INVESTOR UPDATE FOURTH QUARTER 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTOR UPDATE

FOURTH QUARTER 2021

U N L E S S O T H E RW I S E I NDI C A T E D, ALL RPT F I NA NCIA L I NF O R MA T I O N IS P R E S E N T E D ON A C O NS O L I DA T E D B A SI S A ND I NCL UDI NG I T S P RO - RA T A S HARE

O F UNCO NS O L I DA T E D J O I NT V E NT URE S AND IS AS OF OR FOR THE Q UA RT E R E NDE D DE CE MB E R 3 1 , 2 0 2 1 . UNL E S S O T HE R W IS E I NDI CA T E D, A L L

DE MO G RA P HI C DA T A I S S O URCE D F RO M E S RI . RECO NCI LI AT IO NS OF NO N-G AA P MET RI CS CAN BE FO UND ON T HE CO MP ANY’S W EBSIT E AT

I NV ES TO RS .RPT RE A LT Y. CO M O R BY F O L L OW ING THI S LI NK : 4 Q 2 0 2 1 INVE ST OR PRES ENTAT IO N RECO NCI L IAT IO N O F NON- GA AP F INANCI A L MEA SURES.

FOR IMPORTANT INFORMATION REGARDING FORWARD-LOOKING STATEMENTS IN THIS PRESENTATION, SEE SLIDE 2.

The impact COVID-19 has, and will continue to have, on the Company and its

F O R WA R D

tenants is highly uncertain, cannot be predicted and will vary based upon the

duration, magnitude and scope of the COVID-19 pandemic, including any related

variants, the short-term and long-term effect of COVID-19 on consumer

LO O K I N G behaviors, the effectiveness and availability of vaccines or cures for COVID-19

and the willingness of people to take available vaccines, as well as the actions

S TAT E M E N T S taken by federal, state and local governments to mitigate the impact of COVID-

19, including social distancing protocols and restrictions on business activities,

and the effect of any relaxation or revocation of current restrictions. Additional

factors which may cause actual results to differ materially from current

expectations include, but are not limited to: our success or failure in

implementing our business strategy; economic conditions generally and in the

commercial real estate and finance markets such as the inability to obtain equity,

This presentation contains forward-looking statements within the meaning of debt or other sources of funding or refinancing on favorable terms to the

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Company and the costs and availability of capital, which depends in part on our

Securities Exchange Act of 1934, as amended. These forward-looking statements asset quality and our relationships with lenders and other capital providers;

represent our expectations, plans or beliefs concerning future events and may be changes in the interest rate and/or other changes in the interest rate

identified by terminology such as “may,” “will,” “should,” “believe,” “expect,” environment; the discontinuance of London Interbank Offered Rate (“LIBOR”);

“estimate,” “anticipate,” “continue,” “predict” or similar terms. Although the forward- risks associated with bankruptcies or insolvencies or general downturn in the

looking statements made in this document are based on our good faith beliefs, businesses of tenants; the potential adverse impact from tenant defaults

reasonable assumptions and our best judgment based upon current information, generally or from the unpredictability of the business plans and financial

certain factors could cause actual results to differ materially from those in the condition of the Company's tenants; the execution of deferral or rent concession

forward-looking statements. The ongoing impact of the novel coronavirus (“COVID- agreements by tenants; our business prospects and outlook; acquisition,

19”), or the impact of any future pandemic, epidemic or outbreak of any other highly disposition, development and joint venture risks; our insurance costs and

infectious disease, has, and could continue to cause adverse effects on the coverages; increases in the cost of operations; risks related to cybersecurity and

financial condition, results of operations, cash flows and performance of the loss of confidential information and other business interruptions; changes in

Company and our tenants (including their ability to timely make rent payments), the governmental regulations, tax rates and similar matters; our continuing to qualify

real estate market (including the local markets where our properties are located), as a REIT; and other factors detailed from time to time in our filings with the

the financial markets and general global economy as well as on our ability to enter Securities and Exchange Commission ("SEC"), including in particular those set

into new leases or renew leases with existing tenants on favorable terms or at all. forth under “Risk Factors” in our latest annual report on Form 10-K. Given these

uncertainties, you should not place undue reliance on any forward-looking

statements. Except as required by law, we assume no obligation to update these

forward-looking statements, even if new information becomes available in the

future.

FOURTH QUARTER 2021 INVESTOR UPDATE 2

K E Y M E S S AG E S

RPT believes it offers investors a strong return potential of over 30%, given an

above average earnings growth and dividend, as well as multiple expansion

potential, resulting from the material improvements to RPT’s underlying

cashflows.1

Transforming Portfolio and Increasing Cash Flow Strength

RPT was the most active shopping center retail buyer in the U.S. in 2021, acquiring $732 million of gross assets on our balance

sheet, as well as through our grocery anchored and net lease joint venture platforms

Improved exposure in Boston, Atlanta, Tampa and Nashville and reduced exposure to Detroit, Chicago and Cincinnati

Signed four grocer leases throughout the year, materially compressing cap rates at several of our centers

Accelerating Leasing Activity Positioning RPT for Strong Future Growth

Initiated 2022 operating FFO per diluted share guidance of $1.00 to $1.05 per diluted share, representing an 8% increase at the

midpoint over last year, and including expected same property NOI growth of 3.0% to 5.0%2

