The illusory promise of the livestock revolution - Meatification of diets, industrial animal farms and global food security

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The illusory promise of the livestock revolution Meatification of diets, industrial animal farms and global food security Thomas Fritz

The illusory promise of the livestock revolution

Meatification of diets, industrial animal farms and global food security

Thomas Fritz | FDCL| January 2014

Editor

Forschungs- und Dokumentationszentrum

Chile-Lateinamerika – FDCL e.V.

Gneisenaustraße 2a, D-10961 Berlin

Fon: +49 30 693 40 29 / Fax: +49 30 692 65 90

eMail: info@fdcl.org / Internet: http://www.fdcl.org

Author: Thomas Fritz

Publisher: FDCL-Verlag, Berlin

Layout: Monika Brinkmöller

Print: Copy House

Cover photo: Matt Mac Gillivray/ Flickr

This publication has been produced with

financial support from the European Union.

The contents of this publication are the sole

responsibility of publishing organisations

and can in no way be taken to reflect the views of the Euro-

pean Union. This publication is published within the frame-

work of the EU funded project „Put MDG1 back on track:

supporting small scale farmers, safety nets and stable mar-

kets to achieve food security“. Partners in the project are:

Glopolis (CZ), FDCL (DE), SOS Faim Belgium und SOS

Faim Luxembourg.

© FDCL-Verlag, Berlin, 2014 ISBN: 978-3-923020-63-8

The illusory promise of the livestock revolution Meatification of diets, industrial animal farms and global food security Thomas Fritz Berlin, January 2014

Contents

Introduction................................................................................................................... 3

Uneven development of the Livestock Revolution........................................................ 3

Inefficiency of industrial animal farms......................................................................... 5

Meaty diets’ land demand............................................................................................ 6

Volatile food prices and the competition between feed and food................................ 7

Meat production, trade and export dumping............................................................... 9

Livestock’s contribution to climate change................................................................. 11

Inclusive business models: leaving the poor behind.................................................. 13

Conclusion................................................................................................................... 14

2

Introduction

The recent worsening of the global food crisis, thors described as supply-driven, the Livestock

which had been sparked by sharply rising and Revolution was understood as demand-driven.

extremely volatile food prices in 2007-2008, Population growth, urbanisation and income

triggered a heated debate about its potential growth in the developing world would be fueling

drivers. Among the factors singled out com- the growing demand for animal-based products

modity speculation and the growing diversion like meat, milk and eggs.1

of crops to biofuels ranked high on the list of The joint report suggested that the Livestock

suspected culprits. Yet, the long-time trend of Revolution will be associated with major benefits

increasingly ‘meaty’ diets driven by industrial for consumers and producers alike. While con-

livestock production received far less attention, sumers could improve their nutrition by eating

although the channeling of enormous amounts more animal protein, producers would be offered

of cereals and oilseeds into feed troughs repre- valuable new income opportunities. The report

sents an important share of global harvests and claimed that growing demand for animal pro-

is known to be a highly inefficient way of using ducts would hold promise “for relieving wides-

plant protein and the land needed to grow these pread micronutrient and protein malnutrition”2,

crops. But even though the rapidly expanding and that the changing diets of billions of people

system of industrial factory farms draws so heav- “could provide income growth opportunities for

ily on harvests and increasingly scarce natural many rural poor”3, provided that proper policies

resources like land and water, it continues to be are put in place.

portrayed as a means for furthering global food The question being explored over the fol-

security and for providing livelihoods for poor lowing pages is if the perceived benefits of the

smallholders in the developing world. Livestock Revolution for the world’s poor have

Back in 1999, the United Nations Food and actually materialised so far. What will be un-

Agriculture Organisation FAO, together with the dertaken is a kind of reality check of some of

International Food Policy Research Institute IFPRI the expectations and promises surrounding the

and the International Livestock Research Institute global trend towards mass production of ani-

ILRI, argued in a joint report that global agri- mal-based food and increasingly meaty diets.

culture underwent a profound transformation, The lens through which this transition is being

dubbed the ‘Livestock Revolution’. Unlike the analysed is its impact on food security in the

earlier Green Revolution, which the report’s au- Global South.

Uneven development

of the Livestock Revolution

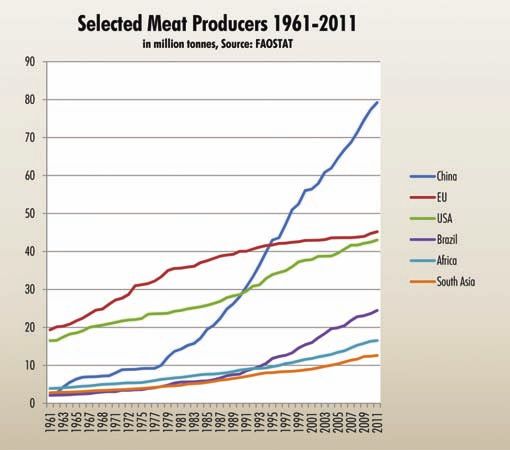

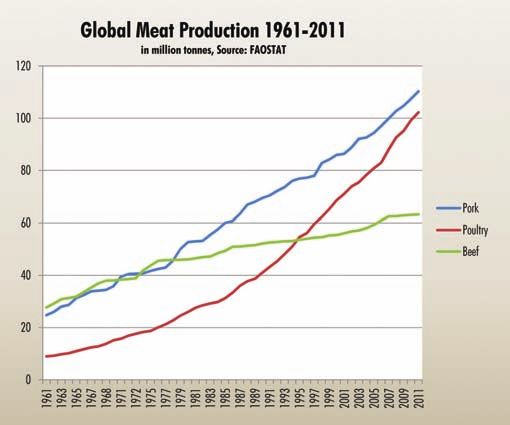

Although on a global scale production and con- pork, while beef production grew at a more mod-

sumption of meat indeed grew considerably est rate (see figure 1). Beginning in the 1980ies,

in the last decades, this trend actually exhibits China’s output climbed rapidly so that the Asian

very uneven patterns. Between 1961 and 2011, country is now the largest producer in the world,

global meat production has been risen from 71 followed by the EU and the US (see figure 2). Yet,

million tonnes to almost 299 million tonnes, with when assessing these figures, it has to be tak-

the sharpest increase reported for poultry and en into account that China with its 1.35 billion

3

Figure 1 people is far more populous than the

EU (507 million) and the US (317 mil-

lion). Africa and South Asia still register

pretty low meat outputs given that the

African continent is home to more than

one billion people, and India alone, as

the biggest South Asian nation, counts

some 1.2 billion people.

