a very high shel-

problem: 95 percent of core need among renters ter cost burden – paying more than 50 percent of

relates to affordability. Not surprisingly, low income for shelter. In the United States, the 50

income is a key determinant of core need: 85 percent benchmark is used as an indicator of

percent of households with incomes below ‘worst case need,’ also labelled ‘severely bur-

$10,000 and 61 percent of those with incomes dened households.’ These terms have not tradi-

below $20,000 are in core need. tionally been used in Canada, but recent efforts

Caledon Institute of Social Policy 3by advocates to highlight the severity of the Another important factor underlying

affordable housing issue have begun to cite the trends in income and core housing need is the

number of households paying greater than 50 high incidence of households that receive social

percent. In the 1996 Census, some 830,000 assistance. In most provinces and territories,

renters were identified above this benchmark – social assistance benefits include an explicit shel-

22 percent of all renters.3 ter component, which is always more than 30

percent (and often greater than 50 percent) of the

total benefit cheque. Thus these households are

captured under the measure of core need, even if

Understanding the affordability problem

they have been able to obtain housing within the

Clearly, affordability problems are cre- shelter component provided to them.5

ated by a combination of two key factors – low

incomes and high relative rents. With a deep Estimates suggest that more than half of

and lingering recession and slow economic core need households are recipients of social

recovery, the 1990s were characterized by stag- assistance (commonly known as ‘welfare’). The

nant income, especially among renters. Between percentage varies by household type and region,

1991 and 1996, the average real income of renters in part reflecting wide variations in the level of

declined by 12.4 percent.4 welfare benefits.

Incomes have grown since 1996, Recently, analysts and advocates have

although most renters have not shared in the begun to use a shelter-cost-to-income ratio of 50

gains. As higher-income renters exercise the percent as a more extreme indicator of afford-

option of moving into ownership, the renter pro- ability problems. As the shelter component of

file is dominated by the remaining lower-income welfare often makes up as much as 50 percent of

households. the total welfare payments, social assistance

Table 2

Social Assistance Families as Percentage

of All Families in Core Housing Need

Family Lone Parent Non-family Total Non-senior

% % % %

Atlantic 65 87 55 68

Quebec 64 80 68 70

Ontario 46 75 42 52

Prairie 40 54 39 44

BC 37 65 27 38

Canada 49 74 49 56

Source: Statistics Canada, HIFE 1996 data file.

Caledon Institute of Social Policy 4caseloads affect the number of households with The broad measure of renter households

serious affordability problems. paying more than 30 percent also appears to have

declined by 1998, but only marginally compared

Between 1990 and 1995, the number of to the 50 percent benchmark. This suggests

households in core housing need increased by that core housing need may too have declined,

47 percent and the number of households pay- although CMHC has not undertaken an analysis

ing greater than 50 percent of income for rent of core need using the more current data files.

grew by 43 percent. During the same period,

there was a marked increase in welfare caseloads, A more refined measure and data source

associated in part with the 1990 recession and is required to track these important trends –

slow recovery – especially in central Canada. In ideally, one that separately tracks the circum-

March 1990, welfare cases totalled 1,056,000. stances of social assistance recipients and the

The caseload peaked at 1,675,900 in 1994 and working poor (although these are not distinct

in 1995 stood at 1,659,200, a rise of 57 percent groups due to transitions back and forth). The

since 1990 – and a larger increase than the relatively high incidence of welfare households

number of households in core housing need.6 in the core housing need population also sug-

So the rising welfare caseload appears to have gests that solutions should include an exami-

an important impact on housing need statistics, nation of ways to improve this component of

especially in assessing households with a high social assistance programs.

shelter cost burden.

Since 1995, welfare cases have followed Shifting factors underlying affordability

a steady decline, in part due to reduced benefits problems

(e.g., Ontario), more restrictive eligibility

(especially for single people and youth) and the As noted in the first half of the 1990s,

improving economy. Total cases have fallen the primary causes of rising core need were

back below their 1991 levels – from 1,659,200 growing welfare rolls and stagnant income

in 1995 to 1,198,200 by March 2000, a reduc- among lower-income Canadians. Between 1991

tion of 461,000 (28 percent).7 and 1995 real rents declined, although quite

marginally (-2.5 percent), so the primary cause

Reflecting the decline in welfare of increased affordability problems was weak

caseloads, data from the Statistics Canada 1998 income.

Survey of Household Spending indicate that the

number of renter households paying more than The cause of core housing need appears

50 percent of income for rent has fallen signifi- to have shifted through the second half of the

cantly from 830,000 in 1995 to 464,000 house- 1990s and into the new millennium. Since 1996,

holds in 1998. At the same time, the number of increasing rents have become the more important

renters paying between 30 and 50 percent of factor – rising by as much as 25 percent between

income on shelter increased by 250,000 house- 1996 and 2000 in some centres. This percent-

holds – suggesting that while incomes may have age varies across the country, with the largest

improved marginally, possibly as households increases evident in Alberta, Saskatchewan and

moved into work, most are still paying well over Ontario. Rents in Alberta jumped more than 20

30 percent for shelter and continue to experience percent in only three years, while those in Ontario

affordability problems.8 grew by more than 10 percent.

