Investment opportunities in the New Zealand Petfood industry - v1.02; February 2014 Part of the Food and Beverage Information Project ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investment opportunities in the New Zealand Petfood industry v1.02; February 2014 Part of the Food and Beverage Information Project www.foodandbeverage.govt.nz

Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

2

Objectives of Coriolis’ assignment

Petfood emerged as one of the six best “emerging growth opportunity” sectors of the New Zealand food & beverage industry in previous research

§ All 559 food-related HS trade codes were screened and ranked using qualitative and qualitative methods

§ Petfood was achieving strong export volume and value growth

§ Petfood had strong comparative advantage and clear links into existing New Zealand strengths

§ See related document (http://www.med.govt.nz/sectors-industries/food-beverage/pdf-docs-library/information-project/coriolis-report-investors-guide.pdf)

Coriolis was asked to develop the case for further investment in the New Zealand petfood industry

§ Make the case for further investment in the industry

§ Targeting investors, both domestic and international

§ Provide a potential investor with a preliminary overview of the industry

§ Including the facts and analysis required to “come up to speed” on the industry and the opportunity

Project incorporates extensive, recent independent research

§ Interviews with all multinational industry participants and most key domestic firms

§ Extensive quantitative analysis of all available data sources on the industry

§ Surveys, benchmarks from other countries, commercial research and Coriolis expertise

3

The New Zealand petfood industry presents investors with a strong potential opportunity for growth

Key Takeaways

§ Petfood is an attractive market with strong fundamentals

– Petfood is a growing global market

– Petfood is strongly on trend with changing global consumer behaviour

– Petfood is a profitable industry, particularly in the growing super-premium (cat and dog) sector

– Petfood is attracting investment from both global multinational companies and private equity

§ New Zealand has a vibrant petfood industry with strong comparative advantage

– New Zealand has a strong supply of safe raw materials, some of which are unique, and there is a strong and

competitive Petfood ingredients sector

– New Zealand has a vibrant retail Petfood industry of both global leaders and innovative local firms driving industry

growth

§ There are clear opportunities for growth in both products and markets

– Continued marketing, innovation and new product development leveraging strengths in safe, fresh, free-range meat

– Continued market development to build position in both existing and emerging new markets

4

New Zealand has the opportunity to be part of the growing global demand for petfood, taking advantage of

its strong reputation as a safe, free range supplier of unique meat based ingredients and brands

Global Demand New Zealand’s disease free status allows preferential access into key markets.

Demand for petfood is growing globally. The increasing number of pet-owners are treating their

pets as part of the family, demanding better quality and spending more on their companions. The second export area is in value added retail ready petfood products. Two distinct exporting

Trends in petfood are strongly mirroring trends in human food. groups are in New Zealand; MNC’s and medium sized New Zealand based firms. Mars, for

example, is a significant exporter of pouched cat food to Australia. Many medium sized firms

Key markets for petfood are richer Western markets with high pet penetration and numbers, in also exist in New Zealand, some are already exporting petfood globally while others are looking

particular USA, Australia and Western Europe. But strong growth, and a higher dollar per kilo, is to export super-premium meat based products to new markets through specialty channels and

occurring in key Asian markets and South America where small dogs in particular are treated invest in extrusion based cooking of dry pellets.

with premium dog foods and treats.

New Zealand firms have successfully innovated in this space, both in product and processes.

Dry foods dominate the petfood market, seen as more convenient and logistically easier. Large Firms are required to overcome the real challenges involved in exporting meat based products.

multinational corporations (MNC’s) such as Nestle and Mars take the lion share of this market. To assist in this, technology has focussed on packaging and producing petfood and treats in

Their large factories are located close to major markets (USA, Europe) or in developing rolls, frozen, freeze-dried and air dried states.

countries, such as Thailand.

Challenges also exist around supply. As meat processors become more efficient at maximising

New Zealand use and value of the carcass, less waste is produced. New human consumption markets (e.g.

New Zealand is traditionally a primary based exporting economy, specialising in: dairy, meat, China) have been found for offal and by-products traditionally used for petfood. Reducing stock

fruit, and food and beverages. Food and beverage products make up 56% of all exports. Petfood numbers of both sheep and deer also add supply pressure. Companies must develop strong

comprises 1.4% of this, reflecting New Zealand’s low penetration in the global market and supply relationships and consider vertical integration or investment along the supply chain.

almost no presence in the dry category (Tux baked biscuits have a large share in New Zealand

but are not exported and Addiction dry kibble is produced solely for the export market). Opportunities

Opportunities exist throughout the supply chain for investment to increase the quality of

However, New Zealand’s comparative advantage in meat and protein is driving growth in its ingredients and to highlight and target key high value customers and markets. In retail ready

petfood industry, particularly due to the availability and reliability of meat based ingredients (in petfood products, multiple opportunities exist in the super premium categories of cat and dog

particular lamb and beef) and innovation around retail ready products. food and treats. For medium sized companies, the biggest opportunity is in finding in-market

partners to enhance sales and distribution. To attract additional investment, New Zealand must

promote its unique species, good reputation, disease free status as well as its Asian positioning,

Petfood exports can be separated into two main areas, the first being ingredients consisting of

with its close proximity and free trade agreements providing access into these key markets.

either frozen MDM (mechanically deboned meat) or MBM (meat and bone meal). Ingredients

are exported to large multinational corporations who then manufacture the finished retail ready

petfood. Our advantage in this space is in having unique species such as lamb and deer.

Advantages are also in having high food safety standards/regulations and free range stock.

5

Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

6There are a large number of pets around the globe; companion pets such as dogs and cats are in over a third

of households in many markets

Total number of cats and dogs Households owning a cat Households owning a dog

Animals; millions; 2013e % of households; 2013e % of households; 2013e

New Zealand 47% USA 37%

USA 74 72

Canada 38% Canada 35%

China 11 28

USA 32% Australia 34%

Japan 10 12

United Kingdom 26% New Zealand 30%

United Kingdom 99

Australia 22% United Kingdom 18%

Germany 8 5

Germany 17% Japan 17%

Canada 95

Japan 10% Germany 14%

Australia 23

Hong Kong 4% South Korea 14%

3

South Korea 0.3 Cats Dogs China 2% Hong Kong 7%

New Zealand 1 1 South Korea 2% China 7%

Source: Euromonitor; Coriolis analysis & classification 7Petfood supports a wide range of prices, from discount store brands to super-premium products

EXAMPLE: Retail shelf price per kilogram of select dog food products in the United States

US$/kg.; actual; 1/2014

$45.74

$33.05

$12.12

$7.91 $8.33

$4.85 $5.58

$3.14

$2.12

$0.88

Ol' Roy bag Pedigree Ol' Roy can Eukanuba Nutro Hills Iams Woof Vital Missing SmartBones

Prescription

Diet

Source: Wal-Mart online; PetSmart online; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 8Pet owners globally spent a total of $92 billion on pet care in 2012; almost three quarters ($67b) was on dog

and cat food; petfood is a large category globally

Global Petcare retail sales Global retail sales: Cat and dog food vs. select categories

