Shifting sands: trade partner patterns since 2018 - ECOSCOPE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Shifting sands: trade partner patterns since 2018 by Seung-Hee Koh, Catherine MacLeod and Elena Rusticelli Global trade policy is undergoing a sea-change. The share of global merchandise imports subject to trade restrictions has risen particularly rapidly since 2018, initially due to a sharp increase in tariffs on bilateral trade between the United States and China. Since then, trade policy choices have steadily become more harmful to global trade in goods (Figure 1, Panel A). Trade policy uncertainty has also increased, alongside policy discussions about the re-location of value chains and ongoing changes in the design of national industrial policies. The latest OECD Economic Outlook (OECD, 2023) analyses trends in imports of manufactured goods across major OECD economies to understand what impact this has had on trade patterns. So far, the increasing use of trade policies has coincided with a period of subdued world trade growth, but has not reduced global merchandise trade intensity (the ratio of trade in manufactures and commodities to GDP in volume terms). Nonetheless, since the global financial crisis, global trade intensity has risen only marginally, following a period of very sharp rises in the 1990s and early 2000s. The COVID crisis saw a shallower decline and faster rebound in merchandise trade intensity than the global financial crisis (Figure 1, Panel B). In 2022, global trade in goods was 22% of global GDP in volume terms, marginally higher than 2018. The recent resilience of trade in volume terms may be linked to the huge increase in demand for goods during the COVID pandemic, as well as strong policy support during the pandemic and energy crises. Merchandise trade as a share of GDP generally rose in OECD countries between 2018 and 2022,

including in Europe and Japan, offsetting a decline in Chinese

merchandise trade intensity. However, merchandise trade

intensity was relatively unchanged in the United States, where

weak export growth offset a rise in import intensity.

Underneath the general rise in the value and volume of trade,

imported manufactured goods at a country-level reveal

important and differing shifts in the composition of

manufactured goods imports since 2018 in the major economies

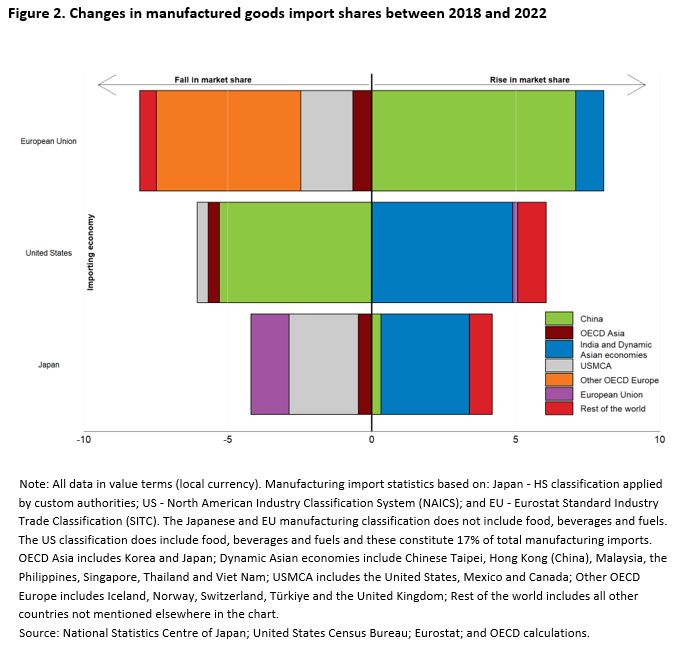

(Figure 2). A particular issue of policy interest is the

evolution of trade with geographically distant partners for

key inputs (far-shoring) compared to trade with geographically

closer trade partners (near-shoring).

Shifting far-shoring: In the US, there have been sharp

declines in China’s share of manufactured imports since

2018 – which have typically coincided with rising import

shares from dynamic Asian economies. This includes goods

where the 2018 tariffs are still applied. Evidence of

near-shoring is limited, with Mexico and Canada’s share

of imports rarely rising in the same categories where

China’s share has fallen.

Expanding far-shoring: in the EU, China’s weight in

manufactured imports has continued to grow steadily. In

contrast to the US, this has been alongside rising

import shares for dynamic Asian economies. As for the

US, there is limited evidence of near-shoring: the share

of imports from other OECD countries in Europe has

fallen, largely driven by changes in import shares from

the United Kingdom.

Changes at the margin: In Japan, the shifts in import

shares have been much smaller than in the US or Europe.

Its trade with the wider Asian region has increased

steadily, although increases have been larger for

dynamic Asia than China. As in Europe, this has been

accompanied by a decline in the share of imports from

other advanced economies.

So far, these shifts in trade patterns have occurred whilst

aggregate trade has continued to expand broadly in line with

global activity. However, in a global economy with slowing

long-term growth prospects the economic costs of more harmful

trade policies may become more evident over time.

References: OECD (2023), OECD Economic Outlook, Volume 2023 Issue 1, OECD Publishing, Paris, https://doi.org/10.1787/ce188438-en.

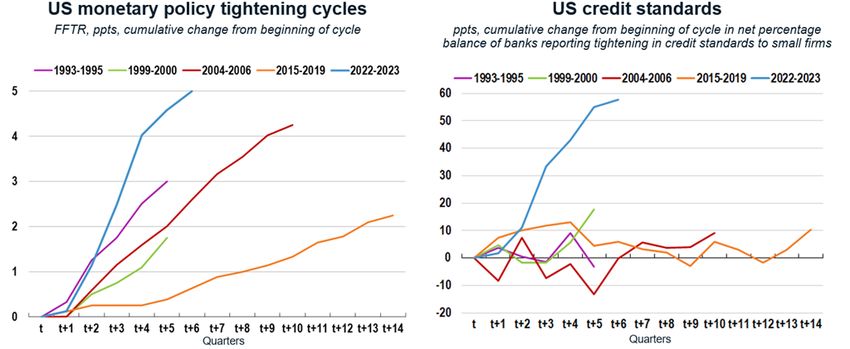

Monetary policy and credit standards: this time it’s different by Almira Enders and Dennis Dlugosch, OECD Economics Department The current monetary policy tightening cycle observed in many countries stands out for several reasons. In particular, it is rapid, globally synchronised and accompanied by an equally rapid tightening of credit standards (OECD, 2022). Since February 2022, the US Federal Funds Target Rate has risen by 500 basis points (Figure 1 Panel A). No tightening cycle since the mid-1980s has seen such a big increase in policy rates in such a short period of time. Central banks in other main advanced economies have acted comparably aggressively in their fight against high inflation. The European Central Bank, for example, has raised its policy rates by 400 basis points since June 2022. The increase of policy rates has been quickly transmitted to money market and bank lending rates over the past year (OECD, 2023). Figure 1. Policy rates and credit standards have tightened in sync

