Spectrum of Adviser Platforms and the Rise of White Labelling - May 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Spectrum of Adviser Platforms and the Rise of White Labelling May 2021

Contents

Introduction 3

Methodology 3

NextWealth View 6

Four key learnings from our research 7

Major players/ market overview 8

Drivers of adoption 12

Operational efficiency 12

Client experience 14

Margin 15

Price: from price taker to price maker 15

Considerations: Questions to ask platform providers when thinking about

launching a white-label platform 16

Compliance framework 16

Client money and CASS responsibilities: 18

Orphan clients 18

Investment in tech 19

Integrations 19

Financial stability and strength 21

Cultural alignment 23

Costs and charges 23

Functionality 25

Additional platform services 28

Brand and client interface 28

APIs, what are they and what do you need to ask providers about them. 30

Concluding thoughts 33

Platform Profiles 34

Advance by Embark 34

IFDL - Ascentric 35

FNZ 36

Fundment 37

Fusion Wealth 38

Hubwise 39

P1 Platform 40

Praemium 41

Seccl 42

SEI 43

2

Introduction

Like many things, it’s hard to define specifically what makes they offer custom integrations and data feeds. At the far

a platform a white-label or bespoke solution as there is no right of the spectrum, the financial advice firm will typically

clear distinction. In figure 1, we present the platforms on take on permissions for safeguarding and arranging of client

a spectrum based on the level of branding, customisation assets and will have CASS oversight responsibilities.

and the legal arrangement. We refer to these as white-

This report is part of NextWealth’s Adviser Tech Stack series.

label solutions in this report. Others use the terms platform

To support this free report, we also produce a paid-for

operator and platform service provider.

report and bespoke workshops for platforms to understand

The purpose of this report is to help executives at financial the options in more depth and provide additional analysis

advice businesses understand the options available, and competitive comparisons.

important things to consider and to take a broad view of

This report is organised into five sections:

the major players. Our research suggests there is a shift

happening with more advice firms launching white-label • NextWealth view

solutions. The decision to launch a platform should never

be taken lightly – despite some appealing aspects, it is a big • Market overview

undertaking and comes with a lot responsibility.

• Drivers of adoption

We categorise firms that offer branding and some

• Considerations

customisation of the platform as offering a white-label

solution. These firms, presented to the right of centre on • Profile of major players

our spectrum, offer more than just ‘spray on branding’ –

Methodology

Online survey of 218 advisers, conducted in February 2021.

Roundtable 10 CEO, CTO and COOs of large financial advice businesses and consolidators with a mix of those who have

launched a white-label platform, those planning to and those who have decided against it.

Interviews with representatives at platforms.

uestionnaire sent to 28 platforms. Responses were received from the 24 firms listed below. For those that didn’t reply,

Q

estimates are provided.

• 7IM • Fidelity FundsNetwork • Parmenion

• Advance by Embark • Fusion Wealth • Praemium

• Aegon Platform • Hubwise • Raymond James

• AJ Bell Investcentre • James Hay • Seccl

• Aegon Retirement Choices • Multrees • SEI

• IFDL - Ascentric • Nucleus • Standard Life Wrap

• Aviva • Old Mutual Wealth • Transact

• BNY Mellon Pershing • P1 • True Potential

3

Executive Summary

Market overview and adoption

• N

early half (47%) of financial advisers in businesses with £250m or more in assets under advice say they plan

to launch a platform in the next three years. 8% are already underway on the process.

•

On average, financial advisers put 55% of new client money on their preferred platform. This rises to 77%

among financial advisers working in firms with a white-label platform.

• 6

2% of financial advisers use a third-party platform with no branding. Take-up of branding options is higher

among advisers in larger firms.

Main drivers Argument for white-labelling Argument against white-labelling

Operational Large firms can have more control of Benefits can mostly be gained with a single

efficiency implementing CIP. Reduces risk, costs and platform provider, without incurring the

offers simplicity. Ability to control costs helps expense and significant responsibility,

to build case to transfer assets reducing the in particular client money and CASS

number of legacy systems that must be used. responsibility.

Client Offers firm more control over client As above, mostly can be gained with a single

experience experience and to develop the firm’s own platform. Also, cost of middle office (data and

brand. tech) can be high.

Ability to Firm earns revenue from platform fee and Creates potential conflicts of interest.

capture margin diversifies revenue streams.

Comes at a cost – advice firm takes

responsibility for oversight, governance and

service.

Control White-labelling allows firms to become Financial advisers have in the past negotiated

over price a price-maker rather than a price-taker. hard on third-party platform fees and those

Financial advisers are facing increasing savings are passed to customers. By moving to

competition from lower cost options, notably a single platform for most business, financial

Vanguard. Having more control over the value advice firms could command more clout when

chain means greater control of pricing. negotiating the price.

4

7 key considerations for advice firms contemplating the white-labelled

platform route

1. Compliance framework: running a platform comes firm and its white-label partner are compatible in how

with responsibilities. With a third-party platform, the they operate and make decisions. This is hard to assess

contractual arrangement for custody is typically between objectively, but insight can be gleaned by asking for

the client and platform. With a white-label platform, references.

the agreement is usually between the advice firm and

5. Additional services provided by platforms: third-party

the client and fees are paid to the adviser. The financial

platforms provide more than just custody. Careful

advice firm may take responsibility for arranging and

consideration must be given to assessing the importance

safeguarding of assets and will have responsibility for

of service, technical expertise and the other support

CASS oversight.

provided.

2. Tech upgrades: whilst any changes necessary to comply

6.

Functionality, in particular the tax wrappers and the

with new rules and regulation would typically be paid for

degree to which the SIPP is integrated into the platform

by the underlying tech provider, any bespoke upgrades

is an important consideration that must be probed.

of a white-label platform are usually paid for by the

advice firm. 7. Integration with other tech: our research repeatedly

shows this is a priority and frustration for advice firms.

