Markets Outlook RESEARCH - BNZ

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

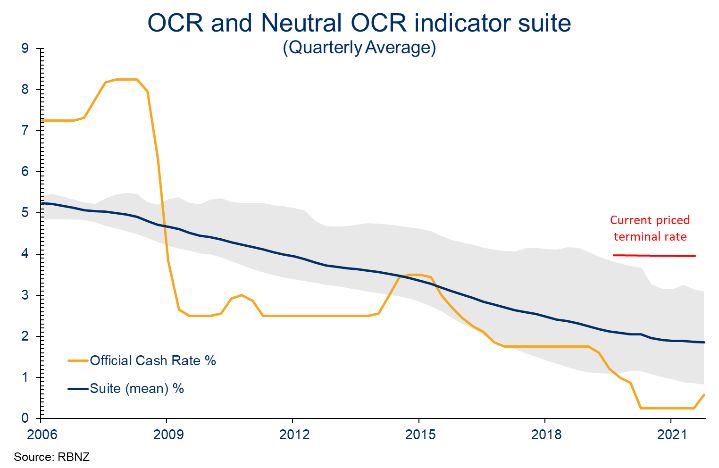

RESEARCH Markets Outlook 11 April 2022 Confusion Still Reigns • RBNZ to reinforce aggressive tightening cycle • Consumer confidence is at record lows, the housing • But April’s move a line ball call as retail spending market is softening and retail spending is under pressure. crushed • QSBO this week’s key leading indicator Rates higher, sooner • PMI and next week’s PSI to provide coincident details • NZ restrictions to ease further? We have no idea what, exactly, the RBNZ will do with the cash rate on Wednesday afternoon. The debate amongst financial market participants is whether the RBNZ will hike the rate 25 or 50 basis points. There are very sound arguments for either approach. At the margin, we think the case for 25 is more compelling but we do understand why the MPC members could conclude otherwise. While the specifics of Wednesday’s Monetary Policy Review are open to debate the key messages are a given. The Reserve Bank is facing into rampant inflation and an unsustainably tight labour market so will need to progressively raise its cash rate until such time that overall monetary conditions are contractionary. For all but financial But terminal cash rate already above neutral market participants this is all you need to know. Unless it breaks tradition, a forward track will be not provided at the Monetary Policy Review. If the RBNZ was to produce an interest rate track, we would also expect it to be more aggressive than it projected back in February. The main, but not exclusive, reasons why we think the RBNZ should go 25 and not 50 are: • Uncertainty about economic outcomes is conceivably the greatest it has ever been. • Overall monetary conditions are much more restrictive than a glance at the cash rate would imply. • The mortgage curve has already moved higher at this meeting and will probably head higher still, even if the RBNZ was to do nothing at all. Mortgage rates higher come what may • Banks test borrowers’ ability to repay with rates well in excess (sometimes as much as 3.0%) of the actual lending rate. • The terminal cash rate is already priced at around 4.1% (well above anyone’s perception of neutral). In the February MPS the RBNZ said it thought neutral was 1.86% but acknowledged this was the mean of a set of estimations with a range of 0.82% to 3.09%. If the RBNZ is aggressive this week then the priced terminal cash rate could head as high as 4.5%. Would the RBNZ really want this given its view on where neutral sits? www.bnz.co.nz/research Page 1

Markets Outlook 11 April 2022

Business and consumer confidence surveys should play a In contrast, core retail sales fell 1.4% in the month to be

major role in determining the RBNZ’s decisions. In this down 9.0% nominally over the last two months. Could you

regard, it is disappointing the release of NZIER’s March have ever imagined we would be arguing about a 25 or 50

quarter QSBO was postponed from April 5 to April 12. While basis point increase in the cash rate when retail spending

still released before the Monetary Policy Review is made looks so egregious?!

public, it is sufficiently late for it to be problematic for MPC

members to fully digest its content. Given the latest readings, March quarter retail spending

looks like it will be flat, to down but maybe not so down as

We will, of course, still peruse the survey for insight on what we have penciled in for the quarter. That said, it remains

is happening within the business community but would be consistent with our expectation that GDP growth for the

surprised if it didn’t just reaffirm what we already know, March quarter will be near zero, well lower than the RBNZ’s

namely: 1.6% February MPS pick.

• Business confidence is under pressure On Thursday the Government will announce whether, or

• Costs are skyrocketing not, New Zealand will stay under its current “red traffic light

• Margins are declining setting”. There is growing hope we may move from red to

• The labour market is extremely tight orange. This would mean that restrictions on indoor

