Morning Comment - AFS Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Morning Comment March 11, 2021

Arne Petimezas • House Sends Aid Bill to Biden, Checks to U.S. Pocketbooks

Analyst • Biden says he will announce the ‘next phase’ of the U.S. Covid response Thursday

+31 20 522 0244 • Italy’s Salvini Hints at Time Limit for Draghi as Premier

a.petimezas@afsgroup.nl • ECB Draft Forecasts Assume Any Inflation Pickup Will Be Fleeting

• From Black Forest to Cologne, German towns fear Greensill losses

• Today’s ECB preview is divided in two parts. In the first part we briefly discuss the

economic and pandemic situation in the Eurozone before moving to the second

part: the meeting itself. We mostly discuss pandemic bond buying as other policy

tools are not in play at this point. In a nutshell regarding the economy and

pandemic, the light at the end of the tunnel is brighter for sure. Too bad that the

tunnel happens to be longer than feared. Regarding the bond market turmoil, we

think the ECB will continue to make half-hearted attempts at controlling yields. It

will be a mix of verbal interventions and pulling forward pandemic bond

purchases. However, the ECB will remain very much on track to undershoot its

purchase commitments.

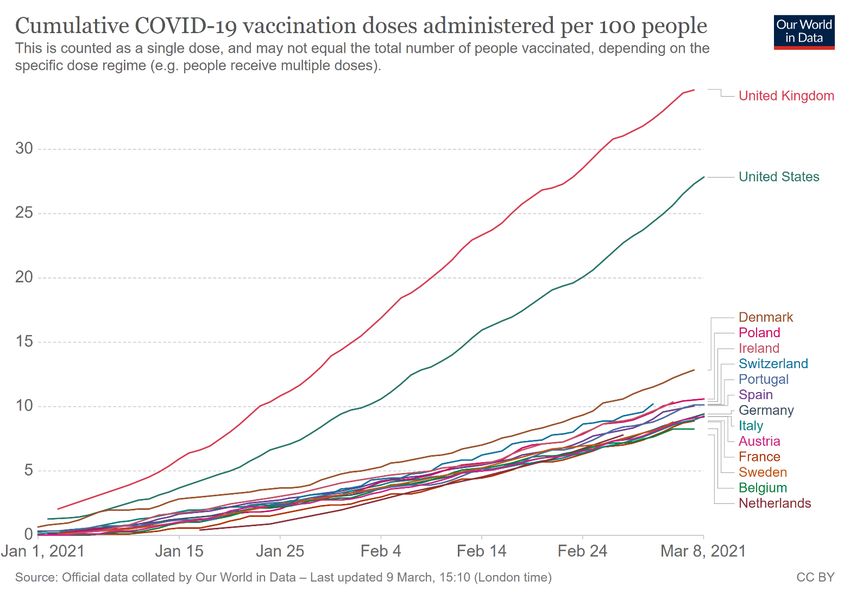

• The vaccination campaign in the EU remains a mess. Despite all our wealth and

(supposed) institutional prowess and – most important of all – buying prowess,

the USA and UK are walking away:

Page 1 of 11

• As things stand now, the EU will barely able to reach the target of inoculating

70% of all adults by August (200 million citizens). In the February 25 Comment we

estimated that, excluding the single shot Johnson & Johnson vaccine, EU nations

will have administered 336 million doses by mid-August. That’s 70 million short of

the target if the remainder is covered by the J&J vaccine. Earlier this week it was

reported that Johnson & Johnson will probably not meet its delivery target of 55

million doses for Q2. If the 55 million deliveries are stretched out to mid-August,

we will be close enough to the 400 million mark. But any more disruptions and the

target will have to be cut for the second time (the initial deadline was June).

• Lockdowns remain tight, despite a strong decrease in fatalities:

Page 2 of 11Note that the decline in fatalities is overstated in the sense that we still include

the UK, where the vaccination campaign is much more advanced than on any

country in the continent.

• Case growth remains persistently elevated in four of the biggest five countries in

the Euro Area. And even in Germany, where case growth is low, rules remain

tight:

Page 3 of 11Daily new cases per 100,000 inhabitants, 7-day moving average (geometric mean); ECDC limit = 25 / 100,000

(NE=Netherlands; DE=Germany; AT=Austria; BE=Belgium; FR=France; ES=Spain; PT=Portugal; DK=Denmark; GB=United Kingdom; IE=Ireland

CH=Switzerland; PL=Poland; SE=Sweden; CZ=Czech Republic; IT=Italy) ----------------------------------------------------------- Source: Johns Hopkins; AFS

