Middle East Real Estate Predictions - 2023 Dubai market review - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Middle East Real Estate Predictions 2023 Dubai market review

Middle East Real Estate Predictions | 2023

Contents

Executive summary 04

Dubai real estate market performance

Hospitality market 08

Residential market 10

Office market 12

Retail market 14

Industrial and logistics market 17

Key contacts 18

03

Middle East Real Estate Predictions | 2023

Executive summary

Dubai real estate market performance

Pent-up demand from travellers and increased spending by residents led the post-pandemic recovery of the real estate sector in

Dubai. Amidst global economic uncertainty and recessionary fears, Dubai’s status as a safe haven has attracted investors to the

market throughout 2022. However, inflation remains a concern for consumers and is expected to impact sentiment resulting in

price discovery and rent increases leading into 2023.

Hospitality

Occupancy for Dubai averaged 70% at the end of 2022, compared to the same period in 2021, while the average

ADR over this period has increased by 37% year-on-year to AED 641. This is higher than the majority of the

regional and international markets.

Residential

Average sales prices for residential property in Dubai increased by approximately 12% between Q3 2021 and

Q3 2022 to reach AED 1,203 per sq ft. Average rents also increased by approximately 19% over the same period,

rising to AED 73 per sq ft as as at the end of 2022. Gross yields reflect 6.1% compared to 5.7% in 2021.

Offices

Office rents have recovered to pre-pandemic levels registering an increase of 12% at the end of 2022 over the

same period.

04

Middle East Real Estate Predictions | 2023

Retail

Consumer spending growth fueled the retail sector recovery in both online and traditional mall formats. The

Economist Intelligence Unit (EIU) estimates that the total UAE retail sales volume will increase by approximately

4.2% in 2022, with sales expected to increase by 3.9% on average between 2023 to 2026.

Industrial and logistics

Average warehouse rents have continued to recover as demand from logistics companies remains buoyant and

freight movements at the airports surpass 2020 levels by 22% and 3% at Dubai International Airport (DXB) and

Dubai World Central (DWC) respectively.

05

Middle East Real Estate Predictions | 2023 Dubai real estate market performance 06

Middle East Real Estate Predictions | 2023

Hospitality market 08

Residential market 10

Office market 12

Retail market 14

Industrial and logistics market 17

07Dubai’s hospitality market

The hospitality market recovery strengthened during 2022 as key

performance indicators tracked higher than the previous year despite total

visitor numbers remaining below pre-pandemic levels.

Review of 2022 performance Dubai hotel performance percentage change, January 2021 to

Dubai welcomed 10.1 million overnight visitors in the first nine September 2021 vs January 2022 to September 2022

70

months of 2022, with the highest number of international guests

64%

arriving from India at 1.2 million and more than double the

60

number of visitors from Oman, KSA and the UK compared to

the previous year. International visitors are still lower than pre-

50

pandemic levels, with a total of 12.1 million visitors in Dubai during

Y-o-y% change from 2021

2019.

40

37%

The YTD September 2022 occupancy for Dubai averaged 70% 30

compared to 59% for the same period in 2021, while the average

ADR over this period has increased by 37% year-on-year to 20 20%

AED 641. This is higher than the majority of the regional and

international markets, as shown on the following page. 10

As seen in the adjacent graph, both ADR and occupancy improved 0

significantly from the previous year as a market-wide recovery Occupancy (%) ADR RevPAR

was supported by ease of travel and the lifting of capacity and

Source: Business Intelligence and Reporting (DTCM)

personal protective equipment (PPE) related restrictions. The

first three months of the year were the strongest for occupancy

performance, reaching 91% in March.

