Reading: a new city in the south east of England? - Savills

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Savills World Research

UK Cross Sector

Reading

savills.com/research

Spotlight | 2017

Reading: a new city in

the south east of England?

Summary Reading has a strong tech economy and enviable location. But, to grow into a city, it needs more

space. We examine its potential, and the options for urban development and growth beyond its boundaries

Reading’s International Reading punches Reading is a key Old and obsolete

employment market companies and above its weight component in the office stock has been

is the same size as the digital and from an employment wider regional largely absorbed

many regional cities. tech sector are perspective, but is economy. We believe through permitted

Its infrastructure and continuing to set constrained in terms that the traditional development. This

rail network supports up headquarters of housing delivery golden triangle of has delivered more

a large and vibrant in Reading’s town by its tightly drawn knowledge economies than one-third of new

economy. See p2 centre, thanks to boundaries. This of Cambridge, Oxford housing stock. New

the delivery of modern restricts the town from and London can be homes in the town

office stock with a achieving its potential. extended to form a centre are particularly

highly accessible See p6 knowledge kite. See p3 appealing to young

location. See p2 people working in the

tech sector. See p4

OVERVIEW

Punching above

its weight

With modern office stock and high accessibility, Reading’s employment market and

corporate investment outperforms many major UK cities, including Oxford and Leeds

T

here are several reasons why Reading operates and out-of-town locations. Reading exceeds total

like a regional city market. It has excellent office investment in larger regional cities such as

transport links to markets across the country Glasgow, Bristol, Leeds and Cardiff, highlighting

and fast journey times to central London. its strong performance and high-quality office stock.

Crossrail will improve journey times and connectivity

even further when it becomes operational in 2019. Global appeal

International corporations continue to locate in

Modern office stock Reading. The town’s talented catchment workforce

Despite Reading’s modest population of 163,000, the and large business parks attract these occupiers as

town’s strong office provision has enabled businesses they favour campus-style working environments.

to grow and expand without leaving the area. Historically, large out-of-town business parks have

Reading is the dominant office market in the outer attracted traditional technology and pharmaceutical

south east, outperforming many other large office occupiers. Here, business parks with greater amenities

markets. The long-term average office take-up is more have performed best at attracting such companies

than 400,000 sq ft and the town has an estimated and this will remain the case going forward.

office stock of around 10 million sq ft. Following amenity improvements, 76,000 sq ft

Reading ranks fourth for office investment flows, was let at Arlington Business Park in the first half

highlighting the town’s appeal and its ability to offer of 2017. Prior to those improvements, there had

prime office investment opportunities in town-centre been limited transactional activity in recent years.

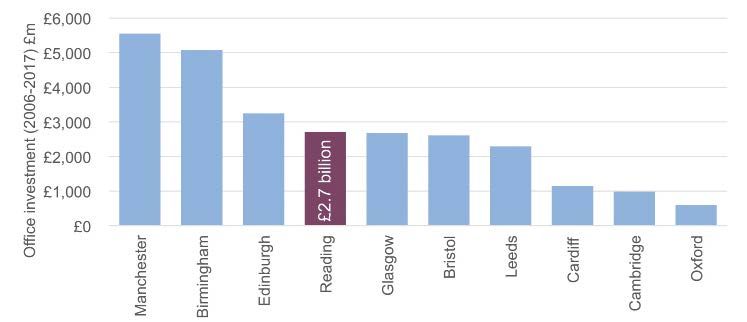

Office appeal Despite its smaller population, office investment in Reading (2006-2017)

is higher than many larger cities, reflecting the quality of the office stock and occupiers

£6,000

Office investment 2006-2017 (£m)

£5,000

£4,000

£3,000

£2,000

£2.7 billion

£1,000

£0

Manchester

Leeds

Cardiff

Cambridge

Oxford

Birmingham

Edinburgh

Bristol

Reading

Glasgow

Source Property Data

2 savills.co.uk/research

OVERVIEW

In town, there is a growing trend for serviced providing an appropriate stock of property to cater

office operators leasing space that meets the for company needs.

co-working culture. This targets Reading’s strong The flow of global corporate investment helps us

start-up community – particularly in the tech identify the strength and location of commercial real

and software sector. estate. Reviewed alongside property demand and

According to the Tech Nation 2017 report, supply, this provides a guide to the market potential

there were, on average, 605 start up births per year in the short to medium-term.

from 2011-2015 and more than 40,000 digital jobs We have reviewed 212 corporate investment deals

based in the town. With this thriving tech scene, in Reading since 2012, including venture capital (VC)

co-working operators accounted for 24% of take-up and mergers and acquisitions (M&A). Within the

in the first half of 2017. M&A market, there have been deals worth £10 billion:

People working in Reading are a rich mix of 87% involving companies headquartered in the UK

international and domestic workers. Some 29% of and 13% with headquarters in the US. The strength

tech businesses say they employ people from outside of the M&A market is an indicator of the more mature

the EU, the highest figure in the UK. This provides companies present, and the US prevalence in Reading.

