Interest-Only Mortgages and Consumption Growth: Evidence from a Mortgage Market Reform - Department of ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Interest-Only Mortgages and Consumption Growth:

Evidence from a Mortgage Market Reform

Claes Bäckman and Natalia Khorunzhina∗

January 17, 2019

Abstract

We use detailed household-level data from Denmark to analyze how the

introduction of interest-only mortgages affected consumption expenditure and

borrowing. Four years after the reform interest-only mortgages constituted 40

percent of outstanding mortgage debt, making up more than half of mortgage

debt for borrowers in the top and bottom decile of the income. Using an ex-ante

measure of exposure motivated by financial constraints, we show that households

more likely to use an IO mortgage increased their consumption substantially fol-

lowing the reform. The increase in consumption is driven by higher borrowing at

the time of refinancing and by borrowers with lower pre-reform leverage ratios.

Housing wealth effects and labor market dynamics are unlikely to explain the

results.

JEL Classification: D14, E21, G21, R21, R30 ;

∗

Bäckman: Department of Economics and Knut Wiksell Centre for Financial Studies, Lund Uni-

versity, Tycho Brahes väg 1, 223 63 Lund, Sweden. Email: claes.backman@nek.lu.se. Khorunzhina:

Copenhagen Business School, Department of Economics. Porcelœnshaven 16a, 2000 Frederiksberg,

Denmark. Email: nk.eco@cbs.dk. We would like to thank Marcus Asplund, João Cocco, Fane Groes,

Søren Leth-Petersen, Sumit Agarwal, Irina Dyshko and seminar participants at Riksbanken and

Aarhus University for helpful comments.1 Introduction

Four year after a 2003 mortgage market reform that introduced interest-only mort-

gages in Denmark, these new mortgage products made up close to 50 percent of out-

standing mortgage debt and aggregate mortgage debt had increased by 40 percent.

This mortgage credit expansion occurred proportionally across the income and wealth

distribution, was associated with a decline in leverage and was followed by a rapid

increase in house prices. House price growth had trended downwards prior to the

reform, but started accelerating once mortgage banks were allowed to sell the new

products. Quantitatively, Denmark experienced a similar increase in household debt

as the United States over the same time period, even as the regulatory loan-to-value

ratio was unchanged, sub-prime borrowing was nonexistent and there was no increase

in securitization.1

How can we explain these developments? The explanatory power of several expla-

nations for the rise in US debt and defaults is limited by the Danish institutional

framework, as Danish mortgage banks are strictly regulated in their ability to extend

credit to sub-prime borrowers or to increase securitization, and Danish borrowers face

full recourse on their debt and thus have incentives not to unduly speculate on rising

house prices. Moreover, the impact of interest-only mortgages is difficult to recon-

cile with traditional models where borrowing is based on collateral constraints for a

simple reason: amortization payments do not constrain borrowing in these models

(see Guerrieri and Uhlig, 2016, for an overview of collateral-based models).2 This

modeling approach to credit constraints is also difficult to reconcile with the facts,

as the regulatory loan to value ratios in Denmark were constant and aggregate lever-

age declined (Justiniano et al., 2018, reports similar statistics for the United States).

Recent macroeconomic models that incorporate payment-to-income (PTI) constraints

1

In the United States, interest-only mortgages and similar unconventional products accounted for

approximately 50 percent of mortgage origination in 2007, having increased from one percent in 2000

(Justiniano et al., 2017). See also Barlevy and Fisher (2011) and Dokko et al. (2015).

2

Lower amortization payments could be used to increase consumption smoothing (Cocco, 2013),

which would lead to a rise in debt as households stop paying down their debt . However, we will show

that this effect is not sufficient to explain the increase in borrowing and consumption.

1provide more scope for an effect, as amortization payments directly enter the con-

straint (Grodecka, 2017; Kaplan et al., 2017; Greenwald, 2017). However, it is a-priori

unclear how many households are affected by payment constraints, and indeed also

how changing such constraints affect borrowing and consumption.

In this paper we provide empirical support for the importance of payment-to-income

constraints, and examine how a relaxation of such constraints affect borrowing and

consumption expenditure. Our first contribution is to provide an intuitive and novel

equation for when payments constraints are binding and to test how households re-

sponded to a relaxation of this constraint. For households bound by a PTI constraint,

borrowing is limited by the payments that they have to make to use the collateral.

With both a loan-to-value constraint and a payment constraint, borrowing will be

determined by the lesser of the two constraints and we can write up the condition for

when payments are binding: for a sufficiently high house value to income ratio the

payments on the mortgage constrain borrowing, not the value of the collateral. This

simple prediction fits the data on borrowing well. House value to income ratios strongly

predicts whether households use interest-only mortgages: 62 percent of homeowners in

the top quartile had an IO mortgage, compared to 32 percent in the bottom quartile.3

Amromin et al. (2018) report similar statistics for the United States. Consistent with

an interaction between two binding constraints, leverage is declining in house value to

income ratios and interest-payments to income are increasing.

We estimate the impact of the introduction of interest-only mortgages on consumption

expenditure of existing homeowners using their house value to income ratio measured

prior to the reform as our measure of exposure. Our empirical strategy is similar to

Mian and Sufi (2012) and Berger et al. (2016). An extensive analysis of time-trends

indicates parallel trends in consumption growth prior to the reform across groups with

differing levels of exposure to the reform, followed by a clear break with increasing

consumption growth for groups with high exposure and continued higher consumption

3

This pattern holds after controlling for a wide range of household demographic and financial

characteristics.

2levels. We estimate that one standard deviation higher house value to income is asso-

ciated with an approximately 5 percent increase in consumption growth. In aggregate,

IO mortgages increased consumption by 7.6 percent between 2004 and 2010, corre-

sponding to 52 percent of the total increase in consumption expenditure. We find that

the effect is driven by older households and by households with low ex-ante leverage.

Higher leverage in 2002 is associated with a lower response to interest-only mortgages.

While this is inconsistent with a relaxation of binding collateral constraints, the result

is consistent with binding PTI constraints limiting households ability to access their

collateral.