Signed not open ABR and estimated recovery income of $6.9 million as of December 31, 2021, with an additional $3.3 million in

advanced lease negotiation, in total representing $0.11 of Operating FFO per share

Comparable new lease spreads of 72.8% and 32.5% during the fourth quarter 2021 and on a trailing twelve-month basis,

respectively, demonstrating the mark-to-market opportunity in the portfolio

Focused On External Growth Opportunities

Secured an additional $500 million of commitment from GIC to our core grocery-anchored R2G platform, providing additional upside

in management fee income

Closed on $791 million of investment activity in 2021, significantly improving the quality of the portfolio by increasing exposure by

annualized base rent ("ABR") to high-growth markets such as Boston, Tampa, Atlanta, and Nashville by 12% while reducing

exposure to non-core markets like Detroit, Chicago and Cincinnati by 8% versus 2020

We expect to remain active on the investment front, in both large and small opportunities where we can allocate assets to one or all

of our three strategic platforms

FOURTH QUARTER 2021 INVESTOR UPDATE 3

Why Invest

in RPT?

01

Compelling Total

02

Marked Improvement

03

Strong Internal Growth

Return Potential In Portfolio Quality Potential

04

Differentiated

05

Enhanced External

06

Flexible Balance Sheet

Business Model Growth Opportunities to Support Growth

Initiatives

FOURTH QUARTER 2021 INVESTOR UPDATE 4

01

RPT trades at a relative value discount

despite having refreshed its business

through both external investment

activity and internal leasing success

that has significantly improved the

durability of our cash flows.

• Strong relative total return potential

• Attractive absolute total return potential

Compelling

Total Return

Potential

FOURTH QUARTER 2021 INVESTOR UPDATE 5

Strong Relative Total Return Potential

RPT screens well versus peers on dividend yield, expected growth and on a

relative value basis despite material improvements to portfolio quality, tenant

credit and geographic mix.

Higher Dividend Yield + Higher Expected Growth + Higher Multiple

Expansion Potential

Higher Dividend Yield Higher Growth Expectations Higher Potential for Multiple Expansion

4.4% 9.0% 8.4% 18.0

4.2% 15.3

2022 FFO per share growth 2

Price to 2022 FFO multiple 3

8.0% 16.0

4.2%

7.0% 14.0 12.0

Dividend Yield 1

4.0% 6.0% 12.0

5.0% 10.0

3.8%

4.0% 8.0

3.6% 2.7%

3.6% 3.0% 6.0

2.0% 4.0

3.4%

1.0% 2.0

3.2% 0.0% 0.0

RPT Peer Avg RPT Peer Avg RPT Peer Avg

Peer average includes: BRX, KIM, KRG, SITC, REG, PECO, FRT.

FOURTH QUARTER 2021 INVESTOR UPDATE 6

Attractive Absolute Total Return Potential

Prior to COVID-19 and BEFORE the portfolio quality, tenant credit and geographic mix

improvements achieved since the pandemic started, RPT’s multiple was almost in-line with

peers providing the potential for significant multiple expansion from current levels that RPT

believes could result in over a 30% total shareholder return.

Potential Drivers of Multiple Expansion

• Higher expected 2022 SP NOI growth versus peers

• Higher expected 2022 FFO growth versus peers

• Increasing grocery anchored exposure

• Improving tenant credit

• Better market mix

1 2 3

Peer average includes: BRX, KIM, KRG, SITC, REG, PECO and FRT.

FOURTH QUARTER 2021 INVESTOR UPDATE 7

C O M PA N Y S N A P S H O T

Our Size is Our Advantage

RPT’s smaller portfolio size should allow us to adapt to a rapidly evolving retail landscape

more quickly than larger peers.

Peer Average: 210 Assets1 90

210

CARGO SHIP

572

FOURTH QUARTER 2021 INVESTOR UPDATE 9

RPT At-a-Glance

RPT is an open-air shopping center REIT with enough size to matter to retailers but small enough to quickly respond

to changing market dynamics.

Financial Operating Balance Sheet Corporate

Snapshot Snapshot Snapshot1 Snapshot

12.4% 93.1% 6.8x $2.2B

SAME PROPERTY LEASED RATE

NET DEBT TO ANNUALIZED TOTAL MARKET CAPITALIZATION

NOI GROWTH

ADJUSTED EBITDA

3.4% 90.7% $14M 56%

SAME PROPERTY BASE OCCUPANCY TOTAL CASH 2 % FEMALE EMPLOYEES

RENT GROWTH

90.6% 32.5% 0.0% 50%

DEBT MATURING

SAME PROPERTY OPERATING NEW-COMPARABLE RENT % FEMALE INDEPENDENT

IN 2022

EXPENSE RECOVERY RATIO SPREAD (TTM) TRUSTEES

(excl. principal amortization)

$0.25 9.0% 9.6% 24

BLENDED RENT

OPERATING FFO/SHARE DEBT MATURING AVERAGE YEARS OF

SPREADS (TTM)

THROUGH 2023 EXPERIENCE OF NAMED

(excl. principal amortization) EXECUTIVE OFFICERS

FOURTH QUARTER 2021 INVESTOR UPDATE 10Geographically 100% 100% 86%

Diversified with a OPEN-AIR CENTERS

(Based on annualized base rent “ABR”)

SUBURBAN MIX

(Based on ABR)

NATIONAL & REGIONAL TENANTS

(Based on ABR)

