Institutional Presentation - 2Q19 - Amazon S3

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

| Apresentação do Roadshow

Institutional Presentation

2Q19

1

Disclaimer

Statements regarding the Company’s future business perspectives and projections of operational and

financial results are merely estimates and projections, and as such they are subject to different risks and

uncertainties, including, but not limited to, market conditions, domestic and foreign performance in general

and in the Company’s line of business.

These risks and uncertainties cannot be controlled or sufficiently predicted by the Company management

and may significantly affect its perspectives, estimates, and projections. Statements on future

perspectives, estimates, and projections do not represent and should not be construed as a guarantee of

performance. The operational information contained herein, as well as information not directly derived from

the financial statements, have not been subject to a special review by the Company’s independent

auditors and may involve premises and estimates adopted by the management.

2

| COMPANY OVERVIEW

1 Platform of brands of reference

Arezzo&Co is the leading Company in the footwear, handbags and accessories

industry through its platform of Top of Mind brands

4

1

Company overview

Arezzo&Co is the reference in the Brazilian retail sector and has a unique positioning combining

growth with high cash generation

Leading company

in the footwear Development of

and accessories Controlling Asset light: high Strong cash

collections with

industry with shareholders are operational generation and

efficient supply

presence in all reference in the efficiency high growth

chain

Brazilian states sector

13.5 million pairs of shoes (1) More than 47 years of ~11,500 models created 90,3% outsourced Net revenues CAGR:

experience in the sector per year production 9.7% (2014 - 2018)

1.5 million handbags (1)

Wide recognition Average lead time of 40 ROIC of 27.7% in 2Q19 (3) Net Profit CAGR: 6.1%

More than 3,000 points of days (2014 - 2018 )

sale 2,515 employees

15 to 18 launches per year Increased operating

~12% total market share and leverage

~28% market share on AB

classes

1. As of 2018

2. Refers to the Brazilian women footwear market (source: Company estimates).

3. Results excluding the adoption of IFRS 16 / CPC 06 (R2) 5

1

Successful track record of

entrepreneurship

The right changes at the right time accelerated the Company's development

FOUNDATION AND

INDUSTRIAL ERA RETAIL ERA CORPORATE ERA INDUSTRY REFERENCE

STRUCTURING

70’s 80’s 90’s 00’s 2011 - 2019

Founded in 1972 Consolidation of industrial Focus on retail Specific brands for each

Focused on brand and product business model located in R&D and production segment

Minas Gerais CONSOLIDATE

outsourcing on Vale dos Sinos Expansion of distribution LEADERSHIP POSITION

1.5 mm pairs per year - RS channels

and 2,000 employees Franchises expansion Efficient supply chain

Launch of new brands International expansion

Opening of the first 9 owned stores in us

shoe factory

First store Opening of the flagship

store at Oscar Freire Merger

Launch of the first design with

national success +

Strategic Partnership

(November 2007)

Launch of new brands

Schutz launch

Commercial operations

centralized in São Paulo

Initial Public Offering (IPO)

Fast Fashion concept February 2011

6

1

Shareholder Structure

Others Aberdeen Management³

44.6% 4.6% 0.0%

Birman Family Float

50.8% 49.2%

1. Arezzo&Co capital stock is composed of 90.954.280 common shares, all nominative, book-entry shares with no par value

2. Shareholder structure as of August 05th, 2019

3. Includes LTI plan

7

1

Strong platform of brands

Strong platform of brands, aimed at specific target markets, enables the Company to capture

growth from different income segments

1972 1995 2008

TRENDY FASHION POP

NEW UP TO DATE FLAT SHOES

EASY TO USE BOLD AFFORDABLE

ECLETIC PROVOCATIVE COLORFUL

16 – 60 YEARS 18 – 40 YEARS 12 – 60 YEARS

CHANNELS AND % REVENUE CHANNELS AND % REVENUE CHANNELS AND % REVENUE

O F MB EX O F MB EX O F MB EX

14 406 1,219 127 17 73 1,094 138 3 157 1,569 124

12% 65% 13% 2% 20% 18% 26% 25% 5% 50% 37% 1%

WEB GROSS REVENUE WEB GROSS REVENUE WEB GROSS REVENUE

R$ 85.8 MM (8%) R$ 68.9 MM (11%) R$ 15.6 MM (7%)

RETAIL PRICE POINT RETAIL PRICE POINT RETAIL PRICE POINT

R$ 240.00 / PAIR R$ 380.00 / PAIR R$ 140.00 / PAIR

GROSS REVENUE GROSS REVENUE GROSS REVENUE

R$ 977.1 MM (50.1%) R$ 604.1 MM (30.9%) R$ 239.3 MM (12.2%)

Notes:

1. Points of sales (LTM); O = Owned Stores; F = Franchised Stores; MB = Multi-brand Stores; EX = Exports (including US and ROW wholesalers).

2. % of each brand gross revenues (LTM) does not include other revenues (not generated by any of the 6 brands).

3. Gross revenues LTM, including external market; does not include other revenues (not generated by any of the 6 brands). 8

4. % of Company’s total gross revenues of LTM.