Household consumption expenditure remains higher even as the housing market cycle

turns and house prices decline by an average of 30 percent. The lack of a reversal

strongly suggests that our results are not driven by housing wealth effects or labor

market dynamics. In addition, the empirical evidence from Denmark suggest that

wealth effects are small. Browning et al. (2013) find very limited evidence for housing

wealth effects during 1987-1996. When we extend their results up until 2010, we find

that the only years when house prices have a significant impact on consumption are

between 2004 and 2006.4 This result is driven by a higher refinancing rates in high

house price growth areas relative to low growth areas. If we control for refinancing,

there is no evidence of a housing wealth effect. Andersen and Leth-Petersen (2018)

find similar results using household-level survey data on house price expectations in

a later period in Denmark. We concur with their assessment that the existence of a

housing wealth effect is intimately linked to the functioning of the mortgage market.

If interest-only mortgages relax borrowing constraint, we expect to see higher borrow-

ing at the time of refinancing (what Greenwald, 2017, calls the “frontloading effect”).

We provide evidence for this effect by exploiting the timing of when the household

chooses to refinance to an IO mortgage (Fadlon et al., 2015; Druedahl and Martinello,

2017). Using year and household fixed effects to address endogeneity concerns related

4

This result holds for any subgroup of the population that we consider, including liquidity con-

strained, borrowing constrained and across age groups.

3to fixed household characteristics and business cycle effects, we compare the behav-

ior of households who chose to refinance to an IO mortgage in different years. The

increase in consumption expenditure is almost entirely driven by higher borrowing at

the time of mortgage refinancing: there is a spike in consumption expenditure at the

time of refinancing, followed by a reversion towards the previous trend. On average

half of the increase in mortgage debt at the time of refinancing goes into consumption

expenditure. We therefore do not find strong evidence for an increase in consumption

expenditure levels due to interest-only mortgages. However, while we find that the

main impact is through higher borrowing at the time of refinancing and not through

lower payments afterwards, an analysis of heterogeneous responses suggest that older

borrowers use the reduction in payments to increase consumption afterwards. This is

consistent with consumption smoothing behavior on behalf of older households, who

after retirement wish to live off their wealth. The consumption smoothing argument

not only applies to young households with rising incomes (Cocco, 2013), but also to

older households who after retirement have income lower than their permanent income.

In essence, the forced savings inherent in amortizing mortgages are a cost for these

households, which can be reduced by choosing an IO mortgage instead.5

These results are similar to the results in the literature that studies the household

response to lower interest payments (Agarwal et al., 2017; Abel and Fuster, 2018).6

Bhutta and Keys (2016) find that interest payments have a substantial impact on

household borrowing, an effect is particularly pronounced among younger borrowers

with prime credit scores. Our results also provide an alternative mechanism for the

higher sensitivity to interest-rates documented by Beraja et al. (2018): borrowers

constrained by mortgage payments are not able to borrow against the value of their

collateral, and therefore end up with higher equity. When the mortgage rate falls

5

Note that this requires that the household face binding credit constraints - households who can

borrow unrestrictedly could undo any amortization payment by either refinancing their mortgage and

increased their debt (Hull, 2017), or could simply borrow more initially and use the additional funds

to amortize (Svensson, 2016).

6

See also Di Maggio et al. (2017), who find that lower mortgage payments substantially increase

consumption and Cloyne et al. (2016), who show that borrowers in the United Kingdom and the

United States increase their spending in response to lower interest payments.

4borrowers are able to take advantage of their collateral, and borrowing increases.

We also contribute to the theoretical macroeconomic literature that tries to explain

the boom and bust in house prices. Within recent models incorporating PTI con-

straints there is disagreement on the impact of credit shocks. Greenwald (2017) shows

that in a model where all agents are homeowners (without a rental market) relaxing

PTI constraints leads to a large increase in debt, house prices and consumption.7 In

contrast, Kaplan et al. (2017) construct a model where households choose whether to

become a homeowner (with a rental market) where credit supply shocks have no im-

pact on house prices or consumption, but have a large impact on the homeownership

rate. They instead argue that house price expectations (beliefs) were the key driver

behind the housing boom and bust. The key differences between Greenwald (2017)

and Kaplan et al. (2017) is the presence of a rental market that can absorb credit

supply shocks. A perfect rental market implies that credit supply shocks move the

homeownership rate, whereas a model where all households are homeowners implies

that the effect will come through prices. While we do not discount the importance of

beliefs for driving house prices, we note that in Denmark the homeownership rate did

not change in response to the introduction of interest-only mortgages (Bäckman and

Lutz, 2018). This provides scope for a response in borrowing and house prices. Indeed,

house prices increased following the introduction of interest-only mortgages (Bäckman

and Lutz, 2018). This also implies that a part of the increase in consumption comes

through a wealth effect. This would still represent a causal impact of the introduction

of IO mortgages on consumption, as any housing wealth effect arises from rising house

prices due to IO mortgage.

The Danish institutional framework for mortgage financing helps rule out several other

confounding factors. Mortgage debt is more strictly regulated in Denmark compared

to the United States, with corresponding incentives for both mortgage banks and

households to not unduly speculate on rising house prices.8 Danish mortgage banks

7

See also Favilukis et al. (2017) and Justiniano et al. (2018).

8

Brueckner et al. (2016) argue that because IO mortgage postpone repayments, the higher risk

of negative equity makes this product riskier. In their model, this risk is mitigated if house price

5are legally required to evaluate the income and house value for each borrower to assess

whether the borrower can repay a standard 30-year fixed rate mortgage product even

in the face of increasing interest rates. This requirement is incentivized through reg-

ulation that mandates that the mortgage banks are liable for any losses incurred on

mortgage bonds by investors, even as those bonds are sold off to investors (Campbell,

2013). Other criteria for mortgage lending did not change during the boom. Mortgage

borrowing was limited to 80 percent of the house value, and borrowers were evaluated

on their ability to afford higher interest payments. Borrowers have a strong incentive

to conform to these limits and not to overextend themselves, as all debt in Denmark

is full recourse (and the laws are enforced). Indeed, there was no default crisis in

Denmark even as housing markets declined by 30 percent - mortgage arrears peaked

at 0.6 percent of outstanding mortgage debt.

Our paper is related to several other studies that examine consumption and borrowing

for Danish households in the period around the financial crisis. Andersen et al. (2016)

study how leverage in 2007 affected consumption growth between 2007 and 2009.