Reading with a degree of insulation from Brexit and During the same period, there was £2 billion of

underlines its identity as a leading technology hub other types of corporate venture capital investment.

in a global context. These are more reflective of the start-up community

We believe the traditional golden triangle of and an indication of future growth. The corporate

knowledge economies – Cambridge, Oxford and strength of Reading lies in the IT and B2B sectors

London – can be extended to Reading to form and the corporate transactions reflect this. A more

a knowledge kite. This is based on the advanced detailed breakdown of the deals shows that the software

knowledge economy that exists in Reading and the sector accounts for 37% of the overall five-year total.

thriving technology sector. How Reading performs, corporately, is impressive

Furthermore, as highlighted by the National compared with key cities across the UK. In terms

Infrastructure Commission, the improved East West of the IT sector, Reading is in third place. Only

Rail Link will provide a greater service between Cambridge (£24 billion ARM acquisition by SoftBank

Cambridge and Oxford, and also connect them to and Alibaba Group) and Bristol (£12.5 billion

Reading. This will ensure Reading remains a key acquisition of EE by BT) are ahead. Reading also

component in the regional and wider economy. performs well in the B2B market – lying third behind

Manchester and Edinburgh.

Leading target for investment This demonstrates that Reading has a significant and

The past 20 years has shown that Reading has the diverse offering for employees and exceeds the level of

ability to attract global companies. To support this, corporate investment activity in most major UK cities.

the commercial property market has responded by Overall, it will remain a leading corporate location.

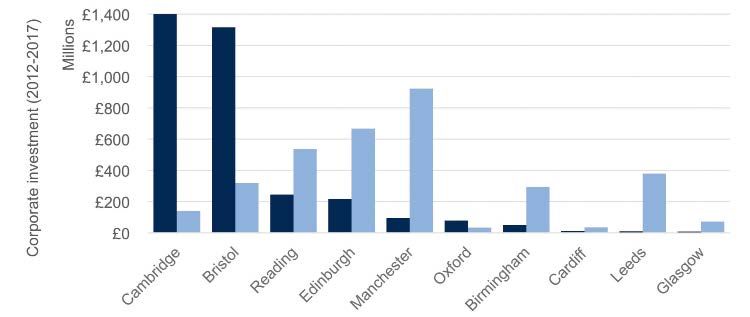

Attracting investment Ranking third for both IT and B2B company investment since 2012, investment

in Reading exceeds the level of corporate venture capital investment activity in most major UK cities

£1,400

Corporate investment 2012-2017 (£m)

£3.3 billion

£1,200

Reading is 3rd

£1,000 for IT and B2B

investment

£800

£600

£400

£200

£0

Cambridge

Bristol

Reading

Edinburgh

Manchester

Oxford

Birmingham

Cardiff

Leeds

Glasgow

Key IT companies

Businesses providing services to other businesses (B2B): professional services, construction and transportation

Source Company data

savills.co.uk/research 3

DEVELOPMENT

Primed for city status

Reading may be meeting its current targets, but it must develop more living

and office space in and around the town centre to meet its potential as a city

O

n the face of it, Reading is achieving its The result is that locals are competing for housing with

housing targets. In the year to March 2016, large numbers of people who commute to the capital.