Caledon Institute of Social Policy 5While rising rents in Ontario have been These statistics reveal the important role

identified as a consequence of removing rent played by the private sector in contributing to a

controls, the more important factor in Ontario stock of housing that, over time, has remained

and other provinces has been the persisting low or become affordable. But the stock in this sec-

levels of new supply and the consequent decline tor is also susceptible to erosion. As rents rise

in rental vacancy rates. As the supply of avail- with inflation, the number of private units rent-

able units declines (and fails to keep pace with ing below affordable benchmarks declines. In

population and household growth), the natural other cases, units are demolished or the property

result is upward pressure on rents. This pro- is converted to ownership (condominiums) and

blem is especially apparent in the lower levels the units may no longer be available at moderate

of the rental sector, where low-income house- rents.

holds seek accommodation.

Between 1991 and 1996, the total number

of renter households in Canada increased by

180,000. This figure reflects net growth in rental

Low levels of new construction households, since some moved to ownership, but

this growth was not matched by new production.

The vast majority of housing in Canada During these five years, a total of 111,000 new

has been produced and operated in the private rental units were constructed with just over half

market. The social housing stock – i.e., units of these (54 percent) built as social housing. The

built and operated by public agencies, nonprofit other half, produced for the private sector, were

corporations and co-operatives under various typically at higher rents, far above affordable

social housing programs – accounts for roughly levels. The shortfall in new production (roughly

700,000 dwelling units in a total stock of just 70,000 units) was taken up by vacancies in the

over 10 million dwelling units. Rental housing existing stock, which were relatively higher

accounts for just under four million units, so (nationally almost 5 percent) through the early

social housing constitutes less than one-fifth (18 1990s but declined substantially to a national

percent) of the rental housing stock. overall average of only 1.6 percent (much lower

in some centres).

Some of these social housing units are in

mixed-income projects and provided at market Following a building boom in the late

rent, although most have subsidized rents. The 1980s, the level of private rental development

1996 Census reported a total of 1.6 million units already had slowed by the early 1990s, and pri-

renting below $500 a month (affordable at 30 vately initiated development has continued to fall.

percent of income for households with income New private rental housing construction fell from

of $20,000; this $500 rent/$20,000 income an average of well over 30,000 units annually in

benchmark is used here as a crude benchmark the 1980s to only 13,000 between 1990 and 1995

of affordability to illustrate the relative size of and subsequently to only 6,000 annually from

existing social housing stock and to highlight 1995 to 1999.

recent changes). So social housing comprises

roughly one-third of the existing affordable stock. The 1991 to 1996 period brackets the era

By comparison, two-thirds of affordable units are in which new social housing programs were

in the private rental sector and include older almost entirely eliminated, although completion

apartments (many smaller units) and apartment of projects approved in 1994 and 1995 (Ontario,

suites in homes.

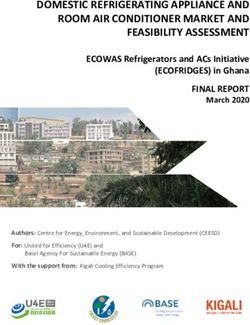

Caledon Institute of Social Policy 6Rental construction and vacancy rates declined through

1990's

30.0 6.0%

Private Social Vacancy

Completions (000's units) 25.0 5.0%

20.0 4.0%

Vacancy Rate (%)

15.0 3.0%

10.0 2.0%

5.0 1.0%

0.0 0.0%

89 90 91 92 93 94 95 96 97 98 99 0

BC and Quebec) stretched into 1996.9 As a the rate of return on investment is poor and un-

result, the decline in private rental construction competitive. Notwithstanding recent increases

was exacerbated by the cessation of social hous- in rent levels, new production of rental units is

ing construction (except a little in BC and Que- not expected to increase in any significant way.10

bec).

Low supply and persisting demand

inevitably applied pressure to rents, directly

Lack of new rental construction worsens exacerbating the affordability problem. This

problem of affordability has become especially acute at the lower end of

the market where there are already far more

This decline in new supply – both pri- households seeking lower priced units than there

vate and social – has been a critical factor are units. As noted, the 1996 Census reported

driving the affordable housing crisis. As rental a total of 1.57 million units renting below $500.

construction has failed to keep up with new In comparison, there were 1.68 million house-

household growth and demand, the rental holds with incomes below $20,000 that can

market has become increasingly constrained. theoretically can afford no more than $500 at 30

Although lower rental apartment vacancy rates percent of income – indicating an absolute short-

and increasing rents are a prerequisite to new fall of almost 110,000 lower rent units.

rental investment, recent analysis of rental

markets has found limited interest in new con- In addition, of the 1.57 million units

struction from developers and investors. Risks renting below $500 per month, just fewer than

to investors and developers remain high while 600,000 of these are occupied by households

Caledon Institute of Social Policy 7with incomes above $20,000. This means that Erosion of the existing affordable housing stock

600,000 lower-income households in need of

affordable units do not have access to the lower While the level of new production is not

priced stock – and must occupy higher priced keeping up with demand and need, and con-

units and pay a larger proportion of their limited strained access contributes to persisting afford-

income for housing. ability problems, this situation is worsened by a

process of ongoing erosion of the existing pri-

vately owned affordable stock.

