THE LONG TERM BET! North's ascendance within Bengaluru's office market

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

Megha Maan

Senior Associate Director | Research |

India

+91 96 6718 8334

megha.maan@colliers.com

Teni Alice Abraham

Analyst | Research | Bengaluru

+91 73 3865 9579

teni.abraham@colliers.com

THE LONG TERM BET!

North’s ascendance within Bengaluru’s office market

COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

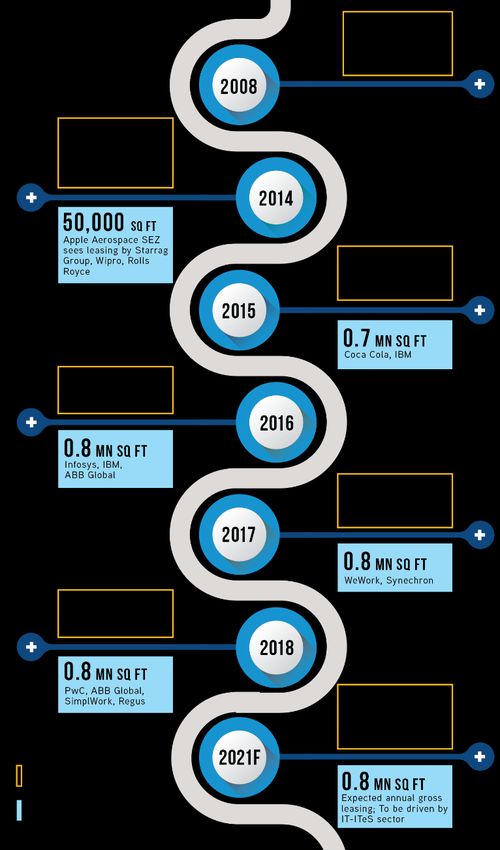

Evolution of North Bengaluru Kempegowda International Airport (KIA)

Summary & Recommendations commenced operations in 2008, spurring

developers’ interest in North Bengaluru.

Bengaluru topped the list as the preferred This micromarket, stretching over 25 km

location in Asia for technology groups as (15.5 miles) from Hebbal Junction to the

detailed in Colliers’ report Top Locations in airport, has since touted itself as the

Asia – Technology) (18 September, 2018). emerging commercial hub of Bengaluru,

with a planned aerotropolis1 similar to

Factors supporting Bengaluru’s top spot Amsterdam’s Schiphol airport and

include its high long-run economic growth, Frankfurt am Main airport.

availability of office space, and strong pool North Bengaluru started gaining

of talent. attention from occupiers in 2014 with

However, due to challenges including major transactions from the technology

overburdened infrastructure and limited sector. Alongside commercial

vacancy in preferred locations such as the developments, social infrastructure has

been improving and residential

Outer Ring Road (ORR), Central Business

developments have started. Currently,

District (CBD) and Secondary Business there is 4.0 million sq feet (371,750 sq

District (SBD), we expect office demand to meters) of operational Grade A office

shift to Whitefield and North Bengaluru stock and an additional 5.7 million sq

(defined as the micromarkets of Hebbal feet (520,445 sq meters) of new supply

and Yelahanka), where quality supply is scheduled through 2021.

available at very competitive rents. North Bengaluru has yet to witness the

> We recommend occupiers to consider strong demand seen in the preferred

North Bengaluru for expansion and locations of ORR, CBD and SBD. However,

consolidation as infrastructure as rents increase in these micromarkets,

amidst low vacancy, we expect occupiers

improves and supply becomes

will start to see North Bengaluru as a

available.

desirable location for their offices.

> We also recommend developers to

provide flexible options to occupiers

Megha Maan

looking for 50,000-100,000 sq feet Senior Associate Director

(4,645-9,295 sq meters) of space, thus Research | India

increasing the attractiveness of large,

affordable floor plates.

Teni Alice Abraham

Analyst

Note: all figures as of Q4 2018

1An airport based township or urban development is termed as Aerotropolis

Research | Bengaluru

2 Source: Colliers International

COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

TABLE OF CONTENTS

Page

Summary & Recommendations 2

Occupier Strategy 4

Developer Strategy 4

North Bengaluru in context 5

Delineating the North 6

Increasing supply should favour the North 7

3

COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

OCCUPIER STRATEGY DEVELOPER STRATEGY

Over the past three years, North Bengaluru has captured the attention of Based on our conversations with developers in North Bengaluru, they are

various sectors. For example, in 2018 the technology sector accounted for currently apprehensive about building speculatively in this micromarket.