3. Financial strength and stability: advice firms must

Integrations can be custom built, delivered via API or

carefully assess financial strength and stability of any

managed via the Origo Integration Hub. Many platform

tech partners. It is also important to get a sense for the

providers – third-party and white-label – claim high

commitment to the market and the ability to weather

levels of integration but financial advice businesses tell

various market cycles.

us these can deliver poor outcomes.

4. Cultural alignment: it can be important that the advice

5NextWealth View

This report reveals a subtle but substantial shift among large The third, but no less important, driver is about the client

financial advice businesses toward launching a bespoke or experience. Firms want to build their brand, develop their

white-label platform. The shift is being driven by a desire client proposition and offer a slick tech experience for

to capture margin, improve operational efficiencies and clients. This is critical for those looking to build and scale –

improve the client experience. they need to attract next-gen clients and deliver a next-gen

proposition. Many believe a bespoke platform will help by

It’s a hard to argue against a proposition that will cost giving the firm more control over data in particular, allowing

clients the same or less while allowing firms to clip the the firm to build better tools for serving clients.

ticket. The decision to launch a platform comes with

huge responsibilities but the basic economic argument is White-labelling makes sense for firms that are trying to

appealing. grow and scale and possibly list a financial advice business.

These firms will typically have an in-house DFM and will be

Operational efficiency is a more powerful force than many actively looking to acquire financial advice practices. They

realise. Let’s take a step back to understand the context. Our will be driven by a desire to diversify and grow revenue and

survey for this report found that half of financial advisers deliver significant operational efficiencies.

are not satisfied with their tech stack. Platforms tend to

get high scores. But financial advisers want to have more The path to launch a white-label platform can also make

control over their tech stack – and many believe a white- sense for DFMs who want to have their own custody to

label platform will give them that control. make managing models more efficient. Model portfolios

on platform operate under pretty serious constraints. They

In large financial advice businesses that have discretionary can’t practically hold investment trusts or listed securities

permissions or that manage their own models, the and they are optimised for clients accumulating wealth. In

operational headache of managing those across multiple order to unlock further growth, a platform can be a good

platforms is not to be underestimated. It also introduces option.

risk and cost.

But in our view, with the exception of capturing margin, the

Another issue is the multitude of systems advisers need to drivers can be addressed through a strategic partnership

deal with from product providers, in particular for legacy with one third-party platform. And working with a third-

products. The decision to move a client from a legacy party platform can significantly reduce risk. The governance

product usually comes down to cost. If an adviser can reduce and oversight responsibilities of platform operators are,

the cost of the alternative product, it’s easier to justify. quite frankly, a bit scary, and they can’t be abdicated or

Modern product, similar cost – who would argue with that? outsourced.

Having control of more of the value chain allows the adviser

to control the cost, thereby helping to justify the move.

6NextWealth View - continued

Four key learnings from our research

Sharing the spoils with clients – a case of triumph over hope?

We would be remiss not to mention cost and the client. There is certainly an opportunity to pass cost savings to clients in a

white-labelled model. In the agent as client model, the degree to which the agent passes on the benefits of the cost savings

to the client is largely the gift of the agent.

One would hope to see a good proportion of any cost savings shared with clients, whether that becomes a triumph of hope

over experience or not, time will tell. We think the regulator will have some comment to make about the various functions

fulfilled by the agents and the provider and the relative splits and whether or not that is appropriate.

It can end in tears

Several of our interviewees reminded us that many firms have tried to launch platforms. Some have succeeded, others

haven’t.

We will continue to see large financial advice businesses, particularly PE-backed consolidators pursue a white-label platform

strategy. We will also see more mid- to large-size firms go this path. But there will be others who decide that simplifying

choice to a limited number of platforms achieves the firm’s aims while avoiding the governance responsibilities that come

with being a platform operator.

Clarification of the rules

White-labelling makes sense for some firms – there’s no doubt. But we think many of the issues that firms face can be

achieved by mostly working with a single platform. We think this makes business sense and is good for the customer.

There is a lingering perception that the regulator frowns on use of a single platform. Certainly, shoehorning has no place

in a quality business. But, wrappers and product availability are broadly comparable across platforms and by putting most

business with a single platform, firms can negotiate better fee deals for clients.

Platforms – pull up your socks

On the issue of operational efficiency, we think third-party platforms need to pull up their socks. Platforms were set up

to manage money at an account level. More needs to be done to support firms to extract MI and to manage portfolios

efficiently. They ignore these demands from advice firm head offices at their peril.

7Major players/ market overview

We place platforms on a spectrum. There is no clear line distinguishing platforms offering a branded client portal

and those offering a more tailored offering. Figure 1 shows our platform spectrum of choice available to financial

advice businesses, based on responsibilities, branding and customisation.

Firms at the left end of the spectrum offer no branding options to advisers and those at the right of the spectrum

offer full branding capabilities, customised data feeds and integrations and require the financial adviser firm to

take on regulatory responsibilities such as safeguarding and arranging of client assets.

Figure 1: Spectrum of platform choice

8Use (current and anticipated) of white-label platforms

Nearly 1 in 10 financial advisers say they use a bespoke platform, rising to 25% of advisers at firms with £250m

or more assets under advice.

Financial advisers who work in firms with a white-label platform tend to place more assets on that platform than

average. This is important – one of the considerations for firms in launching a platform is the buy-in they will get

from financial advisers, particularly independent financial advisers.

•

On average, financial advisers place 55% of new client business on the preferred platform. This compares to

an average of 77% among those with a white-label platform.

Figure 2: Share of new business on the primary platform

9Adoption of branding features on platforms

On our platform spectrum, the basic level of customisation • O

ur analysis also suggests that financial advisers who

is branding, sometimes referred to as ‘spray-on branding’ of use branding features offered by a platform place a larger

the client portal. Figure 3 shows low take-up by advisers of proportion of client assets with that platform: those that

branding features, but take-up is higher at larger firms. use a platform with no branding place an average of 54%

of new business on their preferred platform, compared

• 6

2% of advisers are using a third-party platform with no to 63% with a branded client portal and 77% for those

branding. 20% are using a branded portal which sits on with a fully customised platform.

top of a third-party platform.