Constrained access to affordable units Between 1991 and 1996, the number of

rental units renting below $500 declined by

The low availability of modest rent 310,000 (roughly 10 percent of the total rental

units underpins one of the core problems in stock). At a time when new rental construction

the area of affordable housing. The problem is was falling toward an all-time low level, the ero-

not solely an issue of absolute shortage. A rela- sion of lower priced stock is perhaps the most

ted concern is limited access for lower-income serious issue facing the affordable housing sec-

renters. tor. Policy options need to examine ways to pre-

serve this asset.

As a rational entrepreneur, a landlord

seeking to rent out a vacant unit typically will

try to minimize risk – he will prefer tenants

perceived to have greater probability of paying Consolidation – The context for housing policy

the rent. Lower-income households, especially

The preceding section has provided an

those living beyond their means, have a greater

overview of the key issues that underpin the

risk of not paying the rent. Inevitably, they will

affordable housing problem and help to frame

face a greater challenge in securing housing –

the context for which solutions must be sought.

especially if due to their inability to pay high

In summary:

rents, they previously have been evicted or are

in arrears and do not have a sound reference. • Low levels of new rental investment and

production (and limited investor interest).

In a tight rental market in which there are CMHC projections of household growth

few units available and landlords can be selec- indicate a requirement of 45,000-50,000

tive, tenants with good jobs will tend to be pre- new rental units annually through the next

ferred. While there is a fine line between pru- decade to meet new demand. This com-

dent landlord behaviour and discrimination, the pares with current production of less than

bottom line is constrained access for low-income 9,000 annually.

tenants, especially those stereotyped as ‘poor

tenants’ – which often includes social assistance • Erosion of the existing lower priced rental

recipients and lone parents with children. One stock. Between 1991 and 1996, in excess

way to address this issue is by facilitating non- of 300,000 units renting below $500 were

profit acquisition and increased ownership of this lost due to rent inflation, conversion and

existing stock, as nonprofit landlords will tend demolition.

to be more sympathetic to needy households.

Caledon Institute of Social Policy 8• A ‘crowding out’ effect in which house- lower). These measures include direct pub-

holds that are employed and otherwise per- lic or nonprofit production, measures to lower

ceived by landlords as less risky tenants the costs of production and stimulative meas-

are occupying modestly priced units, lead- ures to induce private production with con-

ing to constrained access to the lower rent ditions on the level of rents.

part of the market for working poor and

welfare households. 2. By increasing a household’s ability to pay

(i.e., increasing or supplementing its income).

• Very limited funding to support new These are referred to as ‘demand-side meas-

social housing initiatives. Most provinces ures’ as they affect the household’s effective

followed the federal cut in 1993 and there demand. Such measures include rent sup-

has been no funding for new development plements or allowances and income assist-

outside of small programs in BC and Que- ance.

bec.

3. A third approach involves measures to influ-

• Predominance of affordability problems

ence the price of existing rental housing. It

due to both low and stagnant income and

includes controlling rent levels to protect

rising rents. Low income was the main

affordability, diverting demand (e.g., by help-

cause in first half of the 1990s; rising rents

ing households buy a home) to reduce pres-

have become the more significant factor

sure on a limited rental sector and capturing

in the second half of the 1990s.

the existing affordable stock by encouraging

• A high proportion of welfare households a transfer in the ownership from private-for-

among core need households affects both profit owners to not-for-profit owners. These

the total count of core need households and approaches have a more limited scope and

possible solutions. are not discussed in any detail, except where

they relate to the two main categories.11

The following potential approaches are

discussed in the next two sections. Each meas-

Responding to the need – Possible policy

ure is first outlined and key terms are explained.

options

The advantages and disadvantages of each

The goal of social housing policy is to measure are then reviewed. The concluding

assist low- and moderate-income households to section of the paper considers the potential

obtain adequate and suitable housing at a price integration of these measures into a compre-

they can reasonably afford. This goal can be hensive strategy.

achieved through two general approaches:

1. Supply measures

1. By reducing or subsidizing the construction

cost of housing so that it is inherently more • Direct support for public/nonprofit pro-

affordable. This approach typically involves duction

actions related to production and accordingly • Incentives for private rental unit devel-

are labelled as ‘supply measures’ (i.e., the opment

primary focus is on influencing the cost of • Creating a level playing field for rental

building so that the rent charged can be development

Caledon Institute of Social Policy 9• Reducing development costs • Typically, operating agreements and any

• Encouraging lower cost forms of devel- ongoing subsidy match the amortization

opment – single-room occupancy, sec- period of the mortgage. Once the mort-

ondary suites gage is fully paid off, the project rents are

• Shifting patterns of ownership (facilitat- required only to cover operating costs and

ing nonprofit ownership). it is assumed that even at low rents, the

operator will be able to continue serving

2. Demand measures lower-income households (in very poor

100 percent targeted projects, this may not

• Rent supplement be feasible with some renewal of subsidy).