• Pricing intentions are through the roof gathering limits would be lifted and folk may not have to be

seated and served in hospitality locations. Additionally, the

The QSBO does not survey the agriculture sector directly so government’s encouragement to work from home will be

developments, both positive and negative, here will not be dropped. Such moves would certainly be a major step

in the summary numbers. forward for the arts, recreation, entertainment and

hospitality sectors and city centres should again see a lot

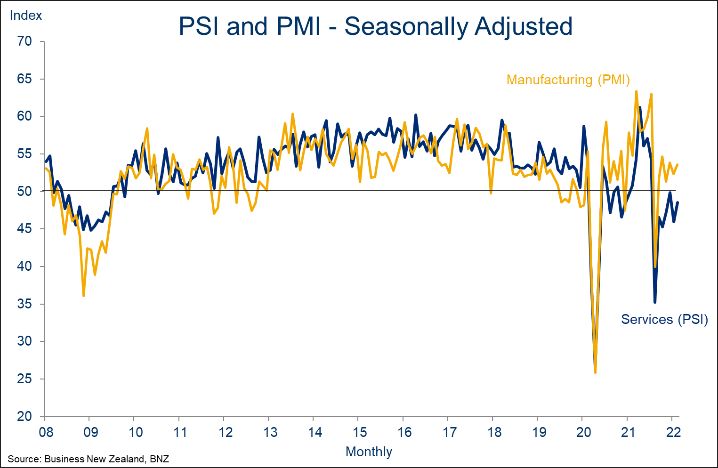

Unfortunately, our own Performance of Manufacturing

more foot traffic. Nonetheless, there is no guarantee such a

Index, released Thursday, will also be too late for the MPC to

move will be made, and it will likely still take some time

contemplate. All things considered, recent past PMIs have

before activity in the disaffected sectors returns to anything

been remarkably robust, with the headline index bouncing

like a previous normal.

back and forth around its average level. We have no reason

to assume the March survey will look any different. The poor With the borders progressively opening there is heightened

cousin has been the Performance of Services index which anticipation that tourism spending will pick up and some of

has been battered by Omicron and ongoing red level the labour market constraints we are experiencing will be

restrictions. We have to wait until next Tuesday to see if this eased. We fear many are thinking immediate significant

index is slowly picking up as folk become used to living with gains will be made. We are a bit more cautious. The next

Covid. step in the opening process is on Tuesday when the border

reopens to:

Services struggling

• temporary work and student visa holders who still meet

their visa requirements

• up to 5000 international students

• Australian citizens

• New Zealand permanent residents arriving from

anywhere in the world.

February tourism and migration data will also be released on

Thursday. As this is largely prior to any border relaxations

(they began midnight February 27), things will continue to

look fairly miserable. In fact, we expect the migration data to

show an increasing net outflow which, we fear, will continue

to gain momentum right through the first half of this year.

Tourism numbers will likewise remain subdued.

Our latest read on consumer spending came this morning To round the week off, on Wednesday we get March month

with the release of March Electronic Card Transactions data. partials for the Q2 CPI with the release of the latest food and

Total card spending rose a surprisingly solid 1.6% but this rental price indices. In the case of food, we are expecting

probably overstates what is happening to domestic demand prices to rise 0.3% for the month, which will deliver a 2.9%

by a significant margin. One of the big drivers for the month increase in food prices for the quarter.

was the 14.5% increase in non-retail spending which

includes, amongst other things, offshore travel bookings. We have been perplexed by how low and stable the official

measure of rental inflation has been. So stable has it been,

www.bnz.co.nz/research Page 2

Markets Outlook 11 April 2022

however, that it is difficult to forecast anything other than a overall CPI increases 1.9% in the March quarter. If we are

continuation of the trend we have been seeing. Accordingly, right that will take the annual increase in consumer prices to

we are looking for rental inflation to nudge up only slightly, 7.0%. For the record, the RBNZ’s February Monetary Policy

to 0.4% in March from 0.3% in February, delivering a 1.0% Statement assumed 1.4% for the quarter, 6.6% for the year.

increase for the quarter.

stephen_toplis@bnz.co.nz

The quarterly increases we have pencilled in for food and

rentals are key building blocks in our expectation that the

www.bnz.co.nz/research Page 3Markets Outlook 11 April 2022

Global Watch

• CPI inflation to hit 8.4% in US; 6.7% in UK Unemployment seen at 48 year low

• China CPI inflation seen lifting to 1.3%; focus on COVID

• ECB meets Thursday: any explicit QE guidance?

• BoC seen hiking 50bps this week

• AU unemployment rate seen at lowest since 1974

Australia

Australian employment data for March is the highlight in

the Easter-shortened week. NAB expect the

unemployment rate to fall one-tenth to 3.9% on the back

of a 50k monthly employment gain. NAB sees participation

ticking one-tenth higher to a new record 66.5%. If realised,

this would see the unemployment rate at its lowest level

since 1974 and cement the string of upside surprises to the

RBA’s February SoMP forecasts (which only saw the Unemployment outpacing RBA Feb forecasts

unemployment rate drifting below 4 in the third quarter).

The labour market continues to demonstrate rude health.

Labour demand indicators have remained strong. Seek job

ads rose a further 5% in March and ABS job Vacancies

(surveyed after the February employment numbers) were

up a further 7% in the 3 months to February. They are now

86% above pre-pandemic!

April’s Westpac-Melbourne Institute Consumer Confidence

on Wednesday will be closely watched for any rebound

following the 4.2% fall to 96.6 in March. The level below

100 indicates that pessimists outnumbered optimists for

the first time since September 2020. NAB sees a rebound Consumer confidence to rebound in April

as likely, given the March numbers were weighed by a

combination of flood impacts, Russia’s invasion of Ukraine

and downstream from that acute and salient inflation

concerns in the form of fuel prices. While none of those

themes have completely disappeared from the backdrop,

some stabilisation points to a rebound in the confidence

numbers for April. The March NAB Business survey is

released tomorrow.

