THE CORDANT FINANCIAL ASSESSMENT - PREPARED FOR: Sample - Cordant Wealth

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE

CORDANT

FINANCIAL

ASSESSMENT

PREPARED FOR:

Sample

TABLE OF CONTENTS

1. WEALTH SNAPSHOT

2. COMPANY STOCK ANALYSIS

3. COMPANY BENEFITS ANALYSIS

4. PORTFOLIO REVIEW

5. TAX ASSESSMENT

6. “ON TRACK” ASSESSMENT

7. WEALTH ACTION PLAN

8. WORKING WITH CORDANT

2

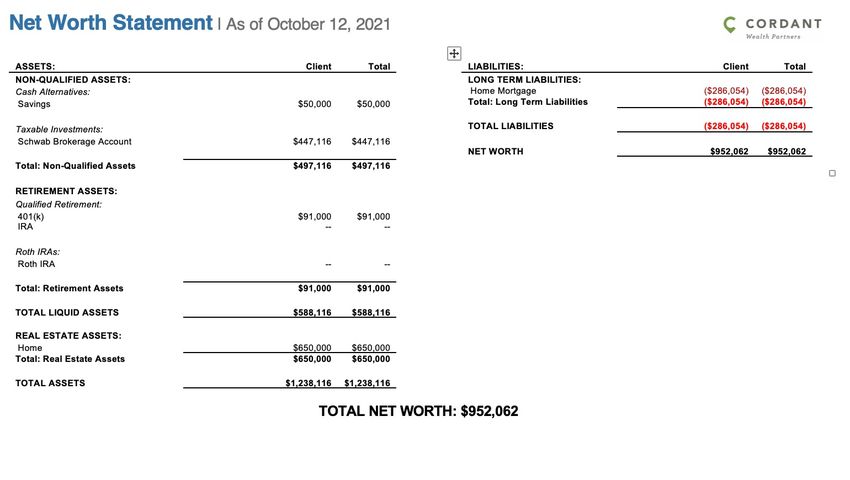

CURRENT WEALTH SNAPSHOT

3

COMPANY STOCK ANALYSIS

VESTED + UNVESTED RSUS

RSU VESTING BY MONTH

AT CURRENT INTC PRICE OF $49.10

$139,886

# SHARES $108,609

$90,540

$84,992 $81,801

$80,770

Vested

RSUs

2,581

$9,771 $9,771

$4,321 $4,321

Unvested

RSUs 2022/1 2022/4 2022/72022/102023/1 2023/4 2023/72023/102024/12024/10

12,521

INTC PRICE

UNVESTED RSU SENSITIVITY ASSESSMENT

$876,470

$813,865

$751,260

$688,655

$626,050

$563,445

$500,840

$438,235

$375,630

$30 $35 $40 $45 $50 $55 $60 $65 $70 4

COMPANY BENEFITS ANALYSIS

COMPANY: INTEL Eligibility & Limits Current Opportunity

$20,500 + $6,500 Catch up

Add Catch up

401(k) Contribution (those over $20,500

contribution

50)

Consider After-Tax 401k

Mega Back Door Roth Allowed $0

contributions

ESPP 15% Discount Maxing N/A

Increase and fund via

Deferred Compensation Eligible 10% of Salary

RSUs

Fund Deferred Comp to

RSU Income Quarterly $100k

reduce tax liability

5

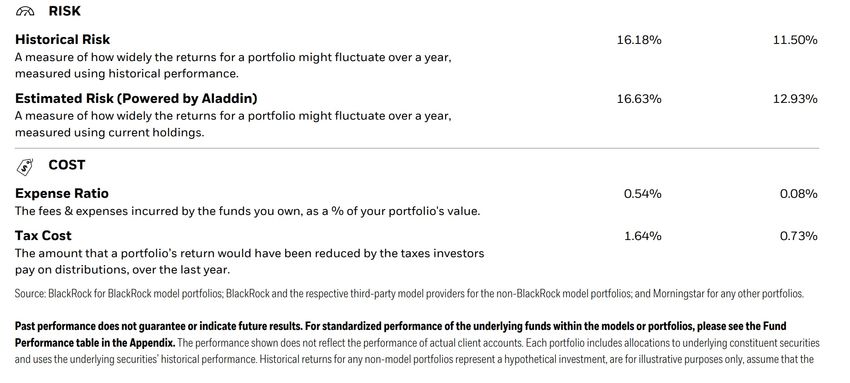

PORTFOLIO REVIEW RISK & COSTS Source: BlackRock for BlackRock model portfolios; BlackRock and the respective third-party model providers for the non-BlackRock model portfolios; and Morningstar for any other portfolios. Past performance does not guarantee or indicate future results. 6