Dubai hotel market performance, January to September 2022

1,000

71% 91% 100%

59%

85%

80%

750 73%

ADR/RevPAR (AED)

63% 61% 69% 60%

64%

500

40%

250

20%

850

601

784

663

888

809

789

462

590

429

447

280

435

263

425

272

446

307

0 0%

January February March April May June July August September

ADR (AED) RevPAR (AED) Occupancy (%)

Source: STR Global

08Middle East Real Estate Predictions | 2023

Post-pandemic recovery UAE Tourism Strategy 2031

The YTD September 2022 data STR shows all performance metrics In mid-November 2022, His Highness Sheikh Mohammed bin

are tracking above 2019 levels with the exception of city-wide Rashid Al Maktoum launched the UAE Tourism Strategy 2031,

occupancy. In addition to international visitors, activity from which aims to strengthen the position of the UAE as one of the

residents has supported the recovery of the hospitality sector in best destinations in the world for tourism.

Dubai.

The goal is to boost the country’s competitiveness as an

ADRs are tracking 22.6% higher than 2019 levels, resulting in a international tourism destination by attracting AED 100 billion as

18% increase in revenue per available room (RevPAR) from 2019 additional tourism investments and welcoming 40 million hotel

levels. guests in 2031.

Data from the Department of Tourism and Commerce Marketing The strategy includes 25 initiatives and policies to support the

(DTCM) shows an increase in the average length of stay, which was development of the tourism sector in the country with a targeted

3.4 nights from January to September 2019 and has increased to gross domestic product (GDP) contribution of AED 450 billion in

4.0 nights over the same period in 2022. 2031, representing an annual increase of AED 27 billion.

Dubai ADR and occupancy vs regional markets, YTD September 2022

350 70% 70%

68%

300 62% 60%

Occupancy (%)

57% 52% 58%

250 47% 51% 50%

ADR (US$)

46%

200 44% 40%

150 38% 30%

100 20%

50 10%

104

140

125

175

214

169

107

169

97

88

75

0 0%

Abu Dhabi Amman Cairo & Casablanca Doha Dubai Jeddah Manama Muscat Riyadh Sharm el

Giza center Sheikh

ADR (US$) Occupancy (%)

Source: STR Global

Dubai ADR and occupancy vs international markets, YTD September 2022

65%

350 68% 70%

300 67% 60%

71% 55%

ADR/RevPAR (US$)

250 70% 50%

Occupancy (%)

60%

200 59% 62% 40%

63% 50%

150

51% 30%

45%

100 20%

50 10%

116

115

175

138

217

202

135

266

306

201

166

73

99

0 0%

Beijing Berlin Beunos Dubai Hong London Los Angeles Madrid New York Paris Rome Sydney Tokyo

Aires Kong

ADR (US$) Occupancy (%)

Source: STR Global

09Dubai’s residential market

Amidst global economic uncertainty and recessionary fears, Dubai’s status as

a safe haven has attracted investors during 2022, with transaction levels rising

year-on-year surpassing 2019 levels.

Review of 2022 performance Dubai ranging from 38% to 43% and Deira was the only location

Average sales prices for residential property in Dubai increased to record a decline of 5%. Transaction volumes have increased by

by approximately 12% between Q3 2021 and Q3 2022 to reach 56% YTD September 2022 when compared to the same period in

AED 1,203 per sq ft. Average rents have also increased by 2021 and have more than doubled from 2019 levels for the same

approximately 19% over the same period, rising to AED 73 per period. Secondary market properties constituted 55% of the total

sq ft as of September 2022. Gross yields reflect 6.1%, compared transactions in the first nine months of this year, with Business

to 5.7% in YTD September 2021 as rental growth has outpaced Bay, Dubai Marina and Jumeirah Village Circle recording the

growth in prices. highest number of transactions.

The average trend masks a much more varied sub-market picture The market continues to be dominated by cash buyers while

with Mohammed Bin Rashed City, Palm Jumeirah and Business demand for affordable villas and townhouses from existing

Bay being the top three sales price growth areas year-on-year residents has driven rental activity in this segment. Rents in this

against Dubai Land, Dubai South and Dubai Creek Harbour as category began to recover by the end of 2020, while the apartment

the locations with the highest price declines. By comparison, rent segment began to show signs of improved performance from the

increases were highest in Jumeirah, Palm Jumeirah and Downtown first half of 2021.

