Kenya Country diagnostic - PRIM E AFRICA - GFRID

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Kenya

Country diagnostic

PRIM

PRIM E AFRICA

E AFRICA

Contents

1. Migration and Remittances 4. Remittances Market Structure

• Remittance flows into and out of Kenya • Market Structure and Value Chains

• Emigration and Migration • Pricing and Transparency

• Informal remittance flows • Access

• Remittance data collection frameworks • Informal channels

• PRIME Africa Corridors

2. Financial Services Landscape

5. Financial Services for Remittance Users

• Payment systems infrastructure and payments interoperability

• Financial services for diaspora

• Know Your Customer requirements

• Case studies of innovation

• Distribution of access points

• SACCOs, Fintechs and payment integrators 6. Stakeholder and Coordination

• Financial Inclusion

• Mobile Money Usage and Growth 7. Policy Actions

3. Regulatory Environment 8. Annex

• Overview

• Licencing 9. Bibliography

• Compliance

• Other association regulations

PRIM E AFRICA

2

Objectives

The Platform for Remittances, Investments and Migrants’ Entrepreneurship (PRIME Africa), is an initiative of the

International Fund for Agricultural Development (IFAD), through its Financing Facility for Remittances (FFR), in

partnership with the European Union. It aims to address the development opportunities that remittances provide

through innovations, partnerships and scalable products that promote more affordable and fast remittances

transfers. Prime Africa’s Objectives are:

1) To reduce remittance transfer costs to Kenya in support of the Sustainable Development Goal (SDG 10.c) and

the Global Compact for Migration

2) Reduce the use of informal channels to Kenya

3) Enhance financial inclusion through remittance-linked financial services.

This Diagnostic provides an assessment of Kenya’s remittance market, especially in light of COVID-19, using a

market-oriented approach. It covers a supply side analysis as well as a review of 3 key inbound corridors.

The findings and recommendations of this diagnostic study will inform the ‘Roadmap’ for a prioritised

approach to interventions leading to the achievement of PRIME Africa goals. It is envisaged that funding will

be made available for the public and private sectors for Roadmap implementation.

Methodology

Data and relevant information for this diagnostic study have been gathered using:

1. Primary Data Collection

• Interviews with key stakeholders: regulators, associations, remittance service providers (money

transfer operators, banks, mobile network operators, aggregators and fintech start ups offering cross

border remittances)

• Mystery shopping exercises for data related to service providers, pricing and products

2. Secondary data

• Desk-based research -Review of relevant, recent and authoritative sources

Data collection was conducted between October 2020 and January 2021.

Two-virtual National Task Force Meetings are scheduled for Q1/Q2 2021.

PRIM E AFRICA

3

Abbreviations

ADLA Authorised Dealer with Limited Authority FSPs Financial Service Providers NHIF National Hospital Insurance Fund

AfDB African Development Bank FX Foreign Exchange Non-DT Saccos Non-deposit-taking SACCOs

AfCFTA African Continental Free Trade Area GCM Global Compact for Migration NPS National Payments System

AFI Alliance for Financial Inclusion GDP Gross Domestic Product NSSF National Social Security Fund

AMFI Association of Micro-Finance Institutions GoK Government of Kenya NTSA National Transport and Safety Authority

AML-CFT Anti-money Laundering / Combating the Financing of G2P Government-to-person ODA Overseas Development Assistance

Terrorism IB/OB Inbound/Outbound PASS Pan African Switch System

API Application Programming Interface IGAD Intergovernmental Authority on Development PEAs Private employment agencies

B2B Business-to-business IMTOs International Money Transfer Operators POS Point of sale

CAK Communications Authority of Kenya IOM International Organization for Migration PSPs Payment Service Providers

CBK Central Bank of Kenya KBA Kenya Bankers Association P2P Peer-to-peer

CDD Customer due diligence KDIC Kenya Deposit Insurance Corporation P2G Person-to-government

CMA Capital Markets Authority KEPSS Kenya Electronic Payment and Settlement System Regtech Regulatory Technology

CRR Cash Reserve Ratio KFRA Kenya Forex and Remittance Association RSPs Remittance Service Providers

CRRF Comprehensive Refugee Response Framework KITS Kenya Interparticipant Transaction Switch REPSS Regional Payment and Settlement System

DFS Digital finance service KMP Kenya Municipal Program ROSCAs Rotational Savings and Credit Associations

DMAG DMA Global KYC Know-Your-Customer RTGS Real Time Gross Settlement

EAC East African Community MFBs Microfinance Banks SACCOs Savings and Credit Cooperatives

EAPS East African Payment System MFIs Micro Finance Institutions SARB South African Reserve Bank

EAMU East African Monetary Union MMPs Mobile Money Providers SASRA SACCO Societies Regulatory Authority

ESAAMLG East and Southern Africa Anti-Money Laundering MoMo Mobile Money SDGs Sustainable Development Goals

Group MNOs Mobile Network Operators SLA Service-level agreement

FDI Foreign Direct Investment MRPs Money Remittance Providers SOE State-owned enterprise

FGD Focus group discussion MSDG Migration and Sustainable Development in Kenya SSA Sub-Saharan Africa

FinTech Financial Technology

MTOs Money Transfer Operators Suptech Supervisory Technology

FIU Financial Intelligence Unit

MVNO Money virtual network operator VSLAs Village Savings and Loan Associations

FRC Financial Reporting Centre

NBFIs Non-Bank Financial Institutions W2B Web to business

PRIM E AFRICA

4

Summary

Migration and Remittances

• Kenya is a net inbound remittance market, receiving USD just over 3 billion in 2020 (with the USA and UK as the main sending markets), compared with outflows at USD

710 million (2018). Remittances account for nearly 3% of GDP and are a leading source of forex in the country.

• The USA, the UK, South Africa, the UAE and Germany are the top send countries (CBK 2020), while according to the FinAccess Survey 2019, Uganda, Tanzania and the

USA are the main receive countries. Germany is the largest send market from the EU, although volumes are small (USD89 million in 2020).