Note: Starting on Dec 16, 2008, the fed funds target rate contains the average of the upper and lower limits of the target range of the fed funds rate. Prior to Dec 16, 2008 the fed funds target rate was a fixed rate. Credit standards refer to net percentage of US domestic banks reporting tightening of standards for commercial and industrial loans to small firms (in percent, not seasonally adjusted). Source: Federal Reserve Board; OECD calculations. While the tightening of credit conditions is a standard transmission channel of monetary policy, the synchronised increase in interest rates and tightening of credit standards is eye-catching in comparison to previous tightening cycles (Figure 1 Panel B).[1] Credit standards are non-price measures that determine access to credit, such as collateral requirements, employment status or income situation. Credit standards can restrict access to credit in addition to sheer the changes in lending rates which affect the supply and demand for credit through their impact on cost of debt and banks’ and borrowers’ balance sheets. The net share of banks reporting tightened credit standards in the current monetary policy tightening cycle has increased, in step with the increase in policy rates. In March and April 2023, the net share of banks tightening lending standards to small firms over the previous three months reached 47% in the

US.[2] While this share is still below the peaks reached during the Covid-19 crisis (70%) and the Global Financial Crisis (about 75%), the current rapid tightening of credit standards is similar to the dynamics seen during the last two severe economic downturns. In the euro area, as well, the current monetary policy tightening was accompanied by the tightening of credit standards, although less rapidly than in the US. The corresponding net share of banks tightening credit standards in the euro area increased to about 24% recently, only a fraction below the last peak reached during the euro area sovereign debt crisis at 28%. In the UK, the share of lenders reporting worsened availability of unsecured credit to households and small businesses widened rapidly to almost 40%, approaching the peak reached during the Covid-19 crisis of about 63%.[3] Bank lending surveys also provide information on the reasons behind changes in lending standards. In the US, most banks have reported tighter lending standards because of a less favourable or more uncertain economic outlook and a reduced tolerance for risk. In the euro area, we observe similar patterns, as higher risk perception and a lower tolerance for risk of banks were the main reasons behind the recent tightening of credit standards. Focussing on small firms and households is interesting because they are usually more exposed to tighter credit standards given that they rely more on bank loans as external source of finance. In the US and the euro area, the evolution of lending standards to small firms appears representative for the overall corporate sector. While in the US more banks have also reported tighter standards for credit card loans; in the euro area, the net share of banks reporting tighter credit standards for households, which includes but is not limited to credit card loans, has receded from their recent peaks over the past two quarters. In the UK, credit availability remains favourable for corporate sector and for secured lending for

households. In the past, banks rapidly tightened credit standards during severe economic downturns, mainly due to the expected deterioration of borrower’s balance sheets (Ciccarelli et al., 2015). In contrast to the current juncture, at that time monetary policy accommodated these economic downturns, by lowering interest rates in response to a slump in aggregate demand and declining inflation. The combined tightening of policy rates and credit standards has several implications for policy makers. First, it adds to the uncertainty over the impact of monetary policy on the real economy and thus makes the transmission channel for monetary policy difficult to gauge. Central banks will need to maintain restrictive monetary policy to curb inflation durably. However, monitoring financial stability and clear communication will be needed to minimise uncertainty about apparent conflicts between the pursuit of price stability and financial stability mandates. Finally, keeping an eye on competition in financial services will be critical to ensure that small business and households continue to benefit from a vibrant financial sector. References Ciccarelli, M., A. Maddaloni and J.-L. Peydró (2015),”Trusting the bankers: A new look at the credit channel of monetary policy”, Review of Economic Dynamics, Vol. 18 (4). OECD (2022), OECD Economic Outlook, Volume 2022 Issue 2, OECD Publishing, Paris, https://doi.org/10.1787/16097408. OECD (2023), OECD Economic Outlook, Volume 2023 Issue 1, OECD Publishing, Paris, https://doi.org/10.1787/ce188438-en. Footnotes

[1] The figure shows the synchronized tightening of policy

rates and credit standards in the US. The euro area bank

lending survey was launched in 2003. This limits a comparison

over several monetary policy tightening cycles.

[2] Based on a survey of lending practices of major US banks

conducted by the Federal Reserve Board System. The number

refers to the net percentage of banks that have tightened

lending standards over the previous three months. The net

percentage is equal to the difference between the sum of banks

answering “tightened considerably” and “tightened somewhat”

and the sum of banks answering “eased somewhat” and “eased

considerably” in percentage of the total number of banks.

[3] Based on the Bank Lending Survey conducted by the

Eurosystem of Central Banks for the euro area and based on the

Credit Conditions Survey conducted by the Bank of England for

the UK.

Do central bank losses

matter?

By Nobukazu Ono and Álvaro Pina, OECD Economics Department

Af

te

r

re

co

rd

in

g si ze ab le ga in s fr om qu an ti ta ti ve ea si ng (Q E) ov er mo st of th e pa st de ca de , se ve ra

l ce nt ra l ba nk s ha ve re ce nt ly re po rt ed fi na nc ia l lo ss es . Fu rt he r lo ss es ar e li

ke ly in th e co mi ng ye ar s. As di sc us se d in th e la te st OE CD Ec on om ic Ou tl oo k (O EC D, 20

23 ), th es e lo ss es ha ve lo ng be en an ti ci pa te d, as pa st ga in s an d cu rr en t lo ss es ar e

tw o si de s of th e sa me co in . Th is is al so th e ca se fo r th e ad ve rs e im pa ct of lo ss es

on th e pu bl ic fi na nc es , wh ic h co me s af te r se ve ra l ye ar s of si gn if ic an t ce nt ra

l ba nk re mi tt an ce s to Tr ea su ri es . No ne th el es s, lo ss es an d th e po te nt ia l ne ed fo

r re ca pi ta li sa ti on fr om th e go ve rn me nt ca n st il l un de rm in e th e cr ed ib il it y an

d pe rc ei ve d in de pe nd en ce of ce nt ra l ba nk s. Th is ca ll s fo r tr an sp ar en cy an d cl ea

r

co

mm

un

ic

at

io

n

in

th

e

pr

es

en

ta

ti

on

of

lo

ss

es

.