US$b; 2012 US$b; 2012

Cheese $130

Oils and fats $117

Bottled water - off

Dog Food $101

trade

$41

45%

Pet Products Cat and dog food $67

$20

22% Cat & Dog

Total $67b

Baby food $52

$92 billion 73%

Other Food Noodles $46

$5

5%

Cat Food Baby milk formula $36

$26

28%

Breakfast cereal $32

Snack bars $12

Source: Euromonitor; Coriolis analysis & classification 9Retail cat and dog food sales are growing at a compound annual growth rate (CAGR) of 4% and global trade is growing at

10%

Global cat and dog food retail sales Global cat and dog food export trade

US$b; 2008-2013e US$b; 2002-2012

CAGR

(08-13)

4% $10.42

$69.0 $9.93

CAGR

$64.9 $65.3 (02-12)

10% $8.78

$60.0

$8.52 $8.34

$56.7 $57.2

$7.27

$6.23

$5.63

$5.23

$4.60

$3.86

2008 2009 2010 2011 2012 2013 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: Euromonitor; UN Comtrade; Coriolis analysis & classification 10Global retail cat & dog food exports were more than $10b in 2012; Europe is strong in the trade, followed by

North America and Asia

Global export value share of retail cat & dog food (HS230910) by country/region Top 25 petfood exporting countries

US$m; FOB; 2012 US$m; FOB; 2012

UK

France $1,473

$359

Denmark 3% Belgium USA $1,312

Hungary $231 Switz.

$443 Italy

$425 2% 4% $267Spain Austria $155 Germany $979

4% 3% $218 $212 1%Lithuania Netherlands $882

2% 2% $145

Germany 1% China $835

$979

Thailand $828

9%

Belgium $443

Other Europe Hungary $425

Europe 62% $762

United Kingdom $359

7%

Netherlands Canada $323

$882 Italy $267

8% Australia $187 2%

New Zealand Denmark $231

Total Australasia 2% $62

$10,424m Poland $224

S. America $289 3% 1%

Other Spain $218

$92

Austria $212

1%

E/SE Asia 16% Australia $187

Thailand

France $828 Czech Rep. $157

$1,473 North America 15% 8% Switzerland $155

14%

Other E/SE Asia Lithuania $145

$66

1% Ireland $139

China Argentina $123

Canada $835

$323 Sweden $91

8%

3% USA

$1,312 Russian Federation $74

12% New Zealand $62

Mexico $28

Note: Denmark, Italy & Austria uses 2011 data as 2012 not yet filed with UN; Source: UN Comtrade database (custom job); Coriolis classifications and analysis 11Global retail cat & dog food exports have been growing at a 10% CAGR over the past decade; exports still

dominated by the European countries

Global export value of retail cat & dog food (HS230910) by sending country/region

US$m; FOB; 2002-2012

10y Absolute 10y CAGR

$10,424 Growth (02-12)

$9,931

$10,000 China +$828 61%

E/SE Asia +$43 11%

10y CAGR Thailand +$592 13%

(02-12) $8,783

$8,519 Other +$77 20%

10% $8,344 S. Amer. +$125 15%

New Zealand +$28 +6%

Australia -$17 -1%

$8,000

Other Europe +$615 18%

$7,267 Lithuania +$73 7%

Switzerland +$75 7%

Austria +$116 8%

Spain +$144 11%

$6,233 Italy +$205 16%

Belgium +$362 19%

$6,000 $5,635

UK +$226 10%

$5,233 Denmark +$57 3%

Hungary +$316 15%

$4,600

Germany +$631 11%

$3,857

$4,000

Netherlands +$497 9%

France +$785 8%

$2,000

Canada +$175 8%

USA +$613 7%

$-

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Note: Denmark, Italy & Austria uses 2011 data as 2012 not yet filed with UN; Source: UN Comtrade database (custom job); Coriolis classifications and analysis 12Petfood is a robust global market with both large multinationals and a strong long tail of regional leaders and

specialist or niche players

Global petcare sales by key manufacturer and other Top 25 petcare firms by sales

US$b; 2011 US$b; 2011

Mars $16.2

Nestle $10.4

Colgate $2.2

P&G $1.8

Del Monte $1.8

Heristo $0.6

Other $12.8 25% Agrolimen $0.5

Nutriara Alimentos $0.5

Mars $16.2 31%

Unicharm $0.4

Total Alimentos $0.4

Blue Buffalo $0.4

American Nutrition $0.4

Total = US

Mogiana Alimentos $0.3

$50b

Next 15 $3.8 7% Partners in Pet Food $0.3

V.I.P. Petfoods $0.3

Natural Balance $0.3

Total $0.4 1% Arovit Petfood $0.3

Unicharm $0.4 1% Ainsworth Pet $0.3

Del Monte $1.8 4%

Nutriara Alimentos

$0.5 1% P&G $1.8 4% Nestle $10.4 20% Dibaq Mascotas $0.2

Colgate $2.2 4% WellPet $0.2

Agrolimen $0.5 1%

Vitakraft-Werke $0.2

Heristo $0.6 1%

Nippon Pet $0.2

Maruha Nichiro $0.2

Top 2 = 51%

Top 5 = 63% Sunshine Mills $0.2

Top 25 = 75% Marukan $0.2

Source: Pet Food Industry magazine; Coriolis analysis and estimates 13Manufacturing and marketing petfood is a highly profitable enterprise

EXAMPLE: Operating profit of Nestle pet care division EXAMPLE: Operating profit % of sales: Nestle divisions & select NZ

%; CHF; FY2012 %; CHF or NZ$; FY2012

21% 20%

Beverages 22%

17% Pet Care 20%

16%

15% 16%

15% Infant formula 18%

15% 15% 14%

13% Nestle Confectionery 17%

Operating

divisions

Dairy 15%

Prepared foods 14%

Water 9%

Fonterra 5%

Silver Fern Farms-2%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: various Nestle annual reports; Fonterra and Silver Fern Farms annual reports; Coriolis analysis 14The industry is attracting investment from large global FMCG/CPG firms

Presence in Petfood by large FMCG/CPG multinationals

1935-2013

Year

entering Method of

Firm Petfood entry Key acquisitions Key brands

Mars 1935 Organic - Kal Kan Foods (1968) Cesar, Greenies, Nutro, Pedigree, Royal Canin, Sheba, Whiskas, KiteKat,

- Royal Canin (2001) Chappi, Catsan, Goodlife Recipe

- Nutro (2007)

1998 Acquisition - Carnation (1985) Purina, Purina One, Alpo, Beneful, Busy Bone, Chew-rific, Deli-Cat, Dog

- Spillers Petfood (1998) Chow, Fancy Feast, Friskies, Gourmet Gold, Mon Petit, HiPro, Kibbles and

- Ralston-Purina (2002) Chunks, Kit ‘N Kaboodle, Mighty Dog, Pro Plan, TBonz, Purina Veterinary

- Waggin’ Train (2010) Diets, Whisker Lickin's

Colgate 1976 Acquisition - Hill’s Pet Products (1976) Hill's Science Diet, Hill's Prescription Diet, Hill's Science Plan