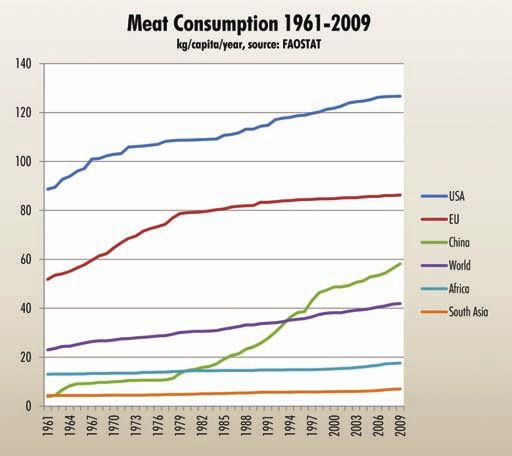

When it comes to consumption, the

geography of meat stills shows a signi-

ficant North-South divide, irrespective

of countries like China where per ca-

pita meat consumption has been cat-

ching up throughout the last decades.

According to FAO estimates, in 2012

per capita meat consumption in deve-

loped countries on average accounts

for 79 kilogramme per year, compared

to 33 kilogramme in the developing

Figure 2

world.4 But a closer look reveals even

larger disparities (see figure 3). While

the US consumes about 120 kg of

meat per capita annually and Western

Europe more than 80 kg, African con-

sumers have to make do with less than

18 kg and South Asians with a meagre

7 kg. Meanwhile, Chinese consumers

started to eat considerable amounts

of meat with roughly 60 kg per capita

and year, though this still equals only

half of US consumption.5

So, in fact, the Livestock Revolu-

tion in the developing world, measu-

red in production and consumption

growth, has mainly been concentrated

in a couple of faster growing emerging

economies like China or Brazil, whe-

reas large parts of Africa and South

Figure 3 Asia haven’t yet participated. While

Latin America, East and Southeast Asia

witnessed significant increases in per

capita meat consumption, Africa’s and

South Asia’s consumption remained

almost stagnant and in some cases is

even declining.6

But despite the concentration on

emerging markets, it has to be kept in

mind that these are highly populated

countries whose changing diets have

a strong impact on world agricultural

markets, the structures of the global

livestock industry and the natural re-

sources needed for the production of

animal-sourced foods. The growth ra-

tes of meat production and consump-

tion in the Global South are also far

4

higher than in the North. In the period 1991- half of the world’s pork output.9 Despite me-

2007, meat production and consumption in de- chanisation proving to be more complex for

veloping countries grew by more than 4 percent cattle farming than for poultry or swine, inten-

annually, compared to 0.7 percent in industria- sive cattle production systems are also on the

lised countries.7 rise, as can be seen by the growing number of

Though FAO predicts considerably lower feedlots where thousands of cattle are densely

future growth rates of meat consumption in confined in large outdoor installations.

the South (yearly rates of 1.7 percent in the Unlike mixed farming systems where feed-

period up to 2050), the ongoing growth would stuff and livestock production are locally

still pose a huge challenge for agriculture and linked, be it on the same farm or in a limited

eco-systems given that industrialised countries’ geographical area, industrial livestock systems

meat demand would also continue to grow by strongly depend on feed purchases on natio-

an estimated 0.7 percent annually until 2050. nal and international markets. The concentra-

If these predictions come true, this would mean ted compound feeds fed to the special breeds

that global meat production, which amounted of high-performing animals mainly consist of

to 299 million tonnes in 2011, could climb to grains and oilseeds which have frequently been

at least 455 million tonnes by 2050.8 shipped across long distances, with maize

It is expected that this growth will almost ex- and soybeans the most important feed crops

clusively by accounted for by industrial animal traded internationally. Due to their import de-

farms which already dominate the global pro- pendency, animal farms also shift the social

duction of poultry and pork. Industrial produc- and environmental impact of feed cultivation

tion systems contribute more than two thirds of to those countries where the required amounts

global poultry meat production and more than of crops are being produced.

Inefficiency of industrial animal farms

As global livestock systems are increasingly Yet, the conversion of feed crops into meat

shifting from using food waste, harvest residues, is highly inefficient, as a large proportion of

and grasses to farmed crops as main feed com- the plant energy contained in feed crops gets

ponents, growing amounts of cereals and oil- lost because animals use the biggest part of

seeds have to be directed to feeding animals. Of the acquired energy for their own metabolism.

the estimated 2.3 billion tonnes of cereals such A recent study at the University of Minnesota

as wheat, maize and barley produced global- (US) calculated the global losses of calories

ly in 2012/13, more than 800 million, some caused by the diversion of a group of 41

35 percent, end up in feed troughs.10 Similar- crops to animal feed.14 Of the calories pro-

ly, more than half of harvested oilseeds such as duced globally by these crops, 55 percent di-

soybeans and rapeseed also find their way into rectly feed humans, 36 percent feed animals

animal stomachs.11 Oilseed meals, the residues and the rest are being used for biofuels and

of oilseed crushing, have become the most im- other industrial purposes. Of the 36 percent

portant protein sources in industrial compound of calories diverted to animal feed, the lar-

feeds, with soybean meal the most frequently gest majority, some 89 percent, gets lost due

used protein. However, in industrialised coun- to animals’ metabolism, so that only about 4

tries with high levels of meat consumption the percent of all crop-produced calories will be

cereals proportion fed to animals is significantly available for human consumption in the form

higher. In the European Union, about 60 percent of animal products like meat, milk and eggs.

of the cereal harvest is used for animal feed,12 Adding these 4 percent to the 55 percent of

while farmers in sub-Sahara Africa and South crop calories directly feeding humans makes

Asia only divert between 10 and 15 percent of 59 percent of all crop calories serving human

cereal harvests to livestock feeding.13 nutrition either in the form of plant-based or

5

animal-based food. This means, conversely, dy, for example, estimates that “reducing the

that 41 percent of crop calories are lost to consumption of grain-fed animal products

animals (32 percent) or industrial purposes (9 by 50% would increase calorie availability

percent). enough to feed an additional 2 billion peo-

Due to the inherent inefficiency of feeding ple.”15 In addition, reducing the demand for

crops to livestock, a reduced consumption of animal-based food may also have a dampe-

animal-sourced foods could free enormous ning effect on the prices of those cereals and

amounts of crop calories for human con- oilseeds which currently serve as main feed-

sumption. The University of Minnesota stu- stuffs for animal farms.