National Tenant

Focus and Suburban 70% 57

Orientation GROCERY/GROCER

COMPONENT ANCHORED

(Based on ABR)

# OF TOTAL MULTI-TENANT

RETAIL PROPERTIES

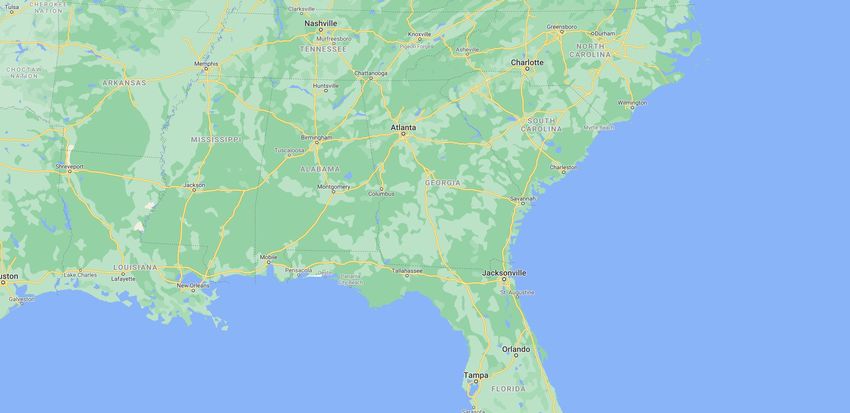

Boston

Milwaukee

Minneapolis

Detroit

Tri-State Area

Chicago

Columbus

Salt Lake Indianapolis

City Baltimore

Denver

St. Louis

Cincinnati

Charlotte

Nashville

Phoenix

Atlanta

Austin Jacksonville

Accelerated flight to the suburbs Orlando

fueled by COVID-19 positions

RPT’s portfolio for growth.

Tampa

Miami

Expand in existing markets

Expand in new markets

Not looking to expand

FOURTH QUARTER 2021 INVESTOR UPDATE 11Initial 2022 Outlook

At the midpoint of $1.03 per diluted share, 2022 operating FFO is projected to

increase by 8% at the midpoint and 11% at the high-end.

2022

Guidance1

$1.00 $1.05

Operating FFO per

diluted share

Selected Expectations

Same Property NOI Growth2 Acquisitions Dispositions

3.0% 5.0% +/- $125M +/- $100M

FOURTH QUARTER 2021 INVESTOR UPDATE 12ESG Progress and Recent Awards

Published our first Corporate Sustainability Report in December 2021

Improved GRESB score by 20% in 2021 versus our inaugural assessment in 2020

2021 Diversity & Inclusion Initiatives include: developing effective strategies to recruit and

attract a more diverse talent pool, providing unconscious bias training for all employees,

supporting community outreach efforts at targeted RPT centers, working with vendors and

subcontractors to further our diversity goals and partnering with third parties to help level the

playing field for underrepresented groups within the commercial real estate industry

Since 2018 RPT has significantly improved the Board of Trustees’ diversity of tenure, skills,

experience, gender and ethnicity through the addition of three new trustees

2022 Focus: Vendor Monitoring, Technical Building Assessments, Green Lease Execution,

and Building Certifications

8TH

YEAR IN

A ROW!

Obtained RPT’s first-time

investment grade credit rating Best Investment Transaction

Portfolio category for our joint venture with GIC

FOURTH QUARTER 2021 INVESTOR UPDATE 1302

The durability of our cashflows

has been greatly enhanced

over the past few years with a

strengthened and healthier

tenant base, increased grocer

exposure, and significant

improvements in both our

geographic mix and household

income.

• Rapid expansion in target markets

• Rising grocer exposure

Marked • Upgrading tenancy

Improvement In

Portfolio Quality

FOURTH QUARTER 2021 INVESTOR UPDATE 14Rapid Expansion into Target Markets

Boston moved from no exposure to our third largest market in 2021.

• Power of the Platform facilitates rapid growth in target Increasing Market Exposure

and expansion markets, while shrinking non-expansion

markets

• Target markets are university-adjacent, high-growth

markets with an outsized tech presence

• First time entrant into the Boston market, which is now

RPT’s #3 largest market; Atlanta jumped to #4 from #12

• Decreased our market exposure in Detroit, Cincinnati,

Boston Atlanta

and Chicago by 8.8%

0.0% to 7.4% 3.7% to 6.9%

Rank at MSA Exposure as MSA Exposure as

MSA Change

4Q21 of 12/31/2019 of 12/31/2021

1 Detroit 19.8% 16.1% (3.7%)

Tampa Nashville

5.7% to 6.8% 5.0% to 5.2%

2 Cincinnati 11.3% 10.0% (1.3%)

3 Boston 0.0% 7.4% 7.4% Decreasing Market Exposure

4 Atlanta 3.7% 6.9% 3.2% Chicago (3.8%)

5 Tampa 5.7% 6.8% 1.1% Detroit (3.7%)

Cincinnati (1.3%)

FOURTH QUARTER 2021 INVESTOR UPDATE 15Rising Grocer Exposure

Since 2019, RPT has made material improvements to its portfolio through proactive asset recycling and

through the Power of the Platforms created in 2019 and 2021 that enabled RPT to transform its portfolio

through the acquisition of $541 million of multi-tenant shopping centers in 2021.

