ISTAT Learning Lab ESG & Sustainable Financing - International Society of Transport Aircraft Trading

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ISTAT Learning Lab

ESG & Sustainable Financing

13 April 2021

Jonathan Drew,

Managing Director, ESG Solutions, Global Banking, HSBC

PUBLIC

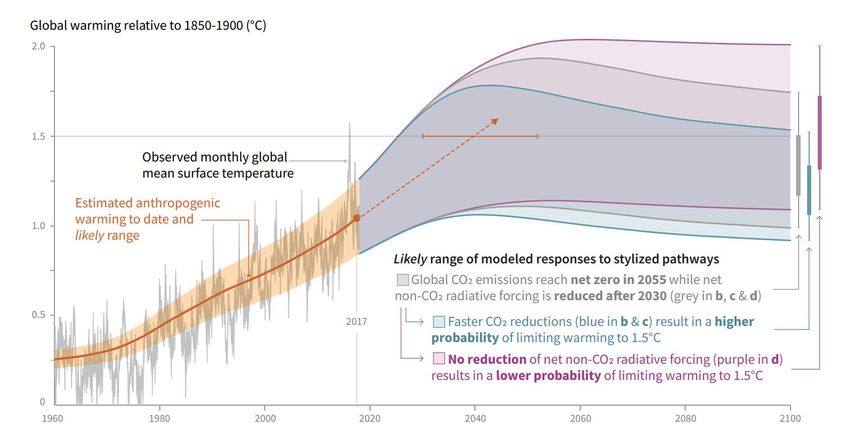

Anthropogenic impact on climate ? Probability of limiting warming to 1.5ºC

Observed global temperature change and modelled responses to stylized anthropogenic emission and forcing

pathways

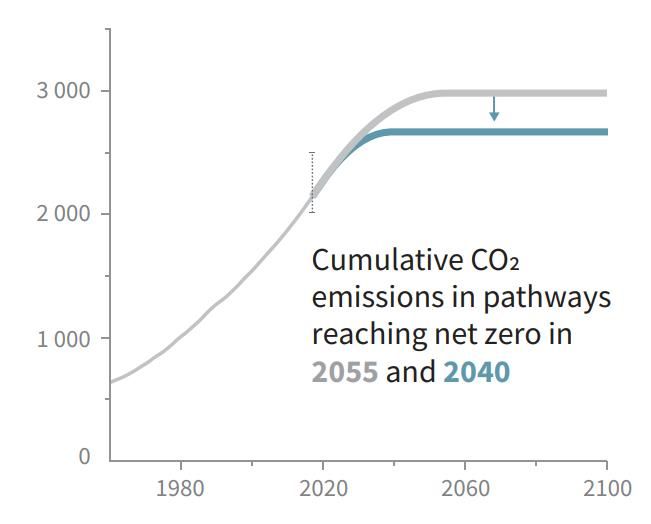

Cumulative net CO2 emissions

Billion tonnes CO2 (GtCO2)

Stylized net global CO2 emission pathways

Billion tonnes CO2 per year (GtCO2/yr)

Source: Intergovernmental Panel on Climate Change Special Report on Global Warming of 1.5°C

PUBLIC 2

Net Zero Targets

Over 100 countries have set decarbonisation goals contributing to 50% of global emissions

Target under discussion

In policy document

Achieved

Proposed legislation

In law

Source: Climate Action Tracker, Bloomberg Green

PUBLIC 3

Achieving Net Zero requires transformation of the global economy

The global challenge $100trn investment required to 2030 globally across sectors2

% of global GtCO2 emissions, top 51

Middle East

Other emgerging Asia

China Europe

26% 5%

India 6% 16% US and Canada

US 13% 6% Latin America

Africa

EU 8%

$100trn

22%

India 7%

29% Asia and emerging markets will lead this

China

Russia 5% transformation, requiring >50% of

7% required infrastructure investment

7% 2%

Developed Asia

Electricity & Heat 30%

Transport 16%

16%

Agriculture 12% Transport

Water and sanitation

Land Use and Forestry 7% 9% 39%

Telecoms

$100trn

Industrial Processes 6% Power transmission and distribution

Primary energy supply chain

14%

Energy efficiency

9% 13%

Notes:

1. World Resources Institute WRI

2. OECD and IEA

PUBLIC 4

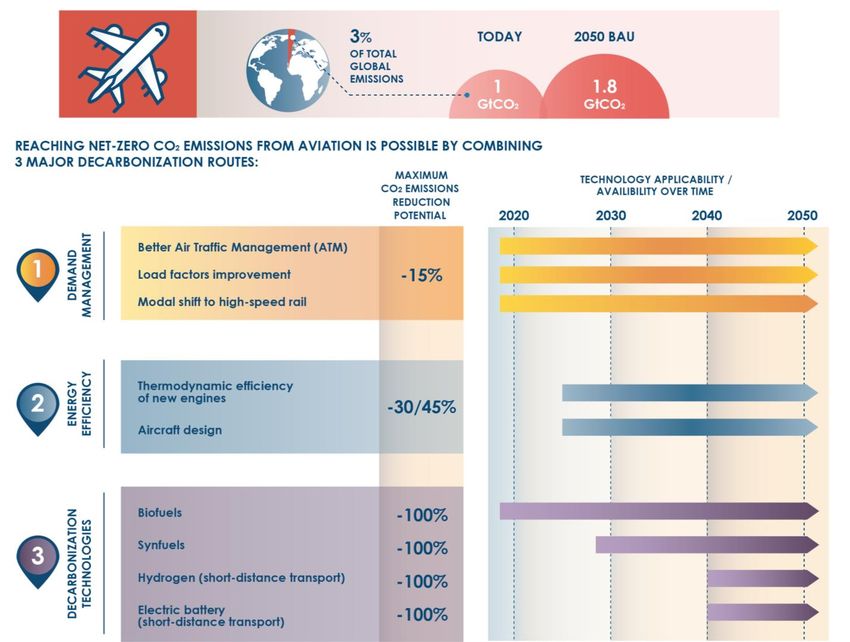

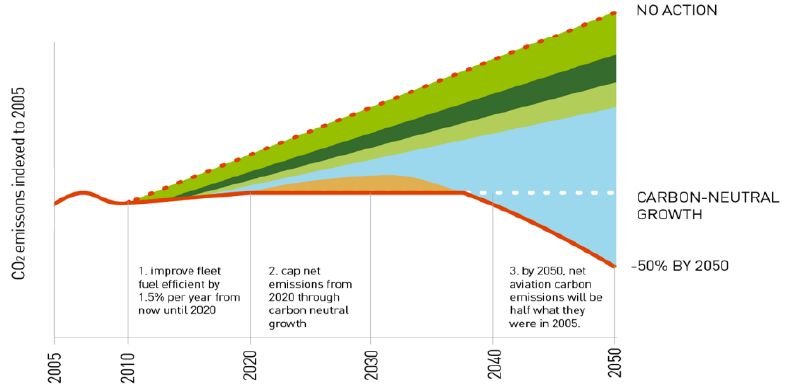

Progress in the Aviation Sector

In 2009, the aviation industry, through the International Air Transport Association (IATA) and the Air Transport

Action Group (ATAG) committed to keep total aviation emissions flat at the 2005 level from 2020 onwards, and

to achieve a 50% reduction by 2050

Corporate members of the Clean Skies for Tomorrow initiative (CST) have developed a joint strategy for

accelerating the transition to carbon neutrality in aviation in Europe by increasing uptake of sustainable

aviation fuels (SAFs) over the next decade

International Air Transport Association (IATA) Schematic CO2 emissions reduction roadmap

Source: Energy Transitions Commission, International Air Transport Association Aircraft Technology Roadmap to 2050

PUBLIC 5

HSBC sets our ambition to build a net zero economy

The transition to net zero carbon emissions presents a clear opportunity to set the global economy on a more sustainable, resilient and inclusive path.

Finance, with its focus on risk and reward, is key to building a future that prioritises resilience, social mobility and the environment alongside economic growth.

Achieving the scale of change needed to meet the Paris Agreement goal to achieve net zero by 2050 or sooner will require significant extra effort, at a faster pace.

For the financial sectors, this means aligning the financed emission - the carbon emissions of the portfolio of customers - to the Paris Agreement goal.

By the end of Climate Week NYC (21-25 Sep): 22 regions, 452 cities, 1,101 businesses, 549 universities and 45 of the biggest investors have now joined the Race to Zero, the United Nations Framework Convention on Climate Change (UNFCCC) global campaign for a

zero-carbon world1.

HSBC’s ambition is to be the leading bank for the transition to net zero through a three-part plan

Becoming a net zero bank Supporting our customers Unlocking new climate solutions

Align our financed emissions2 to achieve net zero by 2050 or sooner Dedicated ESG Solutions Unit to support customers on their journey to HSBC Pollination Climate Asset Management – in order to build world’s

lower carbon emissions leading natural capital managers

Use the Paris Agreement Capital Transition Assessment Tool (PACTA)

Provide between USD750bn and USD1trn of financing and investment over Target $100m CleanTech investment within our technology venture debt

Make regular, transparent TCFD disclosures to communicate progress the next 10 years fund to support CleanTech innovation

Collaborate with stakeholders for globally consistent standard for Increase our portfolio of transition finance solutions to help even heavy- Launch $100m philanthropic programme to scale climate innovation

financed emissions and carbon offset market. emitting sectors to decarbonise ventures between now

and 2025

Be net zero in our operations and supply chain by 2030 or sooner. Apply a climate lens to our financing decisions across developed and

developing economies Help transform sustainable infrastructure into a global asset class, and

create a pipeline of bankable projects

1. New York Climate Week announcements (link)

2. The carbon emissions of its portfolio of our customers

PUBLIC 6

Global Sustainable Bond Market Snapshot

Issuance progression (USD bn) Issuance by sector (FY2020)

USD bn

600

500 CAGR 2015-2020: 100

Global: 64%

Corporate(27%) Financial(17%)

400 Asia-Pacific: 76% 132

EMEA: 62%

300 Americas: 62% 86

$573bn

200 80

64 341

48 49 SSA(56%)

100 26 169

6 46

12 17 81 94

0 31 39

2015 2016 2017 2018 2019 2020

EMEA Americas Asia-Pacific

GSS Bond supply: +185% 2021YTD YoY at USD210bn eq. More than +320% increase in Europe and 160% in APAC

Issuance by bond type (FY2020)

USD bn HSBC market

250 $210bn share

America

s: 5.8%

Green(50%)

200

38

Asia Pacific

Social(28%)

150 41

9.0%

#1

2021 YoY $573bn

$74bn EMEA: +327% Sustainability(19%)

100

APAC: +161% EMEA

15 Americas: +44% 131 6.1%

50 28

#2 SLB(3%)

31

0

2020 - Mar 2021 - Mar

EMEA Americas Asia-Pacific

Source: HSBC Green, Social, Sustainability Bond database – based on Dealogic, CBI, Bloomberg, as of 20th Mar 2021

The data presented above is to the best of our knowledge and may not be fully representative of the SRI market

PUBLIC 7

Global Sustainable Loan Market Snapshot

Global Green and Sustainability Linked Loan (SLL) Volumes by Region Green & SLL Borrowers by Sector (FY2020)

USD bn

240

250

194

200

150 15% Utilities

100 72 Oil and Gas

50 34% General Manufacturing

12 9% Financial Services

0

2017 2018 2019 2020 Retail & Supermarkets

Asia Pacific EMEA N. America Others

Healthcare

9%

Telecommunications

Global Green and Sustainability Linked Loan (SLL) Volumes by Type 4% 7%

Automotive

USD bn 5% Business Services

240 5% 6%

250 6% Others

194

200

150

100 72

50

12

0

2017 2018 2019 2020

Green Loan SLL

Source: Loanconnecter, 5 Jan 2021

PUBLIC 8

Green / Social / Sustainability Bonds and Green Loans

External Review

Use of Proceeds Evaluation Process Funds Tracking Reporting

PUBLIC 9

Green, Social and Sustainability

Use of Proceeds

Support of Green projects including, but not limited to...