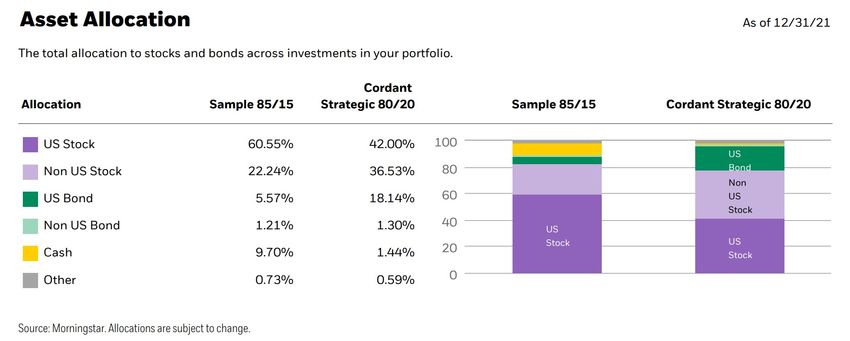

PORTFOLIO REVIEW

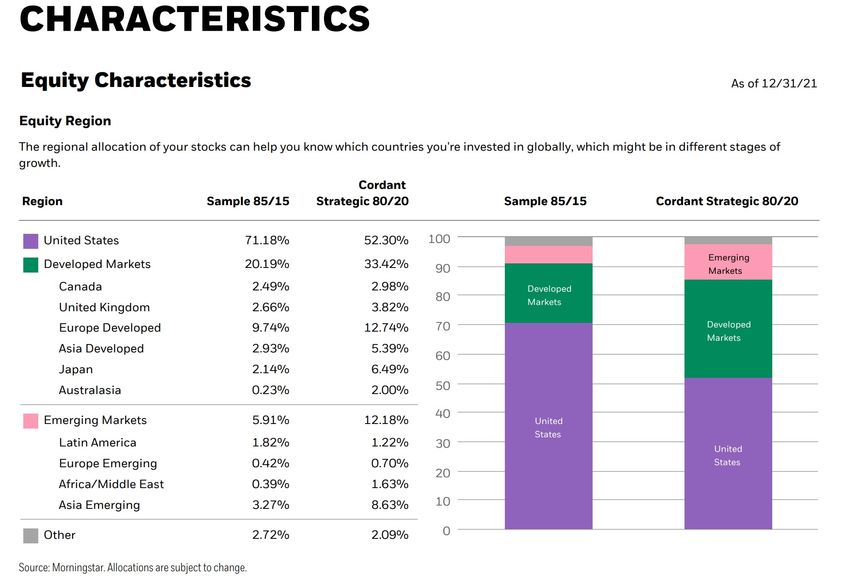

ALLOCATION REVIEW

7

PORTFOLIO REVIEW

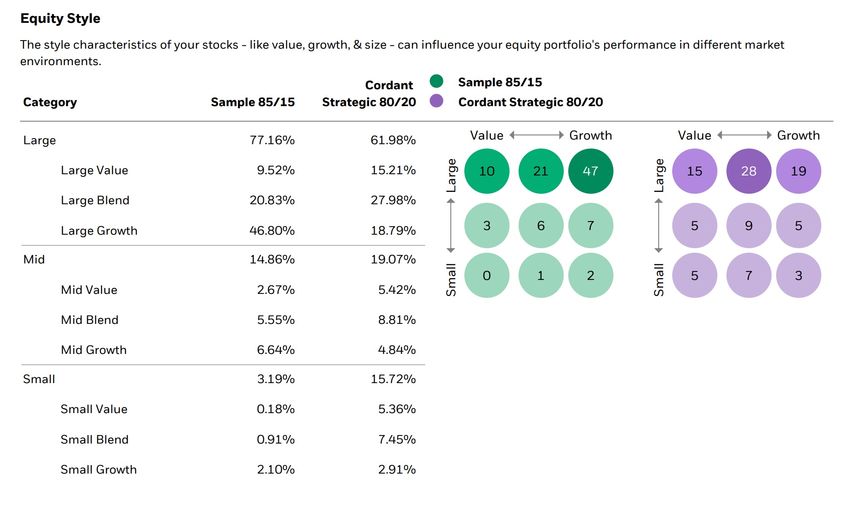

STYLE ANALYSIS

8SAMPLE TAX ASSESSMENT & OBSERVATIONS

OBSERVATIONS:

Total Income: $122,291 Filing Status: Married Filing Jointly Tax Exempt Interest: $0

• OBSERVATION #1

AGI: $117,791 Marginal Rate: 10.0% Qualified/Ordinary Dividends:

Deductions:

Taxable Income:

$45,043

$72,748

Average Rate:

2020 Safe Harbor:

0.0%

$0

$21,215 / $26,498

ST/LT Capital Gains: $3,945 / $72,458

• OBSERVATION #2

Total Tax: $0 Carryforward Loss: $0

• OBSERVATION #3

The marginal tax rate for your ordinary income is as follows: Planning Opportunity Limits Over/Under?

Net Investment Income Tax $250k Under

Marginal Rate Ordinary Income Threshold

Coverdell ESA $190k - $220k Under

10.0% $0 to $19,400 You: $0

Roth IRA Contribution $193k - $203k Under

12.0% $19,400 to $78,950

Lifetime Learning Credit $116k - $136k In Phaseout

22.0% $78,950 to $168,400

Student Loan Interest Deduction $140k - $170k Under

24.0% $168,400 to $321,450

American Opportunity Credit $160k - $180k Under

32.0% $321,450 to $408,200

Child Tax Credit $400k - $440k Under

35.0% $408,200 to $612,350

Qualified Adoption Expenses Credit $207k - $247k Under

37.0% $612,350 and above.

Saver's Credit $39k - $64k Over

The marginal tax rate for your capital gains and qualified dividends IRA Contribution Deductibility - Covered $103k - $123k In Phaseout

income is as follows: Spouse

IRA Contribution Deductibility - Non- $193k - $203k Under

Taxable

Covered Spouse

Income Qualified Income

Marginal Rate Threshold ($72,748 Total)

0.0% $0 You: $72,748 $72,748

15.0% $78,750 $0

20.0% $488,850 $0

Total Itemized Deductions: $45,043 vs. Standard Deduction of

$25,700

Deduction Amount Claimed

Health Care Expenses $28,762

Taxes Paid $10,000

Mortgage and Investment Interest Expense $4,984

Charity $1,297

TOTAL $45,043

All tax assumptions on based only on Federal marginal tax brackets and are included for illustration purposes only. The