1

Strong platform of brands

Strong platform of brands, aimed at specific target markets, enables the Company to capture

growth from different income segments

2009 2015 2018

DESIGN CASUAL COMFORT

EXCLUSIVITY YOUNG WELLNESS

IDENTITY URBAN BEAUTY

SEDUCTION MODERN SELF CARE

20 – 45 YEARS 15 – 30 YEARS 30 – 60 YEARS

CHANNELS AND % REVENUE CHANNELS AND % REVENUE CHANNELS AND % REVENUE

P MM EX P MM EX P MM EX

4 26 47 5 427 23 2 292 95

29% 5% 62% 40% 48% 0% 30% 55% 1%

WEB GROSS REVENUE WEB GROSS REVENUE WEB GROSS REVENUE

R$ 3.6 MM (4%) R$ 3.7 MM (12%) R$ 1.9 MM (14%)

RETAIL PRICE POINT RETAIL PRICE POINT RETAIL PRICE POINT

R$ 1,500.00 / PAIR R$ 320.00 / PAIR R$ 230.00 / PAIR

GROSS REVENUE GROSS REVENUE GROSS REVENUE

R$ 90.7 MM (4.6%) R$ 30.3 MM (1.5%) R$ 13.4 MM (0.7%)

Notes:

1. Points of sales (LTM); O = Owned Stores; F = Franchised Stores; MB = Multi-brand Stores; EX = Exports (including US and ROW wholesalers).

2. % of each brand gross revenues (LTM) does not include other revenues (not generated by any of the 6 brands).

3. Gross revenues LTM, including external market; does not include other revenues (not generated by any of the 6 brands). 9

4. % of Company’s total gross revenues of LTM.

1

Multiple distribution channels

Flexible platform through different distribution channels with specific

strategies, maximizing the Company's profitability

NUMBER OF STORES – DOMESTIC MARKET 2Q19

2,621 Broad

636 franchises FRANCHISE____________406

45 owned multibrand¹ distribution

in more than OWNED STORE__________14

stores in clients in network

250 cities in MULTIBRAND____________1.219

Brazil more than throughout

Brazil

1,361 cities Brazil

FRANCHISE____________73

OWNED STORE__________17

MULTIBRAND____________1.094

Gross Revenue Breakdown by Channel2 – (R$ mm)

44,0% 20,4% 14,7% 9,2% 0,1% 11,7% 100,0%

FRANCHISE____________157

OWNED STORE__________3

1.921 MULTIBRAND___________1.569

OWNED STORE__________4

MULTIBRAND___________26

OWNED STORE__________5

MULTIBRAND___________427

Notas: OWNED STORE__________2

1. Without store overlap between brands

2. LTM MULTIBRAND____________292

3. Domestic Market – multibrand without overlap. 10| BUSINESS MODEL

2

Unique business model in Brazil

Customer focus: we are at the forefront of

Brazilian women fashion and design

1 2 3 4 5

NATIONWIDE SEASONED

ABILITY TO SOLID MARKETING EFFICIENT MANAGEMENT

DISTRIBUTION

INNOVATE AND SUPPLY CHAIN TEAM WITH

STRATEGY

COMMUNICATION PERFORMANCE

PROGRAM BASED INCENTIVES

Communication &

R&D Sourcing & Logistics Multi-channel Management

Marketing

BRANDS OF REFERENCE

122

Ability to Innovate

We develop 15 to 18 collections per year

I. Research II. Development III. Sourcing IV. Store Delivery

Creation:

11,500 SKUs / year

Available for

selection:

63% of SKUs created /

year

Stores:

52% of SKUs created /

year

Activities JAN FEV MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Creation

Launch

Orders

Production

Delivery

Normal sale

Discount sale

Winter I Winter II Winter III Summer I Summer II Summer III Summer IV

Arezzo&Co delivers on average 5 new models at the stores per day, allowing for consistent desire-

driven purchases 132

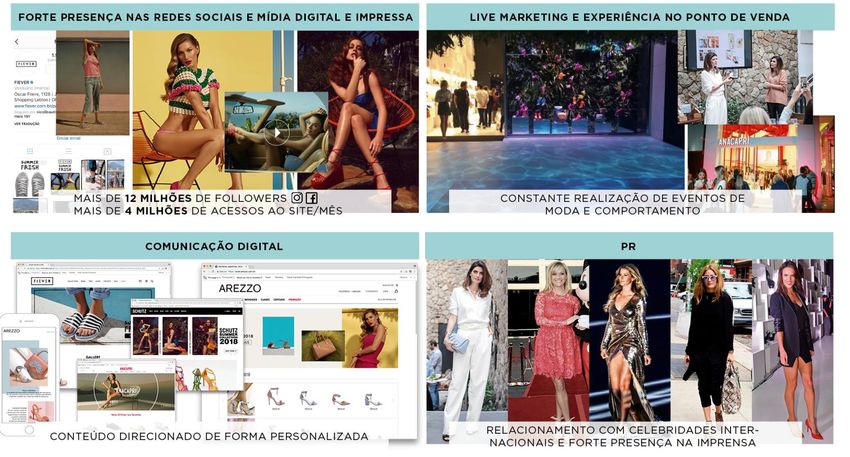

Broad Media Plan

Each brand has an integrated and expressive communication strategy, from the creation of

