ICSC CenterBuild Retail Update November 2017 Garrick H. Brown Vice President of Retail Research, the Americas

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ICSC CenterBuild Retail Update November 2017 Garrick H. Brown Vice President of Retail Research, the Americas Garrick.brown@cushwake.com

Agenda

Notes from the “Retail Apocalypse”

Myths and Realities in the Age of newCommerce

• What is really happening, and why?

• How this trend will play out in 2018 and beyond?

• The good, the bad and the really, really ugly… (Who is growing,

who is shrinking and who is dying?)

Is it

Really?

Major Retailer Bankruptcies

Through November 2017

Aerosoles

Major Retailer Bankruptcies Alfred Angelo

BCBG Max Azria

40.0

Bob’s/Eastern Mountain

Central Grocers

35.0

Gander Mountain

Gordman’s

30.0

Gymboree

HHGregg

25.0

Limited

Marbles: The Brain Store

20.0 MC Sports

Papaya Clothing

15.0 Payless

Perfumania

10.0 RadioShack/General Wireless

Romano’s Macaroni Grill

5.0 Rue 21

Toys R Us

0.0 Traffic Shoes

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 True Religion

Vanity

Major Chain Bankruptcies Forecast Total

Vitamin World

Wet Seal

Source: Cushman & Wakefield Research

Major Chain Store Closures

Have surpassed great recession levels

What’s Really Happening (it’s not

Major Chain Store Closures just about Amazon)?

14,000

Convergence of Four Factors:

12,000 1. Acceleration of newCommerce

2. Over Retailed Marketplace

10,000 3. Race to the Bottom

Discounting (Rise of Off-Price)

4. Shifting Consumer Patterns

8,000

(Millennials Spending

Differently than Past

6,000 Generations)

4,000

2,000

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Major Chain Closures Forecast Major Chain Closures

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Abercrombie & Apparel 60 X X

Fitch 4 – 7K SF

Aeropostale Apparel 154 X X

2 – 4K SF

Aerosoles Shoes 74 X X X X

2 – 4K SF

Alfred Angelo Apparel 64 X X X

2 – 4K SF

American Apparel 110 X X X

Apparel 2 – 4K SF

Applebee’s Restaurant 105 - 135 X X X X

Casual 2 – 5K SF

Ascena Retail Apparel 400 X X

Group 4 – 8K SF

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

BCBG Max Azria Apparel 120 X X

1 – 4K SF

Bebe Apparel 180 X X

2 – 5K SF

*Bed, Bath & Home 15 X X X X

Beyond 20 – 40K SF

Benny’s Dollar 31 X X X

Stores 2 – 5K SF

Best Buy Consumer 20 – 40 X X

Electronics 25 – 40K SF

*Bed, Bath & Beyond is reportedly simultaneously opening 30 new stores.

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Bloomin Brands Restaurant 43 – 60 X X X X

Casual 3 – 6K SF

Bob’s/Eastern Sporting 95 X X X

Mountain Goods 6 – 24K SF

Book World Media 45 X X X

Books 2 – 10K SF

Charlotte Rousse Apparel 5 – 10 X X

2 – 5K SF

Chico’s Apparel 50 X X

3 – 5K SF

Children’s Place Apparel 100 X X

2 – 5K SF

Country Curtains Home 20 X X X X

3 – 4K SF

Crocs Shoes 160 X X X

1 – 4K SF

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Cub Foods Grocery 10 X X

25 – 70K SF

Dillard’s Department 2–5 X

Stores 100 – 200K

Famous Shoes 30 X X X

Footwear 5 – 8K SF

Family Christian Books 240 X X X

2 – 4K SF

Finish Line Shoes 150 X X

3 – 5K SF

*Footlocker/Lady Shoes 100 X X X

Footlocker 2 – 4K SF

Fresh Market Grocery 13 X X

Organic 20 – 35K SF

*Footlocker/Lady Footlocker is reportedly simultaneously opening 90 new stores.

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

GameStop Video 190 X X X X

Games 1 – 3K SF

Gander Sporting 162 X X

Mountain Goods 40 – 60K SF

*Gap/Banana Apparel 200 X X X

Republic 8 – 12K

GNC Misc.. 100 X X X X X

1 – 3K SF

Gordman’s Dept. 101 (50 to X X

Stage Stores)

Guess Apparel 50 X X

3 – 5K SF

*While closing underperforming Gap and Banana Republic stores, the Gap is ramping up

growth of their Old Navy and Athleta concepts.

Source: Cushman & Wakefield Research

Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Gymboree Apparel 350 X X

2 – 5K SF

Hancock Fabrics Misc.. 255 X X

10 – 17K SF

HH Gregg Electronic 220 X X

30 – 50K SF

*Hibbett Sports Sporting 25 - 35 X X

Goods 5 – 6K SF

**IHOP Restaurant 20 - 25 X X X

Casual 2 – 5K SF

J Crew Apparel 50 X X

2 – 5K SF

JC Penney Department 140 X

Store 100 – 200K

* Hibbett Sports is reportedly simultaneously opening 50 – 60 new stores.