Dubai residential sales prices, Q1 2007 to Q3 2022

Lehman Bros. Last market Travel restrictions and

collapse peak lockdown measures

1,600

1,400

Price (AED per sq ft)

1,200

1,000

800

600

400

200

0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Villa Apartment Residential

Dubai residential rents, Q1 2009 to Q3 2022

Last market Travel restrictions and

peak lockdown measures

80

70

60

Rent (AED per sq ft)

50

40

30

20

10

0

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Villa Apartment Dubai average

Source: REIDIN

10Middle East Real Estate Predictions | 2023

Dubai residential sales prices by location, Q3 2022

Palm Jumeirah Villas

AED 4,831 47%

Dubai Marina

AED 1,536 5%

Palm Jumeirah Apartments

Jumeirah Lakes Towers AED 1,857 34%

AED 1,045 2%

Downtown

Dubai Sports AED 2,159 14%

City

AED 724 -1.5%

Business

Dubai South Discovery

Bay

AED 701 -17% Gardens Duabi Land

AED 1,732 27%

AED 556 12% AED 787 -11%

Al Furjan

Mohammed Bin

AED 918 14%

Rashid City

Arabian Ranches Villas AED 2,076 51% Dubai Creek Harbour

AED 1,682 -4%

AED 1,191 -3%

AED 539 18%

Positive Neutral Negative

Source: REIDIN

Note: Sales prices are quoted in AED per sq ft with year-on-year change in %

Metric Apartment Apartment Villa rent Villa sales price Dubai average Dubai average

rent sales price (AED per sq ft (AED per sq ft) rent (AED per sales price

(AED per sq ft (AED per sq ft) per year) sq ft per year) (AED per sq ft)

per year)

2021 AED 64 AED 1,027 AED 58 AED 1,126 AED 61 AED 1,076

2022 AED 74 AED 1,105 AED 70 AED 1,302 AED 73 AED 1,203

Y-o-y trend

17% 8% 21% 16% 19% 12%

11Dubai’s office market

Office rents have recovered to pre-pandemic levels registering an increase

of 12% YTD in September 2022 compared to the same period last year.

Occupiers continue to assess relocation and consolidation opportunities in an

environment of increasing fit-out costs.

Review of 2022 performance The majority of government services, banks and professional

The post-pandemic workplace forms an integral part of corporate services companies have returned to the office while media,

occupier recovery strategies as issues of staff retention and technology and design firms have largely embraced hybrid working

employee engagement came to the fore over the last two models. Demand for office space continues to be defined by

years. The office market in Dubai has historically been driven by growth in business operations in key sectors of the economy.

international companies looking to establish a regional market

base in the Emirate. This segment of the market typically seeks Dubai employment in financial and business services, 2015 to 2022f

prime central business district (CBD) properties, where rents were

the quickest to recover in 2022. 600 15%

Limited grade A stock within or in proximity to the central 500 10%

12%

business district of DIFC/Downtown has allowed building owners 10% 1% 3%

400 8% 5%

to maintain rent levels this year. Inflation linked rental escalations 3%

Persons in Thousands

have impacted ongoing leases for corporate tenants, even as the 300 -0%

role of the office continues to be reassessed. Capital investment

200 -5%

for fit-outs has previously been provided on stock outside of CBD

locations as an incentive to tenants and this trend is expected to 100 -10%

continue. -10%

0 -15%

Dubai Statistics Centre forecasts GDP growth forecast at 4.5% in

2015 2016 2017 2018 2019 2020 2021 2022f

2022 led by the hospitality, food and beverage (F&B), real estate,

wholesale and retail, transport, manufacturing and financial Employment - financial and business service

services sectors. As a result, hiring levels across key sectors is

Year-on-year change (%)

expected to increase and will have a positive impact on office

Source: Oxford Economics; Note: f:forecast

demand.