• Remittance inflows into Kenya hit a record high in 2020 despite COVID-19 and both the World Bank and the Central Bank of Kenya (CBK) projecting a fall. Whilst the

underlying reasons behind this increase are still unknown, it is thought to be due to an increase in the use of formal remittance services and people sending additional

funds to support relatives back home.

• Kenya is a net receiver of migrants with a mixed migrant profile. It hosts over 1 million immigrants, 47% of whom are refugees and asylum seekers.

• There are an estimated half a million Kenyans formally living overseas, who are largely skilled and use legitimate channels to migrate mostly to USA, Europe and within

Africa. Increasingly, lower skilled Kenyans also migrate to the Middle East, with estimates suggesting there are as many as 120 thousand Kenyans living there (official

data is unavailable).

• There is also no data available on the prevalence and scale of informal remittance flows from and to Kenya, however, stakeholder interviews suggest that it is

commonplace from many countries, especially those on Kenya’s borders.

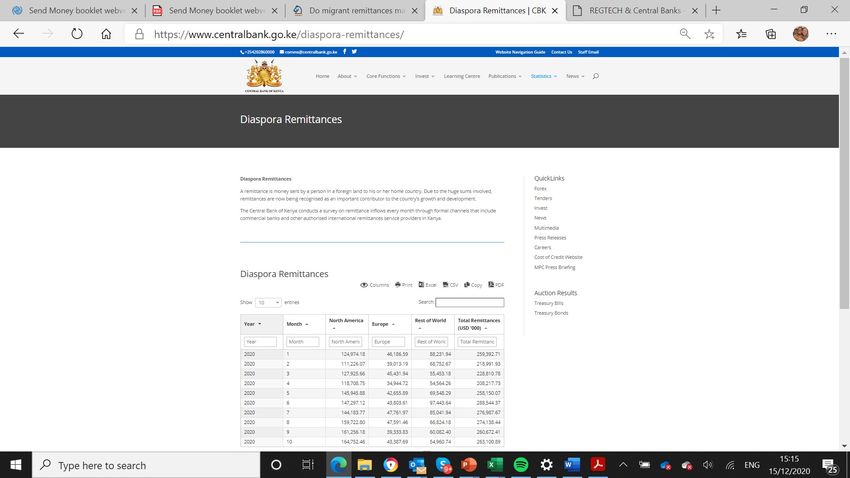

• The CBK currently collects and publishes total remittance inflow data in USD on a monthly basis, broken down into North American and European flows and the Rest of

the World. It also publishes an Annual Report with a summary of the sector performance.

Financial Environment

• Kenya has a well-developed national payments system (NPS) to support remittances, however regional payment systems with potential to reduce costs of intra-regional

remittances are underutilised. The CBK is reviewing its National Payment Strategy 2021-2025 which outlines measures to enhance Kenya’s global lead in digital

payments.

• Kenya has well-established civil registration and national identification systems, where 88% of people have a foundational ID, and is in the process of implementing

integrated biometric identification as a next step.

• The financial services distribution network is extensive and comprises bank and non-bank providers, mostly concentrated in urban areas.

• SACCOs play an important role in providing financial services and are increasingly formalizing their operations. Fintechs have made a strong entry into the market

heightening product diversity and competition.

• Financial inclusion levels are one of the highest in Africa with 8 out of 10 adults formally financially included. This has mainly been achieved through the uptake and use of

mobile money wallets (79% of adults).

• M-PESA is a dominant market player in Kenya's mature mobile money landscape, characterized by activity levels of above 50% and 66% of the customer-base using

advanced digital financial services (such as saving, credit and insurance products).

PRIM E AFRICA

5

Summary

Regulatory Environment

• Money Remittance Regulations for providers wishing to offer inbound and outbound remittances are clear and include mobile money providers. Kenya has no foreign

exchange control regime; however, remittance provider types are limited, and licensing and approvals may take considerable time (although in many cases delays are

caused by the failure of applicants to respond to queries from CBK in a timely manner).

• There are 17 licensed Money Remittance Providers (MRPs) in Kenya. IMTOs do not need to be licensed but operate through commercial banks and licensed MRPs

as agents.

• Kenya developed an AML-CFT framework to comply with and adopt the 40+9 AML recommendations. Following increased incidents of suspected terrorism funding

and a rapidly growing financial services market, 13 MTOs were closed in 2015 until they could demonstrate compliance.

• Risk-based CDD is discretionary and applies to various financial products and to all FSPs, banks, non-banks and PSPs, but there are no tiers or thresholds and there

are no lower-risk or basic accounts.

• Kenya has consumer protection and data privacy laws that cover international remittances; however, services (especially digital) are not always transparent in terms

of pricing and dispute resolution mechanisms are not always clear for digital-based services which undermine trust.

• Kenya has deposit protection insurance in banks, Microfinance Banks and mortgage companies. It also requires operating RSPs to hold some funds in an escrow

account. Kenya also has taxation of mobile money which will increase its costs and has just introduced digital service tax (although financial services are exempt from

this).

Remittance Market Structure

• The structure of the Kenyan remittance landscape varies according to the different migration profiles. It is a highly digitized market driven by high financial inclusion

rates and prevalence of mobile wallets. More than half of all remittances are terminated into M-PESA wallets, and over half of transactions are channeled through

Equity Bank.

• Remittance value-chains to and from Kenya involve a number of players, including the sending party, banks or international remittance aggregators, a licenced entity

in the receive market and pay-out sub-agents. Digital remittance services should be much more streamlined than traditional cash-based products that rely on partners

and pay-out agents.

• In Kenya 41 commercial banks, 14 Microfinance Banks, PostBank, 17 money remittance providers and two MMP have direct license to offer inbound and outbound

money transfers. IMTOs partner with these entities and pay-out via their own networks and sub-agents (mainly forex bureaus and lower-tier banks).

• Whilst market share data for companies is unknown, the type of services and operators used vary by geography, corridors and the profile of migrants. Whilst there is

no official data, interviews suggest SendWave and WorldRemit are the largest senders of remittances into Kenya globally.

