Social Commerce in Indonesia - Empowering entrepreneurs with smart connected capital - AC Ventures

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Social Commerce in Indonesia

Empowering entrepreneurs with smart connected capital

The information contained within this Presentation is proprietary to Agaeti Convergence Capital III L.P. (ACV). It is confidential, legally privileged and protected by the relevant laws. It is not intended to be

distributed to any third party without the written consent of ACV. All of the information contained in the Presentation is subject to further modification and any and all forecasts, projections or forward-looking

statements contained herein shall not be relied upon as facts nor relied upon as any representation of future results which may materially vary from such projections and forecasts.

Research Agenda

Identifying New Consumer Models

Social Commerce: Market Overview

Segmentation

Success stories

Local Players

KPI & Valuation

Investment Timing

Impact of COVID-19

2

Consumer eCommerce models

4

Social Commerce is a subset of eCommerce that involves social-sharing,

allowing businesses to leverage on social networks to drive sales.

Consumer Commerce Models

Marketplace Directory/Listing D2C Platforms Social Commerce New Retail (O2O) Rental

Reseller/Agent Group- Media/Content MLM

Buying/Team

Purchase

“The fundamental driving principle behind social

commerce is trust, where individuals are

Online/Offline Influencer/ Dropshipper Offline Agent empowered to sell and recommend your products to

Agent Affiliate their community, network, followers, and friends.

Social commerce innovation empowers both online

and offline channels, allowing individuals to

commercialize their relationships with others.”

5

What is Social Commerce?

6

Indonesia’s eCommerce market is a US$12B sector, with the

potential to reach US$53B-US$200B by 2025

Indonesia E-commerce Market Size (US$B) Indonesia eCommerce Market (US$B)

60

250

53

201 50

200 43

40

35

150 134

28

30

23

100 90 19

20 15

60 12

50 40 10

27

12 18

8

- 0

2018 2019 2020 2021 2022 2023 2024 2025

2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: McKinsey (2017) Source: WeAreSocial (2018)

eCommerce penetration is only 14% of total eCommerce User in Indonesia (#M) and

Whatsapp Users in Indonesia (#M)

population (2018, #M) ARPU (US$)

300 50 47.42 200

113.50 268.2 44.42

112.37 41.60 187

250 38.97

111.26 40 36.50 161

34.19 150

110.16 200 30 32.03 139

109.07 150 150

107.99 142 130 30 120

150 103 100

106.92

105.86 20 89

100 75

37 63

50 50

10

0

Indonesian Urban Internet Mobile Mobile eCommerce - 0

2017 2018 2019 2020 2021 2022 2023 2024 2017 2018 2019 2020 2021 2022 2023 2024

Population Population Users Internet Social Media Users

Source: McKinsey, Statista, WeAreSocial Users Users

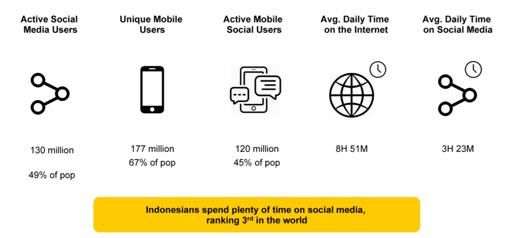

Social Commerce is the amalgamation of eCommerce and Social; 49%

of the Indonesian population is active on social media.

• 130 million active social media users in Indonesia (120 millions of which are on mobile), comprising 49% of the population.

• According to Indonesia’s Ministry of Finance, 64 per cent of all e-commerce transactions in 2018 occurred through social media.

• With about 150 million internet users in a country of 250 million people, Indonesia’s internet population size is fourth worldwide after

China, India and Japan.

• Consumers are becoming more digitally savvy; people spend over 3 hours on social media browsing, discovering, and interacting with

friends.

• PayPal’s survey of 1.4K merchants in 7 Asian countries found that 80% of merchants were already selling through social media channels,

and 92% found that selling through social media improved their financial condition.

Source: WeAreSocial, PayPal 2017

8

Social, Economic and Technology trends demonstrate that Social

Commerce is well positioned to succeed in Indonesia

• Indonesians spend 3h23m on social media daily. • McKinsey forecasts state that online-commerce sales will grow

• 49% of Indonesia’s population is are active on social eightfold, with social commerce contributing to U$25B by

media platforms. Indonesia is ranked 3rd for social media 2022.

usage in the world. • 35% of online sales are generated by women; eCommerce has

• 76% of users shopped online in 2018 via mobile phone led to savings of 11 to 25 percent for customers outside Java.