•

Table 8 shows the branding options offered by platforms.

• F

inancial advisers at larger firms are more likely to

use branding options. Larger firms tend to place more

importance on developing their brand than smaller

practices.

Figure 3: Adoption of branding and bespoke features on platforms

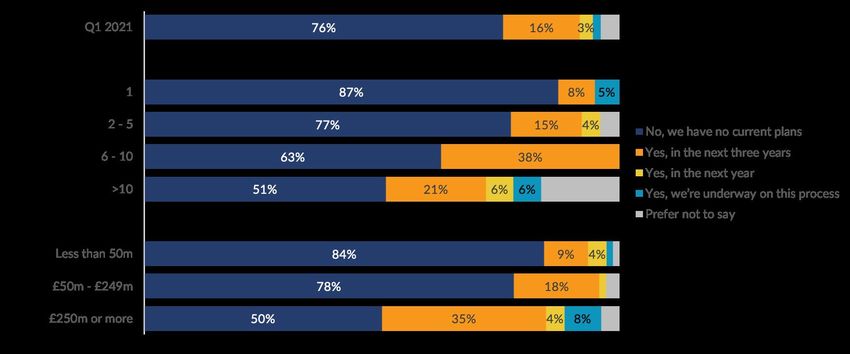

10Future demand for white-labelling

To help understand future demand for white-label platforms, we asked financial advisers about future intent. Three quarters

have no plans to launch a fully customised platform (Figure 4). However, the results vary significantly by size of firm.

• A

mong those in firms with over £250m in assets under advice, 47% plan to introduce such a platform in the next 3 years,

8% are already underway in the process.

Figure 4: Intention to launch a fully customised platform in future (those without one)

11Drivers of adoption

The main drivers of launching a white-label platform are operational efficiency, customer experience, margin and price.

Most firms will have multiple drivers that overlap.

Operational efficiency

The driver we heard most about from financial advice businesses was operational efficiency.

“Businesses usually started in terms of focusing on funds and fund selection. And as we've gone on,

operational efficiency and technology is probably now more important than how I put your investment

proposition together, it's secondary to driving efficiencies in the business.”

The operational efficiencies advisers hope to gain can be grouped into those to support running the investment proposition

and those impacting systems and technology.

Operational efficiency in running the investment proposition

Financial advice businesses running MPS across multiple platforms argue that having one platform from which to run the

investment proposition would deliver huge savings, removing inefficiencies and risk introduced by using so many different

systems to rebalance and manage portfolios. A white-label platform can often be seen as a solution.

“We run across 13 execution venues at the moment and most of those are at scale. But it’s a pain

because they’re all absolutely different. Even the FNZ-based platforms that all use X-Hub.”

“The more complexity you have, the bigger the risk of trading errors and things going wrong.”

“I think the key driver for us is operational efficiency, particularly having our asset management team,

somewhat separate to our financial planning team, and yet effectively running most of the money that

the financial planning team manage. The operational inefficiency there is can be huge in some cases. So,

we feel that we need a tech lead solution that will help us to eliminate all of that.”

Challenges with managing the investment proposition are not just the domain of large consolidators working across multiple

platforms. A mid-size firm with ten financial advisers managing models on an advisory basis told us that launching a platform

was mainly down to efficiency of the investment proposition – from getting sign-off for rebalancing to eliminating paper.

Third-party platforms challenge whether a white-label solution is really necessary. Many of the operational benefits can be

achieved by limiting the number of platforms – preferably to one.

12Operational efficiency: systems

Financial advisers often lament the lack of control they have over the client proposition. Jennifer Ellis from Wellington

Wealth said at NextWealth’s Advice Tech Live event in January that her firm deals with a total of 42 provider systems. This

isn’t by choice: clients arrive with assets in various places and a decision must be made in the client’s interest as to whether

to move those assets – operational efficiency of the firm is not a justification to transfer.

This theme of control over systems was echoed at our roundtable:

“Whenever you're plugging into something that hasn't been designed for you, your business, your

processes, there's only so much efficiency that you can get. And also, with every single platform, you end

up having to have work arounds, which brings business risk to the table.”

“A problem everyone suffers from has to do with legacy issues. There's no escaping, that we're all

carrying a huge amount of legacy baggage. And it's probably even worse when you're actively recruiting

advisers… all those advisers come with their own preferred solutions. And the biggest problem that

we have is getting the data that we need from a huge range of providers, to be able to produce a lot of

documentation, we need the standard MiFID II costs and charges stuff... It's not practical when you're

trying to build a business at scale.”

Some financial advice businesses that have launched a white-labelled platform say it is part of an effort to control the

value chain to be able to more easily justify asset transfers. Controlling the platform cost along with other aspects of the

value chain, allows advisers to control and potentially reduce the cost to help support a decision to move away from legacy

products.

“Provided there is no client detriment in terms of cost or tax or risk profile, then we're going

to do our damnedest to move the assets as quickly as possible to get them over into our

environment, which for the most part is lower cost. That's not the case if we were using a third-

party platform – in order to move the assets, we need to bring the platform charge down so the

overall cost is lower. If you've got legacy stuff elsewhere, it's just a rubbish experience for the

client and more often than not it's a pretty poor experience for the adviser. And, so we throw

the kitchen sink at the migration.”

Third-party platforms balk at the suggestion that an adviser firm can offer a lower cost platform than a negotiated deal.

13Client experience

Closely linked with the previous section on efficiency of systems is the client experience. Financial advice firms want to

build a better experience for clients and a digital proposition to attract the next generation of investor.

Earlier in this report we discussed the operational inefficiencies of managing models on multiple platforms. This can also

impact on the client experience. A CEO of a mid-size financial advice firm said the decision to launch a platform was

connected to a desire to deliver a slicker client proposition, based on client feedback.

“In response to a client survey that we did last year, one of the things that came back very strongly was

that they wanted less hassle, less paperwork, they wanted things to be much more streamlined. And so,

having discretionary powers within our own white-label platform, was a way to deliver that.”

