Q1 2022 Economic and Market Outlook: Years in Weeks

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Cerity Partners Market & Economic Update

March 17, 2022

Q1 2022 Economic and

Market Outlook:

Years in Weeks

Presented by:

Benjamin A. Pace, III James Lebenthal, CFA Thomas Cohn, CFA

Chief Investment Officer Chief Equity Strategist Deputy Chief Investment Officer

Key Themes for the 2022 Short Term Themes 1. U.S. consumers strength tested by higher commodity prices 2. Cyclical Stocks Make a Second Comeback 3. Expect Moderate Stock Returns With Higher Volatility 4. No Breakout in Interest Rates (DESPITE the FED in Tightening Mode) 5. Labor Markets Heal 6. Supply Chain issues SLOWLY dissipate, and Inflation GRADUALLY Normalizes 7. China Is No Longer the Driver of World Economic Growth Long Term Themes 1. Continued Financial Repression Necessitates a Never-ending Search for Yield (Watch Real Yields) 2. Transition Towards Clean Energy/ ESG Driver in the Commodity Markets (demand and supply) 2

Kickstarting 2022

The market has been discounting speculative assets for over a year.

January & February 2021 February 2021 Through March 3rd, 2022

40% 20% 16.17% 15.32%

35.00% 11.00%

35% 10%

30%

0%

25%

-10% -6.67%

20%

-20%

15%

11.35%

-30%

10% -30.33%

5.00% 4.92% 5.69% -34.93%

4.72% -40%

5%

1.70%

-43.07%

0% -50%

-51.07%

-0.82%

-5% -60%

iShares Core iShares iShares iShares ARK Defiance Grayscale iShares iShares Core iShares iShares iShares ARK Defiance Grayscale iShares

S&P 500 ETF Russell 1000 Russell 1000 Russell 2000 Innov ation Next Gen Bitcoin Trust China Large- S&P 500 ETF Russell 1000 Russell 1000 Russell 2000 Innov ation Next Gen Bitcoin Trust China Large-

Growth ETF Value ETF ETF ETF SPAC (BTC) Cap ETF Growth ETF Value ETF ETF ETF SPAC (BTC) Cap ETF

Derived ETF Derived ETF

3 Source: Factset

Uptick in Volatility

Uncertainty has reasserted itself in 2022.

The VIX The History of Recent Market Corrections

90

COVID 19 Pandemic

Global Financial Crisis Current Correction (51 Days) -11.91%

80

COVID Economic Shutdown (33 day s) -33.90%

70

Trade Wars/ Fed Pivot (95 day s) -19.80%

60 Fed

Pivot VIX Product Implosi on (13 days) -10.20%

Euro U.S. Treasury 2.0 /

Crisis Downgrade Russia

50 LTCM Enron China/Energy Invades Commodity Downcycle / HY Sel l-Off (100 days)

9/11 -13.30%

Asian Slowdown Ukraine

Fed

40 Financial Pivot

Crisis China Devaluation (96 Day s) -12.40%

30

U.S. Debt Downgrade (157 days) -19.40%

20

European Debt Crisis (70 days) -16.00%

10

Global Financial Crisis (517 days) -56.80%

0 -70% -60% -50% -40% -30% -20% -10% 0%

Oct-91 Feb-96 Jun-00 Oct-04 Feb-09 Jun-13 Oct-17 Feb-22

4 Source: Factset, Yardeni Research

Geopolitics to the Forefront

Russia’s invasion of Ukraine has become the biggest risk to the markets.

Russian Ruble to U.S. Dollar Geopolitical Events and the Markets

0.0150

0.0140

0.0130

0.0120

0.0110

0.0100

0.0090

0.0080

Mar-21 May-21 Jul-21 Sep-21 Nov-21 Jan-22 Mar-22

5 Source: Factset, LPLImpact to Global GDP

While fiscal policy is wearing off, pent-up demand plus excess savings translate into consumer spending fueling

GDP growth.