Vacancies being created faster than filled

China

Focus will remain on Covid given lockdowns in Shanghai.

On the data front, inflation figures are published this

afternoon. Consensus is for CPI to move higher to 1.3% y/y

from 0.9% as the drag from food price declines eases,

while on the producer side, PPI is seen slowing to 8.1% y/y

from 8.8% on base effects.

www.bnz.co.nz/research Page 4Markets Outlook 11 April 2022

March credit numbers are expected during the week, the and Morgan Stanley. North of the border, the Bank of

date yet to be announced. New Yuan Loans are seen Canada meets on Thursday, with a 50bp hike fully priced.

rebounding out of the seasonally low February figure to

CNY2740bn. A PBoC decision on the 1-year MLF rate is due UK

some time from Wednesday, a 5-10bp cut from its current

2.85% likely. A busy week of data out of the UK. February reads of

Industrial Production and monthly GDP are due Monday.

US (and Canada) That’s followed by labour market data out Tuesday, and

inflation figures for March on Wednesday. Inflation likely

Tuesday’s March CPI is the data centrepiece. The market accelerated as the renewed impulse from Ukraine starts to

consensus sees no slowdown in the pace of price rises with enter the figures, before a spike higher in April when

core inflation expected to be 0.5% m/m, the same as last sharply higher energy costs can be passed through to

month, and taking the annual rate to 6.6% y/y. Headline consumers. That’s a lot for markets to chew on as the BoE

annual CPI inflation is seen lifting to 8.4% from 7.9%. balances the competing pressures of higher inflation and

macroeconomic headwinds.

There is also continued focus on the state of the consumer

given the mixed messages being sent from actual spending Eurozone

and consumer confidence. Thursday’s Retail Sales report is

expected to be choppy, control group sales expected to be The focus will be Thursday’s ECB meeting, which sees no

still soft at -0.1% m/m after Feb’s -1.2%. Thursday also sees new economic forecasts. Given continued higher than

the UoM Consumer Sentiment Survey for early March with forecast inflation, the central question is whether the ECB

the headline index expected to fall further to 59.0 from use this meeting to explicitly signal an end to (APP) QE at

59.4. Also important in the survey is 5-10yr inflation the end of June? NAB think not as it can use the

expectations given the constant reference by Fed officials intervening period to assess further. However, NAB does

of ensuring inflation expectations remain anchored. anticipate a subtle shift in guidance that opens that

possibility given a few officials wanted a quicker end to QE

The April Empire State Survey – first of the manufacturing as judged by the March meeting minutes. The French

regional surveys – is out Friday, and tipped to improve. Presidential election is now down to a two-horse race with

Numerous Fed speakers are scheduled with Brainard in latest polls showing Macron holding a small lead over

Q&A on Tuesday the one to watch. The corporate earnings National Rally’s Le Pen.

season is upon us again, starting Wednesday with JP

Morgan, followed on Thursday by Wells, Citi, Goldmans taylor.nugent@nab.com.au / doug_steel@bnz.co.nz

www.bnz.co.nz/research Page 5Markets Outlook 11 April 2022

Fixed Interest Market Reuters: BNZL, BNZM Bloomberg:BNZ

Rates continue their stampede higher, with fresh multi-year what messaging the RBNZ gives, we would expect a sizeable

highs seen in most markets. The US 10-year rate hit 2.73%, its fall in shorter-term rates in the event the RBNZ decides

highest level in three years, driving NZ swap rates 17-21bps against hiking by 50bps.

higher in illiquid trading conditions last week. Focus turns to

What would happen if the RBNZ hiked 50bps? Again, much

the RBNZ this week, with the market pricing a high chance of

will depend on the messaging. However, with so much

a 50bps OCR increase.

tightening now built in (43bps for April, 45bps for May, 42bps

After continuously flattening since the end of last year, the US for July and 39bps for August), it’s not clear that shorter-term

yield curve steepened aggressively last week as the Fed rates will rise that much further in the event of a 50bps hike.

signalled plans for “rapid” balance sheet reduction (also We think rates are overdue for a period of consolidation after

known as ‘quantitative tightening’ or ‘QT’). The minutes to what has been an exceptionally big move over recent months,

the Fed’s March meeting showed members were generally although it will likely require some stability in global rates for

supportive of a plan to allow $95b of its bond holdings to this to occur.

mature each month, roughly double the pace of the last

period of Fed balance sheet reduction between 2017 and The market now prices a 4% OCR, at face value

2019. When the Fed reduces its balance sheet, by letting its % Market pricing for the OCR

bond holdings mature, it means private sector investors need 4.50

4.25

to absorb more bond supply, all else equal, which tends to put 4.00

3.75 BNZ

some upward pressure on longer-term rates, steepening the 3.50

3.25

Market pricing

curve (by how much is still a source of debate). The US 2s10s 3.00 RBNZ February MPS*

2.75

curve ended the week back in positive territory, at +18bps, 2.50

2.25

having been as low as -8bps at the end the previous week. 2.00

1.75

The recession warning brigade have been stood down, at 1.50

1.25

least temporarily. 1.00

0.75

0.50

Other central banks are moving more hawkishly too. The RBA 0.25

belatedly removed its reference to being “patient”, clearing 0.00

2020 2021 2022 2023

the way for a rate hike in the coming months. The minutes to Source: BNZ, RBNZ. * RBNZ projections are quarterly averages.