PRIM E AFRICA

6

Summary

Remittance Market Structure cont.

• At 7.5% of the send amount, the average cost of sending remittances to Kenya is above the SDG recommended 3%, but lower than the average cost for SSA 8.5% and other intra-

Africa corridors. There are low-cost services from many of the largest send-markets where competition is more intense.

• There is low transparency in Kenya (as in many other countries) on the range of remittance services and the total cost of sending / receiving money. Whilst transparency is

mandated by the Government, full disclosure on total costs to non-customers is often unavailable.

• Digital channels are driving down remittance costs although full impact is yet to be realized as players set up cross border integration partnerships. It is possible to send remittances

mobile-to-mobile wallet to 7 other African countries from Kenya, and it is possible to receive remittances mobile-to-mobile from 6 countries, making it one of the most integrated

globally.

• Access to international remittances in Kenya is among the best on the continent, with a good distribution of MTO agent locations and mobile money agents (where funds have been

received into wallets).

• Anecdotally, the use of informal channels to send and receive money to/from Kenya is high, especially within the East African region. Hawala service providers are also prevalent,

although many of the hawala providers are registered as MTOs in Kenya.

• The main informal channel used within the region is via registered and unauthorised M-PESA agents residing in other countries and offering cross-border money transfer and cash-

in/cash-out services.

• PRIME Africa will focus programme activities in three inbound remittance markets to Kenya, including Germany from the EU and intra-Africa, Uganda and South Africa.

• The average cost of sending money from Uganda to Kenya is 4.1% of the send amount. However, stakeholders suggest that the Uganda to Kenya remittance corridor is still

predominantly informal with transfers made through unauthorised M-PESA agents. These services may even cost more than formal mobile-money transfers, but customers

are willing to pay a premium for the trusted service.

• Kenya's diaspora in South Africa is relatively small with a mix of formal and informal migrants. Stakeholder interviews portray a growing corridor since COVID-19. Notable

usage of informal channel includes Hawala traders and routing money through Botswana to avoid foreign exchange controls.

• The Kenyan diaspora in Germany is the largest in the EU, however, it is still very small with 14 thousand people. Whilst average costs are relatively high at 7.7% of the send

amount, online operators such as WorldRemit and SendWave have much more competitive pricing around 3% of the send amount.

PRIM E AFRICA

7

Summary

Financial Services for Remittance Users

• Kenya has high levels of financial inclusion in terms of account ownership. However, there are opportunities for remittances to further drive usage and increase linkages

between payment channels and financial services. The Kenyan banks offer a wide range of diaspora-related financial services, but Kenyans abroad can also access

domestic products and services.

• The Kenya financial service providers offer a diverse range of diaspora-focussed financial products. There are not many products focussed specifically to remittance

beneficiaries.

• Equity Bank and Kenya Commercial Bank provide two examples of innovation in diaspora financial services. Kenya is a global leader in financial services for the diaspora.

Stakeholder Coordination

• At present, interventions from development partners on remittances are limited in Kenya, apart from descriptive research studies. The CBK plays an active role in

supporting the sector, and the Kenya Forex and Remittance Association (KFRA) advocates for the sector’s interests (for Kenya based operators, but it does not have

many of the key remittance players such as Mpesa or Worldremit, among others).

PRIM E AFRICA

8

Summary Priority Policy Actions

A. Implement a Remittances Data Strategy that enables improved data analytics and generation of market information, including disaggregated remittance inflows,

outflows, channel usage and estimates of informal flows. A review should also include the impact of COVID-19 on the market-place.

B. Expand remittance providers licensing categories to ensure even distribution of access points, improved access and choice.

C. Identify and leverage opportunities for cross-border remittance payment and settlement through regional bloc retail payment systems.

D. Improve transparency in the remittances market and review pricing and cost structures.

E. Address the high use of informal remittance services within the region.

F. Champion an open API culture for ID authentication and verification and between banks and payment service providers (PSPs).

G. Support transition to full payment ecosystem interoperability across channels.

H. Financial education and awareness especially around international remittances, fraud, cyber security and consumer protection.

I. Support industry to lead in innovation for world-leading remittances, payments and remittance linked financial services.

J. Leverage the National Remittances Taskforce Meeting to create a Working Group for the coordination, implementation and review of improving Kenya's remittance

landscape.

(Note that the implementation of a number of these priority actions will be harmonised with that of Kenya National Payments System Vision and Strategy 2021-25

which includes some of the priority areas, such as interoperability and consumer protection.)

PRIM E AFRICA

9

Migration and Remittances

Remittance flows into and out of Kenya

This section provides an overview of the migration patterns and other socio-

economic activities that drive inbound and outbound remittances in Kenya as

Emigration and Migration well as a sender/receiver profile. It also examines informal flows, accuracy,

consistency and accessibility of remittance data.

Informal remittance flows

Important Note on Data:

Remittance data collection frameworks There are a number of different data sources that are used in this next section. Data is not

always consistent across the different sources. Data, where available, has been used by the

Kenyan Government, but is supplemented by international databases where data it is not.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

10Kenya is a net inbound remittance market, receiving USD 3 billion in 2020, with the USA and UK as the main

sending markets, compared with outflows at USD 710 million (2018). Remittances account for nearly 3% of GDP

and are a leading source of forex in the country.

Inbound Remittances (millions of US$)

• Kenya is one of the five highest remittance-recipient countries in Africa, receiving USD 2,787 million in North America Europe Rest of World Total

2019 (CBK, 2019)[1] after Egypt (USD 26,781 million); Nigeria (USD 23,809 million); Morocco (USD 6,735 million)

3.094

and Ghana (USD 3,521 million) (World Bank Annual Inflows 2019a).[2]

2.787

2.687

• Remittances to Kenya remained resilient against the backdrop of COVID-19 and recorded record highs in

1.947

2020. Remittance inflows stood at USD 299.6 million for the month of December 2020, compared to USD 250.3

1.744

million for December 2019, constituting a 19.7% increase. At the end of 2020, cumulative remittance inflows

1.343

1.339

stood at USD 3.094 million, a 10.7% increase from USD 2.787 million in 2019.[1]

1.004

863

813

791

663

629

537

446

• Remittances are an important economic driver in Kenya's economy, contributing 3% to its GDP in 2018

314

(World Bank, 2019b)[3] and recording higher levels than foreign direct investment (FDI)[4] and portfolio equity flows.