campaigns to the point of sale

STRONG PRESENCE IN SOCIAL, DIGITAL AND PRINT MEDIA LIVE MARKETING AND EXPERIENCE AT POINT OF SALE

OVER 12 MILLION FOLLOWERS CUSTOMER ACTIVATION THROUGH FASHION AND

OVER 4 MILLION MONTHLY WEBSITE ACCESS LIFESTYLE EVENTS

DIGITAL COMMUNICATION PUBLIC RELATIONS

INTERNATIONAL CELEBRITIES ENDORSEMENT AND

CUSTOMIZED CONTENT FOR DIFFERENT CLIENTS STRONG PRESENCE IN THE PRESS

142

Communication & Marketing Program

reflected in every aspect of the stores

Stores are constantly changed to incorporate the concept of each new collection, resulting in a

higher level of desire-driven purchases

POS materials (catalogs, packaging, and others)

Store layout & visual merchandising Flagship stores

All visual communication at stores is monitored and updated simultaneously throughout Brazil

15

for each new collection2

Store atmosphere: differentiated concepts

for each brand

Shelves, Niches and Suspended shelves New Store Concept Wall display

Increased number of displayed items

New store concept being tested in flagship stores Display of a large variety of products

Products highlighted in the center of the stores

New digital experience: mobile check-out, RFID mirror Inventory at the sales area: lower necessity of

Favorable lighting project

and touch-screen TV additional space for storage

Distribution of the furniture provides more comfort to the

Expected roll out for 2018/19

customers

Each theme is disposed in different niches Experimental and creative Wellness and style

Atmosphere of a jewelry store Focus on wellness (comfort and style)

Experimental and creative space

Private shop experience Timeless concept

Interaction with the customer

Focus on exclusivity, design and high quality

Collaborative experience

materials

162

Flexible Production Process

Production speed, flexibility and scalability to ensure Arezzo&Co’s expected growth based on

asset light model

Sourcing Model Gains of scale

Arezzo’s scale and structure gives flexibility to source a large number

Owned factory with capacity to produce 1,1mm pairs annually and a

strong relationship with Vale dos Sinos production cluster as the of SKU’s from various factories on a short time frame at competitive

main outsourcing region prices

Certification and auditing of suppliers Joint purchases

In-house certification and auditing ensure quality and punctuality Coordination of material purchase jointly with shoe, handbag and

(ISO 9001 certification in 2008) accessories’ suppliers

New Distribution Center – Espirito Santo State Sourcing model – 90% of production outsourced¹

10%

Arezzo&Co Owned Factories

90% Others

Consolidation and improvement of distribution in

national scale

1 Reception: 100,000 units/day

2 Storage: 100,000 units/day

3 Picking: 150,000 units/day

4 Distribution: 200,000 units/day

172

Operation composed by flagship stores in

key Brazilian locations

Owned stores are key to develop retail know-how and increase brands’ visibility

Flagship Stores Greater brand awareness coupled with operational efficiencies

Owned stores are larger and more productive than average and

are located in key cities of Brazil (mainly SP and RJ)

The direct customer interaction enables the development of retail

capabilities, which are also reflected at franchised stores

Arezzo – Iguatemi / SP

Anacapri – Oscar Freire/ SP

Average Annual Sales per Store LTM (R$ MM)

Fiever – Oscar Freire/ SP

Franchises 1,3

Owned Stores 6,6

Schutz – Iguatemi/ SP Alme – Oscar Freire/ SP

182

Strong focus on performance in both

owned and franchised stores

Structure applied to retail in order to achieve better sales and margin results as well as to

integrate and connect all monobrand stores’ back office

Strong focus on franchise and owned store performance

• All sales team (4,000+ people) get connected through national internet broadcast for three sales conventions per

year, creating an aligned sales pitch and a great sense of motivation before each season

• Large service program to assist franchisees on sales and profitability goals

• Recurring training programs in products, fashion trends, sales techniques, store management, IT, among others

• Strong visual merchandising, trade marketing and ambiance investments and training

192

Efficient management of the franchise

network

Model allows fast expansion with low invested capital

Successful Partnership: “Win – Win” Franchise Concentration per Operator

Intense retail training (# of franchises by # of franchisees)

Ongoing support: average of 6 stores/ consultant and average of

4 or more

22 visits per store/ year

franchises

Strong relationship with and ongoing support to franchisee

10%

IT integration with our franchises amounts to 100%

3 franchises 10%

As mono-brand stores, franchises reinforce branding in each city

they are located

1 franchise

56%

24%

Seal of Excellence from ABF (Brazilian Association of 2 franchises

Franchising)

Notes:

96% satisfaction of franchisees1 1. 96% of the current franchisees indicated they would be interested in opening a

franchise if they did not already have one

2. For a regular Arezzo brand store, with expected annual sales of R$ 2,2 million, the

5-year contract and average payback of 36-48 months2 average investment is approximately R$ 670 thousand, including store capex,

franchise fee, WC and initial inventory)