P&G 1999 Acquisition - Iams (1999) Eukanuba, Iams, Evo,

- Natura Pet Products (2011)

Del-Monte 2002 Acquisition - Heinz’s North America Petfood (2002) Meow Mix, Kibbles n' Bits, 9Lives, Milk-Bone, Pup-Peroni, Pounce, Gravy

- Meow Mix Holdings (2006) Train, Jerky Treats, Canine Carry Outs, Snausages, Nature's Recipe (Cat

- Kraft’s Petfood brands (2006) and Dog), Meaty Bone

- Natural Balance Petfoods (2013)

Unicharm 1986 Organic - Hartz Mountain Corp (2012) Aiken Genki, Neko Genki, Gaines

Source: various published articles; various company annual reports; Coriolis analysis 15The industry has also proven attractive to private equity which is attracted by its stable cash flow and strong

profitability

Major global private equity investment in the Petfood sector – current or recently exited

2007-2013

Firm Target Year Activity Detail

KKR Del-Monte 2007 - Acquisition Acquired producer and distributor of premium branded pet and consumer food

products for the USA market

KKR Pets at Home 2010 - Acquisition Leading UK based specialty retailer of Petfood and accessories and services

Berwind Corp. WellPet LLC 2008 - Acquired Sold by Catterton $400m

In 2012 unveil a $20m dog food processing plant expansion increasing capacity to

80,000 tons pa

Pegasus Capital Halo Purely for Pets pre 2008 - Majority ownership Part owned by Ellen DeGeneres 2008

Advisors

Catterton Partners M.I. Industries/ Nature's - - Investment Premium petfood, kibble, raw an canned, gluten free and grain free

Variety

VMG Partners Natural Balance Petfoods 2013 - Merged with Del- Founded in 1989 by actor Dick Van Patten and company. The company, based in the

Monte Southern California makes super-premium Petfood for dogs and cats.

Aim to expand Del Monte's presence in fast-growing pet specialty channel

VMG Partners Waggin’ Train 2010 - Sold to Nestle Real-meat dog treats business

Advent International Provimi Petfood (PPF) 2011 - Acquisition The third largest producer of private label wet and dry Petfood in Europe, from the

Provimi Group for an enterprise value of €188 million.

Motion Equity Partners Acraplanet (Italy) 2010 - Acquisition Purchased petfood and accessory business for €46m

Retail operation with 50 pet stores

Archer Capital Growth Best Friends Pet Supercentre 2012 - Investment Investment to support expansion plans

Funds

Quadrant Private Equity City Farmers (AU) 2013 - Majority stake Majority stake in petfood retailer for A$93m. Support the expansion of the 31 large

format stores nationwide

Source: various published articles; various company annual reports; Coriolis analysis 16Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

17New Zealand exports four classes of petfood product; some unmeasured amount of meat and offal exports

will also end up in Petfood

Simplified petfood industry supply chain

Model; 2013

Primary ingredients Petfood ingredients Retail-ready Petfood

processors processors manufacturers Markets

Grains Retail-ready Domestic market

4

Product form

- Canned

Vegetables

- Refrigerated

- Frozen

- Air dried

Other ingredients - Freeze dried

- Baked biscuits Export markets

- Kibble, extruded

Packaging

2&3

Meat, organs, offal,

? bones, blood & by- Further-processed

products meat-based ingredients

- Rendered MBM*

- MDM**

Seafood & by-products

1

*MBM – Meat and bone meal **MDM – mechanically deboned meat; Source: Coriolis 18New Zealand petfood exports – both ingredients & retail ready products – are showing strong growth

New Zealand export value of select animal feed codes

US$m; FOB; 2000-2012

$260.1 Absolute 12y CAGR

(00-12) (00-12)

$230.6 Retail Cat and

12y CAGR $221.0 $61.5 dog food +$47m 12.6%

(00-12) $212.5 $216.2 (HS230910)

9%

$49.4 4

$41.4 $46.1 $56.5

Mechanically

Deboned Meat

$64.6 (MDM) +$42m 9.2%

$153.0

$146.9 $60.4 (HS051199)

$135.2 $53.1 $49.3

$129.8 $35.9 $52.5 3

$38.0

$111.5 $113.5 $28.3

$100.8 $37.8

$92.5 $33.2 $36.9

$33.5 $36.1 Meat & Bone Meal

$25.8 $33.5 +$66m 9.5%

$14.8 $99.2 (MBM)

$31.1 $95.7 $91.4

$92.5 $80.3 (HS230110)

$22.5 $19.2 $27.2 $24.2

2

$50.6 $49.8 $58.2

$33.3 $34.2 $31.2 $35.3 $43.6

Seafood Meal

$31.8 $29.4 $34.8

$21.9 $21.6 $19.6 $20.8 $22.2 $23.5 $22.0 $25.5 $25.2 (HS230120) +$13m 3.9%

$17.3

1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Note: HS trade codes; Source: UN Comtrade database (custom job); Coriolis classifications and analysis 19All classes of petfood exports showing long term value per unit ($/kg) growth; retail has been major

standout performer

New Zealand export dollar per kilo of select animal feed codes

US$/kilo; FOB; 2000-2012

3y CAGR 12y CAGR

(09-12) (00-12)

$3.00 Retail Cat and 28.9% 10.3%

dog food

4

$2.50

$2.00

Seafood Meal 9.5% 3.7%

1

$1.50

Deboned Meat 3.4% 6.8%

$1.00 3

$0.50

Meat Meal -15.4% 4.7%

2

$-

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: UN Comtrade database (custom job); Coriolis classifications and analysis 20New Zealand’s total petfood exports of $260m – both ingredients and retail-ready – went to a wide range of

export destinations

New Zealand pet/animal feed export value by destination region New Zealand pet/animal feed export value by country

US$m; reported FOB; 2012 US$m; reported FOB; 2012

Other E/SE Asia

USA $75

Includes all four $5

product types on 2% Indonesia $47

pages prior

Australia $45

Thailand

$4 China $20

2% Japan $14

Indonesia Taiwan $10

$47 USA

18% $75 S. Korea $8

29% Canada $7

North America Netherlands $5

$83 Thailand $4

S. Korea E/SE Asia

$8 $108 Germany $4

3% Total

Taiwan Papua New Guinea $2.2

$260m

$10

Fiji $2.0

4%

Canada France $1.6

China Europe $7

$20 $16 Philippines $1.5

3%

8% Other Germany

$3 Australasia Netherlands Belgium $1.4

$4

$51 $5

1% Hong Kong SAR $1.2

Japan 2%

$14 France $2 1% United Kingdom $1.2

5%Pacific Islands

$6 Australia Other Europe Italy $1.1 HS Codes

2% $45 $6 2% 051199

Malaysia $1.0 230110

17%

230120

Singapore $0.9

230910

Source: UN Comtrade database (custom job); Coriolis classifications and analysis 21New Zealand exports petfood ingredients (including some animal feed) to a wide range of countries;

destinations that are primarily for use in poultry and aquaculture feed earn a lower dollar per kilo