Meaty diets’ land demand

The growing global livestock population Idel and Reichert maintain that “the data

greatly increases the demand for land, ei- indicating livestock as the world’s largest user

ther in the form of grazing land or in the of land are average values that also include

form of arable land dedicated to producing a relevant part of sustainably used grass-

feed crops. Of the roughly 5 billion hectares lands.”20 Thus, from a food security perspecti-

of agricultural land currently available on ve, the problem is not animals’ usage of land

earth, some 1.5 billion hectares are being per se, but factory farms’ growing demand for

used as arable land for crop cultivation, and animal feed occupying large chunks of global

about 3.4 billion hectares are grasslands cropland and reinforcing deforestation as well

like meadows and pastures.16 It is estimat- as the conversion of grassland to cropland. In

ed that one third of the cropland is devoted fact, it is the “industrial grain-oilseed-livestock

to producing animal feed.17 But the world’s complex”, as Tony Weis has called it, that is

grasslands are also largely used as grazing drawing so heavily on natural resources, the-

grounds, many of which still for extensive reby contributing to biodiversity loss, global

livestock farming where animals graze across warming and increasingly fierce land-use

large areas, as for example in the savannahs competition.21

of Africa, South America or Central Asia. It also cannot come as a surprise that be-

Adding the grazing grounds to the cro- hind many of the current land conflicts occur-

plands devoted to animal feed shows that ring across the globe meat consumption emer-

almost 80 percent of all agricultural land ges as a dominant cause. One of the hotspots

is used for raising animals, according to of these livestock-induced land-use conflicts is

FAO.18 However, as Idel and Reichert argue, South America where large-scale monocultu-

“the major issue is not whether livestock is res of soybean and maize plantations as well

the world’s largest user of land, but rather as cattle farms advance into highly biodiverse

how the land and livestock are managed”.19 ecosystems such as the Amazon rainforest or

Indeed, extensive livestock farming where the Brazilian Cerrado provoking sometimes

grasslands are used as grazing grounds for violent conflicts with indigenous peoples and

ruminants like cattle, sheep or goats may be small farmers trying to defend their customary

a largely sustainable production system, as land rights and their traditional modes of food

long as overgrazing and deforestation by production.22

cattle farms can be avoided. Due to rumi- However, a diet change towards reduced

nants’ ability to digest grass and hay, they consumption of animal-based foods could cer-

also do not by themselves compete with hu- tainly contribute to defuse the tensions associa-

mans for food, provided that farmers refrain ted with growing land-use competition. Several

from feeding them cereals and oilseeds to scenarios have already been calculated asses-

boost their output. sing the potential impact of ‘less meat’-diets

6

on global land-use. A study of PBL, the Nether- gy in Gothenburg (Sweden). The Swedish sci-

lands Environmental Assessment Agency, for entists assumed a 25 percent decrease in per

instance, examined the impact of a ‘healthy capita meat consumption only in high-income

diet’ with lower global meat consumption (52 countries such as the US, EU and Australia,

percent less beef, 35 percent less pork and 44 combined with a slightly lower food wastage

percent less chicken meat and eggs until 2050) rate at retail and household levels for the year

compared to a ‘business as usual’-reference 2030. According to this scenario, the required

scenario assuming a doubling of livestock pro- global agricultural area would be reduced by

duction. The scientists estimate that a transition 170 million hectares.24 These and other stu-

towards the ‘healthy diet’ could reduce the glo- dies show that already comparatively modest

bal cropland requirement by 135 million hecta- changes of consumption patterns in societies

res by the year 2050.23 with highly meaty diets could lead to signi-

Another scenario has been calculated by ficant freeing up of land resources currently

scientists of Chalmers University of Technolo- occupied for feeding animals.

Volatile food prices and the

competition between feed and food

The inventors of the Livestock Revolution no- system of global markets, the report argued,

tion where pretty optimistic that the huge di- “individual shocks are smoothed out over time

version of cereals and oilseeds for animal feed through myriad adjustments throughout the

wouldn’t be a threat for the food security of system”.26

consumers depending on cereals as their most Yet, contrary to the belief of the experts,

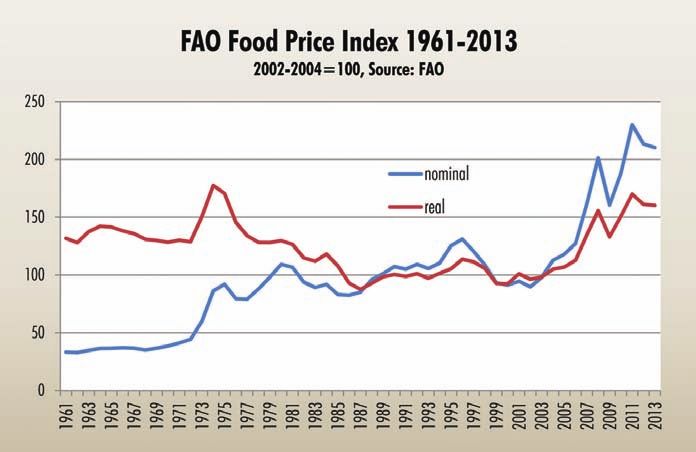

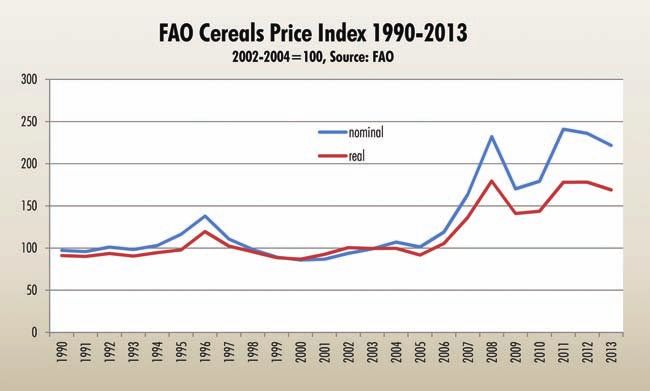

basic food item. In their 1999 report, FAO, IF- beginning in 2007, food prices reversed their

PRI and ILRI wrote that despite growing feed- three-decades-long depression and shot up

stuff demand, “real cereal prices, however, are sharply, with two peaks in 2008 and 2011

not likely to rise very much by 2020”.25 The (see figure 4). Cereal prices followed the same

reason for their as-

sumption of continu-

ing low cereal prices Figure 4

was that “the world is

thought to have con-

siderable reserve ca-

pacity for additional

cereal production”.

The important cereal

producers Austral-

ia, Canada and the

US were believed

to have the ability

to bring addition-

al amounts of land

into cereal produc-

tion and to consid-

erably boost yields

by increasing ferti-

lizer use. And in the

7

Figure 5 general trend of spiking

food prices (see figure

5). Although it is difficult

to forecast future price

trends, most analysts now

expect that at least in the

medium term prices will re-

main higher and volatility

may become a more com-

mon feature of agricul-

tural markets. The recent

OECD-FAO Agricultural

Outlook to the year 2022,

for instance, confirms this

assessment: “Slower pro-

duction growth in com-

bination with strong and

rising demand, are pro-

Figure 6 jected to hold agricultural

product and fish prices

collectively at historically

high levels.” Sluggish

production growth, in

turn, would also “slow-

down the replenishment

of stocks making com-

modity markets more su-

sceptible to high price vo-

latility”.27

The trend towards

higher and more volatile

food prices threatens the

food security of all those

developing countries who

became net food impor-

ters. With the outbreak

of the debt crisis in the

1980ies many developing

Figure 7 countries turned from net

exporters to net impor-

ters of agricultural pro-

ducts. Trade liberalisation

and structural adjustment

programmes imposed by

the World Bank and the

IMF led to the erosion of

their traditional surplus

in agricultural trade. The

international financial

institutions forced Sou-

thern governments to cut

support for domestic ag-

riculture, open markets

for food imports, and to

switch from staple food

production for local mar-

8kets to cash crop cultivation for export mar- more pronounced than that of the quantities

kets. But due to stagnating demand and de- imported, especially in recent years in view of

clining prices for tropical products (such as soaring food prices”, as trade expert Panos Ko-

coffee, cocoa, tea or bananas), the switch to nandrea showed.30 While NFIDCs’ volume of

cash crop exports did not result in sufficient cereal imports grew by 70 percent, their cereal

trade revenues to compensate for the growing import bills increased almost four-fold in the

imports of basic food items such as cereals, period 1994-2012. Konandrea estimates that

vegetable oils and fats.28 the soaring prices have been responsible for

Due to their growing agricultural trade de- 56 percent of the increase in the import bills.

