PPP 2.0 & Stimulus Update - January 7, 2021 Date Mark Ferm - Tronconi Segarra & Associates

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Mark Ferm

Partner

Date

SOLUTIONS BEYOND

THE OBVIOUS

PPP 2.0 & Stimulus Update

January 7, 2021

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLP

Notices

This publication has been prepared for general guidance on matters of interest only; it does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy of completeness of the information

contained in this publication; and, to the extent permitted by law, Tronconi Segarra &

Associates LLP, its members, employees and agents do not accept or assume any liability,

responsibility or duty of care for any consequences of you or anyone else acting, or

refraining to act, in reliance on the information contained in this website or for any decision

based on it.

Copyright 2020 Tronconi Segarra & Associates. All rights reserved.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLP

Today’s Presenters

Thomas E. Mazurek, Jr., CPA Charles P. Pezzino, CPA Daniel A. Spada, CPA

Partner Partner Principal

tmazurek@tsacpa.com cpezzino@tsacpa.com dspada@tsacpa.com

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLP

Agenda

Stimulus Update

Paycheck Protection Program

Employee Retention Tax Credit

Targeted EIDL Advances

Q&A

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLP

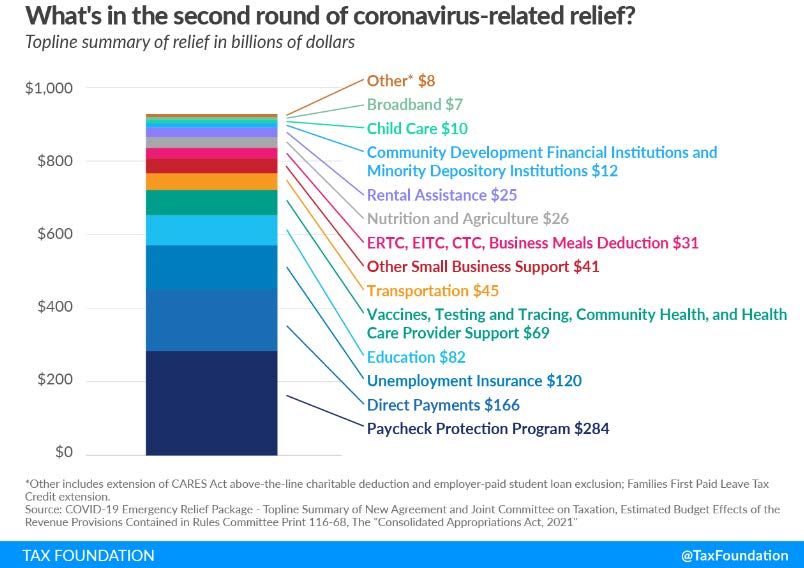

Stimulus Update

$41 billion includes: Targeted EIDL

Grants, Shuttered Venue Operator

Grants, SBA Debt Relief, Enhancements

to SBA lending

Stimulus Update

Emergency rental assistance

The CAA, 2021 provides $25 billion for emergency rental assistance

Extends the CDC’s eviction moratorium until Jan. 31, 2021

Eligible renters will be able to receive assistance with rent and

utility payments, unpaid rent or utility bills that have accumulated

since the beginning of the pandemic

Renters will apply for assistance with entities that state and

local grantees selected to administer the program

Once a renter qualifies for assistance, the administering entity

will send the payment directly to the landlord

Property owners can also assist renters to apply for rental

assistance under the program or apply on behalf of the

tenant

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLP

Stimulus Update

Emergency rental assistance

An “eligible household” is defined as a renter household in which at

least one or more individuals meets the following criteria:

1. Qualifies for unemployment or has experienced a reduction in

household income, incurred significant costs, or experienced a

financial hardship due to COVID-19;

2. Demonstrates a risk of experiencing homelessness or housing

instability; and

3. Has a household income at or below 80% of the area median

income (AMI)

