Market Outlook & Strategy 2019 - A Tale of Two Halves - JF Apex Research 23 February 2019 - Apex Equity

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market Outlook & Strategy 2019

A Tale of Two Halves

By

JF Apex Research

23 February 2019 1

Contents

Market Review 2018

Malaysian Economy & Outlook

Equity Outlook 2019

Events to watch out

Implications of yield curve to equity market

Fundamental & Technical Outlooks

Investment Strategy

Sector at a glance

2

Market Review 2018

• A confluence of unfavourable internal and external factors weighed on the local

market – GE14, trade war, rate hike in the US, slowing global growth.

• With the intense foreign selling, the FBM KLCI ended below the 1700-point level with

a negative return of 5.9% for 2018.

3

Market Review 2018

• Net outflow of foreign funds: RM11.5b for 2018 vs net inflow of RM10.3b in 2017.

• The vigorous net selling by foreign investors was evident during the period of May-July

as a result of policy uncertainty with the new ruling govt., unfavourable external factors

and uninspiring corporate earnings.

4

Market Review 2018

• All sub-sector indexes registered negative returns except for Finance & Consumer

sectors which stood out among the crowd.

• Construction sector was the worst performer (-50.3%) as several mega projects were

slashed and/or are currently under reviewed.

• Industrial & Service/Trading Indices were reclassified as Industrial Product &

Services, Telecommunication & Media, Utility, Transport, Energy, Healthcare Indices

effective Sept 18 and hence no compilations and comparisons.

5

Market Review 2018

• The FBM KLCI outperformed most of the regional peers due to relatively less net

inflow of foreign funds into the local bourse for the past few years against these

nations and the local benchmark index was well supported by local funds.

• Most of the emerging and developed markets recorded negative returns.

6

Market Review 2018

PER (X) Dividend yield (%)

2018 2019 2020 2018 2019 2020

FBMKLCI Index 16.6 15.9 15.0 3.3 3.4 3.7

HSI Index 10.7 9.7 8.8 3.9 4.2 4.5

FSSTI Index 12.5 11.7 10.9 4.2 4.4 4.6

JCI Index 16.6 14.6 13.1 2.2 2.4 2.7

SET Index 14.5 13.4 12.3 3.3 3.6 3.9

PCOMP Index 17.6 15.7 13.9 1.7 1.8 2.0

KOSPI Index 8.7 8.6 7.8 2.3 2.4 2.7

TWSE index 12.7 12.5 11.8 4.7 5.0 5.1

Average (ex-KLCI) 13.3 12.3 11.2 3.2 3.4 3.6

KLCI's premium over

region (%) 24.6 29.6 33.7 3.2 1.5 1.8

• Pricey valuation against Asian peers as regional markets tumbled.

• The local bourse now trades at 16.6x/15.9x 2018/2019 PE, the second highest (for

2018) or the highest PER (for 2019) after the Philippines (17.6x 2018 PE and 15.7x

2019 PE).

• The FBM KLCI is trading at 24.6%/29.6% premium to other major Asian indices with

averages of 13.3x 2018 PE and 12.3x 2019 PE.

• Dividend yield wise, the local bourse looks unattractive as it renders 3.3%/3.4% for

2018/2019 vs regional peers (3.2%/3.4%).

7

Malaysian Economic Outlook

Moderate GDP growth in 2018

2018: (+4.7%) vs. 2017: (+5.9%)

Moderate economic activities in GDP’s components

GDP is expected to grow at +4.8% in 2019 – driven by private consumption and investment

Government spending (Public investment): Key projects such as Pan Borneo Highway, MRT2

line and Gemas – Johor Bahru Electrified Double Track

Private consumption: stable labour market amid rising wages and higher disposable income

8

Malaysian Economic Outlook

Soft inflation during 2018

2018:+0.9% vs. 2017: +3.7%

Due to lower cost of transportation, tax holiday during June’18-Aug’18, muted impact of SST

since its implementation in September amid high base effect from a year ago

2019’s CPI to grow at +2.0% y-o-y

Inflationary pressure from floating fuel price and low base effect arising from the tax holiday

period

Overnight policy rate (OPR) maintain at 3.25% in 2019

Amid prevailing robust economic growth and manageable inflation

9

Malaysian Economic Outlook

Languid 2018 exports and imports

Exports: +6.8% vs +18.8% during 2017 – moderate exports of all main components to key trading

partner

Imports: +4.9% vs +19.8% in 2017 – easing imports of intermediate, capital and consumption

goods

External trade remains tepid for 2019

Exports will grow at a modest pace, still underpinned by manufacturing goods, especially E&E

products

Imports will grow moderately, continued to be supported by consumption and capital goods as well

as intermediate goods

10Equity Outlook 2019

• A tale of two halves for the market – 1H19: Volatile and possibly in a

correction mode for most of the time; 2H19: Market recovery with improving

market sentiment.