• Shelter allowance

• Reform of welfare shelter benefits. • In most nonprofit approaches, ‘affordable

rents’ are established on a rent-geared-

Each general set of approaches, and the to-income (‘rgi’) basis. Although earlier

individual measures in each set, are not mutu- programs used a 25 percent ratio, most cur-

ally exclusive. There are many cases in which rently employ a ratio of 30 percent against

supply and demand measures can effectively gross income.

complement each other. This complementarity

is examined within each approach. • Assisted projects may be fully targeted –

meaning that 100 percent of tenants have

lower incomes and pay rent on a rent-

geared-to-income basis – or mixed income

Supply Measures (where some portion of units are rented at

market rent levels, rather than at subsidized

Supporting public/nonprofit production

rents based on a percentage of income). A

Direct public supply of housing has been mixed income approach generally is pref-

the predominant program response in Canada erable as it avoids the concentration of very

through the postwar period. Although various poor households that was characteristic of

program designs have been employed, the essen- earlier public housing and contributed to

tial elements of this approach include: the stereotyping of projects.

• A public or not-for-profit owner/operator

with a specific mandate to operate hous- advantages

ing for low-income households.12 Nonprofit production helps create a per-

manent stock of units specifically to serve lower-

• Some form of subsidy, either as a capital

income households – a long-term investment in

grant, favourable mortgage rate or ongo-

a permanent asset. This form of ownership also

ing subsidy, so that the rents charged to

provides some assurance that rents will remain

tenants are affordable. Generally, the

affordable over the long term.

project is governed by an operating agree-

ment that specifies the obligations of the

Even after operating agreements and sub-

operator and requires the provider to con-

sidies cease, the public investment remains in

tinue serving lower-income eligible house-

place as the nonprofit charter restricts ongoing

holds.

Caledon Institute of Social Policy 10use to provide affordable housing and most ing involve long-term (35-year) subsidy commit-

nonprofit providers retain this initial motive. ments. As new commitments are layered on in

each year, the subsidy cost mounts exponen-

Nonprofit programs address both supply tially. This problem raises the concerns of

issues and affordability within a single program, finance officials and makes these programs a vul-

which is one reason why they appear to be quite nerable target in times of fiscal restraint.

costly, compared to alternatives that seek to

address only one issue (either supply or afford- The alternative is to ‘front-end’ the

ability). cost with a capital grant. Again, however, this

option tends to be expensive due to the high cost

It is possible, however, to separate the of new development compared with relatively

supply and affordability objectives. One such low revenues at rent-geared-to-income rents (the

approach involves using a nonprofit organi- latter limit capacity to cover operating and mort-

zation to develop housing at market rent level, gage payments).

then stacking rent supplement assistance

(described below) as a separate mechanism to Income mixing improves the viability of

specifically address affordability. the projects and lowers the average capital grant

requirement. But it increases the grant cost per

Another variant is to assist nonprofit rent-geared-to-income household assisted.

housing corporations to purchase existing pri-

vately owned rental properties. This approach Relative to the volume of housing need –

does not add to new supply, but it does ensure more than one million renters in core need and

that long-term affordability is preserved and more than 450,000 paying more than 50 percent

helps stem the ongoing erosion of the relatively of their income for housing – incremental new

more affordable existing private rental stock. supply programs can assist only a very small

number of households in need (at their peak,

Supply programs respond directly to low nonprofit programs produced only 25,000 to

levels of production (as prevail currently) and, 30,000 units annually).

in so doing, have a beneficial effect in moderat-

ing the inflationary impact of low supply (i.e., in

the absence of new construction, there is pres-

sure on rents in the existing stock). Incentives for private rental development

Through the development process, units In building new rental housing, a devel-

can be designed specifically to meet particular oper is faced with a range of costs and, in return,

needs – e.g., accessible or supportive housing. creates an asset that generates a cash flow in the

New supply funding can be geographically tar- form of rents. The value of the property to a

geted to markets with acute supply problems. potential investor is determined not by its cost

but by the level of revenue it can generate. The

market value of the new property is based on the

weaknesses value of future income flows.