the ECB’s last meeting suggested policymakers were growing Global rates going parabolic, NZ following

concerned about potential ‘second-round’ effects from % 5-year swap rates

inflation onto wage and price setting behaviour. Since its last 4.0

New Zealand

meeting, European inflation has surged much higher than 3.5

US

expected and markets are expecting the ECB to start lifting 3.0 Australia

rates in Q3. The Bank of Canada is expected to hike its cash 2.5

rate 50bps this week. 2.0

The increases in global rates have flowed through to the New 1.5

Zealand market with little resistance. There appears to be a 1.0

general lack of investor appetite to step in the way of current 0.5

market momentum. Nervousness ahead of this week’s RBNZ

0.0

meeting may also be limiting investor participation at present, Jan-19 Jul-19 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22

Source: BNZ, Bloomberg

exacerbating thin market conditions.

Volatility is elevated, both in NZ and offshore

Market expectations are elevated heading into this week’s

vol Interest rate volatility measures

meeting. The market has 43bps priced for this meeting, 300

which equates to around a 75% chance of a 50bps hike. At US Treasury volatility

250 (MOVE index)

face value, market pricing of the peak in the OCR this cycle

has pushed above 4% (although this might partly reflect risk 200 1-month realised volatility,

NZ 10yr swap (rhs)

premia). Either way, it is much higher than our revised

forecasts, which see a 3% peak in the OCR early next year. 150

We upgraded our wholesale rates forecasts last week to 100

reflect higher OCR and US 10-year rate assumptions. 50

For this week’s meeting, our central view, albeit one held

0

without much conviction, is that the RBNZ will hike by ‘just’ 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

25bps. While the market reaction will always depend on Source: Bloomberg.

www.bnz.co.nz/research Page 6Markets Outlook 11 April 2022

Foreign Exchange Market Reuters pg BNZWFWDS Bloomberg pg BNZ9

Last week the NZD flew to a high of just over 0.7030, its is growth-sapping and euro-negative – is the key hurdle for

first look above 0.70 since November, before succumbing euro performance.

to broad-based USD strength and ending the week down

over 1% to just under 0.6850. NZD/AUD reached its lowest In global data, US CPI inflation data will be in the spotlight,

level in over a year of just under 0.9150, following a with the headline rate expected to shoot up to yet another

hawkish RBA policy update and ended the week down ½% multi-decade high of 8.4%, and the core rate nudging up to

to 0.9185. Against a backdrop of higher global rates, the 6.6%. While high inflation is well-anticipated, it’s a

yen remained soft, while the euro remained out of favour, reminder of how much tightening is justified by the Fed

with ongoing war in Ukraine a factor. NZD/JPY and this year and beyond.

NZD/EUR crosses were up almost ½% on the week.

Last week we affirmed our NZD projections, which show

Last week the USD was the best performing of the key the currency consolidating in the current quarter and an

majors we follow, with the DXY dollar index hitting its end-Q2 target of 0.69. We still see resistance around the

highest level in nearly a year. The USD’s higher trend has 0.70 level, even though the recovery in risk appetite and

been supported by rising US-global rate spreads as commodity price strength has seen our short-term fair

investors factor in a more aggressive tightening cycle by value model estimate push up just past 0.7150.

the Fed. The FOMC minutes of last month’s meeting

flagged that “many” members thought one or more 50bps We revised up our AUD projections, meaning a nudge

increases could be appropriate this year and would have down to our NZD/AUD profile, to now target 0.90 for later

voted for a larger than 25bps hike if not for Russia’s in the year, which is consistent with a view that sub-0.90

invasion of Ukraine. Investors also woke up to the likely levels could be traded, a level not seen since 2018.

rapidity of the Fed’s balance sheet reduction, as noted in a

hawkish speech by vice Chair-elect Brainard and in the No recent strong link between NZD and NZ-US short rates

FOMC minutes. NZ-US short rate* (rhs)

0.76 1.8

NZD/USD (lhs)

1.6

The US 10-year rate rose 32bps over the week to close at 0.74 1.4

its highest level in over three years at 2.70%, taking its gain 1.2

0.72

this year to 119bps. The US 2-year rate is up a massive 1.0

178bps so far this year, more than the 141bps increase in 0.70 0.8

NZ’s 2-year swap rate. 0.6

0.68 0.4

In the week ahead, domestically the focus will turn to the 0.66 0.2

0.0

RBNZ’s MPR on Wednesday, where most would agree it’s a *Expected tightening next 12 months, NZ-US

0.64 -0.2

lineball call between the Bank delivering either a 25bps or Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 Apr-22

50bps hike to either 1.25% or 1.5%. With the market Source: BNZ, Bloomberg

already pricing in the OCR heading to 4%, it’s hard to

believe that the Bank could be any more hawkish than

implied by that. The lesson from the past nine months is Cross Rates and Model Estimates

that any NZD reaction to the MPR is unlikely to be Current Last 3-weeks range*

sustained for long, so fade any currency reaction.

NZD/USD 0.6847 0.6820 - 0.7030

Tomorrow’s QSBO should be consistent with a

NZD/AUD 0.9187 0.9150 - 0.9350

stagflationary environment, with poor levels of confidence

NZD/GBP 0.5252 0.5220 - 0.5340

and activity and extremely high inflation indicators.