Source: Cushman & Wakefield Research * IHOP is reportedly simultaneously opening 80 – 95 new stores.Announced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Jos A Banks Apparel 85 X X X X

3 – 5K SF

Kings Variety Grocery 19 X X

40 – 80K SF

Kohl’s Department 18 X X

Store 70 – 90K SF

The Limited Apparel 250 X X X

1 – 5K SF

Lucy Apparel 44 X X

1 – 3K SF

Macy’s Department 100 X X

Store 180 – 200K

Marsh Grocery 18 X X

Supermarkets 50 – 125K

SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

MC Sports Sporting 66 X X X

12 – 45K SF

Michael Kors Apparel 100 X X X

2 – 5K

Naturalizer Shoes 7 X X X

1 – 4K SF

Neiman Marcus Off Price 10 X X X

Last Call Apparel 15 – 30K SF

New York & Co Apparel 30 X X

2 – 5K SF

Office Depot Office 100 X X

20 – 40K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Papaya Clothing Apparel 10 – 80? X X

2 – 4K SF

Payless Shoe Shoe 700 X X X X X

Source 2 – 4K SF

Perfumania Beauty 65 X

Fragrances 1 – 2K SF

Portrait Misc. 63 X X X

Innovations 1 – 2K SF

RadioShack Electronic 1,000 X X X X

1 – 4K SF

Ralph Lauren Apparel 23 X X

2 – 5K SF

Regis Beauty 25 X X X X X

Salons 1 – 4K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Romano’s Restaurant 37 -93 X X

Macaroni Grill Casual 2 – 5K SF

Rue21 Apparel 400 X X X

2 – 5K SF

Save A Lot Grocery 13 X X

20 – 65K SF

Sears/Kmart Dept./ 430 X X X

Discount 80 – 160K

Stage Dept. 20 (+ adding X X

50

Gordman’s)

Staples Office 70 X X X

25 – 45K SF

Teavana Misc.. 379 X X X

1 – 3K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Closures

Announced retail closures for 2017 & beyond/typical CRE space usage

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Toys R Toys 200 – 400? X X X

Us/Babies R Us 10 – 40K SF

Traffic Shoes Shoes 12 X X

2 – 4K SF

True Religion Apparel 27 X X X

2 – 6K SF

Vanity Apparel 140 X X

2 – 4K SF

Vitamin World Health 51 X X

Vitamin 1 – 3K SF

Walgreen’s Drug Store 860 X X X

15 – 20K SF

Wet Seal Apparel 171 X X

2 – 4K SF

Source: Cushman & Wakefield ResearchTop Retail Chains in Contraction Mode

Announced bricks-and-mortar closure plans

Closures at Record Levels

Top 20 Major Chain Closures 2017

JC Penney Top Contraction Categories:

Finish Line

Aeropostale

Crocs Consumer Electronics

Gander Mountain

Wet Seal Apparel

bebe

Gamestop

Department Stores

Gap/Banana Republic Consumer Electronics

hhGregg

Family Christian Media (Books, Video, Music,

The Limited Etc.)

Hancock Fabrics

Gymboree Office Supplies

Ascena Retail (various banners) Sporting Goods

rue21

Sears/Kmart

Payless

Walgreens

RadioShack

0 200 400 600 800 1,000 1,200

Announced Major Chain Openings 2017

Source: Cushman & Wakefield ResearchTop Retail Chains in Growth Mode

Announced bricks-and-mortar expansion plans

Value, Value, Value

Top 20 Major Chain Openings 2017

Dollarama Top Expansion Categories:

Sephora

Wendy's

Walmart Dollar Stores

Athleta & Old Navy (the Gap)

Tractor Supply Discount Grocery

Sally Beauty

H&M (All Banners)

Off-Price Apparel

Ross Beauty/Cosmetics

Lidl

ULTA Super Stores (but often in

Five Below smaller sizes—Target)

Retro Fitness

TJX (all banners) Fitness/Health Clubs

AutoZone Fast Food

McDonald's

Starbucks Coffee

Aldi

Dollar Tree Fast Fashion

Dollar General Clicks to Bricks

0 200 400 600 800 1,000 1,200

Announced Major Chain Openings 2017

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

99 Ranch Grocery 5 X X

25 – 50K SF

Academy Sports Sporting 6 X X

Goods 85 – 100K

SF

ALDI Grocery 400 (900 by X X

2022)

15 – 25K SF

Allen Edmonds Shoes 10 X x X

2 – 4K SF

Anthropologie Apparel 10 X X X

4 – 9K SF

Athleta/Old Navy Apparel 240 X X X

4 – 17K SF

AutoZone Automotive 200 X X X

3 – 7K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Bargain Hunt Dollar 30 X X X

20 – 25K SF

Blink Fitness Health Club 50 X X X X X X

14 – 20k SF

Bed, Bath & Home 30 X X X X

Beyond 20 – 40K SF

Burlington Off-Price 30 X

Apparel 45 – 80K SF

Cabela’s Sporting 50 X

Goods 2 – 4K SF

Carter’s Apparel 5 X X X

Children’s 50 – 75K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Cheesecake Restaurant 5 – 10 X X

Factory Casual 5 – 10K SF

Chuy’s Restaurant 10 – 15 X X X X X

Fast Casual

Citi Trends Apparel 10 – 20 X X X X

2 – 4K SF

Costco Discount 30 X X

125 – 150K

CVS Drug Store 50 – 70 X X X X X

14 – 18K SF

Dick’s Sporting Sporting 43 X X

Goods Goods 40 – 80K SF

Dogtopia Pet 20 X X X

Supplies 6 – 9K SF

Dollar General Dollar 1,000 X X X

5 – 10K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Dollar Tree Dollar 650 X X X

7 – 10K SF

Dollarama Dollar 60 – 70 X X X

5 – 10K SF

DSW Shoes 20 X X X

20 – 30K SF

Fallas Discount Discount 20 – 25 X

Stores 13 – 17K SF

Five Below Dollar 100 X X X

5 – 10K SF

Footlocker/Lady Shoes 90 X X X

Footlocker 2 – 4K SF

Fred’s Drug Store 20 – 40 X X X

12 – 18K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Free People Apparel 12 X X X