202

Multibrand stores as tool for increased

capilarity

Multibrand stores widen the distribution network and the brands’ visibility, resulting in a stronger

retail footprint

Multibrand stores’ gross revenue¹ Improved distribution and brand visibility

140,0

11.9%

Greater brand distribution network

2.621

Presence in over 1,361 cities

2.700

130,0

2.342

2.500

Fast expansion at low investment and risk

120,0

3.2% Multibrand stores -

2.300

Main focus: increase share of wallet, through the sale of more

107,4 Gross Revenue (R$ brands at the same POS and also handbags as part of the mix

104,1 MM)

110,0

2.100

Important sales channel for smaller cities and the Brazilian

100,0

# Multibrand stores

1.900

countryside

90,0

1.700

Sales team optimization: internal team and commissioned sales

representatives

80,0 1.500

2Q18 2Q19

Multi-brand stores

Notes:

1. Domestic market only 212

New Organizational Structure

Created in 2017, the structure represented the reduction in the number of CEO reports, besides

more agility in decision making, with more focus on people and sustainability.

Risk, Audit and

Board of Directors Finance Committee

People Committee

Internal Auditing

Strategy, Innovation

CEO/CCO and Brands Committee

Alexandre Birman

Operations Digital Administrative and People, Culture and

Brands International

and Industrial Transformation Finance Business Develop. Business

Cassiano Lemos/

Silvia Machado Maurício Bastos

Cisso Klaus Rafael Sachete Marco Aurélio Vidal

BU Arezzo Planning IT Finance/Legal/Fiscal People Schutz USA

BU Schutz Engineering Squads DT Controller Business develop. UN AB

BU Anacapri Sourcing Innovation Investor Relations Sustainability Exports

BU Fiever Quality Valorizza/CRM Risk Management Governance

BU Alme Industry WEB (BR/USA) Strategic Non productive

LAB Logistics Planning/PMO purchase

Management

(Method, goals and

indicators)

222

Corporate governance

The Board is comprised of 7 members, of which 5 are independent, and has a very large

engagement on the strategic planning of Arezzo&Co

Board of Directors

Natura’s CEO for over a decade and former Board Current CEO of Arezzo&Co and part of the controlling group.

Alessandro Carlucci Alexandre Birman

Member of Lojas Renner, Redecard, Alcoa Latam and Founder of Schutz brand, with over 18 year of experience on

Chairman of the Board Member

Itau-Unibanco the footwear industry.

Founder and CEO of “Ethos Desenvolvimento Humano e

José Bolonha Juliana Rozenbaum Over 13 years of experience as sell side equity research

Organizacional“; Board member of the Inter-American

Vice Chairman of the Board Independent Member analyst, focused on retail and consumer sector

Economic and Social Council (UN, WHO)

Luiza Trajano 28 years of experience in Management and Leadership.

Chairman of the Board of Magazine Luiza and LuizaCred Luiz Fernando Giorgi Current member of people committees for Santander, Sul

Independent member and former member of Sadia S.A. Board. Independent Member

América and Grupo Martins

Guilherme A. Ferreira CEO of Bahema Participações, current board member of

Independent Member Petrobras, Valid, Sul América, Gafisa and T4F

Committees

Risk, Audit and Finance Committee Strategy, Innovation and Brands Committee People Committee

Guilherme A. Ferreira (Coordinator) Juliana Rozenbaum (Coordinator) José Bolonha (Coordinator)

Members: Members: Members:

Alessandro Carlucci, Guilherme A. Ferreira and Alexandre Birman, Luiza Trajano and Juliana Luiz Fernando Giorgi, José Bolonha and Cláudia

Edward Ruiz Rozenbaum Falcão

232

Multibrand and multichannel strategy

Organic growth leveraged by multi-brand, multichannel strategy in footwear and handbags