There is a desire among financial advisers to run a business supported by modern technology. Many express frustration at

having to apologise for their industry to clients. This is particularly acute for those looking to recruit younger clients.

“We try to be quite forward thinking, we want to be thinking, what do the next generation of clients

want, so that we're succession planning the business for the future. And clearly, next gen kind of clients

want a tech-led solution. So, we need to be able to deliver that very efficiently at the right cost, with the

right experience for the client. And I'm not sure we're going to get there by using the traditional retail

platforms.”

Several described platforms as “quite old fashioned” when it comes to data ownership and extracting client data. One

attendee at our roundtable noted that his firm’s preferred platform won’t provide transaction level data for clients.

“They feel like the transactional data for clients is theirs. They won’t distribute it to back office systems,

for example. And that means bringing in even more providers, such as Sprint Technology and Fastrak,

to get the data out that we need and to regurgitate it into a performance manner, because the standard

reports we get from [PLATFORM] just aren’t fit for purpose.”

The CEO of a consolidator told us that data was key to the decision to launch a platform.

“We saw data as the key differentiator, allowing us to provide a better client experience through

personalisation and depth of data.”

Firms believe that white-label platforms will allow them to take more control over data allowing them to deliver a slicker

client proposition. Where there is a strategic drive in a firm to gain control, a white-label platform can make sense.

14Margin

Most believe, despite what financial advisers might say about operational efficiency, that the main reason for launching

a white-label platform is margin. The economics are hard to argue with – the financial advice firm will pay the underlying

tech provider, add a fee for their own services on top and the client will typically pay the same or less than they would with

a third-party platform. The financial advice firm will need to do quite a bit of work for the margin. That additional work is

outlined in the next section, Considerations.

Diversification of revenue streams is also a factor. Responsible businesses want to earn revenue from a diverse set of

sources – in this case, not just financial planning.

We understand that depending on the size of the deal, degree of personalisation and the legal framework, the adviser firm

will pay the underlying platform provider, tech provider or custodian between 4 bps to 20bps. The financial advice firm will

then add on to that to bring the total charges to between 15 bps and 35 bps.

Price: from price taker to price maker.

White-labelling gives firms more control over the value chain which gives them control over pricing. With increased

competition from low cost entrants such as Vanguard, control over the price could be critical in future.

Financial advisers have in the past negotiated third-party platform fees paid by their clients. These savings are passed

directly to customers. By moving to a single platform for most business, financial advice firms could command more clout

when negotiating prices. Some third-party platform providers argue that reducing the cost is a function of scale, something

individual financial advice businesses might struggle to achieve.

15Considerations

Questions to ask platform providers when thinking about launching

a white-label platform

Compliance framework

One of the key differences between third-party platforms who has safeguarding and arranging permissions and who

and white-label platforms is who has the contractual has the CASS client money responsibilities.

arrangement with the client. Typically, with third-party

We recommend reading the ThreeSixty Services paper

platforms, the contractual arrangement exists between the

Operating Your Own Platform, for an expert view on the

client and the platform. A separate agreement is drawn up

compliance considerations and how they will apply to your

with the financial advice business.

firm’s decisions.

Table 1 illustrates that at the far end of the spectrum,

The financial advisers at our roundtable who have launched

BNY Mellon Pershing, FNZ, SS&C, Seccl and SEI will have

white-label platforms emphasised that the responsibilities,

an agreement with the financial advice firm underpinned

no matter what compliance framework is used, are

by SLASTO support oversight. Most other white-label

significant. One said that he “gets shivers” when he thinks

platforms will have a contract with the client and financial

about taking on the CASS responsibility.

advice firm. This is the most important distinction between

white-labelled and third-party platforms determining who is

responsible to the client.

Table 2 summarises the compliance framework options,

Table 1: Parties for contractual agreement

Contractual agreement with Platform and…

Provider Client Firm

Advance by Embark X X

IFDL - Ascentric X X

BNY Mellon Pershing X

Fusion Wealth X X

Hubwise X X

P1 X X

Praemium X X

Seccl X

SEI X

SS&C X

16Table 2: Compliance framework options for white label

platform solution providers

Compliance Safeguarding Client money Regulatory

framework and arranging and CASS reporting

options permission responsibilities responsibility

Appointed representative

Underlying tech provider

Underlying tech provider

Agent of the client

Custody provider

Custody provider

Custody provider

Agent as client

Adviser firm

Adviser firm

Adviser firm

Provider

Provider

Provider

Provider

Advance by Embark X X X X X

IFDL - Ascentric X X X X X X X

BNY Mellon

Not disclosed X X X X X

Pershing

Fundment Not disclosed X X X X

Fusion Wealth X X X X X X

Hubwise Not disclosed X X X

Multrees Not disclosed Not disclosed X X X

P1 Not disclosed X X X X

Praemium X X X X X X X

Seccl X X X X X X

SEI X X X X

SS&C X X X X

17Client money and CASS responsibilities:

A CEO of a platform told us: “client money is what makes me lose sleep - it’s not easy and it brings a huge amount of risk.”

It is among the biggest areas of focus and responsibility of a platform operator and third-party platforms say it is one of the

most compelling arguments for advice firms not to launch a platform.

Most white-label platform providers say they retain the client money responsibilities. But financial advice firms who have

their own platform will need to ensure they have appropriate oversight of the CASS provider. This does not mean obtaining

regulatory responsibility for client money but ensuring adequate oversight. The £8.2m FCA fine against Aviva in 2016 for

Client Money and Assets failings serves as a stark reminder of this. In the press statement at the time, the FCA spokesperson

was quoted as follows:

"Aviva outsourced the administration of client money and external reconciliations in relation to custody

assets, but failed to ensure that it had adequate controls and oversight arrangements to effectively

control these outsourced activities. With outsourced arrangements firms remain fully responsible for

compliance with our CASS rules. Firms are reminded that regulated activities can be delegated but not

abdicated.” https://www.fca.org.uk/news/press-releases/fca-fines-aviva-pension-trustees-uk-limited-

and-aviva-wrap-uk-limited-8-2m

The spokesperson went on to warn others with similar

outsourcing arrangements that there is “no excuse for not

"Regulated activities can be delegated

having robust controls and oversight systems in place.” Financial

but not abdicated” – Spokesperson, The

advice firms launching their own platforms will need to heed

FCA

this advice.