New construction costs and the associated In the same way that an investor in gov-

subsidy costs tend to be quite high on a per unit ernment bonds is prepared to pay a price for a

basis. Most recent versions of nonprofit hous- bond based on an expected rate of return, the

Caledon Institute of Social Policy 11rental investor converts future income to a cur- Currently, potential rates of return on

rent price based on a similar expectation of an modest rental housing have been estimated to be

annual return on his equity. The main differ- less than 5 percent, compared with a minimal

ence is that a government bond is a secure expectation of 12 to 15 percent. Increasing a pri-

investment, easily traded for cash and the annual vate investor’s rate of return to this level likely

interest payments are guaranteed. For the rental will require a capital grant or interest-free deferred

investor, the asset is more difficult to trade for loan in excess of $15,000 to $20,000 per unit;

cash; it must be listed for sale and await a will- this amount will vary significantly between cit-

ing buyer. In addition, the annual cash flow is ies and depend on the type of unit being devel-

not guaranteed. The property may experience oped.

vacancies with no revenues produced or regu-

lations (such as rent controls) may be introduced

or modified and thus constrain the ability to advantages

increase rental income and achieve anticipated

cash flows. Any type of new supply can have a bene-

ficial effect in releasing the pressure of low sup-

Compared to alternatives, rental invest- ply. Even new development at the higher end of

ment is relatively high risk and, as such, demands the rental market will draw some households out

a much higher expectation on rate of return. The of lower priced stock (a so-called ‘filtering’ or

critical issue in the rental market is that the rates ‘trickle down’ effect).

of return remain far below those expected by

potential investors. Costs are too high relative Household growth and new demand cover

to potential rent revenue, mainly because the a spectrum of incomes, including higher-income

costs of production are set outside of the rental households. Without new development, these

sector. Ownership housing and condominiums households occupy lower priced units and crowd

establish land values while construction labour out lower-income households.

costs and materials are established in the wider

market that includes commercial development. Depending on the development econom-

ics in a particular city, stimulus measures lever-

In the past, stimulus programs have been age private investment and will cost less than

used to encourage private development. These assisting nonprofit development (since, unlike

include programs that provide a grant or inter- private developers, nonprofits typically have lit-

est-free loan to a developer in return for mod- tle, if any, equity to invest).

estly designed units (which should command

lower rents than luxury development) and tem-

porary tax measures that provide favourable tax weaknesses

treatment to investors (namely, creating eligible

costs that can be used to reduce taxable income). Stimulus measures have been controver-

sial. Even the housing industry has argued that

Effectively, these programs replace some this type of intervention creates an artificial stimu-

portion of the investor’s own equity with gov- lus and disrupts market equilibrium, taking many

ernment funds without affecting the rental rev- years to rebalance.

enue. So the investor’s rate of return increases

to a level that can make development more The expenditure does not create perm-

attractive. anent affordable housing, although it can be

Caledon Institute of Social Policy 12designed to do so through certain conditions in Explanation of pooling provisions

exchange for the assistance.

When a rental project is sold, investors

Once operating agreements enforcing must pay tax on the difference between the sale

the conditions and targeting expire, the units are price and the depreciated value of the project –

no longer available as affordable housing (the i.e., the original cost of the project less the Capi-

so-called ‘expiring use problem’). tal Cost Allowance (CCA) deductions. ‘Recap-

tured depreciation’ (the difference between the

No long term public asset is created in depreciated value – which applies only to the

return for the government investment. building, not to the land – and the original cost)

is taxed at full income tax rates. Capital gains

taxes apply to the increase in value above the

original cost.

Creating a level playing field for rental

development Prior to 1972, rental investors could

defer paying income taxes on recaptured depre-

The poor economics of rental investment

ciation on buildings sold by ‘pooling’ the recap-

are attributable, in part, to the current tax treat-

tured amount with CCA from other buildings.

ment of rental housing, which is seen as unfair

For example, if they acquired another rental

compared with other sectors and investments.

project in the same year, they could avoid

recaptured depreciation by transferring the

Current inequities in the tax system

excess CCA to reduce the depreciable value of

include:

the newly acquired project.

• GST on rental housing. Rental landlords

The restoration of pooling (also called

cannot charge GST on rents, yet unlike

‘roll-over’) does not eliminate tax liability. It

other goods, rental housing is not zero-

simply postpones the tax penalty on recaptured

rated. So landlords pay GST on supplies

depreciation and capital gains for owners of

and services but cannot claim input tax

rental properties who invest the proceeds in

credits as they do not collect GST and have

another rental property. Thus restoring this pro-

no GST remittance against which to claim

vision creates opportunity for existing investors/

credits.

owners of fully depreciated properties to lever-

age the existing assets without facing large tax

• Small rental investors are not currently

impacts.

considered as ‘small businesses’ and there-

fore are not eligible for the lower small

Ironically, in some cases it is more bene-

business tax rate on the first $200,000 of

ficial from a tax perspective to demolish the pro-

income.

perty and thereby eliminate the recapture of

depreciation. Under this approach the existing

• Elimination of ‘pooling’ provisions that

units, which may be relatively affordable, are

previously encouraged reinvestment in

lost.

new rental projects.