(survey of ages 16-64)., of which 35% of users make • An estimated 90 million Indonesians will have joined the

online payments. consuming class by 2030.

• Annual consumption in other cities is 3x greater than

Jabodetabek, where offline consumption is 6.5x of online,

whilst Jakarta’s offline consumption is only 2x of online

• 100 million Indonesians purchased consumer goods online in

2018, growing at 5.9% YoY.

• Growing eWallet adoption – GoPay, Dana, LinkAja, and others,

with only 3.1% of Indonesian populatin owning a mobile money

account.

• eCommerce users only at ~40M users, with ARPU estimated to

be US$89.

Source: WeAreSocial, PayPal, CLSA

Social Commerce is more than social-media marketing; it is a go-to-

market strategy to acquire scalably, efficiently and effectively

Social Commerce

In the context of Asia, Social Commerce is NOT:

• Social media marketing

• Content Marketing

• Omni-channel software that enable SMEs to

sell on social media

Reseller/Agent Group-Buying Media/Content MLM

From traditional commerce: With examples like Pinduoduo, Meesho and Yunji, Social Commerce

has the use of social network in the context of eCommerce

transactions. It is the utilising of online and offline network, that

Principal Distributor Retailer Consumer

enables social interaction to facilitate online buying and selling of

products and services

Now with social commerce as an additional distribution channel:

Social Agents /

Principal Distributor Commerce Friends / Consumer

Platform Members Social commerce is a go-to-market model for platforms to acquire

customers in a faster, more cost-efficient (lower CaC) and effective

way, and allows for trust.

10Segmenting Social Commerce in Indonesia

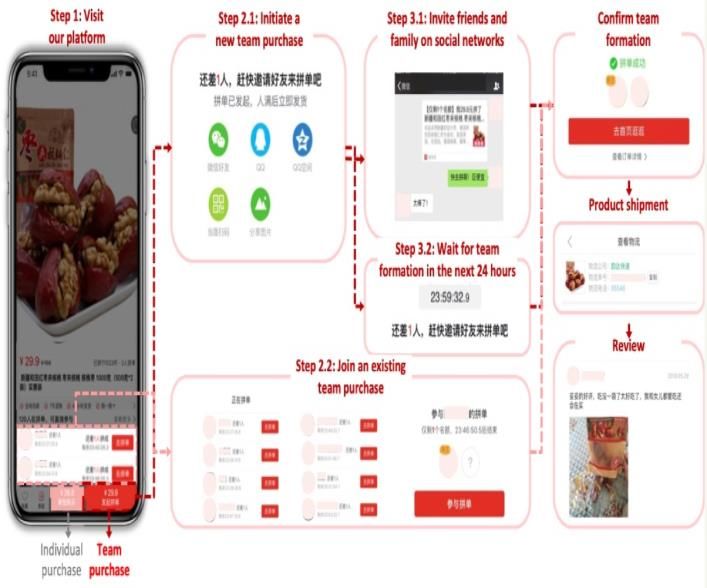

11Social Commerce’s four main models are Agent/Reseller, Group-Buying,

Media/Content Driven, and Membership/MLM

Consumer Commerce Models

Marketplace Directory/Listing D2C Platforms Social Commerce New Retail (O2O) Rental

Reseller/Agent Group-Buying Media/Content MLM

/Team Purchase

“The fundamental driving principle behind social

commerce is trust, where individuals are

Online/Offline Influencer/ Dropshipper Offline Agent empowered to sell and recommend your products to

Agent Affiliate their community, network, followers, and friends.

Social commerce innovation empowers both online

and offline channels, allowing individuals to

commercialize their relationships with others.”

12Social Commerce’s four main models are Agent/Reseller, Group-Buying,

Media/Content Driven, and Membership/MLM

Reseller/Agent Group-buying

Offering products and discounted prices based on users sharing to their social

Platform that reaches out to end consumers that allows them to access product

network to form a team-purchase

through online/offline resellers, that are incentivized through monetary rewards

Value-Adds:

- Significantly reduced / discounted prices

Value-Adds:

- Lower CaC due to virality and sharing features

- Access (additional distributional channel, especially for Rural)

- Aggregating demand and high frequency allows for negotiating power with

- Lower customer acquisition costs

suppliers, and presents a good channel for brands to clear inventory

- High customer trust & loyalty

Challenges:

Challenges:

- Usually focus on products that are cheaper and have high frequency, making it

- Product cannot be easily comparable / must be more complex

difficult to monetize as margins are slim

- On-going agent acquisition, retention and education

- With rising middle class, demand for cheaper and unbranded products could

decrease over time

Content/Media Membership/MLM – offline/online

Utilising user-generated content, reviews and influencers to enhance discoverability, Platforms that empower members with training to manage own stores, promote

promote product and sell on platform product to communities, incentivized by aggregate discounts or cash rewards

Value-Adds: Value-Adds:

- UGC brings trust and authenticity, building positive brand perception - Trust and loyalty due to community and member’s feedback

- Focus on high value goods (high referral items) - Lower CaC, leveraging on community building

- An effective marketing channel through content and partnerships with influencers

Challenges

Challenges: - Reliance on members to generate revenue

- Product will be more complex and have lower purchase frequency - Difficulties in recruiting and retaining members

- Content becomes King, but content may be expensive (made in-house as UGC - Risk of being considered a Pyramid Scheme, as members must continue to

not always reliable) recruit to access rewards

- Sales are dependent on trustworthiness of KOLs

13Social Commerce was built to acquire users with lower CaC, utilizing social

networks to help other users discover product to bridge trust gaps

Reseller Group-Buying Content Driven

Discoverability

• Referral-based • Browse-based • Content-based

• Based on agent/reseller • Discovery from referral • Influencer-based content

referrals (offline and by friends (mostly online,

online) aspirational)

Social sharing

• Sharing on social media & F&F • Sharing to F&F network • Sharing on social media

network (mainly whatsapp, chat- • Affiliate marketing

• Accessing agent’s catalogue based)

• Gamification

• Agent-referral • Virality through sharing • Lower CaC due to UGC, but

CaC

• Lower CaC • Lower average CaC can have digital marketing

• Agent acquisition costs and content creation costs

required • Influencer marketing costs

Social Commerce is essentially eCommerce, but the go-to-market strategy (reselling, group-buying) utilizes social features which

helps bring the CaC down, hence decreasing the cost of GMV, allowing it to scale faster than traditional eCommerce platforms.

14Social Commerce is also meant to increase consumer reach, both

offline and online, with users incentivized to continue to share

Reseller Group-Buying Content Driven

• Strong offline component, starts • F&F and social network • Social media audience

with F&F • Mostly online • Mostly online

• Mostly focused towards tier 2-4 •

Reach

Sharing to result in virality

cities due to low eCommerce • Use of community leaders for

penetration logistics

• Logistics hub built around agents

Incentives

• Agent commission fee • Discounted prices for high • Affiliate marketing fee or

frequency items % commission fee

Nature of Product

• Medium complexity, products • Low complexity, commoditized • High complexity

that require trust • High frequency • Various frequency levels

• Lower frequency • Lower margin • Various margins

• Higher margin • Unbranded items • Stronger brand recognition

The multiple models of social commerce will specialize in different products and utilize different incentivizes to increase customer

reach and transactions, selling different products that vary in complexity, frequency and margins.

15In Indonesia, majority of Social Commerce players are targeting the

Agent/Reseller space, focusing on different product categories

Global/Regional Local

Reseller/Agent

Group-Buying

Media/Content

MLM

16Most Social Commerce players focus on mid to high frequency

products; Fashion all the way to FMCG and Fresh Produce

Frequency Customer Motive

High Frequency Cheap/Discount

Reseller Consumer Reseller Consumer

Low Frequency Access/Referral

17The platforms that focus more on high frequency products are likely to

suffer from lower margins, although CaC will still be lower than

marketplaces due to sharing via personal network

Margins High Margin Awareness

Via Friends / personal network

Reseller Consumer Reseller Consumer

Low Margin Via influencer / “aspirational”

18The challenges for the Agent/Reseller Model include agent

acquisition and retention, as well as high competition

Without negotiating power, social commerce platforms start out by working directly with

retailers generate sales or scraping catalogues from existing eCommerce platforms,

Establishing negotiating power with Principals

negotiating bulk discounts or generating bulk discounts by purchasing SKUs upfront (and

taking on the capital risk).

Cannot be too complex requiring professional intervention (real estate, etc), but also

Products offered must be complex to require cannot be too simple such as products which can be made without much trust (pencils, etc).

trust and validation element Need to focus on product that require trust, reference and advice (i.e. fashion)

Offline presence is required, as the individuals that need agent intervention are ones that

Offline presence required to tap into areas cannot access or do not trust traditional eCommerce platforms, which could be expensive as it

with lower eCommerce penetration requires local community leader recruitment and agent management, and “landgrabbing”.