Their conclusion is that the negative relationship between leverage and consumption

is the result of a spending normalization that occurs because highly levered households

borrowed more on the eve of the crisis to fund consumption. Jensen and Johannesen

(2016) find that a credit supply to banks had a strong negative and persistent effect on

the consumption of their borrowers. Kuchler (2015) finds that in 2012 households with

interest-only mortgages in Denmark have lower savings rate and higher loan-to-value

ratios. Finally, in a closely related study, Larsen et al. (2018) study how homeowners

used interest-only mortgages in Denmark using a different dataset and a difference-

in-difference strategy. Overall, their study corroborate our results by showing that

households with interest-only mortgages increase their consumption and have higher

mortgage debt.

In general, this paper illustrates the importance of payment constraints in the mort-

expectations are high. Our focus on existing homeowners and the fact that default is an prohibitively

expensive option in Denmark limit the concern that households are using IO mortgages to speculate.

6gage market and provides evidence on how credit supply shocks affect macroeconomic

outcomes. The results are important not only for diagnosing the boom-bust episodes

in Denmark, the United States and elsewhere, but also for policies that guard against

future crises. In particular, our results suggest a framework for analyzing the impact

of macroprudential policies on the cross-section of households, and suggest that such

policies can have a large impact on borrowing and consumption expenditure.

2 The introduction of interest-only mortgages

Interest-only mortgages were introduced in Denmark in 2003.9 This new product

was introduced through a regulatory reform, as the regulatory framework specifically

details which mortgage products the mortgage banks are allowed to offer their cus-

tomers. The purpose was to increase affordability and flexibility for temporarily credit

constrained households, where the expectation was that this would be a niche product

that would not impact house prices or consumption.10 The legislation that allowed the

mortgage banks to offer interest-only mortgages, in Denmark referred to as a “deferred

amortization” mortgage (afdragsfrie lån), was introduced to the Danish parliament on

March 12, 2003 and was voted through parliament on June 4. Mortgage banks were

allowed to start selling interest-only mortgages in October of 2003. The new product

allowed for a 10 year period without amortization payments, after which the borrower

had to repay the outstanding debt over the remaining life-span of the mortgage.

Importantly, other aspects of the regulatory framework were unchanged.11 There was

9

Technically, a bank customer could approximate an interest-only mortgage prior to the reform by

either continuously refinancing Hull (2017) or by extracting more equity and using excess funds to pay

the amortization payments. The other banking institutions were also allowed to offer interest-only

mortgages to their customers. Consequently, the reform can be seen as allowing for an easier and less

expensive way of taking out such a mortgage product.

10

Additional material on the process, the motivation and the debate surrounding the introduction

of IO loans can be found at https://www.retsinformation.dk/Forms/R0710.aspx?id=91430 and

at http://webarkiv.ft.dk/Samling/20021/MENU/00766131.htm.

11

Danish mortgage credit banks provide mortgage loans to households and sell bonds to investors

using the payments from the mortgage loans. The mortgage system operates according to a “matched

funding” principle, where each mortgage loan is matched by a mortgage bond sold to investors. A

more comprehensive overview can be found in Association of Danish Mortgage Credit Banks (2009),

Danske Bank Markets (2013), Campbell (2013, p. 28) and Kuchler (2015).

7no government intervention in the mortgage market, neither through direct ownership

of mortgage debt nor through government insurance of mortgage debt. Similar to the

United States, the predominant mortgage contract in Denmark has historically been

the 30 year fixed rate mortgage, which made up over 90 percent of outstanding mort-

gages in the early 2000s. This is the longest maturity allowed, and is also the most

popular. Variable-rate mortgage was introduced already in 1997. The interest rate on

mortgages is decided by investors in mortgage bonds, not by the mortgage bank itself.

All borrowers can refinance with no pre-payment penalty, regardless of their equity po-

sition. In other words, there is no lock-in effect of housing equity for mortgage rates.

Households can refinance to extract home equity up to the maximum loan-to-value

limit of 80 percent. This requirement was enforced throughout our sample period for

all types of mortgages (Ministry of Economic and Business Affairs, 2007). The cost

for refinancing is approximately 10,000 DKK ($1,500) (Andersen et al., 2015). Bor-

rowers are evaluated on their ability to afford a standard 30-year fixed rate mortgage

regardless of the mortgage contract they choose, and all mortgage debt is full recourse.

In the case of a borrower default, the mortgage bank that supplied the mortgage can

enact a forced sale of the collateralized property. If the proceeds from the sale are

insufficient to cover the outstanding debt, the mortgage bank can garnish the incomes

of the borrower until the debt is repaid. This ensures that there is no strategic incen-

tive to default in Denmark, regardless of the equity position. Indeed, any outstanding

debt will have a higher interest rate than previously.

Due to higher principal debt over the first 10 years, total interest-payments over the

life-span of the loan are higher for an interest-only mortgage compared to a mortgage

that is amortized. The law proposal specifically mandates that the mortgage banks

inform their customers of both the higher costs and the higher risk associated with

these products. In a 2011 survey of IO loan holders, 89 percent reported being “very

well informed” or “well informed” about both the higher cost and the higher risk

associated with their mortgage choice (Association of Danish Mortgage Credit Banks,

2011).

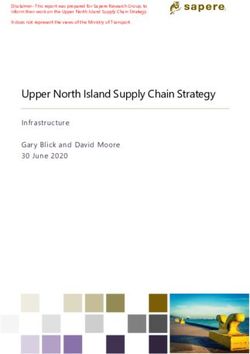

82,000,000 1

Mortgage Debt, Million DKK .9

.8

1,500,000

IO Loan Fraction

.7

.6

1,000,000 .5

55.3 - 68.4

.4

52.6 - 55.3

.3 51.7 - 52.6

500,000

.2 49.0 - 51.7

.1 46.6 - 49.0

0 0 37.0 - 46.6

No data

2000m7

2001m1

2001m7

2002m1

2002m7

2003m1

2003m7

2004m1

2004m7

2005m1

2005m7

2006m1

2006m7

2007m1

2007m7

2008m1

2008m7

2009m1

2009m7

2010m1

2010m7

2011m1

Traditional Mortgage Products Interest-Only Mortgages

IO Mortgage Fraction

Mortgage Debt and IO Mortgage Share over Time

IO Mortgage Share in 2009 Across Municipalities

Figure 1: IO Mortgage Penetration

Notes: The figure plots outstanding mortgage debt in DKK divided into traditional amortizing mortgages and interest-

only mortgages, from Nationalbanken. The grey line plots the fraction of all outstanding interest-only mortgages.