Three Ways to Impact the Global Economy Biggest Impact From Cutting Russia Off Will be on Commodites

Financial Risk spreads, valuations,

Markets banking system, contagion

risk, capital flows, currency

risk

Economic Trade flows, economic

disruption, supply side

Markets shocks

Geopolitical Long-term instability,

globalization, global

Structure

monetary system

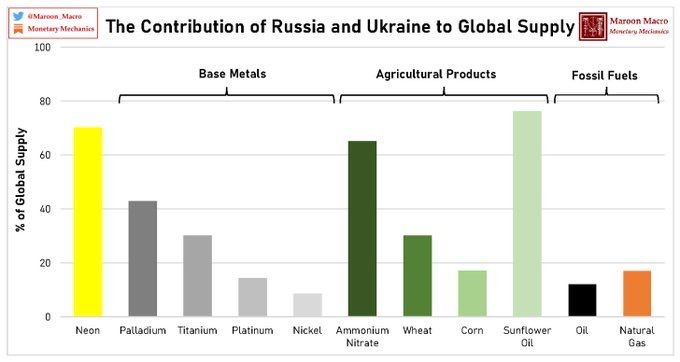

6 Source: Factset, Maroon MacroSupply Shocks Everywhere

Commodity prices are being forced upward by supply disruptions. War in Europe has further propped up

commodities.

Commodities Oil Industrial Metals

200 200 200

180

175 175

160

140

150 150

120

125 100 125

80

100 100

60

40

75 75

20

50 0 50

Dec-19 May-20 Sep-20 Jan-21 Jun-21 Oct-21 Mar-22 Dec-19 May-20 Sep-20 Jan-21 Jun-21 Oct-21 Mar-22 Dec-19 May-20 Sep-20 Jan-21 Jun-21 Oct-21 Mar-22

Bloomberg Commodity Index - Total Return Crude Oil WTI (NYM $/bbl) Continuous - Total Return Bloomberg Industrial Metals Subindex - Total Return

7 Source: FactsetBarometers of Risk

We are watching the bond and credit markets for signs of risk off.

Yield Curve Watch High Yield Spreads

3.5% 1,200

3.0%

1,000

2.5%

800

2.0%

1.5%

600

1.0%

400

0.5%

0.0% 200

-0.5%

0

-1.0% Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Mar-22

Mar-88 Jun-92 Sep-96 Dec-00 Mar-05 Jun-09 Sep-13 Dec-17 Mar-22 ICE BofA US High Yield - Spread - Spread to Worst

8 Source: FRED, FactsetTwo Economic Levers

We would expect both growth and inflation rates to decelerate in 2022.

Growth Inflation

70 7%

Mid Cycle Slowdowns

65

6%

60

5%

55

4%

50

3%

45

2%

40

1%

35

0%

30

Dec-96 Dec-99 Dec-02 Dec-05 Dec-08 Dec-11 Dec-14 Dec-17 Dec-20

Feb-97 Feb-00 Feb-03 Feb-06 Feb-09 Feb-12 Feb-15 Feb-18 Feb-21

Core CPI (Year over year %)

United States - ISM Manufacturi ng PMI

9 Source: Factset, FREDA New Wave

Expect a short-term impact on growth from Omicron.

Hospitalizations in the U.S. Seated Diners on the OpenTable Network

180,000 80%

160,000 60%

140,000 40%

120,000 20%

0%

100,000

-20%

80,000

-40%

60,000

-60%

40,000

-80%

20,000

-100%

0 Feb 18 May 24 Aug 28 Dec 02 Mar 08 Jun 12 Sep 16 Dec 21

Jul-20 Oct-20 Dec-20 Feb-21 May-21 Jul-21 Oct-21 Dec-21 Mar-22

United States 7 Day Average

Hospital Patients

10 Source: Our World in Data, OpenTableNever Underestimate the U.S. Consumer

While fiscal policy is wearing off, pent-up demand plus excess savings translate into consumer spending fueling

GDP growth.

U.S. Total Retail Sales The Goods vs. Services Recovery

$700 140

$650 130

122

120

$600

114

110

$550

100 100

$500

90

$450

80

$400

70

Dec-19 Apr-20 Aug-20 Dec-20 Apr-21 Aug-21

$350

Real Personal Consumption Expendi tures: Durable Goods

Real Personal Consumption Expendi tures: Services

$300

Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Real Personal Consumption Expendi tures: Nondurable Goods

11 Source: Factset, FREDThe Case for Investing

Capital expenditures and the housing market can contribute to GDP growth.

Capital Investment U.S. Housing Starts

20% 2,500

15%

2,000

10%

5%

1,500

0%

-5% 1,000

-10%

500

-15%

-20%

Sep-06 Mar-08 Sep-09 Mar-11 Sep-12 Mar-14 Sep-15 Mar-17 Sep-18 Mar-20 Sep-21 0

Real Gross Private Domestic Investment, Fi xed Investment, Nonresidential Dec-02 Sep-05 Jun-08 Mar-11 Dec-13 Sep-16 Jun-19

Real Gross Private Domestic Investment, Software New Privatel y Owned Housing Units Started (6 Months Average)

12 Source: FactsetWhat Is Causing the Supply Chain Bottlenecks?

Adverse Weather Can’t control and unknown

Labor Shortages Mix of permanent and temporary changes

Should fade in 2022 (depending on

Supply Restrictions

sanctions)

Demand Shifts (Services to Goods) Should fade in 2022

ESG Policy Could be permanent

13 Source: Capital EconomicsThe Choking of Supply Chains

Emerging signs that the supply chain pain has peaked.