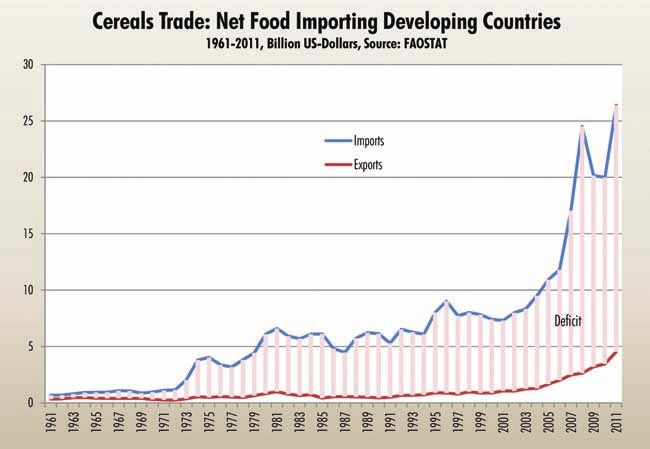

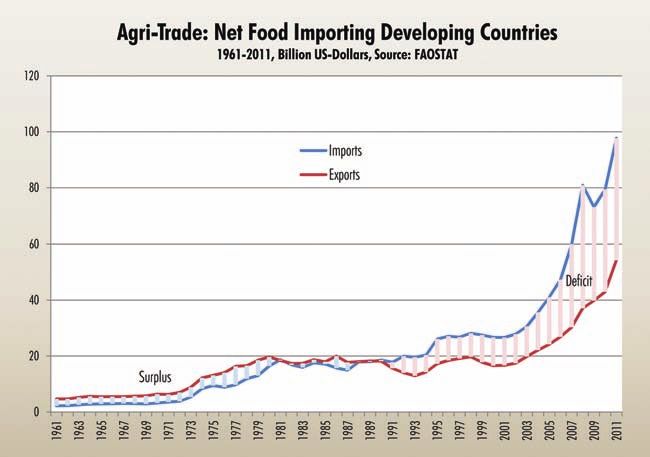

ficit, Net Food Importing Developing Coun- Since higher cereal prices on the internati-

tries (NFIDCs: 79 countries) are particularly onal market may translate into price increases

vulnerable to price spikes on the international on the domestic markets, albeit to a varying

markets (see figure 6). Cereals are the most degree, poor consumers might be forced to

important item in the food import basket of cut back on staple food purchases, as was al-

these countries, accounting for more than 40 ready the case during the global food crisis

percent of the value of all food imports. Parti- of 2008. The diversion of growing amounts of

cularly in the last couple of years, their cereal cereals into feed troughs belongs to the impor-

import deficit increased rapidly approaching tant causes putting upward pressure on glo-

almost 22 billion US$ in 2011 for all NFIDCs bal cereal prices. Rising meat consumption is

(see figure 7). As a consequence of their lost thus intimately linked to the current price trend

self-suffiency, NFIDCs on average are rely- and the ensuing food security risks for poor

ing on imports for 30 percent of their cereal consumers in the developing world. By cont-

consumption; in several countries the import rast, a more generalised transition towards a

share is even higher.29 low-meat diet could have a dampening effect

Many of these countries are now paying a on food prices, as an IFPRI study suggests. In

heavy price for their import-dependency, what its low-meat scenario assuming a 50 percent

is being reflected in their rising import bills. reduction of meat consumption in high-income

Although NFIDCs also increased the volumes countries by 2030, prices for cereals, meat and

of cereal imports in the last years, the “increa- meal drop significantly, particularly if the diet

se in the cost of cereal imports has been much change would also occur in China and Brazil.31

Meat production, trade and export dumping

The Livestock Revolution would not have been zil and Argentina. The US, the EU and Brazil are

possible without accompanying growth of global heading the list of the world’s largest meat ex-

trade in feedstuffs and animal products. On the porters, while the EU and New Zealand domina-

input side, industrial livestock farms depend on te the global dairy export market. Whereas only

cheap supplies of cereals and oilseeds for ani- a small group of developing countries managed

mal feed which are provided by only a handful to increase feedstuff and meat exports, notably in

of global suppliers; on the output side they need South America, the large majority of developing

low trade barriers to export their surplus produc- countries depends not only on imports of cereals

tion of meat and milk given that rich countries’ but also of animal products like meat and milk.

markets are widely saturated. In fact, as long as these countries’ consumption

Exports of feedstuffs and animal products are continues to grow faster than production, their

both highly concentrated among a few key play- import-dependency is also due to grow. What

ers. Major exporters of wheat are the US, EU, is more, in the near future cereals and oilseeds

Canada, Australia and Russia, while maize and imports in food-deficit developing countries may

soybean exports mainly originate in the US, Bra- not only be driven by direct human consumption

9Figure 8 concerns only a hand-

ful of countries, and the

trade between surplus and

deficit countries is expec-

ted to grow. This situation

implies “a vulnerability of

a large number of deve-

loping countries, notably

African countries, to any

world market disturbances

and the crucial need for

securing access to world

imports”, as the INRA re-

searchers emphasize. But

the challenge for the lar-

ge majority of developing

countries doesn’t stop

here, because it also has

to be ensured “that trade

Figure 9 rules do not penalize lo-

cal agricultural production

growth, which is required

for reducing poverty and

malnutrition”.34

Yet, unfortunately, glo-

bal trade policies largely

fail to protect smallholders

in the developing world

from the surplus pro-

duction of animal-based

foods generated by the

Livestock Revolution. The

European surplus pro-

duction of poultry meat is

a case in point. Although

internal demand is largely

saturated, domestic poul-

try production continues

to grow together with ex-

needs but also indirectly by increasing demand ports. In the period 2006-2012, EU-27 chicken

for animal feed, depending on the speed and meat exports more than doubled from 690.000

extent of factory farms’ expansion in the Glo- tonnes to 1.4 million tonnes, with the main