RECEITA

BRUTA

LTM1,2

FOCUS ON SSS

NEW CATEGORIES NATIONAL ROLL-OUT FRACHISES MODEL

44,0%

FOCUS ON BAGS LAUNCH OF START THE

FOCUS ON SSS ON-GOING INVEST. EM READY TO START IN R$ 860.0

SERVICES FRANCHISES FRANCHISES

LIFE STYLE MKT 2019

FRANCHISES SEGMENTATION MM

INCREASE IN SHARE RECENT RECOGNITION

OF WALLET OF THE BRAND IN THE SOLD AT SELECTED

20,4%

CROSS-SELL OF BAGS EXPANSION IN NEW EXPANSION IN NEW

CUSTOMERS CHANNEL POINTS AND IN LINE R$ 398.3

ACTIVATION POS MKT POINTS OF SALE POINTS OF SALE

ATTRACTION CROSS- INCREASE WITH THE BRANDING

MULTIBRAND SELL OF BAGS PENETRATION MM

GROWTH WITH FOCUS

FINALIZE TRANSFER OF 14,7%

PILOT STORES OPENING OF FLAGSHIP OPENING OF FLAGSHIP

FOCUS ON SSS ON SSS FOCUS ON SSS R$ 287.9

RETAINING A MAXIMUM STORES STORES

REFRESH FLAGSHIP

OWNED STORES OF 2 FLAGSHIPS MM

CHANNEL BOOST, EX.: FASHION INFO SHOP

BOOST DIGITAL

LAUNCH IN 2017 IN TOOL FOR ENHANCING TOOL FOR ENHANCING

9,2%

PRESENCE INCREASE

APP BRAZIL AND 2018 USA BRAND AWARENESS BRAND AWARENESS R$ 179.5

TRAFFIC AND

PILOT STORE SHIPPING NEW APP AND EUROPE AND PENETRATION AND PENETRATION

WEB COMMERCE CONVERSION MM

US OPERATION AND

11,7%

FOCUS ON KEY USA PROJECT NOT A CURRENT NOT A CURRENT NOT A CURRENT

SHOWROOM IN R$ 227.9

ACCOUNTS MULTIBRAND STORES FOCUS FOCUS FOCUS

EUROPE

FOREIGN MM

SHARE OF EACH 50,0% 30,9% 12,2% 4,6% 1,5% 0,8% 100%

BRAND (LTM) 2 R$ 977.2 MM R$ 604.2 MM R$ 239.3 MM R$ 90.7 MM R$ 30.3 MM R$ 13.4 MM R$ 1.9 BI

Notes:

1. % of each brand gross revenues (LTM) does not include other revenues (not generated by any of the 6 brands).

2. Gross revenues LTM from the 6 brands; includes foreign market; does not include other (not generated by any of the 6 brands)

LTM Base 242

Strategy

Business model allows multiple growth options

Brands

Other brands

Alme

Channels Fiever Categories

Kiosks Alexandre Birman

Other categories

Dept Stores Anacapri

Outlets Clothing

Online Schutz Other accessories

Exports

Arezzo Leather accessories

Owned stores

Multi-brand Handbags Core

Franchises Footwear Adjacencies

Female

White soles

Brazil

Wellness

North America Class A1 Male

Latin America Teenager

Class A2 Full plastic

Europe Class B1 Children

Middle East

Class B2

Geography Class C1 Segment

Class C2

Positioning

252

Key messages

Arezzo&Co keeps developing its business model in a sustainable way

Consolidated business model with multiple growth opportunities

1 •

•

Sustainable growth and improvement in the profitability of existing brands.

Launch of a new brand Alme and encouraging results in Fiever brand

Staff management an ongoing development

2 •

•

Shareholders value creation sustained by leadership and training of talents

Strengthening of Company’s culture

Ownership of the value chain, greater competitive advantage

3 •

•

More agile and collaborative model

Sell-out oriented to boost results in the value chain

Company’s resilient financial growth

4 •

•

Consistent dividend payout combined with a strong cash flow

Expenses optimization in line with growing revenues

Multi-channel management know-how, excellent platform to lift brands

5 •

•

•

Digital transformation and Omni channel growth as key priorities

Strong knowledge in franchises’ management coupled with efficiency opportunities

Multibrand channel boosting the growth of new brands

2603 | FINANCIAL HIGHLIGHTS

3

Operational and financial highlights

Gross Revenue Breakdown by Brand – Domestic Market (R$ million)

2.500,0 2.000,0

1.500,0

CAGR: 7.0%

2.000,0 1.000,0

1.679

1.524

500,0

65

1.402

1.282 1.307 42

1.500,0

21 220 -

9 9 157

119

72 93 -500,0

443

451 4.6%

458

434 467

1.000,0 -1.000,0

-1.500,0

405 424

500,0

951 15 21 -2.000,0

804 874

767 738 48 57

114 117 -2.500,0

227 228

- -3.000,0

2014 2015 2016 2017 2018 2Q18 2Q19

Arezzo Schutz Anacapri Others

Other: includes A. Birman, Fiever and Alme brands only on the domestic market and other non-brand specific receipts. 283

Operational and financial highlights

Gross Revenue Breakdown by Channel – Domestic and External Market (R$ million)

2.500,0 2.000

CAGR: 8.3% 1.866

1.679

1.800

1.554

2

2.000,0 1.600

1.435

1.358 5 163 1.400

3 129

1.500,0 3 108 299 1.200

5

69 299

44 301

292

1.000

272 384

344 7.7%

1.000,0

304 800

300 305

455 489 600

831 0 1

500,0

686 748

50

400

661 638 41 69

75

104 107 200

185 197

128 152 154 187

– 76 50 66 –

2014 2015 2016 2017 2018 2Q18 2Q19

Foreign Market Franchise Multibrands Owned Stores Web commerce Others Total

Other: includes A. Birman, Fiever and Alme brands only on the domestic market and other non-brand specific receipts. 293

Operational and financial highlights

Key highlights

Sales area increased 5.4% in the last twelve months.

