Risk Outlook: Plenty to worry about beyond Covid - Bizweek

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GLACIERS OF GLOBAL FINANCE

The Currency

Composition of

Central Banks’

Reserve Holdings

ÉDITION 323

ÉDITION 151 –– VENDREDI

VENDREDI01

23JANVIER 2021

JUIN 2017 L’HEBDOMADAIRE DIGITAL GRATUIT

L’ HEBDOMADAIRE ÉLECTRONIQUE GRATUIT

A REPORT BY THE ECONOMIST INTELLIGENCE UNIT

Risk Outlook:

Plenty to worry

about beyond Covid

2021

VENDREDI 01 JANVIER 2021 | BIZWEEK | ÉDITION 323 3

LA TOUR

A REPORT BY THE ECONOMIST INTELLIGENCE UNIT

Risk Outlook: Plenty to worry

about beyond Covid

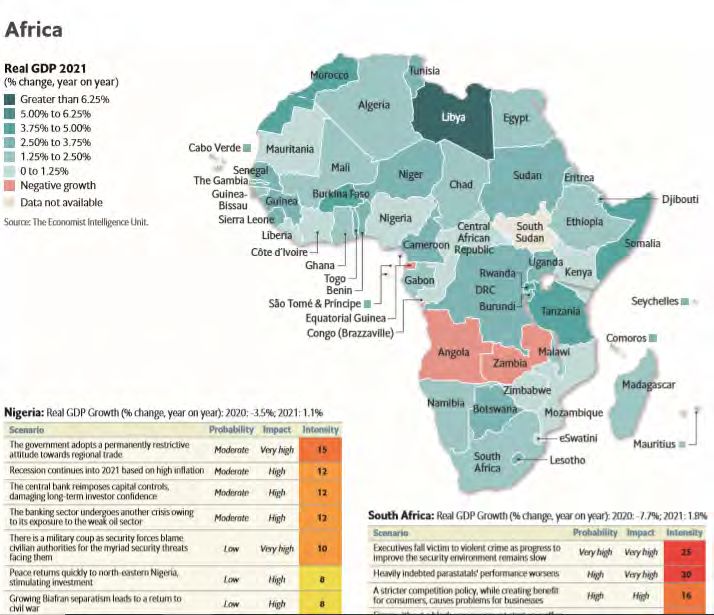

Managing risk in an increasingly bifurcated world in the midst and aftermath of the Covid-19 pandemic will continue to dominate the thoughts of

risk managers. Divergent recovery speeds, differing policy responses, global supply-chain readjustments and ever-present political instability create an

enormously challenging global business environment. Looking beyond that, there is a long tail of country risks, not directly related to—but many

clearly exacerbated by—Covid-19 that businesses are going to have to understand to ensure that they can be managed

W

e are forecasting glob- to accept higher production costs.

al economic growth 3. Political instability continues

of 4.2% year on year to be a threat – joblessness, poverty lev-

in 2021, on the back els and rising inequality have only been

of an anticipated 4.7% worsened by Covid-19.

contraction in global output this year. Of 4. Many countries are newly pri-

course, this number masks enormous re- oritising substantial investment in

gional disparities. We are forecasting huge infrastructure – financing models will

divergence in the speed of recovery for indi- vary amid widespread fiscal constraints,

vidual economies, based on multiple factors: but with record-low interest rates in

fiscal space and commitment; monetary pol- many places helping. Infrastructure in-

icy flexibility; sectoral composition; severity vestment will be pursued to facilitate

and timing of lockdown measures; export job creation and, in some cases, to try

market exposure; and labor market dynam- to keep the potential for social unrest at

ics and demographics. This divergence, bay.

straddling as it does already inflame global Risks to our core country forecasts

trade tensions, cements our expectation of abound. Accelerated vaccine rollout and

an increasingly bifurcated world. We have an unleashing of pentup demand could

produced a series of analyses that spotlight cause several countries to surge ahead on

key issues to watch at a country level in 2021 this chart. Conversely, in other countries

(Things to watch in 2021). Our core scenar- the labour market may be severely dimin-

io for these countries, in terms of their re- ished for an extended period, weighing

covery, is informed by the above checklist. on post-pandemic demand and creating

However, there are other recurring themes recovery laggards.

that will shape the growth outlook and the turing investment, while companies are versus specialism—will create new in-

business environment for these markets in concurrently seeking to diversify their vestment hotspots and strengthen some

NOTE: The Economist Intelligence

the coming years. supply chains. existing investment centres. There will

2. The reassessment of the risk versus be some limits on supply-chain rebalanc- Unit (The EIU) is the research and

1. Global trade and supply chains are analysis division of The Economist

being reshaped – countries are striv- reward equation – as companies weigh ing: the benefits of specialisation will be

up labour costs, political stability, FDI hard for both companies and economies Group, the sister company to The

ing to diversify their export markets and

jostling to capture redirected manufac- policy and the benefits of localisation to give up, and companies will also have Economist newspaper.