• 1H19 – Clouded by a slew of uncertainties with majority risks being

concentrated in the first half of the year. Higher risk premium weighs on

global equity markets with rising risk-off appetite.

• 2H19 – Policies coming to rescue, i.e. possibility of loosening monetary policy

& fiscal stimulus by the US and China so as to prevent any global economic

downturn coupled with uncertainties and risks start to dissipate.

11Equity Outlook 2019 Our house view: • NEUTRAL on outlook – Our year-end 2019 FBM KLCI target of 1700 points. • Our KLCI target is based on market EPS growth forecasts of -3.1% for 2018 and +4.4% for 2019 with target PER of 16.1x 2019 PE (+0.5 SD above mean). • At a worst case scenario, we could see local bourse trending as low as 1525- point level (14.4x 2019 PE or -0.5 SD below mean) in 1H19, indicating 19% decline from the record closing of 1895 points in April 18. • Déjà vu of 2014/2015? To recap, the FBM KLCI registered all time high of 1896 points in July 2014 before seeing oil price collapsed and dragged the index to 1532 points in Aug 15 (19% drop). • Crude oil (Brent): US$60/barrel (average) • USD/MYR: 4.07 (average) • CPO: RM2232/MT (average) 12

Events to watch out

Major events which could derail stock market in 1H19 are: -

• Uncertainty returns upon end of 90-day trade truce.

• Potential slowdown of China economy.

• Brexit bombshell.

• Escalating geopolitical risk in the region.

• US Fed rate hike still on track, albeit at a slower pace.

• Policy uncertainty, dismal corporate earnings and dip in crude oil prices hold

back foreign interests in local bourse.

13Events to watch out

Uncertainty re-emerges upon end of 90-day tariff ceasefire

• End in early March 19.

• Temporary relief to global financial markets.

• We are cautious on the outcome and foresee trade dispute to remain unresolved.

• Arrest of Huawei CFO complicated the talks between the US and China.

• The US is, in fact, escalating a ‘technological cold war’ with China and the on-going tussle is

not centred on tariff and trade per se.

14Events to watch out

Potential slowdown of China economy

• Nov 18’s industrial output and retail sales growth were significantly below expectations.

• Caixin/Markit Manufacturing Purchasing Managers’ Index (PMI) for Dec 18 fell to 49.7

from 50.2 in Nov 18 – the first contraction since May 17.

• China’s economic slowdown set to deepen in 1H19 before seeing the Chinese govt. to

embark on another fresh round of fiscal stimulus and loosening monetary policy to spur

credit growth.

• China expected to grow at 6-6.5% for 2019 vs estimate of 6.6% in 2018 and 6.9% in

2017.

15

• High corporate debt (c.160% of GDP) could mean slower economic growth.Events to watch out

Source: Capital Economics, CEIC

16Events to watch out

17Events to watch out

Brexit bombshell

• Brexit will formally take effect in end Mar 19.

• Possibly a ‘no deal’ Brexit!

• If so, there would be no 21-month transition period and consumers, businesses and public

bodies would have to respond immediately with no clarity about what would happen.

18Events to watch out

Political risk in the region

• Few general elections in ASEAN.

• Thailand – Feb 19, Indonesia – April 19, The Philippines – May 19.

• Expecting exodus of foreign funds from these nations pre and post elections.

• Political stabilities and executions are highly watched.

• Malaysia might benefit, to a certain extent, as some foreign funds could opt to park their

monies in local bourse while deciding their next moves.

19Events to watch out

US Fed rate hike still on track, albeit at a slower pace

• Dec 18’s rate hike brought the Fed funds rate to 2.25%-2.50%.

• Fed may soothe volatile financial markets and counter any slowing economy by softening

its hawkish tone.

• Federal Reserve is expected to have 2 more rate hikes this year against earlier

expectations of 3 times.

• Probably happen during 1H19 (Mar and June 19).

• Strong dollar would persist in 1Q/2Q19 before weakening in 2Q/3Q19 onwards.

20Events to watch out Unfavourable domestic factors hold back foreign interests • Foreign investors rather adopt ‘wait-and-see’ attitude and would continue to trade cautiously in the local bourse, at least for 1H19. • Policy consistency and execution in doubt? Reviewing certain mega projects, undertaking some reform agendas, diplomatic relations with Singapore & China, highly disputed third national car project & Johor-Singapore third bridge. • Uninspiring corporate earnings after dismal 9MFY18 results. Our market EPS growth for 2018 and 2019 are -3.1% and +4.4% respectively. Banking, Utilities, Healthcare sectors and Petronas related counters shall underpin market earnings moving forward. • Oil price remains sluggish does not bode well for the country as Malaysia is a net oil exporter (2014 market downtrend in line with collapse of oil price) • All eyes on fiscal deficit and sovereign rating with current depressed oil price – Govt. targets fiscal deficit of 3.7% in 2018 and 3.4% for 2019 based on oil price assumption of US$70/barrel (vs current level of ~US$60). • Resilient domestic economic growth – GDP: 4.7% (2018) and 4.8% (2019) mainly driven by private consumption and private investment amid softening public consumption and investment. 21

Events to watch out

Era of shrinking liquidity

• Liquidity has driven the market run for the past 9-10 years since the 2008/09 Lehman

Crisis.