New Zealand export MDM (HS051199) by market New Zealand export rendered meat meal (HS230110) by market

US$m; FOB; 2012 US$m; FOB; 2012

$/kilo $/kilo

USA $40.0 $1.05 $0.26

Indonesia $42.9

Australia $4.7 $1.65 USA $28.8 $1.16

“All of the MDM going to the

USA is going into Petfood,

it’s the meat component. Its

Indonesia $3.3 $0.86 China $5.1

going to the large Petfood “The rendered meat going $0.66

companies.” CEO, Meat to Indonesia is going into

Processing Company, 2013 pig and poultry feed. Most

Canada $3.0 $1.32 Canada $3.2 other countries are pet

food.” CEO, Rendering $0.96

Company, 2013

Netherlands $2.5 $0.97 Thailand $2.6 $0.71

Belgium $1.3 $2.68 Other Asia $2.4

$0.72

Thailand $1.3 $1.48 Netheralnds $2.4

$1.04

China $1.2 $0.82 Germany $2.0

$1.18

Italy $0.9 PNG $1.9

$3.57 $0.58

UK $0.7 Fiji $1.9

$16.18 $0.58

Source: UN Comtrade database (custom job); Coriolis classifications, analysis, interviews 22Total NZ retail-ready industry turnover of $375m, of which $234m domestically produced; 32% of domestic

production is exported; domestic industry developing, but supermarkets still 80% of market

New Zealand total retail ready petfood market New Zealand petfood wholesale value by channel

NZ$m; export FOB; domestic and import wholesale; 2012e NZ$m; 2012e

Total Domestic Production 62% NZ$234m

32%

Domestic

production

$158 42%

Pet stores $24

8%

Total Domestic

Market

Total = Total = Rural retailers

Exports $76 NZ$300m Supermarket

NZ$375m NZ$300m $16 6%

20% $241 80%

Vet $10 3%

WHS $6 2%

Imports $141 Other $3 1%

38%

Source: Coriolis estimates 23Both the New Zealand domestic petfood market and exports are showing strong growth; many in double

digits

Five year New Zealand petfood market growth rates (CAGR): by domestic channel and by export market product

%; CAGR; last 5 years

Domestic

by channel Pet superstore 17%

Grocery 7%

Pet shops 6%

Vet clinics 6%

Other 12%

Exports Retail C&D 11%

by product

MDM 12%

MBM 11%

Seafood meal 10%

Source: UN Comtrade database; Euromonitor; Coriolis analysis and estimates 24Two-thirds of New Zealand’s retail cat/dog petfood exports by value go to Australia (primarily Mars); only

the US and Japan also took more than US$5m worth of product in 2012

NZ exports of retail cat & dog food (HS230910) by country/region Top 25 export destinations for NZ retail cat & dog food

US$m; FOB; 2012 US$m; 2012

Australia $39.4

USA $6.7

Japan $6.2

Australia

$39.4 Taiwan $2.3

64% Canada $1.0

Hong Kong SAR $0.9

Germany $0.9

Rep. of Korea $0.6

Aus/Pacific 65% Cook Isds $0.3

Netherlands $0.3

Denmark $0.3

Turkey $0.2

Total Finland $0.2

$61.5m Other 1% Pacific Islands $0.5 1%

Other $0.3 1% United Arab Emirates $0.2

Sweden $0.2

E/SE Asia 18% United Kingdom $0.1

Japan $6.2 10% India $0.1

Europe 4%

North America 12% Italy $0.1

Fiji $0.1

China $0.1

Other Europe Taiwan $2.3 4%

Samoa $0.1

$1.4

Canada Other E/SE Asia $2.8 4% Belgium $0.04

2%

$1.0 USA

Germany 2% $6.7 Russian Federation $0.04

$0.9 11% French Polynesia $0.03

1%

Kuwait $0.02

Note: Global imports do not match global exports (for a range of understood reasons); Some countries use 2011 data as 2012 not yet filed with UN; Source: UN Comtrade database (custom job);

Coriolis analysis 25New Zealand’s existing export markets can be grown significantly; targeting the high growth, high value

markets

New Zealand’s top destinations for retail-ready petfood (HS230910)

US$; CIF; %; 2012

NZ import NZ share of

value in receiving

Total Petfood 10yr Import Share of receiving countries NZ’s $/kilo by Total $/kilo by Overall

Imports CAGR global country import value receiving receiving attractiveness

Country ($m) (%) imports (%) ($m) (%) country country

Australia $195 15% 2% $35.9 18% $2.92 $2.49 !"

Japan $831 3% 9% $6.4 1% $2.23 $2.76 !"

USA $736 17% 8% $3.7While New Zealand currently has a strong presence in Australia it has a wide range of growth opportunities

in other major markets

Top 25 retail cat & dog markets by imports 10y CAGR of import value NZ share of import value by country

US$m; CIF; 2012 % on US$; 2002-2012 US$m; CIF; 2012

Germany $857 Germany 5% Germany 0.1%

Japan $831 Japan 3% Japan 0.8%

United Kingdom $785 United Kingdom 8% United Kingdom 0.0%

USA $736 USA 17% USA 0.5%

Italy $603 Italy 11% Italy 0.0%

Canada $580 Canada 9% Canada 0.2%

France $515 France 12% France 0.0%

Belgium $469 Belgium 6% Belgium 0.0%

Netherlands $353 Netherlands 10% Netherlands 0.1%

Austria $259 Austria 12% Austria 0.0%

Spain $229 Spain 8% Spain 0.0%

Russian Federation $222 Russian Federation 26% Russia 0.0%

Australia $195 Australia 15% Australia 18.4%

Sweden $182 Sweden 9% Sweden 0.1%

Switzerland $178 Switzerland 5% Switzerland 0.1%

Poland $158 Poland 20% Poland 0.0%

Czech Rep. $156 Czech Rep. 21% Czech Rep. 0.0%

Portugal $152 Portugal 9% Portugal 0.0%

Denmark $140 Denmark 6% Denmark 0.2%

Rep. of Korea $113 Rep. of Korea 12% Rep. of Korea 0.8%

Note: Global imports do not match global exports (for a range of understood reasons); Some countries use 2011 data as 2012 not yet filed with UN; Source: UN Comtrade database (custom job);

Coriolis analysis 27Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

28New Zealand has a modern, robust, well-developed petfood value chain

Simplified model of key players in the New Zealand petfood value chain

Model; 2013

Beef, lamb & venison processors

Specialist petfood abattoirs

Nick's Petfoods Petfood manufacturers

Fordes Petfood

Down Cow Others…

Poultry Specialist renderers

Export

Markets

Others…

Pork

Seafood

Local

Market

Vegetable processors

Grain traders

Source: interviews; Coriolis analysis 29New Zealand meat & seafood production growing long term and country is not intensively farmed, indicating

significant spare capacity to produce more meat

Total New Zealand meat and seafood production volume Meat production in tons per square kilometre: NZ vs. peers