* Eligible households may receive up to 12 months of assistance, plus an

additional 3 months if the grantee determines the extra months are needed

to ensure housing stability and grantee funds are available

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPStimulus Update

Direct payments

On Dec. 29, 2020, the IRS and the Treasury Dept. began delivering the

second round of Economic Impact Payments to millions of Americans

who received the first round of payments earlier this year

The initial direct deposit payments began arriving on Dec. 29 for

some and continued into this week

Paper checks began to be mailed on Dec. 30

The IRS emphasizes that there is no action required by eligible

individuals to receive this second payment

Eligible individuals who did not receive an Economic Impact

Payment this year – either the first or the second payment – will be

able to claim it when they file their 2020 taxes in 2021

People can check the status of both their first and second payments by using

the IRS Get My Payment tool

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPStimulus Update

Eligible PPP expenses now deductible

On Jan. 6, 2021, the Treasury Dept. and IRS issued new guidance

allowing deductions for the payments of eligible expenses when such

payments would result (or be expected to result) in the forgiveness of a

PPP loan

Revenue Ruling 2021-02 reflects changes to law contained in the

COVID-related Tax Relief Act of 2020, enacted as part of the

Consolidated Appropriations Act, 2021

No deduction is denied, no tax attribute is reduced and no basis

increase is denied by reason of the exclusion from gross income of

the forgiveness of an eligible recipient's covered loan

Rev. Rul. 2021-02 makes obsoletes Notice 2020-32 and Rev. Rul.

2020-27

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

New guidance

Interim Final Rule (Jan. 6, 2021)

Business Loan Program Temporary Changes: Extension of and Changes

to Paycheck Protection Program “Consolidated First Draw PPP IFR”

Restates existing regulatory provisions to provide lenders and new

PPP borrowers a single regulation to consult on borrower eligibility,

lender eligibility, and loan application and origination requirements

issues for new First Draw PPP loans, as well as general rules relating

to First Draw PPP Loan increases and loan forgiveness.

This rule is not intended to substantively alter or affect PPP rules

that were not amended by the Economic Aid Act.

Additional rules related to second draw PPP loans will be published

separately, and SBA intends to issue a consolidated rule governing all

aspects of loan forgiveness and the loan review process as well.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

New guidance

Interim Final Rule (Jan. 6, 2021)

Business Loan Program Temporary Changes: Paycheck Protection

Program Second Draw Loans

This IFR applies to loan applications and applications for loan

forgiveness submitted for PPP Second Draw Loans

The key differences between First Draw PPP Loans and Second Draw

PPP Loans are described in this IFR, which explains the loan terms,

eligibility requirements, and application process for Second Draw

PPP Loans.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

New guidance

Interim Final Rule - Paycheck Protection Program Second Draw Loans

Second Draw PPP Loans are generally subject to the same terms,

conditions and requirements as First Draw PPP Loans.

The IFR provides that a borrower that was in operation in all four

quarters of 2019 is deemed to have experienced the required

revenue reduction if it experienced a reduction in annual receipts of

25% or greater in 2020 compared to 2019 and the borrower submits

copies of its annual tax forms substantiating the revenue decline.

This method will be particularly important for small borrowers

that may not have quarterly revenue information readily

available.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

New guidance

Interim Final Rule - Paycheck Protection Program Second Draw Loans

Second Draw PPP Loan application and documentation requirements:

The documentation required to substantiate an applicant’s payroll

cost calculations is generally the same as documentation required

for First Draw PPP Loans.

However, no additional documentation to substantiate payroll costs

will be required if the applicant:

i. used calendar year 2019 figures to determine its First Draw PPP Loan

amount,

ii. used calendar year 2019 figures to determine its Second Draw PPP

Loan amount (instead of calendar year 2020), and

iii. the lender for the applicant’s Second Draw PPP Loan is the same as

the lender that made the applicant’s First Draw PPP Loan.