• To recap, the US ended its QE in end 2014 and preluded its normalization of interest rate

in a gradual manner since end-15 with its first rate hike.

• ECB officially ended its QE in Dec 18 but would keep reinvesting cash from maturing

bonds for a period of time. It would maintain its primary rates unchanged till Aug/Sept 19.

• Positive surprise to the markets if Fed reduces rate and ECB restarts its QE in 2019?

22Events to watch out

Repeat of 10-year cycle?

• 1987 - Black Monday in the US; 1997/98 – Asian Financial Crisis; 2008/09 –

Global/Lehman Financial Crisis.

• Investors would trade cautiously with reluctance of taking ‘long-term

investment horizon’.

• However, market usually exhibits a strong rally ahead of any perceived

market crash that could happen.

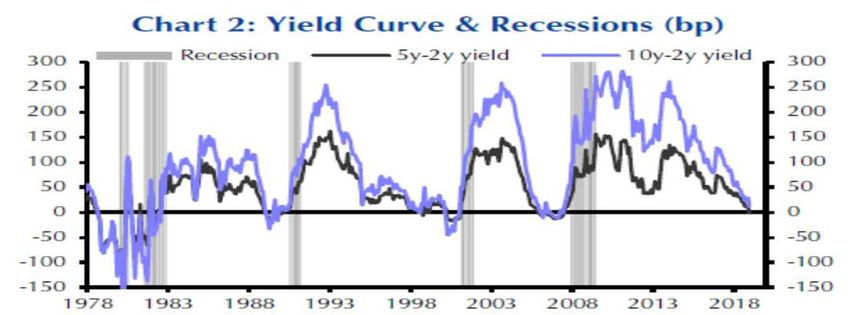

23Implications of yield curve Flattening of yield curve signaling recession ahead? • Recessions in the US have always preceded by an inversion in the yield curve but not every inversion has been followed by a recession, though it does generally signal economic risk. • The shallow slope of the yield curve, i.e. the yield spread between 2-yr and 10-yr Treasury Notes is currently at 18 bps (as of end Dec 18), the flattest in a decade and since 2007 (pre Lehman crisis). • Investors now believe the Fed’s actions will cause the economy to slow and yields to fall, and hence buying more longer-dated paper to lock in current yields, rather than taking the risk of continually rolling over shorter-dated debt where the yields they earn are declining. • A flattening yield curve can have a negative impact to the US banking stocks as they are typically 24 borrow short and lend long.

Source: Capital Economics

25Implications of yield curve

Narrowing Yield Spread between 10-yr MGS & US Treasury Note

• As a result of US Fed’s normalization policy in the form of rate hikes (now at 2.25-2.50% vs Malaysian

OPR of 3.25%).

• 220-240bps in mid-2016 to about 150bps as of end-2017, and thereafter to about 130bps currently (as

of Dec 18).

• Trend is expected to persist in the near future with few more rate hikes in the US while Malaysia has

limited leeway for monetary tightening in view of austerity measures undertaken by the govt. to reduce

debt.

26

• Continuous exit of foreign funds from our capital markets?Implications of yield curve

Implications of rising bond Yield to equity markets

• Asset de-rating is underway for the local bourse.

• Premium between the market earnings yield (market E/P) and 10-yr MGS is narrowing, i.e. stock

getting less attractive to fixed income.

• FBM KLCI’s earnings yield: 5.3% (current P/E of 19x) vs 10-yr MGS: 4.0%.

• Rising yields could alter the value proposition for equities vs fixed income for years to come.

• An uptick of US 10-year Treasury yield – now at 2.7% (vs average of 2.66% for the past 10 years).

• Risky assets in emerging markets look unappealing.

• US Treasury yield is expected to inch up in the near term (bond price trending down whilst yield

picking up) pursuant to Fed tightening, i.e. unwinding its balance sheet and issuance more Treasury

notes and govt. bonds to fund Trump’s tax cut, infrastructure spending.

27Fundamental Outlook

• Market valuation is fairly priced.

• Currently trading at 15.9~16.0x 2019 PE, which is at the range of

+0.5~+1.0 SD above its historical mean PE of 15~16x.