4 – 8K SF

H&M (All Apparel 100 X X X

Banners) 4 – 15K SF

Habit Burger Restaurant 30 – 40 X X X X X X

Fast Casual 2 – 4K

Hammer & Nails Beauty 50 X X X X X X

1 – 2K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Hibbett Sports Sporting 50 - 60 X X

Goods 5 – 6K SF

Home Depot Home DIY 5 – 10 X

100 – 150K

Hobby Lobby Misc.. 60 X X X

40 – 90K SF

Huddle House Restaurant 35 X X

Casual 2 – 4K SF

IHOP Restaurant 80 - 95 X X X

Casual 2 – 5K SF

J. Jill Apparel 15 X X

2 – 5K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Kirkland’s Home 40 X X

Furnishings 6 – 12K SF

Kroger Grocery 35 X X

40 – 80K SF

LA Fitness Health Club 30 – 40 X X

34 – 42K SF

Lidl Grocery 100 X X X

15 – 25K SF

Lululemon Apparel 40 – 50 X X X

2 – 4K SF

Macy’s Off-Price 30 – 40 X X

Backstage Apparel 25 – 40K SF

Marshall’s Off-Price 35 – 50 X X

Apparel 25 – 35K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

McDonald’s Restaurant 200 X X X X X X

Fast Food 2 – 5K SF

Natural Grocers Misc.. 20 X X

1 – 3K SF

Nordstrom Rack Off-Price 25 – 35 X X X

Apparel 25 – 35K SF

Orchard Supply Home DIY 8 – 16 X X

Hardware 25 – 28K SF

Off Broadway Shoes 4–8 X X

18 – 20K SF

Ollie’s Bargain Discount 30 – 35 X X

Market 25 – 35K SF

O’Reilly Automotive 210 X X X

Automotive 7 -12K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Party City Misc.. 25 – 30 X X X

10 – 15K SF

PetSense Pets 30 X X X X

4 – 6K SF

Pollo Loco Restaurant 20 – 30 X X X X X X

Fast Casual 2 -5k SF

Publix Grocery 15 -20 X X

40 – 80K

Rack Room Shoes 20 – 30 X X

4 – 6K SF

Retro Fitness Health Club 125 X X X X X

12 – 15K SF

Ross Dress for Off-Price 100 X X X

Less Apparel 15 – 35K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Sally Beauty Beauty 100 X X X X X

Systems Salons 1 – 4K SF

Sephora Beauty 70 X X X

Cosmetics 3 – 7K SF

Shoe Carnival Shoes 20 X X

5 – 10K SF

Soft Home 17 X X

Surroundings 4 – 6K SF

Sportsman’s Sporting 8 -12 X

Warehouse Goods 15 – 65K SF

Sprouts Farmer’s Grocery 30 X X

Markets 25 – 35K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

Sprint Cellular 40 X X X X X X

Store 1 – 3K SF

Starbucks Restaurant 400 X X X X X X

Coffee 2 – 4K SF

Target Super Store 32 X X X X X

30 – 50K SF

Texas Restaurant 25 – 30 X X X X X

Roadhouse Casual 3 – 6K SF

Tim Horton’s Restaurant 105 X X X X X X

Coffee 1 – 3K SF

TJ Maxx Off-Price 40 – 50 X X X

Apparel 25 – 35K SF

TJX HomeGoods Home 80 X X X

30 – 50K SF

Source: Cushman & Wakefield ResearchAnnounced Major Chain Openings

Not everyone is shrinking…

Retailer Type # Stores Urban Cool Mall & Power & Neighborhood Strip

Avg Size High Streets Lifestyle Regional & Community

Street

TJX AS OF YET Home 5 X X X

UNNAMED NEW 30 – 40K SF

CONCEPT

Tractor Supply Misc.. 100 X X X

15 – 20K SF

ULTA Beauty 100 X X X X

Cosmetics 10 – 30K SF

Urban Outfitters Apparel 4 X X X

4 – 10K SF

Walmart Super Store 89 X X X

40 – 125K

Wendy’s Restaurant 75 X X X X X X

Fast Food 2 – 4K SF

Source: Cushman & Wakefield ResearchThe News Isn’t All Bleak

Some categories and/or concepts are simply on fire!

Food Halls in the U.S.

300

250

200

150

Projected

Existing

100

50

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: Cushman & Wakefield ResearchCool Streets

Millennial-driven up-and-coming alternative urban neighborhoods still hot

The Evolution of Cool Streets

Edgy Cool Bodegas, Bars &

Funky Local… Cheap

Rents

EDGY UP AND

COOL COMING Up and Coming Boutiques, More

Restaurants Arrive…

Rents Climbing

Prime Hipness Funky Local Priced

Out, Cool National

Concepts Arriving…

GONE

MAINSTREAM Rents Climbing

Still Cool, But Going Whole Foods Arrives

Mainstream Rents Climbing

STILL

PRIME

Gone Mainstream Creatives Moving On,

COOL, Replaced by More

HIPNESS

BUT…

Affluent Crowd.

Pottery Barn!