Cash inflow from citizens working abroad is now Kenya’s leading source of forex, ahead of tourism and agricultural

exports.[5] Remittances are included in Kenya’s Vision 2030, the National Migration Policy, the Kenyan Diaspora 2017 2018 2019 2020

Source: CBK, 2017-2020 [1]

Policy and the Draft Kenya National Payments System Vision and Strategy, 2021-2025 with commitments to grow

remittances and reduce the cost. Total remittance inflows and outflows for Kenya (in

millions of US$)

• According to the CBK (2021),[7] top inflows in 2020 were from: USA (USD 1.67bn, 54%); UK (USD 230mn, Total outflows Total inflows

7%); South Africa USD 195mn (6%), Germany USD89mn (3%) the UAE USD73mn (2%) (author’s own

2.719

calculations based on data from the CBK).

1.970

1.739

1.561

• The World Bank estimates that remittance outflows from Kenya were USD 710 million in 2018 ((World Bank,

Bilateral Matrix, 2018). The CBK does not publish outbound remittances or inflow data by corridor. According

to the Matrix, which is based on estimates where data is unavailable, the top 5 outbound remittances destinations

710

for 2018 were: Uganda (USD423m, 59.5%), India (USD84m, 11.8%); Tanzania (USD35m, 4.9%), Egypt (USD18m,

357

319

319

2.5%); and Nigeria (USD13m, 1.8%). According to the FinAccess Survey 2019,[8] the largest outbound corridors

are Uganda (24%), Tanzania (12%) and the USA (10%).

2015 2016 2017 2018

Source: World Bank Bilateral Remittance Matrix, 2015-2018 [6]

PRIM E AFRICA

11The USA, the UK, South Africa, the UAE and Germany are the top send countries (CBK 2020), while

according to the FinAccess Survey 2019, Uganda, Tanzania and the USA are the main receive

countries. Germany is the largest send market from the EU, although volumes are small (USD89 million in

2020).

Source: FinAccess Survey 2019 [9a]

• The FinAccess Survey 2019 is a survey of 11,000 households across Kenya. As

Source: CBK, 2021 [9b] outbound remittance data is not available by corridor from the CBK, the FinAccess

Survey results provides insight. It is not clear from the survey the number of

• This data has not been officially published by the CBK. The data captures households that received or sent money.

formal remittance flows by corridor. The data shows that remittance inflows • The FinAccess Survey captures remittances sent both through informal

from the USA increased in 2020, accounting for nearly 60% of flows in Q4 channels as well as through formal. This may help explain some of the

2020. Remittances from the UK account for 7%. Inflows from South Africa discrepancies between the formal data from the CBK for inbound 2021 (graph on

dropped significantly in Q4 2020. the left) and the FinAccess survey results, especially regarding inflows from

Uganda.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

12Remittance inflows into Kenya hit a record high in 2020 despite COVID-19 and both the World Bank and the CBK

projecting a fall. Whilst the underlying reasons behind this increase are still unknown, it is thought to be due to

an increase in the use of formal remittance services and people sending additional funds to support relatives

back home.

• In response to the COVID-19 pandemic, Kenya had a temporary decline in remittance inflows then recovered

and experience growth; remittance inflows stood at USD 299.6 million for the month of December 2020,

compared to USD 250.3 million for December 2019, constituting a 19.7% increase (CBK, 2021).[10]

Total global remittance inflows into Kenya for

• The CBK had projected a decline of 12.3% (USD 338m) but later revised projections after seeing an 2020

increase of 1% (USD 24.7m) in June 2020. The World Bank also projected a 23.1% fall for Sub-Saharan N.B. COVID-19 pandemic started in March 2020

African countries in April 2020[12] but revised this to a 9% decrease in October 2020[13] . Looking forward, the (in USD million)

World Bank predicts a decline in 2021[13] as the full impact of diaspora job losses and declining business 350

288,5 277,0 299,6

performance is fully realized. 300 274,1 260,7 263,1

259,4 258,2 257,7

250 219,0 229,0 208,2

• The increase in remittance inflows could be related to either the diaspora deepening their support against

200

economic hardships at home, or as a result of travel restrictions prompting a significant shift from informal to

150

formal channels for sending money home. At present this analysis is hypothetical and not supported by data. At

the height of the lockdown in Kenya, financial service providers, including remittance providers, remained open 100

which would have supported the use of formal channels. 50

0

• In response to COVID, the CBK put in place measures to support the economy and the use of digital

t

y

ay

e

n

b

ct

g

c

ch

r

ov

p

Ap

l

De

Au

n

Fe

Ja

Ju

O

ar

Se

M

N

Ju

payments (see Annex 1). Between February and October 2020, the volume of mobile money transactions up to

M

Ksh. 1000 increased by 114% with 200% increase in value, this tier accounts for over 80% of transactions. In the

Source: CBK (2020, 2021)[10][11]

same time period, the monthly volume of payment service provider (PSP) transfers increased by 87% and

business-related transactions increased by 82% and there were 2.8 million additional 30-day active customers

using MoMo.[14] CBK measures were implemented from March 16th 2020 and gradually ended by

31st December 2020,[14] mPesa then issued a 45% price reduction targeting low value transactions under Kshs

1.000 (USD 10).[15]

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

13Kenya is a net receiver of migrants with a mixed migrant profile. It hosts over 1 million immigrants, 47% of whom

are refugees and asylum seekers.