Orphan clients

A potentially thorny issue for financial advice firms launching a platform is orphan clients, or clients that choose to detach

themselves from their financial adviser. Many platforms increase the fee charged for clients who become orphaned. We

understand the regulator requires evidence the relative increase is fair based on the service offered. For firms that have

their own platform permissions, the platform will retain the relationship with the client who has become an orphan. Under

an appointed rep model, the platform provider would take control of that client relationship.

One of our roundtable attendees confirmed that his firm’s aim is to encourage orphan clients to leave the firm rather than

remain on platform. The firm runs an adviser platform and is not geared up for direct access. The other issue is that if the

client is in a DFM portfolio, the account will need to be unlinked from the portfolio. He added:

“There are more downsides than upsides and we really don’t make any money out of it. We’d rather

they clear off and go somewhere that is a better fit from a cost point of view.”

For advisers that are launching their own platform, the requirements will vary depending on who has the contractual

relationship with the client. Firms should be aware of their responsibilities and lay out a policy in advance.

18Investment in tech

Another key consideration is the investment in technology from the chosen provider. This is partly a question of scale,

having the resource to invest, but also a question of culture. Platforms have had to make huge investments in recent years

in tech just to comply with new rules and regulations. From the RDR to pension freedoms to MiFID II, the biggest disruptor

for platforms in the past few years has been regulatory and legislative change. Financial advice businesses need to ensure

their partners have the scale and expertise to adapt and change when needed.

When working with third-party platforms, the provider pays for any required enhancements to the technology.

One provider of bespoke platforms questioned “whether some of the smaller white-label platforms are going to be able to invest

sufficiently to keep up in the next few years.” Day to day fixes are relatively easy but wholesale changes can be costly. One

platform boss gave the example of the 10% drop rule introduced under MiFID II. “If the FCA decides to scrap the 10% drop,

switching that off might be a challenge. It is so integrated into the process. Who pays for that?”

We asked platform providers – both white-label providers and third-party - who pays for bespoke upgrades requested by

financial advisers and upgrades required by regulatory or legislative change.

In most cases, bespoke upgrades, requested by a financial advice firm, are paid for by the requesting firm. Some third-party

platforms won’t build bespoke features for individual firms. The cost of upgrades to comply with new rules and regulations

are paid for by the platform provider or the underlying tech provider. No respondent said this would be paid for by the

financial advice firm.

Integrations

Integrations with other tech are a priority for all firms. Integrations can be custom built, delivered via API or managed via the

Origo Integration Hub. Many platform providers – third-party and white-label – claim high levels of integration but financial

advice businesses tell us these can deliver poor outcomes.

We interviewed technologists David Tonge, Co-Founder and CTO of Moneyhub and Simon Clare, CTO of Bravura Solutions

to get a better understanding of APIs and what questions financial advisers should ask about the APIs offered by advice tech

providers. The Q&A appears in the next section, APIs – what are they and what do you need to ask providers about them.

Membership of the Origo Integration Hub can simplify integrations when a financial advice firm’s other software providers

have signed up. Firms that have signed up to the Integration Hub need to build one connection to access multiple

integrations with platforms and adviser systems. The system makes setting up straight through processing for account

opening, remuneration and valuations between trading partners low-cost, quick and simple.

19Table 3 below lists platforms that are members of the Origo Integration Hub. Readers can view the Origo Integration

Hub Matrix for a list of integrations by firm (https://www.origo.com/services/IntegrationHub/Origo-Integration-Hub-Customer-

Matrix.aspx).

Table 3: Origo Integration Hub

Origo Integration Hub

Provider

Membership

7IM Coming soon

Advance by Embark Yes

Aegon Platform Yes

Aegon Retirement Choices Yes

AJ Bell Investcentre No

IFDL - Ascentric Coming soon

Aviva Yes

Fidelity FundsNetwork Coming soon

Fundment No

Fusion Wealth Coming soon

Hubwise No

James Hay No

Nucleus No

Old Mutual Wealth Yes

P1 No

Parmenion No

Praemium No

Raymond James No

Seccl No

SEI No

Standard Life Wrap Yes

Transact No

True Potential No

20Financial stability and strength

A key consideration when choosing any platform or

technology partner is financial strength and stability. As

readers of this report well know, financial strength alone is

not enough. It is important to get a sense of the commitment

to the market and stability of the business.

Financial advice business bosses at our roundtable

“None of us can confidently say

acknowledged the importance of financial stability in

that Hubwise or probably less

choosing a partner. They pointed out that uncertainty about

likely Seccl might not end up being

future ownership and market commitment exists with all

owned by a private equity investor

firms. They also acknowledged that some of the established

going forward.”

platforms were until quite recently questioned over their

financial strength.

“If we cast our minds back five years or maybe longer, we had the same embryonic concerns about

businesses like Nucleus and Novia, who now have become prey to various private equity groups,

demonstrating that they could weather the initial storm of becoming a platform service operator…

Clearly as part of the evaluation process, the new businesses deserve a greater degree of introspection

than established businesses.”

Advice firms can look at assets and number of clients, as listed in Table 4. A key question to reflect on is whether the firm

will be able to keep up with the continued investment in tech through various market cycles.

One of our roundtable attendees acknowledged that financial strength is important but emphasised the tech first culture in

the firm as even more important: “a greater consideration actually has to do with the fact that they had good tech capability, API

connectivity that we could use – they were talking a language that we understood.”

This point acknowledges that while financial strength is important it must be considered alongside other criteria.

