The Tasmanian housing market: update 2020-21 - Jacqueline De Vries, Maria Yanotti, Julia Verdouw, Keith Jacobs and Kathleen Flanagan. Housing and ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Tasmanian housing market: update 2020-21 Jacqueline De Vries, Maria Yanotti, Julia Verdouw, Keith Jacobs and Kathleen Flanagan. Housing and Community Research Unit, University of Tasmania June 2021

Contents Key Findings 1 Introduction 4 1. Market trends 6 Property values 6 Home buyers 10 The rental market 12 Summary 14 2. Incomes and housing costs 15 Rental affordability 16 Purchase affordability 17 Summary 17 3. Demand and supply drivers 18 Changes in demand 18 Components of population change 18 Local variation 20 Projections of future demand 20 Changes in supply 21 Building approvals 21 Building activity: commencement, construction and completions 23 The demand-supply balance 24 Summary 26 4: Short-stay accommodation 27 Listings 28 Property use 30 Summary 32 5. Housing insecurity and homelessness 33 Social housing 33 Homelessness 36 Summary 38 Conclusion 39 Acknowledgements 41 References 41 2 University of Tasmania

Key Findings

• By March 2021, Hobart dwelling values had increased

Tasmania’s housing market continues 12.5 percent in the preceding 12 months, and by

3.3 percent in the previous month alone. Dwelling

to be under extreme pressure. values across the rest of Tasmania had also increased

Despite some localised fluctuations by 15.3 percent and 2.3 percent respectively.

linked to the effects of COVID-19 • New loan commitments to owner-occupiers had

restrictions, house prices and rents increased by 11.5 percent to $307.5 million in the

remain high, while the private rental December quarter of 2020. By February 2021, loan

commitments to owner-occupiers had reached

vacancy rate remains very low. $334.6 million. Loan commitments to investors

had increased by 51.8 percent to $98.5 million in

December quarter of 2020.

• Loan commitments to first home buyers rose

85.2 percent over the 12 months to October 2019 by

October 2020 were at their highest level since their

post-GFC peak in 2009.

• Only 23.0 percent of loans to owner-occupiers are

to construct new dwellings or purchase newly built

dwellings. This is, however, a higher proportion

than previously.

• In March 2021, the median rent in Tasmania was

$400 per week for a three-bedroom house, up

6.7 percent since March 2020. The median rent for

a two-bedroom unit was $360, up 20.0 percent

since March 2020.

• The private rental market vacancy rate was

1.9 percent in March 2021.

• According to the 2020 Rental Affordability Index,

There are significant affordability Greater Hobart remained the least affordable capital

city in Australia relative to income, and the rest of

challenges across the state due to Tasmania is the least affordable region of the other

continuing low wage growth and ‘rest of state’ areas considered.

relatively static income support

payments. The temporary alleviation

from the coronavirus supplement to

selected income support payments

has now ended and many income

support recipients are again living

below the poverty line.

The Tasmanian housing market: update 2020-21 1

• In the year to June 2020, the Tasmanian population

Border closures associated with had increased by 1.1 percent. Much of this growth

was from interstate and international migration,

COVID-19 have disrupted migration which is now restricted due to COVID-19.

to Tasmania, cutting off its main

• The local government areas with the greatest

source of population increase. number of new residents are Clarence, Launceston,

Due to a range of government Hobart and Brighton, but the greatest rate of

policies designed to stimulate population growth is in the Glamorgan/Spring Bay,

Latrobe, Tasman and Sorell local government areas.

the construction industry and the Only the West Coast, Flinders and Glenorchy local

broader economy in the wake of government areas saw population decreases, but

these were small.

COVID-19, new construction levels

are relatively high, and it is likely that • The number of building approvals increased by

65.1 percent between November and December

there will be a short-term absolute

2020. Commencement numbers accordingly also

over-supply of new housing relative increased in the December quarter of 2020.

to new demand. Whether this will

• In the December quarter of 2020, the number of

translate into increased affordability dwelling completions was 6.8 percent higher than

is not clear, because it depends on in the previous quarter and 26.1 percent higher than

the same period in 2019.

where the new houses are being built

and what kind of properties they are. • Current projections suggest that the balance

between demand and supply will fluctuate over the

next three years, but external factors, especially in

relation to migration, make future trends difficult to

predict with certainty.

• There is little sign that the Short Stay

The short-stay accommodation Accommodation Act 2020 had any meaningful

impact on the level of short-stay accommodation

sector was significantly affected by activity in Tasmania.

the virtual closure of the tourism

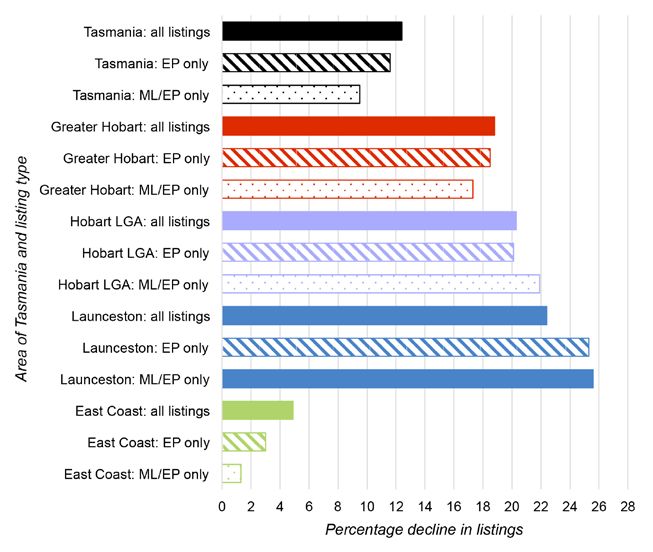

• The number of listings on the largest short-stay

industry during parts of 2020. There accommodation platform, Airbnb, fell around 20

are now signs that the sector is percent in Launceston and Hobart following the

becoming active once more. Despite closure of Tasmania’s borders in March 2020, but

remained relatively stable on the East Coast.

anecdotal evidence that some short-

stay properties returned to the private • Numbers of listings have now started to increase

again, including listings where there are indicators of

rental market during the pandemic, commercial or investor activity.

it is unclear how many did so or

• Yield for Airbnb hosts has returned to pre-pandemic

whether this trend will persist. levels, and the numbers and timing of reviews

suggest that many properties are once again being

leased out regularly.