Kenyan Migrant Stocks 1990-2019

1.200.000

• Kenya is mainly a destination and transit country for people in mixed migration flows from East 1.000.000

Africa, including refugees; irregular and economic migrants; and trafficked persons. Migrants, 800.000

mainly from African countries, transit through Kenya to reach South Africa; the Middle East; North Africa; 600.000

West Africa; Europe; and North America (ILO, 2020).[16]

400.000

200.000

• In 2019, there were just over 1 million international immigrants in Kenya (1,044,854) and as of July

2020, 496,289, (47%) of these migrants were refugees and asylum seekers (latest data available) 0

(UNDESA, 2019; UNHCR, 2020a).[17][18] 1990 1995 2000 2005 2010 2015 2019

Emigrant Immigrant Source: UNDESA (2019)[17]

• Kenya is host to the third largest number of refugees and asylum seekers in the region, following

Uganda (1,444,873) and Ethiopia (916,678) (RMMS, 2018).[19] The majority of refugees are from Somalia Immigrants into Kenya and Refugee & Asylum Seeker

(53.9 per cent), while South Sudanese (24.7 per cent); Congolese (9 per cent); and Ethiopians (5.8 per Numbers

cent) make up the other major nationalities (UNHCR, 2020b).[20] This is attributed to: its geographical

location amidst neighboring countries which have suffered repeated civil strife and wars; having a relatively

reliable transportation network; and stable economy (IOM, 2018: 48).[21]

• Labor migrants from Asian countries, such as Bangladesh, India, and Pakistan, are also found in

Kenya; they mostly come to set up businesses (MGSOG, 2017: 6)[22], although actual numbers of this

category of migrants are yet to be published.

Source: UNHCR (2020a)[18]

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

14There are an estimated half a million Kenyans formally living overseas, who are largely skilled and use

legitimate channels to migrate mostly to USA, Europe and within Africa. Increasingly, lower skilled Kenyans

also migrate to the Middle East, with estimates suggesting there are as many as 120 thousand Kenyans

living there (official data is unavailable).

• Kenyan emigrants stand out for being skilled and educated and leave for employment or education abroad

through regular means. Total number of emigrants are estimated to be 525,400; top destinations are: United

Migrant Stock by Destination

Kingdom, United States of America, Uganda, Canada and South Africa (UNDESA, 2019a).[24a] Other U.K

Countries 149,797

145,942 (29%)

• The number of Kenyans formally living in other African countries are higher than those residing in EU

(28%)

countries, with 137,969 Kenyans residing in Africa versus 38,229 in the EU. The top host countries

include neighbours Uganda, Tanzania and others such as South Africa and Mozambique (UNDESA, 2019b).[24b]

Stakeholder interviews suggest there are significantly more Kenyans in South Africa who did not use legitimate

migration channels.

• According to the UNDESA (2019b), Germany has the largest Kenyan diaspora in the EU with 3% of the total South Africa

diaspora, approximately 14,000 Kenyans residing there. Across the EU, Kenyan diaspora sizes are small, 28,769

below 5000 in each country. The next largest Kenyan diasporas in the EU are in Sweden and Italy with an (5%)

estimated 5,000 and 4,000 people, respectively.

• Increasingly, low-skilled Kenyan migrant workers migrate to the Middle East and the Gulf countries for Canada Uganda USA

work, as job opportunities are generally more than in other regions. This emigration type is facilitated 28,920 36,822 135,187

by private employment agencies (PEAs). Kenya has a tightening of immigration processes to the Middle (5%) (7%) (26%)

East. Except for Egypt, Libya, Sudan and Turkey, data on the number of Kenyans in Middle East and North Africa Source: UNDESA (2019b)[24b]

(MENA) countries is limited (Stakeholder Interviews, 2020). It is estimated that there are between 100 to 120

Please Note: Migrant Stock Bilateral Data from

thousand Kenyans residing in the Middle East.[25a] [25b]

the World Band and UNDESA does not include

data from the GCC. It is estimated there are up to

120 thousand Kenyans in the Middle East.[25a] [25b]

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

15There is no data available on the prevalence and scale of informal remittance flows from and to Kenya, however,

stakeholder interviews suggest that it is commonplace from border countries.

• The CBK does not currently have any data on informal remittance values. Accurate estimations of informal remittances are uncommon.

Informal remittance channels include sending money with friends and family; hawala; traders; bus drivers; informal agents; and

unauthorised/unlicenced operators. By its very nature, data on informal remittances is difficult to collect. Surveys are the only method through

which it is possible to form an understanding of the prevalence of using informal across different corridors.

• The CBK has announced, Jan 2021, that it will be commissioning a survey on diaspora remittances as it seeks to increase the

inflows' support in development and economic growth. The information will include; the efficiency and cost of alternative remittance

channels, difficulties encountered in remitting cash/non-cash transfers, availability of information on investment opportunities for Kenyans in

the diaspora and usage of remittances received. Both the Bank of Uganda and Central Bank of Nigeria are collecting data on informal

remittances, it is recommended to coordinate so that it is possible to compare across countries and corridors.

• It is assumed, and reaffirmed through stakeholder interviews, that the prevalence of informal channels is higher to and from

countries where there are shared borders. For example, there is reported to be high usage of M-PESA person to person (P2P) transfers

from Uganda to Kenya, Safaricom's deactivation of roaming facility from Agent handsets did little to deter the practice. Similarly, there

are some MTN agents in Kenya border towns offering services to Uganda, although not as prevalent as M-PESA (Stakeholder Interviews,

2020).

• In FGDs in 2018 conducted in the UK, by FSD Africa, with participants from the Kenyan diaspora, all used formal channels to send

money home. In the 7 African countries that were involved in the study, the Kenyan diaspora was found to be the most digitised- using online

and app base services mostly terminating to Mobile Money and lowest use of informal Services (FSD Africa, 2018).[26]

• Remittance flows have increased since COVID-19, the trends are under continuous analysis hence the extent of this behaviour

change this is yet to be quantified. Some stakeholders were of the view that increases were due to informal flows going through formal

channels following border and service closures; for example between South Africa to Kenya (Stakeholder Interviews, 2020).