bal South.32 exporting Member States being France, the

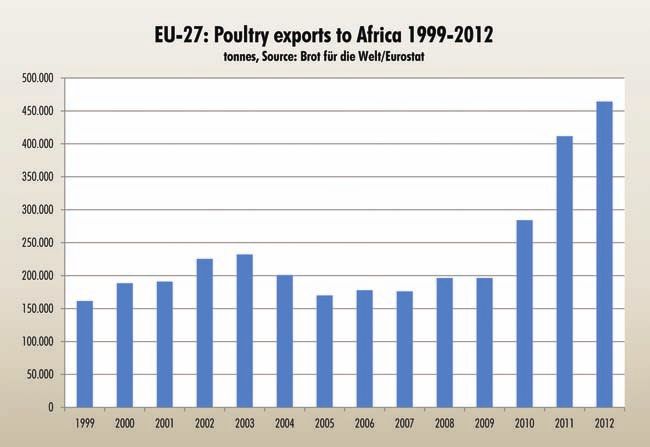

Referring to the concentration among the Netherlands and Germany.35 The African con-

main suppliers, scientists of the French Nati- tinent belongs to the main export destinations

onal Institute for Agricultural Research INRA absorbing more than a third of all EU broiler

provide an image of the 2050 global land- exports, with South Africa, Benin and Ghana

scape with regards to agricultural trade: “a the main markets (see figure 8). Especially in

world divided into two groups of regions with the last three years, EU poultry exports to Africa

one group (OECD, Latin America, and the soared strongly reaching more than 450.000

former Soviet Union) enjoying an agricultu- tonnes in 2012 (see figure 9).

ral surplus and supplying the three regions However, many African countries suffer se-

with a deficit (Asia, Middle East and North verely from the import surges of cheap chicken

Africa, and sub-Saharan Africa).”33 Basically, meat disrupting the market for thousands of

the perspective is even worse as the concent- smallholders breeding chickens in their backy-

ration among the main agricultural exporters ards, on small-scale poultry farms or on the few

10semi-industrial farms in urban and suburban The policy prescriptions requested by the Eu-

areas. Small-scale poultry farming is very wides- ropean Commission include tariff standstill

pread in Africa as poultry and egg production commitments, restrictions on the use of tariff

serves as an important complementary sour- rate quotas and prohibitions of import licen-

ce of nutrition and income for millions of poor ses. 38 In most EPAs the Commission demands

households.36 the inclusion of a so-called ‘standstill clause’

EU exports to Africa consist mainly of frozen prohibiting the introduction of any new tariffs

chicken pieces like wings, legs, necks and gib- or the raising of existing tariffs. 39 Thus, the

lets. The growing trade with these minor broiler policy space of African governments to pro-

parts is a result of changing consumption pat- tect domestic poultry breeders against floods

terns in Europe, where consumers prefer easy of cheap EU chicken imports may be severely

to prepare fresh chicken pieces, particularly constrained.

chicken breast, instead of whole birds. Due to The difficulties of South Africa, which suf-

these changes, the poultry industry makes high fers from chicken imports originating mainly

profits with breast meat sales in Europe, ena- in Brazil and the EU, could be a warning to

bling the sale of other chicken parts at extre- all the ACP countries currently negotiating an

mely low prices on African markets. Often the EPA. To protect the domestic poultry industry,

imported chicken meat is sold at prices about which is made up of a larger industrial and

50 percent lower than meat derived of local a more limited smallholder sector, South Afri-

chickens. As a consequence, lots of small and ca raised tariffs on five categories of chicken

medium-scale producers in countries like Gha- products in September 2013. But due to a free

na, Senegal or Cameroon already lost market trade agreement with the EU, the so-called

share or were forced to close down in the last Trade, Development and Cooperation Agree-

decade following import surges of cheap chi- ment (TDCA) of 1999, the tariff increases will

cken meat.37 only hit suppliers from outside the EU, as the

European chicken dumping, however, has import duty for EU chicken had to be phased

also provoked resistance by African poul- out.40 But South African producers maintain

try breeders and farmers prompting some that European chicken causes the main pro-

governments to impose import restrictions (im- blem because EU producers largely dominate

port quotas, higher tariffs, or outright import the imports of frozen chicken pieces. Accor-

bans), as in the cases of Nigeria, Camero- ding to the South African Poultry Association

on and Senegal. But in the future application (SAPA), “in the three years from 2010, the

of such measures may violate liberalisation EU has gone from a market share of 0.5% in

commitments contained in the Economic Part- chicken pieces to 70%”.41 The South African

nership Agreements (EPAs) currently being government is now investigating the possibility

negotiated between the EU and 75 African, of applying anti-dumping measures on chi-

Caribbean and Pacific region countries (ACP). cken imports from the EU.

Livestock’s contribution to climate change

Industrial meat production may also impair degraded lands and the poorest part of the ru-

food security by contributing to climate change. ral population with little adaptation capacity.”42

The impacts of global warming on agriculture A study by economist William Cline provi-

tend to be more severe in the Global South with des an estimate of the potential agricultural

its higher initial temperatures and lower levels of output changes assuming a 5°C surface tem-

development. As the UN Conference on Trade perature increase of the land area by 2080.43

and Development UNCTAD warns: “Particularly According to Cline’s calculations, agriculture’s

hard hit will be areas with marginal or already output would drop most sharply in developing

11Table 1 through livestock’, FAO

Global warming: changes of agricultural output potential by 2080 revised its previous figure

downwards, now estima-

Without carbon fertilisation With carbon fertilisation ting livestock’s share of

Industrial Countries -6.3 7.7 total anthropogenic emis-

sions at 14.5 percent (yet,

Developing Countries -21.0 -9.1

livestock’s absolute emis-

Africa -27.5 -16.6 sions of 7.1 gigatonnes of

Asia -19.3 -7.2 CO2-eq (carbon dioxide

equivalents) remained con-

Latin America -24.3 -12.9 stant in both reports).46

Source: Cline, William R, 2008: Global Warming and Agriculture. Despite livestock’s lar-