54.0% of total leasing in the North. Banking, financial services and insurance They are looking for commitments from occupiers before the onset of new

(BFSI) companies represented 11.0% of leasing volume, engineering projects. We expect Grade A buildings in the area around Hebbal Junction

companies leased 8.0% of space and flexible workspace operators accounted to continue to be in demand due to their proximity to the CBD and ORR,

for 7.5% of gross leasing. while the area around Yelahanka and further north will likely need better

social infrastructure and residential density to attract sustained occupier

We suggest cost- Based on our market intelligence, occupiers with large requirements of

demand.

above 1.0 million sq feet (92,940 sq meters) are considering North

conscious

Bengaluru for their future expansion plans, and Grade A office developments Based on our discussions with various occupiers, we recommend developers:

occupiers with with large floor plates and opportunities for contiguous expansion are likely

expansion plans to drive their office space planning in the future.

> Provide flexible options for mid-sized occupiers looking for 50,000 sq feet

and companies (4,645 sq meters) to 100,000 sq feet (9,290 sq meters) of office space in

looking for SEZ To capitalise on the current market trends, we recommend the following close proximity to the airport.

strategies for occupiers looking to find the best fit for their business needs.

benefits to > As we expect demand to increase over the next five years, we

consider North > The well-established office market around the Hebbal Junction is suitable recommend developers pay attention to changing technologies with

Bengaluru. for existing occupiers looking for expansion in proximity to the ORR respect to construction and building management systems. Developers

micromarket, regardless of the cost. Well established IT companies should aim to be future-proof and invest in systems that will support

targeting talent acquisition, employee retention and reduction in their premium rentals, such as deploying automated parking slots and charging

attrition rates should focus on Hebbal for future expansion. points for electric vehicles.

> The Yelahanka micromarket offers relocation and consolidation We urge both developers and occupiers to actively participate in public-

opportunities for IT occupiers to hedge against rental increases, as it private partnership (PPP) models to develop social amenities and

offers 40.0% lower rentals than the Bengaluru average. We suggest cost- infrastructure such as the Namma Metro, similar to contributions made by

conscious occupiers with expansion plans, and companies looking for IT- Embassy Group, Infosys and Intel2 for the ORR metro line. Aids could come in

Special Economic Zone (SEZ) benefits to consider this micromarket. the form of financing, construction or even management of associated

facilities.

> Small and mid-sized occupiers looking for office space in proximity to the

airport should consider flexible workspaces. In 2018, prominent flexible

workspace operators such as Regus, SimplyWork and IndiQube

commenced operations in this micromarket, cumulatively leasing

225,000 sq feet (20,910 sq meters).

2 https://economictimes.indiatimes.com/industry/transportation/railways/namma-metro-you-can-own-

it-too/articleshow/66776885.cms

4COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

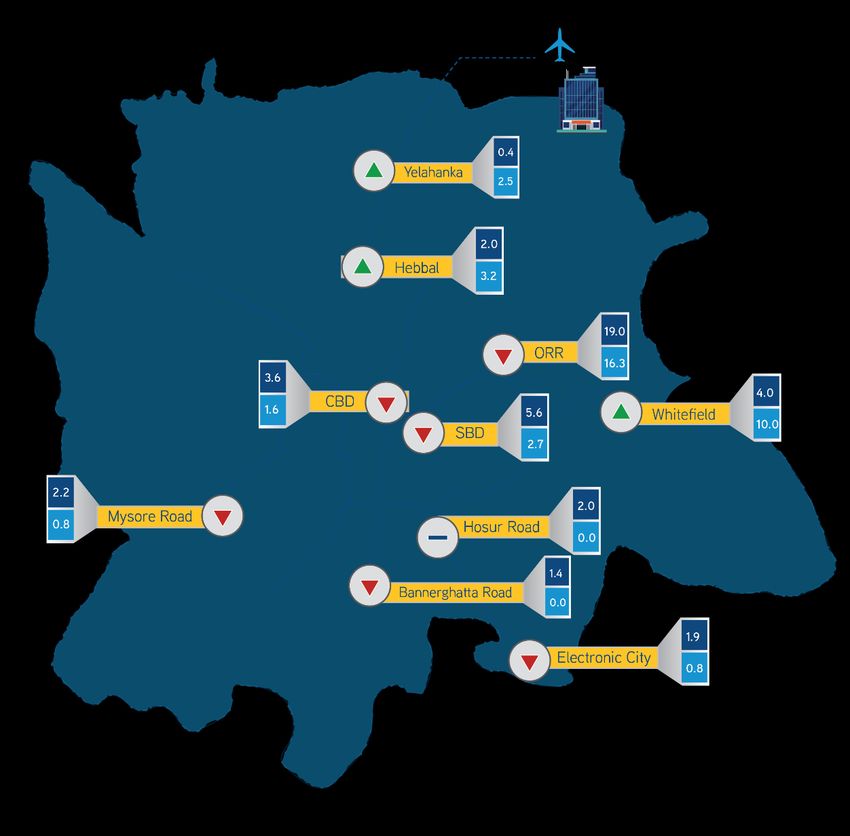

Bengaluru demand and supply dynamics by micromarket (million sq feet)