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

16The CBK currently collects and publishes total remittance inflow data in USD on a monthly basis broken down

by North American and European flows and the Rest of the World. It also publishes an Annual Report with a

summary of the sector performance.

• The Central Bank of Kenya collects inbound remittance data from reports submitted by all

permitted/licensed providers: commercial banks, Money Transfer Operators (MTOs) and Mobile

Money Providers (MMPs). This data is only collected in blocs from the send destinations e.g. North

America, Europe and the rest of the world by value and volume. This data is published monthly by the CBK

and is up to date, latest data available being December 2020 (CBK, 2020a).[28] Monthly remittance data is

useful for tracking remittance inflows patterns and identifying seasonal trends.

• The CBK also publishes an annual report with a summary of sector performance which includes a

summary of remittance inflows (Stakeholder Interview, 2020).

• According to one stakeholder, the CBK collects a lot of data for AML-CFT and reporting purposes,

however it has been suggested that at present the different databases are not comparable, integrated

nor interoperable. Apparently, this is something that the CBK is currently working on improving which will

ultimately improve supervision and oversight. This is an area that has been worked on for some time and the

challenge of being able to manage data across multiple government departments is a significant one.

• The CBK is currently undertaking an online diaspora remittance survey to provide greater insight (April

2021).

• The CBK is currently working on improving their data collection templates and systems from the

RSPs and are aiming to be able to provide more level of detail with more analytics by next year. Currently

data is only published by region. Also, currently banks do not have to report their inter-bank cross-border

account to account to the CBK which means they are not reflected in the remittances data.

• The Kenya National Bureau of Statistics (KNBS) compiles and disseminates the Balance of Payments

statistics. KBNS has also done work on trying to understand remittances:

1. Including emigrants in the 2019 Kenya Population and housing Census 2019

2. including remittances in the Keya Continuous Household Survey Programme

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

17Migration and Remittances

Priority Policy Actions

• Implement a data strategy that among other functions, enables improved data analytics and generation of market information including disaggregated

remittance inflows, outflows, channel usage and estimates of informal flows. Planned amendments to reporting templates could be informed by CBK data needs

as well as market needs with the following considerations:

o Harmonized templates and reporting across the EAC for consistency to ease eventual harmonization of regulations under the East African Monetary Union

(EAMU).

o More detailed outflow to the same level of detail as inflow data (above)

o Information portals publicly available for easy access to disaggregated inflow and outflow remittance data to inform business decisions.

o Access to market share information of remittance service providers to enhance transparency in the market.

• Industry collaboration on CBK's planned diaspora remittances survey launch in Feb/Mar 2021. Recommended collaborators could include: Institute of Africa

Remittances, Financial Sector Deepening Kenya (FSD Kenya) and the Financing Facility for Remittances (FFR) at IFAD to maximise opportunities and ensure

consistency across countries. This would present an opportunity for Kenya to share remittance best practice with other countries.

• Inclusion of remittance modules in household surveys to understand and form national estimates on the size of the informal market. For example, expanding

on the remittance questions in the FinAccess Surveys and coordinate with the Kenya National Bureau of Statistics. Such data would also serve to guide policy

decisions and action plans to formalize informal remittances and support efforts to curb illicit flows.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Recommendations

Remittances Environment Environment Remittance Users Coordination

PRIM E AFRICA

18Financial Environment in Kenya

Payment systems infrastructure and

payments interoperability

Know Your Customer requirements This section looks at:

• The payment system infrastructure in Kenya that supports the remittances

Distribution of access points market

• Identification and addressing systems that are required to access

SACCOs, Fintechs and payment integrators remittances and other financial products

• Financial inclusion in Kenya and the use of digital payment instruments

Financial inclusion

Mobile Money Usage and Growth

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

19Kenya has a well-developed national payments system (NPS) to support remittances, however regional payment

systems with potential to reduce costs of intra-regional remittances are underutilised. The CBK is reviewing its

National Payment Strategy 2021-2025 which outlines measures to enhance Kenya’s global lead in digital

payments.

• Kenya has a well-developed national payments infrastructure that enables remittance companies and banks to be able to settle remittance transactions easily and

direct money into bank accounts and mobile wallets. Kenya has a Real Time Gross Settlement system (RTGS), the Kenya Electronic Payment and Settlement System

(KEPSS) and an Automated Clearing House (ACH), the Nairobi Automated Clearing House (NACH).

• Interoperability between payment channels allows RSPs and remittance recipients to be able to easily move money between different payment channels. Kenya has

some-level of interoperability between different payment channels, with Kenswitch, PesaLink (IPSL) and bilateral agreements all enabling the service.

• Mobile-wallets have been interoperable since 2018 through a multilateral approach, rather than a third-party aggregator, offering real time transactions at the same

cost as inter-network payments. Kenya does not have a central switch that provides full interoperability between bank accounts, cards and mobile wallets where each has

interoperability between themselves. See more information on Kenya’s payment system and interoperability in Annex 2. Despite these levels of interoperability (mostly

account to account), the Kenyan market remains fragmented at authentication and distribution levels. For example, Mobile Money, Agency Banking and Merchant

services are close looped and agents serve customers from multiple FSPs, through different terminals and pre-funded accounts. The implication for remittances is that customers

can only use specified cash out providers thus limiting their choice and Agents end up preferentially partnering with dominant providers as the cost of serving smaller players is

higher.

• The CBK is currently reviewing its National Payment Strategy 2021-2025 which outlines measures to enhance Kenya's global lead in digital payments. Facilitating

industry-led interoperability emerges as a priority area as do trust, security and innovation.

• The Central Bank has two regional payment and settlement systems to process large value payments: The East Africa Payment System (EAPS) and Regional

Payment and Settlement System (REPSS). Whilst these initiatives have the potential to drive down costs of inter-regional remittances (EAPS) and settlement between regional

RSPs, usage is low due to low Intra Africa trade traffic, more competitive bank led legacy systems and low awareness. The PanAfrican Payments and Settlement System

(PAPSS), developed by the African Export-Import Bank (Afreximbank), and currently under development, is designated to support implementation of the African Continental Free

Trade Area (AfCFTA) by enabling cross border trade payments to be made and settled in African currencies (Afreximbank, 2020).[29]

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

20Kenya has well-established civil registration and national identification systems, where 88% of people have a

foundational ID, and is in the process of implementing integrated biometric identification as a next step.