In such cases, additional documentation is not required because the lender already has the

relevant documentation supporting the borrower’s payroll costs.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

New guidance

Interim Final Rule - Paycheck Protection Program Second Draw Loans

Second Draw PPP Loan application and documentation requirements:

For loans with a principal amount greater than $150,000, the

applicant must also submit documentation adequate to establish

that the applicant experienced a revenue reduction of 25% or

greater in 2020 relative to 2019.

Such documentation may include relevant tax forms, including

annual tax forms, or, if relevant tax forms are not available,

quarterly financial statements or bank statements.

For loans with a principal amount of $150,000 or less, such

documentation is not required at the time the borrower submits its

application for a loan, but must be submitted on or before the date

the borrower applies for loan forgiveness, as required under the

Economic Aid Act.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

Comparison between PPP 1.0 and 2.0

PPP 1.0 PPP 2.0

Any business concern, certain nonprofit Any business concern, certain nonprofit

organizations, veterans organizations, organizations, housing cooperatives,

tribal businesses, eligible self-employed veterans organizations, tribal businesses,

individuals, sole proprietors, eligible self-employed individuals, sole

independent contractors or small proprietors, independent contractors or

agricultural cooperatives that: small agricultural cooperatives that:

Was in operation on Feb. 15, 2020; Was in operation on Feb. 15, 2020;

Eligible

Employs not more than 500 Employs not more than 300

Borrowers

employees or meets SBA size employees;

standards Have used or will use the full

Expanded to include 501(C)(6) amount of their first PPP loan;

organizations and housing Experienced a 25% reduction in

cooperatives with less than 300 gross receipts in any quarter of

employees, certain news 2020 compared to the same

organizations quarter in 2019

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

Comparison between PPP 1.0 and 2.0

PPP 1.0 PPP 2.0

The Maximum amount of a covered loan The Maximum amount of a covered loan

made to an eligible entity is the lesser of: made to an eligible entity is the lesser of:

2.5 times the average total 2.5 times the average total

Maximum monthly payroll costs incurred or monthly payroll costs incurred or

Loan paid by the eligible entity during paid by the eligible entity during

Amount calendar year 2019 either (1) the 1-year period before

$10,000,000 the date on which the loan is

made or (2) calendar year 2019

$2,000,000

The maximum amount of a covered loan for eligible entities with a NAICS codes starting with

72 (accommodation and food services) is 3.5 times the average monthly payroll costs

Seasonal employers can use any 12-week period between Feb. 15, 2019 - Feb. 15, 2020

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

Comparison between PPP 1.0 and 2.0

PPP 1.0 PPP 2.0

Either the 24 week period beginning on Begins on the date of the origination of a

the PPP loan disbursement date or if the covered loan ands ends on a date

borrower received its PPP loan before selected by the Borrower that occurs

Covered

Jun. 5, 2020, may elect to use 8 week during the period beginning 8 weeks and

Period

period ending 24 weeks after the date of

origination of the covered loan

Covered period for all PPP loans

extends thru Mar. 31, 2021

Payroll costs – salary/wages, employee Same Payroll costs as 1.0 plus group life,

benefits, state and local taxes assessed on disability, vision or dental insurance

compensation

Allowable Same Nonpayroll costs as 1.0 plus:

Uses of Nonpayroll costs – covered mortgage Covered operation expenditures

PPP Funds interest, rent, utilities Covered property damage costs

Covered supplier costs

Covered worker protection

expenditures

60/40 allocation between payroll and nonpayroll costs continues to apply

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPaycheck Protection Program

Good faith certification

An eligible recipient applying for a covered loan is still required to

make a good faith certification:

That the uncertainty of current economic conditions makes

necessary the loan request to support the ongoing operations of

the eligible recipient

Acknowledging that funds will be used to retain workers and

maintain payroll or make mortgage payments, lease payments,

and utility payments

The CAA has not updated the above certification to

include newly eligible costs

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPEmployee Retention Tax Credit