VENDREDI 01 JANVIER 2021 | BIZWEEK | ÉDITION 323 4

ACTA PUBLICA

GLACIERS OF GLOBAL FINANCE

The Currency Composition of

Central Banks’ Reserve Holdings

The currencies that are being held by central banks as foreign exchange reserves have remained largely steady over decades. Changes in the composi-

tion of these holdings can, at best, be described as glacial in pace. But geopolitical shifts and technological revolutions are reshaping the global econo-

my and the international use of currencies. These forces, and the fallout from the COVID-19 pandemic, could further accelerate the transformations

T

in the reserve holdings of central banks

here are currently around 180 drivers of central banks’ reserve currency has the potential to undergo a sudden, un- economic policies to preserve their growth

national currencies, but only a holdings over recent decades, and how these expected, and accelerated transformation. potential.

few are widely used for inter- drivers have changed. The international use of currencies can

national transactions, such as One key finding is that, given the dollar’s The future of reserve also reflect strategic considerations. For in-

invoicing, paying for imports,

and issuing debt or investing abroad. These

(and to some extent, the euro’s) internation-

al dominance, to date, any shifts in central

currencies stance, reserve currency portfolio decisions

may be influenced by foreign policy consid-

currencies are the U.S. dollar, the euro, and, bank reserve holdings have been minimal. erations and security ties. The fallout from

Our paper suggests a number of econom-

to a lesser extent, the Japanese yen, the Brit- For example, despite China’s growing role trade tensions and international sanctions

ic and financial trends that could impact the

ish pound, and a few others. When crises in the global economy, the Chinese renmin- can prompt countries to consider changes in

future composition of reserve holdings. Ge-

hit, companies and investors usually seek bi has gained only a small foothold in global their reserve holdings and potential issuers

opolitical and technological developments

safety in dollars. transactions, such as issuing foreign debt or to seek to internationalize their currencies.

might prove as significant as economic

Central banks have long held internation- trading in the global foreign exchange mar- The pandemic has accelerated advanc-

considerations, and, together with the cur-

al reserves in these same currencies. This ket. es in financial and payment technol-

rent COVID-19 pandemic, could accelerate

is unsurprising as reserves are intended to The paper also found that financial links ogies. Potential competition from pri-

future transformations. Potential drivers of

back up international transactions as de- seem to be a key driver of reserve currency vate issuers such as Diem – Facebook’s

change include:

scribed above, allowing country authorities holdings, and increasingly so in the last dec- blockchain-based payment system – has

Shifts in international finance: the

to finance balance of payments needs, inter- ade. This would suggest that, as long as the spurred major central banks to acceler-

strong response to the European Commis-

vene in foreign exchange markets, and pro- dollar continues to dominate global finance ate work on central bank digital currencies

sion’s large-scale bond issuance in October

vide foreign exchange to domestic agents. and trade, its dominance as a reserve curren- and cross-border payments. The European

highlights potential demand for alternatives

The slow pace of change in reserve hold- cy looks set to endure. Central Bank and People’s Bank of China,

to dollar-denominated debt. Emerging mar-

ings But, just as slow-moving glaciers can among others, are exploring the issuance of

ket and developing countries could also is-

Building on a novel dataset, a new IMF sometimes unexpectedly surge forward, the central bank digital currencies which could

sue more debt in the currencies of emerg-

staff paper analyzes the composition and currency composition of reserve holdings increase demand for their currencies.

ing creditors, such as China, to help meet

Superior technology platforms could also

increased financing needs. Our paper finds

help new currencies overcome some of the

that the currency denomination of public

advantages of incumbent currencies. De-

debt is an especially important determi-

pending on the adoption and use of public

nant of emerging market and developing

or private digital money, central banks might

countries’ reserve holdings, likely reflecting

have to rethink what constitutes, and how to

central banks’ desire to hedge against risks

hold, reserves going forward.

associated with debt obligations.