21Table 4: Market presence

Provider Assets under Number of adviser Number of linked

influence (£) firm users clients

7IM 16.8 bn 629 31,631

Advance by Embark 26.8 bn 500 110,000

Aegon Platform 92.6 bn 16,567 651,070

AJ Bell 62.5 bn 11,000 346,797

Aegon Retirement Choices 63.0 bn 19,920 1,676,431

IFDL - Ascentric 16.9 bn 3,626 95,302

Aviva 34.4 bn 13,346 292,678

Fidelity FundsNetwork 43.1bn 5,487 354,700

Fusion Wealth 17.5 bn 230 79,203

Hubwise 3.0 bn 340 16,785

James Hay 27.2 bn c.4,500 57,944

Nucleus 18 bn 855 101,704

Old Mutual Wealth 62.5 bn c.7,500 467,822

P1 0.65 bn 17 764

Parmenion 8.2 bn 1,600 80,000

Praemium 2.4 bn 1,787 -

Raymond James 13.6 bn 300 40,000

Seccl 0.28 bn 31 22,000

SEI1 727.0 bn - -

Standard Life 67.0 bn 2,700 419,500

Transact 46.9 bn 3,500 117,200

True Potential 16.2bn 3,010 348,226

Assets represent global holdings

1

22Cultural alignment

Cultural alignment is more difficult to assess objectively. The financial advice firms we interviewed who have launched a

white-label platform recommend obtaining references and speaking to other like-minded firms to find out what it feels like

to be a client of the provider. Other topics to ask about include experience with asset migrations and integrations.

Costs and charges

We are very familiar with standard charging models for third-party platforms – they charge clients a basis point fee and

there are sometimes additional ad hoc charges, again paid for by the client.

The arrangement is different when a firm establishes a white-label platform. The financial advice firm will typically have

a contract with the client who will pay the platform fee to the advice firm. The advice firm will then pay the underlying

platform or tech partner either as a percentage of assets or a fixed fee.

Financial advisers should ask white-label providers about additional charges, such as minimums, dealing charges, etc. Table

5 details the charging structure for the platforms and white-label providers.

23Table 5: Charging structure

ETF/ Investment trusts/

Platform charging structure Fund dealing charges

Securities charges

Additional Customised Provider

Minimum Per client Adviser Required Required

Provider ad hoc by the advice Customised by

fee BPs firm BPs charge charge

charges firm the advice firm

7IM X X X

Advance by Embark X X X

Aegon Platform X

AJ Bell X X X X

Aegon Retirement

X X

Choices

IFDL - Ascentric X X X X

Aviva X X

BNY Mellon Pershing X X X X X

Fidelity

X X

FundsNetwork

Fusion Wealth X X

Hubwise X X X X

James Hay X X X*

Nucleus X X

Old Mutual Wealth X X

P1 X X X X

Parmenion X X X

Praemium X X X X X

Raymond James

Seccl X X X X X

SEI X X X X X

Standard Life X X X X

Transact X X

True Potential X X X

*No specific charge associated with the ETF/Investment Trusts or Securities. However, James Hay require these investment types to be held by

either a Stockbroker or a DFM in which charges are applied.

24Functionality

The functionality provided is a key consideration when looking at white-label platform partners. Many financial advisers say

white-label solutions work well until they don’t. They may work at first with client with relatively simple requirements but as

the complexity increases problems may arise. This can be particularly true when considering how well the SIPP is integrated

is into the platform. Table 6 shows the tax wrappers supported by the platforms. All are widely available except offshore

bonds and LISAs. However, the level of integration with the SIPP wrapper in particular is critical.

Table 6: Tax wrappers and SIPP providers

Tax wrappers support SIPP Provider

Offshore

Onshore

Lifetime

3rd party

Bond

bond

JISA

SIPP

SIPP

SIPP

Own

GIA

ISA

ISA

Provider

7IM X X X X X X X X X

Advance by Embark X X X X X X

Aegon Platform X X X X X X X

AJ Bell X X X X X X X

Aegon Retirement Choices X X X X X

IFDL - Ascentric X X X X X X X X

Aviva X X X X X

BNY Mellon Pershing X X X X X X X X

Fidelity FundsNetwork X X X X X X X

Fundment X X X X X X

Fusion Wealth X X X X X X X

Hubwise X X X X X X

James Hay X X X X

Nucleus X X X X X X X X

Old Mutual Wealth X X X X X X X

P1 X X X X X

Parmenion X X X X X X X

Praemium X X X X X X X

Raymond James X X X X X X

Seccl X X X X X

SEI X X X X X X

Standard Life X X X X X

Transact X X X X X X X X

True Potential X X X X X X X X

* Referred to as a Personal Pension not a SIPP.

25A few attendees at our roundtable encouraged any firm considering launching a platform to look carefully at the SIPP

provider and functionality.

“Whoever it is you're looking at you do need to ask some questions around the SIPP because it's not just

a platform tech. Actually, have a look at who the SIPP provider is and how they deal with things like

drawdown and application processes and basically running a pension scheme. I do know that there are

some issues out there.”

“We have been speaking to the larger providers and the conclusion that we had was that any platform

we go to, needs to have an integrated SIPP. Applying to an AJ Bell and then dealing with transfers

moving across the custodian, there was very little automation that we found.”

26Table 7: Account creation, family linking & fund gating

Accounts can be created for:

Individual Corporate Family Ability to

Provider Trust Charity

investors investors linking gate funds

7IM X X X X X X

Advance by Embark X X X X X X

Aegon Platform X X X X X

AJ Bell X X X X X X

Aegon Retirement

X X X X X

Choices

IFDL - Ascentric X X X X X X

Aviva X X X X X

BNY Mellon Pershing X X X X X X

Fidelity FundsNetwork X X X X X

Fundment X X X X X X

Fusion Wealth X X X X X X

Hubwise X X X X X X

James Hay X X X

Nucleus X X X X X X

Old Mutual Wealth X X X X X X

P1 X X X X

Parmenion X X X X

Praemium X X X X X

Raymond James X X X X

Seccl X X X X X

SEI X X X X X X

Standard Life X X X X X

Transact X X X X X X

True Potential X X X X X X

27Additional platform services

Investment platforms provide services beyond custody and trading. Firms, and their employees, will value these to a greater

or lesser extent. The loss of this support must be weighed in any decision to launch a white-label platform and consideration

given to what will take its place.