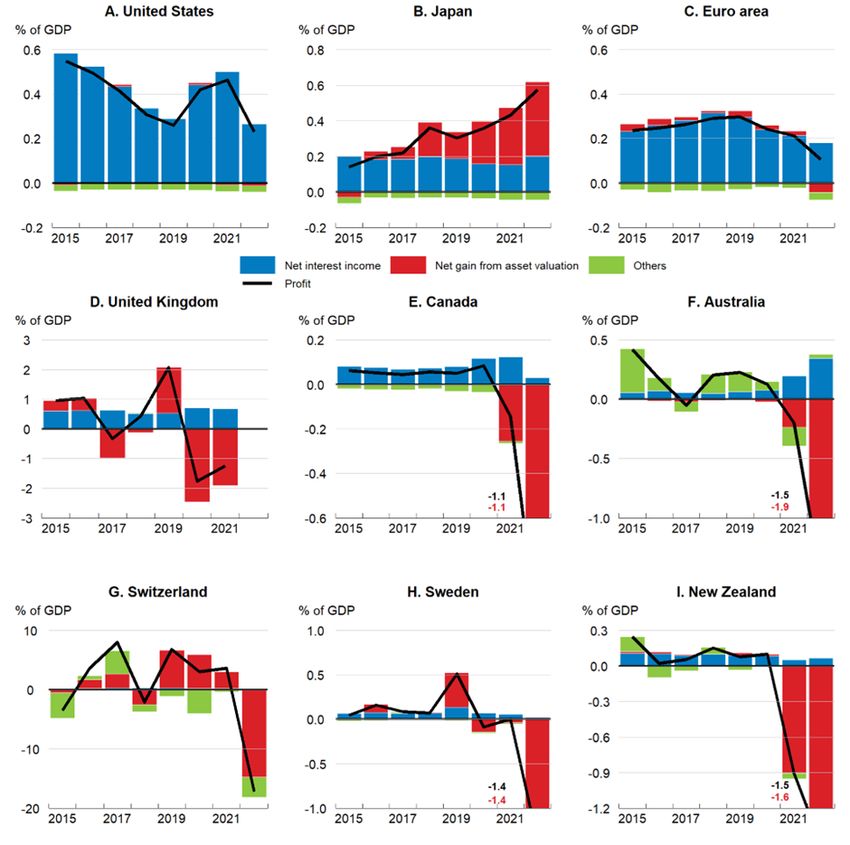

Why are central banks making losses?

Losses largely reflect the large balance sheets built up

during an extended period of QE and the effects of the recent

rises in policy interest rates. QE created a sizeable mismatch

in the maturity of central bank assets and liabilities. On the

liability side, central bank reserves (mainly commercial bank

deposits) rose sharply. The remuneration on these is closely

linked to policy interest rates, and has thus risen rapidly,

to the benefit of commercial banks. In contrast, on the asset

side, QE purchases were mostly long-term fixed-rate bonds that

generate a relatively stable stream of income. When policy

interest rates were at or close to the zero lower bound, the

balance of these two sets of payments generated gains forcentral banks. Even as policy rates were raised through 2022, their impact on whole-year net interest income was still relatively mild (Figure 1), especially where most rate increases took place towards the end of the year, as in the euro area. However, larger impacts are likely in 2023 and 2024 (Anderson et al., 2022; De Nederlandsche Bank, 2022). Higher interest rates also reduce the market value of securities. Valuation losses may thus arise, though this depends on the accounting frameworks and asset sales decisions of central banks. For instance, the Federal Reserve and the Bank of Japan account for securities held for monetary policy purposes using amortised cost. This means that valuation changes do not affect profits unless securities are sold, which has not been the case so far. Eurosystem accounting guidelines, also followed by Sweden, allow central banks to value securities held for monetary policy purposes at either amortised cost or the current market price. While euro area national central banks have generally opted to use amortised cost, the Riksbank has adopted market pricing, making a significant loss apparent in 2022. Mark-to-market accounting brings forward loss recognition, as also illustrated by Australia, Canada, New Zealand, Switzerland and the United Kingdom. In Switzerland, the central bank loss was unusually large in 2022, at 17 per cent of GDP, but these losses stemmed largely from changes in the domestic currency value of foreign exchange reserves, including foreign securities. Do losses hamper fiscal or monetary policy? Central bank losses affect the public finances by reducing or ending central bank payments to the Treasury in the form of income taxes or remittances. Moreover, reverse cash flows (i.e., payments from the Treasury) may occur if central banks are entitled to be compensated by the government for certain losses, such as QE-related losses. For instance, in the United Kingdom, the Bank of England Asset Purchase Facility (APF), through which QE asset purchases were conducted, is fully

indemnified by the Treasury. The annual impact on the general government fiscal balance should in general be modest: over 2015-21, revenues from the central banks considered in Figure 1 rarely exceeded, and were often far below, 0.5% of GDP per year. However, even if small, the negative effect on fiscal balances could be protracted, as losses may persist for several years. Even after the central bank returns to profit, some time may elapse before remittances to the Treasury resume. Central bank losses are not an indication of a policy error and need not hamper the effectiveness of monetary and financial policies. The policy mandates of central banks include price stability and financial stability, but not profit maximisation. Their current losses, as well as their earlier gains from QE, are a by-product of policy actions designed to help achieve their mandates. Moreover, central banks are not subject to capital adequacy requirements or bankruptcy procedures and can operate effectively even with negative equity, as the central banks of Chile, the Czech Republic, Israel and Mexico have done over several years (Bell et al., 2023). However, losses or negative equity can pose communication challenges. For instance, some policy decisions, such as retaining rather than selling government bonds, could be misinterpreted as being motivated by a desire to contain losses rather than as actions to pursue specific policy mandates. This would reduce central bank credibility. Likewise, financial flows from government, including actions to strengthen central bank capital positions, could be misperceived as being inconsistent with central bank independence. This underscores the importance of clear communication about the reasons for losses and of a transparent framework for financial flows between the central bank and the government.

Figure 1: Several central banks now report negative profits Note: Accounting approaches and financial years differ across countries and data should therefore be compared with caution. ‘Net gain from asset valuation’ includes realised gains/losses and, in some countries, unrealised ones. For the euro area, the chart shows the consolidated result of national central banks. The euro area figure for 2022 is based on the 17 member banks who had published results by 29 June 2023. For the United Kingdom, the chart shows the consolidated result of the Bank of England and the Asset Purchase Facility. See Box 1.3 in OECD (2023) for further details.

Source: Board of Governors of the Federal Reserve System; Bank of Japan; national central banks in the euro area; Bank of England; Bank of Canada; Reserve Bank of Australia; Swiss National Bank; Sveriges Riksbank; Reserve Bank of New Zealand; OECD Quarterly National Accounts database; and OECD calculations. References Anderson, A., P. Marks, D. Na, B. Schlusche, and Z. Senyuz (2022), “An Analysis of the Interest Rate Risk of the Federal Reserve’s Balance Sheet, Part 2: Projections under Alternative Interest Rate Paths,” FEDS Notes, Washington; Board of Governors of the Federal Reserve System, 15 July, https://doi.org/10.17016/2380-7172.3174. Bell, S., M. Chui, T. Gomes, P. Moser-Boehm, and A. P. Tejada (2023), “Why are Central Banks Reporting Losses? Does it Matter?,” BIS Bulletin No 68, February, https://www.bis.org/publ/bisbull68.pdf. De Nederlandsche Bank (2022), “Letter regarding DNB’s capital position – September 2022,” 9 September, https://www.dnb.nl/media/p4igu5fc/letter-regarding-dnb-s-capit al-position-september-2022.pdf. OECD (2023), OECD Economic Outlook, Volume 2023 Issue 1, OECD Publishing, Paris, https://doi.org/10.1787/ce188438-en. Monetary policy pass-through

to bank credit conditions:

progressing fast

Ane Kathrine Christensen and Lucia Quaglietti, OECD Economics

Department

Po

li

cy

in

te

re

st

ra

te

s

ha

ve

ri

se

n

at

an

un

us

ua

ll

y

ra

pi

d

pa

ce

si

nce th e en d of 20 21 in ma ny co un tr ie s. Su ch po li cy ch an ge s af fe ct ec on om ic ac ti vi ty th

ro ug h ma ny di ff er en t ch an ne ls . On e ke y ch an ne l is th e sp ee d an d ex te nt to wh ic

h ch an ge s in po li cy ra te s ar e pa ss ed th ro ug h to fi na nc in g co nd it io ns an d cr ed it

gr ow th , an d th us to pr iv at e co ns um pt io n an d in ve st me nt (B er na nk e an d Ge rt le r

19 95 ; Mi sh ki n 19 96 ). A na ly si s in th e Ju ne 20 23 OE CD Ec on om ic Ou tl oo k, su gg es ts th

at ch an ge s in po li cy ra te s in OE CD ad va nc ed ec on om ie s ar e be in g qu ic kl y re fl ec te

d in ba nk cr ed it co nd it io ns fa ce d by ho us eh ol ds an d fi rm s, wi th tr an sm is si on oc cu rr

in

g

at

a

br

oa

dl

y

si

mi

la

r

pa

ce

to

pa

st

ti

gh

te

ni

ng

cy

cl

es

.