Renewable energy Green buildings Climate change adaptation

Sustainable water /

Pollution prevention and control Eco-efficient / circular economy

wastewater management

Waste prevention, reduction;

Clean transportation Sustainable management of living / natural resources

waste to energy

Energy efficiency Terrestrial / aquatic biodiversity conservation Sustainable animal husbandry

Support of Social projects including, but not limited to...

Food security Affordable Housing

Access to essential services Affordable basic infrastructure

Employment generation via SME lending Socioeconomic advancement and empowerment

PUBLIC 10Potential Use of Proceeds

Aviation

Project Categories Description

Air transport (passenger and freighter aircraft) and aircraft manufacturing, maintenance and

Aircraft

technology development

Fuel production, storage and distribution Sustainable aviation fuels (SAFs) including advanced biofuels and electrofuels

Performance improvements through reduction of fuel consumption in airport ground

Air traffic management (ATM)

operations

Airport Airport operations and ground handling and construction of airport infrastructure

Sustainable water and wastewater

Sustainable use and protection of water and marine resources

management

Infrastructure to adapt to extreme weather / climate conditions, information support systems

Climate change adaptation

such as climate observation / early warning systems

Circular economy Improve aircraft decommissioning practices

Pollution prevention and control Noise / air pollution

Terrestrial and aquatic biodiversity

Protection of biodiversity and ecosystems

conservation

PUBLIC 11Green / Social / Sustainability Bonds and Green Loans

External Review

Better recognition by international investors Popular among Asian/China issuers

1 Second party opinion 2 Limited assurance report

Most popular option Assurance performed on internal procedures and policies

Based on GBP / SBP /SBG recommendations aligning with Green/Social/Sustainability Bond Framework

Framew

ork Review performed on issuers Green/Social/Sustainability Bond Framework Can express opinion based on GBP / SBP / SBG

recommendations

based

Popular among Asian/China issuers Systematic approach to achieve a rating

Hong Kong Quality Assurance Agency

3 Climate bond certification 4 (HKQAA)

5 5 S&P

Bond by Based on Climate Bonds Standard that Based on HKQAA proprietary Assessment Based on S&P’s proprietary Green Bond Assessment

bond focuses on projects that deliver GHG- Scorecard and methodology Scorecard and methodology

emissions reduction For Green Bonds and Green Loans Only for Green Bonds

based

Only for Green Bonds / Loans Potential subsidies from HK Government

Code:

Green text = advantage of this option

PUBLIC 12Cliffton Limited / Delhi International Airport Limited

USD450m 144A/RegS Senior Green Bond

Transaction Highlights

On 18th March 2021, Cliffton Limited (“the issuer”)/Delhi International

Airport Limited (“DIAL”) priced US$450mio 4years and 7months

Landmark deal for the company as well as for the market in general given the multiple structuring aspects

senior green bond issuance under 144A/RegS format.

involved in the transaction including a consent solicitation exercise across 3 existing bonds, an any and all tender

On the back of a conducive market backdrop post FOMC and a strong on 1 bond and a new issuance which was labelled green and used an offshore SPV issuance structure and all

investor feedback/indications of interest post the global investor overlaid with a sector deeply impacted by the pandemic which required intensive investor engagement. HSBC acted

calls, the issuer announced the transaction at an Initial Price as a Joint Global Coordinator and played a pivotal role in the structuring of the transaction. HSBC also acted as the

Guidance (“IPG”) of 6.50% area. Strong support from the investors Joint Green Structuring Agent on this trade. The proceeds will be allocated to an Eligible Green Project Portfolio

helped orderbook reach over US$1.5bn (c.3.75x oversubscription)

under DIAL’s Green Finance Framework which has been reviewed by CICERO which has issued a Second Party

ahead of the Final Pricing Guidance (“FPG”) announcement which

allowed the issuer to announce the FPG at 6.25% (#), representing a Opinion

pricing compression of 25bps from the IPG. The company eventually The execution had to navigate significant volatility in the market caused by large and swift moves in US

priced US$450m at 6.25% upsized from initial expectation of

US$300m.

Treasuries but issuer was able to pick a constructive market window immediately after the FOMC rates decision on

17Mar

HSBC acted as a Joint Global Coordinator and played a pivotal

Investor demand was quite robust from the time the transaction was announced with orders reaching more than

role in the structuring of the transaction. HSBC also acted as

the Joint Green Structuring Agent on this trade US$1.5bn ahead of the final price guidance announcement representing a c.3.75x oversubscription. The orderbook

was very well diversified across the geography and in terms of investor type. The deal attracted significant

HSBC also acted as a Dealer Manager & Solicitation Agent on interest from top global real money accounts demonstrating the confidence these investors have in the

DIAL’s tender offer to buyback any-and-all of its outstanding DIAL credit. Limited price sensitivity seen in the book as it continued to grow in US hours with final books at

US$288.75mn 6.125% senior secured notes due 2022 and c.$1.28bn (oversubscription of c.2.8x) despite intra-day volatility in treasuries and price tightening of 25bps from the

consent solicitation on all the existing bonds to approve certain

initial price guidance which allowed the issuer to upsize the transaction to US$450m from earlier expectation of

proposed amendments

US$300m

The transaction achieved multiple objectives for the issuer including refinancing their upcoming bond

maturity, increasing future financing flexibility, and also fully tying up their funding needs for the capex

under the Phase 3A expansion plan of Delhi Airport

Final orderbook over US$1.28bn (including US$20m JLM interest) across 123 accounts at reoffer

By Geography (%) By Investors (%)