New York Fed Global Supply Pressure Index Shipping Rates

5 $14,000

4 $12,000

3

$10,000

2

$8,000

1

$6,000

0

$4,000

-1

$2,000

-2

$0

Jan-20 Jun-20 Nov-20 Apr-21 Sep-21 Mar-22

-3

WCI Shanghai to Los Angeles Container Rate

Feb-98 Feb-01 Feb-04 Feb-07 Feb-10 Feb-13 Feb-16 Feb-19 Feb-22

14 Source: Federal Reserve Bank of New York Liberty Street Economics, BloombergSigns that Inflation Will Likely “Normalize” in the back of half 2022

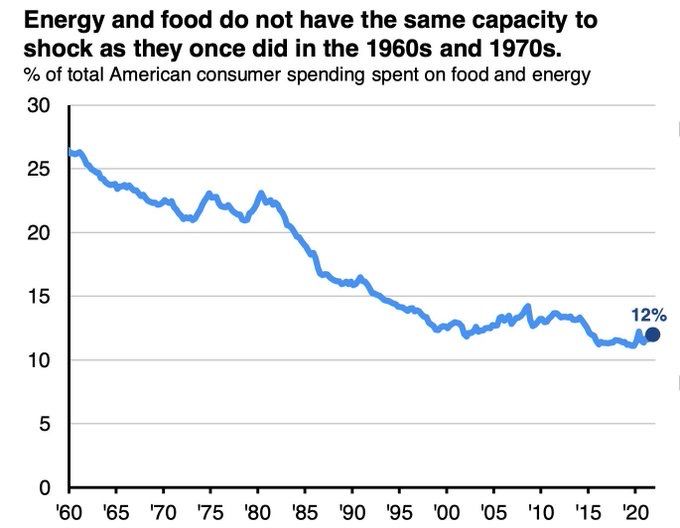

Core inflation will likely start to taper this year.

Energy & Food as a % of Total Spending Goods vs. Service Prices

12%

10%

8%

6%

4%

2%

0%

-2%

-4%

-6%

Nov-01 Nov-03 Nov-05 Nov-07 Nov-09 Nov-11 Nov-13 Nov-15 Nov-17 Nov-19 Nov-21

Consumer Price Index for All Urban Consumers: Durables

Consumer Price Index for All Urban Consumers: Services

15 Source: JPMorgan, FREDUnfreezing the Labor Markets

Don’t pay attention to the unemployment rate.

The Jobs Recovery Labor Force Participation Rate

68%

66%

64%

62%

60%

58%

56%

Dec-91 Dec-94 Dec-97 Dec-00 Dec-03 Dec-06 Dec-09 Dec-12 Dec-15 Dec-18 Dec-21

16 Source: Calculated Risk, FREDThe International Markets Discount

Europe’s proximity and energy exposure to Russia are likely to be headwinds to economic growth.

Forward P/E Ratios IMF Real GDP Forecasts

26x 8.0%

7.2%

24x 7.0% 6.7%

6.2%

22x 6.0% 5.8%

5.6%

20x 4.9%

5.0% 4.7%

18x 4.0%

4.0% 3.8% 3.8% 3.8%

3.5%

16x

3.0% 2.6% 2.7%

2.5%

2.2% 2.3%

14x

2.0% 1.8%

12x

1.0%

10x

Feb-20 May-20 Aug-20 Nov-20 Feb-21 May-21 Aug-21 Nov-21 Feb-22 0.0%

iShares Europe ETF - PE - NTM iShares MSCI Japan ETF - PE - NTM U.S. Germany France Italy Spain U.K

iShares Core S&P 500 ETF - PE - NTM 2021 2022 2023

17 Source: Factset, IMFNo Longer the Growth Engine

The regulatory actions in the education, housing, and health sectors are another headwind to Chinese

growth.

Real Chinese GDP Growth First In, First Out?