• Kenya has a well-established national ID system, administered by the National Registration Bureau, a component of the Ministry of Interior and

Coordination of National Government, State Department for Immigration, Border Patrol and Registration of Persons. About 88% of Kenyans have this

foundational credential which is useful for identification, access to public and private services. It is mandatory for citizens aged 18 years and

above. The civil registration system issues birth certificates which must be produced when enrolling in schools and applying for an ID or passport.

• ID can be checked through the Integrated Population Registration System (IPRS) national database which is real-time. All licensed financial

service providers can access the IPRS upon application and approval by the Ministry of Interior Government through API. The automated fingerprint

identification system checks against duplications and multiple entries (Open Society Justice Initiative, 2019).[35]

• Introduced in January 2019, Huduma Namba is an advanced nationwide biometrics registration that is integrated across several public

services through an e-government portal. The register is meant to link with other existing government databases, such as the National Social

Security Fund (NSSF), National Hospital Insurance Fund (NHIF) and the National Transport and Safety Authority (NTSA). The Government of Kenya

conducted a round of Huduma Namba registration from April to May 2019 and indicates 36m people were registered. More recently, the Government

communicated that issuing of cards for those registered will commence in January 2021 and the current national Identification card will be

phased out at the end of 2021.

• Challenges: There are concerns that Huduma Namba identification contravenes certain provisions of the law including exclusion of currently

unregistered citizens, stateless persons and those unable to provide biometrics which may result in subsequent denial of government services (Citizen

Digital, 2020).[36]

• Under the Common Market Protocol, citizens of the EAC can travel within Kenya, Rwanda, South Sudan and Uganda using national identity cards in

addition to regional and international passports. Issuance of the East African Passport commenced in 2017 and is expected to develop integrated e-

immigration management systems and services (East African Community, 2017).[37]

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

21The financial services distribution network is extensive and comprises bank and non-bank provider which

are mostly concentrated in urban areas.

• Commercial Banks – According to some analysts, Kenya is overbanked. There are 41

commercial banks. The total branch network is 1,401 branches; of the 41 banks, 19 have

Financial Service Access Points 59,578 agents under the agency banking model (CBK, 2020d).[38] The competitive market

environment and recent restrictions on movement due to COVID-19 pandemic has seen banks

investing heavily in digital banking services and encouraging the use of Agents for low value

transactions. Bank Agents double up as Agents for Insurance companies and offer cash-in/cash-

out services, account opening. Agents can pay out remittances, but only in KSH.

• Microfinance Banks compete with commercial banks. They offer a vital service channel to the

significant proportion of the population lacking access to commercial banks (AMFIK, 2017).[39]. For

They can pay out as agents of remittances-licenced entities but are not particularly widely used.

• Mobile Money Providers – There are three Mobile Money providers: Safaricom M-PESA, Airtel

Kenya and Telkom Kenya. M-PESA is the market leader of the 3 Mobile Money providers with

98.8% market share; Airtel Kenya’s Airtel Money 1.1% and Telkom Kenya’s T-Kash 0.05% market

share all three have a total of 246,1374 Agents (CA, 2020).[40] Equity Bank offers Equitel, a Mobile

Virtual Network Operator with a customer base of 1.88 million (Equitel, 2020).[41]

• Microfinance Banks (MFBs) – Three wholesale MFIs focus on lending to MFIs: Micro Enterprises

Support Program Trust (MESPT), Soluti Finance East Africa and Oiko Credit. Of the 34 credit-only

institutions registered with Association of Micro-Finance Institutions (AMFI) (not all MFIs are

registered with AMFI) with a total of 486 fully fledged branches: 230 are in rural areas and 156 in

urban areas (AMFIK, 2017).[39] It is estimated that MFIs serve about seven million depositors and

close to 1.5 million borrowers (ORCA, 2015).[42]

• Kenya Post Office Savings Bank (KPOSB), also known as Postbank Kenya is a special type of

bank regulated by the Kenya Post Office Savings Bank Act Cap 493.B and primarily engaged in

the mobilization of savings for national development and does not offer the full suite of banking

services but is permitted to offer cross border remittances which it does in partnership with main

IMTOs, BDCs, banks and MFIs. It is present in rural areas and makes government disbursements

and partners with utilities and others.

Migration and Financial Regulatory Financial Services for Stakeholders and

- Mix Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

22SACCOs play an important role in providing financial services and are increasingly formalising their

operations. Fintechs have made a strong entry into the market heightening product diversity and competition.

SACCOs began as informal savings associations but have formalised their operations in the last

decade to include Front Office Service Activities (FOSA), Back Office SACCO activities (BOSA), Digital

solution offerings, Agency Banking and card services. The 188 Deposit taking SACCOs are regulated

by SASRA while 6,000 non-deposit taking SACCOS are supervised by the Commissioner for Co-

operatives.

Through their branches, they offer financial service products and are key in expanding reach to rural

areas. Following increasing incidents of fraud, SASRA plans to license non-deposit taking SACCOs

with deposits of over $2 million (SASRA, 2020).[43]

Fintechs: The Fintech landscape has experienced remarkable growth attributed to the mature

payments ecosystem and conducive regulatory environment. There are and estimated 150 fintech

start-ups, including mobile payments companies (examples M-changa, Wayawaya, LipaPlus) and

lending platforms (examples Tala, Branch, Farmdrive, Okash) as well as Tanda which transforms

shops into banking and Mobile Money agents (Nzekwe, 2020)[44] (Tanda, 2021)[45].

See p.38 for Kenyan based Fintechs offering cross border remittance services.