Color scale: ≤ 5/100k green; 6-20/100k green/yellow; 21-100/100k yellow/red; >100/100k red

NE DE AT BE FR ES PT DK GB IE CH SE PL CZ IT

01/02/2021 24 13 16 20 28 93 110 9 35 16 26 43 13 58 20

02/02/2021 23 12 15 20 28 88 100 8 34 16 25 43 13 59 20

03/02/2021 23 12 15 20 28 84 93 8 32 15 24 43 13 58 19

04/02/2021 22 12 15 20 27 82 84 8 31 14 24 43 13 60 19

05/02/2021 22 12 15 20 30 77 77 8 29 17 23 46 13 60 19

06/02/2021 22 11 15 19 29 77 69 8 28 16 23 46 13 60 19

07/02/2021 23 11 15 19 29 77 60 8 27 15 23 46 13 62 19

08/02/2021 21 10 15 18 29 69 53 8 26 15 23 46 13 61 19

09/02/2021 19 10 15 18 28 62 48 7 25 14 22 44 13 62 20

10/02/2021 19 10 15 17 28 55 43 8 24 14 21 44 13 63 20

11/02/2021 19 9 15 17 28 50 38 7 22 13 20 45 13 63 20

12/02/2021 19 9 15 16 25 44 34 7 21 13 19 47 13 64 20

13/02/2021 19 9 16 16 25 44 30 7 20 13 19 47 13 64 20

14/02/2021 19 8 15 16 25 44 27 7 19 13 19 47 14 65 20

15/02/2021 19 8 16 16 25 40 25 7 18 13 18 47 14 66 20

16/02/2021 20 8 16 15 25 36 23 7 18 13 17 49 14 67 19

17/02/2021 21 8 16 15 25 33 21 7 18 12 17 49 15 69 19

18/02/2021 21 8 17 16 25 31 19 7 18 13 16 51 15 71 19

19/02/2021 21 8 17 17 26 30 18 7 17 12 16 52 16 74 19

20/02/2021 21 9 18 18 26 30 17 7 17 12 16 52 17 76 20

21/02/2021 22 9 19 18 27 30 16 8 16 12 16 52 17 79 20

22/02/2021 23 9 19 19 27 28 14 8 16 11 15 52 18 83 21

23/02/2021 25 9 19 20 27 26 13 8 16 11 16 54 19 86 22

24/02/2021 25 9 20 20 28 25 13 9 15 11 16 57 20 89 23

25/02/2021 26 9 20 21 29 23 12 9 15 10 16 57 21 92 24

26/02/2021 26 9 21 20 29 22 11 9 14 10 16 59 21 95 25

27/02/2021 26 9 22 20 29 22 10 9 14 10 16 59 22 99 26

28/02/2021 26 9 22 20 29 22 9 9 13 10 16 59 24 101 27

01/03/2021 26 9 22 19 28 21 9 9 12 10 16 59 24 103 28

02/03/2021 26 9 23 19 29 22 8 9 11 9 16 61 25 104 29

03/03/2021 27 9 24 19 28 20 8 9 10 9 16 63 26 105 30

04/03/2021 26 10 23 19 28 18 8 9 10 9 16 62 27 106 31

05/03/2021 26 9 24 19 28 17 7 9 9 8 16 62 28 106 31

06/03/2021 26 10 24 19 28 17 7 9 9 8 16 62 29 105 32

07/03/2021 26 10 25 19 28 17 7 9 9 8 16 62 30 107 33

08/03/2021 26 10 26 20 29 16 7 9 9 7 17 62 31 105 33

09/03/2021 26 10 27 20 29 14 8 9 9 7 17 61 32 102 34

• To conclude: the pandemic keeps dragging on. But what matters, is that pretty

much everyone – including the ECB – has this final countdown mentality. The

second wave, which started in the autumn of 2020 in case of Europe, will linger on

for a few more months. If the vaccines work as advertised and if natural immunity

lasts, there will be no third wave and associated shutdowns.

• This we-have-vanquished-the-pandemic-and-the-war-is-almost-over mentality is

reflected in business cycle survey data. The Markit PMIs suggest peak in our mini

technical recession will soon be over. The Euro Area economy will show an even

more moderate decline in Q1 following the 0.7% QoQ decline in Q4 GDP. Business

optimism is at its highest level in three years according to the PMI survey.

• The brighter outlook is reflected in economists’ forecast. On Tuesday the OECD

raised the Euro Area growth forecast for 2021 to 3.9% from 3.6%. A quick glance

at Bloomberg shows sell-side consensus has moved up to 4.2%. According to the

OECD, the latest demand boost comes from the spillover of the US stimulus

package justifies the forecast upgrade. As always, in true beggar-thy-neighbor

fashion, the Euro Area is piggy-backing on global demand. Chinese and US fiscal

Page 4 of 11stimulus is measured in high single digit percentage points of GDP. Ours is

measured in tenths of a percentage points of GDP.