Dubai average office rents, Q1 2015 to Q3 2022

125 126 125 126 125 124 124 124 122 140

121 121 121 119 119

116 115 114

112 110 108 110 114

106 103 105 107 120

101 100 99 101 102

100

AED per sq ft per year

80

60

40

20

0

Q1-2015

Q2-2015

Q3-2015

Q4-2015

Q1-2016

Q2-2016

Q3-2016

Q4-2016

Q1-2017

Q2-2017

Q3-2017

Q4-2017

Q1-2018

Q2-2018

Q3-2018

Q1-2022

Q1-2019

Q2-2019

Q3-2019

Q4-2019

Q1-2020

Q2-2020

Q3-2020

Q4-2020

Q1-2021

Q2-2021

Q3-2021

Q1-2022

Q1-2022

Q2-2022

Q3-2022

Source: REIDIN

Note: Rents quoted above exclude service charge

12Middle East Real Estate Predictions | 2023

WTC/SZR** Deira

AED 126 AED 83

DIFC

AED 259

TECOM Downtown

AED 202

AED 165

JLT*

AED 81

Al Barsha

Business Al Garhoud

AED 82 Bay

AED 76

AED 105

Bur Dubai

AED 87

Rents are quoted AED per sq ft per year

Rents are average achieved rents for shell and core offices exclusive of service charges

*Jumeirah Lakes Towers

**World Trade Centre/Sheikh Zayed Road

Area DIFC Bur Al Deira WTC/ Al Busi- Down- TECOM JLT Dubai

Dubai Garh- SZR Barsha ness town aver-

oud Bay age

2020 216 90 75 86 111 77 84 177 166 71 101

2021 239 82 69 80 109 75 87 164 167 72 102

Y-o-y

trend 8% 6% 10% 4% 16% 9% 21% 23% -1% 13% 12%

2022 259 87 76 83 126 82 105 202 165 81 114

Source: REIDIN, Deloitte

13Dubai’s retail market

Consumer spending growth fueled retail sector recovery in both online and

traditional mall formats.

Review of 2022 performance UAE retail sales volume growth, 2017 to 2026f

The EIU estimates that the total UAE retail sales volume will

increase by approximately 4.2% in 2022, with sales expected to 9% 7.7%

increase by 3.9% a year on average over the remainder of the 6% 4.2%

5.3%

4.0% 3.6%

forecast period. 2.7%

Retail sales volume growth

3% 1.9%

0.9% 1.5%

0%

Emaar Malls, which owns and operates approximately 6.8 million

sq ft of retail gross leasable area (GLA)1, registered 24% growth in -3%

revenue during the first nine months of 2022, when compared to -6%

the same period in 2021. Meanwhile average occupancy for the -9%

Emaar portfolio, which includes Dubai Mall, Dubai Marina Mall, -9.7%

-12%

Gold & Diamond Park, Souk Al Bahar and other community retail

2017e 2018e 2019e 2020e 2021e 2022f 2023f 2024f 2025f 2026f

centres stood at 96% as of September 2022. Dubai Hills Mall, the

newest entrant among the portfolio opened in February 2022 and

had achieved an occupancy of 87% as of September 2022. Source: EIU a:actual, e:EIU estimate, f: EIU forecast

Meanwhile, Majid Al Futtaim (MAF) point of sale (POS) data2 shows For residents, ‘other malls’, which include smaller community cen-

that overall, consumer spending increased by 20% from January tres and convenience retail, as well as ‘non-mall’ outlets continue

to September 2022 compared to the same period in 2021 and to dominate in 2022 due to their convenience and proximity to

retail sector growth was 15%, with non-retail up 29%. According to residential areas. Majid Al Futtaim footfall data reveals an increase

the MAF data, fashion spending was the highest growth category of 15% in mall visitors during YTD September 2022 compared to

increasing 23% from 2021 levels and gaining 25% on 2019 levels. the same period in 2021.