Although platforms do not have to incur a high CaC, recruiting and retaining agents have been

one of the greatest challenges for a reseller platform. Many platforms adopt a “controlled

Acquiring and retaining agents/resellers agents” model, where retention is stronger, however investment in training and agent

management is essential.

There are many platforms in the agent/reseller space – the landscape is crowded with players

Strong competition from agent/reseller testing with different consumer products, raising lots of money, going-to-market through

community leaders, and working on a strategy called “landgrabbing”, as they are trying to

platforms

“grab” one city/area first, to have a strong presence there. E.g. Dagangan’s territory is Jogja,

but Super’s territory is Surabaya.

19Group-buying also sees challenges in establishing negotiating power with

suppliers, and also competition from established eCommerce giants

Without negotiating power, social commerce platforms start out by working directly with

Establishing negotiating power with Principals retailers generate sales, negotiating bulk discounts or generating bulk discounts by purchasing

SKUs upfront (and taking on the capital risk).

Focus for group-buying usually starts with fast-moving and high frequency goods as this will

Products sold has to be low complex, fast- result in frequency of sharing and virality, but margins are low and monetization from this will

moving, and thus have low margins not be enough (though there is opportunity to white label).

To overcome the challenges facing Indonesia in online commerce, priority moves include

Requires streamlining of logistics and cash less

resolving logistical bottlenecks, encouraging more cashless payments, and getting more micro,

payments small, and midsize enterprises online.

As growth is driven by price and discounts, One of the concerns about Pinduoduo is product quality, due to Pinduoduo capturing supply

unbranded items result in issues of counterfeit from unbranded FMCG suppliers, which creates concerns around product quality and

counterfeit products.

product

Tokopedia, Shopee, Bukalapak and the other giants are well-funded and have reached a

Strong competition from well-funded certain level of scale – users, merchants and GMV, building out their network effects. Shopee

marketplaces/platforms already offers a ”group-buying” option, although it’s still in the early stages.

20In Indonesia, the highest grossing consumer category in eCommerce is

Travel & Accommodation, with Fashion coming next

Margins High Margin Breakdown of Online Consumer Goods (2019)

0% 3%

15%

14%

40%

Reseller Consumer

10%

9%

10%

Fashion & Beauty Electronics & Physical Media Food & Personal Care Furniture & Appliances

Toy & Hobbies Travel & Accommodation Digital Music Video Games

~ ~ ~ ~

Source: WeAreSocial

Low Margin

21The industry gross profit margins for different consumer products vary,

with beauty and fashion presenting the highest margins

Beauty & Skincare Fashion FMCG Personal Care FMCG Packaged Foods

~ 60 - 90% ~ 30 - 50% ~ 3 - 5% ~ 20 - 30%

Furniture Agriculture Electronics Travel & Accommodations

~ 30 – 40% ~10 - 25% ~ 30 – 40% ~ 30 – 40%

22The gross margins for different consumer products vary, with some social

commerce platforms focusing on one category more than others

Homemade Packaged Goods Snacks F&B Sembako

~ 12 - 15% ~ 8 - 9% ~ 5 - 15% ~ 5 - 6%

Cigarettes Fashion Beauty Skincare

~ 0 – 3% ~30 - 40% ~ 80 - 90% ~ 70– 80%

23Success Stories

24We have seen high value companies adopting each of the four models

we identified in Social Commerce in both India and China

Reseller/Model Group-Buying

EST: 2015, India EST: 2015, China

Valuation: US$575M Valuation: ~US$47B market cap

Category: Fashion & Lifestyle Category: Fashion, FMCG, Electronics,

Business Model: % GMV take Fresh Product

rate Business Model: Advertising (90% of

Traction: 2M+ resellers, 21K revenue) & Merchant Services

suppliers Traction: 536M active buyers, 135 DAU,

US$142B GMV, US$4.2B Revenue

Content/Media MLM/Membership

EST: 2013, China EST: 2015, China

Valuation: US$2.7B Valuation: US$690M market cap

Category: Fashion & Beauty Category: Fashion, Beauty,

Business Model: Advertising & Household, Travel, Electronics

Commission Business Model: Direct sales

Traction: 713M users, 100M commissions (87% of revenue)

active users, 29K brands Traction: 23.2 million buyers, 7.1

million members

25Group-buying/Team Purchase Case Study: Pinduoduo

User Offering Merchant Offering Products: lesser known, cheaper brands, small ticket

• Marketplace that adopts a group- • Helping merchants boost GMV through size strategy

buying / team-purchase mechanism larger volume orders • Household Items Apparel is PDD’s

to allow for discounted prices • Lower barriers to transact online (lower take • Fresh Produce largest grossing