Metric tons; millions; 1961-2011 Metric tons/square kilometre; 2011

Wild Capture

Aquaculture

2.0 Other

Venison Singapore 166

Pork

Chicken

Lamb & mutton

Beef

1.5

Netherlands 79

1.0 Denmark 48

0.5 Ireland 14

New Zealand 5

-

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Note: 2011 is latest data available from United Nations; Source: UN FAO AgStat database; UN FAO FishStat database; CIA World Fact Book; Coriolis classification and analysis 30New Zealand is a major meat exporter and has significant global trade share across a number of meats

New Zealand share of global export value by meat product Situation/drivers

% of US$; 2011

New Zealand and Australia combined command

almost two thirds of the global lamb trade

35% – NZ is the largest lamb exporter in the world

– NZ has a large industry with ample supply

– NZ has a wide range of processors

– If petfood suppliers are using lamb, it is

coming from the Australasia region

New Zealand pioneered deer farming and in the

global leader in farmed venison production

– Venison is sustainably produced

19% – Animals are processed similarly to beef and

lamb (not wild caught by hunters)

17%

Meat “not elsewhere specified” is a catch-all code for

meats undefined when the trade codes were set up

New Zealand exports under this code include possum

(sometimes described on packaging as brushtail);

5% while possum are protected in Australia, they are

3% culled in New Zealand as an introduced pest

1% – NZ is effectively the only global supplier of

this meat

Sheep & lamb Deer & all other Meat "not Boneless beef Prepared beef Goat New Zealand has a large rabbit population that has

game elsewhere the potential to enter the meat supply chain in

secified" quantity

Source: UN FAO AgStat database; Coriolis analysis 31While New Zealand has a secondary position overall in the beef trade, it is strong in “manufacturing beef,”

partially as a offshoot of the growth of the New Zealand dairy industry

Number of dairy cows in New Zealand EXAMPLE: New Zealand share of US frozen boneless beef imports

Head; million; 81/82-10/11 % of US$ value; 1996-2012

5.0

22%

4.5 21% 21% 21%

29y 20%

19% 19%

4.0 CAGR 18%

18% 18%

2.8% 18% 18%

17% 17%

3.5

16% 16%

15%

3.0

2.5

2.0

1.5

1.0

0.5

-

1981/82

1983/84

1985/86

1987/88

1989/90

1991/92

1993/94

1995/96

1997/98

1999/00

2001/02

2003/04

2005/06

2007/08

2009/10

1996

1997

1998

1999

2000

2011

2012

2004

2008

2006

2009

2001

2010

2002

2007

2005

2003

Source: DairyNZ New Zealand Dairy Statistics 2010-11; UN FAO AgStat database; UN Comtrade database; MAF/MPI; Coriolis analysis 32New Zealand has a robust meat industry with a wide range of firms participating; no single supplier

dominates any key species

New Zealand meat slaughter and primary processing share: beef and sheep meat

% of volume; 2012 or as available

Beef & veal Sheep & lamb

Wilson Hellaby

2%

Lean Meats

Alliance

Taylor 3%

9%

Greenlea Preston

8% 5%

AFFCO Wilson Alliance

29% Ovation

17% Hellaby 7%

7%

UBP

5% Other

Taylor Preston

10%

3%

Lean Meats

0%

ANZCO Other

20% 1% AFFCO

12%

SFF

SFF 23%

ANZCO

30%

9%

Source: New Zealand Meat Board; Coriolis analysis 33Livestock and meat processing plants are spread across the country with no single region dominating any

key species

Share of total livestock numbers by region Location of all export certified beef and sheep plants in NZ

As of 30 June 2012 2013

1%

1% 0%

1% 1%

8% 6% Northland

7% 2% Auckland

2% 12% 14%

15% 8% 3%

27%

9%

21%

5% 52% Waikato/B.O.P.

25%

0%

8%

3% 28%

20%

17%

7% Hawke's Bay/Gisb.

4% 57%

7% Tara./Mana./Wel.

3% Tasman/Marl./W.C.

16%

37% 11% Canterbury

31%

14% 12% Otago/Southland

4%

Cattle Sheep Deer Pigs Goats

Source: Statistics New Zealand; Beef + Lamb New Zealand (http://www.beeflambnz.com/Documents/Market/Meat%20processors%20in%20New%20Zealand%20map.pdf ); Coriolis

analysis 34Like livestock, petfood manufacturers are spread across the country; many regions appear to have “spare

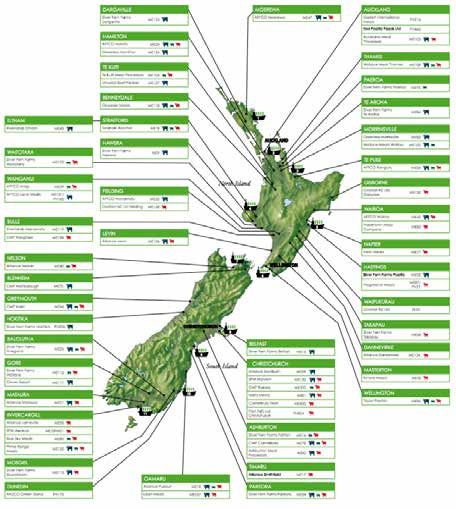

capacity” for more processors

Location of key retail pet food manufacturing firms in New Zealand

2014

Data and interviews give

strong indications of spare

capacity in the Waikato/

BOP region

Data and interviews give

strong indications of spare

capacity in the South Island

Source: Coriolis 35Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

36There are strong drivers in place for the further growth of the New Zealand petfood industry

Conclusions on the future growth potential for the New Zealand petfood industry based on supporting drivers

Model; 2013

Conclusions Supporting drivers

Petfood manufacturers leverage New - Primarily low cost pastoral farming systems (lamb, beef, venison, pork)

Zealand’s position as a low cost producer of - 80%+ of meat production is exported; local price is freely traded world price less shipping

protein - New Zealand exports meat to the US market, itself the world’s largest meat exporter

Petfood manufacturers leverage New - New Zealand has a well-regarded, world-class food safety system

Zealand’s reputation for safe, secure, - New Zealand is an island in the middle of the South Pacific ocean out of the path of migratory birds

disease-free meat - New Zealand has strong biosecurity laws and systems in place to keep out introduced pests and diseases

- New Zealand is free of many of the key global livestock diseases (e.g. foot-and-mouth, BSE, bird flu)

Petfood manufacturers can choose from a - New Zealand has a robust meat industry

wide range of suppliers - Meat production is widely distributed across the country; no single region or species dominates

- New Zealand has 66 export grade meat plants spread across the country

There is ample available supply of raw - New Zealand is not intensively farmed indicating capacity for further production growth

materials for further industry growth - Production of key meat species is growing medium term, other than lamb which is flat

- New Zealand exports 3x as much petfood ingredients by value than retail petfood indicating available supply

New Zealand petfood manufacturers have - Leading petfood firms are strongly leveraging New Zealand unique ingredients to differentiate their products against the

demonstrated an ability to innovate competition

- New Zealand firms are innovating with product states, including freeze dried, cooked rolls and air-dried products

- New Zealand firms are innovating around functional ingredients, unique to New Zealand