One indicator is the extent to which increases in policy rates

have been transmitted into the interest rates on new bank

loans for households and firms. The evidence suggests that

transmission in the current cycle is similar to that in past

tightening cycles on average, but with significant variation

across countries (Figure 1, Panels A and B). In particular,

there have been strong increases in the cost of new bank loans

for non-financial corporations, where bank lending rates have

on average increased almost one‑to‑one with policy rates. The

largest relative increases in new bank lending rates have beenobserved in Australia, Canada, New Zealand, Norway and Sweden, in some cases reflecting an earlier start to policy tightening. In the euro area, bank lending rates charged on short-term loans to non-financial corporations have generally increased faster than those on loans with longer maturities and lending rates on consumer loans to households have risen less than rates on loans for house purchases. Figure 1: Bank credit is slowing down and swiftly becoming more expensive Note: For the current tightening cycle, changes in policy rates, new lending rates and real credit growth are computed between the date of the first policy increase in each country and March 2023. Similarly, changes in bank lending rates across past tightening cycles are computed since the first rate increase and over a period matching the one elapsed since the first increase in the current cycle. Changes across past tightening cycles are computed as simple averages of individual country tightening cycles since 2000. “Average” is computed as a simple average across countries. Bank lending

rates and credit growth to households are for house purchases. Real credit growth is obtained by deflating nominal credit growth by national consumer prices. Source: Central bank statistics; and OECD calculations. Banks generally base the lending rates they charge to firms and households on their own funding costs, plus a mark-up. Rising policy rates have been quickly transmitted to interbank lending rates, but transmission to deposit rates has been sometimes slower. However, deposit rates have started to rise more rapidly recently, with banks trying to counteract tighter liquidity conditions and an acceleration in deposit outflows by offering higher rates to their customers. Fast-rising bank lending rates have been associated with a slowdown in the pace of real credit growth (Figure 1, Panels C and D). On average, the slowdown in real credit growth during the current tightening cycle has been somewhat larger for households than for companies, though credit to firms has contracted sharply in a number of countries in the euro area and in the United Kingdom, while it has remained comparatively resilient in the United States and Canada. In the majority of the countries considered, credit growth has been weaker than at similar points in previous tightening cycles, and also lower than on average over 2000-19, particularly for households. Monetary policy changes may also affect the willingness of banks to make credit available to potential borrowers. Bank lending surveys suggest that slowing credit growth and higher lending rates observed in the major advanced economies reflect a combination of tighter credit standards and falling credit demand (Figure 2). Credit standards have often tightened substantially in recent quarters, especially for mortgage lending in the euro area and for lending to non-financial corporations in the United States. Surveys point to a sharp

decline in credit demand as well, especially for house purchase in the euro area and in the United Kingdom. In the euro area, the decline in credit demand for house purchases is similar to the fall seen during the global financial crisis. Japan is an exception, with credit standards and demand being little changed due to the continued accommodative monetary policy stance. Figure 2: Credit standards have tightened and demand has declined sharply Note: Net percentages are defined as the difference between the sum of the share of banks reporting a tightening in credit standards/rising credit demand and the sum of the share of banks reporting a loosening of credit standards/falling credit demand. Positive (negative) balances indicate tighter (easier) credit standards and rising (falling) credit demand. For the United Kingdom, credit standards are proxied by inverted loans approved. For the United States, the United Kingdom and Japan, credit standards to non-financial corporations are for large firms Source: Central bank statistics; and OECD calculations. The pace of policy rate increases has now begun to slow in many countries, but bank credit conditions could tighten further in the coming quarters, with banks continuing to pass through higher funding costs to households and corporates. As a result, the full impact of policy tightening on activity is

likely to appear with a lag over the course of 2023 and early

2024.

References

Bernanke, B., and M. Gertler (1995). “Inside the Black Box:

The Credit Channel of Monetary Policy Transmission.” Journal

of Economic Perspectives, Vol. 9.

Mishkin F. (1996), “The Channels of Monetary Transmission:

Lessons for Monetary Policy,” NBER Working Papers 5464.

OECD (2023), OECD Economic Outlook, Volume 2023 Issue 1, OECD

Publishing, Paris.

Employment in Sweden: aiming

high

by Hyunjeong Hwang, OECD Economics Department

Sw

ed

en

ha

s

a

ve

ry

hi

gh

la

bo

urfo rc e pa rt ic ip at io n ra te an d on e of th e hi gh es t em pl oy me nt ra te s in th e OE CD ,

bu t ca nn ot af fo rd to be co mp la ce nt . Ma in ta in in g hi gh em pl oy me nt is a pr er eq ui si te

fo r th e su st ai na bi li ty of th e Sw ed is h we lf ar e st at e an d to co un te r th e ag ei ng

- re la te d co nt ra ct io n of th e la bo ur fo rc e an d it s ne ga ti ve fi sc al im pa ct s. Th e

20 23 OE CD Ec on om ic Su rv ey of Sw ed en de lv es in to so me ch al le ng es ho ld in g ba ck la bo ur su

pp ly an d pr op os es me as ur es to ma ke th e Sw ed is h la bo ur ma rk et st ro ng er , mo re in cl us

iv

e,

an

d

co

nd

uc

iv

e

to

su

st

ai

ne

d

ec

on

om

ic

gr

ow

th

.