2 University of Tasmania

• As of December 2020, there were 3,813 applications

Need for social housing remains on the Tasmanian Housing Register, which was 9.6

percent higher than the previous year.

high, as does need for assistance

from Specialist Homelessness • Timely access to social housing remains limited:

in December 2020 only 72 new households were

Services. This indicates that despite accommodated in social housing and the average

new government investment in the waiting time for priority applicants was 53.9 weeks.

social housing and crisis housing • The Tasmanian government has committed to

systems, demand still exceeds the providing 3,500 new homes in total over the next

available supply. four years. This figure does not incorporate sales or

demolition of other social housing properties so the

net gain to the system is likely to be less than this.

• The rate of homelessness in Tasmania at the time

of the 2016 Census was 31.8 homeless people per

10,000 of population, which was less than the

Australian average of 49.8. In March 2021, 2,653

Tasmanian households were receiving support

from Specialist Homelessness Services.

• There is a high level of unmet need for longer-term

housing among Specialist Homelessness Services

clients. In 2019-20, of the 76.6 percent of clients

identified as needing long term housing assistance,

only 7.8 percent had this need met directly,

51.5 percent were referred elsewhere (with an

unknown outcome) and 40.7 percent received

neither long-term housing assistance nor referral.

The Tasmanian housing market: update 2020-21 3

Introduction

There continues to be an acute shortage of affordable

housing in areas of high demand. Government measures

to address this shortage have only had a limited impact.

This report is the latest in a series ‘Affordable housing’ can refer to

prepared by the University of a type of housing product that is

Tasmania to inform public debate available to eligible households

on the Tasmanian housing crisis. at below-market rents (e.g.

The evidence in this report shows properties under the National

that although there was a small Rental Affordability Scheme or

fall in house prices and rents NRAS). However, in this report,

during the early stages of the we are using the term generically

COVID-19 pandemic, in recent and descriptively, to refer to

months both have started to rise housing which low to moderate

again, fuelled by low interest rates, income earners can afford without

increased demand for housing, the compromising their expenditure

cessation of some temporary policy on other essential costs like food,

interventions and the introduction energy and transport.

of housing-related economic

stimulus programs. These increases In Australia, responsibility for

in house prices and rents have housing policy is shared across all

exacerbated the long-standing three levels of government. To be

housing problems in Tasmania, effective, national, state, and local

which remain entrenched due to governments need to coordinate

a long-term failure to adequately their housing-related activities, and

invest in social housing and growing this does not always occur. As a

demand for affordable housing. result, there are multiple points of

tension and contradiction within

the Australian housing system.

In this report, ‘social housing’ refers to public

and community housing. This is housing

owned and managed by government and/

or the community sector and rented out

to eligible households at income-linked

rents. Due to limited supply, households are

usually unable to enter social housing unless

they are assessed as being in greatest need.

4 University of Tasmania

Commonwealth government rental properties that they cannot to new supply, eligibility for this

taxation policy, including in relation afford without unreasonably program is not means tested

to negative gearing and capital compromising their standard and the investment is likely to be

gains tax exemptions, encourages of living. The Tasmanian state capitalised into increased prices

the provision of new housing government could not deliver with little long-term impact on

supply but also contributes to 14,200 new dwellings without affordability.

speculative investment and substantial funding support from

consequent house price inflation the Commonwealth and significant This paper presents data and

(Eccleston et al. 2018a). These in private investment in affordable independent analysis on different

turn create significant housing housing. As this is not forthcoming, aspects of the Tasmanian housing

market pressures at the state Tasmanian government efforts market. It is written to inform

level, yet it is difficult for state are necessarily more limited than and provoke public debate over

governments to fully resolve they need to be to fully address housing policy. Obviously, the

these because they lack the the problem. The Tasmanian effects of the COVID-19 pandemic

Commonwealth’s revenue- government has committed to loom large in the data, but this

raising power. building 3,500 social housing is not a report about COVID-19.

dwellings over the next four years, Rather, it traces significant

For example, the unmet need as well as constructing additional continuities in Tasmania’s housing

in Tasmania’s social housing supported accommodation for market story from before the onset

system has been estimated at target groups (Tasmanian Liberals of COVID-19 and, importantly, as we

14,200 dwellings over the 20 years 2021). However, this welcome integrate COVID-19 into a new way

from 2016 (Lawson et al. 2019). investment is accompanied by of life.

This number is large because so other policies, such as a substantial

many low-income households increase to the First Home Owners

in Tasmania are living in private Grant Boost; although restricted

The Tasmanian housing market: update 2020-21 5

1. Market trends

Given the limited supply of question of competing preferences markets were even less effected.

social housing, most Tasmanians or a series of problematic and In Tasmania over the 12 months

must meet their needs for lifelong compromises depends to April 2021, dwelling values

accommodation in the private largely on household income increased 15.3 percent in regional

market. Finding the right housing and where this income situates areas and 12.5 percent in Hobart

requires weighing considerations a potential purchaser or renter in (see Figure 1). These increases

1. Market trends

including cost (affordability)

and appropriateness, which

relation to the property market. tended to exceed the average for

all regions and all capital cities.

can encompass accessibility

for Given

peoplethe limited

with supplyorof social housing, most Tasmanians must meet their needs for

disabilities Property values

accommodation

other health needs, in the private

proximity to market. Finding the right housing requires weighing

The most marked influence on

considerations

family, including

friends, schools, workcost

and (affordability) and appropriateness, which can encompass

essential services, Tasmanian house prices in the

accessibility forthe size of

people thedisabilities

with or other

last 18 months health

was needs, proximity to family, friends,

the COVID-19

property relative to the size of

schools, work and essential services,pandemic. the size ofPurchase

the property relative

the household, and the cost of prices and to the size of the

household, and the cost

living in the property day to day of living in the property

rents fell in day

most to day

major(heating

cities and cooling,

commuting, and so on).

(heating and cooling, commuting, The extent toduring

which 2020.

these However, this

considerations has

are either a question of

not lasted, and prices and rents

and competing

so on). Thepreferences

extent to whichor a series of problematic and lifelong compromises depends

these considerations are income

either a and where are once again rising. Regional

largely on household this income situates a potential purchaser or

renter in relation to the property market.

Property

Figure values

1: Dwelling value change, capital cities and rest of state, March 2021

Figure

Source: 1: Dwelling

Unpublished value change,

data, CoreLogic. capital cities and rest of state, March 2021

Past month Past 3 months Past 12 months

Sydney 3.7 6.7 5.4

Melbourne 2.4 4.9 0.7

Brisbane 2.4 4.8 6.8

Adelaide 1.5 3.2 8.6

Perth 1.8 5 6

Hobart 3.3 7.6 12.5

Darwin 2.3 5.4 14.2

Canberra 2.8 6 12.1

Regional NSW 2.8 6.6 13.6

Regional Vic. 2.6 7 10.4

Regional QLD 2.3 5.8 10.8

Regional SA 1.4 5.9 13

Regional WA 1.7 4.8 -0.1

Regional Tas 2.3 6.7 15.3

Regional NT 1.1 2.2 3

Combined capitals 2.8 5.6 4.8

Combined regionals 2.5 6.3 11.4

Australia 2.8 5.8 6.2

Percentage change

Percentage (%) %

change Percentagechange

Percentage change % Percentage

Percentage change

change %(%)

(%)

Source: Unpublished data, CoreLogic.