Centers Anchored by Grocer or Grocer Component by ABR

72.0%

+5.7% 71.0%

71.0%

70.0% 69.5%

69.0%

68.0%

% of ABR

67.0%

66.0%

65.3%

65.0%

64.0%

63.0%

62.0%

4Q19 4Q21 4Q21 with SNO

FOURTH QUARTER 2021 INVESTOR UPDATE 16Upgrading Tenancy

We are replacing lower quality tenants with national grocers and retailers, upgrading the

credit profile and compressing the cap rates on our centers, while also enhancing the

customer experience.

Former Tenant New Tenant

Troy Marketplace AA/A1 Rated Grocer

Crofton Centre

Town & Country Crossing

Winchester Center

Highland Lakes AA/A1 Rated Grocer

Front Range Village

Woodbury Lakes

Providence Marketplace

Total NOI: $2.4M Total NOI: $4.5M

FOURTH QUARTER 2021 INVESTOR UPDATE 1703 RPT has significant organic

upside that is being fueled by

below market in-place rents and

occupancy upside. We are using

the opportunities that COVID-19

has presented to enhance the

value of our properties through

the strategic remerchandising

and re-tenanting of our portfolio.

• Accelerating signed not open backlog

• Embedded mark-to-market opportunity

• Enhancing value through leasing

Troy Marketplace

Town & Country Crossing

The Crossroads

Crofton Centre

Strong Internal • COVID-19 has highlighted the importance of

Growth Potential

bricks and mortar

• Our retailers are expanding

FOURTH QUARTER 2021 INVESTOR UPDATE 18Accelerating Leasing Backlog

Signed not opened ABR and estimated recovery income (gross rent) was $6.9 million as of

December 31, 2021, with another $3.3 million in advanced lease negotiation, totaling $0.11 of

annual incremental operating FFO per share by 2024.

Signed Not Commenced Backlog

Total

$5.0 $4.7

$4.5

Pro-rata share of gross rent (in millions)

$4.0 Total $1.7

$3.5

$3.5

$0.4

$3.0

$2.5 $0.05 Total

per share $2.0

$2.0

$0.04

$1.5 $3.1 per share

$3.0 $1.1

$0.02

$1.0

per share

$0.5 $0.9

$0.0

2022 2023 2024

Signed, not commenced - at 12/31/2021 In advanced negotiation

Tenants signed

over the past year AA/A1 Rated

Grocer

FOURTH QUARTER 2021 INVESTOR UPDATE 19Embedded • Fourth quarter 2021 TTM new leases-comparable re-

leasing spread of 32.5%

Mark-to-Market • Since the second quarter of 2018, new leases-

comparable re-leasing spreads have averaged 30%

Opportunity • New leases-comparable rent per square foot has

averaged about $18 since mid-2018 which is significantly

above the current portfolio average rent per square foot

RPT’s low in-place rents and of $15

decentralized leasing platform is • New leases signed since 2Q18 have an average

driving strong re-leasing spreads. embedded rent escalator of 1.8% and 1.7% on a trailing-

twelve-month basis

$20 $17

$16.31

30% average $18.07 $16 33% TTM new

New Comparable ABR per SF - TTM

$18 new re-leasing re-leasing

New Leases-Comparable ABR PSF1

spread $15 spread

$16

$14

$13.93 $13

$14

$12.31

$12

$12

$11

$10 $10

2Q18 - 4Q21 Average 4Q21 TTM

Prior Rent PSF New Rent PSF Prior Rent PSF New Rent PSF

FOURTH QUARTER 2021 INVESTOR UPDATE 20Key points:

Enhancing Value 1. Remerchandising projects consist of re-demising, expanding or

combining spaces similar to the 18 targeted remerchandising

Through Leasing opportunities that we completed in 2019 at high teens yields

2. COVID-19 has fueled renewed demand from grocers and RPT is

currently in various stages of negotiation on several new grocer deals

Active remerchandising and outlot

3. Grocery-anchored centers typically trade at cap rate premiums to

opportunities of $26 million are non-grocery-anchored centers and to power centers driving potential

expected to earn an attractive return NAV accretion

on capital in the low double-digit 4. COVID-19 has created opportunities to accretively remerchandise

range. our properties that did not exist pre-pandemic

Reducing Potential New Tenants

AA/A1

Rated Grocer

FOURTH QUARTER 2021 INVESTOR UPDATE 21Remerchandising

Troy Marketplace

Troy, MI

At our Troy Marketplace asset in the Detroit,

MI market (#14 MSA), COVID-19 impacts

allowed us to take back a recreation tenant

without a buyout, facilitating the signing of a

premier, first-to-state grocer with investment

grade credit at this non-grocery-anchored

credit center which should significantly

enhance the value of the entire property

while positioning the property for success for

years to come.

Value Creation

Favorable Cap Rate

Compression

230 bps

Est. Cap Rate Compression1

Unrated AA/A1

Credit Credit

Rating Rating

Strong Growth 4.6%

Profile 5-YR NOI CAGR

2022 -2027

Signed Grocer

FOURTH QUARTER 2021 INVESTOR UPDATE 22Remerchandising

Town & Country Crossing

We plan to re-demise, expand and Town & Country, MO

combine spaces to attract new types of

tenants at our Town & Country Crossing Old Tenant

center, in the St. Louis, MO market (#20

MSA). We have already signed a lease

with coveted national outdoor and sporting

retailer, REI, whose addition to the center

is expected to enhance the overall tenancy.