“The other benefits that you have with having the life company platforms is that you have actual

technical support for advisers around complex planning issues. Do you then provide that yourself?

Where do all of those things that we historically go to platforms for come in?”

“What worries me is the client support - more than anything. That help desk, which at the moment is

the platform team, is quite small here.”

Brand and client interface

Platforms offer varying degrees of branding options to financial advisers and some even offer a client app. Financial advisers

who are looking to offer a better customer experience and who want to have their brand more prominent in front of clients,

can opt for a third-party platform that offers these branding options.

The CEO of a large financial advice business and DFM described how his firm wanted to be the brand that was front

and centre for clients: “we wanted to be at the front , if you like in terms of brands… we wanted our clients to associate

more with us, as opposed to a Transact, Novia or Nucleus when it came to valuations or whatever the case may be.” They

built a portal reliant on API connectivity with the custodian platforms. As the firm grew organically and now as it pursues

acquisitions of other advice firms, the firm wanted more control over the systems. They have built a back-office system off

of Microsoft Dynamics and recently launched a white-label platform.

The CEO of a platform technology company put it this way:

“Firms are doing this because you want to build your own brand not somebody else's. Value is in you,

not giving value to one of other platforms.”

28Table 8: Branding & apps

Branding options for platform

Logo and brand End client

Provider Branded logo No branding Client login

colours mobile app

7IM X X X X

Advance by Embark X X X

Aegon Platform X X X

AJ Bell X X X X

Aegon Retirement Choices X X X

IFDL - Ascentric X X X

Aviva X X X

BNY Mellon Pershing X X

Fidelity FundsNetwork X X X

Fundment X X X

Fusion Wealth X X X

Hubwise X X X

James Hay X X X

Multrees X X

Novia X

Nucleus X X X

P1 X X X

Parmenion X X X

Praemium X X X

Quilter (OMW) X X

Raymond James X X X

Seccl X X

SEI X X X

SS&C X X

Standard Life Wrap X X X

Transact X X X X

True Potential X X X X

29APIs, what are they and what do you need to

ask providers about them.

Q&A with Simon Clare, CTO Bravura Solutions and David Tonge, Co-Founder and CTO Moneyhub

In our research into the advice tech stack we repeatedly find that lack of integration poses a substantial challenge for

adviser businesses. Firms have invested in the various elements they need to build a tech proposition that suits the firm

and their clients, often on the promise that those elements will seamlessly stitch together, only to find the reality does not

deliver an integrated experience and data has to be manually re-entered.

The finger is frequently pointed at APIs, but what actually is an API? Why do they sometimes not work? What should

advisers ask and expect of their technology partners?

We spoke with Simon Clare, Chief Technology Officer at Bravura Solutions and Dave Tonge, CTO at Moneyhub, to answer

some these questions and find out if we can look forward to a brighter, more connected future.

What is an API?

Simon Clare [SC]: It stands for Application Programming Interface. Basically APIs are ways for computer systems to speak

to each other. It’s a contract - that word is important - a contract or a promise one computer system makes to another. If a

computer system publishes an API, it promises that if you talk to it in this particular way and tell it what to do on a thing it

knows about, then it promises to do that certain thing.

Dave Tonge [DT]: Now, when people talk about APIs they’re generally talking about a way for cloud-based services to talk

to each other.

For example, let’s say you want to take payments on your website, you can use a company called Stripe and they provide an

API so that your web developer can look at their documentation and then create the process for information to be collected

on your website, sent to Stripe and processed back to you.

APIs are also used to transfer data. Let’s look at open banking: all of my financial transaction data is at my bank with my

current account. Maybe I want to use another tool to analyse that data and aggregate it. Before APIs, I would have to log

in to my bank account, hope they had the ability for me to export a file, or I’d have to manually copy down all the bits of

data, then I’d need to go to another tool, try and import the data or manually copy things in. With an API, the tools can be

connected. I can simply authorise a tool to go to my bank transactions and analyse them.

Aside from data transfer, what else is good about APIs?

DT: The good thing about APIs is that they unleash a bit of creativity. Take the example of Google; there are loads of add-ons

for their Office suite. If they had to do technical work for each and every one of those, there would be far less integrations.

Whereas they can say this is our API and anyone with a good idea can create an extension or an add-on that works with

Google.

SC: I think it’s really important to be able to run open systems, and for clients to be able to participate in new emerging ways

in which platforms are communicating. It’s a rapidly evolving world and the more we can maximise the connectivity and

interoperability of our systems the more we can participate in a connected future, where we can plug and play with other

people’s technology.

30Are all APIs ‘open APIs’?

People talk about Stripe’s APIs as being open, because you can just access their website and all the APIs are publicly available.

So are there two types of APIs – open and not?

DT: There’s probably a bit of a scale; it’s not so much one thing or the other. A better way to differentiate would be ‘standards-

based APIs’ and ‘proprietary APIs’. Standards-based APIs are what people think of as ‘open’. For example, again with open

banking, the banks use standards-based APIs, so a tool like Moneyhub can write code once for Barclays and use the same

code to connect with HSBC and the same code for Nationwide. If they all had proprietary APIs we would have to do extra

work to connect to each one separately. Sometimes there’s no choice but to do a proprietary API, if there aren’t common

standards agreed between businesses.

How can advisers figure out the costs involved with APIs?

DT: Something like a payment tool for your website can be quite clear in the pricing model, for example some fee based on

each payment. In other cases the cost models can be tricky, especially if it’s based on usage and it can be difficult to estimate

what your usage costs will be. What I would recommend, and what quite a few companies offer, is more like a per user

based pricing because it’s a lot easier to understand and often you might be paying for existing systems like that already. For

example you might be paying for a back office system on some level of per a number of users.

The other thing I would say is nowadays, providers shouldn’t be charging extra for an API. If you’re already paying them for

some service, the API should be part of that service. Google don’t charge extra for their API. The API is just another way of

accessing that same service.