Source: Cushman & Wakefield ResearchCool Street Contenders Privately-held hipster brands can take chances the big chains can’t—and they’re connecting with Millennials! Source: Cushman & Wakefield Research

Global Hipster Style

Independents are gaining ground globally

•French English Japanese Tretorn

Poys & Pirls Dune London Sasquatchfabrics CMMN SWDN

Pigalle Palace Skateboards Bed J.W. Ford Polar Skate Co

AMI Lazy Oak Freak’s Store

Grind London Magic Stick Entertainment German

Club 75

a number of names* Wacko Maria ACRONYM

Maison Kitsune

Satta GUILTY PARTIES PB 0110

Monsieur Lacenaire

Nasir Mazhar Simon Freund

KENZO

A Cold Wall Scandinavian Boulezar

Helas

Maharishi Acne Studios Hien Le

Carven

Cassette Playa Eytys Mykita

Etudes Studio

Goods by Goodhood L’Homme Rouge Frisur

Andrea Crews

Roundel London Wood Wood A Kind of Guise

Cote & Ciel

Garbstore Armoire d’Homme Kostas Murkidis

Vetements

Nigel Cabourn Rascals Beastin

Magenta

Cottweiler Norse Projects Ucon Acrobatics

Source: Cushman & Wakefield Research

WemotoRise of the Indies Many of the hottest new brands are former pure play eCommerce Source: Cushman & Wakefield Research

Clicks to Bricks

Brand embassies, returns savings driving more pure play growth in physical space

50

40

30

20

10

0

Existing Stores YE 2016 Estimated New Stores 2017

Source: Cushman & Wakefield ResearchEntertain Us!

Millennials spend more on experience than “stuff”

Golf/Sports/Arcade Entertainment Themes Athletics Space

BarCades/Mixed (Dave & Aquatic Parks

Buster’s, Punch Bowl Social, etc.) Trampoline Rooms

TopGolf Indoor Rock Climbing

Miniature Golf Indoor Skydiving

Glow Golf Velodromes (Indoor Cycling Tracks)

Ping Pong (Susan Sarandon)

Bowling Alleys (Lucky Strike, etc.) Culture/Performing Arts Space

Duck Pin Bowling Art Galleries

Indoor Go Cart Tracks Museum Space

Indoor Shooting Galleries (Real Live Theater Space

Guns Optional) Dinner Theaters

Cirque Space

Nouveau Theaters Stand Up Comedy Clubs

IMAX Live Music Venues

Restaurant/Theaters

Bar/Theaters Float Rooms/Sensory Deprivation

Children Themed Theaters

Source: Cushman & Wakefield Research

Hipster/Art House TheatersCraft Brewing Explosion

Trend is still not mature nationally

STATES WITH 100+ BREWERIES

Microbreweries Brewpubs Planned

MASSACHUSETTS 75 29 39

MINNESOTA 74 35 42

Craft Breweries in the United States

INDIANA 54 69 25 6,000

WISCONSIN 73 62 27 5,000

MICHIGAN 87 51 33 4,000

VIRGINIA 117 44 63 3,000

OHIO 100 73 47 2,000

ILLINOIS 99 74 44 1,000

NORTH CAROLINA 133 56 55 0

TEXAS 134 58 105 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

FLORIDA 141 51 76 Brewpubs Microbreweries Regional Breweries

PENNSYLVANIA 84 116 62

OREGON 133 93 26

NEW YORK 170 91 80

WASHINGTON 227 88 52

COLORADO 199 121 67

CALIFORNIA 388 204 156

Source: Cushman & Wakefield ResearchWhat About the “Retail Apocalypse?” Source: Cushman & Wakefield Research

US eCommerce Total Share of Retail

Stronger growth ahead due to ePharma & eGroceries

What’s Really Happening

(it’s not just about

13.0%

12.0% Amazon)?

% of Total Retail Sales

12.0%

11.0% Convergence of Four

9.1% Factors:

10.0%

9.0%

Q3 17

1. Acceleration of

8.0% newCommerce

7.0% 2. Over Retailed

Marketplace

6.0%

3. Race to the Bottom

5.0% 4.2% Discounting (Rise of Off-

4.0% Price)

4. Shifting Consumer

3.0%

Patterns (Millennials

Spending Differently

than Past Generations)

Source: Cushman & Wakefield Research and Moody’s AnalyticsFrom eCommerce to newCommerce

How online keeps evolving…

1995 - 2000 2001 - 2009 2010 - Present 2015 - Present 2017 - ?

The Early Days Pure Play The Age of Omnichannel newCommerce

Years Amazon Age Age

Desktop

Desktop Desktop Desktop Desktop

Initial Launch of Mobile Mobile Mobile Mobile

eCommerce Tablets Tablets Tablets

Post Tech Wreck Ramp ?

Rise (and Fall) Up of New Pure Play Amazon Distribution Amazon Dominance

of Early Players Internet eCommerce Strategy: Speed to Continues Seamless Integration

Consumer over Tax of Omnichannel (now

Distribution Strategy: Retailers Still Building a GIVEN for Retail

Tax Advantages Amazon Dominance eCommerce Survival)

over Speed Infrastructure

Retailers Rush to Build eGroceries

eCommerce Emergence of Bricks

Infrastructure to Clicks Movement ePharma

Source: Cushman & Wakefield ResearchFrom eCommerce to newCommerce

eCommerce GAFO numbers demonstrate bricks-and-mortar challenges

$330,000 40.0%

Retail Sales: GAFO, ($Mil.) eCommerce Share

$320,000 35.0%

$310,000 30.0%

$300,000 25.0%

$290,000 20.0%

$280,000 15.0%

$270,000 10.0%

$260,000 5.0%

2011

Q2-11

Q3-11

Q4-11

2012

Q2-12

Q3-12

Q4-12

2013

Q2-13

Q3-13

Q4-13

2014

Q2-14

Q3-14

Q4-14

2015

Q2-15

Q3-15

Q4-15

2016

Q2-16

Q3-16

Q4-16

2017

Q2-17

Source: US Commerce Department, Cushman & Wakefield ResearchJeff Bezos Vs. the World

Guess who is winning so far?