Value Creation

EXISTING SITE PLAN – TOWN & COUNTRY

Favorable Cap Rate

Compression

190 bps

Est. Cap Rate

Compression1

Strong Growth 4.5% Signed national outdoor

and sporting retailer

Profile 5-YR NOI CAGR

2022 -2027

PROPOSED SITE PLAN – TOWN & COUNTRY

FOURTH QUARTER 2021 INVESTOR UPDATE 23Remerchandising

The Crossroads

Royal Palm Beach, FL

The Crossroads, located in the Miami, FL

market (#7 MSA) is home to a high

performing Publix that has decided to invest

significant capital to upgrade and expand the

store. As a condition of completing this

project, we have signed Publix to a fresh 20-

year lease at a healthy spread. The new and

improved store is expected to attract even

more customers and should compress the

cap rate on the entire center.

PROPOSED SITE PLAN – PUBLIX

REBUILD & EXPANSION

Property & 3-Mile Market Statistics

Favorable Cap Rate 80 bps

Compression Est. Cap Rate

Compression1

Strong Growth 15.8%

Profile 5-YR NOI CAGR

2022 - 2027

FOURTH QUARTER 2021 INVESTOR UPDATE 24Upgrading Tenancy

Crofton Centre

We are replacing a non-credit rated Crofton, MD

and low sales grocer with investment

grade grocer Giant at Crofton Centre

in the Baltimore, MD market (#21

MSA). This deal brings a high-end

grocer into the center, with projected

weekly sales volume of $780K.

Value Creation

Favorable Cap Rate 200 bps

Compression Est. Cap Rate

Compression1

B+ BBB

Strong Growth 7.3% Credit

Rating

Credit

Rating

Profile 5-YR NOI CAGR

2022 - 2027

FOURTH QUARTER 2021 INVESTOR UPDATE 25COVID-19 has Highlighted the Importance of Bricks and Mortar1

BOPIS and curbside pickup now available at all

The year-over-year growth rate of online

stores and next day local delivery from store

grocery sales continued to accelerate in Q3,

now available at 70% of locations.5”

and pickup is now available from all

Whole Foods market stores.2” –#23 tenant

–#15 tenant

In addition, we leveraged our stores to drive fast

and convenient fulfillment of online orders. In Q2,

80% of GAP and Banana Republic revenue is we continued to see about 60% of our online

expected to be driven by off-mall locations revenue fulfilled by stores, including in-store or

by 2023.3” curbside pickup, ship from store, or Best Buy

employees who are delivering product to customers

–#9 tenant out of more than 450 of our stores6”

–#17 tenant

Our stores continue to be an operational strength

to Bed Bath & Beyond during the quarter. In Q1, During Q2, our stores enabled over 90% of our total

31% of our digital demand was fulfilled from sales, and we fulfilled more than 70% of our online sales,

stores, with BOPIS representing 14% and ship either through ship-from-store, in-store pickup or curbside.

Most importantly, we continue to drive significant

from store and the same-day delivery accounting

improvement in the profitability of our eCommerce

for 17%. Our footprint plays a vital role in our

channel, by leveraging fixed costs, sustaining athlete

digital-first, omni-always strategy.4” adoption of in-store pickup and curbside, as well as fewer

–#4 tenant and targeted promotions.7”

–#2 tenant

FOURTH QUARTER 2021 INVESTOR UPDATE 26Our Retailers Are Expanding1

600 new store openings and 1,250 store

Aldi has 450 planned openings. It has renovations planned in fiscal 20215”

2,052 stores and wants to get to 2,500 by

2022.2” –#16 tenant

–#48 tenant

Starbucks plans 850 new openings in 2021

Burlington has long-term plans to open and announced that it plans to add 22,000

1,000 stores, though it plans to reduce the stores to its portfolio by 2030, for a total of

average store’s footprint. It opened 38 55,000. This will include a mix of new store formats,

locations in fall 2020 and plans a total of 51 to including Drive-Thru, Starbucks Pickup and

54 stores in 2021.3” curbside pickup.6”

–#13 tenant

–#91 tenant

Old Navy and Athleta opened 25 and 13

stores, respectively, year-to-date, on a Looking ahead, we remain confident in our

path toward 30 to 40 openings at Old expansion plans and continue to see plenty of

Navy and 20 to 30 openings at opportunity to grow to at least 2,400 Ross Dress

Athleta.4” for Less and 600 dd's DISCOUNTS locations

over time.7”

–#9 tenant

–#8 tenant

FOURTH QUARTER 2021 INVESTOR UPDATE 2704

We are using our size to our

advantage by innovating and

responding quickly to a rapidly

shifting retail landscape. We have a

differentiated business model that

utilizes unique and strategic joint

ventures to capitalize on

dislocations across the retail real

estate landscape.

• Three differentiated, but complementary

external growth platforms

• Power of the platforms

Differentiated

Business Model

FOURTH QUARTER 2021 INVESTOR UPDATE 28Three Differentiated, but Complementary

External Growth Platforms

Three different investment strategies with tailored capital structures to drive scale and outsized growth.