Caledon Institute of Social Policy 13advantages housing in a typical urban center will cost in the

range of $65,000 to $105,000 for one-bedroom

These three possible measures could cor- apartments and from $90,000 to $160,000 for

rect inefficiencies in tax treatment and, while three-bedroom family units.

imposing an expenditure on government, do not

constitute a temporary disruptive measure – Land costs generally will account for 15

unlike short-term stimulus measures. to 30 percent of the cost. In most markets, land

values are established by the more dominant con-

The measures may improve after-tax fea- dominium market (ownership apartment) and

sibility of new production (at least for higher rent rental developers typically are unable to com-

properties) and can stimulate new construction pete against condominium development for land.

with a positive moderating impact on the mar- Land is zoned based on use (e.g., residential) and

ket, thus easing rent pressures. density (units per hectare or as a ratio of the total

site area); land cannot be zoned for tenure. Pro-

Most tax measures would apply only to vincial enabling legislation to empower munici-

private developers. However, any reduction in palities to bonus densities specifically for rental

GST also would benefit nonprofit providers. development could help to address this situation.

Such a provision could increase density for rental

(compared to condominium) use so that the net

weaknesses residual value of the land, per unit, would equate

to the values created by lower density condo-

Federal finance officials have strongly minium development.

resisted expanding tax expenditures and are

reluctant to implement tax changes unless a clear Labour and material costs are established

case can be made on equity grounds. in a competitive market place. Currently, a

booming construction industry in many parts of

These measures have a direct impact upon the country has resulted in shortages of both

the production of affordable housing but may labour and materials with an inevitable upward

stimulate market rent development at higher rent pressure on prices. An affordable housing stra-

ranges. tegy with a long-term vision might seek to direct

assistance on a countercyclical basis, supporting

development in markets that are in a downturn

to take advantage of lower input costs and to help

Reducing development costs offset the costs of an underutilized labour force

(e.g., lower income tax revenues and higher

One of the most critical issues confront- Employment Insurance payments).

ing both private and not-for-profit development

is the relatively high cost of producing new hous- Finally, the trend over the past two

ing, which is a function of land costs, labour and decades has been toward a pay-as-you-go

material costs. Total development costs also have approach to funding the cost of municipal

been increasing as a result of layers of taxes and infrastructure related to new development rather

fees on development. than covering this expense from general pro-

perty tax revenues spread across all existing

While costs vary across the country and development. This practice has resulted in the

depend on the type of development, new rental imposition, by municipalities, of development

Caledon Institute of Social Policy 14cost levies on new construction. Concurrently, Encouraging lower cost forms of development

the GST added another new cost to development

and has carried provincial sales taxes with it in Another way to address the relatively

the Atlantic region where federal and provincial high cost of new development is to encourage

consumption taxes are harmonized. alternate, lower cost building forms.

Two such options are secondary suites

advantages in single detached homes (which are already

being created but often in contravention of local

Measures to lower land costs for rental building regulations) and small unit or ‘single

housing and development charges can have a room occupancy’ (SRO) accommodation.

critical impact in reducing the cost of new

development. A number of municipalities already The formal approval and explicit encour-

have waived development fees for certain hous- agement of secondary suites is a controversial

ing types and, in certain areas such as the inner option in many municipalities. Such suites have

cities, as a mechanism to encourage residential been created in basements or by subdividing the

development in the core and minimize suburban upper floors of existing homes. Distinct from a

sprawl. rooming house, secondary units typically are

created in a home in which an owner occupant

Reduced fees and charges will help to is also resident so there is close management of

encourage private development and new supply tenants (unlike an absentee landlord). The most

while also marginally narrowing the development bothersome issue from neighbours’ perspectives

cost gap faced by nonprofit organizations seek- is the absence of on-site parking and the result-

ing to build. ing use of limited street parking space. The con-

cern from municipalities is one of health and

safety. Often suites are self-built and have not

weaknesses benefited from a permit process that requires

inspections to ensure that the units are safe

Without other complementary measures, (especially regarding electrical wiring).

these cost-reducing approaches will not lower

costs sufficiently to enable development to be Some municipalities have sought to

viable at affordable rents without some subsidy. legalize secondary suites, but few have expli-

Even with free municipal land, nonprofit devel- citly promoted this use either through encourag-

opment for lower-income households is not ing statements in official plan policies or through

viable without additional subsidy. small grants to existing owners. A demonstra-

tion project under Homegrown Solutions (a fed-

Requiring municipalities to lower or erally funded seed grant program administered

remove development costs eliminates municipal by the Canadian Housing and Renewal Associa-

revenue and requires the municipalities alone to tion) did provide funding to the town of Sidney,

shoulder the burden of new development, while BC, for a small homeowner grant of $5,000 to

the province and federal government gain income help offset installation costs of an adaptable suite

tax revenues from the construction labour and for a person with physical disabilities.

ongoing operations (if for-profit).