Source: Nationalbanken

In addition, mortgage banks were required to assess the credit risk of the borrower,

and had to maintain all credit risk on their balance sheet. Mortgage credit banks

use the proceeds from their borrowers to issue mortgage-backed bonds to investors.

Mortgage banks receive fees from borrowers but do not receive interest income or

mortgage repayments, which instead accrue to the bond investor. To limit moral

hazard all mortgage credit banks are legally required to retain all credit risk on their

balance sheets. If a borrower defaults, the mortgage bank who issued the bond has to

replace the defaulting mortgage with a bond with equivalent interest rate and maturity.

Investors therefore bear all refinancing and interest-rate risks, but face no credit risk.

This system operates without government intervention or direct guarantees.

Interest-only mortgages rapidly became a popular product. Three years after the re-

form, Figure 1 shows that close to a third of outstanding mortgage debt in Denmark

was held in interest-only mortgages. IO mortgages remain a popular product even

after the financial crisis, representing approximately 50 percent of outstanding mort-

gage debt in 2011. Moreover, interest-only mortgages are prominently used in areas

with high house price levels such as Copenhagen or the other larger cities, but are

also popular in other areas. When we examine Danish municipalities (approximately

equivalent to a US county) on the right hand side of Figure 1, the lowest penetration

9was 37 percent and the highest one was close to 70 percent. This is somewhat in

contrast to evidence from the United States, where Amromin et al. (2018) and Bar-

levy and Fisher (2011) report that IO mortgages were prominent in areas where house

price growth was high but not elsewhere. The Danish housing decline and following

recession did not reduce the popularity of these products, in contrast to how the use of

similar products evolved in other countries. Barlevy and Fisher (2011) and Amromin

et al. (2018) find that IO mortgages in the United States essentially disappeared after

the housing crash and Cocco (2013) documents that IO mortgages in the UK became

less prominent after a regulatory change in 2000. Even though Danish house prices de-

clined by a similar magnitude as in the United States, these products remain popular

and in use today.

3 Data, Variables and Imputing consumption

Denmark Statistics provides data on wealth, income, and demographic characteristics

for the full population of Denmark. This data is collected through third-party report-

ing and is highly reliable, accurate and comprehensive. We use this data to construct a

panel of individuals which includes information on demographics such as age, gender,

education, marital status, the number of children, and municipality of residence; dis-

aggregated asset and debt information such as stock and bond holdings, cash deposits

at banks, bank debt and the market value of mortgage debt; labor market information

such disposable income, wages and employment status; housing information includ-

ing ownership status, property values, number of properties, and any housing market

transactions.

We add more detailed information about mortgage debt characteristics to this dataset.

Mortgage data is provided annually by Finance Denmark starting in 2009, and contains

information from the 5 largest mortgage banks in Denmark with a total market share

12

of more than 90 percent. We use the origination date to assign the mortgage back to

12

See Andersen et al. (2015) for more information about the registry.

10the years before 2009. Specifically, we aggregate loan values and other characteristics

based on the origination year of the mortgage, and then merge these characteristics to

individuals prior to 2009.13

For each mortgage we observe loan size, bond value, maturity, the origination date of

the mortgage, whether it is an interest-only loan and whether the mortgage has a fixed

interest rate. We also observe a unique loan number, which can be shared between

several individuals. As we observe the total loan size and not the individual’s share

of the mortgage, we calculate a equal weight based on the number of individuals with

the same loan number. For example, if a mortgage loan occurs twice in the data, we

assign half the loan value to each individual.

As we will show later, a crucial variable for our analysis is the house value to income

ratio. We construct this variable for each individual using adjusted tax assessed house

values divided by disposable income. Tax assessed house values in the administrative

data systematically underestimates actual house values, and we therefore adjust them

using a scaling factor. The scaling factor is constructed as the ratio between the actual

sales price and the tax assessed valuation for all housing transaction in a given year.

We then average the scaling factor for each year-municipality cell and multiply the tax

assessed values for each individual based on the municipality they live in.14 Finally,

we divide this measure by disposable income to attain a House Value to Income ratio.

We construct two variables related to credit constraints. First, we measure liquidity

constraints as the sum of stocks, bonds and cash deposits divided by disposable income.

We create a dummy equal to one if liquid assets are less than 1.5 months of income

(Browning et al., 2013). Second, we measure collateral constraints as the value of

outstanding mortgage debt divided by housing wealth, which we refer to as leverage,

or loan-to-value (LTV). We create a dummy equal to one if the LTV ratio is above

13

With this procedure, we are unable to classify whether a mortgage is interest-only or not in the

years prior to the most recent refinancing. In effect, the match is worse the further back in time we

go, as households refinance to take advantage of lower interest rates.

14

Denmark Statistics calculates the equivalent scaling factor, but we are unable to use theirs because

of the municipality reform in 2007. For the years when we can compare our scaling factor to the one

provided by Denmark statistics, the two are consistent.

110.5, and also create deciles of leverage.

Our key outcome variable is consumption expenditure. We impute it based on infor-

mation on income and changes in wealth. By definition, spending in a given year is

equal to disposable income minus the increase in net wealth. Since we observe these

variables, we can compute consumption expenditure for individual i at time t as:

Consumption Expenditureit = disposable incomeit − (net wealthit − net wealthit−1 )

This procedure has been used in numerous empirical studies using Danish data (see

e.g. Leth-Petersen, 2010; Browning et al., 2013; De Giorgi et al., 2016; Jensen and

Johannesen, 2016). More importantly, imputed consumption expenditure has been

validated by comparing it to survey measures, and has generally performed well on

average (Browning and Leth-Petersen, 2003; Kreiner et al., 2015).15 Jensen and Jo-

hannesen (2016) compare an aggregated measure of imputed consumption in Danish

registry data to the value of private consumption in the national accounts, and shows

that the trend in these two measures is very similar from 2003 to 2011.