• Gamified experience to enhance rate, brand requirements) • Apparel / Clothing category

shopping experience • Inventory management and analytics to • Electronics

• Women make up 70% of user-base help merchants reach targets

Key Moats 5.2% PDD 2018 Expenses Breakdown

Risks Market Share

12%

• Clear use-case in tier 3 / 4 cities and • Inconsistent suppliers that platform 5%

for price sensitive user groups are dependent on

• User acquisition costs is much • Reliance on existing social media

lower than other major eCommerce platforms (WeChat)

56%

platforms due to snowball effect of • Intense competition from giants 27%

group-buying and retailers

• AI for user screening, engagement • User loyalty due to high price

data sensitivity

Sales & Marketing G&A R&D Cost of Revenues

Traction FY 2019 Revenue generation is similar to Alibaba’s marketplace play Revenue Model

Advertising /

536M 135M US$142B US$4.2B 3.6M CAC Merchant

Premium

Active Buyers DAU GMV Revenue Merchants US$2 Services

Listing

Online advertising take rate now 2.6%

26Agent/Reseller Case Study: Meesho

User/Agent Offering Merchant/Seller Offering Products: household purchases, driven by women at

• Suite of tools that enable resellers • Sellers have additional online sales

home

to sell products to their friends via channel, expanding their reach to • Apparel/Clothing Apparel is

social media, mainly fashion tier 2-3 cities • Home Meesho’s largest

• Network of • Logistics and supply chain support • Kitchen grossing category

wholesalers/manufacturers/sellers • Beauty

to give vast supply for resellers to

sell

• Resellers can set prices

Key Moats Risks Meesho 2018 Revenue Breakdown Meesho 2018 Expenses Breakdown

3% 19%

• Resellers bridges trust gap in • Logistics costs is high, spending

eCommerce and creates stronger 91% of its total revenue in 2018 on

interaction, as online shopping is still deliveries, and 41.5% of total 3% 45%

governed by personal networks in rural expenses 46% 51%

India • Agents require training and 17%

• Meesho carries no inventory, as sellers retention/re-engagement actvities

send products to Meesho’s last-mile 12%

fulfillment center Logistics Advertising & Marketing

• Negotiating power to go direct to Comission Delivery Fee Penalty Income

Seller Bonus, Rewards, Discount Employee Benefits

manufacturers to source supply

Traction FY 2018 Revenue Model

10-20%

2M US$200M US$11.7M 22K Return

commission Delivery fees

Resellers GMV Revenue Merchants Penalties

from sellers

51% of Revenue comes from Commission Income

27Membership/MLM Case Study: Yunji

User/Member Offering Supply Offering Membership Model: decentralized network of

• Initially, Yunji is more a platform than “members” who help sell products

• Social commerce company relying marketplace, acting as a retailer by

mostly on WeChat sharing in order to holding own inventory instead of • Members signup to be able to access the platform

generate sales by “members” connecting suppliers to buyers • They can then access special discounts/offers along with the ability to open their own

• Members access special discounts/offers • Now, Yunji is focusing on building up their stores

along with the ability to open their own marketplace model • Members promote their products to other users (mostly via WeChat)

stores, and receive incentives through • Apparel is the highest GMV generating • If they manage to sell products or recruit new members, they receive a share of

discounts for future purchases category revenue (not directly through cash but through discounts for future purchases)

Yunji 2018 Expenses Breakdown Yunji 2018 Expenses Breakdown

Key Moats Risks 1%

1%

7% 1%

12%

9%

• High network effect through • Yunji has been under scrutiny from

membership model Chinese authorities because of

• Yunji’s decentralized model enables it suspicion of operating a pyramid

to grow with lesser marketing expense. scheme.The company warns in its

• Yunji operates 41 warehehouses across prospectus that China could at any 82%

China, operated by 3rd Party 87%

time redefine what constitutes

Cost of Revenues Fulfilment

pyramid selling. Merchandise Sales Membership Program Revenues Other Revenues

Sales and Marketing Technology & Content

General & Adminstrative

Traction FY 2018 Revenue Model

Revenue generation

7.1M 23.2M Active US$3.2B US$1.6B Merchandise Return is similar to JD.com’s

members, 6.1M Delivery fees retailer play (holding

transacting members Buyers GMV Revenue sales Penalties

inventory)

Members contribute to 11% of annual revenue and 66.4% of transactions. 87% of Revenue comes from Merchandise Sales