Long-term unemployment, notably among the foreign-born,

remains a significant challenge. With lower educational

attainment and lower Swedish language skills than natives,

foreign-born people may struggle to get a job in a labour

market characterised by a compressed wage distribution that

demands high skills and productivity. Additionally, foreign-

born women often face strong gender and family norms. Re-

skilling and activation policies are key for these groups. A

recent reform of the Public Employment Service, introducing a

purchaser-provider model with outcome-based payments for

employment services could help, but needs to be carefully

monitored and calibrated to align providers’ incentives with

the objectives of the reform and to secure sufficientcompetition. Carefully reviewing social assistance with the aim to strengthen work incentives while ensuring decent living standards for people in need could also help. Taxes on work are high, particularly among above-average income earners in Sweden (Figure 1). The top personal income tax rate is among the highest in the OECD and it applies from a low threshold. As a result, a relatively large share of taxpayers faces the top marginal tax rate. Meanwhile, tax rates on dividends and capital gains are relatively low. The large difference between taxes on labour income and capital income creates incentives for high-wage earners to reclassify their income as capital income in order to minimise their tax obligations. Furthermore, housing taxation is both low and regressive. Shifting taxation away from labour and towards property and capital income would thus help create a more balanced and equitable tax structure, promoting labour supply and inclusive growth while preserving fiscal sustainability. Lengthening working lives as life expectancy increases is essential to strengthen public finances and to ensure sufficient pension income. Reforms in the 1990s made Sweden’s pension system the envy of countries around the world, with in-built sustainability and incentives to lengthen working lives, and many policies have been put in place since to

extend working lives. However, recent reforms to boost basic pensions and to introduce a new tax-funded income pension supplement go in the direction of reducing incentives to remain in work for many older workers and weaken the long-term sustainability of the system. The stated purpose of these changes was “to ensure a reasonable standard of living for pensioners who receive a low level of earnings-related pensions”. However, on average, Swedish pensioners are relatively well-off compared internationally and compared to younger generations in Sweden. Sweden should therefore change direction by holding back the uprating of tax-funded pensions for some time to come. Relaxing strict rent controls, which would improve labour mobility and increase the supply of rental dwellings, should be considered. Waiting times for rental housing can stretch from years to decades in major cities in Sweden, perpetuating the scarcity of rental options. This pushes those with limited queuing time and limited means to buy housing, particularly youth and immigrants, into overcrowded housing, sublet or black markets with significantly higher rents. Greater flexibility in rental housing would facilitate the matching of skills with job vacancies and boost productivity by more efficiently allocating talent to where it is most needed. Further reading: OECD Economic Survey of Sweden (2023), OECD Economic Surveys: Sweden 2023, OECD Publishing, Paris. How Climate Policies Shape

Borrowing Costs and

Investment through the

Banking Channel

More stringent climate policies means that firms’

environmental performance affects their costs of debt as

(sophisticated) investors price transition risks

The OECD Energy Support

Measures Tracker: Looking

back to move ahead

By Cassandra Castle, Assia Elgouacem, Giuliana Sarcina, Enes

Sunel, and Jonas Teusch

In

th

e

pa

st

fe

w

ye

ar

s,

th

e

gl

obal ec on om y ha s ex pe ri en ce d tw o ma jo r cr is es : th e CO VI D- 19 pa nd em ic an d Ru ss ia

’s wa r of ag gr es si on ag ai ns t Uk ra in e. Th e re co ve ry fr om th e pa nd em ic an d th e wa r

ha ve bo th am pl if ie d te ns io ns in th e en er gy se ct or an d pr ov ok ed a su rg e in en er gy pr

ic

es

.

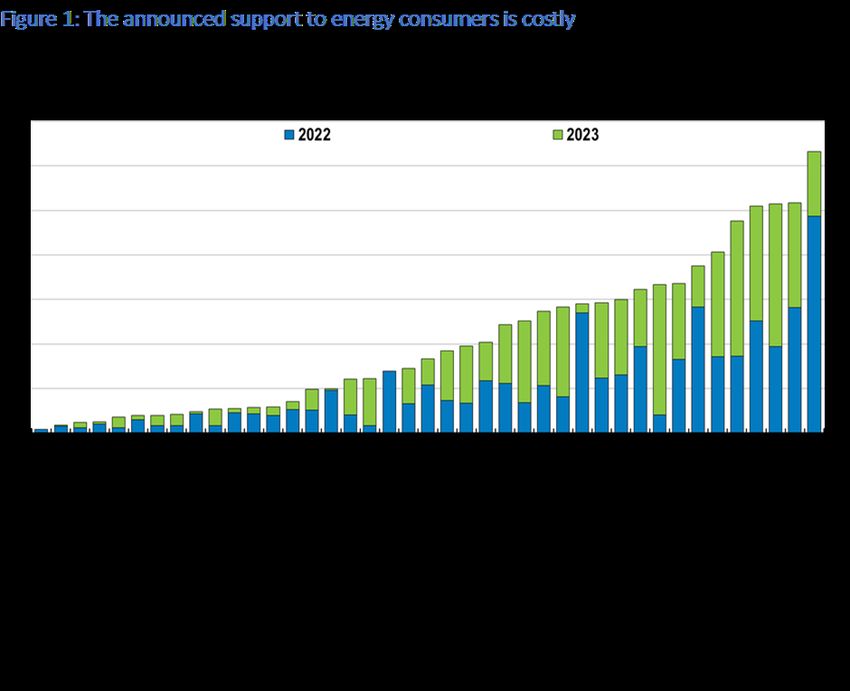

The fiscal response to the energy crisis has been large,

especially in Europe

The OECD Energy Support Measures Tracker, released on 6 June

2023, shows that in 2022, support measures in response to

higher energy prices had a gross fiscal cost of 0.7% of GDP in

the median OECD economy, rising to over 2.5% of GDP in some

European countries (Figure 1). By way of comparison, these

costs exceed what the median OECD country spends on

unemployment benefits and are about half of the expenditure on

family and child benefits. Comparable levels of fiscal support

are foreseen for 2023 in the OECD as a whole. However, the

actual cost of support will heavily depend on the evolution of

energy prices.