The main concern with imputed consumption is that changes in the valuation of items

on the balance sheet will be measured as consumption. For example, unrealized capital

gains on stock portfolio will be measured as consumption. Similarly, an increase in

the interest rate will lead to a decrease in the market value of a fixed rate mortgage,

increasing net wealth and lowering consumption expenditure. This is not an issue for

housing, where we can observe all property transactions. Since we are not interested

in households who do trade housing, we remove them from the sample and do not

include changes in housing wealth in the imputation.

Browning and Leth-Petersen (2003) find that imputed consumption corresponds well to

the self-reported consumption on average, but that outlier values can be problematic.16

15

See also Koijen et al. (2015) for a similar procedure using Swedish data, and Ziliak (1998), Cooper

(2013) and Khorunzhina (2013) for imputed consumption using survey data.

16

Koijen et al. (2015) point to a similar issue for imputed consumption in Swedish administrative

data.

12We winsorize consumption expenditure at the 1st and 99th percentile. Finally, we limit

the sample to individuals who are present during all relevant years (from 2000 to 2010,

a total of 11 periods).

To address concerns over the stock portfolio (Koijen et al., 2015), we approximate

capital gains on stock portfolios with the market portfolio return. Specifically, we

multiply the value of stock holdings at the beginning of the year with the over-the-

year growth in the Copenhagen Stock Exchange (OMX) C20 index, and calculate

active savings as the end-of-year holdings minus stock holdings at the beginning of the

year adjusted for the capital-gains.

Table 1 provides summary statistics by mortgage type using data from 2002. Con-

sumption in both levels and as a share of disposable income is higher for households

with an IO mortgage, a first piece of evidence that IO mortgage holders may be

more constrained. Consistent with higher constraints, we find higher mortgage to in-

come, interest-payments to income and a larger share facing liquidity and borrowing

constraints among households with an IO mortgage. Second, IO mortgage holders ex-

perienced lower income growth and higher house price growth over the housing market

boom period.

The use of the new mortgage product is not concentrated only among low-income

borrowers. Figure 2 shows that, conditional on holding mortgage debt, IO mortgages

proved popular throughout the (a) age, (b) income, and (c) wealth distributions. All

plots are calculated for the year of origination. The IO mortgage share is U-shaped

in the income and wealth distribution, where both the lower and upper ends of the

distribution are more likely to hold an IO mortgage. This suggests that IO mortgages

provide a credit supply shock that affected both high and low income households This is

in line with the findings in Amromin et al. (2018), who argue that in the United States

similar products were primarily used by sophisticated and high-income borrowers with

high credit scores.

The interest-only mortgage share is strongly increasing in mortgage size. Panel (d)

13Table 1: Summary Statistics by Mortgage Choice

IO Mortgage Traditional Mortgage Difference Highest-Lowest

Financial Characteristics

Consumption 210,198 198,014 -12,183***

(132,999) (113,782) [-30]

Disposable Income 199,436 197,941 -1,495***

(93,411) (68,902) [-6]

Mortgage Debt 549,233 447,546 -101,687***

(303,964) (247,147) [-112]

House Value 995,969 854,118 -141,851***

(581,080) (477,178) [-82]

Sum of Liquid Assets 58,995 63,134 4,140***

(173,271) (177,358) [7]

Interest Payments 42,337 35,724 -6,612***

(22,322) (18,102) [-100]

Consumption to Income 1.06 1.01 -0.06***

(0.51) (0.44) [-35.08]

Consumption growth 2002-2006 0.14 0.09 -0.05***

(0.63) (0.57) [-26.63]

House Value to Income 5.14 4.39 -0.75***

(2.65) (2.14) [-94.96]

House Price Growth 2003-2006 40.26 36.25 -4.01***

(14.92) (15.10) [-80.34]

Income growth 2002-2006 -0.00 0.04 0.04***

(0.30) (0.25) [49.44]

Liquid Assets to Income 0.28 0.30 0.02***

(0.58) (0.53) [10.59]

Mortgage to Income 2.61 2.31 -0.30*

(61.37) (5.80) [-2.25]

Mortgage Rate 0.06 0.07 0.00***

(0.02) (0.03) [58.58]

Interest Payments to Income 0.16 0.13 -0.02***

(0.08) (0.07) [-94.36]

Liquidity Constrained 0.55 0.49 -0.07***

(0.50) (0.50) [-40.95]

Borrowing Constrained 0.76 0.71 -0.05***

(0.43) (0.46) [-33.23]

Household Demographic Characteristics

Age 45.85 43.75 -2.10***

(10.43) (9.01) [-65.66]

Education Length 13.63 13.72 0.09***

(2.66) (2.58) [10.62]

Family Size 3.02 3.12 0.10***

(1.22) (1.19) [24.75]

Employment Ratio during the Year 0.97 0.97 0.00***

(0.12) (0.11) [6.91]

Observations 155923 216261 372184

Notes: Descriptive statistics by mortgage choice for 2002. Column 1 includes all individuals who had an

IO mortgage in 2009, and Column 2 includes all individuals who had a traditional, amortizing mortgage

in 2009. Column 3 reports the differences between column 1 and 2, including the results from a T-test for

differences. For each individual we report demographic and financial characteristics. Financial characteristics

include consumption (defined in section 3), disposable income (the sum of income minus taxes, transfers and

interest-payments), mortgage debt as the market value of outstanding mortgage debt, house value as the tax

assessed value of all housing properties multiplied by the scaling factor, liquid assets as the sum of stocks,

bonds and cash deposits holdings, interest payments as the sum of mortgage and bank deb interest payments.

Mortgage rate is the sum of mortgage interest payments divided by the market value of the mortgage. All

variables marked as ”to Income” is the variable itself divided by disposable income. House price growth

is defined as the percentage growth in square meter prices from 2003 to 2006. Personal income growth is

the percentage growth in personal income (defined as the total income that the individual receives from all

sources). Liquidity constrained is a dummy equal to one if liquid assets are less than 1.5 months of income,

and borrowing constrained is a dummy equal to one if mortgage value divided by house value is greater than

0.5. Demographics include age, years of education, family size and the employment ratio during the year.

Standard deviations are in parentheses. ***, **, * denote significance at the 1%, 5%, and 10% for the T-test.