Asia 5%

7% 6%

27% FM

US

Banks

36% EU

30% 89% PB/Corp

Middle East

PUBLIC 13Airport Issuers Precedents

Select Framework Examples

Selection & Evaluation/ Management of

Issuer Use of Proceeds Proceeds Reporting/ External Review Bonds issued

Eligible Categories: No ring-fencing; proceeds earmarked Quarterly reporting

USD1bn 10.6yr and USD3bn

- Sustainable buildings GACM has established a NAICM Green Second party opinion from Sustainalytics

29.9yr

Bond Committee with responsibility for Moody’s Green Bond Assessment score of

- Renewable energy Sept-17

governing the NAICM Green Bond GB1 (‘Excellent’) and S&P Green Evaluation

- Energy efficiency Framework score of E1/77

- Water and wastewater management USD1bn 10yr and USD1bn

Mexico City Airport Trust

- Pollution prevention and control 30yr

Sept-16

- Conservation and biodiversity

Eligible Categories: No ring-fencing; proceeds earmarked Annual reporting

- Green Buildings Green Bond proceeds will be evaluated and Second party opinion from Sustainalytics

selected by Schiphol’s Sustainability EUR500m 12yr

- Clean Transportation

Committee. Oct-18

Royal Schiphol Group (Amsterdam

Airport)

Eligible Categories: Ring-fenced; portfolio based Annual reporting

- Green buildings and infrastructure The selection of Eligible Green Assets is Second party opinion from CICERO

managed by a dedicated group consisting of

- Energy efficiency SEK1bn 5.25yr

senior management members including

- Renewable energy Dec-19

CEO, CFO and responsible for Sustainability

Swedavia Airports - Pollution prevention and control among others.

- Clean transportation

Eligible Categories: No ring-fencing; proceeds earmarked Annual reporting

- Green buildings Second party opinion from CICERO

- Renewable energy

USD450m 4yr and 7m

- Energy efficiency Mar-21

Delhi International Airport - Clean transportation

- Pollution prevention and control

- Sustainable Water Management

DENOTES HSBC AS LEAD MANAGER PUBLIC 14

Source: Climate Bonds Initiative, Issuers’ public documents, HSBC AnalysisSustainability-Linked Bonds and Loans

Sustainability-Linked Bonds (“SLBs”) and Sustainability-Linked Loans (“SLLs”) are any type of instrument for which the financial and/or structural characteristics can vary depending on whether the issuer / borrower achieves predefined Sustainability / ESG

objectives

The Principles have five core components:

1 2 3 4 5

Selection of KPIs Calibration of SPTs Bond characteristics Reporting Verification

• KPIs should be: SPTs should be: • Should include a financial and/or structural impact • Issuers should make readily available and • Issuers should seek independent and external

• relevant, core and material to the issuer’s overall • ambitious and represent a material improvement involving trigger event(s) accessible: verification of their performance level against each

business, and of high strategic significance to the • consistent with the issuers’ overall sustainability / • Variation of the bond financial and/or structural • up-to-date information on the performance of the SPT for each KPI by a qualified external reviewer

issuer’s current and/or future operations ESG strategy characteristics should be commensurate and selected KPI(s) with relevant expertise

• measurable or quantifiable • be determined on a predefined timeline meaningful • a verification assurance report • At least once a year, and in any case for any

• externally verifiable Target setting exercise should be based on a • Fallback mechanisms in case the SPTs cannot be • any information enabling investors to monitor the date/period relevant for assessing the SPT

• able to be benchmarked combination of benchmarking approaches: calculated or observed should be explained level of ambition of the SPTs performance leading to a potential adjustment of

• Issuers should communicate clearly to investors • issuer’s historical performance for a minimum of • KPI(s) definition and SPT(s) (including calculation • Reporting should be published regularly, at least the SLB financial and/or structural characteristics,

the rationale and process according to which the 3 years methodologies) and the potential variation of the annually until after the last SPT trigger event of the bond has

KPI(s) have been selected and how the KPI(s) fit into SLB’s financial and/or structural characteristics been reached

• relative positioning versus peers, where available

their sustainability strategy should be included in the bond documentation • Verification should be made publicly available

• reference to science or absolute levels or

• Clear definition of the KPI(s) should be provided and regional/international targets or proxies • Pre-issuance external review is recommended,

include the applicable scope or perimeter; as well however post issuance verification is a necessary

as the calculation methodology element of the SLBP

KPI: Key Performance Indicator

SPT: Sustainability Performance Target

PUBLIC 15Sydney Airport

AUD1,400m multi-tranche Sustainability Linked Loan

Deal highlights

I. Relationship to Sydney Airport’s overall sustainability strategy

On 23 May 2019, HSBC acted as the Lender for Sydney Kingsford Smith Airport’s

Reporting on objectives against their flagship initiatives and on progress towards achieving them. Primarily, the company

AUD1.4 billion Sustainability Linked Loan (SLL) where the interest rate of the loan is tied

Transaction

to an external Sustainability Performance Target (SPT) which is proposed to be

aims to be Carbon Neutral by 2025. One of the key related objectives is to reduce carbon emissions per passenger by 50%

summary from 2010 baseline levels by 2025 and they had been reduced 30.9% by 2018

Sustainalytics ESG Risk Rating. This represents the 1st Syndicated Sustainability

Linked Loan In Australia

Ongoing performance benchmarking to further assess progress on ESG issues. These include consideration of independent

ESG ratings, inclusion on sustainability indices, and quantitative third-party assessments

Alignment with the Sustainability Linked Loan Principles 2019

I. Relationship to Sydney Airport’s overall sustainability strategy II. Delivering the commitment

1 2 3 4 5 Target Setting - Sustainalytics ESG Risk Rating

Reporting on The final ESG Risk Rating that Sydney Airport is targeting to achieve would place the borrower in the top 5 th

Identifying 3 Creating a Ongoing ESG

material areas of

Implementing 3

Governance

Objectives and to

performance 2 percentile of the Airports sub-industry. Therefore, Sustainalytics is of the opinion that targeting to achieve a

flagship initiatives be Carbon Neutral placement in the top 5th percentile of the Airports sub-industry is ambitious, since it would ensure that the

commitment framework benchmarking

by 2025 borrower is a top performer as compared to its peers.