• With commodity an producer prices rising at an increasingly rapid pace, we will

soon see said price increases filter through in consumer prices. Both headline

and core inflation will easily surpass 2% simply because of a mix of base effects

and demand being unleashed while there are still plenty of supply constraints. For

example, in January we witnessed a 1.5% spike in our index of core services prices,

which includes items that normally would be the least sensitive to price changes.

We also see the same sudden spike in the so-called index of supercore inflation,

which only includes items that are sensitive to the output gap:

• It’s hard to find proof of investors freaking out over inflation. Yes, market-based

measures of inflation compensation are in the rise. But optically, there is no new

regime because of the pandemic – no reflation. The improvements are purely

cyclical, which tragically will mean they will fool the ECB yet again. The charts

below show the 5y5y forward inflation-linked swap rate and the 1-month EONIA

forward 5 years, a proxy for the long term nominal neutral rate of interest.

Page 5 of 11• The declines in long-term inflation expectations perfectly track the cyclical

downswings (black and blue arrows) and upswings (red and green arrows) in

global growth. Post-pandemic, neither the speed of the advance nor the overall

level of inflation expectations are exceptional.

• Which brings us to ECB monetary policy. Starting with the Governing Council

statement, except Lagarde & Co to be a bit less downbeat on growth and inflation

then they were in January. In ECB language, downside risks to growth are still

stronger relatively speaking, but less so than they were at the start of the year.

Also expect the ECB to continue to look through the inflation bounce while being a

bit less worried about underlying price pressures. All in all, cosmetic changes only

that should not move markets in a meaningful way.

• There will be no policy changes and neither will the ECB have to decide on policy

measures in the near future. The TLTRO teaser rates lasts for a little while longer

(until June 2022 that is); the preliminary end date for pandemic QE is still some

time away (March 2022); regular QE of 20 billion euros a month remains on

autopilot indefinitely; and rate cut talk is just talk, and it will be less loud now that

the euro is a bit weaker.

• Where Lagarde will be tested, is how pandemic QE will be used to keep bond

yields in check. This is what we wrote in our January meeting post-mortem on

rising yields:

“If the ECB’s follows through on making purchase volumes flexible, things start to

get complicated. The pace of purchases will depend on what the ECB thinks what

interest rates should be in the context of how the pandemic and the economic

Page 6 of 11recovery unfolds. Confusing? It’s an open invitation for the market to test the ECB’s

resolve by pushing up interest rates, and see where the pain threshold lies.”

• Late last month we learned that Lagarde’s line in the sand was minus 30bps for

the 10y Bund, which translates to a real yield of minus 1.50 percent on the day

of her intervention. This begs the question: will there be a firm commitment to

keeping bond yields at or around a certain level under the threat of more bond

buying? We think not.

• As we explained in last Thursday’s Comment, most Governing Council members

are on board with fuzzy yield curve targeting. They want no explicit yield curve

control, which might very well mean the ECB can no longer control purchase

volumes. Instead, the ECB’s soft yield curve targeting consists of nothing more

than the same optical analysis of charts that we are very much guilty of. And

gauge where nominal and real bond yields are relative to their pre-pandemic level.

They will put some context around bond yield changes. Most importantly, if bond

yield increases are outpaced by rising inflation expectations, why should the ECB

intervene verbally or with more purchases? As a matter of fact, real yields did just

that over the past two weeks:

Note that ECB isn’t against increasing real yields per se. It just happens to be that

they want any increase to be slow and gradual. Under Draghi’s QE the 10y German

Page 7 of 11real yield traded below minus 1.0 percent most of the time. On the eve of the

pandemic it was at minus 1.5 percent.

• Furthermore, the increases in bond yields should not reflect an inordinate

amount of rate hikes being priced in too soon. The preliminary end date for

ending reinvestments of pandemic QE bonds is end 2023. It makes no sense to

price in hikes before that date1. So, keep an eye on EONIA forwards (or soon ESTR

forwards). The ECB should resist a rise in the 2-year and 3-year forwards:

• Finally, risk assets shouldn’t sell off and overall bond yields should remain

comfortably the rate of nominal GDP growth. Regarding the latter, no surprises

here as this has been the case for nearly a decade.

• Now, Lagarde will again speak of a “holistic approach” to (broad) financial

conditions, suggesting that there is some sophisticated and complicated

financial conditions index the ECB has concocted. But that’s all just smoke and

mirrors.