• 1H19: Absence of any positive catalyst whilst immediate outlook

remains uncertain and challenging.

• 2H19: Anticipating foreign funds to return to the emerging markets

which would benefit the local equity market banking on policy

reversal, i.e. stimulus fiscal policy & loosening monetary policy.Technical Outlook

FBM KLCI Technical Chart

29Technical Outlook

• Last year, the FBM KLCI declined from an all-time high near 1900

points in April. Hit a low of 1626 points in December before

rebounding to above1700 points recently.

• Technical indicators are mixed with the RSI being flat below the

overbought zone while the MACD is climbing above the signal line.

• Immediate term: Positive view as the index has just crossed above

the 100-day moving average (blue line). Above the support of 1700

points, further downside if this level fails to hold.

• Longer term: Negative view as the index remains in the downtrend

channel since April 2018. A reversal can be seen if the resistance of

1740 points is broken.Investment Strategy

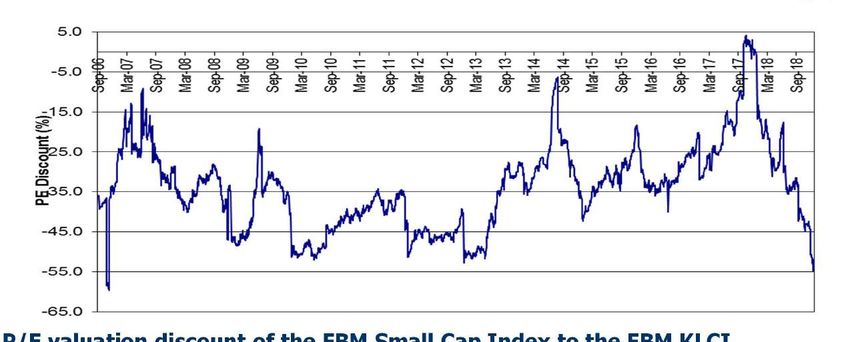

P/E valuation discount of the FBM Small Cap Index to the FBM KLCI

• Are small caps ripe for picking? Valuation looks appealing now.

• The Small Cap Index is currently trading at 8.0x forward PE, which is below its historical mean of

10.4x.

• Valuation gap between the small-cap and large-cap counters has widened to the current 52% PE

discount, which is at its high side (traditionally trading at an average of 34% PE discount)

• Upcycle: 5~25% PE discount; Downcycle: 35~55% PE discount.

31

• We advise investors to bottom fish in 2H19 due to low liquidity & high beta in nature.Investment Strategy

• Equities de-rating well underway pursuant to shrinking liquidity and risk-off sentiment.

• Bottom-up approach in stock selection under current heightened volatility.

• Investors shall stay defensive, favouring Healthcare (IHH, KPJ, Apex Healthcare, YSP,

Top Glove, Hartalega, Kossan, Supermax), Consumer (Brewery – Carlsberg, Heineken,

Non-discretionary – F&N, Nestle, Dutch Lady, Ajinomoto, QL, CCK, Apollo, Cocoland,

Spritzer, Caring, Aeon), and REIT (retail & industrial – IGB, Sunway, Pavilion, Axis).

• Sectors ‘in the theme’ or relatively shelter from prevailing business downcycle – Banking

& Finance (Consumer and SME financing – Aeon Credit, Public Bank, HL Bank, Maybank,

Alliance Bank, ELK-Desa, Takaful), Renewable energy/Utilities (Cypark, Pestech,

Tenaga, Gas Malaysia), O&G (Downstream – Yinson, Dialog, Serba Dinamik), Aviaiton

(AirAsia), Automobile (UMW, Bermaz), Concessionaire (Perak Transit, UEM Edgenta,

PBA), Industrial (SAM, Scientex, Chin Well, Wellcall, VS), Car vendors (Proton - D&O, 32

Pecca), Water proxy (Engtex).Investment Strategy

• Positive: Automobile, Consumer, Glove sectors

• Neutral: Construction, Plantation, Property, Telco, O&G sectors

• Negative: Industrials/Manufacturing sector

• Our top picks under coverage are: UMW(TP: RM6.88), Top Glove (TP:

RM6.37), Padini (TP: RM5.00), LBS (TP: RM1.06), Tasco (TP: RM1.35) and

Pantech (TP: RM0.63).