R2G RGMZ

(Balance Sheet) (Existing GIC Joint Venture) (New Net Lease Platform)

RPT Ownership 100.0% 51.5% 6.4%1

Gross Assets $2.3 billion2 $577 million3 $228 million4

Property Type Grocery-anchored shopping

Multi-tenanted shopping centers Single-tenant assets

centers

Lease Type Average lease lengths with value- Average lease lengths with core-

Long-term net leases

creation opportunities stabilized characteristics

Tenancy Diversified, high-quality tenants

Resilient, investment grade quality

with balanced mix of anchor and Grocery-anchored in top MSAs

tenants

shop tenants

Leverage Profile

Targeting 5.5x-6.5x net debt-to- Targeting leverage of up to 50% Ability to operate at higher target

EBITDA on select assets leverage levels of 60-65%

Remaining capital

to be deployed N/A $1.1 billion $957.5 million

Incremental mgmt.

fee upside5 N/A $0.02 $0.03

FOURTH QUARTER 2021 INVESTOR UPDATE 29Power of the Platforms

Higher achievable economic spreads that will drive greater value creation per dollar deployed through

higher investment yields from arbitrage opportunities and earned management fees.

Strategic Benefits

1. Accelerates AUM Growth and Expansion Into Target Markets: Capital infusions from R2G and RGMZ

accelerate RPT’s expansion into target markets and increases assets under management that can create G&A

efficiencies over the long term

2. Unlocks Large Scale Portfolios: Ability to acquire larger portfolios of properties with different risk/return profiles

and allocate properties across multiple platforms

3. Unlocks Value Dislocations: Monetize value dislocations across retail real estate such as single versus multi-

tenant, essential versus non-essential and larger versus smaller deal sizes

4. Enhances FFO Growth Profile: Higher effective yields fueled by arbitrage opportunities and earned

management fees increases the economic returns and accretion from deployed capital

~50 bps

Management

Fees Enhanced

Effective Yield

= 250 bps

Up to

200 bps

Arbitrage1

FOURTH QUARTER 2021 INVESTOR UPDATE 3005

Our two joint ventures have

provided us with the capital to fuel

a material increase in our assets

under management, accelerate our

expansion into higher growth

markets and allow us to generate

higher economic returns on our

capital to enhance external growth.

• Punching above our weight class

• Striking with precision

• Optimizing capital allocation

• Asset Scoring Model

Enhanced • Power of the Platforms

External Growth • Recent acquisitions

Opportunities

FOURTH QUARTER 2021 INVESTOR UPDATE 31Punching Above Our Weight Class

In 2021, RPT was the most active retail investor in the U.S. by purchase volume,

surpassing large cap REITs, institutional owners, and private equity.

Top REIT, Investment Manager and Private Equity Retail Buyers in 2021

$600

$546 $545

$500 $465

Deal Volume ($ in millions)

$390

$400 $371 $363 $361

$340 $328

$298 $295

$300 $273

$229

$207 $200 $193 $192

$200

$100

$0

Source: JLL

FOURTH QUARTER 2021 INVESTOR UPDATE 32Striking With Precision

Grocery-anchored cap rates have fallen by 50-60bps in the past year and by

roughly 70bps for our $500 million of acquisitions1, driving value creation of

almost $60 million.

Major Market Grocery-Anchored Cap Rates 2021 Acquisitions

6.7%

~70bps

6.6%

6.5%

6.4% Estimated Cap Rate

Cap Rate

6.3% Compression Since

6.2% Acquisition

6.1%

6.0%

5.9%

5.8%

~$57M

Estimated

Value Creation

Source: Real Capital Analytics

FOURTH QUARTER 2021 INVESTOR UPDATE 33Optimizing

Capital

Allocation

Asset Score

RPT is modernizing its

approach towards capital

allocation by combining

advanced data analytics Optimized

with the deep and Tenant Score Capital Market Score

experienced leadership Allocation

across business units

Deep &

Experienced

Leadership

FOURTH QUARTER 2021 INVESTOR UPDATE 34Asset Scoring Model

RPT’s asset score incorporates advanced data analytics with our deep

institutional knowledge base to evaluate four key factors: Competitive Positioning,

Market Dynamics, Cash Flow Risk and Cash Flow Growth

Traditional Data Sources New Data Sources Institutional Knowledge

24 average years of

experience for senior

management

Demographics Market Rents Real-time Foot Retail

Traffic Spending

$13 billion of total

transactions volume

experience

Deep broker and market

Forecasted Growth Tenant Employers Climate Risk relationships

Quality

FOURTH QUARTER 2021 INVESTOR UPDATE 35RPT closed on its first arbitrage acquisition with the

Power of The

purchase of Northborough Crossing in the Boston, MA

market.

• Northborough Crossing is a 646K square foot premier open-air retail

Platforms

destination ideally situated between Boston’s MetroWest suburbs and the

thriving Worcester market amidst a highly-affluent area with an average

household income of $158K within a three-mile radius

• By parceling off select tenants and selling those net lease assets to

Northborough Crossing, Northborough, MA RGMZ, RPT is then able to retain the rest of the center at a lower cost,

increased retained cap rate, and with an enhanced growth profile while

earning management fees on the net lease assets

Signed TJX

$104M 94% Concepts

Contract Price Leased Rate

$158K 7%

Average HH Income 5-Year NOI CAGR

(3-mile) 2022 - 2027

FOURTH QUARTER 2021 INVESTOR UPDATE 36Power of The Platforms

Northborough Crossing, Northborough, MA

Parceling off select net lease assets at the center and selling them to RGMZ has

significant benefits for both RPT and the joint venture.