6 University of Tasmania

8

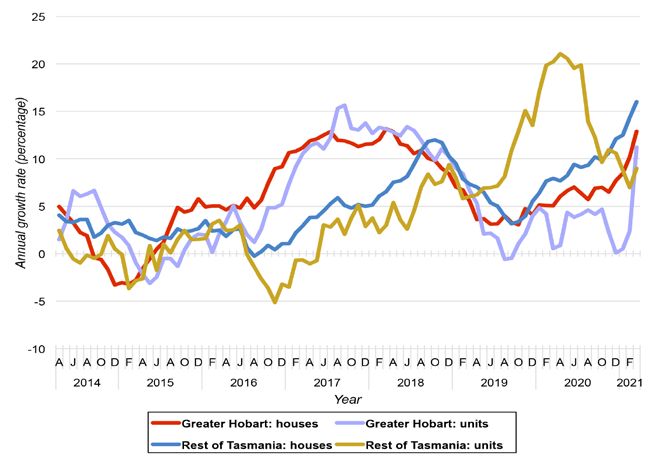

One measure of change to and houses because these are unit prices. In Hobart, prices have

property values is the Residential different products and therefore been volatile, with sharp falls at

Property Price Index, which is operate as different markets. the beginning and end of 2020

an aggregate index compiled to Differences between markets and a steep increase from the

measure the price change in all are also seen when a capital beginning of 2021. In regional

residential dwellings within the city market is compared to the Tasmania, however, unit prices

eight Greater Capital City Statistical market in the rest of the state. have decreased steadily from a

Areas. The Greater Hobart The differences across these substantial high point at the start

Residential Property Price Index sub-markets can be seen in of 2020.

rose 6.1 percent to 172.5 in the Figure 3, which depict the

March quarter of 2021, a rise of seasonally adjusted hedonic home The increase in house and unit

10.2 percent since the same value index for houses and units prices across most of Tasmania is

quarter the previous year (see in Tasmania, broken down into reflected in the fact that median

Figure 2). figures for Greater Hobart and for prices for houses in Hobart are

the rest of the state. This index is now well above the price point of

The index shows a steady increase designed to reflect not just raw half a million. Prices in Hobart did

from March 2009 to 2016, and then prices but dwelling characteristics, drop slightly in the June quarter

a steeper incline from March 2017. such as location, housing type or 2020, but they are now rising

The last major economic disruption number of bedrooms, that affect again (see Figure 4). In March 2021,

in Australia occurred due the those prices. the median house price in Hobart

Global Financial Crisis (GFC). To was $623,750, which represents a

enable this comparison, where Although there have been some 5.7 percent increase in that quarter.

data is available the scale on many fluctuations, house prices in Hobart Prices are lower in Launceston

of the graphs in this report has have generally increased across and the North-West Coast, but

been extended back to include the 2020 and into 2021. Growth in they too are trending upwards.

GFC and its aftermath. regional markets has followed Launceston prices increased by

the same pattern but has been 4.5 percent to $420,000 in the

When analysing movements in consistently higher than in Hobart. March 2021 quarter, while north-

price, economists separate units A different pattern is evident with west prices increased by

Figure 2: Residential Property Price Index (no.), Hobart, March 2009-2021

Source: ABS 2021h.

The Tasmanian housing market: update 2020-21 7

Figure 3: Hedonic home value index, houses and units, Tasmania, 2014-2021

Source: Authors, calculated from unpublished data, CoreLogic.

Figure 4: Median house prices, Hobart, Launceston and North-West, March 2011 to March 2021

Source: Authors, unpublished data, Real Estate Institute of Tasmania.

8 University of Tasmania12.1 percent to $379,000 in the In Hobart and Launceston and Burnie. This local level variation

same period. Burnie local government areas, indicates that housing sub-markets

house prices increased 14.0 percent are shaped by a wide range of

At a local government area level, and 16.9 percent respectively. In macro and micro factors. In small

in the two years to February 2021 the same two-year period, unit markets, price movements need to

there were double digit house price prices rose in all municipalities be interpreted carefully as a small

increases in all municipalities but for which there is available data number of sales can have a large

Flinders and King Island, but these apart from the Northern Midlands, effect on the overall trend.

range from a 13.7 percent increase but again, the size of the increase

in Burnie to a 47.6 percent increase varied widely, from 4.0 percent on

in George Town (see Table 1). the West Coast to 35.4 percent in

Table 1: Median house and unit prices (monthly average), February 2021, and percentage changes since February 2019,

Local Government areas

Note: Figures for smaller municipalities should be used with caution due to the smaller size of their markets.

Source: Authors, unpublished data, CoreLogic.

Houses Units

LGA Median price in Change since Median price in Change since

February 2021 February 2019 February 2021 February 2019

Break O’Day $365,000 + 30.4% $275,000 + 18.3%

Brighton $400,000 + 29.0% $328,000 + 19.3%

Burnie $290,000 + 13.7% $260,000 + 35.4%

Central Coast $375,000 + 25.0% $281,750 + 8.4%

Central Highlands $187,500 + 23.4% - -

Circular Head $260,000 + 20.9% $226,000 + 25.6%

Clarence $580,000 + 18.4% $427,500 + 6.9%

Derwent Valley $355,000 + 34.0% $320,875 + 36.5%

Devonport $335,000 + 21.8% $264,000 + 11.4%

Dorset $330,000 + 32.0% - -

Flinders $312,000 − 10.9% - -

George Town $302,500 + 47.6% $265,000 + 26.2%

Glamorgan/Spring Bay $442,500 + 22.9% $295,000 + 27.6%

Glenorchy $453,000 + 16.2% $355,000 + 18.5%

Hobart $792,375 + 14.0% $600,000 + 20.0%

Huon Valley $476,000 + 25.3% $340,000 + 10.6%

Kentish $392,500 + 31.7% - -

King Island $252,500 0.0% - -

Kingborough $641,500 + 14.6% $435,000 + 11.5%

Latrobe $430,000 + 22.0% $320,000 + 15.4%

Launceston $380,000 + 16.9% $307,000 + 5.9%

Meander Valley $400,000 + 14.6% $302,500 + 10.8%

Northern Midlands $375,000 + 23.0% $275,000 − 1.4%

Sorell $477,500 + 27.8% $363,500 + 19.2%

Southern Midlands $356,000 + 16.7% - -

Tasman $372,500 + 27.6% - -

Waratah/Wynyard $330,000 + 20.0% $267,500 + 20.2%

West Coast $120,000 + 44.6% $77,500 + 4.0%

West Tamar $430,000 + 20.2% $340,000 + 13.3%

The Tasmanian housing market: update 2020-21 9Home buyers • The Tasmanian government • Together with low interest

also offered a HomeBuilder rates, these programs offer

There are currently strong Grant of $20,000 for new substantial upfront incentives

incentives to purchase housing in housing, available for contracts to build or renovate housing