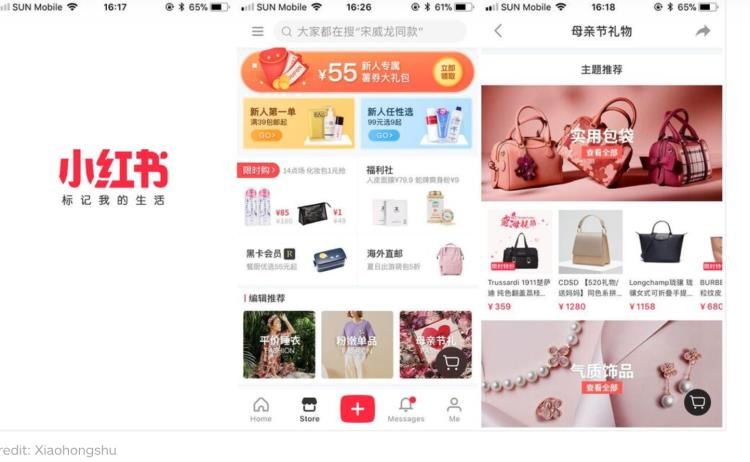

28Content/Media Case Study: Xiaohongshu (RED)

User Offering Leveraging UGC & Content to convert users to transact:

• an ecommerce platform for luxury goods

from overseas – primarily fashion and Advertising UGC Content eCommerce

beauty products.

Focus Areas:

• content-based, social commerce

• premium quality and exclusivity; it has built a highly-engaged community of

platform to discover and review

savvy users who research and review their products extensively on the app

products, utilising influencers/KOLs.

• trusted source of advice and recommendations for its community, working with

Focusing on user-generated content to

China’s biggest influencers

build trust and word of mouth

advertising

Key Moats Risks

• High AOV due to target consumers, • Some users who are window

which have mid-high consuming power shoppers finding products on RED

as 57% of users are from Tier 1 but purchase from other platforms

like Taobao Girls are big purchasers when it comes to cosmetics and fashion.

• The site also includes a high focus on

• complaint from some users that The conversion rate of Xiaohongshu users is as high as 8%,

security, with qualified brands and

the site has become too compared with only 2.6% on Tmall, the biggest ecommerce

retailers having to submit an

commercial and no longer platform for official brands in China. In addition, every customer

application before being accepted on

encourages the same originality on Xiaohongshu makes 3 orders per month on average.

the platform.

from users.

Traction FY 2018 Revenue Model Products: high-end, luxury items

• Fashion

5-10% • Beauty

200M Registered US$105B US$212M 15-20%

Users 30M MAU Commission Fee

Advertising

• Skincare

GMV Revenue Campaign Fee

• Nutritional Supplements

90% of users are middle to upper class women, a lucrative market for global fashion

29Local Players

30Indonesia landscape – Reseller/Agent Model

Founded January 2019 March 2018 November 2018 April 2018 2015

Team Size 10-15 11-50 100+ 500+

HQ Jakarta, Indonesia Jakarta, Indonesia Bandung, Indonesia Jakarta, Indonesia Mumbai, India

Countries

Founders Coal & mining, game development/ Ex bobobox, UrbanIndo, Politeknik Seasoned Media entrepreneur, ex Ex Sony Corp, Seasoned

Background animation, traveltech graduate Colombia Entrepreneurs

Description Digital MLM, social reseller platform platform for creating online Social commerce platform to agent-led commerce group buying online reseller network of

shop websites empower individuals to sell that enables community leaders to housewives and SMBs, who sell

Muslim products, connecting become retailers within their products within their network on

Muslim brands to resellers communities social channels.

Offering Agents – order management Agents – order Agents – order management Super’s main service, SuperAgen – Agents – order management

platform, own online catalogue store management platform, platform, store front Shahria compliant, profits from platform, own online catalogue

Users – view catalogues and make own online catalogue store reseller, order management store

orders Users – view catalogues Users – view catalogues and make

and make orders orders

Target Demographic Tier 1 cities Middle income women, Tier 1 & 2 SMEs, Tier 1 & 2 cities Middle income women, Tier 1/2/3

cities cities

Category Fashion, Lifestyle Fashion, Lifestyle Muslim Fashion, majority for FMCG, packaged food Fashion, Lifestyle

women

Business Model % GMV take rate % GMV take rate % GMV take rate % GMV take rate % GMV take rate/commission

Traction 800 SKUs, 200 Agents, 70 Brands US$10M Annualized GMV 17K resellers 1.1K Agents 2M+ resellers, 21K suppliers

Funding Seed (US$1M) - East Ventures (US$3.2M) - Altos Ventures Series A (US$8.3M) – Jungle Undisclosed – Y-Comb, Insignia, SAIF, Sequoia, DST, Facebook,

Ventures Alpha JWC, B-Cap Partner’s, Arrive Naspers

31Indonesia landscape – Group-Buying/Team-Purchase Model

WeBuy We haven’t seen that many players in

Indonesia that adopt a group-buying

Founded November 2019 2018 October 2018

model. Many players in this space

Team Size adopt the reseller/agent model,

HQ Jakarta, Indonesia Singapore Jakarta, Indonesia focusing on apparel and lifestyle

Countries products.