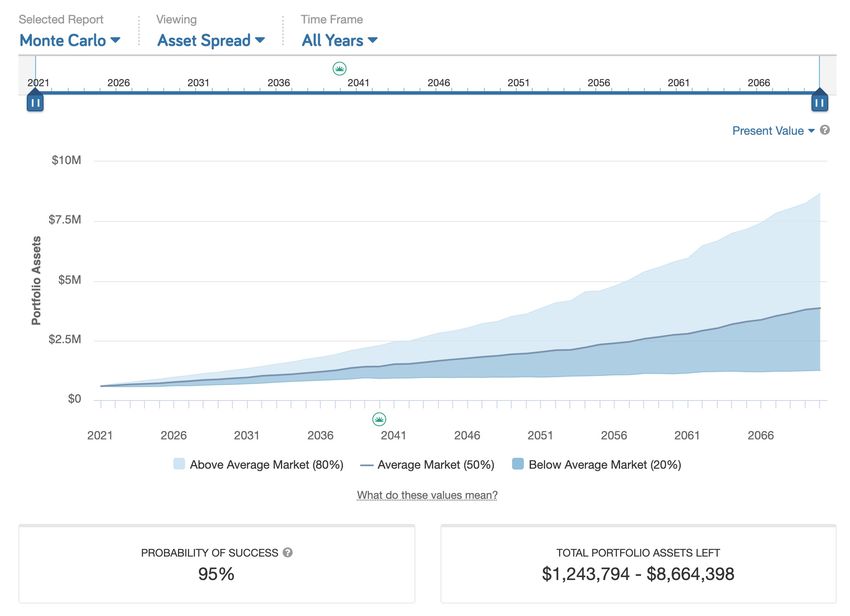

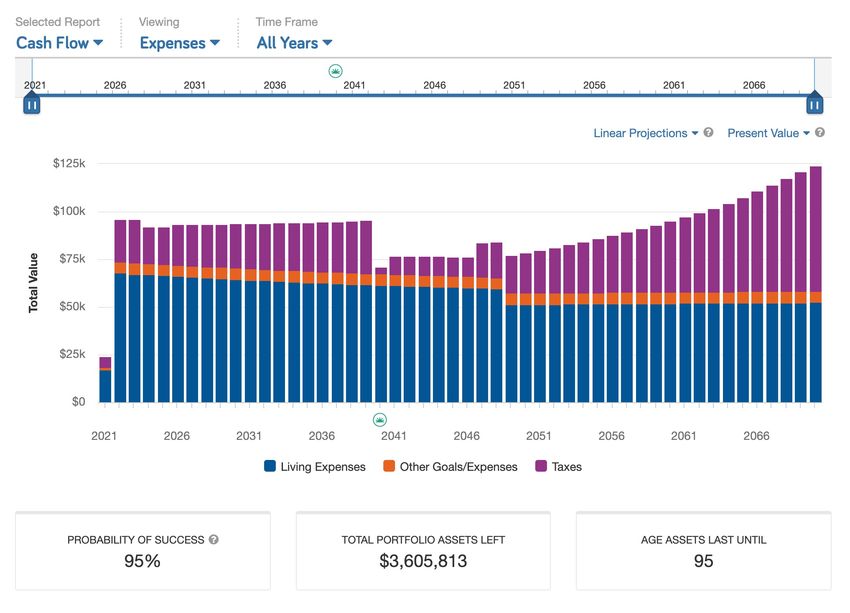

information provided in this analysis is not nor is it intended to be tax or legal advice. 9“ON-TRACK” ASSESSMENT

CASH FLOW AND PROBABILITY ANALYSIS

Projections are based on assumptions provided by you regarding your wealth snapshot and are not guaranteed. Actual results will vary, perhaps to a significant

degree. The projected reports are hypothetical in nature and for illustrative purposes only. Return assumptions do not reflect the deduction of any commissions.

They will reflect any fees or product charges when entered by the advisor/ representative. Deduction of such charges would result in a lower rate of return. Consult 10

your legal and/or tax advisor before implementing any tax or legal strategies.“ON-TRACK” ASSESSMENT PROBABILITY ANALYSIS Projections are based on assumptions provided by you regarding your wealth snapshot and are not guaranteed. Actual results will vary, perhaps to a significant degree. The projected reports are hypothetical in nature and for illustrative purposes only. Return assumptions do not reflect the deduction of any commissions. They will reflect any fees or product charges when entered by the advisor/ representative. Deduction of such charges would result in a lower rate of return. Consult your 11 legal and/or tax advisor before implementing any tax or legal strategies.

WEALTH ACTION PLAN

q Align investments and account beneficiaries with estate plan

q Maximize 401(k) contributions

HIGH PRIORITY

q Identify SERPLUS deferral amount

q Make after-tax contributions in 401(k) and convert to Roth (“Mega

Roth Contributions”)

q Invest and stop using HSA

MEDIUM PRIORITY

q Assess life insurance (likely over-insured)

q Identify plan to reduce individual stock concentrations

12CASH FLOW & FINANCIAL PLAN ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Consider Developing and • Income Modeling and Timing for:

• Salary & Bonus + Deferred Compensation

Income and Expense Plan

• Payout, timing and tax optimization of Salary, Bonus, and accelerated vesting of

RSUs and other equity compensation

• Social Security & Pension

• Portfolio Withdrawals

• Expenses Modeling

• Document objectives: (Lifestyle, Legacy, Growing Net Worth, Etc.)

• Where will I spend money and time? (Lifestyle, Travel, Charity, 2nd Home, Health

Care, Taxes, etc.)