Tasmania’s housing market. Interest signed between 4 June 2020 in Tasmania. The value of new,

rates are at historic lows and are and 31 March 2021. owner-occupier home loans

expected to remain at these levels in December 2020 (excluding

for a further three years at least. • Tasmania’s existing First Home refinancing) was at record

In addition, both the Australian Owners Grant of $20,000 is also highs across all the states and

and Tasmanian governments have available to first home buyers territories except the Northern

put in place policies that provide of new homes, and in the Territory. In Tasmania, owner-

lump-sum payments to new recent state election campaign, occupier loan values rose

home buyers. the government committed 11.5 percent to $307.5 million in

to increasing this to $30,000 the December 2020 quarter,

• The Australian Government’s through the First Home Owners which is 47.8 percent higher

HomeBuilder Grant offers Grant Boost. The additional than in December 2019, and

$25,000 to eligible owner- payment will be available then reached a new high of

occupiers building a new home between 31 March 2021 and $334.6 million in February 2021;

or substantially renovating an 30 June 2022. values dropped slightly to $310.0

existing one, provided contracts million in March 2021 (see

were signed between 4 June • In some circumstances,

Figure 5). The value of investor

2020 and 31 December 2020. applicants can be eligible

home loan commitments rose

It was subsequently extended, for both a Tasmanian First

51.8 percent to $98.5 million in

at the lower rate of $15,000, for Home Owner Grant and the

the December 2020 quarter—

contracts signed between Commonwealth HomeBuilder

which was 45.5 percent higher

1 January 2021 and 31 March grant for the same property.

than December 2019—and

2021. The programs have relatively

increased again in March 2021

generous means-tests.

to $100.5 million.

Figure 5: New loan commitments, owner occupiers and investors (excl. refinancing), seasonally adjusted,

Tasmania, March 2003 to March 2021

Source: ABS 2021g.

10 University of TasmaniaIncentives like the HomeBuilder 36.2 percent on the previous their primary function is as sources

grants and the First Home Owner month and an increase of of wider economic stimulus due

Grant are directed to new supply. 85.2 percent since October 2019 to the large multiplier effect of

Loan commitments for the (see Figure 6). Reflecting the investment in the construction

construction of new dwellings pattern across the rest of Australia, industry. In 2019-20, the Tasmanian

accounted for 18.8 percent of this is the highest level since the Government made 690 grants to

total commitments, with a further peak in 2009, when the then first home buyers, but by the end

4.2 percent for the purchase of federal government’s response of May 2021 the number of grants

newly erected dwellings. This to the GFC included a temporary had already reached 822 (State

is a high proportion relative to tripling of the First Home Owners Revenue Office of Tasmania 2021).

historic trends, although there is Grant. First home owner buyer

fluctuation: the proportion of loans loan commitments remained high In the first six months of 2020,

that are for new construction has in the first quarter of 2021 with a 138 guarantees were issued in

increased by 189.4 percent since further 774 loan commitments. Tasmania (of 6814 across Australia)

March 2020 (from 66 dwellings to through the First Home Loan

191), but the March 2021 figure is Economists have frequently Deposit Scheme, an Australian

13.2 percent lower than it was in criticised the inflationary effect of Government program enabling

the previous month. First Home Owner Grants on house eligible first home buyers to

prices. As noted above, however, purchase a property free of lenders’

According to the National governments used increases to mortgage insurance with as

Housing and Finance Investment First Home Owners Grants in little as 5 percent deposit (NHFIC

Corporation, first home buyers now the wake of the GFC as a source 2020a). Until July 2021 the program

account for more than 40 percent of economic stimulus. This has could only be used to purchase

of total new housing commitments occurred again in 2020: programs properties valued up to $400,000,

(NHFIC 2020b). In Tasmania, there like Home Builder and the boosted which presents a significant limit

were 350 owner occupier loans to First Home Owners Grant in on location and quality in the

first home buyers in October 2020, Tasmania may be presented as current Tasmanian market.

which was an increase of housing assistance programs, but

Figure 6: Number of new loan commitments to first home buyers (owner-occupiers), seasonally adjusted,

Tasmania, March 2005 to March 2021

Source: ABS 2021g.

The Tasmanian housing market: update 2020-21 11The rental market 23 April 2020 and 31 January 2021

landlords were prohibited from

The strong growth in house prices increasing the rents of sitting

has intensified the affordability tenants, and prohibitions on

problems of Tasmanian renters. eviction would have limited tenant

Hobart’s rental market remains mobility and thus the number of

one of the tightest in the country, new leases. As these restrictions

with rents above pre-pandemic lifted, rents for both houses and

levels. Renters’ living costs are units have been increasing across

increasing, driven by housing the state (see Figure 7). At the local

costs and the low vacancy rate. level, however, there is variation.

In March 2021 the median rent House rents have fallen slightly in

for Tasmania was $400 per week the Hobart local government area,

for a three-bedroom house and risen slightly in the Launceston

$360 for a two-bedroom unit local government area, and

(see Figure 7). This represents a remained flat in the Burnie local

6.7 percent increase in median government area (see Figures 8-9).

rent for three-bedroom houses For units, rents have been steady

and a 20 percent rise for two- in Hobart and have increased in

bedroom units respectively since Launceston and Burnie.

March 2020.

Movement in rents was

constrained during 2020: between

Figure 7: Median rents, weekly, houses and units, Tasmania, July 2017 to March 2021

Source: Authors, unpublished data, Real Estate Institute of Tasmania.

12 University of TasmaniaFigure 8: Median rents, monthly average, houses, Hobart, Launceston and Burnie local government areas,

January 2016 to February 2021

Source: Authors, unpublished data, CoreLogic.

Figure 9: Median rents, monthly average, units, Hobart, Launceston and Burnie local government areas,

January 2016 to February 2021

Source: Authors, unpublished data, CoreLogic.