There is currently no sign of major shifts

Changing trade links and invoicing

in the composition of central bank reserve

practices could also alter demand for inter-

currencies. However, the glacial pace of

national currencies. Both the pandemic and

change over recent decades should not be

recent trade tensions have highlighted the

taken as an indication of the future. There is

fragility of global supply chains. Countries

considerable uncertainty around global eco-

are now more interested than ever in ensur-

nomic and financial trends, as well as geopo-

ing critical supplies. A shift toward localized

litical and technological developments, and

production would reduce the demand for

so scope for more dynamic transformation

international currencies. Meanwhile, lower

in the future.

reliance on any single trading partner might

diversify demand for currencies. The recent

conclusion of the Regional Comprehensive A Paper by the IMF’s IMF’s Strategy,

Economic Partnership in Asia – a free trade Policy, and Review Department.

agreement between fifteen nation states in Authors:

the region – may signify a larger role for al- ALINA IANCU,

ternate currencies that currently account for Deputy Unit Chief;

a small share in international reserves. NEIL MEADS,

The credibility of the policies of debt-is- Senior Economist;

suing countries is fundamental for trust in MARTIN MÜHLEISEN,

their currencies. The COVID-19 pandemic former Director;

has highlighted the need for current and

YIQUN WU,

potential issuers to enact sound health and

Economist

VENDREDI 01 JANVIER 2021 | BIZWEEK | ÉDITION 323 5

POST SCRIPTUM

CRISTIAN ALONSO FUTURE

How Artificial Intelligence

(economist in the

IMF’s Fiscal Affairs

Department)

SIDDHARTH KOTHARI

(economist in the

IMF’s Asia and Pacific

Department)

Could Widen the Gap Between

SIDRA REHMAN

(economist in the IMF’s

Middle East and Central

Rich and Poor Nations

Asia Department) The International Monetary Fund’s (IMF) recent staff research finds that new technology risks

widening the gap between rich and poor countries by shifting more investment to advanced

economies where automation is already established. This could in turn have negative conse-

quences for jobs in developing countries by threatening to replace rather than complement

their growing labor force, which has traditionally provided an advantage to less developed econ-

omies. To prevent this growing divergence, policymakers in developing economies will need to

take actions to raise productivity and improve skills among workers

N

ew technologies like artificial larger in advanced economies due to robots ments will tend to increase incomes but also

intelligence (AI), machine being used more intensively there (the increase income inequality, at least during

learning, robotics, big data, and “share-in-production” channel discussed the transition and possibly in the long run

networks are expected to revo- above). As a result, investment gets diverted for some groups of workers, in both ad-

lutionize production processes, from developing countries to finance this vanced and developing economies.

but they could also have a major impact on capital and robot accumulation in advanced There is no silver bullet for averting di-

developing economies. The opportunities economies, thus resulting in a transitional vergence. Given the fast pace of the robot

and potential sources of growth that, for decline in GDP in the developing country. revolution, developing countries need to

example, the United States and China en- Terms-of-trade: A developing economy will invest in raising aggregate productivity and

joyed during their early stages of economic likely specialize in sectors that rely more on skill levels more urgently than ever before,

development are remarkably different from unskilled labor, which it has more of com- so that their labor force is complement-

what Cambodia and Tanzania are facing in pared to an advanced economy. Assuming ed rather than substituted by robots. Of

today’s world robots replace unskilled labor but comple- course, this is easier said than done. In our

ment skilled workers, a permanent decline model, increases in total factor productiv-

Results from a Model in the terms of trade in the developing re- ity—which account for the many institu-

gion may emerge after the robot revolution. tional and other fundamental differences

Our model looks at two countries (one This is because robots will disproportion- between developing and advanced countries

advanced, the other developing) that both ately displace unskilled workers, reducing not captured by labor and capital inputs—

produce goods using three factors of pro- their relative wages and lowering the price are especially beneficial as they incentivize

duction: labor, capital, and “robots.” We of the good that uses unskilled labor more more robots and physical capital accu-

interpret “robots” broadly, to encompass the intensively. The drop in relative price of its mulation. Such improvements are always

whole range of new technologies mentioned main output, in turn, acts as a further neg- beneficial, but the gains are stronger in the

above. Our main assumption is that robots ative shock, reducing the incentive to invest context of the AI revolution.