NORTH BENGALURU

IN CONTEXT

Over the last four years (2014-2018), Bengaluru

has witnessed average annual gross office leasing

of 13.9 million sq feet (1.3 million sq meters),

with the ORR micromarket accounting for 45.0%

of total leasing volume. The SBD and CBD

Colliers expects micromarkets follow with 13.0% and 9.0%,

Whitefield and respectively. Colliers forecasts demand for Grade

Hebbal to witness A office space to increase by 1.0% compounded

high growth in annually over 2019-2021 to 14.5 million sq feet

leasing activity (1.3 million sq meters). However, limited vacancy

over the next three in the preferred micromarkets in the next three

to five years to five years may necessitate occupiers

considering North Bengaluru.

Even though North Bengaluru constituted only

7.0% of Bengaluru’s gross office leasing volume

in 2018 and holds about 4.0 million sq feet

(371,750 sq meters) of Grade A operational

office stock, we expect it to be increasingly

appealing to occupiers with the addition of 5.7

million sq feet of space (520,450 sq meters) by

2021, together with ongoing improvements in

infrastructure.

Complete Namma Metro Cumulative demand forecast 2019-2021 Demand supply equilibrium

Under-Construction Namma Metro Cumulative upcoming supply over 2019-2021 Demand greater than supply

Notes: Supply greater than demand

All values are in millions of sq feet

Data as of Q4 2018

CBD include MG Road and, Richmond Road, Infantry Road, Cunningham Road, Sankey Road, Palace Road, Vittal Mallaya Road and others

SBD includes Indiranagar, Koramangala, CV Raman Nagar and others

5 Source: Colliers InternationalCOLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

DELINEATING THE NORTH North Bengaluru, indicative rents

North Bengaluru can be characterised by a greater number of standalone

Towards

buildings than in the IT parks in more mature micromarkets such as ORR and KIA

Whitefield. Grade A stock in North Bengaluru is about 4.0 million sq feet

(371,750 sq meters), and the robust supply pipeline is scheduled to inflate Yelahanka

North’s stock by over 140% by 2021.

North Bengaluru is typically delineated into two sections. The first section is

Thanisandra

from Hebbal Junction to Thanisandra Road while the second section Road

While ORR is likely commences at Yelahanka and extends towards KIA, with rents varying by up

to continue its to 38.0%.

Bellary Road

dominance, over Hebbal Junction and Thanisandra Road tend to see more active office leasing

the next five years than areas further north. The distance of only about 10 km (6.2 miles) to the Manyata Tech Park

we expect North CBD and ORR contributes to the leasing momentum in this micromarket.

Bengaluru to rise Around 57.0% of Grade A supply in the North over 2019-2021 is Hebbal Jn.

to the third choice concentrated in this stretch. In our opinion, the most immediate demand

for occupiers, after will spill over to this micromarket, especially for technology occupiers. Metro Red line

Colliers projects leasing activity in this micromarket to increase over the next

Whitefield. Road

three years. Rents INR78 (USD1.1) /sq ft/ month

Yelahanka is a relatively dormant market, where the rents are in the range of Rents INR48 (USD0.7) /sq ft/ month

INR45 per square foot per month to INR50 per square foot per month

Rental comparison (INR per square foot per month)

(USD0.6–0.7 per square foot per month), 40.0% lower than average citywide

rents. This may be compared to the citywide average of INR79.0 per square

foot per month (USD1.1 per square foot per month). Factors such as

distance from established residential catchment areas, around 16-20 Km (9-

12 miles) and the lack of residential and social infrastructure in the

micromarket make occupiers sceptical when considering leasing space in this 11% lower rents in Hebbal

micromarket. However, around 2.5 million sq feet (223,050 sq meters) of IT-

SEZ supply is planned through 2020, with most of this scheduled to come

online by mid-2019.