- New Zealand firms are well positioned in and pushing the “Prey Diet”, the replicating a wild animals natural diet

- New Zealand companies are producing products that are firmly “on trend”

Source: Coriolis 37New Zealand has an excellent range of meats available to Petfood manufacturers – some are unique to New

Zealand

Major exporter Domestic production

Lamb Free range beef Seafood Poultry

Possum Deer/Venison Rabbit Pigs (farmed & wild)

Unique to New Zealand

Source: various; photo credit (Copyright free or public domain); Coriolis analysis 38New Zealand is a trusted supplier of food, particularly in Asia, as this example from Japan shows

Japanese public image of foreign products

Index

100

80

Japan

60

Lower cost

& trusted High cost

Safety 100 = safe, -100 = unsafe

40 & trusted

EU

Scandinavia

NZ & 20

Australia

0

-100 -80 -60 -40 -20 0 20 40 60 80 100

-20

Lower cost &

lower trust USA -40

-60

Asia (excl. China)

-80

Low cost &

China low trust

-100

Cost 100 = expensive, - 100 = inexpensive

Source: USDA Gain report JA8713; Coriolis 39New Zealand is a well known and trusted source of ingredients, in particular lamb; “New Zealand” is often

stated front of pack

Ingredients exported from New Zealand, manufactured offshore

Manufactured in, and exported from, New Zealand

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 40New Zealand has particular strength across a number of attractive market niches

Particular niches where New Zealand has strength/opportunity

Model; 2013

Category/ Core NZ strength Consumer angle/marketing pitch Opportunities

segment Driver of NZ success

Lamb Major lamb producer Exotic meat in most markets Further leverage this exotic ingredient

Largest lamb exporter in the world Consumer visualises their dog “chasing a lamb”

Strong food safety systems

Excellent product quality

Farmed deer/ NZ pioneered deed farming Exotic meat in most markets Further leverage this exotic ingredient

venison Largest global producer Consumer visualises their dog “chasing a deer” Leverage sustainable production angle

Perception as a “wild” or “natural prey”

Possum Effectively the only global source of the Highly exotic meat in all markets Create clear point-of-difference vis-à-vis competitors

“Brushtail” product Appeals to consumer as “natural prey” Pitch as helping protect native NZ forests

Animal is introduced pest Can be positioned as sustainable pest control

Rabbit Animal is an introduced pest Appeals to consumer as “natural prey” Pitch as helping protect native NZ plants

Can be positioned as sustainable pest control

Roll or chub Strong in meat; weaker in grains “Fresher”, more natural, more healthy Continue to lead segment growth and innovation

packaging Pioneered in New Zealand Drive growth in the US market

Freeze-dried Strong in meat; weaker in grains More efficient (less weight) Continue to lead segment growth and innovation

Pioneered in New Zealand More health (high meat content)

“Prey diet” Strong in meat; weaker in grains More healthy Embrace emergence of this new positioning

Pioneered in New Zealand More natural for the animal

Source: Coriolis 41In particular there is widespread recognition of New Zealand’s strength in lamb ingredients

Quotes from interviewees supporting New Zealand strength in lamb Examples of global leaders products containing NZ lamb

2013 2013

“New Zealand lamb is highly sought after as it’s BSE free, we have no foot and

mouth disease and we have a good food safety record. This is really important to

the large companies.” CEO, multinational, MDM supplier

Nestle P&G

“New Zealand’s specialty is ovine (lamb). Cats and dogs like variety and New

Zealand is a good high quality supplier of lamb. We are disease free and have high

volumes. Our lamb gets a premium. We have an excess we need to export.” MD,

major renderer

“Brand NZ is very strong in petfood, especially with lamb and venison.” Manager,

medium sized export company

“We use ‘NZ lamb’ on the label because we are perceived to be very near the top of

the quality tree. We are leading the way in super-premium.” CEO, New Zealand

medium sized company

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 42New Zealand petfood manufacturers use a wide range of ingredients, most of them sourced locally

Ingredients being sourced wholly or partially from New Zealand by key petfood manufacturers May not be NZ manufactured or sourced

2013

Firm Lamb Beef Deer Chicken Seafood Fats & by- Veget- Grains Other Vitamins & minerals

products ables

Vegetable oils

Mars ✓ ✓ ✓ ✓ ✓ ✓ ✓ Natural flavours

Some colours

Nestle ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Flax seeds Some grains & cereals (e.g. rice)

Whey protein

Cheese Gelling agents & emulsifiers

Dextrose

Heinz ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Taurine

Methionine

Butch ✓ ✓ ✓ ✓ ✓ ✓ Garlic

Soy

Bombay/ ✓ ✓ ✓ ✓ ✓ Horse

Jimbo’s

Fond Foods/ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Garlic

Chunky Possum

Ziwipeak ✓ ✓ ✓ ✓ ✓ Dried kelp

Parsley

Omega-3

Natural ✓ ✓ ✓ ✓ ✓ ✓ Fruit

Food/ Eggs

K9 Natural Garlic

PetfoodNZ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Fruit

Biophive ✓ ✓ ✓ ✓

Natural Pet ✓ ✓ ✓ ✓ ✓ ✓ ✓ Greenlipped

Treat Co/ mussel

Zeal Omega 3&6

milk

Source: interviews; various company websites; various product ingredient lists; Coriolis analysis 43Leading petfood firms are strongly leveraging New Zealand unique ingredients to differentiate their products

against the competition

EXAMPLE: Ziwipeak Venison & Fish air-dried dog food

2013

Venison offal

28%

Hoki (Blue Grenadier) is

fished commercially only in

New Zealand New Zealand and Australian

pioneered deer farming waters

Hoki fish

and is the largest 12%

global producer Green Lipped Mussels (Perna

canalicula) is a NZ-unique

species farmed in aquaculture;

Green lipped

it is used as a supplement for

mussel

joint health and mobility

3%

Other Lecithin

7% Chicory Inulin

Dried Kelp

Parsley

Naturally preserved with

Vitamin E

Venison meat Vitamins

50% Chelated Minerals

Source: Ziwipeak website and package; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 44As a result of its strength in meat, but limited position in grains, the New Zealand pet food industry has a

strong focus on wet products for export

EXAMPLE: Mars/Whiskas pouch range produced in Wanganui, New Zealand currently being EXAMPLE: Sample ingredients

sold in Coles Australia

Ingredients:

Sheep and/or Chicken

Core NZ Beef

strength Gelling Agents

Vitamins and Minerals

Colouring Agents

Vegetable Oil

Flavours

Plant Extracts

Taurine

Source: Coles Online (accessed January 2014); photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 45Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

46New Zealand companies are innovating with product states, including freeze dried, cooked rolls and air-dried

products

EXAMPLES: Innovative New Zealand products leveraging new product forms, temperature states and meal occasion

As of 2013

K9 Freeze dried cat and dog “A natural, raw diet provides your dog “When we first went to the US we were

food with nutrition it needs to thrive, the the first freeze dried company on the

way nature intended.” shelves. You see more now.”

“Freeze drying preserves the product in its

natural state; it also makes the product

light.”