14Figure 2: IO Mortgage Penetration

1 1

.9 .9

.8 .8

.7 .7

IO Loan Share

IO Loan Share

.6 .6

.5 .5

.4 .4

.3 .3

.2 .2

.1 .1

0 0

20 25 30 35 40 45 50 55 60 65 70 75 80 1 2 3 4 5 6 7 8 9 10

Age Income Distribution

(a) IO Mortgages by Age (b) IO Mortgages by Income

1 .7

.9

.6

.8

Share of IO Loans

Share of IO Loans

.7

.5

.6

.5

.4

.4

.3 .3

1 2 3 4 5 6 7 8 9 10 1 2 3 4 5 6 7 8 9 10

Decile Based on Total Wealth Decile Based on Initial Mortgage Size

(c) IO Mortgages by Wealth (d) IO Mortgages by Mortgage Size

Notes: The figure plots the share of mortgage debt that is interest-only. Age, Income, wealth and initial mortgage

size is calculated for the year of origination. All observations are on the individual level. Data on mortgage choice is

originally from 2009, but matched back in time by year of origination. Panel (a) plots the IO share by age, panel (b)

plots the IO share by income deciles, panel (c) plots the IO share by total wealth, and panel (d) plots the IO mortgage

share based on the initial size of the mortgage.

15reports the IO mortgage share by mortgage size at origination. The share is approx-

imately 38 percent in the lowest decile, but increases rapidly as the mortgage size

increases. In the top decile, the share of IO mortgages is over 65 percent. This rela-

tionship also holds when we control for income or other variables.

In Table 2 we report regression results. The dependent variable in all regressions is a

dummy variable equal to one if the individuals holds an IO mortgage, and zero if not.

We focus on the sample where we can identify the type of mortgage the individual

holds. The independent variables are house value to income and loan value to income,

along with a number of demographic controls. We also control for municipality and

year of origination fixed effects. We standardize house value to income and loan value

ratios to income to have zero mean and unit variance, and provide results separately

for fixed (column 3 and 7) and variable rate loans (column 4 and 8).

The coefficient on the House value to income and Loan size to income ratios are all

positive and strongly significant. A one standard deviation increase in loan size to

income increases the share of interest-only mortgage by approximately 0.09 times a

standard deviation in the first three columns, and by 0.04 of a standard deviation for

the variable rate mortgages. For House value to income, the effect is smaller but still

strongly significant in all regressions. These results are similar to what is reported by

Cocco (2013) for the United Kingdom.17

Overall, interest-only mortgages in Denmark are used prominently across the income,

wealth and age distribution. There is some initial evidence that these products are used

by households that ex-ante were more credit constrained. Moreover, house value and

mortgage size are strong predictors of choosing an IO mortgage, which is consistent

with IO mortgages being more valuable if the reduction in amortization payments

relative to income is larger.

17

All results are robust to using only observations from the years after the reform.

16Table 2: Determinants of Mortgage Choice

House Value to Income Loan to Income

(1) (2) (3) (4) (5) (6) (7) (8)

All Years Controls Fixed Variable All Years Controls Fixed Variable

House value to 0.065*** 0.030*** 0.023*** 0.019***

income (0.000) (0.000) (0.001) (0.000)

Loan size to 0.098*** 0.081*** 0.094*** 0.040***

income (0.000) (0.000) (0.001) (0.000)

Controls No Yes Yes Yes No Yes Yes Yes

Observations 1,529,731 1,528,363 735,565 792,798 1,553,679 1,552,259 744,632 807,627

Notes: The dependent variable is a dummy equal to one if the individuals holds an IO mortgage in 2009. Demographic

controls include age and age squared, years of education, dummies for family size, dummy for female, employment ratio

during the year, an entrepreneur dummy, and a dummy for unemployed. We also include dummies for municipalities

and year of origination. House value to income is the sum of adjusted property values divided by disposable income.

Loan value to income is the mortgage loan size divided by disposable income. House value to income and Loan value

to income are standardized to have zero mean and unit variance. In columns marked by Fixed and Variable we divide

the sample according the interest-rate type. *, **, *** denote statistical significance at the 5%, 1% and 0.1% level.

Regression coefficients estimated with OLS. Robust standard errors in parentheses.

4 Conceptual Framework

How should household consumption respond to a relaxation of borrowing constraints

through an IO mortgage? In this section we consider this question through the lens

of an existing homeowner (which corresponds to our empirical framework). A useful

starting point is that a household that is borrowing unconstrained is by definition

already consuming optimally, meaning that the consumption level is a function of

life-time resources, as in Friedman (1957). An unconstrained household can set a

desired consumption path, borrow when current resources are low relative to lifetime

resources and pay down debt when current resources are high relative to permanent

resources.18 Absent any shocks a relaxation of borrowing constraints through an IO

mortgage should not affect consumption, as the household already could borrow and

consumed optimally by design.19

For a relaxation of borrowing constraints to affect consumption the household needs to

be constrained in her borrowing. Since constraints imply that consumption is below

18

In a model of consumption with an amortization requirement, Svensson (2016) shows that al-

though consumption remain constant with higher amortization payments, borrowing may actually

increase for unconstrained households, as long as the interest rate for borrowing rate is equal to

the interest rate on savings. This is because households borrow more to compensate for the higher

amortization payments.

19

We are abstracting from precautionary savings here, which may be reduced if credit becomes

more readily available. In our empirical results we will investigate this channel more closely.

17the desired level, a relaxation of borrowing constraints induces higher consumption

through higher borrowing. The typical way of modeling this in the macroeconomic

literature has been to relax loan-to-value constraints, where borrowing is constrained

by collateral values (see Guerrieri and Uhlig, 2016, for a comprehensive overview). A

loan-to-value constraint allows the household to borrow an amount M up to a fraction

θH of house value H:

M ≤ θH H

Relaxing this constraint involves either a higher collateral value H or a higher LTV

ratio θH . If the household only faces this constraint, an interest-only mortgage will

not affect borrowing, simply because amortization payments are not in the constraint.