January to March recorded the strongest sales through YTD

September, contributing 44% of the growth for the first nine Inflation remains a concern for consumers and is expected to

months compared to the same period in 2021. This mirrored the impact the overall discretionary spending in 2023. Omnichannel

highest performing months in the hospitality sector as highlighted formats are allowing consumers to search for discounts and deals,

previously. with retailers focusing on a seamless shopping experience through

an increased use of data and technology. The UAE e-commerce

Dubai consumer preferences market is expected to reach US$ 9.2 billion in 2026 according to

The Dubai Mall and Mall of the Emirates have historically been the analysis by the Dubai Chamber of Commerce. This growth

the majority of the demand from visitors, collectively capturing will be supported by increasing mobile e-commerce transactions

51% of total tourist retail demand in 2022. Demand from tourists through the availability of applications.

recovered during 2022 due to ease of travel and the lifting of re-

strictions. Additionally, retail centres continue to rely on resident

footfall and spend.

Note:

(1) Emaar Malls, Q3 2021 Results Presentation

(2) Majid Al Futtaim ‘State of the UAE Retail Economy’ Q3 2022 Report

14Middle East Real Estate Predictions | 2023

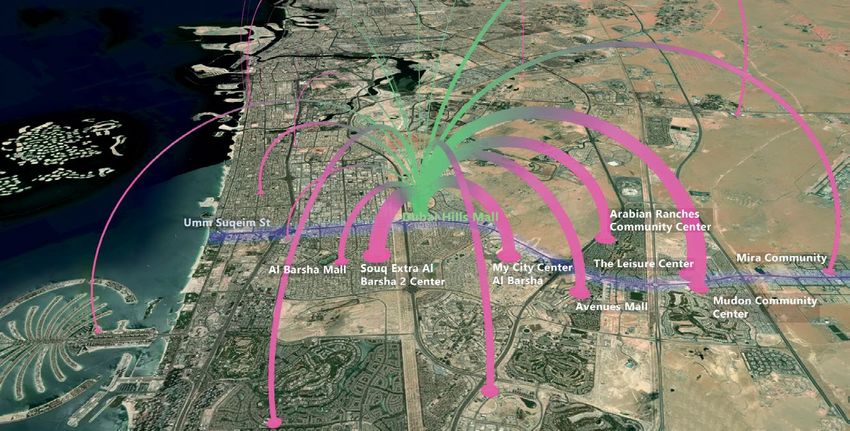

Cannibalising shopping malls:

how does a newly opened asset and its

location affect consumer behaviour?

Spatial cannibalisation, also referred to as, customer loss to competition

or to one’s own assets, is of crucial importance to retailers and commercial

developers alike.

Deloitte has partnered with Perigon AI to analyse the impact of credit card spend allows spending patterns for established centres

a new mall on existing retail developments. If you could reliably and the impact of new centres to be assessed.

estimate spatial cannibalisation when planning for retail expansion,

developing a new mall or monitoring the performance of your As a case study to demonstrate this approach we review

assets, will consumers previously populating other locations switch the impact the newly opened Dubai Hills Mall has had on it's

to your location? How does the location, e-commerce, marketing catchment. Below we see the weekly relative footfall in Dubai Hills

campaigns and tenant mix affect this expansion? Mall starting from week 1 of operations. We can see a steady

growth in the number of visitors to the mall in the first few weeks,

Utilising mathematical modelling and AI to process a vast array of mounting to a spike in week 6.

data ranging from human mobility data to geographically granular

1.0 1. Weekly relative footfall

Relative footfall

A spike in visitors to Dubai Hills Mall

0.8

in the first few weeks, called a honeymoon

0.6 period , known as a phase of discovery,

exploration and 'checking it out'.