• List and rank your spending priorities

• Cash Reserves: How much should I hold in cash?

q Answer the Question: What • Planning Considerations

• Planning through age ____. Based on Best Guess (Family history, etc.), Actuarial

level of lifestyle will my assets

Table, or Life Expectancy Calculator

safely support? • Portfolio Risk/Return Assumptions and Withdrawal Rate

• Align investment risk tolerance to planning inputs

• Consider Stress-Testing Your Financial Plan For Key Variables (Down Market, Inflation,

Spending, Age)

q Consider Putting a Reporting • System in place to track and monitor Balance Sheet and Investment Performance

System in Place

q Will I run out of money if I stop • System in place to track and monitor Balance Sheet and Investment Performance

working?

q Are you retiring before full • Social Security benefits may be reduced if you earn more than $18,960 and are collecting

retirement age? benefits prior to your full retirement age (FRA) or if you earn more than $50,520 in the year

you reach FRA.

• Social Security benefits will be reduced if you collect prior to your FRA.

• You can access your 401(k) penalty-free if you leave your employer in the year you turn 55

or later.

q Are you currently married? • Consider Social Security claiming strategies

• Consider optimal filing status for tax returns

13INTEL BENEFITS ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Intel Deferral Optimization& § 401(k) up to the match

§ ESPP & HSA

Prioritization Strategy

§ Traditional and ROTH 401(k) Deferral; FSA; SERPLUS

§ After-Tax 401k Contributions with subsequent conversion to Roth (“Mega Roth")

q Intel Departure Optimization for § Annual Performance Bonus – Carrot Date: December 31st or, if eligible for retirement, the

Key Dates 16th of your last month of work

§ Quarterly Performance Bonus – Carrot Date: Last date of the quarter – March 31st, June

30th, September 30th and December 31st

§ RSU and OSU Grant and Vesting Dates – Carrot Date: Depends on date of grant

§ SERPLUS – Carrot Date: January 15th

q SERPLUS Assessment Go/No Go SERPLUS DECISON

§ Current exposure to Intel (Stock and SERPLUS)

§ How much of Net Worth is in the plan?

§ How long until retirement/Departure?

Election Decisions

§ What to contribute? How much to defer? When to distribute? How to invest?

q SERPLUS Vs. “Mega Roth” § Current Tax Bracket

Decision § Expected Future Tax Bracket

§ Expected Time for Growth

§ Magnitude of SERPLUS Risk

q Intel Minimum Pension Plan § Do you take it upon leaving Intel or defer

(MPP) Decision (At Separation) § Do you take the Lump Sum or Monthly Income Payout option? (Coordinate between other

pension, Social Security, life insurance and other assets)

§ If taking the monthly income, select the appropriate payout option (single, joint, 10-yr.

certain, etc.)

q Health Care Replacement (At § COBRA and IRMP

Separation) § Private Insurance

§ Medicare

§ SERMA Account balance

14ASSET & INVESTMENT ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Strategy for Intel Stock § How much of my net worth does Intel stock represent? _____________

§ What is my tax liability this year if I sold my shares? _________Next year? ________

§ Stress Testing

§ How much is my intel stock worth now? _____________

§ If the price drops by: -10% ________ -20% ________ -30% ________

§ RSUs Vesting Strategy

§ ESPP Share Strategy

§ Coordination with tax strategy to minimize costs

q Portfolio Strategy – Avoid § Link investments to inputs in financial plan

Common Mistakes § Optimize Risk Level for Financial Goals

§ Minimize Frictions (Taxes, Trading Costs, Expense Ratios)

§ Maximize Returns (for given level of risk)

§ Overcome inertia – Make sure you’re diversified

q Intel Departure Optimization § Will your investment objectives or risk tolerance change?

§ Do you have a loan on any employer retirement plans?

§ If so, you may need to plan for how to pay it back and be mindful before rolling the

balance to another plan.

§ Do you have a deferred compensation plan?

§ If so, coordination strategies may exist between pension, Social Security, or life

insurance.

§ Consider consolidating have multiple accounts with similar tax treatment (multiple 401(k)s or

IRAs) to reduce complications.

§ Will you change your residence?