NZD/EUR 0.6270 0.6190 - 0.6410

The Bank of Canada and ECB also meet this week. A 50bps NZD/JPY 84.94 81.90 - 87.00

hike from the Bank of Canada is widely anticipated. The *Indicative range over last 3 weeks, rounded figures

ECB’s policy update won’t contain any new forecasts, but

language should move in a more hawkish direction after BNZ Short-term Fair Value Models

the latest 7.5% y/y CPI print, with a likely nod to end QE by Model Est. Actual/FV

the end of June, which will then set the scene for rate

hikes beginning in the second half. Any policy tightening NZD/USD 0.7170 -5%

NZD/AUD 0.9000 2%

by the ECB this year will significantly lag that of the US Fed

and most other central banks. The war in Ukraine – which

jason.k.wong@bnz.co.nz

www.bnz.co.nz/research Page 7Markets Outlook 11 April 2022

Technicals

NZD/USD

Outlook: Trading range

ST Resistance: 0.70 (ahead of 0.72)

ST Support: 0.67 (ahead of 0.6600)

We keep resistance at 0.70, with only a brief intra-day

foray above that level last week. We pin the first support NZD/USD – Daily

Source: Bloomberg

level at 0.67.

NZD/AUD NZD/AUD – Daily

Outlook: Trading range Source: Bloomberg

ST Resistance: 0.9450 (ahead of 0.9600)

ST Support: 0.9140 (ahead of 0.9055)

A decisive break below 0.92 puts 0.9140 on the radar,

ahead of a possible move down to the 2020 low of 0.9055.

jason.k.wong@bnz.co.nz

NZ 5-year Swap Rate

Outlook: Higher

ST Resistance: 3.75

ST Support: 3.28

5y has continued higher again and moving towards 3.75

resistance. Hold short and see if 3.75 holds.

NZ 5-yr Swap – Daily

Source: Bloomberg

NZ 2-year - 5-year Swap Spread (yield curve)

Outlook: Lower

ST Resistance: 0.28

ST Support: 0.0

Continue to hold rec’d position targeting move to zero.

NZ 2yr 5yrSwap Spread – Daily

pete_mason@bnz.co.nz Source: Bloomberg

www.bnz.co.nz/research Page 8Markets Outlook 11 April 2022

Quarterly Forecasts

Forecasts as at 11 April 2022

Key Economic Forecasts

Quarterly % change unless otherwise specified Forecasts

Dec-20 Mar-21 Jun-21 Sep-21 Dec-21 Mar-22 Jun-22 Sep-22 Dec-22 Mar-23

GDP (production s.a.) -0.3 1.3 2.5 -3.6 3.0 0.0 2.0 1.1 0.4 0.3

Retail trade (real s.a.) -2.0 2.5 3.0 -8.2 8.6 -1.0 1.5 1.0 0.4 0.2

Current account (ytd, % GDP) -0.8 -2.5 -3.3 -4.6 -5.8 -6.2 -7.1 -7.4 -7.3 -6.5

CPI (q/q) 0.5 0.8 1.3 2.2 1.4 1.9 1.0 1.6 0.6 0.9

Employment 0.6 0.7 1.0 1.9 0.1 0.2 0.2 0.3 0.2 0.1

Unemployment rate % 4.9 4.6 4.0 3.3 3.2 3.1 3.1 3.0 3.1 3.1

Avg hourly earnings (ann %) 4.6 4.1 4.5 3.6 4.1 4.6 5.1 5.1 4.8 4.5

Trading partner GDP (ann %) 0.8 6.8 9.8 4.2 4.1 3.8 3.9 4.7 4.0 4.0

CPI (y/y) 1.4 1.5 3.3 4.9 5.9 7.0 6.7 6.1 5.2 4.2

GDP (production s.a., y/y)) 0.3 3.2 17.9 -0.2 3.1 1.8 1.3 6.3 3.6 3.9

Interest Rates

Historical data - qtr average Government Stock Swaps US Rates Spread

Forecast data - end quarter Cash 90 Day 5 Year 10 Year 2 Year 5 Year 10 Year Libor US 10 yr NZ-US

Bank Bills 3 month Ten year

2020 Sep 0.25 0.30 0.25 0.65 0.15 0.25 0.60 0.25 0.65 0.02

Dec 0.25 0.25 0.25 0.70 0.15 0.30 0.75 0.20 0.85 -0.15

2021 Mar 0.25 0.30 0.75 1.40 0.40 0.85 1.50 0.20 1.30 0.09

Jun 0.25 0.35 1.00 1.75 0.55 1.20 1.90 0.15 1.60 0.17

Sep 0.25 0.50 1.35 1.75 1.20 1.60 1.95 0.15 1.30 0.41

Dec 0.65 0.80 2.15 2.40 2.10 2.45 2.60 0.15 1.55 0.87

2022 Mar 0.90 1.25 2.60 2.75 2.65 2.95 3.00 0.50 1.95 0.83

Forecasts

Jun 1.75 2.10 3.20 3.20 3.40 3.40 3.40 1.70 2.50 0.70

Sep 2.25 2.65 3.25 3.35 3.40 3.45 3.55 2.20 2.75 0.60

Dec 2.75 3.00 3.25 3.45 3.40 3.45 3.65 2.45 3.00 0.45

2023 Mar 3.00 3.15 3.25 3.45 3.40 3.45 3.65 2.70 3.00 0.45

Jun 3.00 3.15 3.20 3.45 3.30 3.40 3.65 2.95 3.00 0.45

Sep 3.00 3.15 3.15 3.45 3.20 3.35 3.65 3.20 3.00 0.45

Dec 3.00 3.05 3.00 3.40 3.00 3.20 3.60 3.20 3.00 0.40

Exchange Rates (End Period)