The Tasmanian housing market: update 2020-21 13Alongside affordability pressures Summary

are issues with availability.

Tasmania’s rental market has Tasmania’s housing market was

been marked by long periods of affected throughout 2020 by the

very low vacancy rates: between economic consequences of the

2004 and 2010, vacancy rates COVID-19 pandemic, but also

hovered around 2 per cent, and by the measures introduced in

a similarly low vacancy rate has response to those consequences,

again persisted since the end of including stimulus measures

2017 (see Figure 10). A vacancy targeting the construction sector.

rate of 3 percent is commonly The effect is that house prices have

considered the point at which continued to increase. First home

the rental market is in equilibrium buyers have been able to enter

between demand and supply; a the market due to the available

vacancy rate of 2 percent therefore grants and incentives, but investors

means demand for rental housing have also benefited. The situation

is unlikely to be met and many in the private rental market is less

prospective tenants will be unable clear, with rents increasing in some

to secure accommodation. The locations and decreasing in others.

decline in the vacancy rate seems This may reflect the moratoriums

to be driven by a shortage of on evictions and rent increases

actual properties—the Anglicare in place during 2020. As these

Australia network’s series of restrictions are lifted, there are

‘snapshot’ surveys has tracked a signs of increasing affordability

steady decline in rental availability, pressure in the market linked to a

with the number of properties declining vacancy rate.

advertised for rent falling 73

percent since 2013 (Claxton 2021: 4).

Figure 10: Private rental market vacancy rate (quarterly), Tasmania, 2004 to 2020

Source: Authors, unpublished data, Real Estate Institute of Tasmania.

14 University of Tasmania2. Incomes and housing costs

The previous section outlined the income of households wholly

the sustained increases in the reliant on the income support

cost of housing in Tasmania, system against the Henderson

both in purchase prices and in Poverty Line, which is calculated to

rents. Increased costs present represent the disposable income

affordability challenges when they needed to support the basic needs

are not matched by increased of a family of two adults and two

capacity to pay. children (Melbourne Institute:

Applied Economic and Social

Research 2020). Equivalence scales

‘Housing affordability is defined by the relationship are used to produce equivalent

between housing expenditure, such as mortgage poverty lines for other household

types. According to the Institute’s

payments or rent, and household incomes. Having December 2019 report, only

housing that is affordable means households can two household types reliant on

access an adequate standard of housing without income support were receiving

incomes above the poverty line:

unduly compromising other needs’ married pensioner couples, single

(NHFIC 2020b: 47). pensioners, and single parents

with one child (the calculation

assumes these single parents

Wage income in Australia has are living on Parenting Payment,

remained stagnant for some years which means their child would be

with no increase to purchasing aged under eight—single parents

power. According to the 2019-20 with a child above this age would

Survey of Income and Housing, be on the much lower JobSeeker

national average ($2,348) and payment). In some cases, the gap

median ($1,841) weekly household between payment and poverty line

income remained unchanged is substantial: a couple reliant on

in the June 2020 quarter from JobSeeker (then called Newstart

the March 2020 quarter and Allowance) was receiving

represented only a minimal 79.5 percent of a poverty line

increase from June 2018 ($2,314 income ($577.60 per week

average and $1,752 median) (ABS compared to a poverty line of

2020a). At the time of writing, data $726.27, while a single person

was not yet available for Tasmania on JobSeeker was receiving just

specifically, but Tasmanian 65.0 percent of the poverty line

incomes have historically been ($352.90 compared to $542.92).

below the national average. This

as an important consideration: it Statutory and other incomes

is not only rent that varies across did shift during 2020 due to

location but also income, which government interventions

means ‘affordability’ has a strong in response to the COVID-19

geographical component. pandemic. JobKeeper, an

Australian Government payment

A high proportion of the made available to workers via

Tasmanian population has eligible employers (defined

historically relied on the Australian primarily by their amount of

social security system for their revenue loss due to the pandemic),

primary source of income. Pension and the coronavirus supplement

increases have been limited in to selected income support

recent years as these are linked payments, including JobSeeker

to wage increases. Allowances Payment, Youth Allowance,

have increased even less as these Parenting Payment and Austudy,

payments are linked to inflation. would have represented a decline

The Melbourne Institute tracks in income for some households

The Tasmanian housing market: update 2020-21 15and an increase for others. Rental affordability was attributed to the effects of

Anecdotally, this adjustment in the pandemic and the broader

income did influence people’s One measure of rental affordability situation in Hobart was ‘dominated

housing choices, especially where that accounts for local household by a more persistent trend of

households had an increase in incomes is the rental affordability declining affordability’ (SGS

income and used it to, albeit index (RAI), which is based on Economics and Planning 2020:

temporarily, improve their housing modelling by SGS Economics. 40). The authors also cautioned

circumstances (Verdouw et The RAI uses a score of 100 to that an overall improvement in

al. 2021). However, JobKeeper indicate the boundary between affordability masks the fact that

payments tapered from affordability and unaffordability: very low-income households

28 September 2020, ultimately scores of 100 or less indicate a may still face extreme to severe

ceasing on 28 March 2021. The household is paying more than affordability problems.

coronavirus supplement has also 30 percent of income in rent,

been withdrawn and income which is a measure of ‘housing Relative to the other ‘rest of

support has largely returned to stress’ or unaffordable housing. state’ areas in Australia, regional

pre-pandemic levels, with the Greater Hobart currently scores 96 Tasmania is the most unaffordable

recent $50 per fortnight increase against the RAI (see Figure 11). of the states included in the

in JobSeeker Payment and research (New South Wales,

comparable payments effectively The 2020 RAI report, drawing on Queensland, South Australia,

negligible given the level of those data from mid-2020, identified Victoria and Western Australia).

payments relative to the poverty Greater Hobart as the least Affordability increased slightly

line (Melbourne Institute: Applied affordable Australian capital in the first half of 2020, again

Economic and Social Research city—it was the only capital city probably due to the impact of

2020). in which households on the local JobKeeper and the coronavirus

average income and renting in the income support supplement, but

private market would be living in the underlying trend is towards

housing stress (SGS Economics greater unaffordability (see

and Planning 2020: 54). Although Figure 11).

this represented a slight increase

in affordability relative to the As an alternative measure of

previous year, this improvement affordability, research undertaken

for the National Housing Finance

Figure 11: Rental Affordability Index, quarterly, Tasmania, 2012 to 2020

Source: SGS Economics and Planning 2020.