Recent models have instead turned towards payment-to-income constraints, where bor-

rowing is limited by mortgage payments Greenwald (2017); Grodecka (2017); Kaplan

et al. (2017). A PTI constraint limits borrowing by restricting interest payment rm

and amortization payments γ to a fraction θY of income Y :

M (γ + rm ) ≤ θY Y (1)

Relaxing this constraint involves either a higher PTI limit θY , higher income, or lower

mortgage payments. While the focus has mainly been on lower interest payments

(Greenwald, 2017, and a higher PTI limit, see e.g.), lower amortization payments with

this constraint has the same effect. For instance, a household with a mortgage interest

rate of 5 percent and a 3 percent amortization rate that wishes to keep mortgage

payments below 20 percent of income is limited to borrowing at most 2.5 times her

current income. If amortization payments were removed, borrowing can increase to 4

times income.20

We therefore have that for a constrained household, an interest-only mortgage increases

borrowing if the PTI constraint is binding, but not if the LTV constraint is binding.

20

Borrowing to income in the initial example is equal to 0.20/(0.05 + 0.03) = 2.5. With lower

amortization payments, the borrowing capacity is equal to 0.20/0.05 = 4 times income.

18The key question is then to decide what constraint is active: if we want to understand

how IO mortgages affect borrowing and consumption, we need to understand who is

constrained by their mortgage payments. We can rewrite the above constraints as:

θY Y

M̄ ltv = θH H and M̄ pti = ,

(γ + rm )

where M̄ ltv and M̄ pti denote the maximum borrowing given the LTV and PTI con-

straint, respectively. For a borrower who has to fulfill both constraint simultaneously,

the minimum of these two terms will determine borrowing. We can use this intuition

to write the overall debt limit M̄ as:

M̄ = min(M̄ ltv , M̄ pti ).

Since household borrowing capacity is subject to both constraints simultaneously, max-

imum borrowing capacity is determined by the lower of the constraints. In other words,

the PTI constraint will be binding if M̄ pti < M̄ ltv , or:

θY Y

< θH H.

(γ + rm )

Rearranging, we arrive at an expression for when the PTI constraint is binding:

H θY 1

> (2)

Y γ + rm θH

The above equation tells us that if a household is facing financial constraints, the

PTI constraint will be binding for sufficiently high values of H/Y . Note that for a

household facing a PTI constraint, interest rates and amortization payments are func-

tionally equivalent. In this sense, amortization payments represent a real constraint

on borrowing, even though they are fundamentally not a cost but a form of savings.

Intuitively, for sufficiently H/Y , the payments for borrowing are binding, not the

value of the collateral. Even if collateral values are high enough that the LTV con-

straint is not binding, the household is unable to take advantage and cannot borrow

19more. Conversely, if H/Y is sufficiently low, lower mortgage payments will not affect

borrowing.

We illustrate this result in Figure 3, where we plot borrowing according to each con-

straint in panel (a) and the maximum borrowing in panel (b). Both house values and

borrowing are scaled by income. Following the institutional framework in Denmark,

we set θH to 80 percent of house values, and θY to 20 percent of income.21 The LTV

constraint implies that maximum borrowing is linear in collateral values – as the house

value to income ratio increases, so does maximum borrowing. This is represented by

the blue line, where the slope is equal to θH . The PTI constraints is irrespective of the

value of the collateral – the red dashed line denoting the PTI constraint is constant

over H/Y . With an interest rate of 7 percent and amortization payments of 3 percent,

maximum borrowing is equal to 2 times income.

In (b) we plot maximum borrowing according to each constraint, where the constraint

switches from the LTV constraint to the PTI constraint at the threshold in equation

(2). For all values of H/Y above 2.5, the PTI constraint is binding.22 This is indicated

by the dashed vertical line in both figures. Intuitively, while the collateral values are

sufficient to meet the LTV constraint, the payment on any borrowing above this level

will not satisfy the PTI constraint. Conversely, for H/Y below 2.5, the collateral

constraint is binding and the household can only borrow 80 percent of the collateral

values, even though the PTI constraint is slack.

This implies that the household is not fully using her collateral above value of H/Y

above 2.5. IN additoin, this means that leverage (borrowing divided by house value)

is declining in H/Y . As the PTI constraint becomes binding, the household is unable

to borrow against collateral and leverage falls.

What would happen with borrowing if we introduced interest-only mortgages with

these two constraints? In Figure 4 we plot the change in borrowing as we set amor-

21

Formally, there is no PTI constraint in the Danish institutional framework, although mortgage

banks seem to enforce this constraint if we examine the data. The LTV constraint is set by law.

22

We have that the PTI constraint is binding if H/Y is greater than 0.2/(0.07 + 0.03) × 1/0.8 = 2.5.

20Figure 3: Borrowing under Two Constraints

6 .8

6

5

5

Borrowing To Income

Borrowing To Income

4 .6

4

leverage

3

3

2 2 .4

1 1

0 0 .2

0 1 2 3 4 5 6 7 8 0 1 2 3 4 5 6 7 8

House Value to Income House Value to Income

LTV Constraint PTI Constraint Maximum Borrowing Leverage

(a) Borrowing with a PTI and LTV Constraint (b) Maximum Borrowing and Leverage

Notes: We set the interest rate to 7 percent and amortization payments to 3 percent,. We set the LTV constraint θH

equal to 0.8 and the PTI constraint θY equal to 0.2. Both house values and borrowing are divided by income.

tization payments to zero, thereby increasing the maximum borrowing capacity of

households constrained by the PTI constraint. This correspond to a shift up of the

red dashed line. For values of H/Y below 2.5 times income, borrowing does not change.

For these households, removing amortization payments has no impact on borrowing.

For values above 2.5, however, borrowing increases. For certain house values to in-

come, the binding constraints switch from PTI to LTV, creating an angled upward

slope of the red dashed line. The increase in borrowing is therefore increasing in H/Y ,

although the effect is non-linear in three sections of the H/Y distribution: (1) zero

when the LTV constraint is binding; (2) equal to the borrowing constraint on the LTV

ratio between the new and old threshold values due to a constraint switching effect;

and (3) equal to the increase in the PTI limit if the LTV constraint does not start

to bind. The switch from the PTI constraint to the LTV constraint in the second

section of the H/Y distribution is emphasized in Greenwald (2017), and implies that

certain households are not able to take full advantage of the potential increase in bor-

rowing. Moreover, only households with values above the new threshold can take full

advantage.