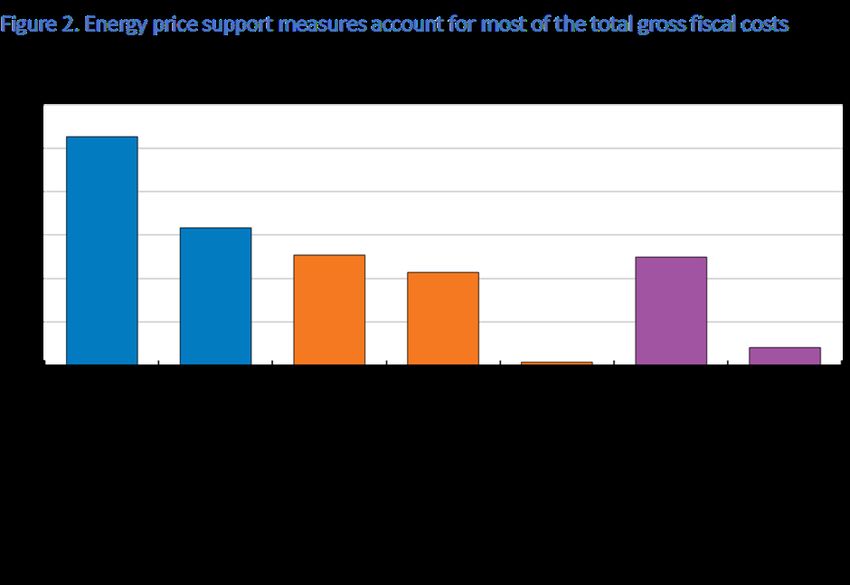

Click for Chart dataThe OECD Energy Support Measures Tracker provides comprehensive data and information on energy-crisis related fiscal support measures Documenting the measures governments have implemented to face the energy price shock and being able to compare them across countries, remains critical to improving support policies and building resilience against future crises. The Tracker systematically catalogues support measures in place from February 2021 to May 2023 in 41 countries – 35 OECD countries and 6 non-OECD economies (Brazil, Bulgaria, Croatia, India, Romania and South Africa).[1] The data have been collected and processed by OECD country, fiscal and energy policy experts and validated by national administrations. The new dataset provides granular information to comprehensively characterise individual support measures. These include start and end dates, gross fiscal costs, type of support and delivery mechanism, main beneficiaries of the measures (indicating whether vulnerable households or firms from specific sectors are targeted, and, where applicable, summary information on the differentiation of support between beneficiaries) and the impacted energy carriers (such as diesel, gasoline, electricity, natural gas). The sheer number and diversity of the measures makes classification challenging. The Tracker classifies more than 550 support measures into two main categories: (1) price measures (e.g. reduced energy taxes and energy price caps), estimated to cost USD 422 billion in 2022-23; and (2) income measures (e.g. transfers and tax credits to consumers), estimated to total USD 383 billion in 2022-23. Within income measures, a distinction is made between measures that reduce the average price of energy in consumers’ energy bills and measures that are unrelated to the level of energy consumption (Figure 2).

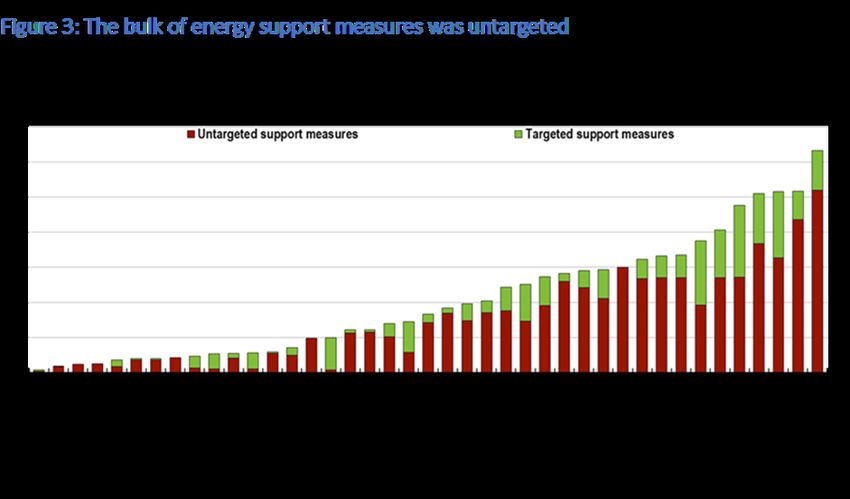

Click for Chart data The measures – which were implemented swiftly amidst uncertainty, political economy constraints, and a focus on administrative simplicity – affect the behaviour of firms and people in different and significant ways, and may contribute to or detract from important longer-term policy objectives. Income support can maintain incentives to save energy whereas price measures weaken them, propping up demand for fossil fuels and effectively acting as a negative carbon price. Among income measures, those that are unrelated to the level of energy consumption tend better to preserve incentives for energy efficiency improvements than those that reduce the average price in the energy bill paid by consumers. Measures were rarely targeted and increased the incentive to consume fossil fuels Untargeted support measures make up the majority of the estimated total cost of support in 2022-23 (Figure 3). Among these, energy price support measures account for over 50% of total spending and carry substantial non-fiscal implications.

While price support measures are straightforward to design and often politically popular, they weaken incentives to save energy and are rarely targeted (over 92% of energy price support measures are untargeted), meaning that they tend to disproportionately support better-off households. Click for Chart data A clear taxonomy of measures and data can enable the design of better energy support policieswhen they are needed Energy prices are receding, but possible renewed tensions in energy markets due to geopolitical developments and bottlenecks along the energy transition may result in higher energy price volatility in the future. Preparing government policy for possible new energy price spikes requires data and information on how support measures affect the behaviour of households and firms, their impact on public finances and their unintended consequences. The OECD Tracker is a resource for policymakers to do just that. More information OECD (2023), OECD Energy Support Measures Tracker, OECD database available at:

http://www.oecd.org/economy/oecd-energy-support-measures-track er/OECD_Energy_Support_Measures_Tracker.xlsx OECD (2023), “Aiming Better: Government Support for Households and Firms During the Energy Crisis”, OECD Economic Policy Papers No. 32, OECD Publishing: Paris, https://doi.org/10.1787/839e3ae1-en [1] The government of Iceland has not taken any energy support measures. The Tracker also includes information on another five countries, for which it was either not possible to quantify the gross fiscal cost of the energy support measures (Argentina, China, Hungary and Indonesia) or these were deemed to have no impact on budget deficits, as is the case of measures providing credit and equity support (Switzerland). América Latina: Estabilidad fiscal y equidad, un camino compartido hacia el progreso. Jens Arnold, Aida Caldera, Priscilla Fialho, Paula Garda, Alberto González Pandiella, Michael Koelle, Alessandro Maravalle, Adolfo Rodriguez-Vargas and Elena Vidal, Departamento de Economía, OCDE Después de dos años con altos crecimientos, mejores de lo esperado, América Latina está volviendo a la senda de bajo crecimiento que tenía antes de la COVID-19. Para 2023 se espera una fuerte ralentización económica, mayor que en el resto del mundo. Esto se debe a una demanda externa que pierde

dinamismo y un consumo doméstico golpeado por la pérdida del poder adquisitivo de los hogares, como consecuencia de elevadas tasas de inflación y del endurecimiento de las condiciones financieras entre otros. Mientras que las economías OCDE crecerán un 1.4% en promedio en 2023, el PIB de los siete países de América Latina aumentará un 1.5%. Para 2024 se prevé una mejora, las economías de América Latina repuntaran ligeramente hasta un 1.7% en promedio, por encima del crecimiento promedio de las economías de la OCDE (Cuadro 1), si bien este crecimiento no será suficiente para lograr la convergencia en PIB per cápita con la OCDE. Por otro lado, la inflación se ha ido moderando gradualmente en la mayoría de los países después de alcanzar niveles históricos, gracias a la rápida y fuerte subida de las tasas de política monetaria y menores precios globales de combustibles y alimentos. Este panorama, ya de si poco alentador, está acompañado de una elevada incertidumbre y de riesgos domésticos y externos inusualmente altos. Un crecimiento mundial menor de lo previsto, especialmente en Estados Unidos y en China, acompañados de una inflación más persistente de lo esperado que implique una política monetaria más restrictiva en el mundo y en la región, representan claros riesgos a la baja. Aunque los buenos niveles de liquidez y capitalización en el sector bancario permitieron que las recientes turbulencias internacionales tuvieran un impacto mínimo en los países de la región, el endurecimiento de las condiciones financieras a nivel global, junto con los signos de inestabilidad en el sector bancario internacional, podrían causar salidas de capitales y un repunte de la aversión al riesgo, junto a volatilidad de los tipos de cambio y del coste de financiación. En términos domésticos, la frecuencia de eventos climáticos severos se ha incrementado debido al cambio climático. Lo mismo sucede con las tensiones sociales que fueron exacerbadas por la pandemia y con las recientes presiones inflacionarias.