33Automotive Overweight

• Tax holiday to boost 2018’s TIV – Auto’s TIV grew 3.8% yoy in 2018 to 598.7k units (vs 2017: 576.6k

units)

• MAA’s TIV forecast of 585k in 2018 vs our forecast of 588.1k units

• Encouraging car sales underpinned by ‘zero-rated’ GST during June’18-Aug’18

• Among top market players in 2018: Perodua (38%), Honda (18%), Proton (13%), and Toyota (11%)

Total Industry Volume 2018

80,000

70,000

60,000

50,000

Commercial Vehicles

40,000

Passenger Vehicles

30,000

20,000

10,000

-

34• Steady outlook for automotive sector in 2019 – Forecast another stable growth of 2.1% for 2019 TIV to

611.3k units (vs 2019 MAA’s forecast of RM600k units)

• Underpinned by new launches, better consumer sentiment towards big ticket items, higher approval

loan rate as well as improvement in profit margin following the strengthening in Ringgit

• NAP to unveil in 2019

• BUY on UMW (TP: RM6.88) – Group to re-focus on its three core businesses which will resume

growth momentum over the medium to longer term

• BUY on Tan Chong (TP: RM1.68) – Group is able to sustain its growth momentum and earnings

recovery is well underway

Total Industry Volume for 2012-2019F

800000

700000

600000

500000

400000

300000

200000

100000

0

2012 2013 2014 2015 2016 2017 2018 2019F

TIV MAA Forecast TIV JF Apex Forecast

35Property Marketweight

• Outlook remains subdued - Slower GDP growth, low affordability pursuant to rising cost of living,

stringent mortgage approval, and oversupply of residential and commercial properties will continue to

weigh on the property market. Hence, we do not foresee the fundamentals of the sector to improve in

2019.

• Tepid transaction activity - Property transaction volume and value remained sluggish in 1H2018.

Total volume 1H2018: -2.4% yoy; Total value 1H2018: -0.1% yoy; House Price Index (HPI) 2017:

+6.5% yoy; Existing stock of residential property in 2QCY18: +3% yoy; Unsold residential property in

2QCY18: +40% yoy.

• Dismal corporate earnings - Most of the property counters delivered lacklustre yoy earnings growth

for its 9MFY18 results due to lower progress billings, higher costs coupled with tumbling new sales. FY19

financial results of the developers are expected to be uninspiring with lower topline as well as shrinking

margins.

• Declining margins - We expect developers to fork out more rebates or incur higher marketing costs

to brush up their promotional activities to market their offerings and inventory. Moreover, with the

concentration of selling affordable housings, it would also affect developers’ product margins.

36• Distressed valuation but no immediate re-rating catalyst.

• The majority of property counters are trading at rock-bottom valuations, 40-60% discount to their

RNAVs with some even trading below their BVs.

• PE multiples wise, large cap stocks and mid-to-small cap stocks are now trading at 10-15x forward PE

and 5-9x forward PE respectively.

• We do not foresee the sector to have a meaningful recovery in the short term due to

prevailing poor market sentiment towards property counters.

• Maintain NEUTRAL on the sector – Long-term investment wise, we have BUYs on LBS

(Target Price: RM1.06), Titijaya (Target Price: RM0.38) and Tambun Indah (Target Price:

RM0.96); SELL on HCK Capital (Target Price: RM1.06).

• Other non-rated property counters under our investment radar are – Mah Sing, Matrix Concept and

UOA Development.

37Plantation Market weight

• Plantation Index underperformed FBM KLCI in 2018 – Soft CPO price

– Soft CPO Price – Higher supply growth outweighed demand growth (record

high inventory of over 3m mt)

– Supply growth - Lifted by high inventory carried forward from 2017 to 2018,

coupled with a decent production in 2018.

– Demand growth – Buoyed by higher domestic intake amid flat export growth

in 2018.

• CPO production forecast for 2019 is 20.1m mt

• CPO average selling price for 2019 is RM2232/mt500,000

0

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Jan2017

Feb2017

Mar2017

Apr2017

May2017

Jun2017

Plantation

Jul2017

Aug2017

Source: JF Apex, MPOB

Sep2017

Oct2017

Nov2017

Dec2017

Jan2018

Feb2018

Mar2018

Apr2018

May2018

Jun2018

Jul2018

Aug2018

Sep2018

Oct2018

Nov2018

Dec2018

Jan2019

Feb2019

Mar2019

Apr2019

May2019

Jun2019

Jul2019

Aug2019

Sep2019

Oct2019

Nov2019

Dec2019

Historical and forecast Palm Oil's inventory (Jan2017-Dec2019)

Export

Production

Closing Stock

Opening Stock

Market weightPlantation Market weight

• Maintain neutral view on plantation sector

- expect CPO ASP will remain soft

- Higher operating costs (minimum wage hike)

- long-standing challenge of shortage of labour

– Stock under our coverage:

• HOLD calls for:

- Kuala Lumpur Kepong (target price: RM22.91)

- IOI Corporations (target price: RM4.37)

- Genting plantations (target price: RM10.37)

due to soft CPO price outlook

- Kim Loong Resources (target price: RM1.25)

and their rich valuation

- C.I. Holdings (target Price RM1.70).