Comparable rentals between

Whitefield & Yelahanka

1USD=INR69.55 as on 31 December, 2018

Source: Colliers International

6COLLIERS RADAR OFFICE | RESEARCH | BENGALURU | 5 MARCH 2019

Key growth drivers, North Bengaluru micromarket Bengaluru supply outlook (2019-2021)

Increasing Others

Large and affordable CBD

5%

availability of residential Hebbal Jn. SBD

4%

premium quality catchment areas 7%

space 3.2 million sq ft

Yelahanka

North

15%

37.8 ORR

43%

mn sq ft

2.5 million sq ft

Development

Affordable

Potential: Upcoming

rents

Namma Metro, Whitefield

26%

available land

IT/ITeS IT- SEZ

Source: Colliers International Source: Colliers International

Moreover, with an upcoming supply of 5.7 million sq feet (520,445 sq

INCREASING SUPPLY FAVOURS THE meters) and 25.0% lower rents than in the ORR, we expect occupiers to

consider North Bengaluru for their future expansions.

NORTH We expect North Bengaluru to undergo transformation and cater to both

commercial and residential demand over the next five years. Currently,

Colliers forecasts increased leasing transactions in the ORR

sovereign wealth funds have formed joint ventures with developers for

micromarket over 2019-2021; however, demand momentum may premium Grade A offices under-construction in North Bengaluru. In addition,

not be sustained by supply. With ORR’s Grade A vacancy at 3.6% and our this micromarket is witnessing affordable residential developments catering

forecast of average annual supply of 5.4 million sq feet (501,858 sq meters) to the Gen X and Y population. For example real estate developer Embassy

over 2019-2021, ORR may mostly fall short in accommodating our estimate Group3 has tied up with the e-commerce giant Amazon to provide smart

of 6.0 million sq feet (557,620 sq meters) of average annual demand. As homes4 at affordable prices. Further, infrastructure projects such as the

Whitefield, Hebbal Junction and Yelahanka are the only micromarkets with Peripheral Ring Road, Red line of the Namma Metro and the ambitious

significant supply compared to their demand, we expect unmet demand to elevated corridors are planned to boost connectivity to this micromarket.

spill over to these areas.

Over the next five years, we expect this micromarket to house better

We anticipate Whitefield and North Bengaluru to gain traction. Over residential and social infrastructure. Colliers suggests occupiers should

the next three years, we expect Whitefield to witness a robust supply consider North Bengaluru for their future expansion plans.

pipeline of around 10 million sq feet (929,370 sq meters), the equivalent of 3https://tech.economictimes.indiatimes.com/news/technology/amazon-partners-embassy-group-for-

26.0% of citywide Grade A supply. The much anticipated completion of the alexa-enabled-smart-homes/64306540. 4A home equipped with lighting, heating, and electronic devices

metro rail connecting Whitefield by 2021 will further boost the demand in that can be controlled remotely by smartphone or computer.

7 this micromarket.Primary Authors: For further information, please contact:

Megha Maan Ritesh Sachdev

Senior Associate Director | Research | India Senior Executive Director | Occupier Services | India

+91 96 6718 8334 +91 99 4569 7377

megha.maan@colliers.com ritesh.sachdev@colliers.com

Teni Alice Abraham Arpit Mehrotra

Analyst | Research | Bengaluru Senior Director | Head - Office Services | Bengaluru & Hyderabad

+91 73 3865 9579 +91 99 6603 0144

teni.abraham@colliers.com arpit.mehrotra@colliers.com

Megha Maan

Senior Associate Director | Research | India

+91 96 6718 8334

megha.maan@colliers.com

About Colliers International Group Inc.

Colliers International Group Inc. (NASDAQ: CIGI) (TSX: CIGI) is a top tier global real estate services and investment management company operating in 69 countries with a workforce of more than 13,000 professionals.

Colliers is the fastest-growing publicly listed global real estate services and investment management company, with 2017 corporate revenues of $2.3 billion ($2.7 billion including affiliates). With an enterprising culture

and significant employee ownership and control, Colliers professionals provide a full range of services to real estate occupiers, owners and investors worldwide, and through its investment management services

platform, has more than $25 billion of assets under management from the world’s most respected institutional real estate investors.

Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice to accelerate the success of its clients. Colliers has been ranked among the top 100 global outsourcing firms by the

International Association of Outsourcing Professionals for 13 consecutive years, more than any other real estate services firm. Colliers is ranked the number one property manager in the world by Commercial Property

Executive for two years in a row.

Colliers is led by an experienced leadership team with significant equity ownership and a proven record of delivering more than 20% annualized returns for shareholders, over more than 20 years.

For the latest news from Colliers, visit our website or follow us on

Copyright © 2019 Colliers International

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any

inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.You can also read