Reporting

Identifying three material areas of commitment: responsible business, planning for the future, and supporting

The SLLP recommends that borrower’s make and keep readily available up-to-date information relating to their

communities. The process to define material areas included engagement with key stakeholders, such as

3 SPTs. Sydney Airport is demonstrating good practice by intending to make their ESG Risk Rating publicly available.

employees, community members, local government, and industry associations. Within each of these pillars,

Rating with its sustainability strategy, and its progress towards achieving the top 5th percentile in the Airports sub-

specific performance targets have been set

industry.

Implementing three flagship initiatives which have been determined to be most relevant to advancing

sustainability performance across the organization. These initiatives aim to: Review

1) increase the climate resilience of its assets and operations; 4 Sydney Airport’s performance against its SPT will be verified by virtue of the ESG Risk Rating being updated

annually by Sustainalytics. In addition, Sydney Airport is demonstrating good practice by intending to make publicly

2) achieve the electrification of vehicles and equipment, and available their ESG Risk Rating.

3) increase airspace and airfield efficiency

Sustainalytics is of the opinion that Sydney Airport’s SLL will support the company’s overall

Describing the governance framework which will support the progress towards meeting the sustainability goals sustainability strategy. In addition, the use of an ESG rating as a basis for target-setting is

and plans described. This structure involves the creation of three working groups or committees focused on the recognized as credible by the Sustainability Linked Loan Principles, and the borrower has

implementation of various aspects of the sustainability strategy; all three bodies report to the Executive committed to disclosing their ESG Risk Rating on an annual basis. Based on the above

Committee and Safety Steering Committee, which in turn reports to the Board Safety, Security and Sustainability considerations, Sustainalytics is of the opinion that Sydney Airport’s SLL is aligned with the

Committee SLLP

PUBLIC 16Climate Transition Finance Handbook – at a glance

Handbook to be used when raising funds in debt markets for climate transition-related purposes, whether this be in Use of Proceeds format or Sustainability-Linked

01 02

Financing purpose should be for enabling an issuer’s climate Climate trajectory should be materially relevant to business

change strategy model

Science-based targets and pathways Transparency of underlying investment program

03 04

PUBLIC 17Transition

ICMA Climate Transition Finance Handbook

Transition happens at the issuer level, not the instrument level, hence issuer-level disclosures need to be demonstrated for a credible instrument.

Climate Transition Finance can be Use of Proceeds or Sustainability-Linked

Transition bond issuances to date

Date Issuer Size Use of Proceeds

Based on the two principles of “Avoidance of Carbon Lock-in” and “Do No Significant Harm” and the list of “Explicitly Excluded Projects”, eligible projects include: Projects in the Public Utility,

Cement, Aluminium, Steel and Fertilizer Manufacturing industries which are in line with strategic pathways of carbon neutrality goals and strategies of the countries or regions the projects are

USD500m

Jan 2021 located in.

CNH 1.8bn

Aligned to ICMA Climate Transition Finance Handbook (2020), as well as in consideration of the climate change mitigation transition activities classification as defined in the TEG Final Report on

the EU Taxonomy

USD600m

Oct 2020 Financing of energy efficient projects, including both aircraft upgrades and R&D into sustainable aviation fuel.

Building of natural gas fired power plants, and associated enabling infrastructure including facilities required for the receipt and delivery of gas to the plants, where the opportunities to develop

Feb 2021 USD300m

renewable energy is limited;

Jun 2020 USD350m

Conversion of coal fired power plants, and the facilities or modifications associated with such conversion, which, in both cases, will result in carbon emission no more than 450gCO2/kWh2 at

Jul 2017 USD500m

baseload.

Infrastructure, equipment, technology, systems and processes that demonstrate a reduction in energy use/losses and reduction in emissions in industrial facilities.

Jun 2020 EUR500m Acquisition and development of biomethane plants and upgrading of existing biogas plants

Activities and projects carried out with the aim to adapt Snam’s gas network to be ready to transport a certain increasing percentage of hydrogen and/or other low-carbon gases

Replacement of pipeline to facilitate the integration of hydrogen and other low-carbon gases, and reduce methane leakage

Feb 2020 EUR500m

Repair and replacement of existing gas pipeline that is already hydrogen-ready in order to reduce methane leakage

PUBLIC 18Etihad Airways

The World’s First Transition Sukuk and First USD Issuance from the Aviation Sector

Summary Terms:

On 28th October 2020, Etihad Airways priced the first

ever transition sukuk globally and the first ever Issuer Unity 1 Sukuk Limited

transition bond or sukuk issued by an airline in the Obligor Etihad Airways P.J.S.C.

USD market. Issue Ratings A by Fitch

Status and

Etihad established its Transition Finance Framework in Senior Unsecured RegS only Unlisted Transition Sukuk

Format

order to issue a Sukuk with a use of proceeds

commitment and a sustainability linked carbon Sukuk Structure Rights to travel based structure

emissions metric to demonstrate its commitment to Issue Size US$ 600,000,000

reducing the emissions intensity of its business. Pricing Date 28 October 2020

Tenor 5 years bullet

Etihad combined its new issue of USD 600mn with a Maturity 3 November 2025

tender offer of USD 300mn in order to partially Re-offer Spread 200bps

refinance its USD Sukuk maturing in 2021. Re-Offer Yield 0.394%

HSBC acted as a Global Coordinator, Joint Re-Offer Price 2.394%

Structuring agent, Joint Lead Manager and Governing Law English Law

Bookrunner on the transaction. Denominations USD 200,000 and integral multiples of USD 1,000 in excess thereof

SPO Provider: Vigeo Eiris

An amount equal to the proceeds will be allocated to finance and/or

Use of Proceeds: refinance new and/or existing projects from in accordance with the

Transition Finance Framework.