Net Revenues (R$ mln) Number of Stores (R$ mln) and Total Area (m2- ‘000)

CAGR 2007-2018: 20.6% Area CAGR 2014-2018: 7.3%

12,2% 1.527

9,8%

10,6% 1.360

6,4% 1.239

9,3% 1.121

11,9% 1.053

963

26,7% 860

18,8%

38,7% 679

572

12,3%

412

89,4% 367

194

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

303

Operational and financial highlights

Gross Profit Evolution (R$ MM) and Gross Margin (%) Net Profit Evolution (R$ MM) and Net Margin (%)

-100 bps

1.000

47,8% 50,0%

46,6% 46,8%

45,8%

44,3%

900 43,3% 42,5%

45,0%

800 40,0%

250,0

11,4% 11,4% 12,0%

711 10,7% 10,8%

700 35,0% +190 bps

624 9,4% 9,3% 10,0%

200,0

8,9%

549

600 30,0%

476 154 8,0%

500

456 25,0%

150,0

143

400 20,0%

120 120 116 6,0%

300

3.1% 15,0%

100,0

27.9%

4,0%

200

179 184 10,0%

50,0 42

100 5,0%

33 2,0%

– –

- 0,0%

2014 2015 2016 2017 2018 2Q18 2Q19

2014 2015 2016 2017 2018 2Q18 2Q19

Gross Profit Gross Margin

Net Profit Net Margin

Results excluding the adoption of IFRS 16 / CPC 06 (R2) 313

Operational and financial highlights

Gross Revenue (R$ MM) EBITDA Evolution (R$ MM) and EBITDA Margin (%)

CAGR: 8.3%

1.866

2.000,0 2.000

1.800,0

1.679 1.800

1.600,0

1.554 1.600

1.435

1.358

1.400,0 1.400

350,0

-20 bps 18,0%

15,3% 15,2% 15,2% 15,1% 14,9%

1.200,0 1.200

300,0

14,8% 14,3%

16,0%

14,0%

1.679

1.000,0 1.000

250,0

232

1.524 206

12,0%

1.402 7.7%

1.307 177

800,0 800

200,0

165

10,0%

1.282 161

600,0

455 489 600

150,0

8,0%

4.0% 6,0%

400,0 400

100,0

405 424 57 59 4,0%

200,0 200

50,0

2,0%

128 152 154 187

–

76 50 66 –

0,0 0,0%

2014 2015 2016 2017 2018 2Q18 2Q19 2014 2015 2016 2017 2018 2Q18 2Q19

Foreign Market Domestic Market EBITDA EBITDA Margin

Results excluding the adoption of IFRS 16 / CPC 06 (R2) 323

Operational and financial highlights

Arezzo&Co has a solid balance sheet with a healthy net cash position, coupled with a strong

ability to generate operating cash flow and dividend payments

Arezzo&Co generated R$155,6 MM in operating cash

Operating cash flow yield¹ 3.6% flow in the last twelve months, translating into cash flow

yield of 3.2%.

Consistent dividend payments, with a payout of more

Dividend Payout (YTD) 92.7% than 92.7% of net profit available LTM.²

Working Capital Decrease in working capital needs by 110 bps from

(% of Net Revenue) 25.2% 2Q19 to 2Q18.

Change in the capex level from 2015, in line or below

Capex / Depreciation LTM -0.9x annual depreciation.

The Company has a strong balance sheet and a

Net Cash / EBITDA 0.3x Net Cash/EBITDA ratio of 0.3x in June/19.

1) Operating cash flow yield = LTM Operating cash flow / Firm value. Considered Firm Value of R$ 4.352,6 MM (as the average from 06/29/2018 to 06/28/2019).

2) Available Net Income = Net income (-) Constitution of legal reserve (-) Constitution of fiscal incentive reserve 333

Operational and financial highlights

Cash Conversion Cycle (R$ thousand) Capex (R$ thousand)

Cash Conversion 2Q19 2Q18 Change Δ 19 x 18

Cycle (in days) Summary of Investments 2Q19 2Q18

#days (R$'000) #days (R$'000) (%)

107 408.558 101 340.401 7 Total CAPEX 17.486 15.014 16,5%

Inventory¹ 70 162.613 66 128.153 4 Stores - expansion and refurbishing 2.209 3.705 (40,4%)

Accounts Receivable² 85 394.770 85 345.085 0 Corporate 4.280 7.377 (42,0%)

(-) Accounts Payable¹ 48 148.825 51 132.837 -3 Other 10.997 3.932 179,7%

¹ Days of COGS

² Days of Net Revenues

Operational Indicators Cash Flow From Operating Activities (R$ thousand)

Δ (%)

Operating Indicators 2Q19 2Q18 Operating Cash Flow 2Q19 2Q18

19 x 18

# of pairs sold ('000) 3.185 3.075 3,6% Profits before incom e tax and social contribution 44.718 34.883

# of handbags sold ('000) 436 308 41,9% Depreciation and am ortization 19.868 8.788

# of em ployees 2.515 2.468 1,9% Others 665 13.541

# of stores* 696 636 60 Decrease (increase) in assets / liabilities (9.758) (28.098)

Owned Stores 54 52 2 Trade accounts receivables 23.388 9.804

Franchises 642 584 58 Inventories (1.064) (14.689)

Outsourcing (as % of total production) 90,3% 91,8% -1,5 p.p Suppliers (36.638) (25.485)

SSS² Sell-in (franchises) 1,3% 7,3% -6,0 p.p Change in other noncurrent and current assets and liabilities 4.556 2.272

SSS² Sell-out (ow ned stores + franchises + w eb) 4,1% 3,9% 0,2 p.p Paym ent of incom e tax and social contribution (14.309) (2.751)

Net cash flow generated by operational activities 41.184 26.363

* Include international stores 343

Operational and financial highlights

Indebtedness (R$ thousand)

Total indebtedness of R$ 175.9 million in 2Q19 against R$ 175.5 million in 2Q18.