170

12%

10% 9.6% 150

7.8% 7.8% 8.0%

8% 7.4% 130

7.0% 6.9% 6.9%

6.8%

6.0%

6% 5.6% 110

5.3% 5.2% 5.1%

4% 90

2.3%

2%

70

0%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 50

Dec-19 Jul-20 Jan-21 Jul-21 Feb-22

Real GDP Growth IMF Forecast MSCI Chi na NR USD MSCI India NR USD MSCI EM NR USD

18 Source: Factset, Morningstar DirectThe Wrecking Ball?

The Fed tightening cycle can pressure asset markets, but usually after overtightening.

Fed Funds Rate Two Year Treasury Yield

7%

3.5%

6%

3.0%

5%

2.5%

4%

2.0%

3%

1.5%

2%

1.0%

1%

0.5%

0%

Dec-92 Dec-95 Dec-98 Dec-01 Dec-04 Dec-07 Dec-10 Dec-13 Dec-16 Dec-19 Dec-22

U.S. Federal Funds Target Rate Market Expecations 0.0%

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Mar-22

19 Source: JPM Guide to the Markets, FactsetCurrency Risks

The weaponization of the financial system has brought the dollar back into focus.

The Dollar Back in focus Alternative Store of Values?

105 110

105

100

100

95

95

90

85

90

80

85 75

70

31-Dec-2021 21-Jan-2022 11-Feb-2022 4-Mar-2022

80

Mar-17 Sep-17 Apr-18 Oct-18 May-19 Dec-19 Jun-20 Jan-21 Jul-21 Feb-22 Bitcoin (BTC/USD) - Price NY Gold (NYM $/ozt) - Price

20 Source: FactsetWall of Worry Risks are always present. They exist in balance with opportunities. Bricks In The Wall Climbing Gear • Geopolitical Risks • Fading Virus Impact • Supply Chain Bottlenecks • High & Growing Profits • Inflation • Supply Chain Onshoring • Interest Rates • Infrastructure Spending • Federal Reserve • Plentiful Jobs • Infrastructure & Taxes • Growing GDP • Social Discord • Fading Fiscal Policy Distortions • Political Disfunction • Fading Monetary Policy Distortions • Climate Change 21

Return to Normal What does that mean? 1. Lower Equity Market Returns than past ten years 2. Higher Volatility than last two years Normal is likely to not “feel good” after the recent past 22 Source: Factset

Do Not Try to Time a Correction . . . Or the Markets!

Note How Long the S&P 500 Stayed Above the 200 Day Moving Average. Normal Volatility is reasserting

itself.

S&P 500 Performance of the S&P 500

Performance of a $10,000 investment between January 1, 1999 and December 31, 2018

23 Source: Yahoo Finance, FactsetEquity Expectations for 2022: A Return to Normal

The last ten years has seen much better than average returns due to earnings multiple expansion.

S&P 500 Annualized Returns

1 Year 3 Year 5 Year 10 Year 20 Year

15.76% 20.08% 16.22% 15.08% 9.17%

Note This

Corrective Decline

24 Source: Yardeni ResearchEarnings are the Lifeblood of the Stock Market Earnings Are Still Being Revised Higher As Of March 10th S&P 500 Operating Earnings per Share 25

Earnings are the Lifeblood of the Stock Market Earnings Are Still Being Revised Higher As Of March 10th S&P 500 Earnings per share Forecasts 26 Source: I/B/E/S data by Refinitiv

Why are Earnings Estimates Not Declining?

Because Demand is Hanging In

TSA Traveler Count - Trailing 12 Months

Number of Dai ly Travellers % of 2019 Level 14 per. Mov. Avg. (Number of Daily Travellers)

2,750,000 140.0%

2,550,000

120.0%

2,350,000

2,150,000 100.0%

1,950,000

80.0%

1,750,000

60.0%

1,550,000

1,350,000 40.0%

1,150,000

No let up in demand for air travel 20.0%

950,000

despite Russia-Ukraine.

750,000 0.0%

3/14/2021 4/14/2021 5/14/2021 6/14/2021 7/14/2021 8/14/2021 9/14/2021 10/14/2021 11/14/2021 12/14/2021 1/14/2022 2/14/2022

27Why are Earnings Estimates Not Declining? Because Demand is Hanging In Las Vegas Strip – Recent RevPAR Trends 28 Source: Company reports at J.P. Morgan

Anecdotally, things look pretty good here in the U.S. Some will say Europe is in recession, but the US matters more. 29

Stock Market Valuation Has Come In May 17, 2017 – March 14, 2022 SPDR S&P 500 ETF Trust (SPY-US) 30

Fundamentals of Four Overweighted Sectors in R1000 Value

Financials

• Yield curve rises and steepens as Fed tapers: helps banks’ net interest margins