Listing Unlisted

Global Coordinator, Joint Structuring Agent, Joint Lead Manager

HSBC Role

and Bookrunner

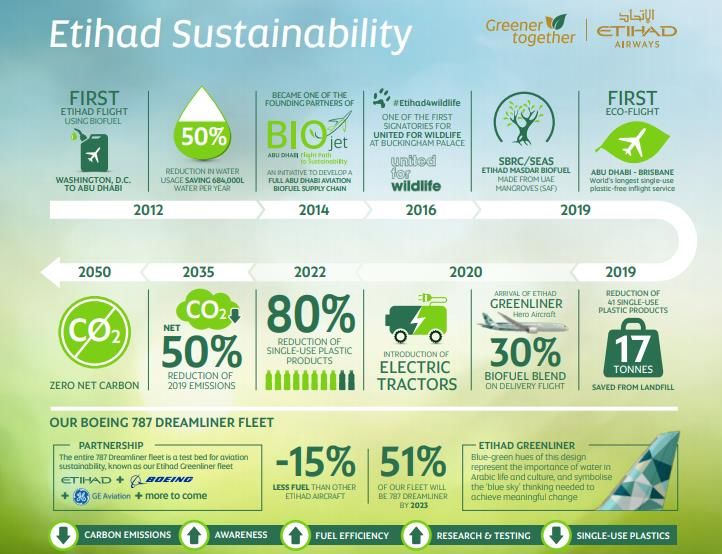

2019 sustainability initiatives overview Sustainability commitments

• Etihad’s biofuel flight in Jan-19, operated by a Boeing 787-9 from Abu Dhabi to Amsterdam, • Etihad continues to be a leader, together with its partners in the UAE and around the world, in pioneering

represented the maiden flight of an aircraft partly powered by fuel derived from the seeds of the new and effective ways of mitigating aviation’s environmental impact

Salicornia plant home grown in the UAE

• The sustainability strategy of the Etihad Aviation Group is aligned to the 17 Sustainable Development

• In Apr-19, Etihad flew a single-use plastic-free flight between Abu Dhabi and Brisbane and in Goals of the United Nations

doing so made a commitment to reduce single-use plastics company-wide by 80% by 2022

• In Jan-20, in the presence of the EU Commission Etihad announced our commitment of zero net carbon

• At the Dubai Airshow in Nov-19, Etihad launched the Greenliner Programme in a strategic, global Emissions by 2050 and halving of 2019 emissions by 2035

eco-partnership with Boeing and GE

• The company remains at the forefront of efforts to pioneer new and effective ways of mitigating aviation’s

• In Dec-2019, Etihad became the first airline to secure funding for a project based on our environmental impact, to reduce carbon emissions and to create cleaner and more sustainable

compatibility with the Sustainable Development Goals of the United Nations. Etihad borrowed transportation for future generations

100 million Euros (AED 404.2 million) to support expansion of the Etihad Eco-Residence, a

sustainable apartment complex for our Cabin Crew PUBLIC 19Etihad Airways

Transition Finance Framework – Use of Proceeds Framework

Etihad established a Transition Finance Framework (the “Framework”) to demonstrate how the Group and its other entities intend to transition the

business in alignment with the goals of the Paris Agreement.

The Transition Finance Framework has two component frameworks: 1) A use of proceeds framework and 2) A sustainability linked finance

framework:

1) Use of proceeds framework

Eligible

Eligibility criteria Example Green Assets Exclusions UN SDGs

Category

Investments in next generation

Development, manufacture and/or installation of Investments in next Aviation

aircraft to replace old fleet (such as

energy efficiency aviation technologies and fuels derived from non-

Boeing 787-9 and Boeing 787-10)

products with a view to improving energy efficiency. RSPO certified palm oil

Research and development into

Eligible Assets should have an energy efficiency Non-waste biofuels that

Sustainable Aviation Fuels (These

Energy (weighted average) that leads to energy savings of compete with food

include the development of

Efficiency at least 15% against previous technologies. production

sustainable alternative fuels, which

R&D in sustainable aviation fuels, including Biofuels that negatively

can be produced in commercial

biofuels, for improved fuel efficiency. Direct impact biodiversity, e.g.

quantities for use not only within the

emissions from the production of biofuels will be at habitat loss or displacement

Emirates, but also nationally and

least 80% lower than fossil fuel counterfactual. of natural ecosystems

internationally.)

• Etihad has established an Environmental Performance Taskforce with responsibility for governing and implementing the initiatives set out in the Framework.

• The respective project team will identify potential eligible projects based on the eligibility criteria outlined in the Use of Proceeds section.

Governance • Once identified, all transition assets will be subject to an extensive due diligence process that will examine all aspects of the projects including, but not limited to:

- Selection validation of selected target group, confirmation of alignment with SDGs, financial analysis of project costs, assessment of project feasibility, scrutiny around the stated

Process and benefits and their measurement.

Management of • The proceeds of each issuance under the Framework will be deposited in the general funding accounts and to be earmarked to eligible projects, with management of

Proceeds proceeds overseen by the Treasury, Tax and Finance department.

• Etihad has established a Sustainable Financing Register to record the allocations and track the use of proceeds of issuances under this framework.

Allocation Reporting: Impact Reporting – Energy Efficiency:

The amount or percentage of allocation to the Eligible Transition Portfolio Reduced and/or avoided GHG emissions (in t. CO2e /year)

Examples of Eligible Assets invested in from the proceeds an issuance CO2 / Revenue Tonne Kilometre

Reporting The geographic distribution of assets funded Use of sustainable aviation fuel (adjusted distance travelled using biofuels)

The portion of the proceeds from each issuance that is for new financing vs. Number of research programs funded

refinancing, and Types of research studies launched

The balance of the unallocated proceeds of each issuance under the Framework Qualitative case studies on R&D projects

PUBLIC 20Etihad Airways

Transition Finance Framework – Sustainability Linked Framework

Etihad established a Transition Finance Framework (the “Framework”) to demonstrate how the Group and its other entities intend to transition the

business in alignment with the goals of the Paris Agreement.