USD Forecasts NZD Forecasts

NZD/USD AUD/USD EUR/USD GBP/USD USD/JPY NZD/USD NZD/AUD NZD/EUR NZD/GBP NZD/JPY TWI-17

Current 0.68 0.74 1.09 1.30 124 0.68 0.92 0.63 0.52 85.1 73.9

Jun-22 0.69 0.76 1.11 1.32 124 0.69 0.91 0.63 0.53 86.1 74.0

Sep-22 0.70 0.78 1.13 1.33 122 0.70 0.90 0.62 0.53 85.4 74.2

Dec-22 0.72 0.80 1.15 1.35 120 0.72 0.90 0.63 0.53 86.4 75.6

Mar-23 0.72 0.80 1.17 1.37 118 0.72 0.90 0.62 0.53 85.0 75.2

Jun-23 0.72 0.79 1.18 1.40 116 0.72 0.91 0.61 0.51 83.5 75.0

Sep-23 0.72 0.78 1.22 1.40 114 0.72 0.92 0.59 0.51 82.1 74.7

Dec-23 0.71 0.77 1.23 1.41 112 0.71 0.92 0.58 0.50 79.5 73.6

Mar-24 0.70 0.76 1.25 1.41 110 0.70 0.92 0.56 0.50 77.0 72.6

Jun-24 0.70 0.76 1.26 1.41 108 0.70 0.92 0.56 0.50 75.6 72.3

Sep-24 0.69 0.75 1.25 1.42 108 0.69 0.92 0.55 0.49 74.5 71.5

TWI Weights

13.6% 17.3% 10.1% 3.2% 5.7%

Source for all tables: Statistics NZ, Bloomberg, Reuters, RBNZ, BNZ

www.bnz.co.nz/research Page 9Markets Outlook 11 April 2022

Annual Forecasts

Forecasts March Years December Years

as at 11 April 2022 Actuals Forecasts Actuals Forecasts

2020 2021 2022 2023 2024 2020 2021 2022 2023 2024

GDP - annual average % change

Private Consumption 2.5 0.4 3.1 2.6 2.0 -1.1 6.2 0.6 2.6 2.0

Government Consumption 5.8 7.5 10.4 4.5 0.9 6.8 10.2 6.8 1.0 0.6

Total Investment 2.6 -4.8 8.8 7.8 -0.4 -7.0 9.6 7.9 0.6 1.2

Stocks - ppts cont'n to growth -0.2 -0.2 0.8 -0.4 0.0 -0.8 1.6 -0.4 -0.1 0.0

GNE 2.9 0.4 6.6 3.7 1.2 -1.8 9.4 2.9 1.7 1.5

Exports 0.3 -17.8 5.4 10.7 7.1 -12.7 -3.0 6.5 11.5 4.1

Imports 1.1 -16.1 19.1 10.8 4.3 -16.1 15.7 10.3 6.8 0.4

Real Expenditure GDP 2.7 -0.2 4.0 3.3 1.7 -0.9 5.0 2.3 2.3 2.6

GDP (production) 2.2 -1.4 5.2 3.8 1.7 -2.1 5.6 3.2 2.2 2.6

GDP - annual % change (q/q) 0.4 3.2 1.8 3.9 1.8 0.3 3.1 3.6 1.4 3.0

Output Gap (ann avg, % dev) 1.4 -1.7 0.3 1.3 0.3 -1.9 0.6 1.0 0.5 0.3

Nominal Expenditure GDP - $bn 324 328 354 377 394 324 350 371 390 410

Prices and Employment - annual % change

CPI 2.5 1.5 7.0 4.2 1.7 1.4 5.9 5.2 1.7 2.2

Employment 2.5 0.2 3.2 0.8 0.6 0.6 3.7 0.9 0.4 1.7

Unemployment Rate % 4.2 4.6 3.1 3.1 3.8 4.9 3.2 3.1 3.7 3.9

Wages - ahote 3.2 4.1 4.6 4.5 2.8 2.6 4.6 4.1 4.8 2.9

Productivity (ann av %) 0.2 -1.9 2.2 2.5 1.2 -3.3 3.5 1.4 1.6 1.4

Unit Labour Costs (ann av %) 2.9 4.6 4.2 2.2 2.2 5.7 2.5 3.7 2.1 1.5

House Prices 7.8 24.1 14.6 -11.5 0.0 17.0 25.0 -9.2 -2.5 3.3

External Balance

Current Account - $bn -7.6 -8.2 -22.1 -24.5 -22.0 -2.7 -20.2 -27.0 -22.9 -19.1

Current Account - % of GDP -2.3 -2.5 -6.2 -6.5 -5.6 -0.8 -5.8 -7.3 -5.9 -4.7

Government Accounts - June Yr, % of GDP

OBEGAL (core operating balance) -7.3 -1.3 -5.7 -0.2 0.5

Net Core Crown Debt (excl NZS Fund Assets) 26.3 30.1 37.6 40.1 39.9

Bond Programme - $bn (Treasury forecasts) 29.0 45.0 20.0 18.0 18.0

Bond Programme - % of GDP 9.0 13.7 5.6 4.8 4.6

(1)