Why don’t they always work? And why do they sometimes work and

then stop working?!

SC: Every API is a promise, and if a provider promises to keep this API up to date, they promise that this API works. If I

change my software from one version to another, that promise still stands. If I change that and I break it, then that breaks

it for everyone who is using my API, so I have to change my API in a controlled process. That effectively is why it might go

wrong sometimes. Whoever is maintaining those APIs has to do a good job of it. They have to maintain them formally.

DT: Fundamentally, some of the problems are down to a mismatch in the different services. If you have a system that is

geared for US 401(k)s and you’re trying to get that system to display UK-based tax wrappers, the problem there is above

the level of the API.

The other problem in the investment world is that a lot of the firms might not have as much technical experience in building

and maintaining high quality APIs. That I think is part of the problem, and the lack of standards. Sometimes there are these

different proprietary APIs and it’s quite easy for one company to blame the other.

Often things go wrong in the consent and authentication stage that is necessary in financial services, for example an open

banking tool has to go to my bank, and the bank has to ask if I’m happy to share my data with the tool, and that pattern is

sometimes where it falls down. The most complex part of the whole pension dashboard system is identifying the user, taking

the user through the authentication and making sure you capture their permissions. And then especially in the adviser world,

you’ve got all these intermediated connections and multiple users.

31What should advisers ask their prospective tech partners?

SC: There are two key questions around APIs. The first is, do they have their own APIs that they maintain and manage? They

should be able to give you documentation that describes what those APIs are and what they do. The second thing is, we’re

in a maturing world where API standards are coming into place now as well. So question two is ‘do they use any open API

standards’? You can’t apply that one across the board yet because we’re not quite at the place where there’s a formal fully

open set of API standards for the industry.

DT: If an advice firm doesn’t have access to large amounts of technical expertise, then ideally what you’re looking for is

existing integrations between the parties. Taking a step back from APIs, what we want to get to is solution A, B and C work

together. So that everything is in sync and we’re not having to manually export data from one place and import it in another.

The way in which that happens nowadays is often through API-based integrations. So you can just ask what are the APIs and

what companies have integrated to it. If the systems aren’t already integrated, then there are tools like Zapier that mean you

might be able to do some of your own integration work. That can be really useful for creating customised workflows. You can

be a little bit less at the mercy of say, a back office provider if there’s a new feature you want to implement. If they provide

a good API, then you might be able to add in logic like, for example, when there’s a new client onboarded, using Zapier you

can say ‘send this email here’ or ‘update this record’. There are all sorts of things you can do.

What does the future look like?

DT: In an ideal world all of this stuff would just speak together. In another five years, not much longer than that, there’s

this whole ‘no code’ movement, things will start speaking together a lot more. There are a lot of people now, especially a

little bit outside financial services, who are moving away from the old way of doing software, where you have something

very specific built for a specific industry to solve a specific problem. Now people are realising a lot of companies actually

have similar problems that need to be solved and the requirements are actually very similar. I think where things are going

is that you have these cloud-based services that maybe do fewer things but do them really well and can speak with other

systems. In the short term that could make things even more complicated for a financial advice firm, and maybe there will

be consultancy fees to pay if you don’t have the experience to hook that all up, but in the long run that is likely to be a far

lower cost than paying a big bill to a proprietary piece of software that is only targeting your niche.

Right now for advisers my advice would be to get their data in order, use a cloud-based system, wherever possible one that

has an API. That won’t fully futureproof you but it will make it a lot easier.

32Concluding thoughts

The shift towards white-label platforms among large financial advice businesses is underway and will become substantial

if third party platforms don’t act soon. While only 9% of firms offer one now, half of firms with over £250m AUA plan to

launch one in the next three years. Many of those will of course decide in the end to pursue a different path, but the threat

to third-party platforms is real. With the exception of margin, third-party platforms can address the other main drivers

that lead to white labelling. Platforms will need to develop their propositions to meet the needs of firms and to support

management of assets at the portfolio and firm level.

The lucrative jingle of margin is tempting. But the responsibilities that come with the role of being a platform operator are

real. Firms must remember that if you say you have a platform and are charging for the platform, you are on the hook for

the oversight responsibilities.

33Platform Profiles

Advance by Embark

Overview

Description provided by Advance by Embark:

At Advance by Embark, we respect the value of professional financial advice. We’re committed to supporting a thriving

intermediary community that is able to deliver advice profitably. At the most fundamental level, it’s our business to be there for

advisers. The Platform’s rich functionality and extensive investment range make it potentially suitable for a broad range of client

types. From those still accumulating wealth, to those in the decumulation phase with a focus more on making their wealth last.

Supporting advisers’ segmentation strategy, our combined product suite, available assets, tools and functionality have been

designed to offer particular benefit for clients consolidating their wealth to facilitate more effective retirement planning, and

who advisers then wish to roll seamlessly – without a platform move – into the retirement phase itself.

Platform details

Ownership: Advance by Embark is a trading name of Sterling ISA Managers Limited (SIML) which is a

wholly owned subsidiary of Embark Group.

Strategic partners: Major distributors such as Openwork, Tenet and SimplyBiz, and important regional advisers

such as Radcliffes and Prosperity in the retail market

Assets Under Influence: £26.8 bn as at Q1 2021

Target customer: No minimum assets, advisers with mass market/mass affluent/HNW clients

Whitelabel offered: Yes

Compliance

Framework offers: • Appointed Representative

• Agent of the client

Safeguarding and

arranging permissions: Held by Advance by Embark.

Client money and CASS

responsibility: Held by Advance by Embark.

Regulatory reporting

responsibility: Held by Advance by Embark.

Orphan client policy: We continue to engage with the client in all matters. They have opportunity to self-serve

following the loss of the adviser. They would move onto our firm's relevant product.

Functionality

Tax wrappers: • ISA • Offshore bond

• JISA • SIPP

• GIA

SIPP Provider Advance by Embark

Branding: Logo and brand colours can be altered

34You can also read