The Transition Finance Framework has two component frameworks: 1) A use of proceeds framework and 2) A sustainability linked finance

framework:

2) Sustainability Linked Finance Framework

Key Performance Indicator (KPI) Sustainability-Performance Targets (SPTs)

Etihad selected the Carbon-dioxide emissions to Revenue tonne kilometres (Co2e/RTK) metric to measure the

emissions intensity of its fleet over the short, medium and long term. The KPI selected is consistent with The Sustainability Performance Target is set at 714 kg

Etihad’s strategic priority to reduce its carbon emissions as part of its sustainability strategy. CO2/RTK for the passenger fleet, which results in a total

o Commitment to Net Zero Carbon emissions as per Etihad Aviation Group (EAG)’s 2050 target CO2/RTK of 574, with a Target Observation Date of 31

o 50% reduction in net emissions by 2035, based on CORSIA established baseline (2019) and a 20% December 2024. This is an aggregate reduction of 17.8%

reduction in emissions intensity (CO2/RTK) in Etihad’s passenger fleet by 2025, based on EAG fleet over the 2017 baseline of 869 g CO2/RTK

transformation plan initiated in 2017

In issuing a Sustainability-Linked Sukuk, Etihad is voluntarily adding to its existing commitments under CORSIA, committing to also invest in additional climate

Sukuk

reduction projects to promote its target to reduce carbon emissions intensity by over 20% from the 2017 baseline (based on Fleet Transformation efforts).

Characteristics

However, if the target is not met, Etihad commit to purchasing additional offsets

On an annual basis until the Observation Date, Etihad will disclose performance on fuel burn, RTK, and CO2/RTK for the passenger fleet and across the entire fleet

on its website as part of its annual press release on performance.

This reporting will be made available within six months of each calendar year end and will also include information on the efforts made to improve emissions intensity,

Reporting

and any other relevant information to enable progress on the SPT.

Reporting on fuel burn and RTKs is also submitted on an annual basis to ICAO as part of Etihad’s reporting under the CORSIA agreement. Etihad will provide a final

report on the performance of the KPI against the predefined SPT within six months of the Target Observation Date.

Etihad will obtain annual verification of performance on fuel burn, RTK and CO2/RTK from an External Verifier. The External Verifier means KPMG Lower Gulf or any

such other qualified provider of third party assurance or attestation services appointed by Etihad.

Verification Fuel burn and RTK reporting is also audited for Etihad’s submissions to ICAO. This verification will be confirmed in the company’s annual results disclosure.

Etihad’s performance on the KPI at the Target Observation Date will be verified by an External Verifier, who will provide reasonable assurance on the performance of

the company under the ISAE 3000 and AA1000 2008 AS Standards (or equivalent).

This verification will be included on the company’s website within six months of financial year end.

PUBLIC 21Pricing Analysis of GSS Bonds - APAC

Over-Subscription Analysis Price tightening Analysis NIP Analysis

20.00 100.00

80.00

80.00

70.00

15.00 60.00

60.00

40.00

50.00

20.00

10.00 40.00

-

30.00

(20.00)

5.00 20.00

(40.00)

10.00

(60.00)

- - May-18 Nov-18 May-19 Nov-19 May-20 Nov-20 May-21

Apr-18 Oct-18 Apr-19 Oct-19 Mar-20 Sep-20 Mar-21 May-18 Nov-18 May-19 Nov-19 May-20 Nov-20 May-21

Conventional GSS Conventional GSS Conventional

Linear (Conventional) Linear (GSS) Linear (Conventional) Linear (GSS) GSS

GSS Conventional Bond GSS/Conve

GSS Bond Conventional Bond GSS/Conventi GSS Bond Conventional Bond GSS/Conventi (average) (average) ntional

(median) (median) onal (average) (average) onal 2018 2H 9.50 16.07 0.59

2018 2H 2.60 x 2.23 x 1.17 x 2018 2H 21.50 20.63 1.04 x

2019 1H (1.62) 3.15 (0.51)

2019 1H 4.00 x 3.79 x 1.05 x 2019 1H 29.50 30.79 0.96 x

2019 2H (0.83) (0.21) 3.94

2019 2H 3.80 x 4.18 x 0.91 x 2019 2H 28.33 28.80 0.98 x

2020 (1.36) 2.15 (0.63)

2020 5.51 x 5.10 x 1.08 x 2020 43.00 38.12 1.12 x

2021ytd (2.89) (0.89) 3.24

2021ytd 6.18 x 5.45 x 1.13 x 2021ytd 43.82 40.71 1.08 x

Overall 0.41 2.01 0.20

Overall 4.68 x 4.25 x 1.10 x Overall 35.84 33.37 1.04 x

The analysis compares the Price Tightening in bps of USD The analysis compares the New Issuance

The analysis compares the Over-Subscription multiple of

GSS bonds and conventional bonds issued in APAC since Premium (NIP) in bps of USD GSS bonds and

USD GSS bonds and Conventional bonds in APAC since

20182H* conventional bonds in APAC since 20182H*

20182H*

GSS bonds on average have larger Price Tightening than GSS bonds achieved negative NIPs in 2020 and

GSS bonds generally achieved higher Over-Subscription

conventional bonds, and this trend becomes more and more 2021ytd, generally showed significantly lower NIP

multiples

significant in recent periods than conventional bonds

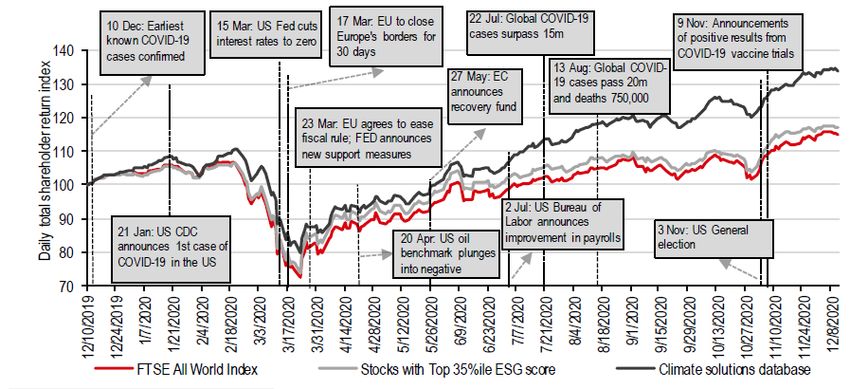

* Deals which HSBC led PUBLIC 22Growth and outperformance of ESG / Green

Outperformance over 12 months of COVID-19 crisis

Source: HSBC Research: ESG and Climate - Strong price momentum in 2020 (18 December 2020), FTSE Russell, Refinitiv Datastream, HSBC