16 University of Tasmaniaand Investment Corporation found are historically low, the cost of Summary

that nationally, as of June 2020, servicing a mortgage has been

the bottom quintile of renters (by equal to or even below the average Affordability is determined not

income) could afford less than cost of paying rent (NHFIC 2020b: just by house prices or rents, but

10 percent of rental stock and the 60). The deposit gap may also have by income. Incomes from wages

second lowest income quintile closed somewhat: the Australian have been static for some time

could afford just 20 percent (NHFIC National Accounts show that the which means that, as rents have

2020b: 55). Affordability was household saving ratio increased increased, affordability in the

defined according to the housing nationally to 22 percent in the private rental market has declined.

stress benchmark of 30 percent or June quarter of 2020, up from Home purchase is somewhat more

less of income spent on rent by a 7.9 percent in March, and it still affordable than it has been due to

household in one of the bottom remained relatively higher, at low interest rates and increased

two income quintiles. In Hobart, 11.6 percent, in March 2021 household savings, but the price of

less than 10 percent of homes were (ABS 2021d). most Tasmanian houses remains

considered affordable according to two high for most income earners.

this definition (NHFIC 2021b). NHFIC now considers a quarter The lowest income earners in the

of available dwellings nationally community tend to be those on

Rents in social housing are to be affordable to prospective income support payments. Many of

income-linked, with most tenants first home buyers in the bottom these individuals and households

paying around 25 percent of their two income quintiles (NHFIC are living well below the poverty

income in rent (plus any applicable 2020b: 62). The picture for Hobart line, with significant consequences

Commonwealth Rent Assistance is slightly different, however, with for their ability to obtain any kind

for those in community housing). only 10-20 percent of properties of housing.

This means that according to affordable to the bottom

the ‘housing stress’ measure of 60 percent of income earners

affordability, social housing tenants (NHFIC 2021).

do not have affordability problems.

However, while social housing

provides an important protection

to tenants by ensuring such

rents, the extremely low level at

which Australian income support

payments are set means that

many social housing tenants may

nonetheless be living in poverty,

particularly those who have

complex health and other support

needs which impose additional

costs.

Purchase affordability

There is a lack of current data on

the affordability of home purchase

specifically in Tasmania. Nationally,

the affordability of home purchase,

measured by the ratio of mortgage

repayments to incomes, improved

for some groups in the population

during 2020. As noted in section 1

of this update, house prices have

continued to rise, which means

that borrowers may have been

taking on higher levels of debt

overall, but because interest rates

The Tasmanian housing market: update 2020-21 173. Demand and supply drivers

In formal terms, demand for housing refers to households’ housing needs and

preferences, and the number of dwellings required to meet these needs or

preferences. Thus, although demand refers to the basic need for shelter, it can also

incorporate a preference for particular types of housing or levels of amenity.

The long-term drivers of housing demand include changes in the population due

to births, deaths or migration; the overall age structure, and therefore life-stages,

of the population; and broader social and economic change.

Housing supply refers to the number of houses available. It is the net result of new

additions to the housing market arising from the construction of new dwellings and

losses to the housing market through demolition. The supply of residential housing

may not always match the number of households in a community, as some

households may use more than one house (e.g. because they live in one property,

but use a second as a holiday home or shack).

Changes in demand the Nation’s Housing 2020 report,

it was estimated that around half

The COVID-19 pandemic has the working population was still

affected the make-up of housing working from home, a pattern

demand in Tasmania, but it is that has persisted into 2021 amid

not yet clear what the long-term ongoing lockdowns. The report

impact might be. The ongoing noted that demand appeared to

shortfall in affordable housing be shifting away from inner-city

supply has been a confounding dwellings to regional centres,

factor. For example, migration although it was not yet clear

increases housing demand more whether this trend would persist

rapidly than natural population (NHFIC 2020b: 6). Even if the

increase (more births than deaths) shift is only temporary, it could

or new household formation, yet still increase housing demand in

although the demand for housing Tasmania in the short and medium

through migration, especially term, including through greater

international student migration, interstate migration to Tasmania.

almost halted during 2020 due to

COVID-19 travel restrictions, unmet

demand for affordable housing in Components of

Tasmania has remained high.

population change

The COVID-19 pandemic has There were an estimated 540,600

also shifted housing preferences people residing in Tasmania

towards free standing dwellings at the end of June 2020 (ABS

that contain extra spaces suitable 2020b). The population had been

for work or study from home and growing steadily in the four years

outdoor areas for fresh air, exercise to March 2020 but following the

and gardening. Less urbanised closure of Australian borders—and

areas have become more desirable Tasmanian borders—it is likely

due to the ability to work remotely this growth has been checked,

and avoid crowded commutes although this was not yet apparent

(see Verdouw et al. 2021). At the in the data available at the time

time NHFIC prepared its State of of writing. What was available

18 University of Tasmaniashowed an annual growth for as a component of population replacement rate of 2.1. This TFR is

the year ending June 2020 of 1.1 growth—from a peak of 50 percent consistent with the rate used in the

percent. The impact of the border of population growth in 2012, it now ‘low’ series of population projection

closures is likely to be significant only contributes 21.9 percent as of assumptions which assume the

because population growth in June 2020. rate will continue to fall, to 1.76

Tasmania, as in the rest of Australia, per woman by 2028 (ABS 2020b).

is primarily driven by net overseas Although Tasmania’s borders are Overall, the difference between

migration, or NOM; NOM has now generally open to interstate births and deaths in Tasmania is

contributed to nearly 60 percent migrants, Australia’s borders beginning to narrow; structural

of population growth over the last are likely to remain closed to ageing of the population and lower

few years. This is followed by net international arrivals, including life expectancy in Tasmania relative

interstate migration (NIM) and international students, for some to Australia means there is likely

natural increase arising from births time to come. This will obviously to be continued increase in the

outnumbering deaths. have an impact on population number of deaths relative to births.

change over the coming years. It This puts Tasmania on trajectory of

Population change in Tasmania has is highly unlikely that substantial natural population decline, which

fluctuated since the previous global population growth will occur due to in turn makes the state more reliant

economic shock of the 2008 GFC natural increase: in 2019, Tasmania on migration for population growth

(see Figure 12), reflecting changes in recorded a total fertility rate (TFR) and therefore more sensitive to

economic conditions which shape of 1.79 births per woman, which changes in migration levels.

employment markets. Natural is less than the rate of 1.85 in 2018

increase is a declining influence and well below the population

Figure 12: Components of population change, and population growth rate, Tasmania,

year ending June 2008 to 2020

Source: ABS 2020b.