substitute for workers. The AI revolution in and potentially leading to a fall not just in Our findings also underscore the impor-

our framework is an increase in the produc- relative but in absolute GDP. tance of human capital accumulation to

tivity of robots. prevent divergence and point to potentially

We find that divergence between developing Robots and wages different growth dynamics among devel-

and advanced economies can occur along oping economies with different skill levels.

three distinct channels: share-in production, Our results critically depend on whether ro- The landscape is likely going to be much

investment-flows, and terms-of-trade. bots indeed substitute for workers. While it more challenging for developing countries

Share-in-production: Advanced economies may be too early to predict the extent of this which have hoped for high dividends from a

have higher wages because total factor substitution in the future, we find suggestive much-anticipated demographic transition.

productivity is higher. These higher wages evidence that this is the case. In particular, The growing youth population in develop-

induce firms in advanced economies to we find that higher wages coincide with ing countries was hailed by policymakers

use robots more intensively to begin with, significantly higher use of robots, con- as possibly a big chance to benefit from a

especially when robots easily substitute for sistent with the idea that firms substitute transition of jobs from China as a result of

workers. Then, when robot productivity ris- away from workers and towards robots in its graduating middle-income status. Our

es, the advanced economy will benefit more response to higher labor costs. findings show that robots may steal these

in the long run. This divergence grows larg- jobs. Policymakers should act to mitigate

er, the more robots substitute for workers. Implications those risks. Especially in the face of these

Investment-flows: The increase in pro- new technologically-driven pressures, a

ductivity of robots fuels strong demand Improvements in the productivity of robots drastic shift to rapidly improve productivity

to invest in robots and traditional capital drive divergence between advanced and de- gains and invest in education and skills de-

(which is assumed to be complementa- veloping countries if robots substitute easily velopment will capitalize on the much-an-

ry to robots and labor). This demand is for workers. In addition, those improve- ticipated demographic transition.

VENDREDI 01 JANVIER 2021 | BIZWEEK | ÉDITION 323 6

DEBRIEF

TOURISM INDUSTRY

Beachcomber secures

Rs 2.5 billion from Mauritius

Investment Corporation

The proceeds from the Bonds will be used principally for the working capital

requirements of the Company’s Mauritian operations and payment of interests in

respect of the Company’s existing indebtedness. The Board is of the view that the

Loterie Shell : Bruno Couve fera le

injection of MUR 2.5 billion, together with other strategic initiatives, will stabilise

the Company’s financial position, pending a gradual return to profitability following

plein gratuitement pendant une

the full re-opening of our borders and a sustained volume of tourist arrivals to our année pour une valeur de Rs 120 000

La campagne promotionnelle de Vivo Energy Mauritius, société

destination détentrice de la franchise Shell à Maurice, entame sa dernière ligne

T he Board of New Mauritius droite. En attendant que soit désigné le grand gagnant de décembre,

Hotels (NMH) has engaged qui repartira avec une BMW 218i Gran Coupé Lounge, le tirage de

in discussions with the Mau- novembre a fait remporter à Bruno Couve douze bons de carburant

ritius Investment Corporation Ltd Shell FuelSave d’une valeur totale de Rs 120 000. Client régulier de

(MIC), and issued a communiqué la station-service Shell Curepipe et membre de Shell SmartClub, pro-

to inform its shareholders and the gramme de fidélité de Vivo Energy Mauritius, Bruno Couve pourra

public at large that, on 29 Decem- faire le plein gratuitement pendant une année pour une valeur de Rs

ber 2020, the Company has signed a 10 000 par mois.

binding term sheet for the issue of

redeemable and convertible bonds El Diablo renaît au LUX* Grand

to the MIC for a total subscription

amount of MUR 2.5 billion (Bonds), Gaube le temps d’un week-end

secured by a floating charge on the

assets of the Company.

The Company retains the option

to redeem some or all of the Bonds as published by the Stock Exchange have evolved the sanitary protocols in our

any time prior to their maturity, of Mauritius during the period of resorts to cater for the safety of our guests

which will be on the ninth (9th) an- 01 January 2020 to 30 June 2020. In and employees. To minimize cash outflows

niversary of the first subscription case of a covenant breach that is not and preserve the jobs of our employees, we

of the Bonds. In the event that remedied, the MIC would have the have initiated cost reduction initiatives and

the Bonds are not redeemed on or right to convert the Bonds pursuant salary cuts and have also received support

before maturity, any outstanding to the abovementioned terms and from the Government in the form of the

Bonds would be converted into or- conditions. Government Wage Assistance Scheme.

dinary shares of the Company at a “Over the past nine months, we have Nevertheless, the significant investments

pre-agreed fixed valuation of MUR put in place several measures to sustain the made in our hotels and the obligations to

7.4529 per share, being computed as business and to actively contribute to the na- our lenders and suppliers continue to impact

the volume-weighted average price tional sanitary response. We have provided on our short-term liquidity position”, says

of ordinary shares of the Company assistance through quarantine facilities and the Company in the communiqué.