In: Finance & Development, March 2008, pp. 23-27 ge contribution to global

warming, FAO’s recom-

Figure 10 mendations focus exclusi-

vely on mitigation options

in the production process

without considering the

option of reduced con-

sumption – a deficit which

provoked some criticism

because changes in con-

sumption patterns could

be more effective.47 Never-

theless, some studies alrea-

dy calculated the potential

impact of a diet change

on global warming. The

study of the Netherlands

Environmental Assessment

Agency PBL, for instance,

examined the impact of its

‘healthy diet’ scenario (52

percent less beef, 35 per-

countries, even when carbon fertilisation effects cent less pork and 44 percent less chicken meat

are being factored in (see table 1). Carbon ferti- and eggs) compared to a reference scenario as-

lisation refers to the phenomenon that, although suming a doubling of livestock production until

warming generally tends to reduce crop yields, 2050. Greenhouse gas emissions in the healthy

the growth of some plants (so-called C3 crops) diet variant are about 10 percent lower than in

may actually increase due to certain levels of the reference scenario.48

higher carbon dioxide concentrations in the Another assessment commissioned by the

atmosphere. As can be seen in table 1, while European Commission calculated the impact

industrial countries’ yields could either mode- of three different scenarios of dietary changes

rately decrease or, when including carbon fer- in the EU-27 for the year 2020: 1) a vegeta-

tilisation, even increase due to climate change, rian diet; 2) a recommended healthy diet (re-

developing countries would suffer significant ducing daily intake to 2,500 kilocalories and

output losses, also when carbon fertilisation is eating 500 grams of fruits and vegetables);

accounted for. 3) one day per week without animal products

Livestock production, especially in inten- (amounts to a reduction of 14 percent).49 If all

sive systems, contributes considerably to glo- EU citizens shift to the vegetarian diet, total

bal warming, although the extent is subject of food-related emissions in 2020 would drop

some debate.44 In its 2006 report ‘Livestock’s by about 40 percent compared to the current

long shadow’, FAO estimated that livestock diet. Shifting to the healthy diet reduces emis-

activities contribute 18 percent to total human- sions by roughly 30 percent, and the weekly

induced greenhouse gas emissions.45 Howe- animal-free day drops emissions by 8 percent

ver, in its 2013 report ‘Tackling climate change (see figure 10).

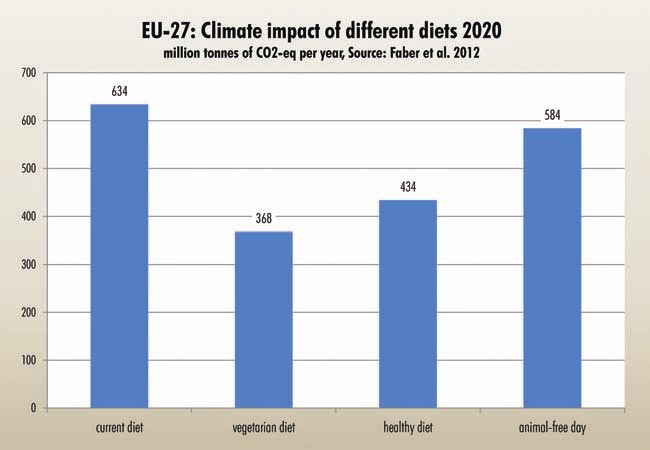

12Similar examinations on national levels reduce greenhouse gas emissions from prima-

confirm this outcome. A report for the United ry production by 19 percent.50 These and other

Kingdom’s Committee on Climate Change assessments show that a global diet change

estimates that a 50 percent reduction in live- could indeed contribute to considerable emis-

stock product consumption (36 percent less sions reductions and would certainly help in

meat, 60 percent less milk and eggs) would the endeavour of cooling the planet.

Inclusive business models:

leaving the poor behind

While not denying the considerable environmen- tion strategies of Western development agenci-

tal and social risks of the Livestock Revolution, the es – could provide pathways out of poverty for

authors of the landmark 1999 FAO, IFPRI and those most in need. “It must be recognised”, the

ILRI report were nevertheless upbeat about the authors admit, “that the majority of agricultural

possibility of spreading its benefits more broad- and rural households in developing countries

ly. They claimed that the risk for poor livestock are unlikely to be recruited directly into agrifood

keepers of being driven out of their traditional industrialisation; even intermediate stages of

markets could be minimised by integrating them sector consolidation, such as contract farming,

into the supply chains of large livestock proces- appear to be undertaken at a scale well beyond

sors through contract farming or the creation of that of the average smallholder farmer.”54

producer cooperatives. This strategy would be Indeed, the as yet rather scarce evidence on

promising since the Livestock Revolution repre- smallholders’ ability to stay in business and to

sented “one of the few dynamic economic trends link up with integrators or processors in fast mo-

that can be used to improve the lives of poor dernising countries is disillusioning. “The study

rural people in developing countries”.51 results in almost all the cases involving pigs and

More than a decade after the proclamation poultry suggest that the smallest independent

of the Livestock Revolution, FAO continues to livestock farms will increasingly have a hard time

spread an optimistic message about its potential remaining in business”, an IFPRI report analy-

benefits, yet its contradictions are also becoming sing the cases of Thailand, the Philippines, India

more visible. A book of its Pro-Poor Livestock and Brazil concludes.55 For commodities such as

Policy Initiative, published in 2012, asserts on broilers and eggs “smallholders in all four coun-

the one hand that the expanding markets for tries have been rapidly losing market share”.56

animal-sourced food in developing countries In the Thai case, the number of smallholders en-

“represent enormous income potential for the gaged in livestock production “has significantly

rural poor, many of whom own livestock”.52 Yet decreased over the last 15 years”.

on the other hand, the authors are pretty frank Evidence from Brazil shows that high levels of

about the limits of this trend by acknowledging indebtedness drove many contract farmers out

that livestock’s potential for poverty reduction of business. Small-scale swine farms exited the

“remains largely untapped”. Among the reasons livestock sector “after they took out loans to in-

for this rather disappointing outcome they men- crease the size of their operations at the request

tion market imperfections, the lack of public ser- of integrators who refused to renew contracts

vices and a “systematic bias towards industriali- with producers with only a few animals, and then

zation and concentration favouring large- over were unable to repay”. The IFPRI report suggests

small-scale operators”.53 that integrators such as slaugtherhouses or dai-

It might appear even more surprising that the ries “have a financial incentive to contract with

FAO scientists openly dismiss the idea that con- larger farms” which will “eventually capture

tract farming and other supposedly ‘inclusive’ market share from smallholders”.57 Summing up

business models – one of the preferred interven- the experiences made so far, FAO expert Jeroen

13Dijkman asserts that the idea traditional small- to complement this approach “with safety net

holders could climb up the ‘livestock ladder’ by programmes to support the most vulnerable”.61

gradually scaling up their production “is largely The livestock development strategy promo-

a myth.”58 ted by international organisations like FAO,

Having read this finding one would expect IFPRI and ILRI actually resembles more a de-

FAO experts to start devising alternatives to the claration of surrender to the forces of the indus-

apparently inadequate contract farming strate- trial livestock complex than a poverty-sensitive

gy. But far from it. They rather recommend that approach where the most vulnerable smallhol-

“reforms in the livestock sector should preferably ders take centre stage. After admitting that the

target the ‘not-so-poor’ farmers”59, the so-called highly praised linkages of contract farmers with

‘upper’ smallholder livestock keepers, “who commercial livestock processors won’t work for

have the minimum asset base for engaging sus- the large majority of poor smallholders, they

tainably in market-oriented livestock production, are taking recourse to the unconvincing opti-

rather than focusing on marginal livestock kee- on of social protection. Their advice effectively

pers”.60 Apparently aware of the social conse- boils down to putting the poorest off by propo-

quences of their advice, FAO scientists acknow- sing safety nets which in many cases may never

ledge that “this strategy is likely to increase rural materialise given either the precarious state of

wealth disparities”. Given that their highly selec- governments’ budgets or the unwillingness of

tive integration strategy excludes the large majo- ruling classes to invest in social programmes

rity of poor livestock keepers, they recommend at all.