• Improving economy reduces loan losses and promotes loan growth

• Share buybacks increase earnings per share

Energy

• OPEC+ is behaving rationally

• Demand for fossil fuel picks up with economic expansion

• Renewable energy sources need fossil fuels during construction

Industrials

• Benefit from economic recovery

• Onshoring of supply chains over long term

• Infrastructure bill increases industrial activity

Materials

• Benefit from economic recovery, onshoring of supply chains, infrastructure, clean energy buildout

31 Source: FactsetWhat Would We Avoid? 10-Year Treasury Yield has a large effect on startup companies due to discounting of cash flow. 32

What Areas of the Market Are We Neutral On?

Large Cap Growth-At-A-Reasonable-Price Tech (i.e. FAANGMA) Will Grow at the Rate of EPS Growth

Aspirational Earnings Aspirational Earnings

33 Source: FactsetWhat Areas of the Market Are We Neutral On?

Large Cap Growth-At-A-Reasonable-Price Tech (i.e. FAANGMA) Will Grow at the Rate of EPS Growth

Apple Shares at Fiscal Year End

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Forward P/E 12.6 14.6 11.5 21.6 32.4 30.2 28.3 26.0 25.2

E.P.S. $2.08 $2.30 $2.98 $2.97 $3.28 $5.61 $5.74 $6.24 $6.45

E.P.S. Growth Rate 10.58% 29.57% -0.34% 10.44% 71.04% 2.32% 8.71% 3.37%

3-Year Compound Annual Growth Rate 23.48%

5-Year Compound Annual Growth Rate 21.95%

Forward 1-Year Compound Annual Growth Rate 2.32%

Forward 3-Year Compound Annual Growth Rate 4.76%

Microsoft Shares at Fiscal Year End

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Forward P/E 17.8 20.8 24.4 26.3 33.1 33.2 32.2 28.1 23.9

E.P.S. $2.10 $2.71 $2.13 $5.06 $5.76 $8.05 $9.19 $10.55 $12.37

E.P.S. Growth Rate 29.05% -21.40% 137.56% 13.83% 39.76% 14.16% 14.80% 17.25%

3-Year Compound Annual Growth Rate 55.77%

5-Year Compound Annual Growth Rate 30.83%

Forward 1-Year Compound Annual Growth Rate 14.16%

Forward 3-Year Compound Annual Growth Rate 15.40%

34 Source: FactsetProfits & Multiples

Earnings growth is likely to be the primary driver of returns in 2022.

Breaking Down S&P 500 Annual Returns

60%

50%

40%

30%

49%

20%

28% 30%

10% 21%

9%

0% 1%

-14%

-10% -22%

-27%

-20%

-30%

-40%

2018 2019 2020 2021 2022 (estimated)

EPS Mult iples

35 Source: FactsetImportant Notes Cerity Partners LLC (“Cerity Partners”) is an SEC-registered investment adviser with offices in California, Colorado, Illinois, Michigan, New York, Ohio and Texas. Registration of an Investment Adviser does not imply any level of skill or training. This commentary is limited to general information about Cerity Partners’ services and its financial market outlook, which may not be suitable for everyone. The information contained herein should not be construed as personalized investment, tax or legal advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this commentary will come to pass. Investing in the financial markets involves risk, including the risk of loss of the principal amount invested; and may not be appropriate for everyone. Please note that any benchmark or financial instrument performance shown is purely for illustrative purposes and does reflect a measure of the performance of an actual portfolio. Benchmark(s) are unmanaged, and the figures for the index shown include reinvestment of all dividends and capital gain distributions and do not reflect any fees or expenses. Investors cannot invest directly in a benchmark. Any forward-looking market data is not guaranteed and is subject to change without notice based on changing market and economic conditions. Cerity Partners’ advisory fee as well as taxes, custodial costs, and underlying investment expenses reduce any performance materially. Certain information contained in this letter may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. No forward looking statements made in this presentation are a guarantee of future performance or market events. The information presented is subject to change without notice and should not be considered as an offer to sell or a solicitation of an offer to buy any security. All information is deemed reliable but is not guaranteed. For information pertaining to the registration status of Cerity Partners, please contact us or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Cerity Partners, including fees and services, send for our disclosure statement as set forth on Form ADV Part 2A using the contact information herein. Please read the disclosure statement carefully before you invest or send money. ©2022 Cerity Partners LLC, an SEC-registered investment adviser. All Rights Reserved. 14678470 (03/22) 36

You can also read