Founders Background Seasoned Entrepreneur, ex 2x entrepreneur, Chicago Booth MBA

Investment Banking

In the past, we’ve seen players such as

Description Group-buying platform based in Group-buying platform based in Group-buying platform based in Indonesia DealKeren, Disdus (acquired by

Indonesia Singapore (also recently launched a reseller Groupon), LivingSocial (said to rebrand

platform)

to Ensogo, after being acquired by

Category FMCG – essential items FMCG, baby products Fashion, Lifestyle DealKeren), Maiplay (Eduordo Savern

was an advisor) and Dskon.com.

Target Demographic Middle income customers, Tier 1/2/3 Low to middle income customers, Tier

cities 1/2/3 cities None of the players in the services

category have failed to find ways to

Business Model % GMV take rate % GMV take rate % GMV take rate

Advertising & Merchant Services Advertising scale. Assumption is that they focused

on non-essential services such as

Traction US$2.5 AOV, 5.9 orders per Undisclosed 270K monthly active users

transacting users,, April GMV US$22K

travel, restaurants, hotels, spas, etc.

Mucho is the only established group-

buying platform currently present in

Indonesia, sourcing product directly

Funding Seed (US$1M) – East Ventures, RHL Undisclosed - GFC Seed (US$3M) – Qiming Venture Partners from China.

Ventures, AC Ventures

32Indonesia landscape – Group-Buying + Agent (Hybrid)

Founded July 2019 April 2018 October 2018

ChiliBeli’s model is an agent-model,

Team Size 246 100+ however there is a group-buying

Founders Background Serieal tech entrepreneurs, ex Seasoned Media entrepreneur, ex Jakarta, Indonesia component to it, where Agents can be

consultants, ex Ant Financial, ex MIT, Colombia incentivized by discounts, and not just

ex Nanyang, Ex Lazada, Ex Tmall

financial incentives.

Description social commerce platform that agent-led commerce group buying that 2x entrepreneur, Chicago Booth MBA

connects manufactures/farmers with enables community leaders to become

agents directly through various instant retailers within their communities

messaging tools

Similar to ChiliBeli, Super also started

Model Marketplace model connecting Super’s main service, SuperAgen – Group-buying platform based in Indonesia

farmers with agents, with agents then Shahria compliant, profits from (also recently launched a reseller platform)

as an agent model for FMCG and

sharing it with their network and reseller, order management packaged foods products for Mom &

earning a comission Pops. However, they now have an

Category Fresh produce FMCG, packaged foods Fashion, Lifestyle element of group buying.

Revenue Model . 3.5% gross margin, -6.8% CM2 margin. % GMV take rate % GMV take rate

GMV take rate

Mucho has two separate platforms –

Traction US$600K Feb GMV, Undisclosed Undisclosed one for group-buying (Mucho) and the

other for agent/reseller (Milliku).

Mucho’s group-buying platform is for

fashion items, whilst Milikku is for

FMCG/Sembako items. This is quite

opposite from both Meesho and PDD.

Funding Seed (Undisclosed) Undisclosed – Y-Comb, Insignia, Alpha Seed (US$3M) – Qiming Venture Partners

Series A (US$10M) – Lightspeed, JWC, B-Cap Partner’s, Arrive

Kenesys, Golden Gate, Surge

33Valuation 34

The Valuation Comps for Social Commerce platforms are are 0.6x – 1.6x

EV/GMV and 7x – 25x for EV/Rev

Model Monetization

Agent/Reseller Model Group-Buying Model

10.0 Agent-Reseller % GMV take

14.0 13.3

7.7

Model rate/commission

12.0 8.0 % Agent fee

10.0

6.0

8.0

6.0 4.0 Group-Buying % GMV take rate

Model Advertising

4.0 2.0

0.6 Merchant Services

2.0 0.9

0.0

0.0

EV/GMV EV/Rev

EV/GMV EV/Rev All Social % GMV take rate

Commerce Advertising

Models Merchant Services

India – All Social Commerce Models China – Social Commerce Models

8.0 7.4

30.0

25.1 7.0

25.0

6.0

20.0 5.0

15.0 4.0

3.0

10.0

2.0

5.0 1.6 0.7

1.0

- 0.0

EV/GMV EV/Rev EV/GMV EV/Rev

Confidential and proprietary to CV 35Is the opportunity now?