• The ECB will try to prevent inordinate increases in bond yields with verbal

interventions and by pulling forward pandemic bond purchases. Some hoped

that, given the upward pressure on yields, the ECB would have gone all in with

purchases. In reality, purchase volumes in recent weeks were below the post-

summer of 2020 average of 20 billion euros:

1

And the end date will be shifted out time and again, but that’s another story.

Page 8 of 11The takeaway: if the ECB can control yields with lower purchase volumes, that’s all

good to Lagarde & Co.

• At the current pace of purchases the ECB will have undershot its pandemic

purchase commitment of 1,850 billion euros by more than 100 billion euros by

March 2022. If the ECB were to boost purchase to combat rising yields, in the

future the ECB would lower purchase volumes at the first opportunity. We’re sure

the undershooting of the purchase commitment is very much intentional.

• So, the bottom line: no hard yield targets, just some vague idea where bond

yields should be relative to the overall economic conditions. Which means that

the target of pandemic QE – we can’t stress this enough – is not only a moving

target, it is also a fuzzy target. Also notice how the inflation mandate aspect has

been thrown completely out of the window.

• Unsurprisingly, even the ECB’s biggest cheerleaders are getting fed up with the

ECB’s unconstructive ambiguity. If the aim is to target financial conditions, why

not make the conditions more explicit and forget about pre-announced volume

commitments? And if the ECB finds its inflation target so important – which it still

is – why cut back on purchase volumes? We had a lot of schadenfreude when

Frederic Ducrozet of Pictet, who most of the time goes out of his way in praising

the ECB for this and that, accused the ECB of trolling. That triggered a response by

the former Vice President, Vitor Constancio, who was clearly annoyed :

Page 9 of 11• Finally, there is always the possibility that we’re completely wrong and that the

ECB has gotten its act together and will make a full-hearted attempt at reigning

in yields, but without going for explicit yield curve control. They could shift out

the preliminary end of pandemic QE by a quarter to June 2022. That would signal

the ECB will meet its purchase commitment after all. By definition they would

then also shift out the end date for reinvestments by a quarter or more. They

would add extra juice by committing to actually boost bond purchases when

needed. There would be strong language (‘committed to prevent an unwarranted

tightening’). However – and we know we are repeating ourselves here – we just

do not see such a thing happening. And even if there is such a dovish surprise

today, we will soon find out that the emperor has no clothes. Lagarde & Co will

allow higher yields at a later stage. And they will still weasel out of their purchase

commitments when possible.

• There is also the risk for another bone-headed hawkish surprise, such as the one

we witnessed in January. Such a surprises would mean the ECB walks further

away from its purchase commitment under pandemic QE.

Page 10 of 11TIME REGION EVENT PERIOD CONSENSUS PRIOR

10:00 South Afr. Current Account as a % GDP 4Q 4.00% 5.90%

10:00 South Afr. Current Account Balance 4Q 180b 297b

11:00 Ireland Sells Bonds

13:45 ECB Interest Rate Decision

13:45 Eurozone ECB Main Refinancing Rate Mar/11 0.00% 0.00%

13:45 Eurozone ECB Marginal Lending Facility Mar/11 0.25% 0.25%

13:45 Eurozone ECB Deposit Facility Rate Mar/11 -0.50% -0.50%

14:30 ECB President Christine Lagarde Holds Press Conference

14:30 US Initial Jobless Claims Mar/06 725k 745k

14:30 US Continuing Claims Feb/27 4200 4295k

16:00 US JOLTS Job Openings Jan 6650 6646

17:30 US Sells 4-Week; 8-Week Bills

19:00 US Sells 30-Year Notes

19:30 Bank of Canada Deputy Governor Schembri Gives Speech

Federal Reserve Weekly Balance Sheet

EMA expected to Approve J&J vaccine for EU

Consensus data: Bloomberg News; All Times Are in Central European Time

AFS GROUP AMSTERDAM

The AFS Morning Comment only summarizes recent market movements and contextualizes upcoming political, economic and central bank

events. Any views expressed in the AFS Morning Comment are limited in scope. Under Recital 29 and Article 12(3)(a) of the MiFID II

Delegated Directive, such publications are considered a minor non-monetary benefit which can be freely distributed without charge.

AFS Group does not accept any liability whatsoever for any direct or consequential loss arising from the use of this document. This

document is for information purposes only and is not, and should not be construed as, an offer to buy or sell any securities or derivatives.

The information contained in this document is published for the assistance of the recipient, but is not to be relied upon as authoritative or

taken in substitution for the exercise of judgement by any recipient.

Page 11 of 11You can also read