Comparison between CARES Act and CAA

CARES Act CAA, 2021

Applicable Time Period Qualified wages paid after Mar. 12, Qualified wages paid after Mar. 12, 2020

Credit is Available 2020 and before Jan. 1, 2021 and before Jul. 1, 2021

Effective Jan. 1, 2021, Businesses with

Businesses with operations that operations that were either (1) fully or

were either (1) fully or partially partially suspended by a COVID-19

suspended by a COVID-19 governmental order or (2) gross receipts

Eligibility

governmental order or (2) gross declined by 20% compared to gross

Requirements

receipts declined by 50% compared receipts in the same quarter in 2019

to gross receipts in the same (also provides safe harbor in which

quarter in 2019 business can use prior-quarter gross

receipts to qualify for the credit)

50% of qualified wages paid to Effective Jan. 1, 2021, 70% of qualified

Percentage

employee plus cost of health wages paid to employee plus cost of

of Wages

benefits health benefits

Effective Jan. 1, 2021, capped at $7,000

Maximum Credit Capped at $5,000 per employee per employee ($10,000 x 70%) for each

Amount ($10,000 x 50%) annually of the first 2 quarters of 2021 (possible

$14,000 credit per employee)

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPEmployee Retention Tax Credit

Comparison between CARES Act and CAA

CARES Act CAA, 2021

Businesses > 100 employees cannot

Effective Jan. 1, 2021, the threshold

take the credit for wages paid to

increases to 500 employees

employees performing services

Employer Size – whether

(even at reduced capacity)

employee is working or An employer < 500 employees will

Businesses < 100 employees can

not now be eligible to claim the credit,

take the credit for wages paid to

even if employees are performing

employees performing services or

services

employees who are not working

For 2021, the IRS is expected to

draft guidance to allow an advance

For 2020, there were no provisions payment of the credit for

Advance Payments to receive credit before qualified businesses with < 500 employees,

wages were paid based on 70% of the avg. quarterly

payroll for the same quarter in

2019

Limitations on The credit is allowed for hazardous

No credit for pay rate increases

Hazard Pay duty pay increases

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPEmployee Retention Tax Credit

Retroactive changes

Clarifies that group health care plan expenses can be considered “qualified

wages” even when no other wages are paid to the employees

Clarifies the determination of gross receipts for certain tax-exempt

organizations by reference to section 6033 of the IRC

Provides that businesses who received a PPP loan in 2020, and who are

otherwise eligible, should be able to file amended employment tax returns to

claim the ERTC with respect to qualified wages paid in excess of the amount

that were paid with a forgiven PPP loan (no double dipping)

The IRS is expected to issue guidance on how to claim the credit retroactively

on the fourth quarter Form 941 (due Feb. 1, 2021) or by filing amended returns

later

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPEmployee Retention Tax Credit

Significant decline in gross receipts (2020)

A significant decline in gross receipts begins:

on the first day of the first calendar quarter of 2020

for which an employer’s gross receipts are less than 50% of its gross

receipts

for the same calendar quarter in 2019.

The significant decline in gross receipts ends:

on the first day of the first calendar quarter following the calendar

quarter

in which gross receipts are more than of 80% of its gross receipts

for the same calendar quarter in 2019.

The credit applies to qualified wages (including certain health plan expenses) paid during this

period or any calendar quarter in which operations were suspended

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPTargeted EIDL Advances

Eligible applicants

Eligible applicants include:

Businesses, cooperatives or agricultural enterprises with 300 or

fewer employees, most private nonprofits, faith-based

organizations, sole proprietors, independent contractors or

businesses defined as small per SBA size standards;

Suffered an economic loss of greater than 30%;