750 homes were added, up from 264 and 360

in the two previous years and above the Office supply needs to expand

town’s target estimate of 699. But with strong and There is clear demand for new office stock in the

growing employment, our research suggests that town centre, highlighted by interest in Thames

Reading needs many more than this target to reach Tower, R+ and The White Building.

its full potential as a city. A total of 110,000 sq ft had been let at these three

In the past few years, delivery has been boosted new buildings by the end of the first half of 2017.

by office to residential conversions in the town centre. Strong demand for new, high-quality office space

In the year to March 2016, 254 homes had been in the town centre has resulted in record rents. The

converted from offices, providing 34% of new supply. letting performance of this new stock is encouraging

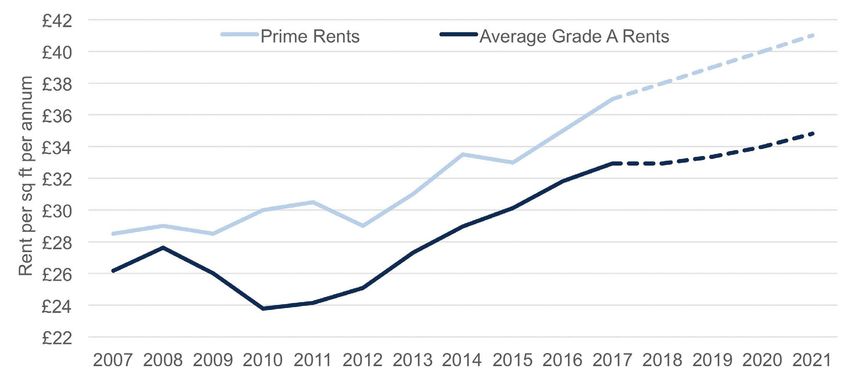

The strength of office to residential conversion is and we forecast rents to reach £40psf by 2020.

a good indicator of rental demand for inner city For Reading to cement its status as the leading

stock, as much of this enters the buy-to-let market. office market in the south east and be recognised

However, office space for conversion is a finite as a regional city, more development in the town

resource and cannot be relied on for sustainable centre will be needed.

levels of new supply. Our analysis indicates a shortage of town centre

office space by 2019. As such, Reading may not be

Central Reading revitalised able to satisfy large requirements in the Thames Valley.

Many new homes built in the last three years have Occupiers here are more footloose than in other office

been in the town centre, evidence of the revitalisation markets and they will move if they can’t satisfy their

of this part of Reading. Here, recent sales have exceeded requirements in one market.

£500psf, much higher than the average of £385psf. For Reading to capitalise on demand from central

Compared with London, £500psf is relatively affordable London, it is crucial there is high-quality stock

and sits in the mainstream part of the market, where available in the town centre. It is unlikely central

there is a severe supply demand imbalance in the capital. London occupiers will consider out-of-town locations.

Prime rental office outlook Strong demand for new, high-quality office space in Reading

town centre has resulted in record rents. We forecast these to reach £40psf by 2020

Prime rents Average grade A rents

Maximum rent per sq ft per annum (£)

Source Savills Research

4 savills.co.uk/research

DEVELOPMENT

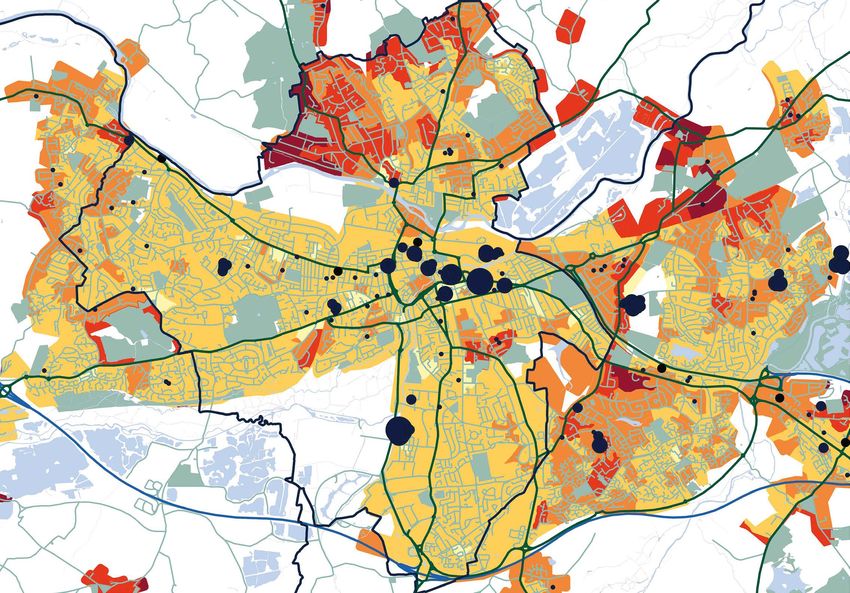

Residential supply Many of the new homes built in Reading in the last three years

have been in the city centre, evidence of the revitalisation of this part of Reading