0.4

0.2

Dubai Hills Mall visitation

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28

Weeks after opening

Note: The indicated relative footfall is a score obtained from streams of big data, depicting footfall on a given

week between its all-time minimum (0) and all-time maximum (1). As seen on the graph, footfall in Dubai Hills

Mall reached its maximum on week 6 during the period analysed.

2. Where do these customers come from? Ranches - Mira Community axis, along Umm Suqeim Street.

We see the trade areas clustered around Dubai Hills Mall (green The honeymoon period attracted customers from a wide range of

pin) in the first week, expanding to cover larger swathes of Dubai neighbourhoods such as Palm Jumeirah, Dubai Marina, and JLT,

reaching peak coverage on week 6. The primary trade areas of considered as high-end central high-end central areas with an

the mall then come back to 'normal' with the mall and the Arabian abundant supply of retail destinations.

Week 1 Week 6 Week 11

155.0% 3. Mall cannibalisation

4.5%

What happened to the visitation patterns

4.0%

for other retail destinations after

3.5%

3.0% Dubai Hills Mall opened? Is there any

2.5% cannibalisation effect? As seen on the left

2.0% graph, 4.6% of all of all regular visitors to

1.5% Souq Extra Al Barsha 2 switched to Dubai

1.0% Hills Mall. On the right tail, 1.1% of all the

0.5%

visitors to Mall of the Emirates switched to

0.0% Souq My City Arabian The Lei- Avenues Mudon AI Barsha Mira Mead- J3 The Village Club Vista Mall of Dana Dubai Hills Mall. We can immediately see

Extra Center AI Ranches sure Mall Commu- Mall Commu- ows Mall Mall Mare the Mall

AI Barsha Barsha Commu- Center nity nity Village Emirates that the retail destinations affected the

2 Center nity Center

Center most are primarily community centers and

smaller retail lifestyle destination concepts,

Percentage of customers cannibalised by Dubai Hills Mall

rather than big shopping malls.

4. Cannibalisation string plot

If we look at the spatial distribution of the

retail destinations most cannibalised by

Dubai Hills Mall, we can see an interesting

pattern: They are concentrated near the

mall, and spread along Umm Suqeim

Street and its extension, Al Qudra Road

(highlighted in blue), serving Dubai's

outer communities, to include Al Barsha 2

and Dubai Hills, to Arabian Ranches,

Sustainable City, and beyond.

Mall cannibalisation 1% 2% 3% 4% 5%

5. A quick look at the tenant mix at Dubai Hills Mall

Dubai Hills Mall is placed on the artery connecting the upscale outer communities to Downtown Dubai. Dubai Hills Mall has accordingly

been positioned to attract residents from these communities as its primary trade area. The tenant mix reveals how community-oriented

its offerings are, to include family entertainment, F&B concepts, DIY hardware shops and barbershops. We can also see a selection of

comparison goods, offering brands seen in Dubai's 'super regional centres' in a more accessible format.

16Middle East Real Estate Predictions | 2023

Dubai’s industrial and logistics

market

Average warehouse rents continue to recover as demand from logistics

companies remains buoyant and freight movements at the airports surpass

2020 levels.

Review of 2022 performance UAE imports and exports, 2018 to 2025f

The two Dubai airports (DWC and DXB) have a combined capacity

500

of almost 2.8 million tons and are supported by airport adjacent as

well as city-wide warehousing facilities. At the end of 2021, freight

400

movements at the two airports had increased in comparison to

the 2020 levels, although they were still below 2019 levels. DXB

300

is currently the third busiest hub in the world for international

US$ billion

air freight with rapid transfer time to Port Rashid or Jebel Ali.

200

Meanwhile, DWC’s dedicated bonded link to Jebel Ali Port has

enabled a rapid transit of sea to air cargo, supporting a swifter

100

recovery for the industrial and logistics market in Dubai.