Gross receipts must have declined at least 30% during an

8-week period between Mar. 2, 2020 – Dec. 31, 2021,

relative to a comparable 8-week period immediately

preceding Mar. 2, 2020, or during 2019; and

Located in a low-income community as defined for the new

markets tax credit (NMTC) in section 45D(e) of the IRC

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPTargeted EIDL Advances

Eligible applicants

The term “low-income community” means any population census

tract if —

A. the poverty rate for such tract is at least 20%, or

B. (i) in the case of a tract not located within a metropolitan

area, the median family income for such tract does not

exceed 80% of statewide median family income, or

(ii) in the case of a tract located within a metropolitan area,

the median family income for such tract does not exceed

80% of the greater of statewide median family income or the

metropolitan area median family income

Use the CIMS mapping tool to search by address, census tract or

other geographic area of interest to determine program eligibility

for NMTC

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPTargeted EIDL Advances

Eligible applicants

Also permits eligible small businesses in low-income communities

that previously received an EIDL advance under the CARES Act to

receive additional funds, up to $10,000

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPStimulus Relief

Example

Central Perk is a coffee shop and retailer located in Buffalo, NY. It’s business has

been negatively impacted by the pandemic, including restrictions imposed by

New York State

Year Q1 Q2 Q3 Q4 Total

2019 250,000 275,000 225,000 250,000 1,000,000

2020 250,000 100,000 125,000 125,000 600,000

2021 150,000 200,000

The business received a PPP loan for $62,500 in 2020 and has not yet

applied for forgiveness with its lender. The owner also spent $5,000 on PPE

and social distancing-related improvements in 2020.

The business received an EIDL advance (2020) for $4,000 (for 4 employees)

What new stimulus relief can Central Perk take advantage of in 2021?

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPPPP Loans

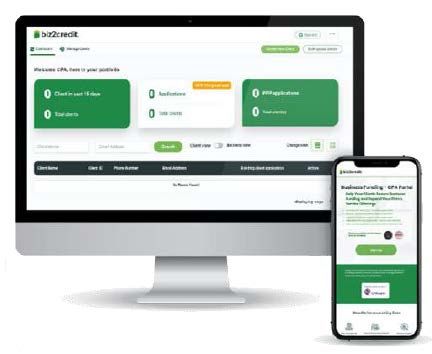

CPA Business Funding Portal

The AICPA, CPA.com and fintech leader Biz2Credit have launched a

platform for CPA firms, to help practitioners guide small businesses

through the PPP loan process, from applying for new PPP 2.0 loans to

calculating loan forgiveness, integrated with data imports for bank

statements and payroll and the latest PPP guidance from the AICPA

Tronconi Segarra & Associates LLP can provide

an end-to-end PPP solution for your business,

including:

Determine PPP 2.0 loan eligibility

Process loan application thru Biz2Credit

Prepare loan forgiveness application

Call 716.633.1373 or email us at COVID19team@tsacpa.com

for more information about these services

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPUpcoming Webinars

COVID-19 Panel of Experts:

Live Q&A with HR, Legal and Accounting

Thursday | Jan. 14, 2020 | 10am

Register

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPContact us

If you have additional questions:

Visit our COVID-19 Resource Center

https://www.tsacpa.com/coronavirus-covid-19-resource-center/

Email our Response Team

covid19team@tsacpa.com

Follow Tronconi Segarra & Associates on for updates on the latest COVID-19 developments

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPtsacpa.com

This publication has been prepared for general guidance on matters of interest only; it does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy of completeness of the information

contained in this publication; and, to the extent permitted by law, Tronconi Segarra &

Associates LLP, its members, employees and agents do not accept or assume any liability,

responsibility or duty of care for any consequences of you or anyone else acting, or

refraining to act, in reliance on the information contained in this website or for any decision

based on it.

Copyright 2020 Tronconi Segarra & Associates. All rights reserved.

SOLUTIONS BEYOND THE OBVIOUS PRESENTED BY TRONCONI SEGARRA & ASSOCIATES LLPYou can also read