Emmer

Green

Caversham

Tilehurst

Woodley

Lower Earley

Whitley

Key

Average house price Number of new build sales (three years to June 2017)

(year to June 2017) 1-10 10-20 20-40 40-60 60-80

Below £200,000

£200,000-£400,000

£400,000-£600,000

£600,000-£800,000

£800,000+

Source Savills Research using Land Registry

savills.co.uk/research 5PLANNING

Meeting growing

demand

Despite its strong tech economy, enviable location and transport links, Reading is

constrained by its housing stock. We highlight untapped potential both in town and beyond

T

o accommodate its growing housing need Build to rent is not just an urban phenomenon.

and emerge as a true city, Reading requires We have seen many successful family housing models

more homes of all tenures. These homes which use a build-to-rent delivery and funding

should meet a range of demands, including approach. Both Sigma and Mill have acquired house-

private rent, affordable, and open market sale. builder stock on mixed-tenure developments and

House prices, affordability, and demand for Help deliver family housing stock for the rental market.

to Buy, all point to the need for more mixed-tenure Housing associations are also delivering rented

developments. The delivery models of housing stock on large housing developments. This build-to-

associations such as L&Q and Places for People aim to rent solution will be focused around the delivery of

meet a range of housing need, from build to rent and professionally managed, good-quality family housing

shared ownership through to open market sale and that is less amenity driven and in locations where

affordable homes, and Reading needs to see more families want to live.

of this type of housing delivery.

Demand for Help to Buy

Private rent on the rise As well as homes for rent, Reading is in desperate need

With strong economic growth and good transport of homes for open market sale. With the average house

links to London, there is high demand to support costing nine times annual earnings (up from six times

this tenure for rented housing in Reading. in 2013), it has become less affordable for local people.

Almost one-third of households rent privately in First-time buyers have been supported by Help to

Reading, which is significantly above the national Buy. They make up 93% of those using the scheme in

average and more in line with central London, which Reading since it was introduced. In the town centre,

points to the need for more rental supply. Rents have new supply has sold to investors leaving little stock for

been growing despite an increase in stock following first-time buyers. Additional supply is needed to meet

the rise in stamp duty in 2016. The success of the the local owner-occupier market.

office to residential conversion market also indicates

demand for urban living and rented housing.

Driven by international occupiers and the push

into the tech economy, we believe there is untapped Almost one-third of households rent

demand from ‘urbanite techies’ for purpose-built

rented housing. As yet, Reading has not seen the privately in Reading, significantly

delivery of any new build-to-rent schemes, while above the national average and

there is a strong market for this type of product

in the town centre. This group is likely to be young more in line with central London

and prefer to rent.

6 savills.co.uk/researchPLANNING

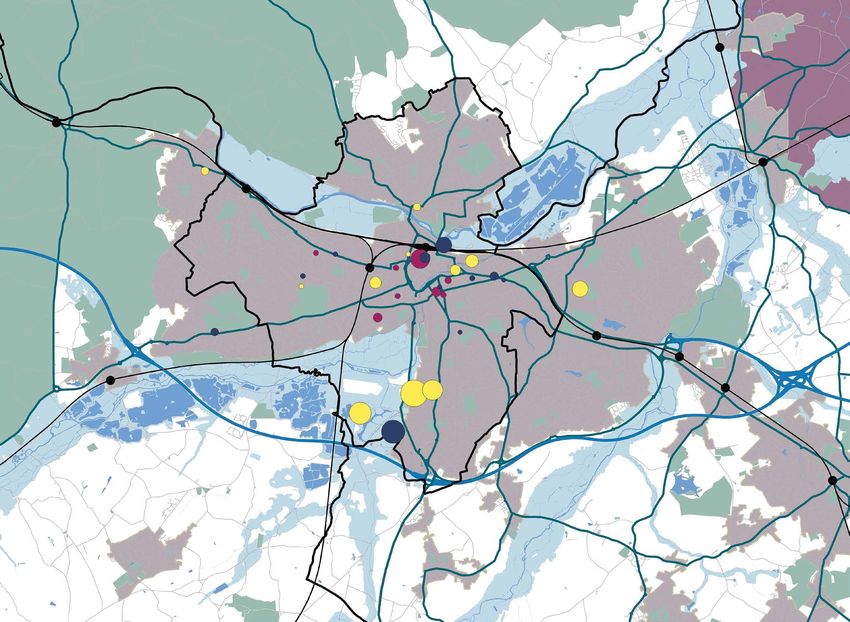

Beyond the boundaries There is the potential to deliver more than 20,000 homes in

and around Reading, but it means working collaboratively with neighbouring authorities