• Upgrade from SELL to HOLD for IJM Plantation (target Price RM1.50) in view

its recent retreat in share price.

• HOLD on Boilermech (target price: RM0.68) due to weak outlook of planters.Rubber Glove Overweight (upgraded) • Strong USD benefiting glove makers o US interest rate hike spillover to 2019 o Revenue mostly denominated in USD o Positive topline growths (ie. Higher average selling price) • Demand remain robust o Rising global demand for gloves o Average 10% growth rate per year • Minimal impact from vinyl gloves segment o Intense competition - supply disruption for China normalized o Lower impact - contribute around 10% to the topline • Stable cost of material o Latex price remain stable/increase steadily - supply outweighs demand. o Nitrile Butadiene remain stable - low crude oil price o If any spike in costs, glove makers are able to pass on costs customers

• Minimal impact from rising operating cost o Natural gas tariff – less than 10% of overall operating costs o Minimum wages – offset by strengthening of USD against MYR • Key risk o Oversupply of gloves or Overcapacity o Rapid rise in minimum wages • Favourable outlook o Continue to deliver growth o Demand for nitrile disposable glove remains intact • BUY on Top Glove (TP: RM6.37) due to strong growth prospects • HOLD on Hartalega ( TP: RM6.05) as share price fully valued • Non-rated stocks such as Supermax, Kossan are worth a look.

Consumer Overweight

• Strong surge in (Consumer Sentiment Index) CSI

• Surpassed threshold of 100-point level

• Foresee CSI to maintain at the healthy level for 1H2019

• Better spending for lower and middle income group

• Budget 2019 announcement.

• Lower fuel price, increase in minimum wages, cash grants for B40

household, 30-day rapid travel passes• Positive outlook for the sector

• Better consumption - staple goods, small ticket and fast moving

consumer goods

• Eg, Nestle, QL, Sprtizer, Aeon

• Less positive – big ticket items as 3 month tax holiday in 2018 ended

• Key risk

• Weakening of MYR

• Threat of competition from online retailers

• BUY call on Padini (TP: RM 5.00) as value re-emerges from recent sell

down

• BUY on Oriental Food (TP: RM0.66) as elevated operating costs weigh on

earnings

• HOLD call on Hai-O (TP: RM3.00) due to slowing MLM division

• HOLD on Ajinomoto (TP: RM21.60) due to higher marketing expenses,

raw material cost coupled with fluctuations in forex.Construction Market weight

• Worst performer in 2018 following cut and revision in mega infrastructure

projects.

– Under review (total value worth RM150b) :

- East Coast Rail Line (c.RM55b) – regained traction with recent news flow

- KL-Singapore High Speed Rail (c.RM60b) – without timeline

- MRT 3 (c.RM40b) - without timeline

– Cost cutting (total amount reduction of RM23.84b):

- MRT2 (RM39.35b -> RM30.53b, -22.4%)

- LRT3 (RM31.65b -> RM16.63b, -47%)Construction Market weight

• Focus shifting from mega projects to smaller scale jobs (building

works) - especially those related to benefits of “rakyat” or public amenities, i.e.

schools, hospitals and affordable housings.

• Construction players to face margin contractions - intense competition

among contractors to secure smaller pool of jobs.

• Low orderbook replenishment but earnings are supported by sizeable

outstanding orderbook - outstanding orderbook for construction companies are

close to RM81.8b, with an average earnings visibility of around 2 years.Estimated Outstanding Orderbook for Listed Construction Companies