Financial Variables

NZD/USD 0.60 0.71 0.69 0.72 0.70 0.71 0.68 0.72 0.71 0.71

USD/JPY 108 109 119 118 110 104 114 120 112 112

EUR/USD 1.11 1.19 1.10 1.17 1.25 1.22 1.13 1.15 1.23 1.23

NZD/AUD 0.97 0.93 0.93 0.90 0.92 0.94 0.95 0.90 0.92 0.92

NZD/GBP 0.49 0.51 0.52 0.53 0.50 0.53 0.51 0.53 0.50 0.50

NZD/EUR 0.55 0.60 0.62 0.62 0.56 0.58 0.60 0.63 0.58 0.58

NZD/YEN 65.1 77.5 81.5 85.0 77.0 73.6 77.4 86.4 79.5 79.5

TWI 68.9 74.8 73.9 75.2 72.6 74.3 73.0 75.6 73.6 73.6

Overnight Cash Rate (end qtr) 0.25 0.25 1.00 3.00 2.75 0.25 0.75 2.75 3.00 2.00

90-day Bank Bill Rate 0.71 0.33 1.45 3.15 2.80 0.26 0.92 3.00 3.05 2.15

5-year Govt Bond 0.80 1.00 2.90 3.25 2.85 0.40 2.20 3.25 3.00 2.50

10-year Govt Bond 1.15 1.75 3.20 3.45 3.30 0.90 2.35 3.45 3.40 3.00

2-year Swap 0.65 0.50 3.00 3.40 2.75 0.28 2.22 3.40 3.00 2.25

5-year Swap 0.80 1.15 3.20 3.45 3.05 0.49 2.56 3.45 3.20 2.70

US 10-year Bonds 0.90 1.60 2.10 3.00 3.00 0.90 1.45 3.00 3.00 3.00

NZ-US 10-year Spread 0.25 0.15 1.10 0.45 0.30 0.00 0.90 0.45 0.40 0.00

(1)

Average for the last month in the quarter

Source for all tables: Statistics NZ, EcoWin, Bloomberg, Reuters, RBNZ, NZ Treasury, BNZ

www.bnz.co.nz/research Page 10Markets Outlook 11 April 2022

Key Upcoming Events

All times and dates NZT

Median Fcast Last Median Fcast Last

Monday Wednesday Continued

NZ Card Spending Total MoM Mar -7.6% JN Core Machine Orders MoM Feb -1.5% -2%

CH PPI YoY Mar 8.8% NZ RBNZ MPR, OCR Apr 1.2% 1.2% 1%

CH CPI YoY Mar 0.9% UK CPI YoY Mar 6.7% 6.2%

UK Monthly GDP (MoM) Feb 0.8% JN BOJ Kuroda Speech at the 97th Trust Companies Assembly

UK Industrial Production MoM Feb 0.7% CH Trade Balance CNY Mar 604.68b

UK Trade Balance GBP/Mn Feb -£7.15b -£16.2b Thursday

JN BOJ Governor Kuroda speaks US PPI Ex Food and Energy YoY Mar 8.4% 8.4%

CH Aggregate Financing CNY Mar 3550.0b 1190.0b CA Bank of Canada Rate Decision Apr 1% 0.5%

CH New Yuan Loans CNY Mar 2740.0b 1230.0b NZ Business NZ Manufacturing PMI Mar 53.6

Tuesday AU Employment Change Mar 30.0k 50k 77.4k

US Fed’s Evans, Bostic, Bowman, Waller speak AU Unemployment Rate Mar 3.9% 3.9% 4%

NZ NZIER QSBO, Net confidence, sa 1Q -34 NZ Govt reviews COVID traffic light settings

NZ Net Migration SA Feb -558 EC ECB Deposit Facility Rate Apr -0.5% -0.5% -0.5%

UK BRC Sales Like-For-Like YoY Mar 2.7% Friday

AU NAB Business Confidence Mar 13 Good Friday

GE CPI YoY Mar 7.3% 7.3% US Retail Sales Advance MoM Mar 0.6% 0.3%

UK ILO Unemployment Rate 3mth Feb 3.8% 3.9% US Initial Jobless Claims Apr 173k 166k

GE ZEW Survey Expectations Apr -48.5 -39.3 US Continuing Claims Apr 1500k 1523k

NZ Border opens to Australians, temp. work & student visa holders US Business Inventories Feb 1.3% 1.1%