Caledon Institute of Social Policy 15The SRO approach involves development There are few proponents pushing this

of very small bed-sitting rooms, which gener- approach. It is a new concept and, as such, even

ally range in size from 150 to 300 square feet (a more risky than conventional rental, for which

typical bachelor/studio suite is usually 350 to 400 there remains limited investor appetite.

square feet). Well-designed small suites can pro-

vide cost-effective options for urban singles and

have become popular in a number of US cities.

Given that almost half of core need households Shifting patterns of ownership and facilitating

are low-income single individuals, this building not-for-profit ownership

form potentially could respond to significant

demand. Much of the effort of the nonprofit hous-

ing sector is focussed on building new housing.

SRO type development can be cost- Without subsidies, the costs are prohibitively

effective since the total floor area per suite is high and, even with subsidies, the subsidy

much less than that required in a typical bach- requirements per unit remain significant.

elor or one-bedroom apartment. Few residents

can afford to own a car, so parking requirements In other sectors, where poverty similarly

and costs can be reduced when located in areas limits access to necessities, the solution is to seek

served by public transit if municipalities agree lower cost options. Food banks provide food at

to this regulatory relaxation. A study for the no cost, and used clothing stores make available

Ontario Ministry of Housing in 1999 found that clothing at affordable prices. If lower-income

suites could be developed in large urban centers households can afford a vehicle, or must have

at a cost of 40 to 50 percent of the typical new one for transport to work, most lower-income

one-bedroom unit. households also drive older used cars. While

many households seek housing in the older

existing rental stock, the practice of drawing upon

older depreciated assets is not frequently utilized

advantages

by nonprofit providers, even though a large hous-

Alternate building forms such as second- ing stock already exists and properties often are

ary suites (apartments within homes) and SRO provided for sale – typically at values far below

units have significant cost advantages and can the cost of building new.

effectively augment more traditional building

forms. This dismissal of property acquisition as

an option is, in part, a legacy of former nonprofit

These approaches could stretch any lim- programs. A number of nonprofit housing pro-

ited subsidy funds further since per unit costs viders did pursue acquisition/rehabilitation, and

are lower. typically expended more than the cost of build-

ing new because the properties were in serious

state of disrepair. Few providers went out to find

a reasonably sound 20- to 30-year-old apartment

weaknesses that needed merely minor repair and painting.

The second factor that acted to preclude this

Regulatory barriers and neighbourhood

option was that the social housing funding pro-

resistance (‘Not In My Backyard’ or NIMBY)

grams required all tenants to be in core housing

may limit opportunities.

Caledon Institute of Social Policy 16need, with incomes below specified thresholds. In lower cost markets – such as Prairie

It was problematic to acquire buildings that cities – existing detached homes can be acquired

already were occupied with some tenants not in for as little as $20,000 to $30,000. Some com-

core need, as this would require evictions. So munities are exploring options for purchasing a

providers avoided this option. portfolio of existing homes as a rental portfolio

instead of constructing new buildings.13

Far more multiple unit rental properties

are sold each year than the number of nonprofit This acquisition approach also can pro-

units that were constructed by the programs of vide opportunities for lower-income households

the early 1990s. Although not all properties will gradually to become homeowners. A critical

be appropriate, due to poor condition or high element of an assisted ownership program is

price, a significant number of existing proper- counselling and ongoing mentoring as well as

ties are regularly transacted (and this could be linkage to employment and human resource train-

increased if rollover provisions of the tax sys- ing to enhance employability. Despite low house

tem were revised as discussed under a separate costs, these lower-income households generally

option above). Tax reform would encourage would be unable to qualify for a mortgage, even

existing owners to sell to nonprofit buyers with- though the ongoing ownership carrying costs

out incurring significant income tax impacts and may be less than paying rent on an apartment.

would provide a source for selective acquisition With modest assistance – such as nonprofit

by nonprofits. mentoring, a loan guarantee and a modest down

payment grant of up to $7,500 – low-income

Currently, as these properties are offered households can be assisted in obtaining a home

for sale, new private investors (including insti- of their own with no ongoing subsidies.

tutional investors and Real Estate Investment

Trusts or REITs) are the purchasers. Typically,

new investors upgrade the property with the advantages

intent of increasing the rental cash flow and

these acquired properties move beyond afford- The primary advantage of an acquisition

able levels. The alternative – purchase by non- approach is the relative cost effectiveness of the

profit organizations – effectively can preserve properties, compared with new construction.

and potentially expand the remaining stock of

housing that is relatively affordable to lower- Because the properties already exist, pur-

income households. With nonprofit providers, chasers do not have to contend with NIMBY type

access to lower-income households would be challenges.

improved as they no longer would be competing

against ‘better’ higher-income tenants. Acquisition permits the retention of an

existing mix of market tenants while slowly

Any such nonprofit acquisition will introducing lower-income tenants on unit turn-

require some subsidy, ideally a capital grant to over. Acquisition with existing tenants remain-

facilitate down payment. But because the total ing can effectively facilitate a mixing of income

cost per unit typically is much lower than build- without added cost (since market rents cover

ing new (40 percent to 50 percent lower), the breakeven rent).

grants can be more effectively used and stretched

to secure more units.