Name RM>3B Name > RM 5b

VIZIONE HOLDINGS BHD 3,910 GAMUDA BHD 11,100

AHMAD ZAKI RESOURCES BERHAD 3,200 IJM CORP BHD 8,800

EKOVEST BHD 3,000 WCT HOLDINGS BHD 6,000

HOCK SENG LEE BERHAD 3,000 GEORGE KENT (MALAYSIA) BHD 5,500

SUNWAY CONSTRUCTION GROUP BH 5,205

Name RM>1B Name > RM 2b

JAKS RESOURCES BHD 1,880 KERJAYA PROSPEK GROUP BHD 2,670

MGB BHD 1,830 EVERSENDAI CORP BHD 2,400

MUHIBBAH ENGINEERING (M) BHD 1,800 GABUNGAN AQRS BHD 2,400

KIMLUN CORP BHD 1,800 PESONA METRO HOLDINGS 2,000

MUDAJAYA GROUP BHD 1,800

TRC SYNERGY BHD 1,636

GADANG HOLDINGS BHD 1,510

CREST BUILDER HOLDINGS BHD 1,300

MITRAJAYA HOLDINGS BHD 1,200

ECONPILE HOLDINGS BHD 1,100

Name RM 500m

PUNCAK NIAGA HOLDINGS BHD 489 BINA PURI HOLDINGS BHD 900

HO HUP CONSTRUCTION CO BHD 375 ADVANCECON HOLDINGS BHD 876

IREKA CORP BHD 323 IKHMAS JAYA GROUP BHD 820

FAJARBARU BUILDER GROUP BHD 318 OCR GROUP BERHAD 791

BENALEC HOLDINGS BHD 239 INTA BINA GROUP BHD 748

PINTARAS JAYA BHD 200 GDB HOLDINGS BHD 614

WIDAD GROUP BHD 93

MERCURY INDUSTRIES BHD 25

Source: Companies’ annual report, quarterly reports and media as at December 2018Construction Market weight

• Maintain market weight for construction sector - lacking infrastructure projects and

positive news flow to spur the sector for 2019

• Valuation looks cheap - construction sector is now trading at 10.6x trailing PE, which is

below its historical average of 15.6x.

• BUY calls:

– IJM Corporation (target price: RM2.05) Orderbook: RM8b/ Property unbilled sales:

RM2b

– Gadang (target price: RM0.68) Orderbook: RM1.43b/ Property unbilled sales:

RM100.9m

– HOLD call :

– Gamuda (target price: RM2.70) Orderbook: RM11.1b/ Property unbilled sales: RM2.3b

– Ikhmas Jaya (target price: RM0.11) mainly due to its sizeable trade receivable despite

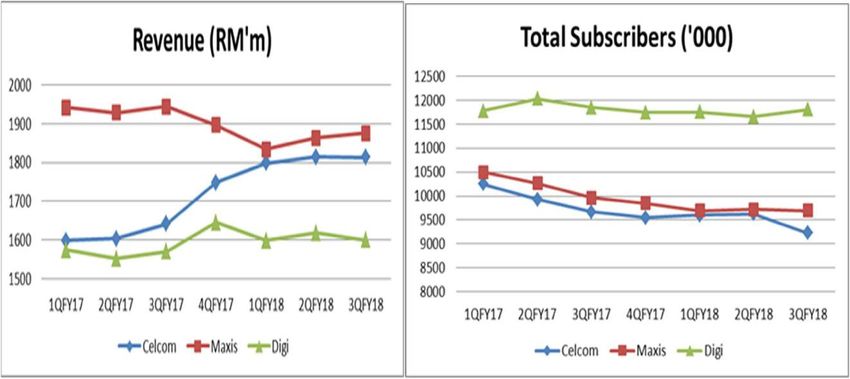

an orderbook of RM820m.Telecommunications (Marketweight)

• Downgrade to Neutral due to lack of catalyst, flat earnings growth

and unattractive dividend yield.

• Challenges: price competition, pressured ARPU and regulatory

risks. Earnings growth expected to be flat due to difficulties in lifting

ARPU amid intense competition. Telcos are maintaining their profit

margins with ongoing cost cutting initiatives and attracting more

postpaid subscribers.

• With the mobile market being matured, opportunities are seen in

fixed broadband and digital services. Our top pick is Axiata with due

to its earnings growth potential and exposure to regional markets.

49Telecommunications (Neutral)

Telecommunications (Neutral)

Telecommunications Axiata (BUY, TP: RM4.95) • We see value emerging after the recent sell down in share price. Catalyst would be earnings recovery in its two biggest subsidiaries Celcom (Malaysia) and XL (Indonesia). Growth will also be driven by earnings momentum as its regional subsidiaries continue to outperform in the respective countries. • Its ongoing cost cutting program aims to reduce costs by RM5b by 2022, translating into 300 basis points of EBITDA margin improvement. Axiata has managed to achieve RM1b of cost savings so far this year. Telekom Malaysia (HOLD, TP: RM2.50) • Share price tumbled over 50% last year on concerns of reduced earnings and dividend after the new government lowered broadband internet prices. • Earnings are expected to drop 20% after the price reduction of broadband packages. Currently, revenue from Internet accounts for over one-third of total revenue. Challenges include price competition, more entrants into the fixed broadband market and regulatory risks. • Slashed dividend payout - TM reduced its dividend policy of RM700m or 90% of normalized PATAMI, whichever higher, to 40%-60% of PATAMI 52

Telecommunications Maxis (HOLD, target price: RM5.51) • Continues maintain a steady growth in its postpaid segment thanks to growth in shared lines propositions, while seeing decline in its prepaid segment impacted by SIM consolidation and migration to postpaid from prepaid. • We do not foresee any significant positive catalyst to drive the share price in the near term. Meantime, lower EBITDA margin is expected from the termination of its network sharing and alliance agreement with U Mobile. The stock’s dividend yield stands at unattractive level of 3.72%. Digi (HOLD, target price: RM4.71) • Digi continues to attract more postpaid subscribers but lower prepaid subscribers. Postpaid revenue fueled by strong take-up and plan upgrades to value postpaid plan with device bundles. • We do not foresee any potential catalyst in near term which will drive the Group’s future earnings. However, better earnings are expected due to its optimized cost agenda. • Digi has an unattractive dividend yield of 3.36%. Healthy cash flow, attractive dividend payout ratio of 100% along with its higher EV/EBITDA as53 compared to its peers.