Benefits to RPT Benefits to RGMZ

Reduced cost basis Resilient and high-quality tenancy

Sold $65 million of parcels to RGMZ which would Access to essential and high credit quality tenants in an

significantly reduce RPT’s basis in the retained asset attractive market

Enhanced yields on retained asset Superior demographics

240-basis point spread between the going-in cap rate and $158K average 3-mile household income and 73% of

the retained cap rate after parcel sales population with an Associates Degree or higher within 3

Capitalize on property size discount miles

Enables RPT to purchase a large property that typically Enhanced returns from leverage

includes a size discount, due to reduced trading liquidity, Stable cash flow with strong tenancy allows for target

that we likely would have passed on without the potential leverage of 60-65%

parcel sales to RGMZ Proprietary deal flow

Access to Boston market Single-tenant carve-outs from a multi-tenant center not

Facilitates entry into the attractive Boston market available to traditional net lease players

Maintains management of the center Attractive pricing

RPT retains day-to-day responsibility for leasing and Value dislocations available by working with RPT allows

property management of the center as manager of the net both parties to attain better yields than buying individually

lease platform Location within premier shopping center

Benefits from traffic of multi-tenant open-air centers

FOURTH QUARTER 2021 INVESTOR UPDATE 37RECENT ACQUISITIONS

Boston Portfolio

Our newly acquired Boston portfolio has an expected 4% 5-Year NOI CAGR.

153,725 SF

97.4% Leased

2

Bedford Marketplace

Bedford, MA

510,154 SF

95.7% Leased

1

3

Dedham

Dedham, MA

4

645,785 SF 283,979 SF

94.1% Leased 86.6% Leased

Northborough Crossing Village Shoppes of Canton

Northborough, MA Canton, MA

FOURTH QUARTER 2021 INVESTOR UPDATE 39Southeast Portfolio

Our newly acquired Southeast portfolio has an expected 5% 5-Year NOI CAGR.

1 218,859 SF

SF 77,099 98.4% Leased

97.9% Leased

2 Woodstock Square

Atlanta, GA

Bellevue Place

Nashville, TN

3

104,431 SF

100.0% Leased

460,962 SF

91.4% Leased

East Lake Woodlands

Tampa, FL

Newnan Pavilion

Atlanta, GA

81,544 SF 163,476 SF

95.4% Leased 97.2% Leased

4

5

6

Highland Lakes Plaza South Pasadena Shopping Center

Tampa, FL Tampa, FL

FOURTH QUARTER 2021 INVESTOR UPDATE 4006

A flexible and proactive balance

sheet strategy allowed RPT to

weather the pandemic while

positioning the Company for

future growth opportunities.

• Strong liquidity and investment grade balance

sheet

• Flexible and opportunistic liability management

Flexible Balance

Sheet to Support

Growth Initiatives

FOURTH QUARTER 2021 INVESTOR UPDATE 41Strong Liquidity and Investment

Grade Balance Sheet1

We have about $240 million of net liquidity after debt repayments through 2023.

Total Total

$329 $329

$14M

Total Cash2

$315M

Unused Revolver

Capacity

$ in millions

Revolver Net

Capacity Liquidity

6.3x

$315 $240

Net Debt to Annualized

Adjusted EBITDA3

BBB- Debt

Repayments

2

'22-'23

4

Investment Grade

Cash $89

Credit Rating from Fitch

$14

Sources Uses

FOURTH QUARTER 2021 INVESTOR UPDATE 42Flexible and Opportunistic

Liability Management1

As of December 31, 2021

4.8% $250

All of 2023 maturities are expected to be refinanced in 2022

Debt Maturities excl. principal amortization (millions)

Floating Rate Debt

$200 $190

Only 9.6% of

debt maturing

34.0% $150 through 2023 $129 $130 15%

Debt Prepayable $100 $88 $852

Without Penalty $75 $70 $75 $70

$50

0.0% $0

$0

2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

$0

2032

Debt Maturing in 2022

(excl. principal amortization)

Secured Unsecured Bank Unsecured PP Revolver Target

FOURTH QUARTER 2021 INVESTOR UPDATE 43FOOTNOTES

Footnotes SLIDE 3 1) See footnotes for slide 6. 2) Represents guidance provided in our earnings release or earnings call, which was subject to the assumptions therein. We have not updated or reaffirmed that guidance or any of the of the supporting assumptions and are not doing so by restating it herein. Expected same property NOI growth excludes the net impact of reversals of prior period rental income not probable of collection that benefited 2021 same property NOI, including the Company’s share of unconsolidated joint ventures. SLIDE 6 1) Dividend yield is based on the most recently announced quarterly dividend annualized divided by the stock price as of February 14, 2022. 2) 2022 FFO per share growth reflects the midpoint of 2022 FFO per share consensus estimates sourced from S&P Cap IQ Pro on February 14, 2022, divided by 2021 FFO per share sourced from S&P Cap IQ Pro on February 14, 2022. 3) Price to 2022 FFO multiple reflects the stock price on February 14, 2022, divided by 2022 FFO per share consensus estimates sourced from S&P Cap IQ Pro on February 14, 2022. SLIDE 7 1) Dividend yield is based on RPT’s announced first quarter 2022 quarterly dividend rate of $0.13 annualized, divided by the stock price as of February 14, 2022. 2) 2022 FFO per share growth reflects consensus 2022 FFO per share estimates sourced from S&P Cap IQ Pro on February 14, 2022, divided by 2021 FFO per share sourced from S&P Cap IQ Pro on February 14, 2022. 3) Multiple expansion reflects the peer average price to FFO multiple of 15.3x multiplied by the midpoint of RPT’s 2022 OFFO per share guidance divided by the stock price on February 14, 2022, less RPT’s OFFO growth. Peer average includes: BRX, KIM, KRG, SITC, REG, PECO, FRT. SLIDE 9 1) Simple average of total assets including joint venture assets owned by BRX, RPAI, KRG, SITC, WRI, ROIC, FRT, KIM and REG as of December 31, 2020. 2) As of December 31, 2021, the Company’s multi-tenant property portfolio consisted of 57 multi-tenant shopping centers (including ten shopping centers owned through a joint venture). SLIDE 10 1) Balance sheet snapshot information reflects the consolidated portfolio and the Company’s pro-rata share of joint ventures, except for total cash. 2) Consolidated portfolio cash, cash equivalents, and restricted cash balance of $14 million as of December 31, 2021. SLIDE 11 1) As of December 31, 2021, the Company’s multi-tenant property portfolio consisted of 57 multi-tenant shopping centers (including ten shopping centers owned through a joint venture). FOURTH QUARTER 2021 INVESTOR UPDATE 45