As robust as eCommerce

growth continues to be…

55% Total Retail Sales

Amazon continues to

45% eCommerce Sales

outperform even those

numbers…

Amazon Sales

35%

Amazon accounted for 43%

25%

of all USA eCommerce sales

in 2016…

15%

Amazon sales surged 33.7%

in Q3 2017.

5%

Q3 2009

Q3 2010

Q3 2011

Q3 2012

Q3 2013

Q3 2014

Q3 2015

Q3 2016

Q3 2017

-5%

-15%

Source: US Commerce Department, Company Reports/SEC Filings/ Cushman & Wakefield ResearchAmazon/Whole Foods

Amazon didn’t buy a grocery chain; they bought 462 eGrocery fulfillment centers

eGroceries has only just

Online Grocery Market Share 2016

begun in the USA

USA

Amazon’s $13.7B purchase

Netherlands of Whole Foods means

Spain disruption for grocers, not

so much for landlords

Czech Republic

China Traditional grocers need to

ramp up eGrocery efforts…

Taiwan

France Likely scenario for 2018:

Blue Apron, HelloFresh or

United Kingdom other “Meal Kit” operator is

Japan

acquired by traditional

grocery chain to accelerate

South Korea eGrocery rollouts…

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

Online Grocery Market Share 2016

Source: Kantar Worldpanel, Statista, Cushman & Wakefield ResearchLook for Strong Growth from Amazon/Whole Foods

But still just in denser urban and suburban locales

2016: 52.1% of all USA

eGrocery sales came from

just eight states…

Or, more specifically, dense

urban markets within those

eight states…

OH PA NY

IL 3.3% 3.9% 13.8%

4.3% NJ

Final Mile still rules

CA 3.9%

12.3%

TX

5.3%

FL

5.3%

Source: IBISWORLD, Cushman & Wakefield ResearchAmazon/Whole Foods Has Some Catching Up to Do

Combined grocery market share in 2016 was roughly 3%

Look for aggressive growth

from Amazon/Whole Foods

likely to begin 2H 2018.

We anticipate that as many

as 500 new stores in

different formats may be

opened in the next five

years…

Source: Kantar Worldpanel, Statista, Cushman & Wakefield ResearchWhat’s Next for Amazon? Furniture and Pharma both on the horizon… FURNITURE & PHARMA Source: Cushman & Wakefield Research

Walmart Innovations…

Looking to catch up; leveraging competitive advantages to compete w/Amazon

Build the most compelling complement to the physical store network

• Q2 2017 online revenues reported up 60% • Scan and Go

• 67 million SKUs online; up 30% from Q1 2017 • Curb-side services

• Online grocery in 900 locations • Uber and other pilot partners

• Easy re-order • Store associate private delivery

• Click and collect discounts • Jet influences in reshaping

strategy

• In-store technology – The 100 Towers

• Latch-key delivery

Source: Company filings, Retail Info Systems, Chain Store AgeAnd What’s Going on Here?

Is Walmart going upscale?

+

+

+

+ ?

Source: Cushman & Wakefield Research2018: the Year of M&A Mania? Undervalued concepts ripe for acquisition… Will we see the emergence of a retail duopoly? Source: Cushman & Wakefield Research

The “Apocalypse” Story Isn’t Going Away Any Time Soon

Next year likely to see peak closures

Challenges Next Year:

Major Chain Store Closures

14,000 Bankruptcies Likely Not to

Reach 2017 Levels, but Still

12,000 Elevated…

10,000 Can Sears Survive Another

Year?

8,000

Increased Department Store

6,000 Closures

4,000 Second Wave of Strategic

Closures to Follow

2,000 Department Store

Consolidation as Tenants

0

Exercise Co-Tenancy

Clauses

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Major Chain Closures Forecast Major Chain Closures M&A Consolidations

Source: Cushman & Wakefield Research and Moody’s AnalyticsDanger Zone

Bankruptcies will persist in 2018 and beyond

Credit downgraded, late

Potential Vulnerabilities Ahead payments, have sought

Apparel & Department Stores restructuring or hired financial

advisers or have issued “going

6,000

warning” concerns.

4,878

5,000

4,000 2018 Bankruptcy Watch

Sears

3,000 2,710

Neiman Marcus

2,000 1,667

1,430 J. Crew

1,020 Vince

1,000 554 575 564 650

335 364 368 300

86 262 187 David’s Bridal

0

Nine West

Claire’s

Lands’ End

Charming Charlie

Potential Vulnerabilities Ahead Bon-Ton

99 Cents Only

Source: Cushman & Wakefield Research and Moody’s Analytics Charlotte RusseNot A Good Combination…

USA has most retail space per capita and lowest sales PSF

The Father of the American Mall

Sales per Square Foot per Capita

30 $3,500

“I am often called the father of

the shopping mall. I would like

$3,000

25 to take this opportunity to

disclaim paternity once and for

$2,500

20

all. I refuse to pay alimony to

those bastard developments.

$2,000 They destroyed our cities…”

15

$1,500

Viktor Gruen

10

$1,000

5

$500

0 $0

USA Canada Australia UK France China Germany

Square Footage per Capita Sales per Square Foot per Capita

Source: Turner Construction Cost Index, Cushman & Wakefield ResearchOver-Retailed, But Not All Retail is Suffering

Neighborhood/Community and Strip Centers doing fine…

Shopping Center Total GLA Vacancy Vacancy Share of Malls and Power Centers

Type (MSF) Rate Rate Retail have been most impacted

Q3 2016 Q3 2017 Market by current wave of

closures…

Power Centers 754.5 4.8% 5.0% 7.1%

But Malls only account for

8.4% of all USA retail and

Shopping Centers 3,537.2 8.0% 7.8% 33.1%

(Neighborhood, Power Centers account for

Community, Strip) 7.1% of all USA retail.