The Tasmanian housing market: update 2020-21 19Local variation Table 2: Regional population change, number and growth rate, Tasmanian

local government areas, year ending June 2020

Changes in population at a

Source: ABS 2020c.

statewide level are distributed

differently at the local level, with

some areas experiencing rapid Population change Population growth

growth while others may see a LGA

(no. of people) rate (percentage)

decline in the resident population.

In the year to 30 June 2020, Break O’Day + 59 + 0.9

the local government areas

in Tasmania with the greatest Brighton + 449 + 2.5

number of new residents were

Burnie + 152 + 0.8

Clarence (which increased its

population by 916 people or Central Coast + 220 + 1.0

1.6 percent of population),

Launceston (779 people or Central Highlands + 36 + 1.7

1.1 percent), Hobart (531 people

Circular Head + 73 + 0.9

or 1.0 percent), and Brighton (449

people or 2.5 percent) (see Table 2). Clarence + 916 + 1.6

However, the highest growth rates

occurred in the more regional local Derwent Valley + 95 + 0.9

government areas of Glamorgan-

Devonport + 114 + 0.4

Spring Bay (3.2 percent), Latrobe

(2.8 percent), Tasman (2.7 percent) Dorset + 51 + 0.8

and Sorell (2.7 percent). In only

three local government areas did Flinders −6 − 0.6

the population decline between

George Town + 149 + 2.1

June 2019 and June 2020: the West

Coast (a decrease of 43 people or Glamorgan/Spring Bay + 147 + 3.2

-1.0 percent), Flinders (14 or -

0.6 percent) and Glenorchy (16 or Glenorchy − 16 0.0

0.0 percent).

Hobart + 531 + 1.0

Huon Valley + 402 + 2.3

Projections of future

Kentish + 78 + 1.2

demand

King Island +2 + 0.1

In 2019, the Tasmanian

Department of Treasury and Kingborough + 313 + 0.8

Finance’s ‘middle’ series of

population projections estimated Latrobe + 323 + 2.8

that Tasmania’s population would

Launceston + 779 + 1.1

grow at a rate of 0.2 percent per

year, reaching about 569,000 by Meander Valley + 193 + 1.0

2042 (Department of Treasury and

Finance 2019: 19). As part of this Northern Midlands + 161 + 1.2

overall growth, the population

Sorell + 427 + 2.7

would increase in 14 of the state’s

local government areas and would Southern Midlands + 111 + 1.8

and decline in the other 15. The

Hobart local government area Tasman + 65 + 2.7

would see the greatest number

of new residents, due to higher Waratah-Wynyard + 73 + 0.5

NOM made up primarily of West Coast − 43 − 1.0

younger people, and Brighton was

predicted to see the fastest growth, West Tamar + 351 + 1.5

20 University of Tasmaniawith a percentage increase of growing interstate migration being (ABS 2021c). In-fill development has

1.18 percent per annum driven by lifestyle factors combined been relatively limited and much

(Department of Treasury and with growing acceptance of of the growth in private housing

Finance: 2019: 10). However, the remote working arrangements. supply occurs on the urban fringe.

changes COVID-19 has caused to During the post-war period, as did

NOM and continued uncertainty Overall, Tasmania’s future other states, Tasmania constructed

about interstate travel and population has become much broadacre social housing

consequently to NIM mean the more uncertain due to the developments, but these were

assumptions that underpin these changes brought by the pandemic. smaller in scale than those on the

projections may no longer be valid. Although international migration mainland, and Tasmania’s extensive

remains constrained, there may rent-to-purchase scheme and later

The Australian Government’s be an increase in migration sales programs have meant that

population projections from 2020 from interstate. This will have even the most concentrated areas

were less conservative than the implications for housing demand of social housing are in fact mixed

Tasmanian government’s, even and the supply response needed communities of home owners,

with adjustments to assumptions to meet it. private renters, and social renters

due to COVID-19. Its ‘middle’ case (Flanagan 2019).

shows Tasmania’s population

reaching 569,000 by 2028-29. Changes in supply

This was based on assumptions

With the cessation of large-scale Building approvals

consistent with those in the

2020-21 Budget: that further government construction of public As noted in Section 1, the Australian

localised outbreaks of COVID-19 housing in the 1980s, meaningful and Tasmanian governments have

would be largely contained, that growth in new housing supply in used various programs of grants

state border restrictions would Tasmania has depended largely to stimulate economic growth

be lifted by the end of 2020 and on activity in the private sector. via the housing market. These

that the restrictions on gatherings This, along with the relatively small programs include the boosted

and on international travel would size of the Tasmanian market, First Home Owners Grant and the

continue until a population-wide has had implications for the type state and national HomeBuilder

vaccination program was fully of stock that is added to overall programs. There is evidence that

implemented by the end of 2021 supply. According to the last these types of programs have

(Centre for Population 2020). At Census, Tasmania has a higher triggered an upsurge in building

the time of writing in mid-2021, proportion of detached housing approvals across Australia,

some of these assumptions appear than the national average, and a including in Tasmania, where

overly optimistic, although there is correspondingly lower proportion building approvals numbers

mounting anecdotal evidence of of semi-detached housing and flats increased by 65.1 percent to 464

Figure 13: Monthly building approvals, seasonally adjusted, Tasmania, March 2006 to March 2021

Source: ABS 2021f.

The Tasmanian housing market: update 2020-21 21Figure 14: Total number of building approvals and number of approvals not yet commenced (quarterly, original

time series), Tasmania, December 2005 to December 2020

Source: Authors, collated from ABS 2021e, 2021f.

Figure 15: Number of dwellings commenced and number of dwellings under construction

(quarterly, original time series), Tasmania, December 2005 to December 2020

Note: The ABS defines a building commencement as the first performance of physical building activity on a site, in the form of materials fixed in place

and/or labour expended. Commencement includes site preparation but excludes delivery of building materials, the drawing of plans and specifications

and the construction of non-building infrastructure such as roads (ABS April 2021).

Source: ABS 2021e.