Payment Integrators: The expanding payments ecosystem has led to the emergence

of integrators who serve various providers especially merchants to enable them accept various

payment instruments. IPSL (PesaLink), Jambopay, Cellulant, DPO and iPay are examples.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

23Financial inclusion levels are one of the highest in Africa with 8 out of 10 adults formally financially included. This

has mainly been achieved through the uptake and use of mobile money wallets (79% of adults).

• Kenya has one of the highest financial inclusion rates in Africa after Mauritius and Financial inclusion by country

South Africa with 83% of people formally financially included (FinAccess, 2019)[46] ;

6.1% informal; and 11% excluded). This is largely driven by the high adoption of mobile

money.

• 77% of the rural population are financially included compared to 91 percent in urban areas.

• The gender gap in financial services usage declined marginally from 8% to 7%

between 2016 and 2019 and 5% (91% men and 86% women) for mobile usage,

encouragingly this is way below sub-Saharan Africa’s average of 13%. This is largely

attributed to affordability, low literacy skills and where families do not approve of usage

(GSMA, 2020).[47]

• Inclusive solutions targeting previously excluded segments such as youth, women,

elderly, persons living with disability, low-income earners, MSMEs and Islamic

Finance are increasing and bridging gaps. Examples include: youth

savings products; alternative credit scoring based lending to reduce reliance on collateral-

based lending; low-value basic accounts, dedicated call centre line serving persons with

disabilities and Sharia'h compliant microfinance (CFI, 2018).[48] Financial services usage by FSP type

• Financial literacy efforts are paying off, the dynamic nature of

advancements in technology, necessitates sustained efforts. CBK, Payment providers

and Development partners have typically championed such efforts.. Awareness levels are

increasing even amongst bottom of the pyramid and illiterate customers (OECD/INFE,

2020).[49]

• Usage of informal services especially amongst rural dwellers and older

persons persists. These include savings groups, and Rotational Savings and

Credit Associations (ROSCAs) and Money Lenders (FinAccess, 2019).[46]

Source: FinAccess, 2019

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

24M-PESA is a dominant market player in Kenya's mature mobile money landscape characterized by activity levels

of above 50% and 66% of the customer-base using advanced digital financial services.

• Kenya's mobile money ecosystem is mature with intense competition and collaboration

between service providers: mobile money, commercial banks, MFBs and Fintechs.

Agents 195,854 24,805 2,525 -

• Mobile money is the key driver of narrowing the financial services access Active Customers 30,193,833 310,359 13,999 1, 660,000*

and usage gap, a conducive regulatory landscape has also been a key enabler. The Market share 98% 1% 0.04% -

Communications Authority (CA) reported 30.5 million mobile money accounts in Kenya,

P2P/Send Money √ √ √ √

served by over 200k agents (CA, 2020).[50]

Cash in/cash out √ √ √ √

1st Generation

• M-PESA is a dominant market player with 98 percent market share. Equity Bank Bill Payment √ √ √ √

Products

offers Equitel, a Mobile Virtual Network Operator. Other MNOs offering mobile money in Airtime Purchase √ √ √ √

Kenya include Airtel and Telkom’s T-Kash. Mobile Money providers enable remittance

Bulk Payments √ √ √ X

inflows and outflows.

Cross Border

√ √ X √

Remittances

• Growth in the use of mobile money has been significant with activity rates amongst

all subscribers increasing from 51 percent to 71 percent between 2016-2019.

Merchant payments √ √ √ √

Digital Lending √ √ √ √

• According to FinAccess (2019),[51] 66% of customers are advanced DFS users Digital Savings √ √ X X

mainly determined by uptake of second-generation products such as mobile

2nd Generation Microinsurance √ √ X √

investments, crowdfunding, and overdraft solutions. However, remittance use cases are

Products Crowd Funding √ √ X X

limited, for example users including diaspora customers can only transfer to or receive via

Mobile Money. Investments √ √ X X

Bank2Wallet/Wallet2

√ √ √ √

• Diasporans with an M-PESA wallet using roaming services can access all self- Bank

service services (those not requiring an agent or merchant). Roaming is not available in Card Solution √ X X √

all countries, for example, Safaricom has no roaming partner in some markets such

Overdraft √ X X √

as Lesotho.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Recommendations

Remittances Environment Environment Coordination

*Equitel customer base considered bank

PRIM E AFRICA clients and not counted in MNO market share.

25Financial Environment

Priority Policy Actions

• Support transition to full payment ecosystem interoperability across channels: The current situation requires pre-funding of accounts for liquidity management. A

national switch would enhance efficiency of settlement mechanisms. This, in turn, would enable operators to free up funds otherwise tied up in pre-funded accounts. A real time

cross border interoperable platform integrating national and regional retail payment systems would then be more achievable from this vantage point and

could ease the flow and settlement of cross border payments, ultimately reducing costs for both users and service providers.

• Agent interoperability would benefit agents by enabling consolidation of different service provider floats into a single account, In future this could possibly be

extended to bank agents under Pesalink model .

• Merchant interoperability – a universal Quick Response (QR) code would ensure interoperability but more importantly eliminate the need for Point of Sale devices as

both merchants and customers can access it through app based smart phone or feature phones. This would be a significant move towards a fully open, efficient and

affordable payments ecosystem driving down costs especially for the poor and informal businesses (FSD Kenya, 2018).[52]

• Identify and leverage opportunities for cross border remittance payment and settlement through regional bloc retail payment systems. The Pan Africa Payment and

Settlement system (PASPP) looks promising as it has a Digital Payment module whose usage can extend to remittances (Afreximbank, 2020).[53]

• Open APIs for authentication and verification of e-KYC as currently KYC must be repeated for each service onboarding. This would also expand the number of providers

who can safely access this register for e-KYC authentication (CBK, 2020b).[54]

• Advocate for service providers to sustainably make permanent some COVID measures such as reduced fees, expansion of transaction and balance limits.

Migration and Financial Regulatory Financial Services for Stakeholders and

Market Structure Remittance Users Coordination Recommendations

Remittances Environment Environment

PRIM E AFRICA

26You can also read