South Oxfordshire Emmer Green

and Playhatch

250

homes

Reading

Theale

and Calcot

300

Whitley

homes

2,000+ 450

homes homes

Winnersh

South of the

M4 area

West Berkshire Grazeley* 15,000 3,000

homes* homes Wokingham

Key AONBs and open green space Green belt Flood risk area Surface water area A and B roads

Motorways Key rail stations * Proposed Under construction Detailed consent In planning

Number of homes 200 400 600 800 1000 Planned and/or consented homes

Source Savills Research

Locating new land for new homes areas could provide 5,000 more homes Most of these areas cross into

To grow into a city, Reading needs more in the area. A further three smaller sites; neighbouring districts. Although West

space – not just urban sites, but also to Emmer Green & Playhatch, Theale and Berkshire, Wokingham and Reading

expand outwards. However, the district Calcot and Winnersh have sites for 1,000 have enough land in their five year land

of Reading is constrained by flooding risk to the north, west and east of the town. supply, South Oxfordshire does not. This

and areas of outstanding natural beauty Grazeley is a proposed garden district can work with Reading to provide

(AONBs). If it is to deliver significantly more settlement which could accommodate up homes to the north of the town subject to

homes, Reading needs to look beyond to 15,000 homes to the south of Reading. significant infrastructure improvements.

its boundaries. This means working with It is at a very early planning stage and, To unlock large-scale development north

neighbouring authorities. if progressed, is a potential option for of Reading, new or improved transport

There are two key areas for the meeting the housing needs of the West links will be needed. Areas to the south

development of new homes: Whitley and of Berkshire Planning authorities that can access the M4, but the congestion

South of the M4 area (which includes comprise Wokingham Borough, West on the A34 into Reading will need to be

Shinfield Meadows). Between them, these Berkshire and Reading Borough Councils. resolved to accommodate the new growth.

savills.co.uk/research 7Reading in numbers

9x 1/3 £33.50psf

Price of the average Reading house The proportion Average grade A rent

compared with average annual earnings of private rental

households in

Reading. This is 79,400

34% 93% well above the Number of

The proportion of The proportion national average office-based

new build housing of first-time employees

delivered through buyers that have 5,000

office to residential

conversions in the

used Help to Buy

since it was

Number of new 3rd

homes being built Reading is in the

year to March 2016 introduced at two sites on the top three UK cities

outskirts of Reading for both IT and B2B

– Whitley and South

£64,076 of the M4 area

sector investment,

since 2012

Gross value added (GVA) per employee

in Reading. For Bristol, Birmingham

and Manchester, GVA is £52,860, £322,000 £640m

£49,463 and £47,487, respectively The average house Office investment

price in Reading volume in 2016

Savills development We provide bespoke services for landowners, developers, occupiers and investors

across the lifecycle of residential, commercial or mixed-use projects. We add value by providing our clients

with research-backed advice and consultancy through our market-leading global research team

Research

Lucy Greenwood Jacqui Daly Simon Preece Steve Lang

Residential Research Residential Research Commercial Research Commercial Research

020 7016 3882 020 7016 3779 020 7409 8768 020 7409 8738

lgreenwood@savills.com jdaly@savills.com spreece@savills.com slang@savills.com

Reading office

Phil Brown Rebecca McAllister Ed Keeling Abby Malton Andrew Cox Jon Gardiner

Head of Office Head of Planning Head of Development Head of Residential Account Manager Office Agency

(Planning) 01189 520 534 01189 520 507 Development Sales (Estates team) (Greater London & South East)

01189 520 506 rmcallister@savills.com ekeeling@savills.com 01189 520 523 01189 520 512 020 7409 8828

pbrown@savills.com amalton@savills.com akcox@savills.com jgardiner@savills.com

Savills plc: Savills is a leading global real estate service provider listed on the London Stock Exchange. The company was established in 1855 and has a rich heritage with unrivalled

growth. It is a company that leads rather than follows, and now has more than 700 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted, in part or in whole, nor may it be used as a basis for any contract, prospectus,

agreement or other document without prior consent. While every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss

arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.You can also read