In Figure 11 in the appendix we examine how borrowing would change if we instead

change the LTV ratio. Borrowing increases if the LTV constraint is binding, but the

21Figure 4: Borrowing under Two Constraints

6 1

5

.8

Borrowing To Income

Borrowing To Income

4

.6

3

2 .4

1

.2

0

0 1 2 3 4 5 6 7 8 0

House Value to Income 0 1 2 3 4 5 6 7 8

House Value to Income

LTV Constraint New LTV Constraint

PTI Constraint New PTI Constraint Leverage Leverage with new PTI

(a) Maximm (b) Maximum Borrowing and Leverage

Notes: The interest rate is 6 percent and amortization payments are 2 percent of mortgage debt, and the collateral

constraint, θH , is equal to 0.8 and is the slope of the LTV constraint. Both house values and borrowing are divided by

income.

higher maximum LTV ratio also makes the PTI constraint tighter. Effectively, this

result arises because the borrower is able to borrow more against the collateral, which

means that the PTI constraint becomes binding earlier.

Although simple, the conceptual framework illustrates key points for how IO mort-

gages will affect consumption among constrained households. First, IO mortgages

can have a large impact on borrowing and through that channel on consumption for

households that are constrained. Functionally, amortization payments have the same

impact on borrowing as interest rates, as they both enter the payment-to-income con-

straint directly. Although amortization payments are not strictly a cost, they can be

a constraint. If we further believe that not consuming optimally represents a utility

cost, as indeed our consumption models imply, amortization payments reduce utility

directly. In that sense, amortization payments are a utility cost.

Second, Beraja et al. (2018) document that households with higher equity respond

more strongly to a decrease in the interest-rate. The authors argue that with higher

equity, a borrower can not only reduce her costs but also borrow more in response

to an interest-rate cut, which implies that the regional distribution of home equity

is important for monetary policy transmission. In their theoretical model the differ-

ences in the equity distribution occurs because of refinancing incentives, which in turn

22generate convexities in the response to interest rates. In our setup, such convexity

occurs because of constraint switching effects – lower interest rates are most valuable

for households with high H/Y because of the PTI constraint, and those households

also have higher equity (as Figure 3 shows, leverage, which is directly analogous to

equity, is declining in H/Y ).

4.1 Empirical support for two borrowing constraints

The simple framework above has clear predictions that are validated in the data. First,

if IO mortgages are able to relax the binding PTI constraint and if this constraint is

indeed related to H/Y , IO mortgages would be increasing in H/Y . This is indeed what

we find in the data – panel (a) in Figure 5 shows that the house value to income ratio

strongly predicts IO mortgage use. The figure plots the loan share against the house

value to income ratio measured in 2002, showing a strong positive correlation between

IO mortgage share and house value to income ratio for binned bivariate averages,

or “binscatters”.23 Second, the figure shows that consumption to disposable income

ratio is increasing in house value to income ratios. Effectively, this implies that the

consumption rate is higher for households with a high house value to income ratio,

which we take as evidence that these borrowers are more likely to be constrained. The

higher spread around the line in panel b) indicates that there is more variation within

each bin, showing that there is heterogeneity in consumption to disposable income

across house value to income ratios.

Third, we plot leverage over H/Y in panel c). This pattern is consistent with binding

payment-to-income constraints interacting with collateral constraints as in Figure 3.

Borrowers with high house value to income ratios who face two constraints are unable

to borrow against their home equity, and thus leverage is lower.

23

The results are robust to excluding any controls and to focusing on mortgage originated between

2004 and 2006, if we use loan size at origination or loan-to-income values, if we focus only on mortgage

originated in the housing boom, if we use municipality-level data, if we split the sample into households

aged below 40 and above 40, and if we focus on the sample that we use in the estimation.

23Figure 5: House Value to Income and Key Outcomes

.8

1.04

Consumption to disposable income

.7

1.02

IO Loan Share

.6

1

.5 .98

.4 .96

0 2 4 6 8 10 0 2 4 6 8 10

House Value to Income Housing Wealth to Income

(a) IO Loan Share (b) Consumption to Income

1 .35

.3

Interest Payments to Income

.8

.25

Leverage

.6

.2

.4 .15

.1

.2

0 2 4 6 8 10 0 2 4 6 8 10

House Value to Income House Value to Income

(c) Leverage (d) Interest Payments to Income

Notes: The figure plots key outcome variables against the house value to income ratio. House value to income ratio is

the adjusted tax assessed house values divided by disposable income. Panel (a) plots the IO mortgage share against

house values to income. IO mortgage share is calculated using the data from 2009. Panel (b) plots interest-payments

to income against house values to income. Interest-payments to income is the total interest payments divided by

disposable income. Panel (c) plots leverage against house value to income, where leverage is defined as the loan value

divided by total house values. Panel (d) plots consumption to disposable income against house value to income, where

consumption is defined is Section 3. All bins control for year of origination and municipality fixed effects.

24Finally, the conceptual framework predicts that interest-payments are increasing in

H/Y (see Figure 12 in the appendix), but that the curve becomes flat as the borrower

hits the PTI constraint. The figure in panel d) does not fully support this prediction,

instead showing that interest payments to income continues to increase with house

value to income ratios. However, panel a) shows that the IO mortgage share is also

increasing in H/Y . If borrowers can substitute amortization payments for interest-

payments, interest-payments to income continue to increase in H/Y , albeit at a slower

pace. This is indeed what the figure shows. A regression analysis (not reported here)

confirms that the coefficient on H/Y is smaller for values of H/Y higher than 4. The

difference in the coefficients is statistically significant.

Overall, a framework with both a PTI and a LTV constraint generates clear predictions

for borrowing that correspond well to the data. Although the framework is simple,

borrowers appear to act as the theory suggests: borrowing seems to be constrained by

mortgage payments and loan-to-value ratios simultaneously.

5 The Impact of IO Mortgages on Consumption

Expenditure

We use two different methodologies to estimate the impact of IO mortgages on con-

sumption and borrowing. Because we cannot perfectly observe who holds an IO mort-

gage and since this decision may be correlated with other variables that drive consump-

tion growth, we begin with a strategy that leverages an ex-ante measure of exposure

to IO mortgages in an intent-to-treat analysis.

5.1 Empirical Strategy

Our exposure measure follows the intuition developed in the conceptual framework

to estimate the effect of relaxed borrowing constraints on consumption expenditure.

25You can also read