Conclusion

In contrast to the rather optimistic expectations se factory farms strongly depend on growing

some international organisations associated with supplies of farmed feed purchased on world

the Livestock Revolution, it seems that the evidence markets. But the conversion of feed crops into

collected so far requires a more skeptical view, animal products such as meat is highly ineffici-

particularly with regards to the poverty impact. ent, as a large proportion of plant energy gets

What is true is that the Global South indeed wit- lost to animal’s own metabolism. This inherent

nessed a growing production and consumption of inefficiency is often overlooked by those clai-

animal-sourced food, albeit more concentrated ming the potential nutritional benefits of gro-

in faster growing emerging economies like China wing meat consumption.

or Brazil, whereas large parts of Africa and South The fierce land-use competition driven by

Asia haven’t yet participated in this process. But feed demand, causing deforestation and land

despite the concentration on emerging markets, it grabbing, further calls into question the per-

has to be kept in mind that these are often highly ceived benefits of the Livestock Revolution for

populated countries whose changing diets have a global food security, as does livestock’s large

strong impact on world food markets and on the contribution to global warming. Furthermore,

related demand for natural resources. In addi- the diversion of growing amounts of cereals

tion, it cannot be ruled out that other developing into feed troughs belongs to the important

countries will also experience a similar transition causes putting upward pressure on global ce-

in the years to come. reals and food prices, already expected to be

The most crucial problem, however, is that higher and more volatile for the foreseeable

growing livestock production will almost ex- future. Rising meat consumption is thus inext-

clusively by accounted for by industrial animal ricably linked to the current price trend and the

farms which already largely dominate the glo- ensuing food security risks for poor consumers

bal production of poultry and pork. Due to the in the developing world.

breeding of high-yielding animals and the de- Another risk for food security is facto-

coupling of crop and livestock production, the- ry farms’ surplus production, large parts of

14which is being dumped on developing coun- ‘less-meat’ diets for cooling the planet, defu-

tries’ markets, thereby pushing smallholders sing land conflicts and dampening the food

and less competitive commercial producers price increase, this option is either not pursu-

out of the business. This risk for poor livestock ed with the required vigour or entirely disre-

holders is being compounded by free trade garded, particularly by some of the influential

agreements restraining the protection of lo- international organisations as well as official

cal markets against import surges, as is the agricultural and consumer policies.

case with the Economic Partnership Agree- So it is up to civil society, NGOs and soci-

ments currently being negotiated between the al movements to reverse the trend towards the

EU and ACP countries. The hope that sizeable meatification of diets and to challenge the ‘in-

amounts of poor smallholders might eventu- dustrial grain-oilseed-livestock complex’ fier-

ally benefit by linking up with livestock pro- cely defending the profits extracted out of this

cessors through contract farming has also not socially and environmentally destructive pro-

materialised. Generally, it is only a minority duction system. This priority also requires to

of larger farmers which is being contracted, question widespread dietary aspirations among

while smallholders increasingly face the risk of societies, as Tony Weis reminds: “While the me-

being driven out of their traditional markets. atification of diets has long been held as a goal

Given the enormous social and environ- and measure of development and a marker of

mental risks associated with the Livestock class ascension, it should instead be understood

Revolution, a dietary change reducing the as a vector of global inequality, environmental

consumption of animals products, particular- degradation, and climate injustice.”62 Indeed,

ly among the more wealthy income groups, the perception of meat consumption as a sign

emerges in many respects as one of the most of a desirable wealthy western lifestyle belongs

effective remedies. But despite the benefits of to the challenges to be overcome.

Endnotes

1 Delgado, Christopher, et al., 1999: Livestock to 2020 13 Erb, Karl-Heinz, et al., 2012: The Impact of Industrial

– The Next Food Revolution. IFPRI, FAO, ILRI, Washing- Grain Fed Livestock Production on Food Security: an

ton May 1999 extended literature review. Vienna, February, p. 33

2 Ibid, p. 60 14 Cassidy, Emily S, et al., 2013: Redefining agricultural

3 Ibid, p. 1 yiels: from tonnes to people nourished per hectare. In:

Environmental Research Letters Volume 8 , Number 3,

4 FAO, 2013: Food Outlook. November 2013, Rome July-September 2013, 034015, doi:10.1088/1748-

5 Figures derived of FAO’s food supply database at 9326/8/3/034015

FAOSTAT. http://faostat3.fao.org/faostat-gateway/go/ 15 Ibid, p. 6

to/download/C/CL/E (consulted December 2013)

16 Alexandratos, Nikos/Bruinsma, Jelle, 2012: World Agri-

6 Pica-Ciamarra, U./Otte, J., 2009: The ‘Livestock Rev- culture Towards 2030/2050: The 2012 Revision. FAO,

olution’: Rhetoric and Reality. Pro-Poor Livestock Policy ESA Working Paper No. 12-03, June, Rome, p. 102

Initiative, Research Report, November. FAO, 2009: The

State of Food and Agriculture 2009: Livestock in the 17 FAO, 2009: The State of Food and Agriculture 2009:

balance, Rome Livestock in the balance, Rome

7 Alexandratos, Nikos/Bruinsma, Jelle, 2012: World 18 Ibid

Agriculture Towards 2030/2050: The 2012 Revision. 19 Idel, Anita/Reichert, Tobias, 2013: Livestock Production

FAO, ESA Working Paper No. 12-03, June, Rome and Food Security in a Context of Climate Change and

8 Ibid Environmental and Health Challenges. In: UNCTAD

2013, Trade and Environment Review 2013: Wake up

9 FAO, 2009: The State of Food and Agriculture 2009: before it is too late – Make agriculture truly sustainable

Livestock in the balance, Rome now for food security in a changing climate. Geneva,

10 FAO, 2013: Food Outlook, November 2013, Rome pp. 137-170

11 Erb, Karl-Heinz, et al., 2012: The Impact of Industrial 20 Ibid, p. 138

Grain Fed Livestock Production on Food Security: an 21 Weis, Tony, 2013: The meat of the global food crisis.

extended literature review. Vienna, February, p. 33 The Journal of Peasant Studies, 40:1, pp. 65-85, DOI:

12 See EU cereals balance sheets: http://ec.europa.eu/ 10.1080/03066150.2012.752357

agriculture/cereals/balance-sheets/index_en.htm

1522 Fritz, Thomas, 2013: Bread or Trough: Animal Feed, Com- 42 Hoffmann, Ulrich, 2011: Assuring food security in

petition for Land and Food Security. FDCL, Berlin, January developing countries under the challenges of cli-