PUBLIC 23Key Climate Change Regulation for Financial Services

Growing focus on how FIs manage climate change risks by international bodies and regulators

Joint Committee on Climate Change (JC3) set up to support the financial Climate stress test by 2021

industry’s response to climate-related risks Climate stress test by 2022 Partners with IFC to lead Asia Chapter of the Alliance for Green

Discussion paper on “Climate Change and Principle-based Taxonomy” issued in Commercial Banks

Convened the Green Finance Industry Taskforce (GFIT), and issued a

2019 proposed taxonomy for Singapore-based FIs to identify green or

transition activities

To launch Climate Biennial Exploratory Scenario exercise to explore financial Announced plans to have banks undertake stress tests to measure their

risks from climate change by 2021 resilience to a broad range of scenarios, including “climate change

financial risks”

Launched pilot climate stress test in 2020 (voluntary)

83 members and 13 observers of global Central Banks and Supervisors

Published in 2020 the NGFS climate scenarios for central banks and supervisors To implement mandatory climate risk reporting for the

and the accompanying Guide to scenario analysis for central banks and supervisors financial sector in line with TCFD recommendations

PUBLIC 24The Task Force on Climate Related Financial Disclosure (TCFD)

Transition Risks Opportunities Governance: The organization’s governance around climate-related risks and

Policy and Legal Resource Efficiency opportunities

Technology Energy Source Governance

Market Products/Services Strategy: The actual and potential impacts of climate related risks and

Risks Opportunities Strategy

Reputation Markets opportunities on the organization’s businesses, strategy, and financial

Physical Risks Resilience

planning

Strategic Planning Risk

Acute Management

Risk Management

Chronic

Risk Management: The processes used by the organization to identify, assess,

and manage climate related risks

Metrics and

Financial Impact

Targets

Metrics and Targets: The metrics and targets used to assess and manage

relevant climate related risks and opportunities

Revenues Balance Assets & Liabilities

Income Statement Cash Flow Statement

Expenditures Sheet Capital & Financing

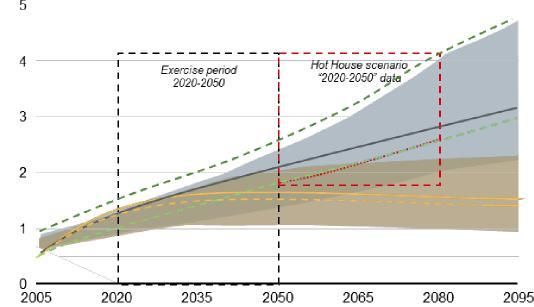

Climate-Related Metrics and Associated Risk Types Network of Central Banks and Supervisors for Greening the Financial System (NGFS)

Emissions Level

HGH emissions Emissions Intensity

Embedded Emissions The NGFS have outlined 3 scenarios (Orderly, Disorderly and Hot House World) – mapped to RCP scenarios1 below

Transitional Risks

Energy Usage

Energy/Fuel Energy Intensity

Energy Mix

Water Usage

Water Water Intensity

Water Source

Locations within a Coastal Zone

Location

Locations within a Flood Zone

Physical Risks

Land Cover Type

Land Use

Land use Practices

R&D into low carbon products, services, technology

Risk Adaption/ Mitigation

CapEx into deployment of low carbon products, services, technology

1. Source for NGFS / RCP overlap diagram: IIASA NGFS Climate Scenarios Database. 90% uncertainty range based on the MAGICC6 model for each Representative Concentration Pathway (RCP)

PUBLIC 25What’s Next?

Key themes

Fuels

Technology Operations

Regulations Consumer

Behaviour

PUBLIC 26Disclaimer

The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) has prepared this document (the “Document”) for information purposes only. This Document does not constitute a commitment to underwrite or purchase or subscribe for all or

any portion of the securities mentioned herein. Any such commitment shall be evidenced only by a fully executed subscription agreement, purchase agreement or similar contractual document. This Document should also not be construed as an

offer for sale of or subscription for any investment, nor is it calculated to invite/solicit any offer to purchase or subscribe for any investment.

HSBC has based this Document on information obtained from sources it believes to be reliable but which it has not independently verified. HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability for the

contents of this Document and/or as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Document. HSBC and its

affiliates and/or its or their respective officers, directors and employees may have positions in any securities mentioned in this Document (or in any related investment) and may from time to time add to or dispose of any such securities (or

investment). HSBC and/or any of its affiliates may act as market maker or have assumed an underwriting commitment in the securities of any companies discussed in this Document (or in related investments), may sell them to or buy them from

clients on a principal or discretionary basis and may also perform or seek to perform banking or underwriting services for or relating to those companies. As HSBC is part of a large global financial services organisation, it or one or more of its

affiliates may have certain other relationships with the parties relevant to the proposed activities as set out in this Document, and these proposed activities may give rise to a conflict of interest, which the addressee hereby acknowledges.

No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This Document, which is not for public circulation, must not be copied, transferred or the content disclosed to any

third party and is not intended for use by any person other than the addressee or the addressee's professional advisers for the purposes of advising the addressee hereon.

The Hongkong and Shanghai Banking Corporation Limited

Level 17 HSBC Main Building

1 Queen’s Road Central

Hong Kong SAR

© Copyright. The Hongkong and Shanghai Banking Corporation Limited 2021, ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

PUBLIC 27You can also read