Ré-ouverture du Tamarina Golf

& Spa Boutique Hotel L’une des boîtes de nuit les plus populaires de Maurice s’apprête à

Après quelques mois de fermeture pour rénovation, Boma ou encore observer les dauphins qui se balad- renaître de ses cendres en 2021. LUX* Grand Gaube mettra sur pied

le Tamarina Golf & Spa Boutique Hotel a rouvert ses ent dans la baie le matin au petit déjeuner, l’espace l’incontournable El Diablo, discothèque mythique dans le nord du

portes au public ce décembre avec un espace com- principal, avec son magnifique deck perché au cœur pays, le temps de deux soirées… d’enfer. L’hôtel n’a pas voulu faire

mun complètement revisité et agrandi. Son restaurant d’une nature luxuriante, font de Tamarina un des lieux dans la demi-mesure : les adeptes de l’ancienne discothèque y retro-

principal, « L’escale » a en effet été totalement rénové préférés de ceux qui souhaitent profiter du meilleur uveront le même décor, les mêmes deejays, les mêmes équipes et les

offrant plus d’espace au restaurant, ainsi qu’au bar, de la côte ouest. Dans le cadre de sa réouverture, et mêmes barmen, les 8 et 9 janvier prochain. Trois pistes de danse, à

pour profiter de la vue imprenable sur la magnifique pour la période festive, Tamarina Golf and Spa Bou- savoir Le Lounge, El Diablo et Pass Out, ont été aménagées pour ac-

baie de Tamarin. Que ce soit pour admirer le couch- tique offre tout un éventail de forfaits exclusifs. Le cueillir les fêtards. Si vous êtes fan de El Diablo, ne manquez surtout

er de soleil, regarder les surfers qui s’attaquent aux séjour en demi-pension est actuellement à partir de pas l’offre Early Bird disponible jusqu’au 31 décembre.

vagues mythiques de la baie, se réchauffer autour d’un Rs 2,500 par personne et par nuit.

Une nouvelle salle de classe pour

La grande famille ABC les enfants du Centre d’Amitié

Les Medine Volunteers, étaient une fois de plus sur le terrain pour

solidaire avec les plus démunis venir en aide à la communauté, cette fois ci au Centre d’Amitié à

Bambous. Pendant trois après-midis consécutives, à l’initiative de

la Fondation Medine Horizons, les employés volontaires de Medine,

Offrir un peu de magie de Noël et aidés d’étudiants de Uniciti Education Hub, se sont ainsi relayés

de joie à des enfants nécessiteux et pour redonner un coup de neuf et réorganiser les salles de classe de

leur redonner le sourire en cette fin cette école pré-primaire qui accueille des enfants issus de milieux vul-

d’année. C’est dans cet optique que nérables, ce, afin de créer un nouvel espace pouvant accueillir une

le Groupe ABC, à travers la Fonda- classe additionnelle.

tion Sir J. Moilin Ah-Chuen, a récem-

ment organisé une distribution de

cadeaux à l’attention de 200 enfants Des promos et des cadeaux à gogo

issus de familles défavorisées. Cette

distribution, organisée avec l’appui

avec MC Vision/CANAL+ Maurice

Terminer l’année sur une note festive. C’est dans cette optique que

d’ONG partenaires dont Caritas

MC Vision/CANAL+ Maurice est allé à la rencontre de ses abonnées

Tranquebar, Caritas Roche Bois et

à Quay 11, Port-Louis, le 23 décembre. Cette journée a également

Ki Fer Pas Mwa, a bénéficié, comme

ployés du Groupe ABC qui ont fait par le biais d’une collecte organisée à vu la présence du Père Noël avec des valises pleines de promos et de

pour les années précédentes du sou-

don de jouets et de matériel scolaire travers le Groupe. cadeaux.

tien des directeurs, cadres et em-

You can also read