A pesar de estas dificultades, un futuro próspero y equitativo en América Latina es posible. Navegar los riesgos en el horizonte requiere fortalecer las cuentas públicas al tiempo que se atienden las crecientes demandas sociales y se mejora el crecimiento de una forma duradera. Cuadro 1. Perspectivas económicas de los países de América Latina Nota: América Latina (ALC) es la media ponderada por PIB a paridad de poderes de compra de los 7 países en la tabla para el PIB; y la media simple de los países incluidos en el cuadro para la inflación. Fuente: OCDE Perspectivas Económicas No. 113, junio de 2023. Fortalecer las cuentas públicas y proteger a los más vulnerables La situación fiscal permanece frágil en la región. Si bien los déficits fiscales disminuyeron en 2022, la deuda pública sigue históricamente elevada y la carga de intereses ha aumentado, siendo ésta muy sensible al endurecimiento de las condiciones de financiación globales. Todo ello junto con un crecimiento débil plantea riesgos para la sostenibilidad fiscal. Proseguir la consolidación fiscal es crucial para restaurar la confianza

de los mercados y reducir los costes del servicio de la deuda a la vez que se enfatiza el gasto social para apoyar a los pobres y hacer frente a las necesidades crecientes en educación, sanidad y protección social. Alcanzar estos objetivos requerirá la movilización de ingresos de manera progresiva, favorable al crecimiento y equitativa. Los programas de transferencias de apoyo social en un contexto de alta inflación deben ser temporales y focalizados hacia los más vulnerables y reducir los incentivos a la informalidad. Fomentar la participación laboral de las mujeres: clave para impulsar el crecimiento inclusivo Para impulsar el crecimiento potencial y reducir las desigualdades en América Latina será clave una agenda de reformas para mejorar el acceso y la calidad de la educación, incrementar la competencia y reducir las brechas de infraestructura (transporte y digital). Pero también incrementar la participación laboral de las mujeres será un ingrediente prioritario. La brecha en las tasas de participación femenina en el mercado laboral respecto a los hombres es grande, mayor que el promedio de la OCDE (Gráfico 1). Además, cuando las mujeres trabajan tienen más probabilidades de tener trabajos informales con peores condiciones laborales, reduciendo sus salarios. Cerrar estas desigualdades de género impulsarían muy significativamente el crecimiento en la región de una forma equitativa. No solo se incrementaría el número de personas en la fuerza laboral, sino que también se impulsaría la productividad, al mejorar la adecuación entre trabajadores y empleos. A su vez, el mayor crecimiento económico también tendría un impacto fiscal positivo, ayudando en el reto de fortalecer las cuentas públicas. ¿Como hacerlo? Promover el acceso a la educación inicial, que a pesar del progreso reciente es insuficiente en la mayoría de los países de América Latina, es clave para aumentar la participación laboral de las mujeres. La tasa de participación

escolar de los niños menores de 6 años es a menudo más baja en los hogares de menores ingresos, donde las necesidades de cuidado impiden que las madres participen en el mercado laboral. Deben incrementarse la oferta de plazas en las guarderías y subsidios para los hogares con menos recursos. Estas distorsiones de género en el mercado laboral están también estrechamente relacionadas con las desigualdades en la formación de las mujeres. Por tanto, es crucial seguir invirtiendo en educación básica accesible y de calidad. Finalmente, es necesario promover campañas de sensibilización y educación para combatir estereotipos de género tan arraigados en los países de América Latina. Gráfico 1. La brecha de género en participación laboral en los países de Latinoamérica está muy por encima del promedio de la OCDE Participación laboral, población 15-64 años de edad, por sexo, 2021 Fuente : OCDE, base de datos de estadísticas de población activa; y Perú: INEI. Más información: OECD Economic Outlook, junio 2023– Reporte completo en inglés con las proyecciones macroeconómicas, los principales desafíos estructurales e información detallada por país.

Perspectivas económicas de la OCDE para países de América Latina, junio 2023. Información detallada para Argentina | Brasil | Chile | Colombia | Costa Rica | México | Perú A Long Unwinding Road By Clare Lombardelli, OECD Chief Economist The global economy is turning a corner but faces a long road ahead to attain strong and sustainable growth. Global GDP growth slowed substantially throughout 2022, but several of the factors weighing negatively are now unwinding. Falling energy prices and headline inflation, easing supply bottlenecks and the reopening of China’s economy, coupled with strong employment and relatively resilient household finances, all contribute to a projected recovery. Nevertheless, the recovery will be weak by past standards. We project global growth to be 2.7% in 2023, with a modest pick-up to 2.9% in 2024 – both well below the average growth rate in the decade preceding the COVID-19 pandemic.

Policymakers need to act decisively on macroeconomic and structural policy to deliver stronger and more sustainable growth. This is hard. Core inflation remains too persistent. Debt levels are too high. And potential output is too low. Monetary policymakers need to navigate a difficult road. Although headline inflation is declining thanks to lower energy prices, core inflation remains stubbornly high, more so than previously expected. Central banks need to maintain restrictive monetary policies until there are clear signs that underlying inflationary pressures are abating. Some economies grappling with stubbornly high core inflation may require additional interest rate increases. However, policymakers must keep a watchful eye, given the uncertainties around the exact impact of the rapid and globally synchronised monetary policy tightening following an extended period of low interest rates. The tightening has already revealed some vulnerabilities in financial markets. Should further financial market stress arise, central banks should deploy financial policy instruments to enhance liquidity and minimise contagion risks. Clear communication will be crucial to avoid confusion about the potential conflict between pursuing price stability and financial stability mandates.

The choices for fiscal policymakers are clearer but no easier to implement given the inherent political sensitivity of policy choices with direct redistributive effects. Fiscal policy played a vital role in supporting the global economy through the shocks of the COVID-19 pandemic and Russia’s war in Ukraine. However, in the aftermath, most countries are grappling with higher budget deficits and higher public debt. The burden of debt servicing is increasing and spending pressures related to ageing and the climate transition are building. As the recovery takes hold, fiscal support should be scaled back and better targeted. Energy price support should be withdrawn as energy prices fall. Vulnerable households inadequately covered by existing social protection systems, will continue to need support, as still high food and energy prices particularly burden the most disadvantaged. Limited resources should be targeted only to those who really need it and to high-priority productivity-enhancing investments, including those driving the green transition and improving labour supply and skills. Gradually unwinding fiscal support will help reduce the burden on monetary policy, strengthen buffers against future crises and prepare for longer-term challenges Emerging-market economies face challenges from tight global financial conditions: higher debt servicing costs, capital outflows, and reduced credit availability from foreign lenders. Moreover, rising geopolitical tensions and concerns about supply chain security have prompted several countries to implement trade and investment restrictions. Increasingly restrictive trade policies risk curtailing the gains from global trade and harming the development prospects of low- income countries. Ultimately only ambitious structural policy reforms can sustainably raise long-term economic growth and people’s quality of life around the world. Revitalising labour and