Footnotes SLIDE 12 1) Represents guidance previously provided in our earnings release or earnings call, which was subject to the assumptions therein. We have not updated or reaffirmed that guidance or any of the of the supporting assumptions and are not doing so by restating it herein. The Company does not provide a reconciliation for non-GAAP estimates on a forward-looking basis where it is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing and/or amount of various items that would impact net income attributable to common stockholders per diluted share, which is the most directly comparable forward-looking GAAP financial measure. This includes, for example, acquisition costs and other non-core items that have not yet occurred, are out of the Company's control and/or cannot be reasonably predicted. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Forward-looking non- GAAP financial measures provided without the most directly comparable GAAP financial measures may vary materially from the corresponding GAAP financial measures. The Company’s 2022 guidance reflects management’s view of current and future market conditions, including current expectations with respect to rental rates, occupancy levels, acquisitions and dispositions and debt and equity financing activities. To the extent actual results differ from our current expectations, the Company’s results may differ materially from the guidance set forth above. 2) Expected same property NOI growth excludes the net impact of reversals of prior period rental income not probable of collection, including the Company’s share of unconsolidated joint ventures. SLIDE 20 1) Weighted average new leases-comparable base rent PSF and prior rent PSF from 2Q18 to 4Q21. SLIDE 22-25 1) Reflects difference between JLL cap rate assessment relative to cap rate calculated based on gross property book asset value and 2021 NOI. SLIDE 26 1) All information contained in this slide is based upon public information, RPT has not verified such information independently and makes no representation as to the accuracy of such information. 2) Source: Amazon 3Q20 earnings call. 3) Source: GAP 2020 Virtual Investor Meeting. 4) Source: Bed Bath & Beyond 1Q21 earnings call. 5) Source: At Home 4Q20 earnings call. 6) Source: Best Buy Q2 Fiscal Year 2022 earnings call. 7) Source: Dick’s Sporting Goods 2Q21 earnings call. FOURTH QUARTER 2021 INVESTOR UPDATE 46

Footnotes SLIDE 27 1) All information contained in this slide is based upon public information, RPT has not verified such information independently and makes no representation as to the accuracy of such information. 2) Source: CNBC. 3) Source: Globe St. 4) Source: GAP 2Q21 earnings call. 5) Source: Source: Dollar Tree 4Q20 press release. 6) Source: CNN. 7) Source: Ross Stores press release on October 11, 2021. SLIDE 29 1) Reflects RPT’s equity ownership only and does not contemplate RPT’s preferred investment. 2) Reflects total assets of $1.9 billion plus accumulated depreciation of $0.4 billion as reported on the Company’s Condensed Consolidated Balance Sheet as of December 31, 2021. 3) Reflects total assets of R2G of $561 million plus accumulated depreciation of $16 million as of December 31, 2021. 4) Reflects total assets of RGMZ of $227 million plus accumulated depreciation of $1.0 million as of December 31, 2021. 5) Expected incremental management fee upside per share if full amount of remaining capital is deployed. SLIDE 30 1) Arbitrage reflects the difference between the going in acquisition cap rate versus the retained cap rate after selling net lease parcels to the net lease platform. SLIDE 33 1) Acquisitions include Northborough Crossing, Village Shoppes of Canton, Bedford Marketplace, Dedham, South Pasadena Shopping Center, Bellevue Place, Eastlake Woodlands, Woodstock Square, and Newnan Pavilion. SLIDE 42 1) Information on this slide reflects the consolidated portfolio only except for Net Debt to Annualized Adjusted EBITDA. 2) Cash, cash equivalents, and restricted cash balance of $14 million as of December 31, 2021. 3) Adjusted for ABR and estimated recovery income from leases that have been signed but have not yet commenced and leases in advanced negotiation. 4) Includes principal amortization. Excludes $35.0 million balance on revolving credit facility due in 2023 as this facility has two six-month extensions available at the Company's option provided compliance with financial covenants is maintained. FOURTH QUARTER 2021 INVESTOR UPDATE 47

Footnotes SLIDE 43 1) Information on this slide reflects the consolidated portfolio plus RPT’s pro-rata share of joint ventures. 2) Assumes the exercise of two six-month extension options on RPT’s unsecured revolving line of credit. FOURTH QUARTER 2021 INVESTOR UPDATE 48

You can also read