Butch dog roll A lightly cooked and wrapped meat based “Globally customers aren't used to meat

product with over 75% meat; no sugar, no rolls this product is new for them.”

wheat, no gluten, no yeast, no artificial

flavours

Zeal air-dried treats “Absolutely no 'nasties' – no vaccines, “We have a range of 18 real dried Veal,

hormones, steroids, antibiotics, Sheep and Venison meat and bone treats

colouring, flavouring, and are also non- to choose from.”

HTP. We have a range of real dried Veal,

Sheep and Venison meat and bone treats”

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 47New Zealand companies are innovating around functional ingredients, unique to New Zealand

EXAMPLES: Innovative New Zealand unique ingredients added to petfood

As of 2013

Ingredient Health Benefits Product Example food

Green-lipped mussel – Pain relief Glucosamine

– Hip and Joint Health Liprinol

– Movement and Mobility Mucopolysaccharides

– Anti inflammatory Betain

omega-3 fatty acids

Deer antler/velvet – Promote growth and Chondroitin Sulphate

immune system Glucosamine

development Collagen

– Cardiovascular and Amino acids

nervous system health

King Salmon – Brain function Omega 3 & 6 & oils

– Shiny coat Protein

– Control of inflammation in Amino acids

the digestive tract Bioactive peptides

– Support for joint cartilage

Manuka honey – Dental care Antibacterial

– Gut health Antiviral

– Skin care

Flax seed oil/flake – Omega 3 Immune, circulatory and

structural systems

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 48New Zealand companies are well positioned in and pushing the “Prey Diet”, the replicating a wild animals

natural diet

EXAMPLES: Innovative New Zealand products replicating wild prey

As of 2013

K9 Sausages Possum Patties

minced chicken Possum, heart, kidney, liver,

frame, heart, ground bone.

“animals diet should kidney, liver, green

replicate an animal with tripe and Power Patties are made

bone, offal and meat” tukkathyme. with minced chicken frame,

green tripe, heart, kidney

and liver.

Lamb Feast Venison Feast

Lamb meat, lamb bone, Venison meat, venison blood,

lamb blood, lamb green venison bone, venison green tripe,

“natural goodness of fresh tripe, lamb liver, broccoli, venison liver, broccoli, cauliflower,

whole foods, blended into cauliflower, carrot, spinach carrot, spinach (chard), cabbage,

a convenient feed (chard), cabbage, apple, apples, pears, venison hearts,

product.” pear, lamb hearts, lamb venison kidneys, eggs, green

kidneys, eggs, green lipped lipped mussel

mussel and garlic.

Air dried Venison cuisine

Moist Lamb – cat food Venison - Meat (includes up to 3% finely

Lamb - Meat, Liver, Tripe, ground bone) Venison - Liver, Lung,

Heart, Kidney, Green- Tripe, Heart and Kidney, New Zealand

“designed to mirror wild prey” Lipped Mussel, Vitamins, Green-Lipped Mussel, Lecithin, Chicory

Minerals, Taurine, DL- Inulin, Dried Kelp, Parsley, Naturally

Methionine. preserved with mixed tocopherols

(Vitamin E), Vitamins, minerals

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 49New Zealand companies are producing products that are firmly “on trend”

EXAMPLES: Innovative New Zealand products that are inline with identified global petfood industry trends

As of 2013

Trend Description Example Producer Example Product

Natural and Organic – No preservatives, added colours, Zeal

flavours Jimbos

– Free from hormones, antibiotics Butch

– Free range cows, sheep, deer

Humanised Food – Reflecting products available for human Zeal (pet milk)

consumption Addiction (Homestyle

venison and cranberry

dinner)

Raw Food / Dried / – 100% Natural ingredients Addiction (dehydrated)

Dehydrated – Fast re-dehyration times more ZiwiPeak (dried)

convenient K9 (freeze dried)

Biophive (air dried)

Gluten free (grain free) – Move away from allergen inducing Ultra

grains Zeal Grainfree

Superpets

Convenience Packaging – Convenient and easy opening food , Maranui free flow frozen

single serve pouches and cans or patties + resesalable fresh

resealable containers meat

Jimbos free flow patties

Mars pouches (x12)

Weight management – Use of lean meats such as venison, Addiction (weight

turkey management)

Source: various; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis analysis 50New Zealand has world-class food and beverage research and development capabilities, including a long

history of meat-specific research, spread across a wide range of universities and research institutes

Key Food & Beverage Industry research bodies in New Zealand

2013

RESEARCH AND SCIENCE ORGANISATIONS UNIVERSITIES

Source: Coriolis analysis 51Mars is working with AgResearch to leverage New Zealand’s meat science capabilities to develop successful

new products

“Mars Incorporated has already confirmed new research funding and is “Mars worked with AgResearch to create a premium petfood product,

making an ongoing commitment to research and development in New being made at Mars’ Wanganui manufacturing plant, to grow export

Zealand, with product innovation being a core part of our long term markets.” Jonathan Cox, Product and Innovation Manager, Mars, FoRST, Press

vision. [I am] optimistic there will be further growth opportunities for release, May 2009

Mars in Wanganui.” Jonathan Cox, Product and Innovation Manager, Mars, FoRST,

Press release, May 2009

“Agriculture Minister David Carter will be in Wanganui today to sign a

memorandum of understanding between the three partners [Mars,

“In 2007, we started some work with AgResearch and Massey AgResearch & Massey] and also to launch a new range of pet care

University that was looking at new ideas for pet food. We have products produced by Mars Petcare factory. The product is the result of

developed a new protein innovation with them. The research has funding received from TechNZ and the signing will form a new group

allowed us to bring out a new range of products under the Whiskas called Protein Innovation NZ.” Wanganui Chronicle, May 2009

brand, which we have launched in Australia… … That launch has been

reasonably successful, and we've seen a marked increase in volumes

required for that market. This project and growth in demand for our

product were linked." Colin Fergus, plant manager, Mars Petfood Wanganui, May

2009

52As a result of being an island nation with strong biosecurity controls, New Zealand is free of a wide range of

animal diseases; this leads to higher yields and excellent market access

EXAMPLES: Livestock diseases that are and are not present in New Zealand*

2013

Major global diseases

Species Present in New Zealand Not present in New Zealand (select)

Cattle Bovine TB Foot-and-mouth

Johne’s Disease Bovine Spongiform encephalopathy (BSE)

Bovine Brucellosis

Sheep Footrot Scrapie

Foot-and-mouth

Blue tongue

Deer Bovine TB Foot-and-mouth

Chronic Wasting Disease

Horse - Potomac horse fever

African Horse Sickness

West Nile virus

Equine encephalomyelitis

Poultry - Highly Pathogenic Avian Influenza (Bird flu)

Infectious Bursal Disease

Newcastle’s Disease (Fowl pest)

Pigs - Foot-and-mouth

Porcine Reproductive & Respiratory Syndrome

Porcine Brucellosis

Classical Swine fever

Salmon - Infectious Salmon Anemia (ISA)

* Full list available at MPI http://www.biosecurity.govt.nz/pests/surv-mgmt/surv/freedom 53Looking beyond food, New Zealand has clear comparative advantage in a some other product categories; of

these nutraceuticals/supplements stands out for growth

Screen of potential/emerging opportunities across wider pet products and petcare

Model; 2013

Product Overall Growing Growing NZ Growing NZ Traditional sources of comparative advantage Comments/notes

category global production export

market Safe/secure Unique raw Low cost Lack of key

systems materials protein diseases

Supplements/ Leveraging unique plants & animals

nutraceuticals

#" !" #" !" #" #" $" #" Growing in human-grade space

Emerging market for pet supplements

Veterinary !" !" !" !" #" $" $" #" Lack of diseases key driver of success to date

medicines Leveraging strength in farm animal health

Pet litter (cat, Growing hay, straw & bedding exports

small animal)

!" !" $" !" !" !" $" !"