-

E-commerce focused zones such as Dubai CommerCity and Dubai 2009 2020 2021f 2022f 2023f 2024f 2025f

South’s e-commerce cluster have been added to the supply in Imports USD$bn Exports US$bn

recent years, while JAZFA is also developing additional logistics

Source: Fitch Solutions; Note: f:forecast

capacity. Meanwhile, there are still limited international grade

specification warehouses in other parts of Dubai and this could

lead to redevelopment projects in older areas such as Al Quoz,

Umm Ramool among others.

Dubai key logistics indicators, 2021 vs 2022 (millions)

Metric DWC DXB Jebal Ali Road freight

cargo throughput cargo throughput tonnage tonnes

throughput

2021f 0.94 m 2.65 m 7.05 m 30.64 m

Y-o-y

trend 5% 3% 1% 3%

2022f 0.99 m 2.73 m 7.14 m 31.46 m

Source: Fitch Solutions

f: forecast

Dubai average warehouse rents, Q3 2022

JAFZA

AED 22

DAFZA

AED 26

Dubai South Al Quoz

AED 26 DIP AED 35

AED 26

Rents are quoted AED per sq ft per year

Rents are average achieved rents for purpose built warehouses exclusive of service charges

Source: Deloitte

17Middle East Real Estate Predictions | 2023 Key contacts Stefan Burch Partner Head of Real Estate Deloitte Middle East sburch@deloitte.com Oliver Morgan Partner Head of Real Estate Development Deloitte Middle East omorgan@deloitte.com Jaime Liversidge Director Head of Real Estate Valuations Deloitte Middle East jliversidge@deloitte.com Dunia Joulani Director Head of Travel, Hospitality and Leisure (EMEA) Deloitte Middle East djoulani@deloitte.com Manika Dhama Director Head of Research, Real Estate Development Deloitte Middle East mdhama@deloitte.com 18

Middle East Real Estate Predictions | 2023

19This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte Professional Services (DIFC) Limited would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte Professional Services (DIFC) Limited accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication. Deloitte & Touche (M.E.) LLP (“DME”) is the affiliate for the territories of the Middle East and Cyprus of Deloitte NSE LLP (“NSE”), a UK limited liability partnership and member firm of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”). Deloitte refers to one or more of DTTL, its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms are legally separate and inde- pendent entities. DTTL, NSE and DME do not provide services to clients. Please see www.deloitte.com/ about to learn more. Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our network of member firms in more than 150 countries and territories, serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 300,000 people make an impact that matters at www.deloitte.com. DME is a leading professional services firm established in the Middle East region with uninterrupted pres- ence since 1926. DME’s presence in the Middle East region is established through its affiliated indepen- dent legal entities, which are licensed to operate and to provide services under the applicable laws and regulations of the relevant country. DME’s affiliates and related entities cannot oblige each other and/ or DME, and when providing services, each affiliate and related entity engages directly and independent- ly with its own clients and shall only be liable for its own acts or omissions and not those of any other affiliate. DME provides audit and assurance, consulting, financial advisory, risk advisory and tax services through 26 offices in 15 countries with more than 5000 partners, directors and staff. About Deloitte in the Dubai International Financial Centre Deloitte Professional Services (DIFC) Limited (“DPSL”) is incorporated in the Dubai International Financial Centre (“DIFC”), with commercial registration number CL0748 and is registered with the Dubai Financial Services Authority (“DFSA”) as a Designated Non-Financial Business or Profession. DPSL is a sublicensed affiliated entity of DME. DPSL has a 100% wholly owned subsidiary in the DIFC namely Deloitte Corporate Finance Advisory Limited (DCFAL) which has commercial registration CL2220. DCFAL is regulated by the DFSA and licensed to provide regulated financial advisory services. DPSL & DCFAL co-inhabit with their principal place of business and registered offices at Al Fattan Currency House, Building 1, 5th Floor, Dubai International Financial Centre, Dubai, United Arab Emirates. Tel: +971 (0) 4 506 4700 Fax: +971 (0) 4 327 3637. © 2023 Deloitte Professional Services (DIFC) Limited. All rights reserved.

You can also read