22 University of Tasmaniaapprovals between November and (ABS 2019). Previous University of Figure 14). This shows the potential

December 2020, a 95.0 percent Tasmania housing market updates lag between building approvals

increase since December 2019 (see noted a growing time lag between and building starts. Some of

Figure 13). Approval numbers were approvals and commencements the dwellings that have been

lower in January 2021 but were in Tasmania, possibly due to a lack approved but which have not yet

again in the mid-400s in February of access to skilled labour, finance commenced may never be built.

and March. or project management expertise

(Eccleston et al. 2018c; Jacobs et Despite these 546 dwellings not

According to NHFIC, the time lag al. 2019). This underscores that yet commenced, the growth

between building approval and there is no guarantee that building in overall approvals meant that

completion is on average approvals will necessarily lead to commencement numbers did

12 months for a detached or commencements. increase in the December quarter

medium density dwelling and two of 2020. In that quarter there were

years for an apartment. In practice, 891 commencements, which was

the lag varies depending on the Building activity: an increase of 11 percent year on

type of building being constructed, year as well as an increase from

prevailing planning and market

commencement, the previous quarter (see

conditions and access to materials construction and Figure 15). These commencements,

and labour (NHFIC 2020: 34). completions and the number of dwelling units

Historically (between 2014 and that have proceeded beyond

2019), the average time between ABS statistics for the December commencement and are now

approval and commencement quarter of 2020 show there considered under construction,

for houses in Tasmania was were 1,013 building approvals indicate the number of dwellings

2.6 months and the average in Tasmania. There were also coming on line. For the December

time between commencement approvals for 546 dwellings sitting quarter of 2020 there were 2,367

and completion was 7.0 months ‘on the books’ and classified as dwelling units under construction,

‘not yet commenced’ (see

Figure 16: Number of dwellings completed (quarterly, original time series), Tasmania, December 2005 to

December 2020

Source: ABS 2021e.

The Tasmanian housing market: update 2020-21 23which was a slight decline from the are classified as public or private, imply that all new construction is

previous quarter (-1.6 percent) and the latter figure may not be in the right form or the right place

a slight increase from the previous equivalent to new social housing to match demand. There are also

year (1.3 percent). The previous supply). The total represents an reports of concerns within the

major peak in construction, in increase of 6.8 percent from the industry about critical shortages

March 2010, coincides with the previous quarter and 26.1 percent in construction materials which

GFC stimulus package which from the previous year (see could push up costs and put at risk

included measures targeted at the Figure 16). timely completion of new housing

construction industry. supply (Coulter 2021), as well as

The increased building and an ongoing shortage of building

The number of dwelling construction activity is most likely labour (Mawby 2021).

completions is also tracking connected to the economic

upward. In the December quarter stimulus measures introduced

of 2020, 875 dwelling units by the Commonwealth and The demand-supply

completed, comprised of 823 State Governments. There is new

private sector dwellings and 51 housing supply being built and

balance

public sector dwellings (due to this includes some social housing. The balance between supply

complexities in the way dwellings However, this does not necessarily and demand is formed by the

Figure 17: Actual and projected annual changes in supply, demand and supply-demand balance,

Greater Hobart, 2019-2025

Note: ‘Supply-demand balance’ refers to the difference in new demand and new supply. A negative balance implies there is not enough new supply to

meet new demand and a positive balance implies that there is too much new supply relative to new demand.

Source: NHFIC 2020b: 76.

24 University of Tasmaniarelationship between the amount undersupply of housing of around for already formed households)

of underlying demand in the 200,000 dwellings in Australia with economic adjustments that

market and the net supply of (NHFIC 2020b: 5). According to incorporate factors such as in

housing. Although the ratio NHFIC, which now has carriage unemployment rates, income and

between demand and supply can of monitoring the national supply cost of housing.

be quantified for a given point of and demand for housing,

in time, the relationship itself is over the following decade NHFIC’s modelling for 2020 found

dynamic. In a well-functioning construction levels increased at Greater Hobart to have a small

market, a significant level of unmet a rate that broadly kept supply under supply of housing but

demand would be expected to and demand in balance. NHFIC projected a moderate over-supply

stimulate a supply response, but has supplemented the National of 800 dwellings to develop by

the many factors at play in housing Housing Supply Council’s model 2021 as new demand fell and

markets mean they do not always of underlying housing demand there was a net increase in new

function well. (which is based on new household dwellings (see Figure 17). This was

formation derived from population expected to remain in balance

In 2010, the former National growth and age structure rather until 2024 when demand was

Housing Supply Council than changes in housing demand expected to increase to the point

estimated there was a cumulative of another undersupply unless

Figure 18: Actual and projected annual changes in supply, demand and supply-demand balance,

rest of Tasmania, 2019-2025

Note: ‘Supply-demand balance’ refers to the difference in new demand and new supply. A negative balance implies there is not enough new supply to

meet new demand and a positive balance implies that there is too much new supply relative to new demand.

Source: NHFIC 2020b: 76.

The Tasmanian housing market: update 2020-21 25a construction program was 2020, demand for apartments

maintained. This pattern was has fallen due to restrictions

consistent with NHFIC’s projections on migration, including from

for Australia as a whole. international students. There is now

an oversupply of apartments in

For the rest of Tasmania, NHFIC’s major cities such as Melbourne or

projection for 2021 was a fall in Sydney, which is expected to lead

new household formation, and to lower rents for those dwellings.

therefore a fall in demand, leading However, this has not happened in

to an over-supply of 700 new Hobart, where rents have remained

dwellings. In 2022 this balance high. As noted above, historically

would shift to an undersupply of the Tasmanian market has been

500 dwellings, before returning dominated by detached housing

to a small oversupply in 2024 (see and this is expected to continue

Figure 18). with demand for freestanding

homes growing. The market

The accuracy of these projections

for detached housing, as well

depends on a range of factors.

as regional markets with spare

The housing market is currently

capacity in the building industry,

more dynamic and hence less

are also more likely to benefit from

predictable than ever. COVID-19

the various stimulus programs.

has altered the economic outlook

and is driving unanticipated

changes in intrastate, interstate

and international migration.

Summary

Subsequent policies that seek to The balance between housing

actively influence construction, demand and housing supply is

such as the various stimulus always dynamic, but with the

programs, were not incorporated changes brought by COVID-19,

into NHFIC’s model. including restrictions on migration,

affecting demand, and economic

The models are also broad. An stimulus measures targeted at

over-supply of 700 homes, for construction, affecting supply, it

example, may be less significant is now inherently unpredictable.

once those 700 homes are Although there are signs that the

distributed across the entirety stimulus measures are leading

of the ‘rest of Tasmania’. Certain to increased activity within the

communities may experience building sector, there are no

an under-supply even though in guarantees that the resulting new

aggregate the entire state is in supply will be of the type or at

over-supply and vice versa. Nor do the price point needed to resolve

raw supply numbers incorporate Tasmania’s affordability challenges

the amenity or price of newly built in the short-to-medium term.

dwellings, which means shortages

of certain types of housing, such

as affordable housing or housing

which meets universal design

principles, may persist despite an

oversupply in other segments of

the market.

For example, the supply of new

apartments coming onto the

market peaked in 2017 and was

already in decline prior to the

pandemic, particularly in capital

cities (NHFIC 2020b: 24). Since

26 University of TasmaniaYou can also read