Caledon Institute of Social Policy 17Homeownership and scattered rental port- scale to tackle the large backlog of these pro-

folios offer options to access existing rehabili- blems. Some form of rental assistance is neces-

tation programs to upgrade dwellings. sary to address the affordability gap.

This section describes two alternative

weaknesses program approaches to assist households facing

affordability problems – rent supplements and

There appears to be reluctance on the part shelter allowances – as well as a variant on shel-

of many providers in the nonprofit sector to pur- ter allowances applied to existing welfare bene-

sue acquisition. Most prefer new construction, fits.

as they are concerned with adding to the supply.

The acquisition option is limited by the

Rent supplement

availability of properties offered for sale on the

market and requires careful selection and assess- A rent supplement approach involves an

ment of potential properties. agreement between a public funding agency and

a landlord in which the landlord agrees to enter

The option is well suited for market down- into contracts to provide rental units for low-

turns. The best window for an acquisition income tenants on specified terms. Usually, the

approach in many cities already may have passed, tenant’s out-of-pocket rent will be based on a

as currently the rental market is under high pres- rent-geared-to-income basis. The contract will

sure from low vacancies and rising rents (which make up the difference between the tenant-paid

tend to raise the value of existing properties for rgi rent and the actual market rent on the units.

sale). During the term of the agreement, there may be

an inflationary index to allow the market rent to

increase annually, increasing the landlord’s rental

income but leaving the tenant protected at the

Demand Measures

rgi rent. As assisted tenants leave, during the

The brief overview of housing need term of the agreement, the funding agency has

highlighted the predominance of affordability the right to place a new low-income tenant into

problems. Low-income households cannot find the unit.

housing at low enough costs (rent) to match their

low income and 90 percent of core need problems Rent supplements are dependent on

are related to affordability. In 1998, more than securing the interest of private landlords. How-

1.5 million renter households paid more than 30 ever, there is a poor history of rent supplement

percent of their income for housing and roughly success in most provinces, despite efforts adver-

500,000 paid more than 50 percent [Statistics tising for landlords to participate. Even for pro-

Canada Survey of Household Spending]. perties for which rent supplements have been

negotiated, many landlords have elected not to

While supply approaches can play an renew these contracts when terms expire. Initial

important role in moderating the market pressures terms for agreements in the 1970s were gener-

that exacerbate affordability problems, supply ally for 15 years with renewals now usually on a

initiatives cannot be implemented on a sufficient 3- to 5-year term.

Caledon Institute of Social Policy 18In cities with low vacancy levels, which It can be stacked on nonprofit supply but

currently predominate in much of the country, focussed only on the affordability issue (sepa-

landlords generally can fill their buildings with rate from supply).

private market tenants, without the difficulties

related to having their tenants selected by a third Over the long run, it is more cost-effec-

party. In addition, administrative requirements tive to stack rent supplements on nonprofit hous-

associated with this approach generally are seen ing as the annual rate of increase in nonprofit

by landlords as a deterrent. Thus, there may not break-even costs has been found to inflate more

be significant opportunities to use and retain rent slowly than market rents.

supplements as a means of providing assistance

to low-income tenants living in privately oper-

ated rental housing. weaknesses

While there are difficulties in applying a A rent supplement does not address lack

rent supplement program in the private market, of supply.

there has been a long tradition of stacking rent

supplements on nonprofit projects. The options is dependent on a willing

landlord and available units – but few landlords

A number of existing older nonprofit are interested.

projects are not rgi based, but include units

Lack of renewal at term can result in dif-

with rents slightly below market levels. This

ficulty for existing tenants.

approach facilitated either by a capital grant or

a favourable mortgage rate that helped to lower

Historically, there has been low landlord

the breakeven rent below market levels. Allo-

take-up of rent supplements due to administra-

cating rent supplements to these units to allow

tive burden and to restricting use and rent on the

rgi assistance to tenants with very low incomes

contracted units.

could provide a low-cost rent supplement option;

over time, breakeven rents will not rise as

quickly as market rents.14

Shelter allowance

A further option is to utilize a rent sup-

plement program in conjunction with nonprofit Unlike a rent supplement in which the

acquisition of existing properties. This option is landlord is implicated directly in a formal agree-

discussed in the next section on preserving and ment, shelter allowances are direct payments to

expanding the affordable housing stock. the tenant and, as such, overcome the necessity

to negotiate agreements with landlords.

advantages A feature of shelter allowances, as

opposed to both rent supplements and social

This option addresses affordability pro- housing supply programs (in which the number

blems. of units is limited by the size of the existing stock

and any new production), is that all tenants who

A rent supplement agreement is specific are in need and eligible for assistance potentially

to contracted units, so thier condition and qual- can receive it. There would be no waiting lists

ity can be verified. (and unmet need) with shelter allowances. This

Caledon Institute of Social Policy 19You can also read