§ If so, this may impact tax liability, cash flow planning, and your Medicare Advantage

plan if you move out of the network.

q Consider rolling over accounts § If I want to move my accounts where do they go?

upon separation § Tax-Deferred Accounts into a Rollover IRA: 401(k), Retirement Contribution Plan,

Pension

§ Taxable Funds into a Taxable account: SERPLUS Distributions, Intel stock and

RSUs at eTrade

q How to get a paycheck in § How much do I need in my bank account? ________________________________

retirement? § When will I rebalance to generate a "paycheck?" __________________________

§ What order will I withdraw funds from my investment accounts? (Taxable, Tax-Deferred, Tax-

Free)

15TAX PLANNING ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Annual Withholding Strategy § HSA and FSA contributions

§ Withholding planning: Avoids unexpected $’s owned and help prevent penalties

q Annual Tax Planning Strategies § Review Joint vs. Separate Returns to optimize

Deduction Opportunities

§ Bunching Charitable contributions

§ Accelerating or prepaying medical expenses and (or) property taxes

Investment Income Considerations

§ Any Capital gains and loss carry forward?

§ Net income tax

§ Additional Medicare tax

q ROTH Conversion Strategy § Do you expect to have large Required Minimum Distributions?

§ If so, consider strategies to reduce the RMD such as Roth conversions.

§ Upon retirement, do you expect your income to be lower?

§ If so, consider deferring any Roth conversions until you are in a lower tax

bracket.

q Tax Optimization of § Tax-Loss Harvesting

Investments § Asset Location

§ Minimize Turnover in Taxable assets

16ESTATE PLANNING ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Does Your Estate Plan Match § Do you have an Estate Plan in place? If so:

§ Any Changes to Estate Objectives?

Your Current Objectives?

§ Any Changes to Beneficiaries and Fiduciaries?

§ Any Changes to Assets and Property?

§ Any Changes to Minors and Children Covered in Estate Plan?

§ E.g., Minors reaching the age of 18

§ Do the account beneficiaries on accounts need to be reviewed and possibly updated?

§ This includes retirement plans, life insurance, and TOD accounts

q Charitable Estate Strategy § If Charitably inclined, consider charitable giving strategies now to reduce your tax

burden. Examples:

§ Donor Advised Funds (DAF)

§ Charitable Remainer Trusts (CRTs)

*Pair with appreciated company stock for more savings

17INSURANCE & RISK MANAGEMENT ACTIONS

ACTION ITEM ISSUES TO CONSIDER OWNER DUE DATE

q Health Insurance Strategy at § COBRA and IRMP

§ Private Insurance

Separation From Intel

§ Medicare

§ SERMA Account balance

§ Will you need additional insurance such as vision or dental coverage?

§ Are you contributing to an HSA?

§ If so, consider HSA and Medicare coordination issues.

q Life Insurance Strategy § Have your needs for life insurance changed?

§ Are you over/under funded?

q Long-Term Care Insurance § Are you concerned about funding long-term care?

§ If so, consider LTC insurance, self-insurance strategies, and assisted living

communities.

§ If you have LTC insurance, does it need to be reviewed to ensure that it meets your

needs?

18NEED HELP EXECUTING THE PLAN?

WORKING TOGETHER

19ABOUT CORDANT

FIDUCIARY FEE ONLY INDEPENDENT

We’ve adopted the highest As a fee-only advisor with a We are free to structure our

legal standard of care, choosing transparent fee structure, we do business in the way that best

to act as an unwavering fiduciary not sell any products and are serves our clients, not

in the best and exclusive compensated solely for the constrained by the whims of a

interest of our clients. advice we provide. Wall Street bank.

$250 ~100

MILLION CLIENT HOUSEHOLDS

IN CLIENT ASSETS

CLIENTS:

BASED IN SERVING CLIENTS

ACROSS THE US

PORTLANDDISCLOSURES

The information contained in this assessment is for informational and discussion purposes

only. It is based on information and assumptions provided by you regarding your current

wealth snapshot. The calculations do not infer that Cordant assumes fiduciary duties nor

should the calculations provided be construed as financial, legal or tax advice. Please consult

with your tax, legal and financial advisors before engaging in any transactions.

This information is supplied from sources we believe to be reliable, but we cannot guarantee

its accuracy. Such information is subject to change, is not independently verified. Planning

and investment advice is provided by Cordant only after obtaining complete financial and

background information from each client. Even thought the majority of our clients are current

and former Intel employees, we are not suggesting that Cordant, Inc. is affiliated, associated

with, or endorsed by, Intel.

All investments have the potential for risk of loss and each investor should understand the

risks and discuss any questions with Cordant.

21THANK YOU CordantWealth.com

You can also read