36The long-term goal for Social Commerce platforms would be to aggregate

demand, optimize operations and establish a powerful supply side

Lower number of SKUs that are Social commerce is highly

selling at a higher frequency allows operational, especially in

for platform to negotiate better logistics and marketing.

prices, thus reducing costs. Key is to Improving efficiencies

dominate a category of SKUs. operationally is necessary to

continuously improve

Aggregating demand allows for economics.

platform to optimize operations and Large network of

agents or White-labelling popular SKUs

logistics. Potential to utilize based on customer data is also

agents/community leaders/mitras to users/eyeballs that

allows for an option for future, through

carry out last-mile delivery, or build manufacturing or repackaging,

last-mile logistics hubs around these monetization via

advertising or as it increases margins up to

communities. 30%, depending on SKU.

premium listing

Supply side access has to be strong,

through bringing offline businesses Agent and merchant

online, or acquiring supply that have stickiness is essential, so

yet to succeed in current platforms, add on services such as

to help them gain significant marketing, analytics and

customer access, and in return also micro-financing can

obtain products at better prices. help with retention.

37Social Commerce in Indonesia presents an interesting opportunity for

investment, although there are risks to consider such as competition and

current logistics infrastructure

Score (1-10) Description

Funding Requirements 7 Funding requirements are high due to the need to build scale, supply defensibilities and compete

with eCommerce giants

Fundraising Landscape 9 Space has seen traction from notable investors due to the tier 2/3 opportunity, especially in the

reseller space

Competitive Landscape 4 Landscape is crowded with multiple players, however no clear winner yet

Market Potential 10 eCommerce will hit US$200B by 2025, with opportunities for social to drive that growth

Consumer Behavior 9 With more users spending time online, social commerce is well positioned to tap into social

behavior and eCommerce activity

Supply Chain 6 Need to achieve scale first to build supply chain, but more brands are keen to build stronger

online presence

Logistics Infrastructure 4 Not quite there yet, especially in remote areas. Logistics costs will continue to be a challenge

Tech Infrastructure 8 Simple and straightforward

Growth Vs. Risk 5 Potential to scale with funding discounts and marketing, but competition is high risk

Regulatory Environment 10 Only concerns will be around MLM / Pyramid scheme

Note that each of attribute above is weighted equally, with 0 being most unfriendly factor and 10 being most friendly factor.

Market Timing Score 71/100 Overall timing score is 71, indicating that there is strong opportunity but also risks

38So why is Social Commerce interesting NOW?

Is it because there is more

opportunities in tier 2-4 Is It because social Is it because social commerce platforms

cities, and the current commerce models has had high interest form investors

eCommerce solutions are have been successful worldwide, and would be able to

not tailored to that? in other countries? continue to raise?

Is it Indonesia’s eCommerce

space is massive but still have

untapped potential that there is Is it because there a valid pain

still much space for Social point that social commerce

Commerce to grow, and scale Is it because social commerce platforms effectively solve

faster than traditional platforms have the potential to better than other eCommerce

eCommerce platforms? scale faster through their reach platforms? I.e. trust gap?

than traditional eCommerce

platforms?

39Impact of COVID-19

40Impact of Co-Vid 19

Strengths Weaknesses

• Selling via online network, social media • Offline agent recruitment will be challenging, so

(Whatsapp, Line, etc) reduces the need for marketing via online channels is essential

offline presence. Both agent and team • Increase competition from eCommerce players with

purchase model strongly depends on online funds to burn via discounts, marketing and logistics,

sharing. as well as stronger merchant base

• Can scale faster than traditional commerce, as • Supply chain disruptions due to factory closures and

people spending more time online and on import challenges

social media • Fall in demand for non-essential items

Opportunities

• Doubling down on essential/FMCG/sembako items, as well as medical supplies

• Renegotiating contracts merchants, retailers, factories and distributors

• Potential to onboard more businesses, as SMEs are now looking to build stronger presence online (also

supported by the government)

• Opportunity to scale and capture eyeballs, through gamification and social media sharing

41Michael Soerijadji | Managing Partner Adrian Li | Managing Partner

michael@acv.vc adrian@acv.vc

Confidential and proprietary to ACVYou can also read