Malls (Lifestyle, 899.2 5.4% 6.2% 8.4%

Regional Mall, Super Shopping Centers

Regional Mall) (neighborhood, community

and strip centers) have

Specialty Centers 85.7 5.0% 4.9% >1.0%

(Outlet, Airport, etc.) actually seen vacancy

declines.

Freestanding Retail 5,400.4 3.0% 3.2% 50.5%

We estimate that the

marketplace is over-retailed

by roughly 1.5 Billion

TOTAL RETAIL USA 10,676.0 4.8% 5.3% 100.0%

Square Feet.

Source: Costar Group, Cushman & Wakefield ResearchFeeling Good in the Neighborhood

Neighborhood/Community/Strip vacancy continues to slowly fall

What’s Really Happening

(it’s not just about

70.0 12%

Amazon)?

60.0

10% Convergence of Four

50.0 Factors:

40.0 8%

Million Square Feet

1. Acceleration of

30.0

Forecast newCommerce

6% 2. Over Retailed

20.0 Marketplace

3. Race to the Bottom

10.0 4% Discounting (Rise of Off-

Price)

0.0

4. Shifting Consumer

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017 Q3

2017 Q4 (F)

2018 (F)

2019 (F)

2020 (F)

2%

(10.0) Patterns (Millennials

Spending Differently

(20.0) 0% than Past Generations)

Net Apsorption (MSF) New Construction (MSF) Overall Vacancy

Source: Costar Group, Cushman & Wakefield ResearchPower Centers More of a Question Mark

Will traditional power center tenants re-tenant troubled malls?

What’s Really Happening

(it’s not just about

45.0 9%

Amazon)?

40.0 8%

35.0 Convergence of Four

7% Factors:

30.0

Million Square Feet

6%

25.0 1. Acceleration of

20.0 5% newCommerce

2. Over Retailed

15.0 4%

Forecast Marketplace

10.0 3. Race to the Bottom

3%

5.0 Discounting (Rise of Off-

2% Price)

0.0

4. Shifting Consumer

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017 Q3

2017 Q4 (F)

2018 (F)

2019 (F)

2020 (F)

(5.0) 1%

Patterns (Millennials

(10.0) 0% Spending Differently

than Past Generations)

Net Apsorption (MSF) New Construction (MSF) Overall Vacancy

Source: Costar Group, Cushman & Wakefield ResearchDollar-Dazed

Race to the bottom has some winners

What’s Really Happening

Dollar General will open

(it’s not just about

1,000 new stores in 2017. Amazon)?

This will be the fifth Convergence of Four

consecutive year that Dollar Factors:

General has opened at least

750 new stores. 1. Acceleration of

newCommerce

2. Over Retailed

Over the last five years, dollar

Marketplace

store chains have grown by 3. Race to the Bottom

over 7,000 units in the USA. Discounting (Rise of Off-

Price)

That equates to a new dollar 4. Shifting Consumer

store opening once every four Patterns (Millennials

hours in the USA for five Spending Differently

straight years. than Past Generations)

Source: Cushman & Wakefield ResearchIt’s Never Been Better for Off-Price

Department stores are just as challenged by off-price as online…

Projected Amazon Market Share Projected Clothing And Accessory

of Clothing And Accessories Revenues In 2021

16% $ 62B

BILLION $

8.2%

%

6.6% $26B

$23B

2016 2017 2021 AMAZON TJ MAXX MACY’S

Source: Cowen & Company, Cushman & Wakefield ResearchBut What Does it Mean for Malls?

Bifurcation in performance continues to widen…

Closures Impacting the

Weakest Properties, Not All

Properties

If the goal is to reduce your

physical footprint, while

looking to boost your online

sales… This inherently means

that your remaining physical

locations are more important

than ever before…

Source: Cushman & Wakefield Research,Not All Malls are in Trouble

It’s all about class…

Class A and above malls

Approximate Number of Malls by Class accounted for more than

200 70% of all mall retail sales in

150 2016.

100

There are roughly 670 Class

50

B and C malls in the US, but

0 they only accounted for 28%

A++ A+ A A- B+ B+ B- C+ C C- D of all mall sales last year.

A++ A+ A A- B+ B+ B- C+ C C- D

Class D malls accounted for

Approximate Share of Total Mall Value by Class less than 0.2% of all mall

25.0 sales last year…

20.0

15.0

10.0

5.0

0.0

A++ A+ A A- B+ B+ B- C+ C C- D

A++ A+ A A- B+ B+ B- C+ C C- D

Source: Cushman & Wakefield Research, Fung Global, Green Street Advisors, BloombergNot All Malls are in Trouble

It’s all about class…

Death Spirals Will

Accelerate in 2018 &

Sales PSF

Strengthening Beyond…

$1,200 Position

Number of US Malls 2007:

$1,000 1,350

Average Sales PSF 2016: $480 PSF

$800 If Below… Watch Out! Number of US Malls 2017:

Weakening 1,150

Position

$600

Number of US Malls 2027:

850

$400

$200

$0

A+++ A+ A A- B+ B B- C+ C C- D

Sales PSF

Source: Cushman & Wakefield Research, Fung Global, Green Street Advisors, BloombergAgenda

Do the Old Development Rules Still Apply?