product markets; removing barriers to cross-border trade; promoting competition and adapting competition policies to the digital era; and enhancing skill development are essential elements of the structural reform agenda. Private and public investment is needed in human, tangible and intangible capital to enable people to make the most of their skills and capabilities, and to harness the ever-increasing opportunities from technological transformation. Investment in education and skills is critical to enable people to flourish in the future economy and reap the benefits of increased productivity. Policymakers need to unwind the impact of a sequence of negative shocks to the global economy and face a complex set of challenges in doing so. They need to calibrate monetary and fiscal policies to curtail inflation and rebuild fiscal buffers without overly reducing growth. Delivering sustainably higher rates of growth will need bold and forward-thinking structural policy reforms allowing us to harness the opportunities of rapid technological advances, demographic shifts, and the climate transition. More information: Editorial from the OECD Economic Outlook, June 2023 Clare Lombardelli’s Twitter Clare Lombardelli’s LinkedIn La route est encore longue Clare Lombardelli, Cheffe économiste de l’OCDE L’économie mondiale a amorcé un tournant, mais la route est

encore longue pour parvenir à une croissance forte et durable. La croissance du PIB mondial a sensiblement ralenti tout au long de 2022, mais plusieurs des facteurs qui la brident encore commencent à s’estomper. Le recul des prix de l’énergie et de l’inflation globale, l’atténuation des perturbations de l’offre et la réouverture de l’économie chinoise sont autant de facteurs qui, conjugués à la vigueur de l’emploi et à la relative résilience des finances des ménages, contribuent à la reprise prévue. Celle-ci sera néanmoins timide par rapport aux rebonds observés dans le passé. D’après nos projections, la croissance mondiale s’établira à 2.7 % en 2023, avant de se redresser légèrement pour atteindre 2.9 % en 2024, soit bien en deçà du taux de croissance moyen enregistré durant la décennie qui a précédé la pandémie de COVID-19. Les décideurs publics doivent agir avec détermination sur les leviers macroéconomiques et structurels pour asseoir une croissance plus forte et plus durable. La tâche est ardue : l’inflation sous-jacente est trop persistante, les niveaux d’endettement sont trop élevés et la production potentielle est trop faible. Les autorités monétaires doivent négocier un virage délicat.

Malgré la décrue de l’inflation globale due au recul des prix de l’énergie, l’inflation sous-jacente reste obstinément forte, en tout cas plus élevée qu’on ne l’avait anticipé. Les politiques monétaires doivent rester restrictives tant qu’aucun signe d’atténuation des tensions inflationnistes sous-jacentes ne sera clairement confirmé. De nouveaux relèvements des taux d’intérêt pourraient être nécessaires dans certaines économies en proie à une inflation sous-jacente résolument élevée. Les autorités doivent toutefois rester vigilantes compte tenu des conséquences incertaines du resserrement monétaire rapide et synchronisé opéré à l’échelle mondiale après une longue période de faibles taux d’intérêt. Ce changement de cap a déjà mis au jour certaines vulnérabilités sur les marchés financiers. Si les tensions devaient s’accentuer, les banques centrales devraient mobiliser divers instruments de politique financière pour accroître la liquidité et réduire autant que possible les risques de contagion. Elles devront à tout prix communiquer clairement pour éviter toute confusion quant au conflit potentiel entre le double mandat de stabilité des prix et de stabilité financière. Les choix qui s’imposent aux autorités budgétaires sont plus évidents, mais pas plus faciles à mettre en œuvre, les décisions qui ont des effets redistributifs directs étant toujours politiquement sensibles. La politique budgétaire a joué un rôle essentiel en soutenant l’économie mondiale face aux chocs provoqués par la pandémie de COVID-19 et la guerre menée par la Russie en Ukraine. Cependant, la plupart des pays sont aujourd’hui aux prises avec des déficits budgétaires plus amples et un endettement public en hausse. La charge du service de la dette s’alourdit tandis que les tensions sur les dépenses liées au vieillissement démographique et à la transition climatique s’accentuent. Alors que la reprise va s’installer, il faudra réduire et mieux cibler les mesures de soutien budgétaire. Les aides

liées aux prix de l’énergie devraient être démantelées à mesure que ceux-ci diminueront. Les ménages vulnérables, dont la protection sociale est actuellement insuffisante, continueront d’avoir besoin d’aide, le niveau toujours élevé des prix de l’alimentation et de l’énergie pesant particulièrement sur les plus défavorisés. Les ressources disponibles, limitées, devraient être consacrées à celles et ceux qui en ont réellement besoin, ainsi qu’aux investissements hautement prioritaires propices aux gains de productivité, notamment ceux qui favorisent la transition écologique et améliorent l’offre de main-d’œuvre et les compétences. La suppression progressive des aides budgétaires permettra de moins solliciter les instruments de politique monétaire, de renforcer les marges de manœuvre pour affronter les crises futures, et de se préparer à faire face aux enjeux à plus long terme. En raison du durcissement des conditions financières à l’échelle mondiale, les économies de marché émergentes traversent des difficultés, notamment un alourdissement du service de la dette, des sorties de capitaux ou une réduction de l’offre de crédit des prêteurs étrangers. Par ailleurs, la montée des tensions géopolitiques et les préoccupations grandissantes concernant la sécurité des chaînes d’approvisionnement ont incité plusieurs pays à prendre des mesures limitant les échanges et l’investissement. Des politiques commerciales de plus en plus restrictives risquent de réduire les gains tirés du commerce mondial et de compromettre les perspectives de développement des pays à faible revenu. En définitive, seules des réformes structurelles ambitieuses peuvent améliorer durablement la croissance économique à long terme et la qualité de vie des populations partout dans le monde. Tout train de réformes structurelles doit impérativement viser à redynamiser les marchés du travail et des produits, à lever les obstacles aux échanges

internationaux, à favoriser la concurrence et à adapter les politiques en la matière à l’ère numérique, ainsi qu’à renforcer les compétences. Des investissements privés et publics dans le capital humain et les actifs matériels et immatériels seront indispensables pour permettre aux individus d’utiliser au mieux leurs compétences et aptitudes, et tirer parti des perspectives toujours plus nombreuses offertes par la transformation technologique. Il est primordial d’investir dans l’éducation et les compétences afin que chacun puisse s’épanouir dans l’économie future et récolter les fruits d’une productivité accrue. Les décideurs publics vont devoir estomper les effets induits par une succession de chocs négatifs sur l’économie mondiale, et affronter pour cela une série de défis complexes. Il leur faut notamment ajuster les politiques monétaires et budgétaires de façon à réduire l’inflation et à reconstituer des marges de manœuvre budgétaires sans trop freiner la croissance. Pour améliorer durablement les taux de croissance, ils ne pourront se dispenser de mener des réformes structurelles audacieuses et novatrices qui nous permettront de mettre à profit les perspectives ouvertes par les progrès technologiques rapides, les évolutions démographiques et la transition climatique. Editorial des Perspectives économiques de l’OCDE

You can also read