US NFIB Small Business Optimism Mar 95 95.7 US U. of Mich. Sentiment Apr 59 59.4

Wednesday US Fed’s Mester, Harker speak

US CPI Ex Food and Energy YoY Mar 6.6% 6.4% Saturday

US Fed’s Brainard speaks US Empire Manufacturing Apr 1 -11.8

NZ Food Prices MoM Mar 0.3% 0.1% US Manufacturing Production Mar 0.5% 1.2%

US Fed’s Barkin speaks

Historical Data

Today Week Ago Month Ago Year Ago Today Week Ago Month Ago Year Ago

CASH AND BANK BILLS SWAP RATES

Call 1.00 1.00 1.00 0.25 2 years 3.61 3.41 3.01 0.46

1mth 1.38 1.34 1.05 0.26 3 years 3.70 3.51 3.16 0.63

2mth 1.53 1.51 1.27 0.29 4 years 3.70 3.52 3.20 0.84

3mth 1.68 1.67 1.49 0.32 5 years 3.70 3.52 3.22 1.07

6mth 2.21 2.19 1.98 0.33 10 years 3.69 3.49 3.28 1.85

GOVERNMENT STOCK FOREIGN EXCHANGE

04/23 2.58 2.48 2.10 0.24 NZD/USD 0.6847 0.6948 0.6746 0.7030

04/25 3.29 3.11 2.76 0.65 NZD/AUD 0.9188 0.9212 0.9385 0.9222

04/27 3.38 3.21 2.89 1.03 NZD/JPY 84.96 85.32 79.73 76.90

04/29 3.42 3.25 2.97 1.43 NZD/EUR 0.6283 0.6335 0.6166 0.5903

05/31 3.44 3.29 3.02 1.73 NZD/GBP 0.5254 0.5297 0.5189 0.5116

04/33 3.45 3.30 3.05 1.97 NZD/CAD 0.8607 0.8676 0.8651 0.8832

04/37 3.49 3.38 3.20 2.28

05/41 3.53 3.44 3.31 2.58 TWI 73.9 74.6 73.5 74.3

GLOBAL CREDIT INDICES (ITRXX)

Nth America 5Y 71 64 75 51

Europe 5Y 77 70 80 51

www.bnz.co.nz/research Page 11Markets Outlook 11 April 2022 Contact Details BNZ Research Stephen Toplis Craig Ebert Doug Steel Jason Wong Nick Smyth Head of Research Senior Economist Senior Economist Senior Markets Strategist Senior Interest Rates Strategist +64 4 474 6905 +64 4 474 6799 +64 4 474 6923 +64 4 924 7652 +64 4 924 7653 Main Offices Wellington Auckland Christchurch Level 4, Spark Central 80 Queen Street 111 Cashel Street 42-52 Willis Street Private Bag 92208 Christchurch 8011 Private Bag 39806 Auckland 1142 New Zealand Wellington Mail Centre New Zealand Toll Free: 0800 854 854 Lower Hutt 5045 Toll Free: 0800 283 269 New Zealand Toll Free: 0800 283 269 National Australia Bank Limited Ivan Colhoun Alan Oster Ray Attrill Skye Masters Global Head of Research Group Chief Economist Head of FX Strategy Head of Markets Strategy +61 2 9237 1836 +61 3 8634 2927 +61 2 9237 1848 +61 2 9295 1196 Wellington New York Foreign Exchange +800 642 222 Foreign Exchange +1 212 916 9631 Fixed Income/Derivatives +800 283 269 Fixed Income/Derivatives +1 212 916 9677 Sydney Hong Kong Foreign Exchange +61 2 9295 1100 Foreign Exchange +85 2 2526 5891 Fixed Income/Derivatives +61 2 9295 1166 Fixed Income/Derivatives +85 2 2526 5891 London Foreign Exchange +44 20 7796 3091 Fixed Income/Derivatives +44 20 7796 4761 This document has been produced by Bank of New Zealand (BNZ). BNZ is a registered bank in New Zealand and is only authorised to offer products and services to customers in New Zealand. Analyst Disclaimer: The Information accurately reflects the personal views of the author(s) about the securities, issuers and other subject matters discussed, and is based upon sources reasonably believed to be reliable and accurate. The views of the author(s) do not necessarily reflect the views of the NAB Group. No part of the compensation of the author(s) was, is, or will be, directly or indirectly, related to any specific recommendations or views expressed. Research analysts responsible for this report receive compensation based upon, among other factors, the overall profitability of the Global Markets Division of NAB. NAB maintains an effective information barrier between the research analysts and its private side operations. Private side functions are physically segregated from the research analysts and have no control over their remuneration or budget. The research functions do not report directly or indirectly to any private side function. The Research analyst might have received help from the issuer subject in the research report. New Zealand: The information in this publication is provided for general information purposes only, and is a summary based on selective information which may not be complete for your purposes. This publication does not constitute any advice or recommendation with respect to any matter discussed in it, and its contents should not be relied on or used as a basis for entering into any products described in it. Bank of New Zealand recommends recipients seek independent advice prior to acting in relation to any of the matters discussed in this publication. Any statements as to past performance do not represent future performance, and no statements as to future matters are guaranteed to be accurate or reliable. Neither Bank of New Zealand nor any person involved in this publication accepts any liability for any loss or damage whatsoever which may directly or indirectly result from any advice, opinion, information, representation or omission, whether negligent or otherwise, contained in this publication. USA: If this document is distributed in the United States, such distribution is by nabSecurities, LLC. This document is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of nabSecurities to create legal relations on the basis of information provided herein. www.bnz.co.nz/research Page 12

You can also read