Net cash of 0.3x versus 0.5x EBITDA in 2Q18.

Cash position and Indebtedness 2Q19 1Q19 2Q18

Cash 257.135 299.755 283.172

Total debt 175.957 174.253 175.501

Short-term 153.533 81.827 162.002

% total debt 87,3% 47,0% 92,3%

Long-term 22.424 92.426 13.499

% total debt 12,7% 53,0% 7,7%

Net debt (81.178) (125.502) (107.671)

35Appendix

36A

Key financial indicators

Δ (%) 2Q19 Δ (%)

Key financial indicators 2Q19 2Q18

19 x 18 Pro forma 4 19 x 18

Gross Revenues 489.482 454.679 7,7% 489.482 7,7%

Net Revenues 393.546 373.859 5,3% 393.546 5,3%

COGS (209.215) (195.108) 7,2% (209.234) 7,2%

Depreciation and am ortization (cost) (743) (329) n/a (469) n/a

Gross Profit 184.331 178.751 3,1% 184.312 3,1%

Gross margin 46,8% 47,8% (1,0 p.p) 46,8% (1,0 p.p)

SG&A (135.210) (130.987) 3,2% (134.894) 3,0%

% of net revenues (34,4%) (35,0%) 0,6 p.p (34,3%) 0,7 p.p

Selling expenses (84.011) (88.314) (4,9%) (91.976) 4,1%

Ow ned stores and w eb commerce (29.009) (31.059) (6,6%) (32.546) 4,8%

Selling, logistics and supply (55.002) (57.255) (3,9%) (59.430) 3,8%

General and adm inistrative expenses (43.488) (32.126) 35,4% (45.384) 41,3%

Other operating revenues (expenses) 5 11.414 (2.088) n/a 11.398 n/a

Depreciation and am ortization (expenses) (19.125) (8.459) 126,1% (8.932) 5,6%

EBITDA 68.989 56.552 22,0% 58.818 4,0%

EBITDA Margin 17,5% 15,1% 2,4 p.p 14,9% (0,2 p.p)

Net Incom e 40.568 33.123 22,5% 42.356 27,9%

Net Margin 10,3% 8,9% 1,4 p.p 10,8% 1,9 p.p

Working capital¹ - as % of revenues 24,4% 26,3% (1,9 p.p) 25,2% (1,1 p.p)

Invested capital² - as % of revenues 42,7% 36,9% 5,8 p.p 37,4% 0,5 p.p

Net cash/EBITDA LTM 0,3x 0,5x - 0,3x -

Cash 257.135 283.172 (9,2%) 257.135 (9,2%)

Total debt 175.957 175.501 0,3% 175.957 0,3%

Net cash³ 81.178 107.671 (24,6%) 81.178 (24,6%)

(1) Working Capital: current assets minus cash, cash equivalents and financial investments less from current liabilities minus loans and financing and dividends payable.

(2) Invested Capital: working capital plus fixed assets and other long term assets less income tax and deferred social contributions.

(3) Net debt is equal to total interest bearing debt position at the end of a period less cash, cash equivalents and short-term financial investments.

(4) Excluding the impacts of IFRS 16 / CPC 06 (R2)

(5) Net non-recurring effect of R$ 8.4 million due to the recovery of extemporaneous tax credits arising from the exclusion of income tax and social contribution on the ICMS tax benefit in 2016. 37A

Store History

Store Information 2Q18 3Q18 4Q18 1Q19 2Q19

Sales area¹,³ - Total (m ²) 42.044 42.504 43.965 44.086 44.322

Sales area - franchises (m²) 35.567 36.075 37.691 37.704 37.768

Sales area - ow ned stores² (m²) 6.477 6.429 6.274 6.382 6.553

Total num ber of dom estic stores 627 640 673 677 681

# of franchises 579 590 628 632 636

Arezzo 388 393 405 405 406

Schutz 67 68 73 74 73

Anacapri 124 129 150 153 157

# of ow ned stores 48 50 45 45 45

Arezzo 14 14 14 14 14

Schutz 22 22 17 17 17

Alexandre Birman 4 4 4 4 4

Anacapri 3 3 3 3 3

Fiever 4 5 5 5 5

Alme 1 2 2 2 2

Total num ber of international stores 9 9 12 13 15

# of franchises 5 5 6 6 6

4

# of ow ned stores 4 4 6 7 9

(1) Includes areas in square meters of the stores overseas

(2) Includes seven outlet type stores with a total area of 2,217 m²

(3) Includes areas in square meters of expanded stores

(4) Includes Alexandre Birman and Schutz stores, 3 in New York, 2 in Miami, 1 in Los Angeles, 1 in Las Vegas, 1 in New

Jersey, and 1 in San Francisco. 38A

Balance Sheet - IFRS

Assets 2Q19 1Q19 2Q18 Liabilities 2Q19 1Q19 2Q18

Current assets 877.448 928.010 842.426 Current liabilities 420.301 428.398 360.659

Cash and Banks 7.842 5.691 17.464 Loans and financing 153.533 81.827 162.002

Financial Investments 249.293 294.064 265.708 Lease 36.390 34.272 0

Trade accounts receivables 370.837 394.770 333.982 Suppliers 111.810 148.825 107.352