Is it Still as Easy as Following the Rooftops?

• Where are the new rooftops? Urban Vs. Suburban?

• Demographic Shifts to Watch…

• The hourglass economy—Don’t get stuck in the middle…

• Upscale, discount or experiential—what it means by shopping

center type?The Urban Growth Trend is Real

Urban share of household growth

Demographic Shifts to Watch

Urban Areas More Than

Doubled Their Usual Growth

Rates from 2010 – 2015.

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchThough Suburban Still Captured Most the Growth

Suburban share of household growth

Demographic Shifts to Watch

Despite urban surge, we are

still a nation of suburbs…

Rural populations, however,

continue to dwindle.

Population Distribution 2015

Urban 15%

Suburban 64%

Rural 21%

2010 – 2015 Growth Capture

Urban 21%

Suburban 71%

Rural 8%

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchMillennials and Empty Nesters Fueled Urban Growth

Urban population growth by age

Demographic Shifts to Watch

Young and Old Fueled Urban

Growth

It wasn’t just Millennials!

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchMillennials and Empty Nesters Fueled Urban Growth

Urban population growth by age

Demographic Shifts to Watch

But Urban Growth Rate of

21% Expected to Fall to 15%

Over Next Decade

Reasons:

Costs

Millennials Raising Families

Boomer Population Declines

Generation Z Likely to be

Urban Aspirational but Pricing

Likely to be Issue

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchSo Where Are the Rooftops Now?

Here is where the old development rules still apply, with caveats..

Southeast Leads the Way

Florida and Texas continue to

lead the nation in population

growth…

Ground-up development,

particularly of

neighborhood/community

centers, following patterns of

growth…

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchPopulation Continues to Grow…

Household formation and home ownership growth

12.5 Million More Households

Household Formation by Home Ownership Growth by

Year Born Year Born Between 2015 and 2025…

2000s 2000s

1990s 1990s

1980s

13.3 million losses from older

1970s 1980s generations offset by 25.8

1960s 1970s million gains in households

1950s

1940s

1960s (Millennials, Generation Z,

1930s 1950s etc.)

0 5 10 15 20 25 1940s

1930s

2025 Households (Millions) This should translate into 5.3

2015 Households (Millions) -5 0 5 10 million more homeowners by

2025…

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchWhere are the Rooftops Going to Be?

Projected household growth by region (millions) 2016 - 2025

Demographic Shifts to Watch

Most of the growth will be in

the South

5.3 million more homeowners

7.2 million more renters

Wildcard:

Impact of driverless cars…

Source: John Burns Real Estate Consulting, Cushman & Wakefield ResearchBut Can You Build It? In a High-Risk Environment, What Still Pencils? • What’s happening with costs? • The construction labor crisis… • The coming wave of defaults… Crisis = opportunity, or does it?

Costs Going Up, Up, Up!

Can it even pencil?

Turner Construction Turner Construction

Cost Index Cost Index

Index Index

% %

Q3 17 1044 5.6 Q3 17 1044 1.26

2016 989 4.7 Q2 17 1031 1.18

2015 943 4.5 Q1 17 1019 1.29

2014 902 4.4 Q4 16 1006 1.11

2013 864 4.1

2012 830 2.1

2011 812 1.6

2010 799 -4.0

2009 832 -8.4

2008 908 6.3

Source: Turner Construction Cost Index, Cushman & Wakefield ResearchConstruction Labor Market Status

Labor shortage a major problem…

Jobs Back, but Not Here

Construction Share of

Recovery Status

Nonfarm Employment

Male participation in workforce

Net Construction Net Construction

Job Losses Job Gains

(2005): 73.3%

10-Year Average 2017Q2 %

(GFC Peak to (GFC Trough to

Trough) 17Q2)

Male participation in workforce

Midwest 4.2% 4.0% -392.9 228.4 -11.4% (2017): 69.2%

Mitigating factors:

Northeast 3.9% 4.0% -209.1 194.3 -1.4%

Immigration policy

South 5.5% 5.2% -756.6 466.0 -10.8%

Opioid crisis

West 5.5% 5.3% -837.4 506.8 -16.2%

U.S. 4.9% 4.7% -2,265.0 1,429.0 -10.8%

Source: Bureau of Labor Statistics (updated Sept 2017), Cushman & Wakefield Research

Note: Jobs figures are in thousandsWorsened by Hurricanes…

The perfect labor storm…

Worsened by Hurricanes

Estimated Cost ($ Billions) adjusted for inflation

Harvey destroyed 30,000

Ivan (Sept 2004) homes in Houston—roughly

same as existing residential

pipeline…doubling demand.

Ike (Sept 2008)

10,000 to 20,000 workers

Andrew (Aug 1992

could be needed in Houston

alone…

Sandy (Oct 2012)

After Katrina, construction

Katrina (Aug 2005) worker wages increased 12%

in Mississippi… that was

Harvey (Sept 2017) before labor shortage…

0 20 40 60 80 100 120 140 160 180 200

This time around?

Estimated Cost ($ Billions) adjusted for inflation

Source: National Oceanic and Atmospheric Administration, Chicago Tribune, Cushman & Wakefield ResearchWorsened by Hurricanes…

The perfect labor storm…

Local Wages Already Up 40%+

Last Year Hourly Mean Wage;

Texas: $14.62/hr.

Florida: $14.00/hr.