Oil and Gas (Marketweight)

• Remain Neutral on the sector due to weak oil prices, oversupply

concerns and scarce jobs. Valuations are depressed but recovery is

expected to be slow as award of contracts and capital investments

have not picked up significantly.

• Oil price plunged 40% from US$80/barrel to US$50/barrel in 4Q18.

We expect oil prices to stabilize as OPEC and several producing

countries agreed to cut production by 1.2m barrels a day for 6

months starting January 2019.

• Offshore capital expenditure is expected to pick up later this year

with international oil companies (IOCs) and national oil companies

(NOCs) starting to pour in investments. Petronas’ upstream capex

for 2019 is expected to increase to RM14-15b from RM12b in 2018.

Award of contracts is expected to accelerate slowly from 1H19.

• We prefer companies with large orderbook to sustain earnings in the

immediate term while riding the recovery.

54Bursa Malaysia Energy Index (red) vs Brent Crude

price (yellow)Oil and Gas Sapura Energy (BUY, TP: RM0.50) • Share price hit record low after being dragged by lacklustre earnings, high gearing and impairments. However, we have seen signs of improvement after its recent corporate exercises and kitchen sinking. • To reduce gearing level to 0.7x from 1.7x currently using cash from two recent corporate exercises, namely rights issue to raise RM4b and selling a 50% stake sale in the Exploration & Production (E&P) arm to OMV for RM3.7b. • Huge orderbook OF RM19.4b, its highest in 24 months, after new contract wins of RM9.3b year-to-date. Bid funnel improved significantly as Sapura bids for US$8.8b worth of jobs this year compared to US$2.5b in 2017. • Earnings from Engineering & Construction (E&C) division to improve given the gradual pickup in global capex spending coupled with maiden contribution from the SK408 gas fields coming on stream in end-2019. However, the Drilling division is still loss making with an 56 utilisation rate of 44%.

Bumi Armada (HOLD, TP: RM0.66) • FPSO (floating production storage and offloading) contracts remain as main earnings driver to cushion the low utilisation rate in its offshore support vessels. FPSO earnings are driven by FPSO Kraken (North Sea) and Olombendo (Angola). • Orderbook remains steady at RM21bn with another RM10.3bn worth of potential extension that could sustain Bumi Armada’s earnings for the next few years. • Share price was battered following concerns of high gearing level at 1.8x and impairments. As such, we are lowering our recommendation to Hold until it resolves its debt through refinancing.

Pantech (BUY, TP: RM0.63) • Earnings were significantly impacted after Pantech suspended the export of carbon steel butt welded fittings to the US following a 183% anti-dumping tax imposed on Pantech amid the US-China trade war. • Going forward, earnings will be sustained by ongoing orders from the Refinery and Petrochemical Integrated Development (RAPID) in Pengerang, Johor and its new galvanising plant in Pasir Gudang. • Potential upside could come if the US Department of Commerce’s decision is reversed as the management is using legal means to contest the anti- dumping tax. Should the US upholds its decision, Pantech as a major player in supplying pipes, valves and fittings (PFV), is able to sell its products to other countries albeit at lower margins. • The company pays an attractive dividend yield of 5%.

Thank You

JF APEX SECURITIES BERHAD - DISCLAIMER

Disclaimer: The report is for internal and private circulation only and shall not be reproduced either in part or

otherwise without the prior written consent of JF Apex Securities Berhad. The opinions and information contained

herein are based on available data believed to be reliable. It is not to be construed as an offer, invitation or

solicitation to buy or sell the securities covered by this report.

Opinions, estimates and projections in this report constitute the current judgment of the author. They do not

necessarily reflect the opinion of JF Apex Securities Berhad and are subject to change without notice. JF Apex

Securities Berhad has no obligation to update, modify or amend this report or to otherwise notify a reader thereof in

the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or

subsequently becomes inaccurate.

JF Apex Securities Berhad does not warrant the accuracy of anything stated herein in any manner whatsoever and

no reliance upon such statement by anyone shall give rise to any claim whatsoever against JF Apex Securities

Berhad. JF Apex Securities Berhad may from time to time have an interest in the company mentioned by this report.

This report may not be reproduced, copied or circulated without the prior written approval of JF Apex Securities

Berhad.

59

Equity Market OutlookYou can also read