Inventory 163.368 162.613 140.861 Other liabilities 118.568 163.474 91.305

Taxes recoverable 57.554 42.903 48.899 Non-current liabilities 204.966 260.079 24.089

Other credits 28.554 27.969 35.512 Loans and financing 22.424 92.426 13.499

Non-current assets 426.667 404.581 213.878 Related parties 1.428 1.452 1.436

Long-term receivables 60.003 60.400 59.363 Other liabilities 9.715 9.130 9.154

Aplicações financeiras 0 0 0 Lease 171.399 157.071 0

Trade accounts receivables 10.948 11.070 10.569 Shareholder's Equity 678.848 644.114 671.556

Deferred income and social contribution 20.811 20.410 25.207 Capital 352.715 341.073 341.073

Other credits 28.244 28.920 23.587 Capital reserve 49.035 47.909 45.925

Investments property 3.314 3.324 3.325 Profit reserves 90.033 90.033 178.748

Property, plant and equipment 299.640 275.874 77.831 Tax incentive reserve 136.443 136.443 64.658

Intangible assets 63.710 64.983 73.359 Other comprehensive income 7.257 5.515 1.916

Total assets 1.304.115 1.332.591 1.056.304 Accumulated Profit 43.365 23.141 39.236

Total liabilities and shareholders' equity 1.304.115 1.332.591 1.056.304

39A

Income Statement - IFRS

2Q19

Income Statement - IFRS 2Q19 2Q18 Var.% Var.%

Pro forma

Net operating revenue 393.546 373.859 5,3% 393.546 5,3%

Cost of goods sold (209.215) (195.108) 7,2% (209.234) 7,2%

Gross profit 184.331 178.751 3,1% 184.312 3,1%

Operating incom e (expenses): (135.210) (130.987) 3,2% (134.894) 3,0%

Selling (97.908) (94.581) 3,5% (98.111) 3,7%

Administrative and general expenses (48.717) (34.319) 42,0% (48.182) 40,4%

Other operating income, net 11.415 (2.087) -647,0% 11.399 -646,2%

Incom e before financial result 49.121 47.764 2,8% 49.418 3,5%

Financial income (4.403) (12.881) -65,8% (2.914) -77,4%

Incom e before incom e taxes 44.718 34.883 28,2% 46.504 33,3%

Income tax and social contribution (4.150) (1.760) 135,8% (4.148) 135,7%

Current (5.381) (9.001) -40,2% (5.381) -40,2%

Deferred 1.231 7.241 -83,0% 1.233 -83,0%

Net incom e for period 40.568 33.123 22,5% 42.356 27,9%

40A

Cash Flow Statement - IFRS

Cash Flow 2Q19 2Q18

Operating activities

Income before income tax and social contribution 44.718 34.883

Adjustm ents to reconcile net incom e w ith cash from

20.533 22.329

operational activities

Depreciation and amortization 19.868 8.788

Income from financial investments (3.478) (4.605)

Payments of Interest on loans (190) (1.685)

Interest and exchange rate 207 12.858

Other 4.126 6.973

Decrease (increase) in assets

Trade accounts receivables 23.388 9.804

Inventory (1.064) (14.689)

Recoverable taxes (14.305) (9.036)

Change in other current assets 1.689 (1.005)

Judicial deposits 466 (857)

(Decrease) increase in liabilities

Suppliers (36.638) (25.485)

Labor liabilities 6.528 10.545

Fiscal and social liabilities 3.396 (781)

Variation in other liabilities 6.782 3.406

Paym ent of incom e tax and social contribution (14.309) (2.751)

Lease - -

41A

Cash Flow Statement - IFRS

Cash Flow 2Q19 2Q18

Net cash flow from operating activities 41.184 26.363

Investing activities

Sale of fixed and intangible assets 987 (2)

Acquisition of fixed and intangible assets (17.486) (15.014)

Financial Investments (243.012) (182.058)

Redemption of financial investments 290.187 244.619

Net cash used in investing activities 30.676 47.545

Financing activities w ith third parties

Increase in loans 6.358 45.770

Payments of loans (2.227) (60.872)

Créditos (débitos) com partes relacionadas, exceto sócios

Instalment Lease (10.410) -

Net cash used in financing activities w ith third parties (6.279) (15.102)

Financing activities w ith shareholders

Interest on equity (20.847) -

Profit distribution (54.153) (48.796)

Receivables (payables) w ith shareholders (24) 198

Issuing of shares 11.642 -

Repurchase of shares - (1.814)

Net cash used in financing activities (63.382) (50.412)

Increase (decrease) in cash and cash equivalents 2.199 8.394

Cash and cash equivalents

Foreign exchange effect on cash and cash equivalents (48) 778

Cash and cash equivalents - Initial balance 5.691 8.292

Cash and cash equivalents - Closing balance 7.842 17.464

Increase (decrease) in cash and cash equivalents 2.199 8.394

42Contacts CFO Rafael Sachete IR Officer Aline Penna IR Coordinator Victoria Machado IR Analyst Marcos Benetti Telephone: +55 11 2132-4303 ri@arezzoco.com.br www.arezzoco.com.br

You can also read