23 Stehfest, Elke, et al., 2009: Climate benefits of chang- mate change: key trade and development issues of a

ing diet. In: Climatic Change. 2009. 95, pp. 83-102 fundamental transformation of agriculture. UNCTAD,

Discussion Papers, No 201, February, p. 3

24 Wirsenius, Stefan, et al., 2010: How much land is

needed for global food production under scenarios of 43 Cline’s scenario concentrates on land areas, i.e.,

dietary changes and livestock productivity increases in oceans (which warm less than land) have been

2030? In: Agricultural Systems, Volume 101, Issue 9, excluded. In this scenario the global mean warming,

November 2010, pp. 621–638 including oceans and land, is estimated at about 3°C

by 2080. See: Cline, William R., 2008: Global Warm-

25 Delgado, Christopher, et al., 1999: Livestock to 2020 – ing and Agriculture. In: Finance & Development, March

The Next Food Revolution. IFPRI, FAO, ILRI, Washington 2008, pp. 23-27

May 1999, p. 36.

44 See, for instance, Goodland, Robert/Anhang, Jeff,

26 Ibid 2009: What if the key actors in climate change are

27 OECD, FAO 2013: OECD-FAO Agricultural Outlook cows, pigs, and chickens? World Watch, November/

2013-2022: Highlights, p. 22 December 2009, pp. 10-19. See also the response

28 Fritz, Thomas, 2011: Globalising Hunger: Food Secu- to Goodland and Anhang by Herrero, M., et al.,

rity and the EU’s Common Agricultural Policy (CAP). 2011: Livestock and greenhouse gas emissions: The

Berlin, November, pp. 38-43 importance of getting the numbers right. Animal Feed

29 Konandrea, Panos, 2012: Trade Policy Responses to Science and Technology, 166-167:779-782

Food Price Volatility in Poor Net Food-Importing Coun- 45 FAO, 2006: Livestock’s long shadow: environmental

tries. ICTSD/FAO, Issue Paper No. 42 issues and options. Livestock, Environment and Devlop-

30 Ibid, p. 19 ment Initiative (LEAD), Rome

31 Msangi, Siwa/Rosegrant, Mark W., 2011: Feeding the 46 FAO, 2013: Tackling climate change through livestock

Future’s Changing Diets – Implications for Agriculture – A global assessment of emissions and mitigation

Markets, Nutrition, and Policy. Advance Copy, IFPRI, opportunities. Rome

2020 Conference Paper 3, February 47 See: http://www.eating-better.org/blog/19/Eating-Bet-

32 Guyomard, Hervé, et al., 2013: Trade in feed grains, ter-responds-to-new-FAO-Livestock-report.html, http://

animals, and animal products: Current trends, future pros- www.earthisland.org/journal/index.php/elist/eListRead/

pects, and main issues. In: Animal Frontiers, January 2013, fao_underplays_impact_of_livestock_industry_emissions/

Vol. 3, No. 1, pp. 14-18. FAO, 2009: The State of Food 48 Stehfest, Elke, et al., 2009: Climate benefits of chang-

and Agriculture 2009: Livestock in the balance, Rome. ing diet. In: Climatic Change. 2009. 95, pp. 83-102

33 uyomard, Hervé, et al., 2013: Trade in feed grains, 49 Faber, Jasper, et al., 2012: Behavioural Climate

animals, and animal products: Current trends, future Change Mitigation Options. Domain Report Food, CE

prospects, and main issues. In: Animal Frontiers, Janu- Delft, Fraunhofer ISI, LEI Wageningen UR, Delft, April

ary 2013, Vol. 3, No. 1, pp. 14-18. 50 Audsley, Eric, et al., 2011: Food, land and greenhouse

34 Ibid, p. 17 gases: The effect of changes in UK food consumption

35 Figures derived of the last USDA GAIN Reports: EU-27 on land requirements and greenhouse gas emissions. A

Poultry and Products Annuals 2011 and 2012. EU-28 report prepared for the United Kingdom’s Commission

Poultry and Products Annual 2013. See also: European on Climate Change. Cranfield University, Murphy-Bok-

Commission 2012: Agriculture in the European Union: ern Konzepte, April

Statistical and Economic Information Report 2012. 51 Delgado, Christopher, et al., 1999: Livestock to 2020

European Union, Directorate-General for Agriculture – The Next Food Revolution. IFPRI, FAO, ILRI, Washing-

and Rural Development, p. 316 ton May 1999, p. 64-65

36 Fritz, Thomas, 2011: Globalising Hunger: Food Secu- 52 Otte, J., et al., 2012: Livestock sector development for

rity and the EU’s Common Agricultural Policy (CAP). poverty reduction: an economic and policy perspective

Berlin, November, pp. 70-78 – Livestock’s many virtues. FAO, Rome, p. xvi

37 EED, ACDIC, ICCO, APRODEV, 2007: ‘No more 53 Ibid

chicken, please’, November 2007 54 Ibid

38 CTA, 2012: agritrade, Executive brief, Poultry sector, 55 Delgado, Christopher L., et al., 2008: Determinants

update August 2012. Technical Centre for Agricultural and Implications of the Growing Scale of Livestock

and Rural Development, Wageningen Farms in Four Fast-Growing Developing Countries.

39 ODI/ECDPM, 2009: ‘The Interim Economic Partner- IFPRI Research Report 157, Washington, p. 121.

ship Agreements between the EU and African States 56 Ibid, p. 114.

– ODI/ECDPM, ‘The Interim Economic Partnership 57 Ibid, pp. 121-122

Agreements between the EU and African States – Con-

tents, challenges and prospects’, Overseas Develop- 58 Dijkman, Jeroen, 2009: Innovation Capacity and the

ment Institute/European Centre for Development Policy Elusive Livestock Revolution. In: LINK Learning, Innova-

Management, July 2009 tion Knowledge, United Nations University UNU-MERIT,

News Bulletin, October 2009, p. 1-4

40 The Poultry Site, 2013: Global Poultry Trends 2013:

Chicken Imports Rise to Africa, Stable in Oceania. 13 59 Otte, J., et al., 2012: Livestock sector development for

November 2013 poverty reduction: an economic and policy perspective

– Livestock’s many virtues. FAO, Rome, p. xvii

41 Agritrade, 2013: South African poultry sector problems

compounded by rising EU exports. CTA Technical Cen- 60 Ibid, p. 130

tre for Agricultural and Rural Cooperation (ACP-EU), 61 Ibid, p. 131

15 April 2013 62 Weis, Tony, 2013: The meat of the global food crisis.

The Journal of Peasant Studies, 40:1, p. 81

16The illusory promise of the livestock revolution Meatification of diets, industrial animal farms and global food security Thomas Fritz | FDCL| January 2014

You can also read