Cages/housing Capabilities in metal fabrication

!" $" !" $" $" !" $" $" Major exporter of wood and some metals

Pet apparel China dominates global trade

$" !" $" $" $" $" $" $" No clear leverage or drivers for success

Grooming China dominates global trade

supplies

$" !" $" $" $" $" $" $" No clear leverage or drivers for success

Pet diapers/ Limited market outside Japan

nappies

$" !" $" $" !" $" $" $"

Toys China dominates global trade

$" !" $" $" $" $" $" $" No clear leverage or drivers for success

Live pets Trade is typically breeding stock not volume

$" $" $" $" #" $" $" #" Growing cultural and ethical issues

$%%!%%#"

Low Medium High

Source: Coriolis from interviews; Coriolis estimates & analysis of available data 54Contents

Summary & conclusions

Large & attractive global market

New Zealand petfood exports are growing

Modern and robust value chain

Strong drivers of success

Track record of innovation

Investment opportunities

Appendix 1 – Key firm profiles

55New Zealand has a robust petfood industry with a wide range of firms participating

Key firms in the New Zealand petfood industry

2013

Manufacturers Example Companies

Multinationals*

Retail-ready

Product form

Larger

- Canned

- Refrigerated

- Frozen

- Air dried

- Freeze dried

- Baked

- Dry kibble

Medium

Smaller/Other

*Significant petfood imports; Source: Coriolis 56Three major multinationals have petfood operations in New Zealand

Profiles of the key multinational firms in the New Zealand petfood sector

NZ$m; various; 2013 or as available

Year Production Turnover % Employees

Company founded (tpa) (NZ$) Export1 (FTE) Ownership Brands Note/comments

~1988 14-18,000 $70-$75m 80% 250 Private USA (Mars Pedigree, Whiskas, - Mars Petcare

(NZ) (190 manuf) Family) MyDog, Schmackos, - www.mars.com/global/

Optimum, Royal brands/petcare

Canin, Temptations,

Nutro

1926 ~10,000+ $65-70m 0% ~40 (manuf) Public Swiss; listed Purina, Tux, - Nestle – Purina

(NZ) 100-140 (Nestle) Friskies, Tux, Cat - www.purina.co.nz

Chow, Fancy Feast, - Tux production only in NZ

Waggin Train

1932 ~30,000 $80-90m 15% 150 Private Equity: USA Champ, Chef, - HJ Heinz

(NZ) (Berkshire Hathaway PurePet, Nutriplus, - www.heinzwatties.co.nz/

and 3G Capital) Bruno, Gourmet - NRM, Farmlands contract

manuf. dry

1. NZ production value; Source: interviews, various industry publications; various published articles; company websites and annual reports; Coriolis analysis 57Multinationals in New Zealand – and those sourcing from New Zealand – have a wide range of supply options

Further details on multinationals in New Zealand or sourcing from New Zealand

2013 or as available

Global position Location of NZ factory Location of NZ Source of supply Meat processors with plants near the

NZ facility tonnage (tpa) head office factory

Firms with own manufacturing in New Zealand

Mars #1 petfood firm globally Manawatu- 14-18,000 Auckland Primarily lower North AFFCO, Alliance, ANZCO, Inghams,

Wanganui Island Kintyre, Ovation, Progressive Meats,

Silver Fern Farms, Taylor Preston,

Nestle #2 petfood firm globally Manawatu- ~10,000+ Auckland Primarily lower North Tegel

Wanganui Island

Heinz Former global petfood Hawke’s Bay ~30,000 Auckland Primarily Napier, AFFCO, Alliance, Crusader, Greenlea,

major; sold US business Gisborne, Waikato and Inghams, Ovation, Silver Fern Farms,

to Del Monte; NZ Lower North Island Tegel

potentially a portfolio

orphan

Firms identified to be sourcing from New Zealand

Unicharm #2 Japan petfood firm None - None Canned meat based -

#9 global petfood firm product currently

contract packed in NZ

P&G #4 global petfood firm None - Sales agency Nationwide Nationwide

Colgate #3 global petfood firm None - Auckland Nationwide Nationwide

Source: Coriolis from interviews and analysis 58New Zealand has a robust group of larger petfood producers

Profiles of the key larger-sized firms in the New Zealand petfood sector

NZ$m; various; 2013 or as available

Year Production Turnover % Employees

Company founded (tpa) (NZ$) Export1 (FTE) Ownership Brands Note/comments

1976 10-20,000 $15-20m 5-10% 50-60 Private NZ: (Roby Butch, Golden Boy, - Butch Petfoods

Family) Wag, Hound Dog, - www.bpfstore.co.nz

Bow Wow, - Dog rolls

GingerTom, Carnivore

1967 3,500 $14m 0% 40-50 Private NZ: Jimbos - Bombay Petfoods

(Lawson, David Purely Petfoods - www.jimbos.co.nz/

Allan, others) First Choice - Fresh meat products

Max

2007 2-2,500 ~$10- 0% - Private NZ: (Baker, Superior Chunky, - Fond Foods Ltd

$12me Larkman, Page, Chunky, Possyum - www.superiorchunky.co.nz

others)

2007 500 $10-15m 97% 43 Private NZ/USA: ZiwiPeak - Ziwipeak Ltd

(Stewart, Woodd, - www.ziwipeak.com

Mitchell (USA))

2006 800-900 $5-10m 75% 25 Private NZ: (Smith, K9 Natural - Natural Food Group

Stewart, Bowers, - www.k9natural.com

others)

2013 3,000 $6m 98% 14 Private NZ/Sing: Petfood NZ - PetfoodNZ International Ltd

(2005) (VLR Global, 60%, - www.petfoodnz.com

Moulds,20%, Taylor - Started in 2005, sold, bought back

20%) 2013

2011 250-300 $5-10m 95% 15-20 Private NZ: (Signal, Biophive - Biophive NZ

(dry) Lloyd, others) eN’vee - www.biophive.com/

“Superior Farms Pet - www.superiorfarmspetnz.com

Provisions” - Venison and lamb based treats,

chews, supplements & ingred’s

(bulk & private label)

e = Estimate ; 1 NZ production value; Source: interviews, various industry publications; various published articles; company websites and annual reports; Coriolis analysis 59You can also read