Recent employment ads for

construction help in;

Houston: $21/hr. /($14.62)

Florida Keys: $20/hr./$14.00)

Source: Bureau of Labor Statistics, Cushman & Wakefield ResearchUSA New Construction by Product Type

Historical and Forecast

Development Outlook

Commercial Development in Major Markets

300

While retail development is

down, office construction

250 remains robust and industrial

is setting records…

200

150

100

50

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 (F) 2019 (F) 2020 (F) 2021 (F)

Office (MSF) Industrial (MSF) Retail (MSF)

Source: Turner Construction Cost Index, Cushman & Wakefield ResearchLand & Development Costs are Up, But…

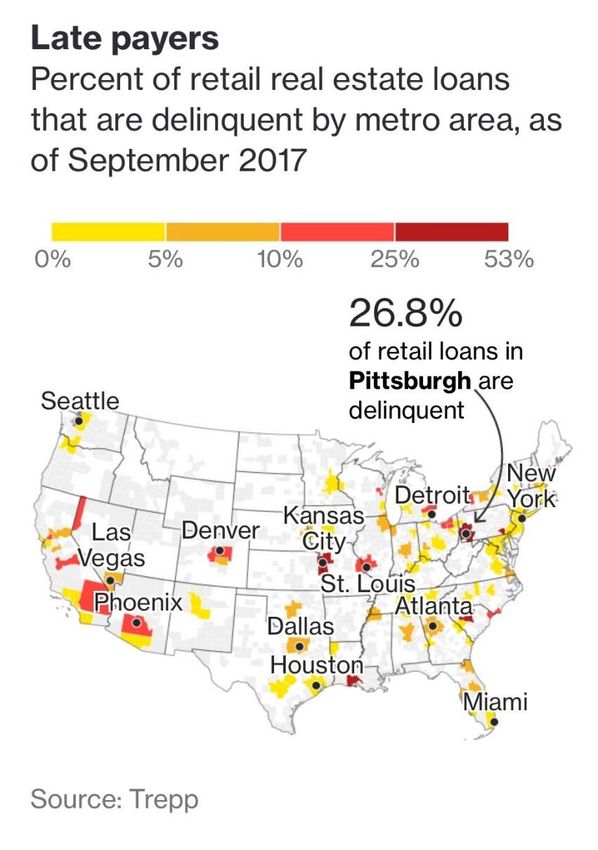

Dead/dying malls will be had for pennies on the dollar

Retail Delinquencies to Soar

According to Trepp

Retail Delinquency Rate as of

September 2017: 5.7%

We think that number will hit

10% over the next few years.

Source: Trepp, Cushman & Wakefield ResearchCan Dead Malls be Repositioned for eCommerce?

The exception, not the rule

FedEx/Mesquite Mall

Mesquite Mall was one of the

Dallas area’s first enclosed

malls, built in 1959.

The mall lost ground to

competitors through the 1980s

and 1990s and was closed in

2001.

It was demolished in 2006.

FedEx just built a 334,000

square foot distribution center

on the site.

Source: Cushman & Wakefield ResearchSo Where Does This Leave Us?

The story of retail development over the next decade will largely be a tale of mixed-use redevelopment

Challenges Opportunities Solutions

Dead/Dying Malls—Mostly Suburban Population Growth to Redevelop Dead Suburban Malls

Suburban Increase as Mixed-Use Lifestyle Centers

w/Substantial Housing, Office,

Medical and/or Hospitality

Department Store/Apparel Explosion of Food Retail, Shift Centers Towards

Consolidation Entertainment Retail, Experiential Entertainment Focus or Discount

Concepts, Off-Price Apparel & Focus

Discounter Demand

Rising Power Center Vacancies Mixed-Use Works Here Too Mixed-Use Works Here Too

Source: Cushman & Wakefield ResearchThe New Lifestyle Mixed-Use Food/Drink Heavy, Entertainment/Experientially Focused Open Air Centers The Wharf Avalon Legacy West The Bloc Washington, DC Alpharetta, GA Waco, TX Los Angeles (Downtown), CA Hoffman/Madison Marquette PGIM KDC/Columbia Ratkovich Brickell City Centre City Point FIGat7th Phipps Plaza Miami (Downtown), FL Brooklyn, NY Los Angeles (Downtown), CA Atlanta (Buckhead), GA Swire Properties Extell, et al Brookfield Simon

There is No Room for Mediocrity in Retail Anymore

Follow Viktor Gruen’s Original Vision

The Father of the American Mall

• You must give people a reason to come to your store or your “As art patrons, merchants

shopping center in the age of newCommerce. can be to our time what the

church and nobility were to the

Middle Ages.”

• If your shopping center is the center of your community, it will thrive.

• If it isn’t, then build a community around it. Viktor GruenGet on My Mailing List!

Garrick.Brown@Cushwake.com

©2017 Cushman & Wakefield.

The material in this presentation has been prepared solely for information purposes, and is

strictly confidential. Any disclosure, use, copying or circulation of this presentation (or the

information contained within it) is strictly prohibited, unless you have obtained Cushman &

Wakefield’s prior written consent. The views expressed in this presentation are the views of

the author and do not necessarily reflect the views of Cushman & Wakefield. Neither this

presentation nor any part of it shall form the basis of, or be relied upon in connection with any

offer, or act as an inducement to enter into any contract or commitment whatsoever. NO

REPRESENTATION OR WARRANTY IS GIVEN, EXPRESS OR IMPLIED, AS TO THE

ACCURACY OF THE INFORMATION CONTAINED WITHIN THIS PRESENTATION, AND

CUSHMAN & WAKEFIELD IS UNDER NO OBLIGATION TO SUBSEQUENTLY CORRECT

IT IN THE EVENT OF ERRORS.You can also read